Contingent Workforce Management Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

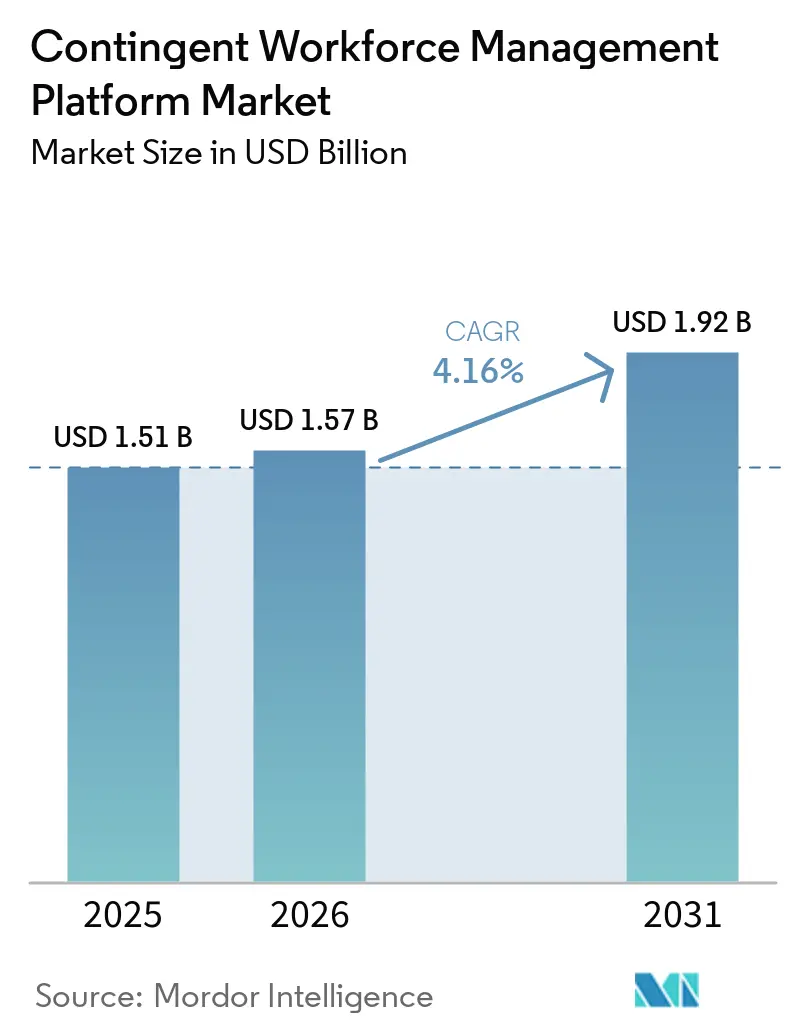

| Market Size (2026) | USD 1.57 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

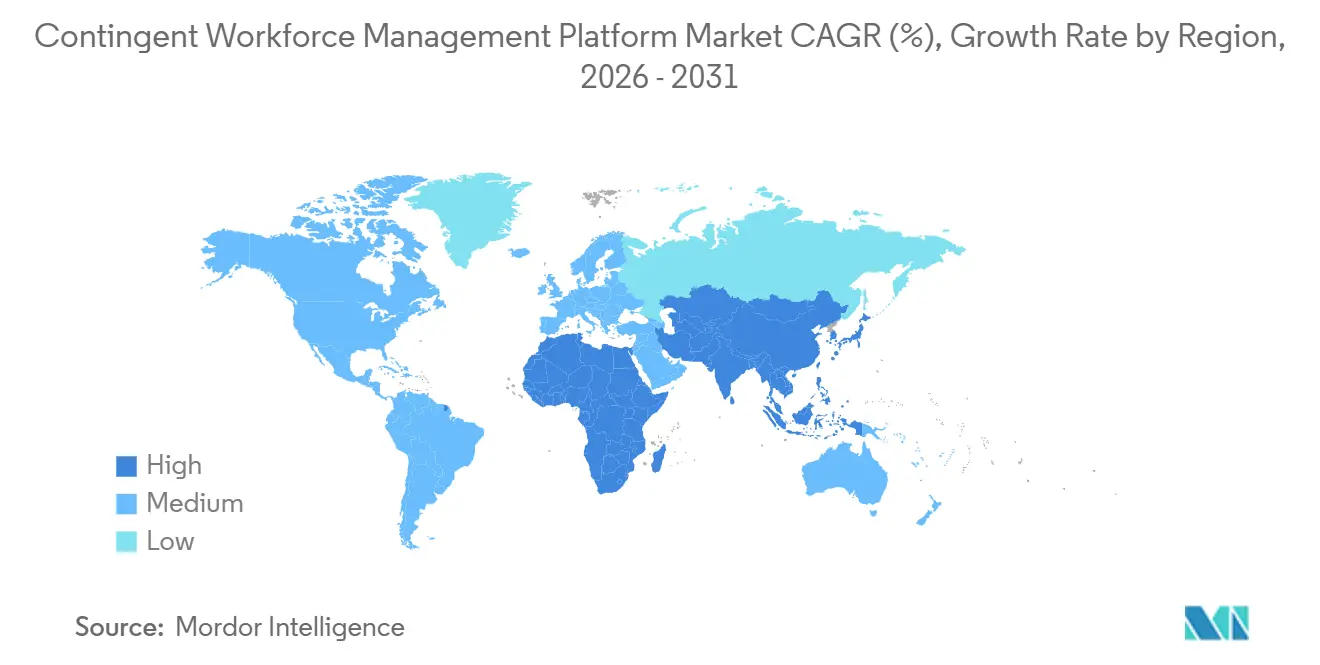

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

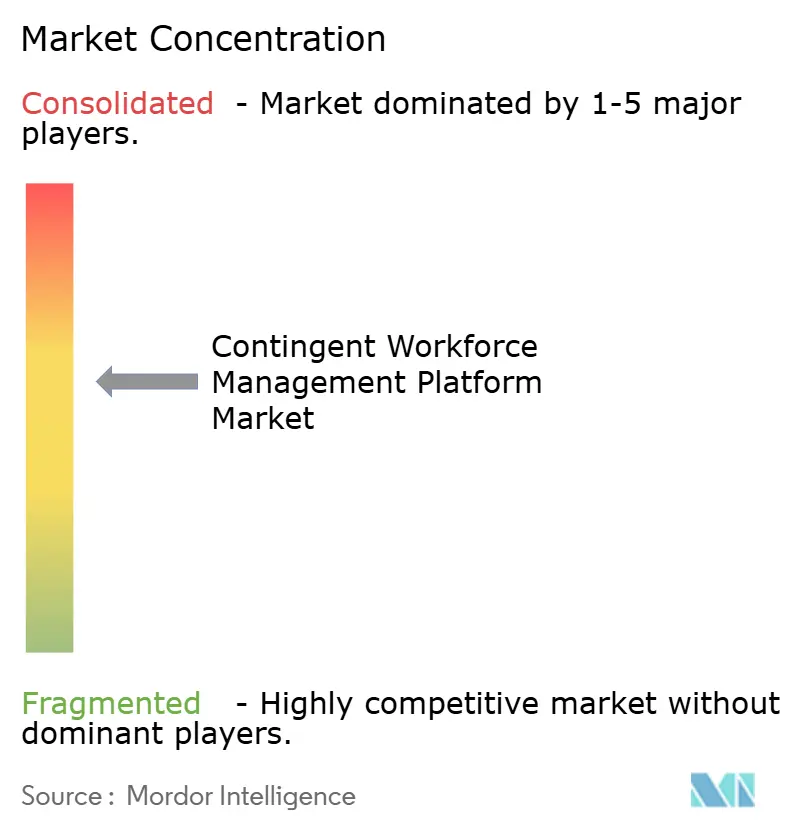

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contingent Workforce Management Platform Market Analysis by Mordor Intelligence

The contingent workforce management platform market size is projected to be USD 1.51 billion in 2025, USD 1.57 billion in 2026, and reach USD 1.92 billion by 2031, growing at a CAGR of 4.16% from 2026 to 2031. Demand is being shaped by a durable shift in enterprise labor strategy, as organizations rely more heavily on contractors, consultants, project specialists, and other non-employee talent across core business functions. That shift is moving buyers away from spreadsheet tracking and manual approvals toward governed platforms that can manage sourcing, onboarding, classification, tenure, invoicing, and supplier oversight in one place. Competition is now centered on compliance automation, AI-enabled visibility into spend and skills, and broader lifecycle coverage that goes well beyond simple requisition efficiency. The strongest revenue base still comes from large enterprise programs, but faster growth in services, cloud deployments, SMEs, and healthcare shows that the buyer mix is expanding. This leaves the contingent workforce management (WFM) platform market positioned between procurement digitization and workforce risk control, with growth supported by cloud migration, direct sourcing, and tighter cross-functional governance.

Key Report Takeaways

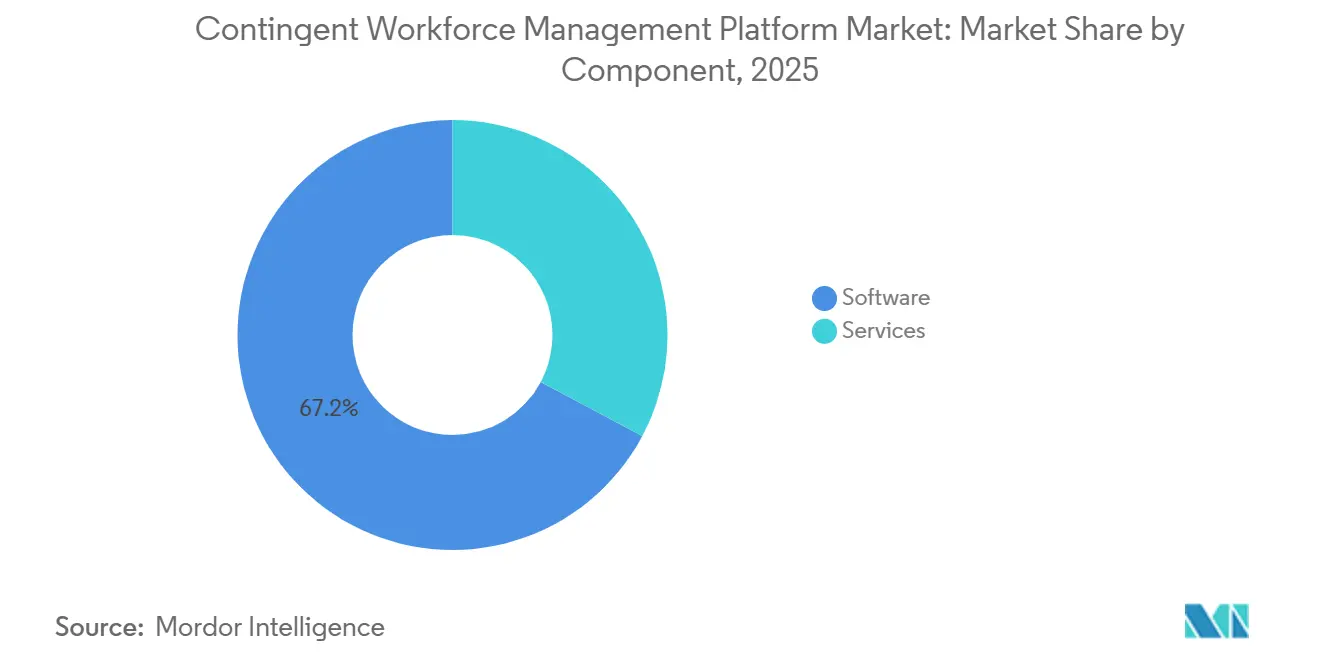

- By component, software held a 67.22% share in 2025, while services is forecast to expand at a 6.72% CAGR through 2031.

- By functionality, vendor management system retained the leading 35.66% share in 2025, while talent sourcing and direct sourcing integration is projected to record the fastest 5.99% CAGR through 2031.

- By deployment mode, on-premises accounted for 68.43% of revenue in 2025, while cloud-based deployment is set to grow at a 7.55% CAGR through 2031.

- By organization size, large enterprises represented 69.88% of revenue in 2025, while small and medium-sized enterprises are expected to advance at a 7.04% CAGR through 2031.

- By end-user industry, information technology and telecommunications led with a 38.21% share in 2025, while healthcare and life sciences is forecast to grow at a 5.45% CAGR through 2031.

- By geography, North America held a 37.65% share in 2025, while Asia-Pacific is expected to register the fastest 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Contingent Workforce Management Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Reliance on Flexible and Project-Based Labor | +1.2% | Global | Short term (≤ 2 years) |

| AI-Enabled Visibility, Matching, and Spend Optimization | +1.0% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Tightening Worker Classification and Labor Compliance Requirements | +0.7% | North America and EU | Short term (≤ 2 years) |

| Need for Faster Access to Specialized Digital And Professional Skills | +0.6% | Global, with early gains in APAC and North America | Medium term (2-4 years) |

| Expansion of Direct Sourcing and Private Talent Pool Strategies | +0.4% | North America and Europe | Medium term (2-4 years) |

| Convergence of Services Procurement and Contingent Labor Workflows | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Reliance on Flexible and Project-Based Labor

Flexible labor is now part of planned operating models, especially in sectors where delivery timelines, technology needs, and cost pressures change faster than permanent hiring cycles can adjust. That change raises the value of systems that can manage worker type, supplier use, approvals, onboarding, contract controls, and payment workflows with a common governance layer. The contingent workforce management (WFM) platform market benefits because enterprises want program-level visibility and consistent policy enforcement, rather than local contractor administration handled via email and spreadsheets. Higher-value external roles, including interim leaders and specialist consultants, also require stronger controls around tax treatment, intellectual property, contract value, and country-specific engagement rules. Buyers are therefore favoring platforms that can manage the full external worker journey and maintain auditable records across multiple talent channels. Beeline’s June 2025 acquisition of MBO Partners reflected this need for broader external talent coverage, including independent contractors, consultants, gig workers, and payrolled professionals, within a single, compliant environment.

AI-Enabled Visibility, Matching, and Spend Optimization

AI has moved from optional product differentiation to a baseline expectation in the contingent workforce management platform market. Enterprises now want faster matching, cleaner spend visibility, rate benchmarking, workflow suggestions, and better forecasting built directly into everyday program management. Beeline introduced Beeline AI in April 2025 with skills-proximity scoring, agentic capabilities, and automated compliance policy management built on its contingent labor data foundation. SAP Fieldglass strengthened the same direction in its May 2026 release through AI-assisted resume assessment, AI-enhanced statement-of-work collaboration, and automated worker role suggestions from SOW details.[1]SAP Fieldglass, “SAP Fieldglass May 2026 Release Preview,” SAP, help.sap.com These tools reduce sourcing and intake friction, but they also raise buyer expectations around explainability, oversight, and clear audit trails for decisions that affect external talent engagement. Vendors that combine automation with human review are gaining ground because procurement, HR, and legal teams want speed without giving up control.

Tightening Worker Classification and Labor Compliance Requirements

Worker classification rules are turning compliance from a legal back-office issue into a central buying decision in the contingent workforce management platform market. The EU Platform Work Directive created a rebuttable presumption of employment where direction and control are found, and member states must transpose the rules by December 2, 2026. In the United States, California’s AB5 guidance continued to reinforce retroactive liability exposure when independent contractor tests are not met, and documentation is weak. Platforms with classification workflows, tenure alerts, approval logic, and structured records help enterprises apply rules more consistently across departments and geographies. Centralized programs also create a stronger audit trail than decentralized purchasing channels, which rely on manual files and fragmented approvals. This makes compliance automation an important retention factor because once policies and controls are embedded in the operating model, switching platforms becomes more disruptive.

Need for Faster Access to Specialized Digital and Professional Skills

The need for scarce digital and professional skills is also supporting the contingent workforce management platform market. Enterprises increasingly need AI engineers, cybersecurity specialists, analytics talent, and transformation leaders on short notice, which favors pre-built sourcing channels and reusable external talent communities. This is shifting platform value from simple vendor routing toward private talent pools, skills-based matching, and better coordination between sourcing and compliance steps. Beeline AI applies skills-proximity scoring to improve matching, while SAP Fieldglass added AI-supported role suggestions from statement-of-work inputs in its May 2026 release. As direct sourcing matures, buyers want skills taxonomies, screening support, and reusable candidate workflows that can shorten time-to-fill without weakening governance. Vendors that can help enterprises activate specialized talent within days are moving closer to strategic workforce planning rather than remaining only administrative procurement tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex Integration with HRIS, ERP, Procurement, and Payroll Stacks | -0.8% | Global | Short term (≤ 2 years) |

| Data Privacy, Cybersecurity, and Cross-Border Data Transfer Risk | -0.6% | EU, North America, APAC | Medium term (2-4 years) |

| Rising Identity Fraud and Worker Verification Burden in Remote Hiring | -0.5% | North America, with spillover globally | Short term (≤ 2 years) |

| Governance Friction across HR, Procurement, Legal, and Finance Stakeholders | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex Integration with HRIS, ERP, Procurement, and Payroll Stacks

Integration remains the most persistent adoption barrier in the contingent workforce management platform market. Contingent labor programs usually cut across HR, procurement, finance, and payroll systems that were built separately and often use different definitions for worker type, cost center, supplier data, and invoicing rules. Beeline states that its platform supports 845 HCM and ERP integrations, including 500 Oracle, 440 SAP, and 405 Workday connections, which shows how broad the technical landscape has become. The same material notes that legacy batch-processing architectures can still create timing gaps and validation issues when buyers expect real-time API behavior. Integration cost and complexity can delay deployment decisions, especially when enterprises also need local tax, billing, supplier, and worker rules aligned across countries. Even so, organizations that postpone automation often continue to accumulate fragmented records and weaker auditability, which can make later transitions even harder.

Data Privacy, Cybersecurity, and Cross-Border Data Transfer Risk

Data governance risk continues to slow rollout decisions in the contingent workforce management platform market. These platforms hold personal data, rate cards, invoices, identity documents, work location details, and sensitive engagement records across several jurisdictions and internal teams. Cross-border programs face added pressure when data residency rules differ across the EU, India, China, and other markets that large employers must support within a single operating model. Vendors are responding with privacy-by-design architecture, local control options, and stronger security credentials to reassure regulated buyers. Magnit highlighted this direction when its VMS achieved Germany’s C5 cloud security certification in 2025, a meaningful trust signal for buyers who treat cloud assurance as part of vendor selection. The challenge is not only technical; legal, compliance, procurement, and IT teams must also agree on access, retention, monitoring, and transfer rules before a deployment can scale smoothly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Retention Masks a Services Inflection Point

Software held 67.22% of the contingent workforce management platform market share in 2025, while services are projected to expand at a 6.72% CAGR through 2031. Software remains the core revenue engine because buyers still want a system of record that centralizes requisitions, worker data, supplier lists, approval rules, timesheets, invoices, and reporting within a single operating layer. Configurable software also gives enterprises a practical way to enforce policies around tenure limits, onboarding steps, role approvals, and rate controls across business units that may otherwise manage external talent differently. The continued weight of software therefore reflects its role as the operational backbone of formal contingent labor programs, especially in global organizations with large spend under management. Yet the faster growth in services shows that many enterprises do not want to manage complex rollouts, integrations, and policy alignment on their own.

Implementation, integration, and managed support are becoming part of the standard buying package for buyers with global programs and cross-system complexity. The services mix is also moving beyond one-time setup work toward recurring support around compliance monitoring, supplier performance, analytics review, user administration, and program optimization. That change matters in the contingent workforce management platform industry because service teams often become part of day-to-day governance after the platform goes live and internal ownership matures. It creates a stickier revenue profile, with services reinforcing software retention and helping buyers handle multi-country operating models that are difficult to standardize quickly. The result is that end-to-end vendors and their partners are broadening their managed-service capabilities rather than relying solely on license growth, especially where buyers want measurable outcomes tied to compliance, fill rates, and spend visibility.

By Functionality: VMS Remains the Core, but Direct Sourcing Redefines Value

VMS retained a 35.66% share in 2025, while talent sourcing and direct sourcing integration are set to expand at a 5.99% CAGR through 2031. VMS remains the foundational layer because it connects requisitions, suppliers, approvals, timesheets, invoicing, and reporting into a single, governed workflow, rather than leaving them spread across several tools and email chains. Large enterprise programs still depend on this core capability to control spend and enforce policy across many geographies, cost centers, and staffing partners. Its leading share, therefore, reflects continued relevance rather than simple buyer inertia, since point solutions still struggle to replace the breadth of control that VMS platforms provide. At the same time, the faster growth of direct sourcing shows that buyers now want platforms to improve talent access and administration.

Enterprises are trying to reduce agency markup and improve reuse of pre-vetted talent pools before opening demand to the wider supplier network. SAP Fieldglass added AI-enhanced statement-of-work collaboration and automated worker role suggestions in May 2026, showing how sourcing features are moving closer to planning and intake workflows rather than staying separate from them. Compliance and risk management modules are also gaining weight as classification rules tighten and buyers want stronger evidence that engagement decisions were applied consistently. Spend management and rate benchmarking tools are attracting more finance attention as enterprises seek clearer visibility into contractor pricing, markups, and supplier performance across business lines. Contractor lifecycle management is expanding as external talent mixes now include independent professionals engaged through AOR and EOR models, while other modules, such as DEI tracking and mobile-first field labor support, show how the contingent workforce management platform industry is broadening beyond the historic VMS core.

By Deployment Mode: On-Premises Incumbency Gives Way to Cloud Momentum

On-premises held a 68.43% share in 2025, while cloud-based deployment is forecast to expand at a 7.55% CAGR through 2031. The installed base still leans toward on-premises because many large enterprise programs were designed before cloud VMS products cleared internal requirements for security, customization depth, and complex system connectivity. That legacy position keeps on-premises relevant in organizations where contingent labor governance is tightly linked to older ERP and HR environments or internal hosting policies. Even so, the wide growth gap shows that new investment is moving toward cloud-native delivery models across the buyer base. Buyers want faster updates, easier remote access, cleaner analytics delivery, and less dependence on local infrastructure management.

Magnit’s 2025 C5 certification in Germany supports this cloud transition by addressing a common objection from regulated buyers who prioritize security assurance in deployment decisions.[2]Magnit, “Magnit | Integrated Workforce Management Platform,” Magnit, magnitglobal.com Migration is rarely a full replacement, because many large organizations are keeping parts of recordkeeping and compliance processes in older environments while adding cloud modules for analytics, direct sourcing, and mobile access. This hybrid phase helps incumbents protect installed revenue, but it also creates openings for vendors that can deliver faster implementation and cleaner user experiences without demanding a complete rebuild. Vendors that support both deployment modes without compromising service quality are better positioned to retain legacy customers and attract newer cloud-first buyers. The contingent workforce management platform market is therefore moving through a staged transition, not a sudden break, and that favors providers that can manage coexistence as well as modernization.

By Organization Size: Large Enterprises Anchor Revenue, SMEs Expand Reach

Large enterprises accounted for 69.88% of revenue in 2025, while SMEs are projected to grow at a 7.04% CAGR through 2031. That split reflects the long history of formal contingent labor programs in multinational companies that manage large external workforce budgets across several regions, suppliers, and business units. Large buyers usually require stronger controls around policy enforcement, invoicing, data visibility, cross-border engagement, and stakeholder governance, which has made them the natural first adopters of VMS platforms. Their dominance also reflects the fact that they are more likely to treat contingent labor as a managed category with formal spend under management and executive oversight. SMEs are growing faster because vendors now offer lighter configurations that reduce the implementation burden that previously kept many smaller buyers out of the category.

These newer offerings lower the adoption threshold for companies that had been managing contractors through email, spreadsheets, staffing agency relationships, and disconnected finance processes. Beeline said customers using its Professional solution reported more than 80% lower onboarding time and 97% fewer manual errors, highlighting the operational appeal of mid-market packages built for speed and simplicity. In the contingent workforce management platform industry, this matters because smaller buyers tend to judge value on ease of use, time to launch, and total ownership cost more than on deep customization. Sales cycles are often shorter in this segment, but price sensitivity is stronger, and product simplicity matters more when internal teams are lean. That is pushing vendors toward guided setup, self-serve onboarding, and subscription models that fit buyers, formalizing mixed employee and contractor workforces for the first time.

By End-User Industry: IT and Telecom Leads, Healthcare Builds Fast

Information technology and telecommunications accounted for 38.21% in 2025, while healthcare and life sciences are forecast to grow at a 5.45% CAGR through 2031. IT and telecom remain the largest end-user group because project-based labor is deeply embedded in software delivery, network operations, cybersecurity programs, data modernization, and broader digital transformation work. Employers in this sector have long relied on staffing suppliers, statement-of-work arrangements, and specialist contractors, which makes formal governance platforms a natural fit. The segment’s scale also reflects the need to coordinate many external roles across distributed teams, fast project cycles, and high demand for scarce technical talent. Healthcare and life sciences are growing faster because providers and related organizations need more flexible staffing while still managing strict credentialing, scheduling, licensure, and compliance requirements.

That combination makes platform-grade workflow control more valuable than informal agency coordination, especially when multiple sites and worker types must be monitored within a single process. Banking, financial services, and insurance buyers use these platforms because external workers may access regulated systems, customer records, and sensitive internal data that require documented oversight. Manufacturing organizations depend on them to manage technical contractors, facility access, safety certifications, and shift-based labor needs that differ by location and production cycle. Retail and e-commerce organizations gain from more structured oversight of seasonal and high-volume flexible labor, especially when demand changes quickly, and supplier use must remain visible. As adoption spreads into energy, logistics, and public sector environments, the contingent workforce management (WFM) platform market is broadening from its technology-heavy roots into sectors where compliance discipline and scheduling complexity matter just as much as sourcing speed.

Geography Analysis

North America held 37.65% of the contingent workforce management platform market share in 2025 and remained the largest regional revenue base. The United States anchors demand because many large enterprises in the region already run formal contingent programs that integrate procurement, HR, finance, legal, and supplier management into a single operating model. Buyers in this region also face complex classification and co-employment exposures, which keep governance features high on the purchase agenda and support continued investment in formal systems of record. California’s AB5 guidance continued to reinforce the need for documented contractor tests and consistent classification workflows in 2026. Canada and Mexico are also becoming more relevant to program design as multinational employers extend common governance standards across North America instead of managing each country through local exceptions.

Europe is becoming a regulation-led growth area for the contingent workforce management platform market. The EU Platform Work Directive introduced a rebuttable presumption of employment where direction and control are found, and member states must transpose the rules by December 2, 2026. That legal pressure supports demand for platforms that can monitor classification, tenure, approvals, and worker status across different national rules and corporate entities.[3]European Labour Authority, “Addressing Platform Workers’ Employment Misclassification: Legal Frameworks, Enforcement Strategies and the New Platform Work Directive,” European Labour Authority, ela.europa.eu The United Kingdom remains important as vendors must support separate off-payroll compliance needs alongside the EU framework, while Germany stands out for its compliance-heavy temporary labor environment and strong demand for governed external workforce processes.

Asia-Pacific is forecast to grow at a 6.31% CAGR through 2031, the fastest regional rate in the contingent workforce management platform market. China, India, Japan, and Southeast Asia are expanding the pool of project-based and platform-mediated work, which is drawing more formal governance and technology investment from local firms and multinational employers. India stands out as a major growth point because global enterprises continue to manage large contractor populations in IT and digital services delivery, and need better visibility across suppliers and engagements. The Middle East is still early in adoption, but the UAE and Saudi Arabia are creating space for structured oversight of external workforces as non-national labor programs expand under diversification efforts. South America and Africa remain less mature, yet Brazil and South Africa serve as the main regional anchors for multinational buyers seeking more consistent contingent workforce control and clearer audit trails.

Competitive Landscape

The contingent workforce management (WFM) platform market is moderately consolidated at the enterprise tier, but it remains fragmented in the mid-market and specialist layers. Beeline, SAP Fieldglass, Magnit, and Workday VNDLY compete most directly where buyers want large-scale programs, deep policy coverage, global reach, and broad integration coverage. Beeline expanded its scope in June 2025 by acquiring MBO Partners, which added AOR and EOR capabilities for independent talent into its platform model. That move addressed a long-standing gap in which independent contractor categories often sat outside formal VMS governance, even when temporary staffing was already managed centrally. As a result, enterprise competition is shifting from pure requisition management toward broader control of all external talent categories.

Product differentiation now centers on AI depth, compliance automation, and the ability to support sourcing, engagement, and spend control in one environment. SAP Fieldglass has reinforced its position through broad country and language support and through Joule AI support for requisition creation, statement-of-work intake, and workflow acceleration. Flextrack launched agentic AI on Salesforce in April 2026, aimed at mid-market users who want autonomous workflows with GDPR and CCPA auditability. Magnit has also pushed AI-led workflow and analytics capabilities through its Maggi companion and its direction for an integrated workforce platform. These moves are raising buyer expectations across the contingent workforce management platform market, especially around explainability, speed, and operational visibility that can support procurement, HR, and finance simultaneously.

White space remains in healthcare-focused contingent management, where clinical credentialing and workforce governance need to work together without extra manual layers. Another open area is SME-oriented deployment across Asia-Pacific, where local regulatory support and lighter implementation models can matter more than enterprise feature depth. Vendors are also investing more heavily in worker verification, skills models, and rate intelligence as they search for harder-to-copy product advantages. This leaves the contingent workforce management platform market with a stable enterprise core, active capability expansion, and meaningful room for new competition at the edges.

Contingent Workforce Management Platform Industry Leaders

Magnit, LLC

Avature Limited

Worksuite Inc.

Eqip AG

Ceipal Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP released the SAP Fieldglass May 2026 update, introducing AI-assisted resume assessment in German, Spanish, and French, AI-enhanced SOW collaboration with automated worker role generation, and a simplified "essentials" contingent module for accelerated implementations across Financial Services, Healthcare, Public Sector, and Manufacturing verticals.

- April 2026: Flextrack launched agentic AI capabilities natively integrated into its Salesforce-based VMS, enabling autonomous workflows for job description creation, supplier recommendations, and real-time risk flagging with full GDPR and CCPA audit trails. The launch represented a significant capability upgrade for mid-market contingent program managers seeking AI-driven workforce intelligence without developer intervention.

- March 2026: Synergie completed its acquisition of a majority stake in Agilus Work Solutions, Canada’s eighth-largest staffing player with revenues of CAD 300 million (USD 219 million) in 2025, significantly expanding Synergie’s Canadian footprint in IT, engineering, and professional staffing and accelerating its North American strategy.

- January 2026: Atlantic International Corp. acquired Circle8 Group in an all-stock transaction, creating a combined global workforce solutions platform with USD 1.2 billion in unaudited annual revenue and extending the company’s reach into higher-margin European IT and technology talent solutions.

Global Contingent Workforce Management Platform Market Report Scope

Platforms in the contingent workforce management arena assist organizations in overseeing external workers, including contractors and freelancers. Offering features like vendor management and compliance tracking, these platforms navigate a procurement-centric ecosystem, often collaborating with staffing agencies. Their main objectives are to enhance workforce flexibility, manage costs, and uphold regulatory standards for temporary labor.

The Contingent Workforce Management Platform Market Report is Segmented by Component (Software, and Services [Implementation and Integration, and Support and Maintenance]), Functionality (Vendor Management System [VMS], Contractor Lifecycle Management, Talent Sourcing and Direct Sourcing Integration, Compliance and Risk Management, Spend Management and Rate Benchmarking, and Other Functionalities), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-sized Enterprises), End-User Industry (Information Technology and Telecommunications, Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Manufacturing, Retail and E-commerce, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration |

| Support and Maintenance |

| Vendor Management System (VMS) |

| Contractor Lifecycle Management |

| Talent Sourcing and Direct Sourcing Integration |

| Compliance and Risk Management |

| Spend Management and Rate Benchmarking |

| Other Functionalities |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Information Technology and Telecommunications |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By component | Software | |

| Services | Implementation and Integration | |

| Support and Maintenance | ||

| By Functionality | Vendor Management System (VMS) | |

| Contractor Lifecycle Management | ||

| Talent Sourcing and Direct Sourcing Integration | ||

| Compliance and Risk Management | ||

| Spend Management and Rate Benchmarking | ||

| Other Functionalities | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End-User Industry | Information Technology and Telecommunications | |

| Banking, Financial Services, and Insurance | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the contingent workforce management platform market?

The contingent workforce management platform market stands at USD 1.57 billion in 2026 and is projected to reach USD 1.92 billion by 2031, advancing at a 4.16% CAGR over 2026-2031.

Which segment leads revenue in contingent workforce management platforms?

Software remains the largest component with a 67.22% share in 2025, supported by its role as the system of record for requisitions, suppliers, approvals, invoicing, and reporting.

Why is cloud-based deployment growing faster than on-premises?

Cloud-based deployment is forecast to grow at 7.55% through 2031 because buyers want faster upgrades, easier access, better analytics delivery, and lower infrastructure burden than older on-premises models.

Which functionality is expanding the fastest in this space?

Talent sourcing and direct sourcing integration is the fastest-growing functionality at a 5.99% CAGR through 2031, as enterprises try to reduce agency dependence and activate private talent pools faster.

Why are SMEs becoming a more important buyer group?

SMEs are projected to grow at a 7.04% CAGR because vendors now offer lighter packages with pre-built integrations, quicker onboarding, and lower implementation effort than classic enterprise deployments.

What are the main barriers to wider adoption?

Integration across HRIS, ERP, procurement, and payroll systems remains the largest barrier, while privacy, cybersecurity, cross-border data controls, identity verification, and stakeholder alignment also slow rollout speed.

Page last updated on: