Enterprise Performance Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

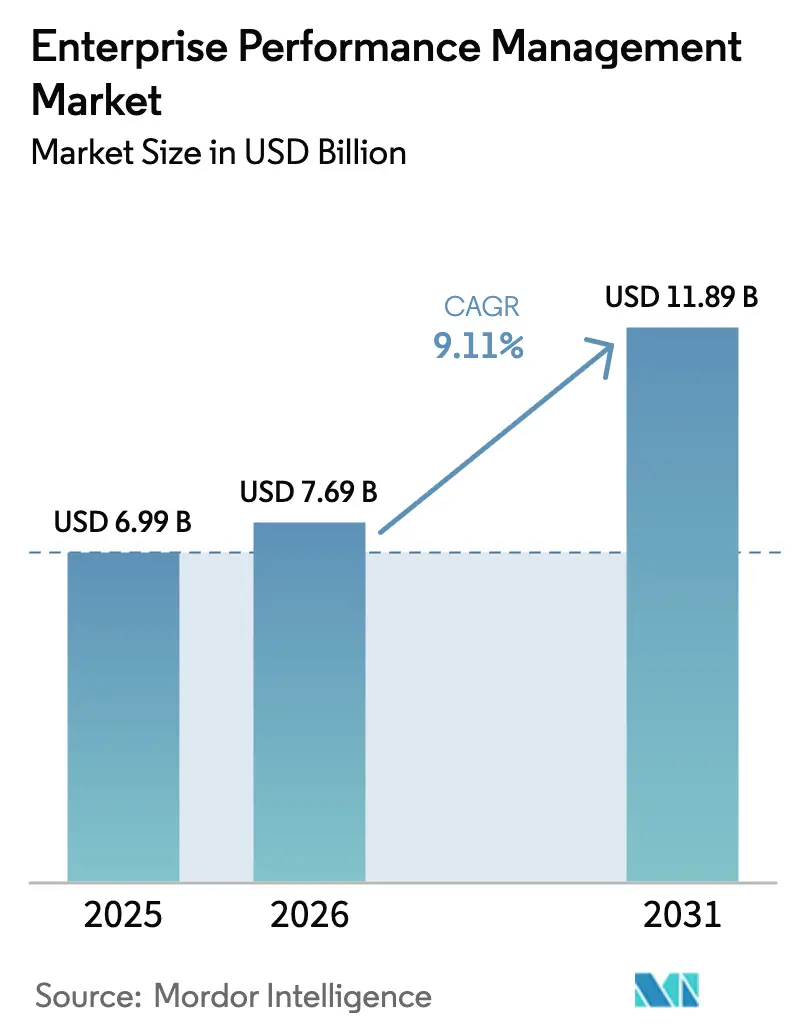

| Market Size (2026) | USD 7.69 Billion |

| Market Size (2031) | USD 11.89 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Performance Management Market Analysis by Mordor Intelligence

The Enterprise Performance Management Market size is projected to expand from USD 6.99 billion in 2025 and USD 7.69 billion in 2026 to USD 11.89 billion by 2031, registering a CAGR of 9.11% between 2026 to 2031.

Continuous, AI-assisted scenario modelling is supplanting legacy annual budgeting, allowing finance teams to recalibrate quarterly forecasts in hours. Mandatory disclosures such as the European Union’s Corporate Sustainability Reporting Directive are pulling non-financial data most notably carbon-intensity metrics into the same planning workflows that govern cash-flow projections. Mid-market organizations in North America are accelerating cloud migration to cut close cycles by up to 40%, while large banks integrate climate-risk stress tests directly into EPM models to meet updated regulatory guidelines. Competitive dynamics favour vendors able to embed generative AI and ESG functionality natively, pushing the market toward unified data models that eliminate reconciliation overhead.

Key Report Takeaways

- By component, solutions captured 71.42% of 2025 revenue, whereas services are advancing at a 9.89% CAGR through 2031.

- By deployment mode, cloud installations accounted for 66.58% of the 2025 base, and the segment is expanding at a 9.57% CAGR to 2031.

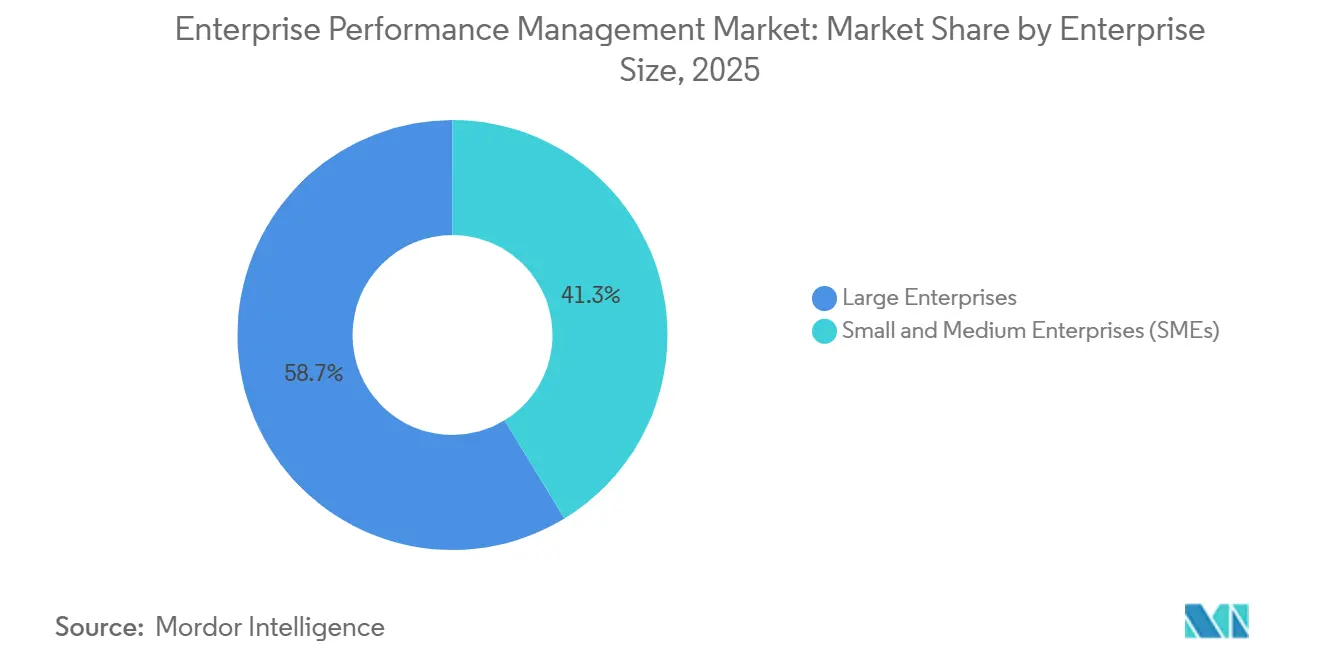

- By enterprise size, large enterprises owned 58.72% of 2025 spending, but small and medium enterprises are set to grow at a 10.01% CAGR.

- By end-user industry, banking, financial services, and insurance held 24.29% of 2025 spending, while healthcare is forecast to rise at a 10.34% CAGR to 2031.

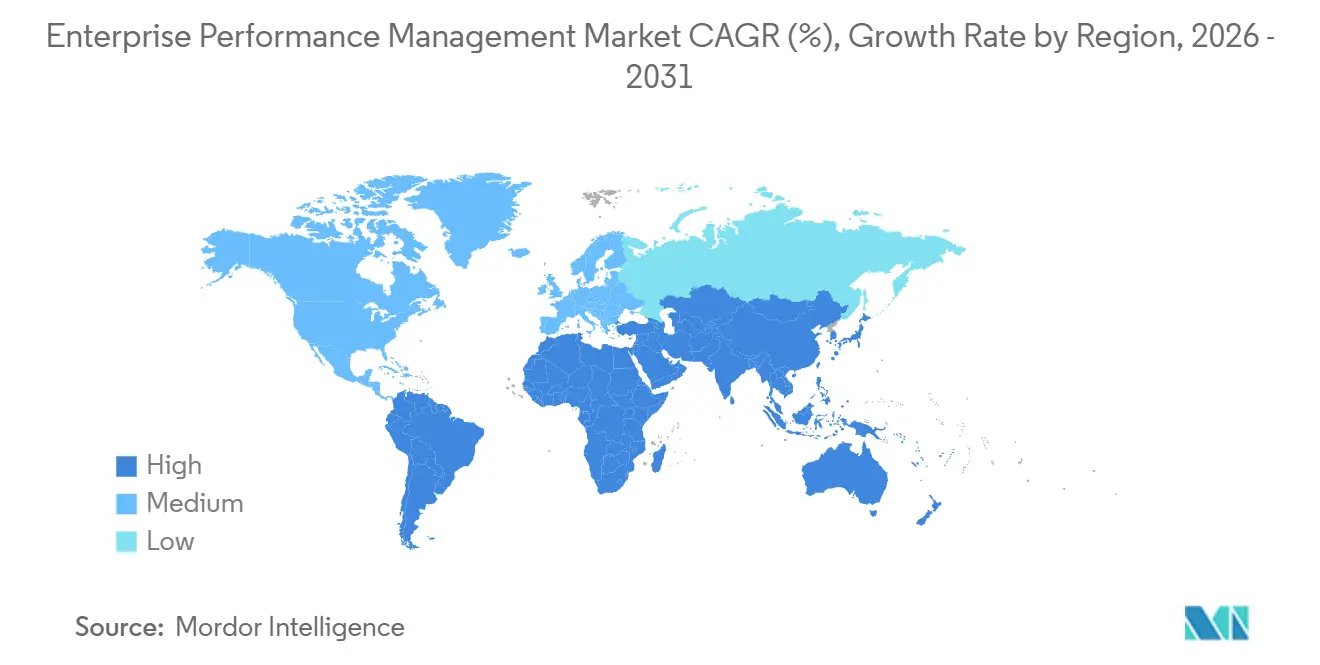

- By geography, North America accounted for 41.37% of the market in 2025, while Asia Pacific represented 10.46% of global revenue, with the remaining 48.17% contributed by other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Performance Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Cloud-Native EPM Suites for Real-Time FP&A in Mid-Market North America | +1.80% | North America, spillover to Europe and Asia Pacific | Medium term (2-4 years) |

| Integration of AI/ML for Scenario Modeling in European Multinationals | +1.50% | Europe, North America, Asia Pacific | Medium term (2-4 years) |

| Convergence of EPM with ESG and Integrated Reporting Mandates in EU | +1.30% | Europe, expanding to North America and Asia Pacific | Long term (≥ 4 years) |

| Digital Finance Transformation Programs Spurred by US SOX Modernization Act | +1.00% | North America, multinational corporations globally | Short term (≤ 2 years) |

| Adoption of xP&A Across Global Retail Supply Chains | +1.20% | Global, with concentration in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Rise of API-First Composable Finance Architectures Enabling Plug-and-Play EPM Modules | +1.40% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Cloud-Native EPM Suites for Real-Time FP-and-A in Mid-Market North America

Mid-market companies are discarding on-premises consolidation tools in favour of cloud suites that deliver real-time variance analysis and rolling forecasts. Subscription pricing removes upfront capital expenditure, while mobile access supports remote work patterns. Oracle reported 25% year-over-year growth in Fusion Cloud EPM bookings for organizations with USD 500 million-USD 2 billion in annual revenue.[1]Oracle Corporation, “Q2 2025 Earnings Call Transcript,” ORACLE.COM Workday noted that its Adaptive Planning customer count exceeded 6,500 in early 2025, up 30% from 2024, attributing the expansion to embedded anomaly-detection models.[2]Workday, “Adaptive Planning Customer Growth Press Release,” WORKDAY.COM Natural-language query interfaces are widening user adoption beyond finance specialists.

Integration of AI and ML for Scenario Modelling in European Multinationals

European manufacturers and pharmaceutical firms have embraced probabilistic forecasting to account for currency swings and supply-chain shocks. Anaplan disclosed that 40% of its European customers adopted the Predictive Insights engine within 12 months of launch. IBM added automated what-if generation to Planning Analytics in late 2024, enabling thousands of scenario permutations in minutes. Regulatory drivers amplify demand: updated European Banking Authority stress tests require climate-risk simulations over decade-long horizons.

Convergence of EPM with ESG and Integrated Reporting Mandates in the EU

The Corporate Sustainability Reporting Directive obliges roughly 50,000 companies to publish environmental and social metrics alongside financials, forcing alignment between sustainability and finance data pipelines.[3]European Commission, “Corporate Sustainability Reporting Directive Explained,” EUROPA.EU Wolters Kluwer launched an ESG module for CCH Tagetik that cuts manual data entry by 60%, while OneStream embedded carbon accounting into its unified platform in 2025. Early adopters report 30% shorter audit preparation cycles because non-financial disclosures now share lineage with statutory actuals.

Adoption of xP-and-A Across Global Retail Supply Chains

Retailers link procurement, inventory, and promotions within a single planning model to manage volatile demand. Board International’s Intelligent Planning Platform helped a European grocer reduce stockouts by 18% while safeguarding margins. Workday’s 2025 roadmap introduced workforce-planning modules that connect store labour budgets to traffic forecasts, tightening alignment between operations and finance. McKinsey research found 20-30% gains in seasonal forecast accuracy when merchants integrated point-of-sale data and weather information.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Quality Silos in Decentralized ERP Landscapes of Large Asian Conglomerates | -0.90% | Asia Pacific, particularly China, India, Japan, South Korea | Medium term (2-4 years) |

| Shortage of FPandA Talent Restricting Advanced EPM Rollouts in Europe | -0.70% | Europe, spillover to North America | Long term (≥ 4 years) |

| Perceived Security Risks Hindering Cloud Migration in Middle East Financial Institutions | -0.50% | Middle East, particularly UAE, Saudi Arabia | Short term (≤ 2 years) |

| High TCO for Multi-Module EPM Suites among Latin American SMEs | -0.60% | Latin America, particularly Brazil, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of FP-and-A Talent Restricting Advanced EPM Rollouts in Europe

CFOs struggle to recruit analysts who can configure driver-based models and interpret machine-learning outputs. PwC’s 2025 workforce survey indicated that 58% of European finance leaders cite FP-and-A talent shortages as a top three obstacle. Deloitte observed that average project timelines have stretched to nine months, versus six in North America, due to extended user training. Professional bodies have launched cloud-EPM certifications, yet supply remains insufficient.

Perceived Security Risks Hindering Cloud Migration in Middle East Financial Institutions

Banks in the UAE and Saudi Arabia hesitate to place balance-sheet data on global clouds given data-sovereignty rules. The UAE Data Protection Law mandates local storage of resident data, complicating single-tenant deployments. Saudi guidelines require regulatory approval before transferring critical information abroad. Oracle and SAP have opened regional cloud regions, but premium pricing and lengthy audits dilute immediate ROI. Analysts expect convergence toward international standards within two to three years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Implementation Complexity Rises

Solutions accounted for 71.42% of 2025 revenue, reaffirming software subscriptions as the primary spending driver in the Enterprise Performance Management market. Services, however, are growing faster at a 9.89% CAGR because multi-module deployments across finance, sales, and supply-chain functions require change-management, data-integration, and training expertise that most organizations lack internally. Advisory firms reported 35% headcount growth in EPM practices to meet this demand.

Service momentum is sustained by subscription-based managed offerings that provide monthly close assistance and model tuning. Implementation projects average six to nine months, and enterprises allocate 40-50% of their budgets to workshops that align operational and financial metrics. As generative-AI copilots proliferate, user-training packages are expanding to include prompt-engineering curricula, further lifting services revenue.

By Deployment Mode: Cloud Dominance Deepens

Cloud installations represented 66.58% of the 2025 base and are advancing at a 9.57% CAGR, underscoring a decisive shift in the Enterprise Performance Management market toward subscription delivery. API-first architectures allow finance leaders to layer best-of-breed modules onto existing ERP cores without disruptive replacements. On-premises footprints persist in defense and certain financial sectors with strict data-localization mandates.

Quarterly feature updates on multi-tenant clouds shrink the innovation gap, delivering AI forecasting and natural-language query tools without protracted upgrades. Hybrid deployments, mixing on-premises transaction processing with cloud planning, are emerging in jurisdictions such as China where residency rules remain stringent. Sovereign-cloud offerings promise further momentum by satisfying local compliance without sacrificing elasticity.

By Enterprise Size: SMEs Accelerate Adoption

Large enterprises claimed 58.72% of 2025 spending thanks to complex consolidation needs, yet SMEs are set to grow at a 10.01% CAGR, widening overall penetration in the Enterprise Performance Management market. Low-code platforms priced between USD 10,000 and USD 50,000 annually have lowered barriers for finance teams of fewer than ten employees. Subscription models let smaller firms add modules incrementally as scale dictates.

Large organizations maintain absolute spending leadership due to multi-currency consolidations and integrated ESG reporting. Still, SME-targeted vendors such as Vena and Prophix reported double-digit growth by packaging pre-built templates and low-code configuration wizards. Private-equity ownership accelerates adoption as portfolio companies standardize reporting.

By End-User Industry: Healthcare Surges on Value-Based Care

BFSI captured 24.29% of 2025 expenditure, driven by Basel III capital reporting and real-time profitability analysis, yet healthcare is the fastest-rising segment at a 10.34% CAGR as providers pivot to value-based reimbursement. Hospitals leverage EPM to tie clinical outcomes such as readmission rates to financial forecasts, positioning the Enterprise Performance Management market to support dynamic cost-allocation across departments.

Financial institutions continue to expand models to incorporate climate-risk adjustments under evolving regulatory regimes, while manufacturers and retailers embed xP-and-A to align production and inventory with volatile demand. Government agencies adopt EPM to meet transparency mandates requiring monthly budget-versus-actual disclosures.

Geography Analysis

North America retained 41.37% of 2025 revenue, reflecting early cloud adoption and Sarbanes-Oxley driven audit controls. U.S. mid-market firms migrate to AI-enabled suites to trim close cycles, whereas Canadian corporates integrate ESG data to comply with federal climate-disclosure rules. Mexico’s shared-service expansion fuels multi-currency consolidation demand. Platform consolidation trends favour unified suites that lower total cost of ownership.

Asia Pacific is the fastest-growing region at a 10.46% CAGR, led by transformation programs in India and China where conglomerates standardize planning across numerous subsidiaries. Japanese reforms mandating quarterly guidance accelerate cloud-planning uptake. Data-quality silos, however, lengthen implementations by up to 50% in decentralized ERP environments.

Europe’s trajectory is shaped by ESG reporting convergence, with large corporates integrating carbon metrics into statutory workflows. The Middle East faces adoption headwinds due to security concerns, despite new in-country cloud regions, while Latin American SMEs wrestle with total cost of ownership amidst currency volatility. Africa’s nascent market centers on South African and Nigerian banks implementing EPM to support regional expansion.

Competitive Landscape

The top five vendors Oracle, SAP, Workday, IBM, and Anaplan held roughly 45-50% of 2025 revenue, indicating moderate concentration within the Enterprise Performance Management market. ERP incumbents cross-sell planning modules that inherit native data integrations, but pure plays such as OneStream, Planful, Vena, and Prophix win multi-ERP environments through unified data models that eliminate reconciliation. OneStream surpassed 1,400 customers by combining consolidation, planning, reporting, and ESG in a single platform.

Strategic focus converges on three themes: embedding generative AI to automate variance narratives, expanding into ESG and supply-chain planning, and deepening vertical specialization. SAP’s Joule copilot enables natural-language queries, while Oracle patented ML algorithms that flag consolidation anomalies. Talent shortages in Europe create service-partner opportunities, prompting vendors to add low-code configuration to reduce dependency on scarce FP-and-A experts.

Midsized healthcare and retail remain white-space opportunities, as unified EPM-ESG and xP-and-A capabilities are still nascent in those verticals. Sovereign-cloud offerings are emerging as a regional differentiator in markets with stringent residency rules, potentially reshuffling regional vendor rankings over the next four years.

Enterprise Performance Management Industry Leaders

IBM Corporation

SAP SE

Oracle Corporation

CA Technologies (Broadcom Inc.)

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mayer Brown advised Empresas Públicas de Medellín on a USD 650 million unsecured facility to modernize 26 power plants and fund an EPM rollout, illustrating infra-linked finance strategy.

- February 2025: Nucleus Research published the 2025 CPM Technology Value Matrix highlighting generative-AI narrative reporting; vendors use the ranking in go-to-market messaging to capture up-market deals.

- January 2025: IBM bought AST for Oracle Cloud EPM expertise, signaling a services-led growth hedge as software margins compress.

- November 2024: Board International acquired Prevedere to integrate external economic intelligence, strengthening xP&A positioning for retail and CPG clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Enterprise Performance Management (EPM) market as all software and associated subscription services that help an organization plan, budget, forecast, consolidate, and analyze performance across finance and operations, regardless of deployment mode or enterprise size. These platforms sit above core transactional systems and feed decision makers with KPI-level insight.

Scope exclusion: basic spreadsheet tools and standalone business-intelligence dashboards are outside the boundary.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- BFSI

- IT and Telecom

- Healthcare

- Manufacturing

- Retail and E-Commerce

- Energy and Utilities

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- UAE

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and surveys with CFOs, FP&A leads, system integrators, and regional channel partners in North America, Europe, Asia-Pacific, and the Gulf validated adoption triggers, average selling prices, and renewal ratios, enabling us to stress-test secondary findings and close information gaps.

Desk Research

We gathered foundational numbers from open public sources such as the U.S. Bureau of Economic Analysis, Eurostat's ICT enterprise statistics, Reserve Bank of India payment-system reports, and filings on the SEC's EDGAR database. Then, we verified vendor adoption trends through association portals such as the Software & Information Industry Association. Subscription inputs were enriched with D&B Hoovers company financials and Dow Jones Factiva news analytics, which allowed us to benchmark revenue implied by disclosed client wins against macro indicators.

Broader demand signals, cloud-spend trackers, OECD digital-transformation indices, and customs shipment codes for server infrastructure anchor the total addressable pool before being refined to the EPM stack. The list above is illustrative, not exhaustive; many other domain sources supported data checks and clarifications.

Market-Sizing & Forecasting

A top-down and bottom-up blend was applied. We first reconstructed global spend by mapping cloud and on-premise deployment revenues to sectoral IT-spend ratios. Then, we corroborated totals with sampled supplier roll-ups and regional channel checks. Key variables inside the model include average user-per-license counts, cloud migration velocity, regulatory compliance spending per industry, FP&A head-count trends, and mid-market ERP penetration. Multivariate regression links these drivers to historic EPM revenue so future values can be projected; scenario analysis adjusts for currency swings and macro slowdowns. Data voids in bottom-up estimates are bridged with analog markets of similar digital-workload density before being re-validated through expert calls.

Data Validation & Update Cycle

Mordor analysts run variance and anomaly checks against independent spend trackers, then a senior reviewer signs off. The model refreshes annually, with interim updates when material vendor disclosures or policy shifts occur.

Why Mordor's Enterprise Performance Management Market Baseline Earns Trust

Published estimates differ because firms pick varying component lists, inflation bases, and refresh cadences.

We focus on the full software plus subscription layer in current dollars and revisit assumptions each year, which keeps our baseline aligned with real purchasing power.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.05 B (2025) | Mordor Intelligence | - |

| USD 7.16 B (2025) | Global Consultancy A | excludes support subscriptions and uses prior-year exchange rates |

| USD 6.30 B (2025) | Industry Publisher B | narrower end-user mix and conservative cloud-shift assumption |

| USD 8.30 B (2027) | Data Services C | older base year with linear roll-forward, no mid-forecast refresh |

The comparison shows that values swing when the scope trims services, when currency locks at historic rates, or when models lack mid-period updates. By grounding inputs in verified spend drivers and by recalibrating annually, Mordor Intelligence delivers a balanced, transparent baseline that decision makers can replicate and trust.

Key Questions Answered in the Report

What is the projected value of the Enterprise Performance Management market by 2031?

The market is forecast to reach USD 11.89 billion in 2031, rising at a 9.11% CAGR from 2026.

Which deployment mode is growing fastest in Enterprise Performance Management?

Cloud deployment is expanding at a 9.57% CAGR, driven by API-first architectures and subscription pricing.

Why are services outpacing software growth in Enterprise Performance Management?

Organizations need external expertise to configure multi-module suites, integrate ESG data, and train users on AI features, lifting services to a 9.89% CAGR.

Which region is expected to grow quickest through 2031?

Asia Pacific leads with a 10.46% CAGR, propelled by large-scale finance-transformation programs in China and India.

How is ESG regulation influencing Enterprise Performance Management adoption?

EU mandates require companies to consolidate non-financial KPIs with financials, spurring demand for unified EPM-ESG platforms that cut audit prep time by 30%.

What competitive advantage do pure-play vendors hold over ERP incumbents?

Pure plays offer unified data models and vertical-specific features that minimize reconciliation work in heterogeneous ERP landscapes, winning deals in multi-system environments.

Page last updated on: