High-Speed LPDDR5X DRAM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

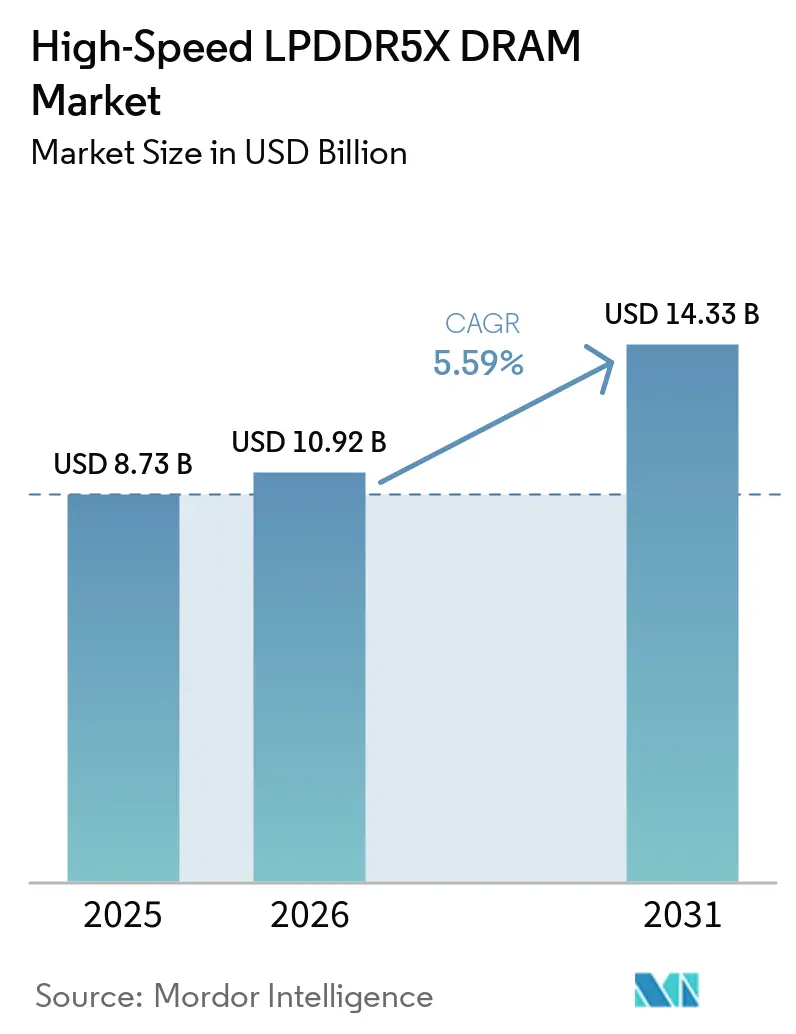

| Market Size (2026) | USD 10.92 Billion |

| Market Size (2031) | USD 14.33 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Speed LPDDR5X DRAM Market Analysis by Mordor Intelligence

The high-speed LPDDR5X DRAM market size is expected to increase from USD 8.73 billion in 2025 to USD 10.92 billion in 2026 and reach USD 14.33 billion by 2031, growing at a CAGR of 5.59% over 2026-2031. The high-speed LPDDR5X DRAM market is being driven by a clear rise in on-device generative AI workloads, pushing device makers toward faster memory and higher per-device content. The same market is also gaining from a broader shift in product roadmaps, as suppliers and OEMs move more programs toward LPDDR5X qualification across premium and upper mid-range devices. A second demand stream is emerging from AI servers and AI PCs, where LPDDR5X is now packaged in new module formats that extend its role beyond smartphones. This overlap between mobile and compute demand is tightening procurement discipline and is making supply planning more central to competitive performance. The arrival of CXMT as a fourth credible producer also changes the structure of the high-speed LPDDR5X DRAM market, adding new capacity in selected channels while making sourcing decisions more sensitive to region, customer profile, and platform requirements.

Key Report Takeaways

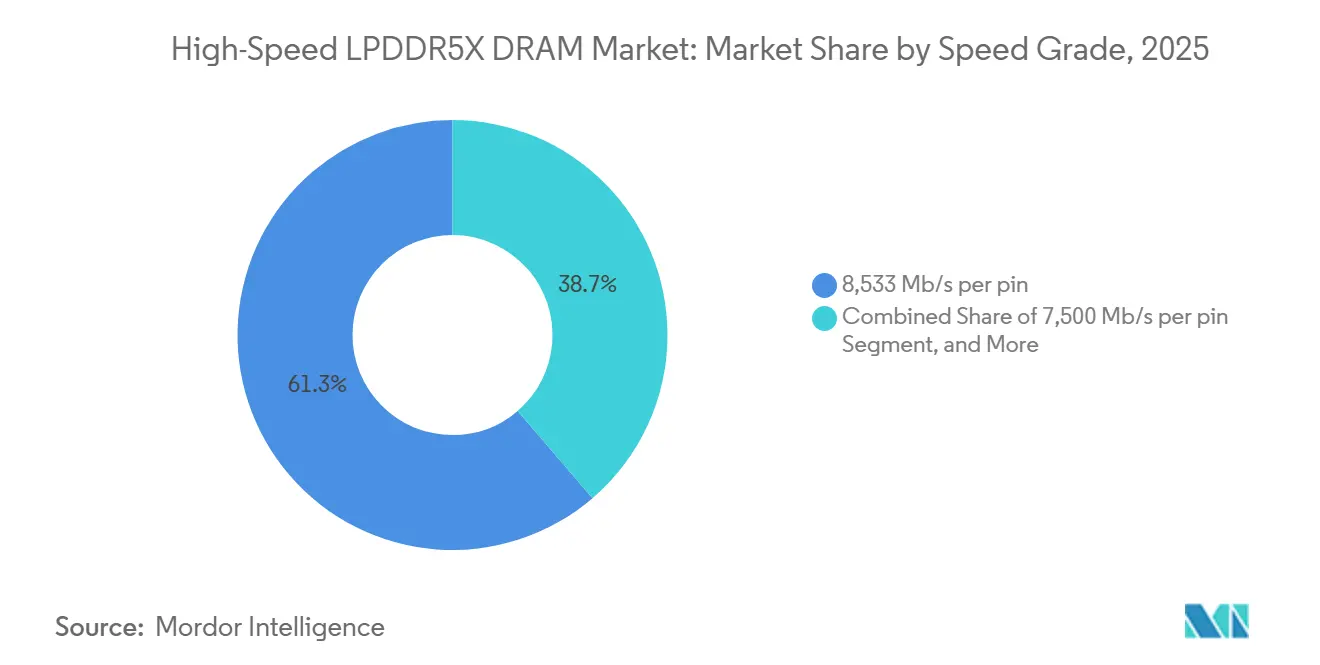

- By speed grade, the 8,533 Mb/s per pin tier accounted for 61.29% of revenue in 2025, while the 10,667/10,700 Mb/s per pin tier is projected to grow at a 6.39% CAGR through 2031.

- By die density, the 16 GB segment accounted for 42.31% of revenue in 2025, while configurations above 32 GB are projected to grow at a 6.76% CAGR through 2031.

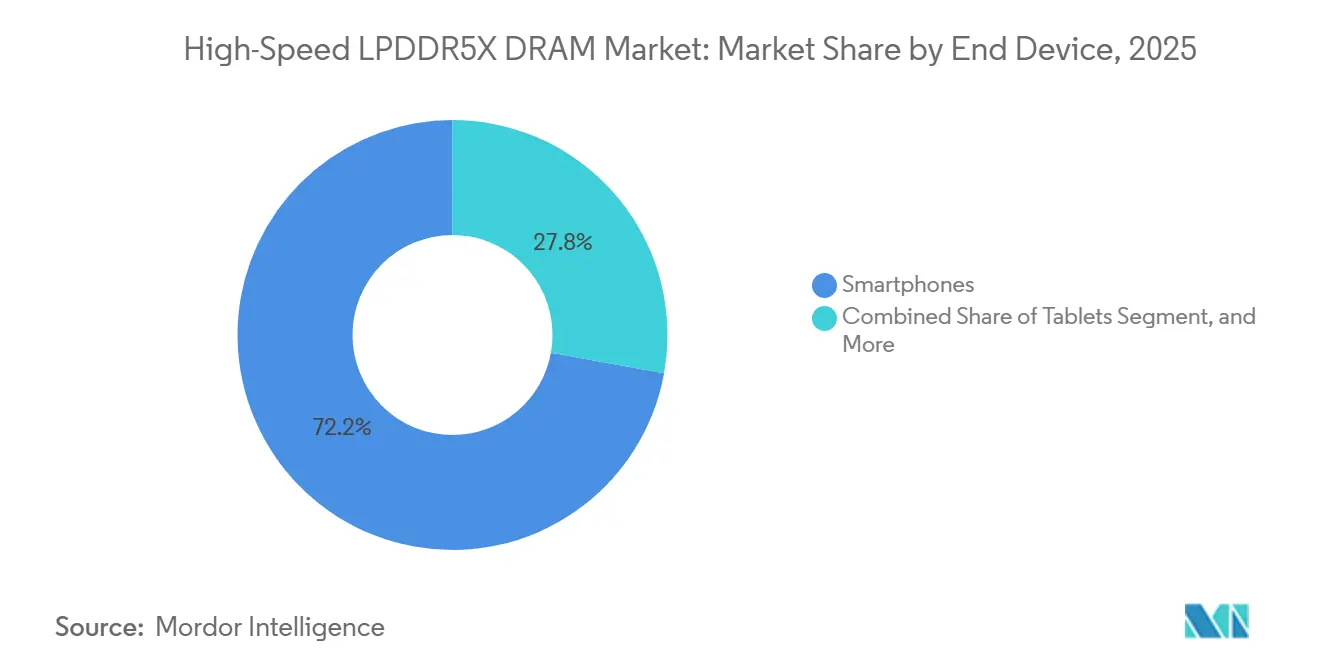

- By end device, smartphones accounted for 72.16% of high-speed LPDDR5X DRAM market revenue in 2025, while thin-and-light notebooks and AI PCs are projected to record the fastest growth at a 6.53% CAGR through 2031.

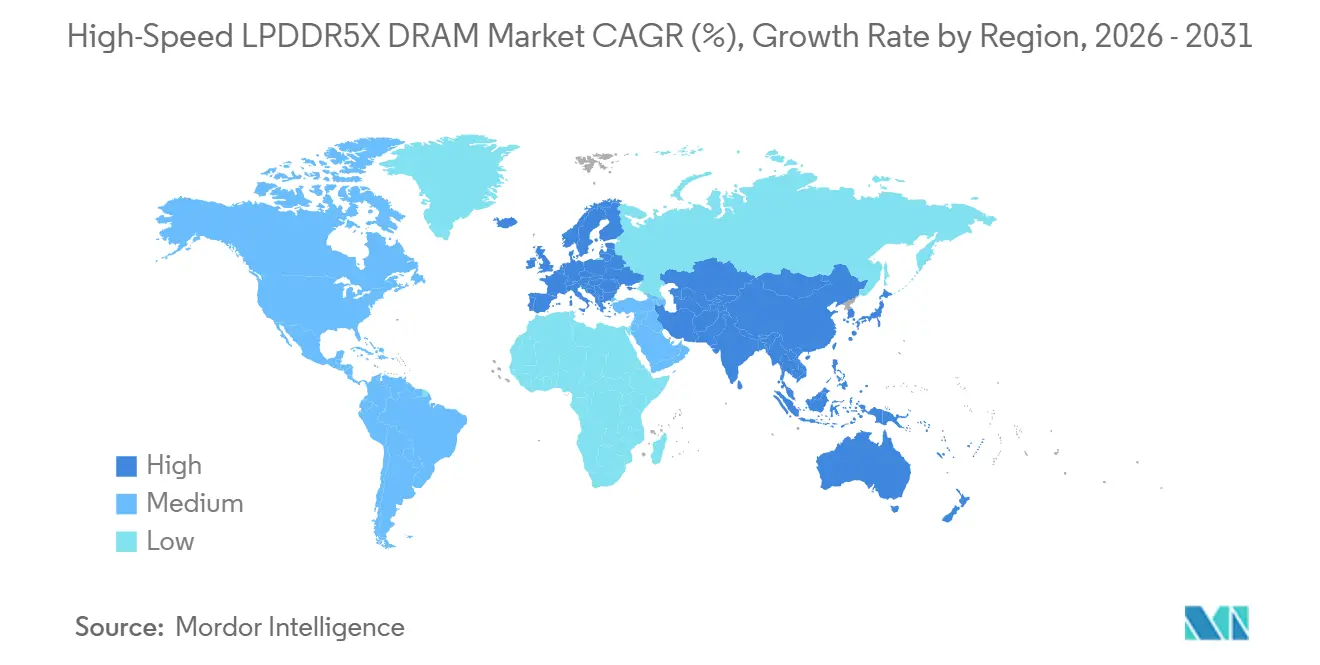

- By geography, Asia-Pacific held 81.21% of revenue in 2025, while Europe is projected to expand at a 6.37% CAGR through 2031 in the high-speed LPDDR5X dynamic random access memory (DRAM) market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Speed LPDDR5X DRAM Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GenAI Flagship Smartphone Memory Content Expansion | +2.0% | Global, with highest intensity in Asia-Pacific and North America | Short term (≤ 2 years) |

| 8533-Ready Premium SoC Standardization | +1.3% | Global, led by Asia-Pacific SoC design ecosystem | Short term (≤ 2 years) |

| LPDDR4X Production Drawdown Accelerating Migration | +0.8% | Global, near-term impact concentrated in China and emerging Asia | Medium term (2-4 years) |

| AI PC and Chromebook Low-Power Memory Uptake | +0.5% | North America and Europe leading, Asia-Pacific scaling | Medium term (2-4 years) |

| Automotive Centralized Compute and Safety-Grade LPDDR Adoption | +0.4% | Europe and North America (ISO 26262 compliance), early Asia-Pacific | Long term (≥ 4 years) |

| Thin-Package Thermal Gains Enabling Higher Capacities | +0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GenAI Flagship Smartphone Memory Content Expansion

On-device AI is changing smartphone memory decisions faster than earlier handset upgrade cycles had assumed. Micron said in June 2025 that its 1γ-based LPDDR5X at 10.7 Gbps improved Llama 2 query response time by 30%, translation results by more than 50%, and recommendation engine performance by 25%, which tied bandwidth directly to visible AI performance gains in mobile devices. Micron also said those samples were being supplied in 16 GB packages, with an 8 GB to 32 GB capacity range planned for 2026 flagship smartphones, which aligns with the move toward richer memory configurations in AI-ready phones. Samsung's ultra-thin LPDDR5X package addresses heat resistance and thickness constraints, enabling practical use of higher memory density in slimmer phone designs. This keeps the high-speed LPDDR5X dynamic random-access memory (DRAM) market closely tied to flagship AI phone launches, as device makers now need both higher capacity and faster data rates to support on-device inference.

8533-Ready Premium SoC Standardization

The 8,533 Mb/s per pin class has become the most stable performance point for premium LPDDR5X deployments. JEDEC's LPDDR5X documentation established a common framework for controller validation and operating parameters, helping the broader ecosystem align around this grade. CXMT later confirmed mass production of LPDDR5X products and publicly showed continued progress across 8,533 Mbps, 9,600 Mbps, and 10,667 Mbps variants, which indicates that mainstream supply depth at the core premium grade is improving. This matters in the high-speed LPDDR5X DRAM market because a widely accepted speed grade lowers qualification friction and lets more device programs move to volume production on a common footing. It also creates a clearer boundary between the grade that drives scale and the faster bins that remain tied to premium differentiation and newer node transitions.

LPDDR4X Production Drawdown Accelerating Migration

The transition away from LPDDR4X is pushing more device roadmaps toward earlier LPDDR5X qualification. As newer LPDDR5X products become available across more speed grades and packaging options, the cost and design case for sticking with older memory weakens in premium and upper mid-range platforms. The migration is not moving at the same pace across the whole device stack, because entry-level platforms still depend on processor compatibility and tighter bill-of-materials constraints. Even so, the high-speed LPDDR5X DRAM market is benefiting from a wider platform shift that now reaches beyond the flagship tier. This is making LPDDR5X qualification a more immediate product-planning task rather than a later performance upgrade.

AI PC and Chromebook Low-Power Memory Uptake

AI PCs are reshaping notebook memory requirements because local AI workloads need more capacity without giving up power efficiency in thin systems. Micron and Lenovo said in their AI PC white paper that LPCAMM2, based on LPDDR5X, can reach up to 9,600 MT/s and deliver up to 85% lower active power consumption than DDR5 SODIMMs in the cited comparison. Micron also launched the Crucial LPCAMM2 at 8,533 MT/s with capacities up to 64 GB, supporting modular LPDDR5X adoption in AI-ready notebook platforms. MediaTek took the same approach with Chromebooks, introducing Kompanio Ultra, and Lenovo and Acer followed with Chromebook Plus systems that pair the processor with up to 16 GB of LPDDR5X.[1]Acer, “Acer Chromebook Plus Spin 514 - First Acer Chromebook With MediaTek Kompanio Ultra Processor,” Acer Newsroom, news.acer.com This gives the high-speed LPDDR5X DRAM market a second strong growth path, as notebook and Chromebook programs are now adding volume through both module-based and soldered implementations.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supplier Concentration and Allocation Risk | -0.5% | Global | Short term (≤ 2 years) |

| Memory BOM Inflation for Price-Sensitive Devices | -0.4% | Global, most acute in emerging-market and entry-tier smartphone segments | Short term (≤ 2 years) |

| Mid-Tier Processor Compatibility Gaps | -0.3% | Emerging Asia, South America, and Middle East and Africa | Medium term (2-4 years) |

| High-Speed Signal and Thermal Validation Burden | -0.2% | Global, with higher burden in automotive and edge deployments | Long ter |

| Source: Mordor Intelligence | |||

Supplier Concentration and Allocation Risk

Supply in the high-speed LPDDR5X DRAM market remains concentrated around a very small group of advanced manufacturers. Samsung, SK hynix, and Micron continue to lead the most advanced LPDDR5X products, while CXMT is still building its position as a fourth credible source.[2]Samsung Electronics Co., Ltd., “Samsung Electronics Begins Mass Production of Industry's Thinnest LPDDR5X DRAM Packages for On-Device AI,” Samsung Global Newsroom, news.samsung.com SK hynix's server-focused SOCAMM2 launch shows that LPDDR5X dies are now being directed into additional high-value formats beyond smartphones, which can tighten allocation discipline across the market. CXMT's IPO prospectus showed a planned investment path for technology upgrades, but it also confirmed that the competitive catch-up process is still underway rather than complete. That leaves the high-speed LPDDR5X DRAM market exposed to allocation pressure whenever flagship phone demand, AI PC demand, and AI server packaging demand rise at the same time.

Memory BOM Inflation for Price-Sensitive Devices

Higher LPDDR5X content creates a clear cost issue for price-sensitive devices, even when the technical case for the memory standard is strong. Micron and Lenovo highlighted the power and performance advantages of LPDDR5X for AI PCs, but those same benefits come with higher system memory expectations that are easier to absorb in premium products than in value-focused products. MediaTek, Lenovo, and Acer all placed LPDDR5X into more capable Chromebook designs, which supports the view that the memory standard is moving up the compute stack rather than down into the lowest cost tiers first. In the high-speed LPDDR5X dynamic random access memory (DRAM) market, premium phones and notebooks can more easily support that cost structure than entry devices. This keeps adoption strongest in higher-value platforms and limits how quickly the addressable volume base can expand in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Speed Grade: 8,533 Mb/s Holds The Core While Faster Bins Build Momentum

The 8,533 Mb/s per pin tier held 61.29% of the high-speed LPDDR5X DRAM market share in 2025, making it the primary volume grade for premium device programs. That position reflects a long validation window across leading system-on-chip roadmaps, because the LPDDR5X extension gave memory controller teams time to optimize around this speed class. In the high-speed LPDDR5X DRAM market, that maturity matters because it lowers the risk of moving large flagship and upper-tier volumes onto a single widely accepted grade. The earlier 7,500 Mb/s tier has been giving way as OEMs and suppliers standardize on higher speeds, consistent with the broader shift toward more capable AI-ready devices. CXMT's move into mass production at 8,533 Mbps also broadens supply options at the grade that carries the largest commercial weight.

The 10,667/10,700 Mb/s per pin segment is projected to grow at a 6.39% CAGR through 2031, making it the fastest-rising speed class in the high-speed LPDDR5X DRAM market. Micron said in June 2025 that its 1γ-based LPDDR5X operates at 10.7 Gbps and delivers a 43% speed increase over the 7.5 Gbps 1β generation, while also targeting 2026 flagship smartphones. Samsung also developed a 10.7 Gbps LPDDR5X product optimized for AI applications, demonstrating that leading suppliers are pushing the upper end of the speed range in parallel. The 9,600 Mb/s tier keeps a strong middle role, because it supports notebook modules and automotive memory programs that need a balance of speed, validation, and system-level stability. This creates a layered structure inside the high-speed LPDDR5X DRAM market, where 8,533 Mb/s drives scale, 9,600 Mb/s supports broader platform flexibility, and 10,667/10,700 Mb/s captures the next premium upgrade cycle.

By Die Density: 16 GB Leads Current Volume While Higher Capacities Gain Speed

The 16 GB segment accounted for 42.31% of the high-speed LPDDR5X DRAM market in 2025, keeping it at the center of flagship smartphone memory design. That lead reflects how 16 GB still fits the current balance between AI performance, thermal limits, package thickness, and system selling price. Samsung's work on 12 GB and 16 GB ultra-thin LPDDR5X packages supports this mainstream flagship role by improving heat resistance and reducing package height for dense mobile layouts. In the high-speed LPDDR5X DRAM market, 16 GB remains the volume center because it is already established across major premium device lines. That makes it the most dependable configuration for near-term revenue, even as higher capacities gain more attention.

Above 32 GB configurations are projected to expand at a 6.76% CAGR through 2031, which makes them the fastest-growing density tier in the high-speed LPDDR5X DRAM market. SK hynix began mass production of a 192 GB SOCAMM2 module in April 2026 for NVIDIA's Vera-Rubin platform, and the company said the module delivers more than double the bandwidth and over 75% better power efficiency than conventional RDIMM. Samsung has also pointed to the development of 24 GB and 32 GB packages in ultra-slim form, indicating that higher-capacity phone configurations are increasingly a packaging and thermal challenge rather than only a node challenge. CXMT said its LPDDR5X lineup supports greater product progression across advanced variants, broadening the supply discussion for higher-density tiers. This means the high-speed LPDDR5X DRAM market is likely to keep 16 GB as the revenue anchor while 24 GB, 32 GB, and server-linked modules capture the strongest growth.

By End Device: Smartphones Lead Revenue While AI PCs Shift The Mix

Smartphones accounted for 72.16% of the high-speed LPDDR5X DRAM market in 2025, confirming that handsets remain the largest demand pool for this memory category. The segment held that position because LPDDR5X is now closely tied to flagship phone requirements around AI processing, multimedia workloads, and power-efficient high-bandwidth operation. Samsung, Micron, and CXMT have all advanced LPDDR5X products that meet this smartphone-centered demand pattern, whether through thinner packages, higher-speed grades, or broader product availability. Tablets followed smartphones in market weight, largely through premium tablet lines that share the same need for low-power, high-speed memory. Even with that dominance, the high-speed LPDDR5X DRAM industry is no longer shaped solely by phones, as other device classes are now adding meaningful volume and new package requirements.

Thin-and-light notebooks and AI PCs are projected to grow at a 6.53% CAGR through 2031, making them the fastest-growing end-device category in the high-speed LPDDR5X DRAM market. Micron's LPCAMM2 launch and the Micron-Lenovo white paper both show how LPDDR5X is moving into modular notebook systems without sacrificing the power advantages that made it valuable on mobile platforms. Chromebooks are part of the same expansion, because MediaTek's Kompanio Ultra and the Lenovo Chromebook Plus 14 and Acer Chromebook Plus Spin 514 all pair AI-capable processing with LPDDR5X memory. Automotive IVI, ADAS, and central compute are also building a steadier role, with Samsung, SK hynix, and Micron all linking LPDDR5X to safety-focused vehicle applications. This broader demand mix gives the high-speed LPDDR5X DRAM market more resilience, because growth is now spread across phones, notebooks, Chromebooks, and automotive compute systems.

Geography Analysis

Asia-Pacific accounted for 81.21% of the high-speed LPDDR5X DRAM market in 2025, reflecting the region's deep concentration of memory manufacturing, device assembly, and end-product demand. South Korea remains the leading production center, with Samsung and SK hynix driving much of the advanced LPDDR5X roadmap across mobile, computing, and automotive use cases. China reinforces the region on both the demand and supply sides, as it is a major smartphone manufacturing base and the home market for CXMT's LPDDR5X expansion. CXMT's IPO prospectus said the company had established a growing domestic smartphone LPDDR customer base, including Xiaomi, OPPO, vivo, and Transsion, underscoring the growing relevance of local sourcing in China. Taiwan and Japan add support through packaging, electronics manufacturing, and high-reliability applications, while India and Southeast Asia continue to absorb rising smartphone assembly volumes and a gradual move toward LPDDR5X-enabled models.

Europe is projected to grow at a 6.37% CAGR through 2031, making it the fastest-growing region in the high-speed LPDDR5X DRAM market. The strongest support comes from software-defined vehicle programs and centralized vehicle compute, where low-power memory must meet strict reliability and safety requirements. NXP's S32N7 platform demonstrates how automotive compute architectures are moving toward domain- and central-processing models that align with higher LPDDR5X content requirements. Europe also benefits from AI PC adoption in enterprise and education purchases, which supports demand for LPDDR5X notebook designs and related module formats.

North America remains a strategically important part of the high-speed LPDDR5X dynamic random access memory (DRAM) market because it combines AI PC platform activity, hyperscale compute demand, and Micron's position as the region's large-scale DRAM producer. Micron's current LPDDR5X component and LPCAMM2 module portfolio gives system makers in the region access to both mobile and notebook-oriented form factors.[3]Micron Technology, Inc., “LPCAMM2,” Micron Technology Products, micron.com SK hynix's SOCAMM2 program for NVIDIA's Vera-Rubin platform further underlines North America's role as an emerging demand center for LPDDR5X in AI server deployments. The Rest of the World, including South America, the Middle East, Africa, and Oceania, remains a smaller revenue pool, where LPDDR5X adoption is likely to remain gradual because local demand still leans toward imported devices and cost-sensitive product tiers.

Competitive Landscape

The high-speed LPDDR5X DRAM market is highly concentrated at the fabrication level, and competitive advantage still depends on node leadership, package design, and validation depth. Samsung has pursued a multi-track strategy through ultra-thin LPDDR5X packaging for mobile devices, 10.7 Gbps-class performance development, and automotive-grade LPDDR5X for safety-critical vehicle systems.[4]Samsung Electronics Co., Ltd., “Samsung Electronics Begins Mass Production of Industry's Thinnest LPDDR5X DRAM Packages for On-Device AI,” Samsung Global Newsroom, news.samsung.com SK hynix has taken a packaging-led step by moving LPDDR5X dies into 192 GB SOCAMM2 modules for NVIDIA's Vera-Rubin platform, which extends the memory into a server-oriented format with a different demand profile. Micron has focused on 1γ-based LPDDR5X and LPCAMM2, emphasizing high speed, low package height, and power efficiency as key differentiators in flagship smartphones and AI PCs. These moves show that the high-speed LPDDR5X DRAM market is being shaped as much by package strategy and end-platform fit as by pure bit supply.

CXMT is the most important emerging competitor in the high-speed LPDDR5X DRAM market because it has moved from participation claims to visible production and customer sampling milestones. The company announced LPDDR5X mass production in October 2025 and later demonstrated product speeds up to 10,667 Mbps, giving the market a clearer view of its speed-grade ambitions. CXMT's IPO prospectus also said the company had reached the fourth-largest position in global DRAM revenue rankings by the fourth quarter of 2025 and planned to direct USD 4.13 billion of IPO proceeds toward upgrades, including USD 1.82 billion for DRAM process advancement. That does not remove the lead held by Samsung, SK hynix, and Micron, but it does create a more meaningful supply alternative for Chinese OEMs and for customers that value regional diversification. As a result, the high-speed LPDDR5X DRAM market remains concentrated, but is no longer limited to a fixed three-supplier structure.

Automotive and AI PC module supply remains the clearest area where supplier positioning can still shift. Samsung, SK hynix, and Micron all have automotive-grade LPDDR5X credentials tied to ISO 26262 and ASIL-D level requirements, which gives them a stronger foothold in safety-critical vehicle memory programs. Micron's LPCAMM2 launch also gave it an early commercial position in modular LPDDR5X for AI-ready laptops. SK hynix's SOCAMM2 program and Samsung's thin-package work show that both companies are also targeting new form factors and thermal requirements beyond the classic smartphone socket. This means competition in the high-speed LPDDR5X DRAM market is broadening across use cases, but the top tier still depends on advanced process control, product validation history, and the ability to package LPDDR5X for several end markets.

High-Speed LPDDR5X DRAM Industry Leaders

Samsung Electronics Co., Ltd.

SK hynix Inc.

Micron Technology, Inc.

ChangXin Memory Technologies, Inc.

Nanya Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SK hynix began mass production of its 192 GB SOCAMM2 module, based on 1cnm process (sixth-generation 10 nm-class) LPDDR5X, designed for the NVIDIA Vera-Rubin AI server platform. The module delivers more than double the bandwidth and over 75% improved power efficiency compared to conventional RDIMMs, directly targeting the large language model training and inference bottlenecks in cloud service provider data centers.

- November 2025: CXMT showcased its DDR5 and LPDDR5X product roadmap at IC China 2025, publicly demonstrating LPDDR5X chips at speeds up to 10,667 Mbps with capacities up to 16 Gb per die, the first comprehensive public disclosure of its competitive position across both standards. The company confirmed that its 8,533 Mbps and 9,600 Mbps LPDDR5X products were in mass production and its 10,667 Mbps variant was in active customer sampling.

- October 2025: ChangXin Memory Technologies (CXMT) announced it had begun mass production of LPDDR5X DRAM, including 8,533 Mbps and 9,600 Mbps speed grades, and was in customer sampling for the 10,667 Mbps variant, representing China's first mass-produced high-performance mobile DRAM meeting international flagship-device specifications. The announcement was made via CXMT's official website on October 28, 2025, and coincided with a major capacity expansion across its Hefei fabrication facilities.

- September 2025: Acer announced the Chromebook Plus Spin 514 at IFA Berlin, the first Chromebook powered by the MediaTek Kompanio Ultra processor with an integrated 50-TOPS NPU, featuring up to 16 GB of LPDDR5X. The product's launch marked the extension of LPDDR5X into the Chromebook market segment, previously dominated by lower-performance LPDDR4X configurations.

Global High-Speed LPDDR5X DRAM Market Report Scope

The High-Speed LPDDR5X DRAM Market refers to the global market for advanced Low-Power Double Data Rate 5X (LPDDR5X) dynamic random-access memory solutions designed to deliver ultra-high memory bandwidth, low latency, and enhanced power efficiency for next-generation computing and intelligent electronic devices. LPDDR5X DRAM represents the latest evolution of low-power memory technology, enabling faster data processing and improved system responsiveness for artificial intelligence (AI), machine learning, high-resolution multimedia, advanced connectivity, edge computing, and autonomous applications.

The High-Speed LPDDR5X DRAM Report is Segmented by Speed Grade (7,500 Mb/s per pin, 8,533 Mb/s per pin, 9,600 Mb/s per pin, and 10,667 / 10,700 Mb/s per pin), Die Density (8 GB, 12 GB, 16 GB, 24 GB, 32 GB, and 64 GB and Above), End Device (Smartphones, Tablets, Thin-and-Light Notebooks / AI PCs, Chromebooks, Automotive IVI, ADAS, and Central Compute, and Embedded/Edge AI Devices and AR/VR), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| 7,500 Mb/s per pin |

| 8,533 Mb/s per pin |

| 9,600 Mb/s per pin |

| 10,667 / 10,700 Mb/s per pin |

| 8 GB |

| 12 GB |

| 16 GB |

| 24 GB |

| 32 GB |

| 64 GB and Above |

| Smartphones |

| Tablets |

| Thin-and-Light Notebooks / AI PCs |

| Chromebooks |

| Automotive IVI, ADAS and Central Compute |

| Embedded / Edge AI Devices and AR/VR |

| North America | |

| Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Speed Grade | 7,500 Mb/s per pin | |

| 8,533 Mb/s per pin | ||

| 9,600 Mb/s per pin | ||

| 10,667 / 10,700 Mb/s per pin | ||

| By Die Density | 8 GB | |

| 12 GB | ||

| 16 GB | ||

| 24 GB | ||

| 32 GB | ||

| 64 GB and Above | ||

| By End Device | Smartphones | |

| Tablets | ||

| Thin-and-Light Notebooks / AI PCs | ||

| Chromebooks | ||

| Automotive IVI, ADAS and Central Compute | ||

| Embedded / Edge AI Devices and AR/VR | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the high-speed LPDDR5X DRAM market size in 2026 and where is it headed by 2031?

The high-speed LPDDR5X DRAM market is expected to reach USD 10.92 billion in 2026 and is forecast to reach USD 14.33 billion by 2031 at a 5.59% CAGR.

Which end device contributes the most revenue to LPDDR5X DRAM demand?

Smartphones led with 72.16% of revenue in 2025, which kept handsets as the largest demand center for LPDDR5X memory.

Which speed grade is the most widely used in current LPDDR5X deployments?

The 8,533 Mb/s per pin tier held 61.29% of revenue in 2025, reflecting its broad validation across premium device platforms.

Why are AI PCs becoming important for LPDDR5X adoption?

Thin-and-light notebooks and AI PCs are projected to grow at a 6.53% CAGR through 2031 as LPCAMM2 and AI-ready system designs expand the role of LPDDR5X in PCs.

Which region is expanding the fastest for LPDDR5X demand?

Europe is projected to grow at a 6.37% CAGR through 2031, supported by software-defined vehicle programs and AI PC adoption.

What is driving growth in higher LPDDR5X die densities?

Above 32 GB configurations are projected to grow at a 6.76% CAGR as AI server modules and higher-memory premium devices require denser LPDDR5X packaging.

Page last updated on: