Continuous Performance Management Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

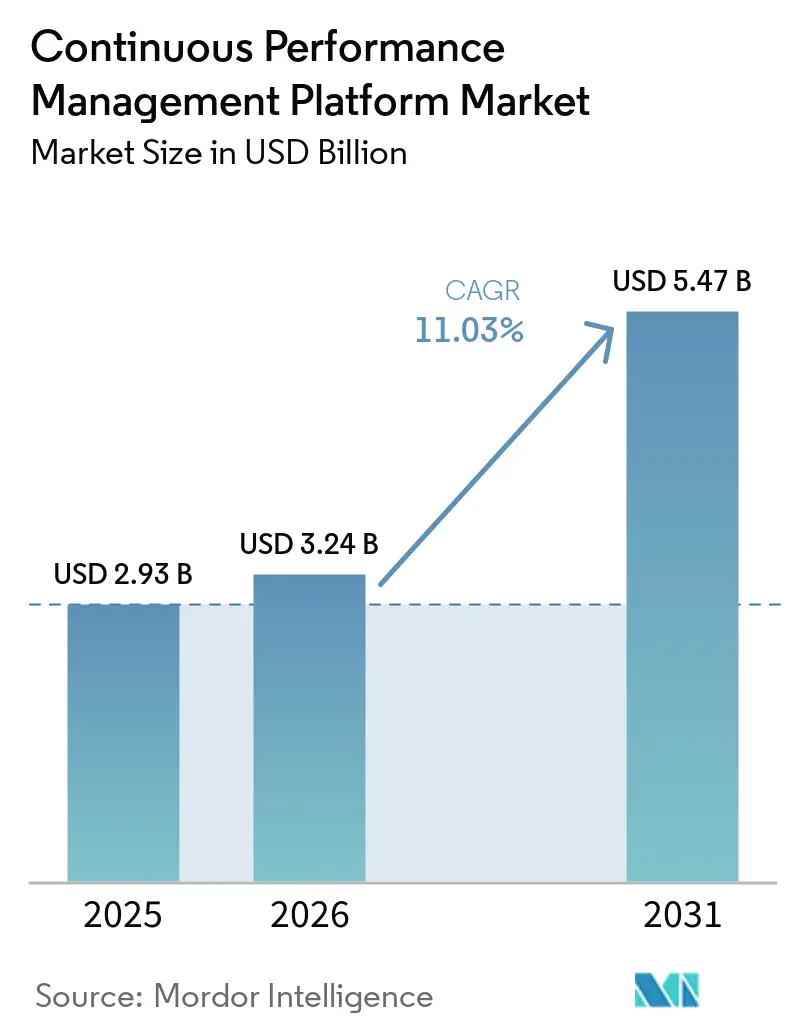

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 5.47 Billion |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

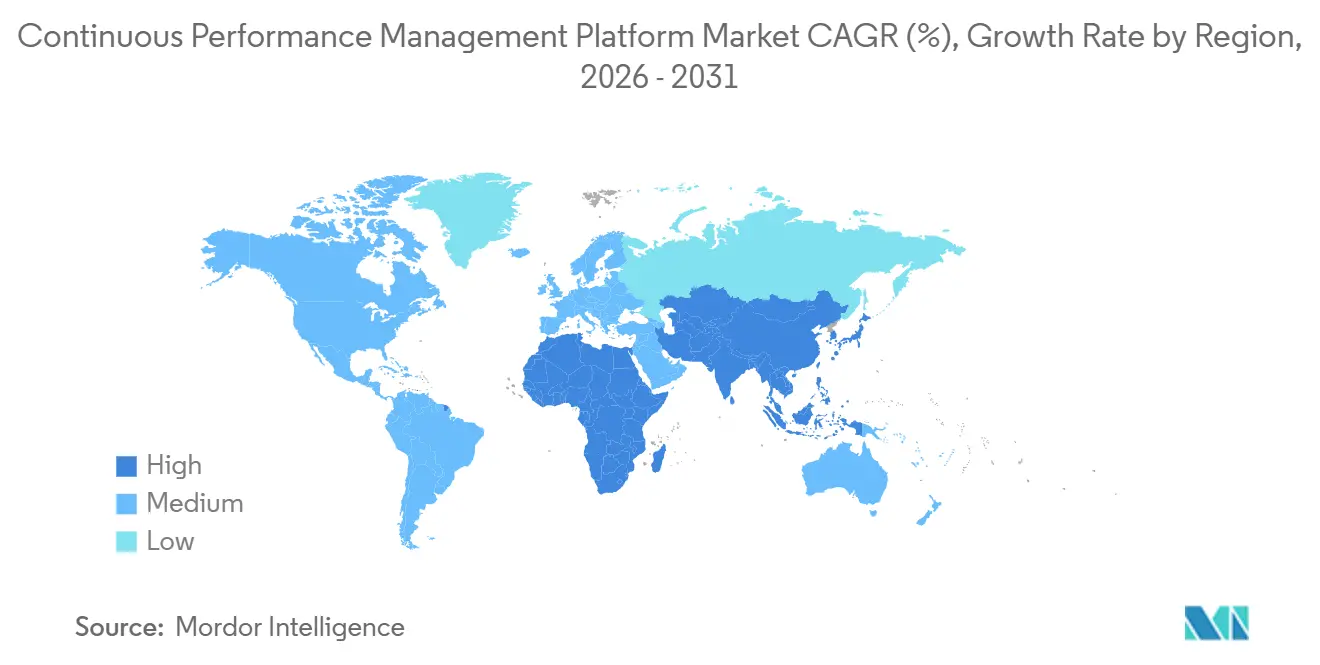

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Continuous Performance Management Platform Market Analysis by Mordor Intelligence

The continuous performance management platform market size is expected to be USD 2.93 billion in 2025, USD 3.24 billion in 2026, and reach USD 5.47 billion by 2031, growing at a CAGR of 11.03% from 2026 to 2031. Surging demand for real-time feedback loops that link goals to execution, the steady infusion of generative AI into talent workflows, and shrinking tolerance for annual reviews are reshaping adoption patterns across regions. Platform vendors now position nightly HRIS synchronizations and agent-driven analytics as table stakes, while buyers elevate scalability, data-privacy controls, and explainability to the top of their evaluation checklists. Consolidation is accelerating as private equity and large platform providers acquire AI-native specialists to enrich skills graphs and analytics engines. At the same time, resistance to cultural change, manager fatigue, and emerging compliance rules restrain the speed of transformation, forcing providers to bundle change-management playbooks with every deployment.

Key Report Takeaways

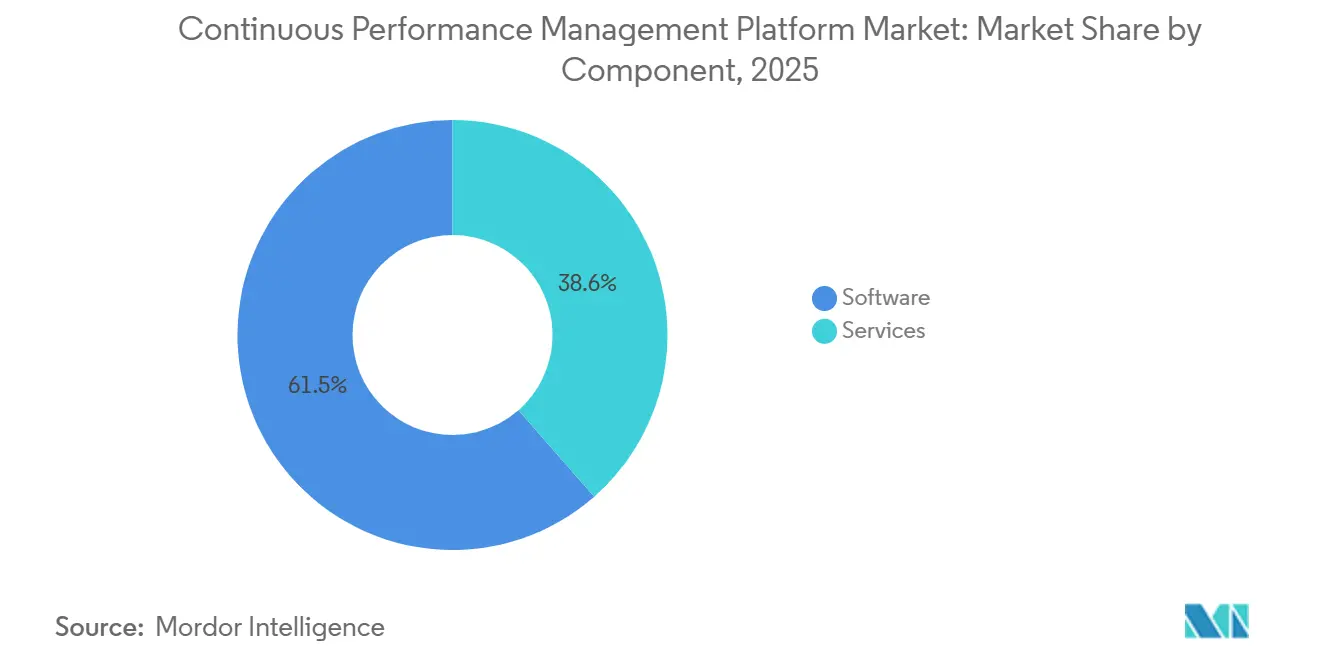

- By component, software led with 61.45% of the continuous performance management platform market share in 2025, while services are forecast to expand at a 12.21% CAGR through 2031.

- By deployment mode, on-premises solutions held 68.19% revenue share in 2025, but cloud-based offerings are projected to grow at a 13.01% CAGR to 2031.

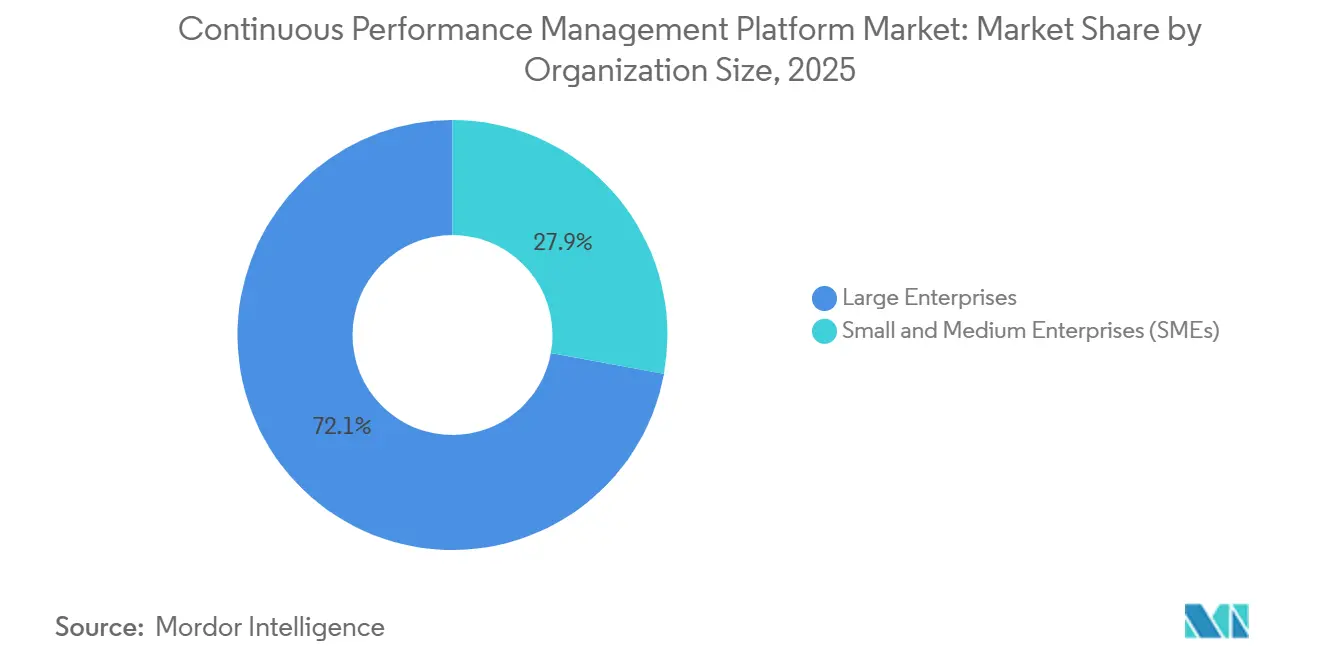

- By organization size, large enterprises accounted for 72.12% of 2025 revenue, whereas small and medium enterprises are set to register a 12.67% CAGR during 2026-2031.

- By end-user industry, IT and telecom captured 26.11% of 2025 sales, yet healthcare and life sciences is advancing at an 11.54% CAGR to 2031.

- By geography, North America captured 36.86% share in 2025, and Asia-Pacific is the fastest-growing region with a 11.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Continuous Performance Management Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread shift from annual reviews to continuous feedback frameworks | +2.4% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising adoption of cloud‑based HR solutions for scalability and cost efficiency | +2.1% | Global, strongest in North America and Asia‑Pacific | Short term (≤ 2 years) |

| Expansion of remote and hybrid work models requiring real‑time performance visibility | +1.8% | Global, notably North America, Europe, urban Asia‑Pacific | Short term (≤ 2 years) |

| Integration of AI and analytics for data‑driven talent decisions | +2.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing demand for OKR alignment within agile project teams | +1.2% | Global, concentrated in IT, telecom, BFSI, professional services | Medium term (2-4 years) |

| Emergence of employee sentiment analysis using passive listening data streams | +0.9% | North America and Europe, emerging in Asia‑Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread Shift From Annual Reviews to Continuous Feedback Frameworks

Organizations are abandoning once-a-year appraisals because episodic reviews fail to capture the speed of role evolution and strategic pivots. Betterworks research reported that only 16% of firms view talent decisions as predictive, while 73% acknowledge intelligence gaps that derail initiatives. Embedding feedback into Slack and Teams removes context-switching, captures performance signals in flow-of-work, and delivers faster course corrections. SAP’s 1H 2026 Goal Creation and Goal Progress Agents proactively flag outdated objectives, cutting end-of-cycle surprises.[1]SAP, “1H 2026 Release Highlights Of SAP SuccessFactors Performance And Goals Management,” sap.com The shift is acute in retail, where senior-leader turnover averages 22%, forcing real-time alignment among constantly changing teams. Procurement cycles are compressing, and vendors offering nightly HRIS synchronizations alongside real-time calibration analytics are winning deals.

Rising Adoption of Cloud-Based HR Solutions for Scalability and Cost Efficiency

Cloud deployment eliminates capital expense and multi-month upgrades that hamper on-premises systems. A 2026 peer-reviewed study found that cloud HRM platforms integrating distributed computing raised data accuracy, appraisal reliability, and operational responsiveness in SMEs. ICON Corporate Finance estimated that 60% of enterprises intend to increase investment in AI-driven HCM platforms, rewarding vendors able to iterate features weekly. Lattice’s roadmap delivers AI-powered review drafts and seamless Workday and Rippling integrations that keep talent data aligned. Consumption-based models such as Workday Flex Credits further reduce procurement friction and let firms scale AI usage without contract renegotiations.

Expansion of Remote and Hybrid Work Models Requiring Real-Time Performance Visibility

With 58% of organizations now supporting permanent hybrid work, line-of-sight management has faded, driving reliance on digital performance signals. AI gives workers back 75 minutes per day on average, yet only 10% of HR leaders feel confident that workforce skills align with near-term goals. Platforms that surface engagement data, goal progress, and automated coaching nudges help close perception gaps between managers and employees. Deloitte’s 2026 Human Capital Trends study highlighted that human-centric AI approaches yield superior returns, making explainability and transparency essential. Native Slack, Teams, and Outlook nudges that capture feedback in context mitigate the micro-feedback fatigue that fuels manager burnout.

Integration of AI And Analytics for Data-Driven Talent Decisions

Generative AI is moving from chatbot novelty to core workflow automation. The 2026 SHRM survey found 39% of firms already running AI in HR, with performance management the most common use case in midsize organizations. Oracle’s 25D release offers AI-suggested goals, generative document evaluations, and a Talent Advisor agent that synthesizes promotion readiness and team insights. Competitive edge lies in marrying proprietary skills graphs with large language models, enabling context-rich recommendations that remain transparent. Buyers now require SOC 2 Type II certification, GDPR readiness, and audit logs before green-lighting AI deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and compliance concerns under GDPR and CCPA | -1.6% | Europe, North America, expanding globally | Short term (≤ 2 years) |

| Organizational resistance to cultural change in performance evaluation | -1.3% | Global, especially hierarchical and regulated sectors | Medium term (2-4 years) |

| Algorithmic bias risks in AI‑powered evaluation models | -0.8% | Global, with heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Overload of micro‑feedback leading to manager burnout | -0.7% | Global, concentrated in high‑adoption early‑mover firms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Compliance Concerns Under GDPR And CCPA

Performance platforms capture sensitive ratings, coaching notes, and sentiment scores, exposing employers to strict data-protection rules. The UK ICO logged nearly 43,000 complaints in 2024-2025, and from 19 June 2026 it can issue preliminary findings based solely on complainant submissions. AI-generated summaries fall under personal-data definitions, forcing vendors to offer minimization controls, retention schedules, and role-based access. The EU AI Act classifies evaluation algorithms as high risk, layering extra transparency and bias-mitigation requirements. Providers sporting SOC 2, ISO, and GDPR-ready attestations gain an edge as buyers de-risk compliance exposure.

Organizational Resistance to Cultural Change in Performance Evaluation

Shifting to continuous feedback disrupts engrained rituals. Perceptyx found only 51% of employees see improvements following action plans, exposing a 20-point execution gap. Managers accustomed to annual cycles often lack skills to run weekly check-ins or real-time calibrations. Deloitte warns of “cultural debt” when AI reshapes norms without parallel behavior support. Platforms now embed behavioral-science nudges, prioritized action queues, and phased rollouts to mitigate inertia. Vendors that measure fairness perceptions and recognition-sentiment metrics alongside goal attainment can flag trust erosion before it poisons adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as AI Complexity Rises

Services revenue is accelerating as customers struggle to integrate AI outputs, map data flows, and train managers on continuous feedback. In 2025 software still commanded 61.45% of the continuous performance management platform market, yet implementation and integration engagements are expanding at a 12.21% CAGR. The continuous performance management platform market size for professional services grows because Oracle’s 25D features and SAP’s agent releases demand configuration, governance, and change-management expertise.[2]Oracle, “Feature Summary: HCM 25D,” oracle.com Support contracts also balloon as HR teams lack the capacity to measure AI success metrics, corroborating SHRM’s finding that 56% of firms never track AI ROI.

A second growth engine is compliance consulting: data-protection impact assessments and role-based access design remain mandatory when AI qualifies as large-scale monitoring. Vendors able to bundle consultancy with recurring managed services lock in multi-year revenue, pushing the continuous performance management platform market beyond a license-centric model.

By Deployment Mode: Cloud Overtakes Legacy On-Premises

Cloud adoption is set to eclipse on-premises during the forecast, expanding at a 13.01% CAGR as enterprises seek frictionless upgrades, lower CapEx, and elastic AI consumption. Although legacy installations retained 68.19% of the continuous performance management platform market share in 2025, vendor roadmaps reveal weekly cloud feature drops versus annual on-premises patches. Workday Flex Credits exemplify the pay-as-you-grow model, and a 2026 academic study confirmed cloud architectures improve appraisal-cycle responsiveness and data accuracy.

Highly regulated sectors still deploy on-premises versions to satisfy data-sovereignty rules, preserving a sizable installed base. Yet procurement math is shifting: specialized SaaS vendors quote four-to-eight-week implementations, well below the nine-to-eighteen-month timelines of suite upgrades, accelerating time-to-value and solidifying cloud’s ascendancy within the continuous performance management platform market.

By Organization Size: SMEs Accelerate Adoption

Small and medium enterprises are closing the functionality gap, with the segment advancing at a 12.67% CAGR through 2031. Affordable SaaS packages embed OKR templates, real-time feedback, and AI-assisted goal drafting that once required enterprise-scale budgets. Large organizations still dominate revenue at 72.12%, but integration complexity, layered approvals, and union rules slow their refresh cycles.

SMEs bypass legacy modules entirely, embracing cloud-native stacks from BambooHR, 15Five, and Leapsome that promise 4-8 week rollouts. SHRM’s 2026 survey shows performance AI adoption more prevalent in midsize than extra-large firms, indicating leapfrog behavior. As a result, the continuous performance management platform market size contribution of SMEs grows steadily, forcing vendors to diversify packaging and price points.

By End-User Industry: Healthcare Leads Growth

Healthcare and life sciences will outpace all industries with an 11.54% CAGR, propelled by clinician shortages and distributed care models that demand precise performance visibility. The continuous performance management platform market size within healthcare benefits from dashboards that tie productivity and patient-outcome metrics to development paths. IT and telecom, holding 26.11% share in 2025, continues to favor OKR alignment and agile sprints, but growth is now incremental rather than explosive.

BFSI clients emphasize audit logs and retention schedules to meet regulatory scrutiny, while retail experiments with AI-driven goal cascades that align merchandising automation with revenue uplift. Manufacturing integrates uptime and quality KPIs, and education pilots faculty development use cases. Vendors that deliver industry-specific data models and compliance guardrails capture outsized deal flow across these verticals.

Geography Analysis

North America held 36.86% of 2025 revenue and remains the largest regional contributor, buoyed by dense ecosystems of HCM vendors, consultants, and early adopters. U.S. firms show a high tolerance for piloting unfinished AI, but the regulatory backdrop is tightening as 19 states now regulate employer AI. Canada and Mexico trail in adoption yet benefit from multinational cloud rollouts that standardize processes across the continent.

Asia-Pacific is the fastest-growing region at an 11.98% CAGR, underpinned by CHRO mandates to shift from headcount planning to skills-based strategies. India’s IT services clusters and Australia’s mature services economy mirror North American adoption curves, while China blends performance data with manufacturing KPIs. Data-residency laws and fragmented regulations complicate cross-border implementations, but local-language interfaces and regional data centers are lowering barriers.

Europe presents a mixed picture: cloud uptake is strong in Germany and the UK, but GDPR obligations and works-council consultations elongate sales cycles. The UK ICO’s new complaint rules elevate compliance risk, and the EU AI Act classifies performance algorithms as high risk, forcing vendors to invest heavily in transparency features. Middle East and Africa plus South America are nascent yet promising, with Saudi Arabia, the United Arab Emirates, Brazil, and Argentina piloting cloud HR stacks under digital-first government programs. Infrastructure gaps and currency volatility temper growth, but multinational subsidiaries are seeding demand that gradually radiates to local firms.

Competitive Landscape

The continuous performance management platform market is moderately fragmented. Global HCM suites, SAP SuccessFactors, Oracle Cloud HCM, Workday, Dayforce, compete head-to-head with specialists such as Betterworks, Lattice, Culture Amp, 15Five, and Leapsome. Workday launched its Performance Agent in 2025, and Lattice announced its AI-powered review drafts for summer 2026.[3]Lattice, “Spring/Summer 2026 Product Release,” lattice.com Thoma Bravo’s USD 12.3 billion Dayforce buyout signals private-equity conviction that recurring HCM revenue can be amplified through AI add-ons. Phenom’s Included acquisition underscores the premium on people analytics engines capable of reconciling disparate HR data.

Technology depth is the new battleground. Providers racing to embed agentic AI, skills graphs, and explainability dashboards increasingly differentiate on SOC 2 and GDPR readiness, nightly HRIS synchronizations, and native Slack and Teams integrations. Specialists win on speed, four-to-eight-week launches, whereas suites tout single-platform simplicity. Industry-specific extensions, especially for healthcare and retail, offer a green-field opportunity where many general-purpose suites still lack domain flavor.

Pricing innovation is also shifting power dynamics. Workday Flex Credits and consumption-based AI licensing reduce lock-in fears, while point solutions push modular packages at SMB-friendly price points. Vendors reliant on annual-review templates face margin pressure as buyers equate lack of continuous-feedback tooling with strategic risk, accelerating churn toward AI-native alternatives.

Continuous Performance Management Platform Industry Leaders

SAP SE

Oracle Corporation

Workday Inc.

UKG Inc.

ADP, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Betterworks unveiled AI-powered Talent Intelligence that converts continuous performance data into real-time workforce insights.

- April 2026: SAP rolled out SuccessFactors 1H 2026, adding Goal Creation and Goal Progress Agents across the suite.

- January 2026: Phenom acquired Included to embed agentic analytics that reconcile inconsistent HR data.

- November 2025: Thoma Bravo closed its USD 12.3 billion acquisition of Dayforce to accelerate AI leadership.

Global Continuous Performance Management Platform Market Report Scope

Software solutions in the Continuous Performance Management Platform Market facilitate real-time performance tracking between managers and employees. These platforms enable continuous feedback, structured check-ins, goal alignment, and coaching. By offering data-driven insights, CPMs move beyond traditional annual review cycles. The market encompasses both standalone CPM tools and CPM modules integrated into broader Human Capital Management (HCM) suites.

The Continuous Performance Management Platform Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises [SMEs]), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and Consumer Goods, Manufacturing, Government and Public Sector, Education, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Continuous Feedback Software |

| Performance Review Workflow Software | |

| Talent and Skill Development Tracking Software | |

| Integration and API Management Modules | |

| Other Software | |

| Services | Implementation and Integration Services |

| Support and Maintenance Services |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and Consumer Goods |

| Manufacturing |

| Government and Public Sector |

| Education |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Continuous Feedback Software |

| Performance Review Workflow Software | ||

| Talent and Skill Development Tracking Software | ||

| Integration and API Management Modules | ||

| Other Software | ||

| Services | Implementation and Integration Services | |

| Support and Maintenance Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-User Industry | IT and Telecom | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Retail and Consumer Goods | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Education | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current continuous performance management platform market size and how fast is it growing?

The market stands at USD 3.24 billion in 2026 and is projected to reach USD 5.47 billion by 2031 at an 11.03% CAGR, according to Mordor Intelligence.

Which deployment model is expanding fastest across performance platforms?

Cloud-based deployments are growing at a 13.01% CAGR because organizations value faster upgrades, elastic AI licensing, and lower capital expense, notes Mordor Intelligence.

Why are services revenue rising faster than software in this space?

Enterprises need integration, change-management, and compliance expertise to embed agentic AI and configure nightly HRIS synchronizations, driving a 12.21% CAGR for services.

Which end-user industry will see the highest growth through 2031?

Healthcare and life sciences lead with an 11.54% CAGR as health systems confront clinician shortages and adopt productivity-driven goal alignment.

How does data privacy regulation affect platform adoption in Europe?

GDPR and the forthcoming EU AI Act add transparency, audit, and retention obligations, lengthening procurement cycles and favoring vendors with mature compliance toolkits.

Page last updated on: