Colombia Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

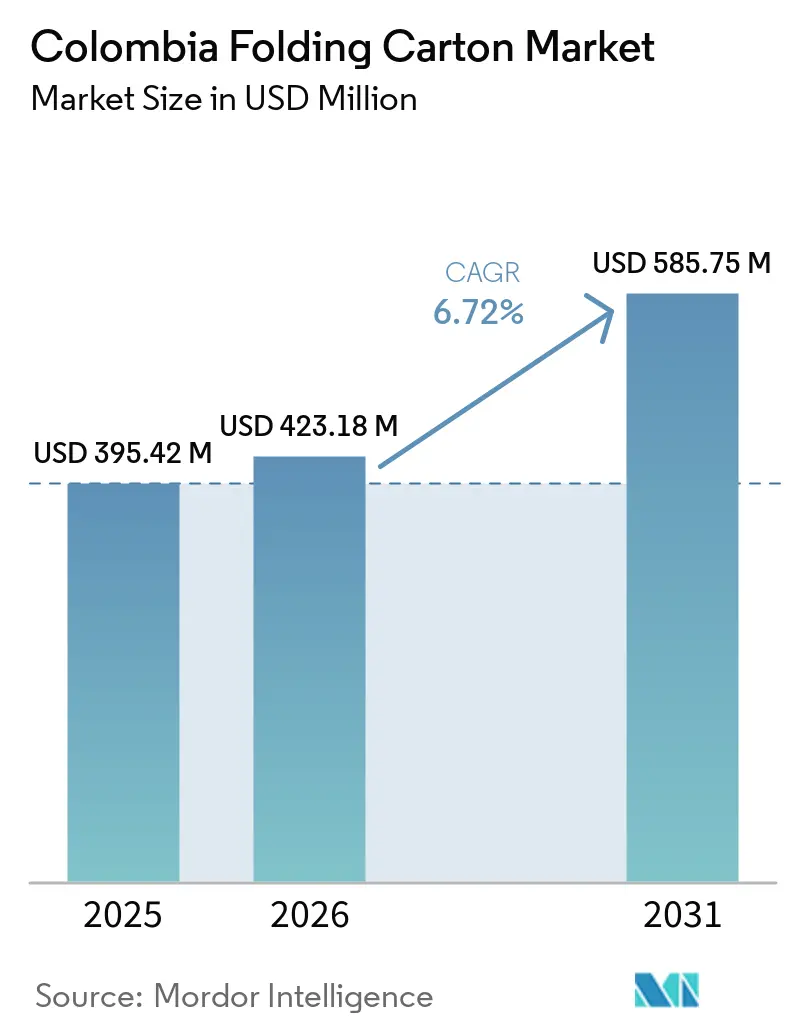

| Base Year Market Size (2025) | USD 395.42 Million |

| Market Size (2026) | USD 423.18 Million |

| Market Size (2031) | USD 585.75 Million |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

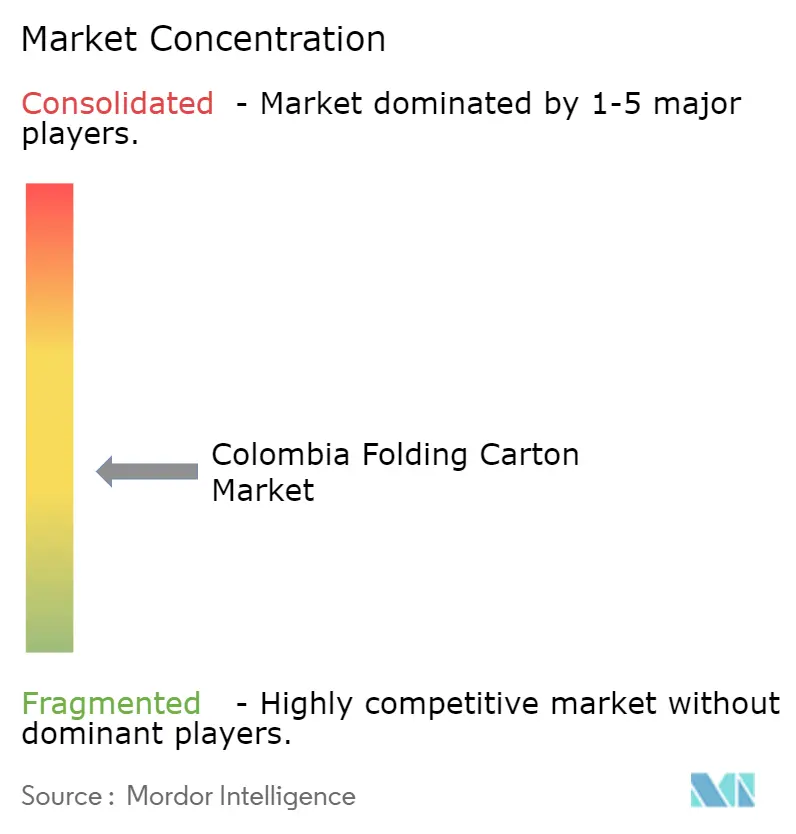

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Folding Carton Market Analysis by Mordor Intelligence

The Colombia Folding Carton Market size is expected to increase from USD 395.42 million in 2025 to USD 423.18 million in 2026 and reach USD 585.75 million by 2031, growing at a CAGR of 6.72% over 2026-2031. Demand is accelerating as single-use-plastic restrictions tighten, nearshoring shifts multinational production lines to the Andean corridor, and brand owners search for fiber-based formats that balance sustainability with shelf impact. Converter profitability nevertheless remains tethered to imported virgin pulp prices, which compressed margins by up to 220 basis points during the 2024 commodity spike, before a partial rebound late in 2025. Supply-chain resilience is another theme, with Buenaventura port congestion in 2026 reinforcing the value of regional cartonboard sourcing contracts. Technology adoption rounds out the outlook: digital presses, barrier coatings, and short-run automation are becoming decisive differentiators as order sizes fragment and lead-time expectations shrink.

Key Report Takeaways

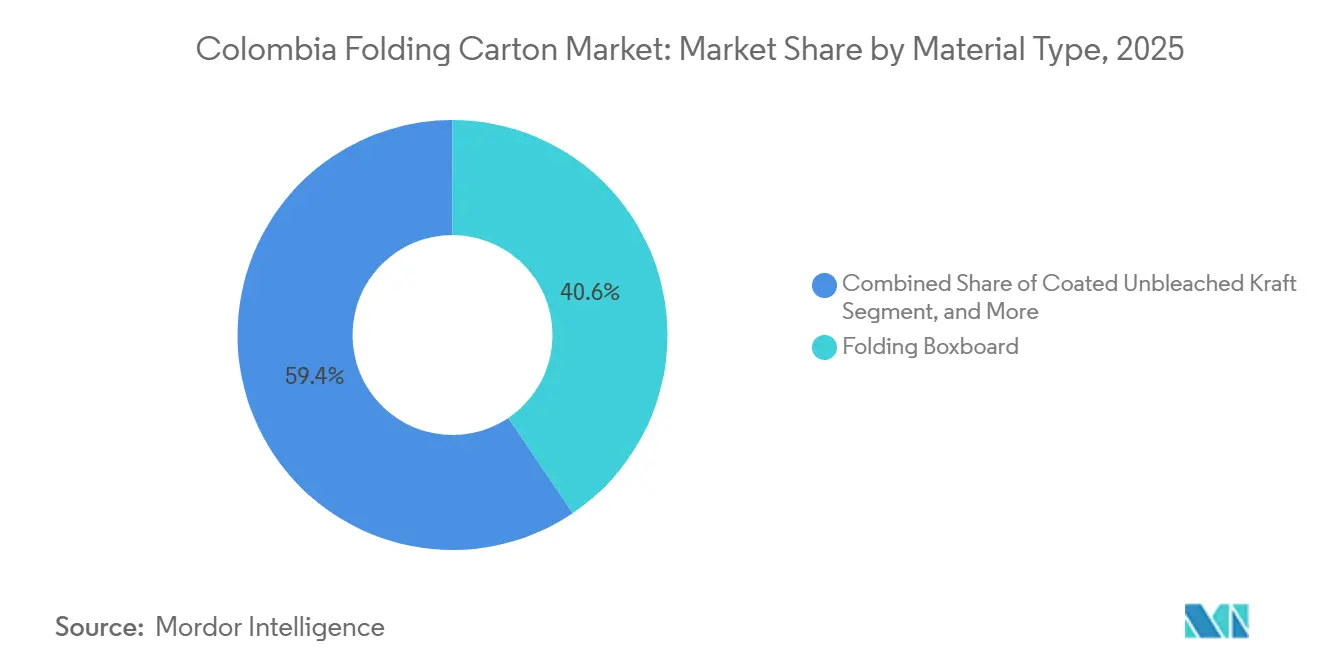

- By material type, folding boxboard captured with 40.56% of the Colombia folding carton market share in 2025.

- By printing technology, the Colombia folding carton market size for digital printing is projected to grow at a 9.12% CAGR to 2031.

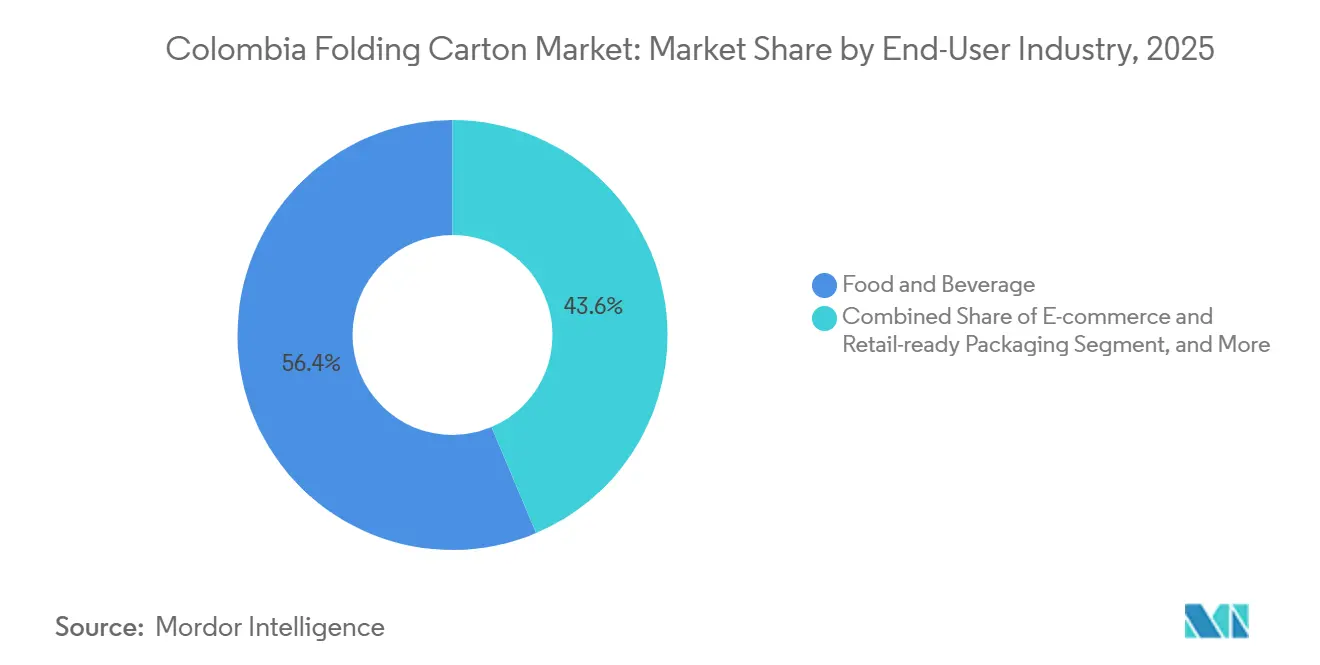

- By end-user industry, the food and beverage industry captured 56.37% of the Colombia folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Packaging Solutions | +1.8% | National, early adoption in Bogotá, Medellín, Cali | Medium term (2-4 years) |

| Expansion of the Food and Beverage Processing Industry | +1.5% | National, concentrated in Valle del Cauca, Antioquia, and Cundinamarca | Long term (≥ 4 years) |

| Rising Adoption of E-commerce and Retail-Ready Packaging | +1.3% | National, spill-over to cross-border fulfillment hubs | Short term (≤ 2 years) |

| Government Initiatives on Plastic Reduction | +1.1% | National Ministry of Environment and Sustainable Development | Medium term (2-4 years) |

| Surge in Nearshoring of Consumer Goods Manufacturing to Colombia | +0.9% | Free Trade Zones in Barranquilla, Cartagena, Bogotá, Medellín | Long term (≥ 4 years) |

| Shift Toward Premiumization of Craft Spirits Requiring High-Quality Folding Cartons | +0.6% | National, export-oriented production in Caldas, Quindío | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging Solutions

Law 2232’s first enforcement phase in 2024 outlawed several single-use plastics, and, paired with the IPUSUI tax in 2025, which lifted the landed cost of polyolefin films by up to 12%, tilted brand economics toward recyclable paperboard. Nestlé’s USD 100 million upgrade earmarked funds for converting chocolate bars to sleeve-type cartons, reinforcing corporate support for fiber formats. Consumer surveys show willingness to pay a 5-8% premium for recyclable cartons, sustaining demand after the initial compliance push.[1]Federación Nacional de Comerciantes, “Encuesta Preferencias de Empaque Sostenible 2025,” fenalco.com.co As enforcement phases proceed, converters with FSC or PEFC certification gain preferential access to government and multinational tenders, locking in multi-year volumes. Together, legislation, taxation, and consumer sentiment underpin a structural tilt toward cartons across household staples.

Expansion of Food and Beverage Processing Industry

Bavaria’s investment in canning and Lactalis’s additions to its aseptic dairy line in 2024-2025 translated into larger multipack and portion-control carton runs, pushing up demand in Valle del Cauca and Cundinamarca. Value-added coffee exports rose 14% year-over-year in Q1 2025, and most premium roasters shifted to valve-equipped cartons that preserve aroma while signaling origin authenticity. Export-driven processors must satisfy European retail criteria for certified fiber, prompting converters to formalize chain-of-custody systems. These higher technical standards spill over domestically, raising the baseline for color fidelity and barrier performance. As Colombia reinforces its role as a net food exporter, carton volumes remain tightly coupled to processing capacity expansion.

Rising Adoption of E-Commerce and Retail-Ready Packaging

Digital transaction volume reached 272 million in H1 2025, a 26.7% jump that is pushing brands toward formats that move seamlessly from shipper to shelf. Retail-ready designs marry corrugated outers and folding-carton inserts, eliminating case-cutting labor and lowering in-store restocking costs by up to 40%. These shorter product life cycles and localized promotions favor digital presses, where Colombian converters now deliver sub-1-week lead times on 500-unit runs. Converters able to automate CAD-to-press workflows capture higher margins despite premium ink costs, because brands prize agility over unit price. As e-commerce share climbs, shelf-ready hybrid cartons are becoming a default specification for household and personal-care goods.

Government Initiatives on Plastic Reduction

Resolution 1407 in 2024 introduced a 30% recycled-content target by 2030 and a tiered eco-fee that penalizes non-recyclable substrates, widening the cost gap between mono-material cartons and multi-layer flexible films. Government procurement rules also now favor recyclable packaging, shifting 12% of public-sector pharmaceutical bids to blister-card cartons in 2025. Because paperboard recycling rates already surpass 60%, brand owners find compliance less capital-intensive than retrofitting pouch lines. The regulatory path likewise encourages investment in aqueous barrier and dispersion-coated grades: converters that install these modules unlock pharmaceuticals and fresh-food niches with durable demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Pulp Prices | -1.2% | National, all converters importing pulp | Short term (≤ 2 years) |

| Competition for Flexible Plastic Pouches | -0.9% | National, snack foods, pet treats, dry goods | Medium term (2-4 years) |

| Logistics Bottlenecks at Port Terminals Affecting Cartonboard Imports | -0.7% | Buenaventura, Cartagena, Barranquilla | Short term (≤ 2 years) |

| Limited Availability of High-Barrier Coatings for Local Converters | -0.5% | National, pharmaceutical, and fresh-food segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Pulp Prices

Bleached-hardwood kraft pulp oscillated between USD 450 and USD 800 per ton from 2024-2025, a swing amplified by Colombia’s total reliance on imports and absence of hedging facilities for mid-tier converters. Suzano’s announced USD 15-per-ton hike for January 2026 will shave another 40-60 basis points off converter margins unless brand contracts allow automatic pass-through. Capital-budget freezes triggered by pulp uncertainty also delay barrier-coating investments that could diversify revenue into higher-margin pharmaceutical work. Price visibility, therefore, remains a gating factor for both profitability and technology adoption in the Colombian folding carton market.

Competition from Flexible Plastic Pouches

Mono-material polyethylene pouches now deliver recyclable solutions with moisture-barrier performance that once required multi-layer structures, eroding paperboard’s hold on snack and dry-food categories. Compared with form-fill-seal lines, carton erectors run at roughly half the speed and carry 40-50% higher capital cost, giving plastic a unit-cost edge. However, breakthroughs in cellulose nanofiber coatings and dispersion barriers are starting to narrow the oxygen-transmission gap, allowing cartons to regain premium segments that value consumer experience and shelf presence. The pace at which converters commercialize these coatings will determine whether cartons can reclaim share or cede further volume to pouches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Substrates Accelerate Expansion

White line chipboard’s 8.26% CAGR makes it the fastest-growing substrate in the Colombia folding carton market as e-commerce shippers and tobacco cartons emphasize cost and recycled content. Folding boxboard retained 40.56% of 2025 revenue, underscoring its indispensability for pharmaceutical blister cards and high-end cosmetics where brightness and stiffness drive shelf impact. Solid bleached sulfate, while premium-priced, secures food-contact niches that require FDA and INVIMA compliance, especially for frozen desserts and dairy wraps.[2]Instituto Nacional de Vigilancia de Medicamentos y Alimentos, “Serialization Guidance 2024,” invima.gov.co

The recycled pivot is structural rather than cyclical: recycled substrates held 34% of demand by 2025, up from 28% in 2020, aided by extended producer responsibility fees. Klabin’s Piracicaba II mill, inaugurated in 2025, now offers barrier-grade kraftliner that reaches Colombian converters in 10-15 days versus 35-45 days for European shipments, lowering freight by USD 100 per ton. The new regional option supports just-in-time inventories, freeing working capital for converters keen to upgrade die-cutting capacity.

By Printing Technology: Digital Penetration Quickens

Lithographic presses still accounted for 51.79% of technology revenue in 2025 because they deliver metallic inks, embossing effects, and Pantone fidelity demanded by premium spirits and personal-care brands. Yet digital printing, set to grow at 9.12% through 2031, captures pharmaceutical serialization and craft-beverage limited runs where 500-unit orders cannot amortize offset plate costs. Gross margins on digital work reach 32%, enabling converters to recover the hardware payback within 24-30 months.

Flexography bridges the mid-tier, serving dry-food cartons at lower plate costs, while gravure remains viable only for ultra-long tobacco runs. Adoption of 7-color extended-gamut flexo on new Bobst lines narrows the perceived quality gap with offset, allowing converters like Smurfit WestRock’s Guarne plant to compete for premium SKUs without offset-length make-ready times. The technology mix is thus diversifying in lockstep with SKU proliferation.

By End-User Industry: E-Commerce Redefines Specifications

Food and beverage end-users contributed 56.37% of 2025 revenue, underpinned by roasted-coffee and craft-beer multipacks that rely on carton rigidity to protect glass and maintain brand aesthetics. However, e-commerce and retail-ready formats are the fastest climbers at an 8.64% CAGR, reshaping pharmaceutical and personal-care packaging toward frustration-free designs that collapse flat for recycling. INVIMA’s serialization mandate, in effect since 2024, requires variable-data codes on every prescription unit, pushing converters toward digital printers that sync with line-level traceability systems.

Personal-care brands, meanwhile, pay premiums for soft-touch and holographic finishes that reflect premiumization in domestic and export channels. Tobacco volume may stagnate, but holographic foils and tactile varnishes keep per-unit value high. Electrical and electronics packaging, a smaller slice, demands anti-static coatings and cushioned inserts, offering an opportunity to converters that master multi-step assembly cells.

Geography Analysis

Bogotá, Medellín, and Cali form a manufacturing triangle that generated 68% of folding-carton consumption in 2025. Cundinamarca’s pharmaceutical cluster alone accounted for 22% of national volume, supplying blister cards to Ecuador and Peru under Andean Community trade accords. Antioquia’s textile and personal-care operations lifted regional carton demand 7.8% in 2025 as detergent and shampoo lines shifted from pouches to rigid formats. Valle del Cauca’s food-processing belt leaned on Buenaventura port for cartonboard imports, despite the February 2026 congestion that stretched dwell times to 18 days.

Caribbean Free Trade Zones in Barranquilla and Cartagena attracted USD 1.2 billion of FDI during 2024-2025, much of it aimed at nearshoring consumer-goods plants that follow global packaging standards.[3]Ministerio de Comercio, Industria y Turismo, “Inversión Extranjera en Zonas Francas 2025,” mincit.gov.co Local converters upgraded die-cutting accuracy to secure these contracts, shortening export lead times to the United States by two weeks. Cross-border carton exports to Ecuador and Venezuela climbed 14% in 2025, reinforcing Colombia’s regional packaging hub status.

Infrastructure constraints temper the upside. Inland trucking from Buenaventura to Bogotá costs twice as much as the Brazilian or Mexican equivalent due to poor road conditions and limited carrier competition. The government’s USD 800 million port-expansion project will not finish before 2029, so converters continue to hold buffer stock, tying up working capital. Smarter sourcing contracts and regional mill relationships thus remain critical countermeasures for market participants.

Competitive Landscape

The Colombia folding carton market partitions into an integrated paperboard tier and a fragmented converter tier of more than 40 players. Smurfit WestRock’s three local mills supply 524,000 tons per year yet prioritize corrugated boxes, leaving folding-boxboard import gaps that mid-tier converters fill via European and Brazilian suppliers. MM Packaging Colombia’s 2024 acquisition of Plegacol created a EUR 30 million (USD 32 million) platform with 16,000 tons of conversion capacity, signaling a roll-up strategy aimed at service-level differentiation.[4]MM Packaging, “Plegacol Acquisition 2024,” mmpackaging.com

Papelsa lifted its Yumbo plant to 117,000 tons in 2025 and added cogeneration to slash electricity outlays 30%, allowing sharper price-to-service ratios against import-heavy rivals. Converters embracing inkjet lines report backlogs despite 20% price premiums, proof that speed and SKU flexibility outweigh cost in many bids. Barrier-coating scarcity remains the steepest entry barrier: equipment costs of USD 2-3 million stretch the balance sheets of independent shops, but those that crack pharmaceutical oxygen-barrier specs consistently command double-digit margins.

Certification gaps also shape competition. Only 35% of installed folding-carton capacity holds FSC or PEFC credentials, yet export-oriented brands make such papers non-negotiable. Shops with documented chain-of-custody status routinely win North American private-label contracts, leaving uncertified peers vulnerable to domestic price wars. The next battleground will likely be compostable windows and water-based adhesives, areas where very few Colombian lines currently possess turnkey capability.

Colombia Folding Carton Industry Leaders

Smurfit WestRock plc

Amcor plc

Klabin S.A.

Cartones América S.A.

MM Packaging Colombia S.A.S.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Suzano confirmed a USD 15-per-ton pulp price increase effective immediately, citing fiber scarcity and higher energy costs.

- February 2026: Buenaventura port congestion extended container dwell times to 12-18 days, forcing pharmaceutical importers to air-freight emergency cartonboard at 4-5× ocean rates.

- July 2025: IPUSUI tax declarations on single-use plastic imports took effect, pushing polyolefin film costs up 8-12%.

- March 2025: Klabin inaugurated the Piracicaba II mill in Brazil following a BRL 1.56 billion (USD 312 million) investment, adding 240,000 tons of barrier-grade paperboard capacity.

Colombia Folding Carton Market Report Scope

The folding carton market refers to the industry that produces, distributes, and uses paperboard-based packaging solutions, primarily for consumer goods, food and beverages, pharmaceuticals, and other sectors. This report provides an in-depth analysis of the Colombia folding carton market, covering key trends, growth drivers, challenges, and opportunities.

The Colombia Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the market size value of the Colombia folding carton market?

The Colombia Folding Carton Market size is expected to increase from USD 395.42 million in 2025 to USD 423.18 million in 2026 and reach USD 585.75 million by 2031, growing at a CAGR of 6.72% over 2026-2031.

Which material leads revenue share in Colombian folding cartons?

Folding boxboard led with 40.56% revenue share in 2025, reflecting its dominance in pharmaceutical blister cards and cosmetics cartons.

Why are digital presses gaining traction among Colombian converters?

Digital printing supports short-run jobs, pharmaceutical serialization, and rapid product launches, yielding margins of 28-32% and growing at a 9.12% CAGR through 2031.

How are government policies shaping packaging choices?

Law 2232’s plastic bans and the IPUSUI tax raise the cost of plastic and push brands toward recyclable cartons, while Resolution 1407 adds a 30% recycled-content mandate for packaging.

Which geographic regions consume the most folding cartons in Colombia?

Bogotá-Medellín-Cali’s industrial corridor represents 68% of demand, with Cundinamarca’s pharmaceutical hub alone taking 22% of national volume.

What is the main risk facing Colombian folding-carton converters?

Volatile imported pulp prices, driven by supply constraints and currency swings, can compress converter margins by 40-60 basis points per USD 15-per-ton price change.

Page last updated on: