China Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

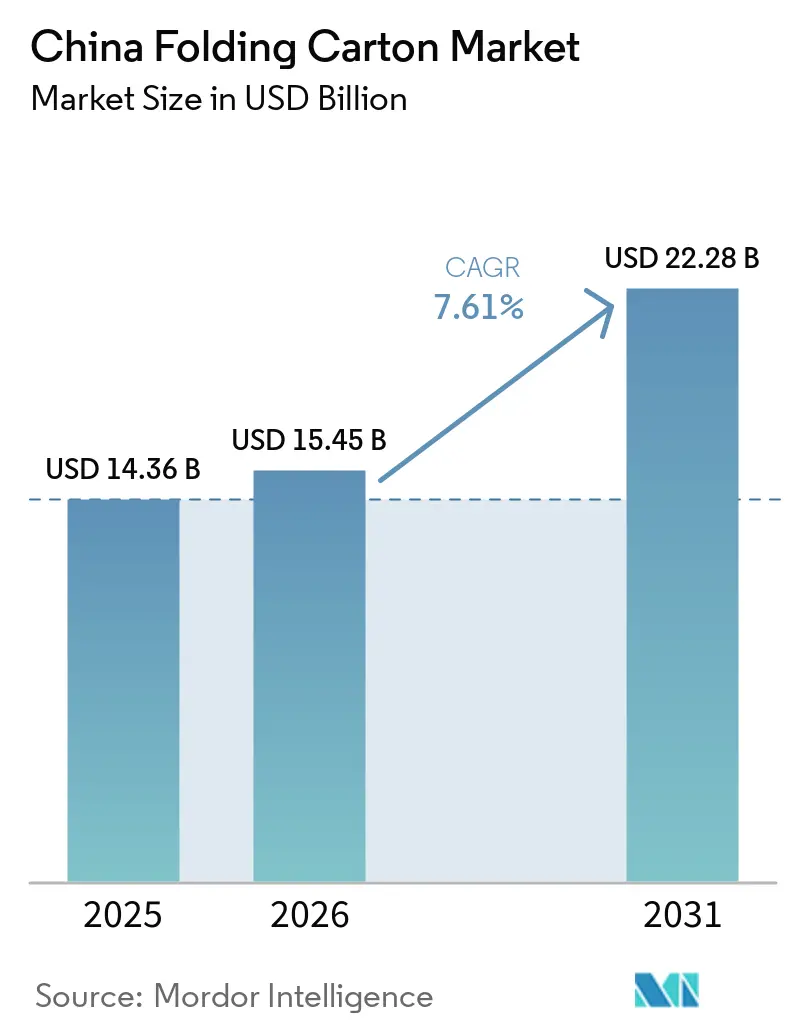

| Base Year Market Size (2025) | USD 14.36 Billion |

| Market Size (2026) | USD 15.45 Billion |

| Market Size (2031) | USD 22.28 Billion |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

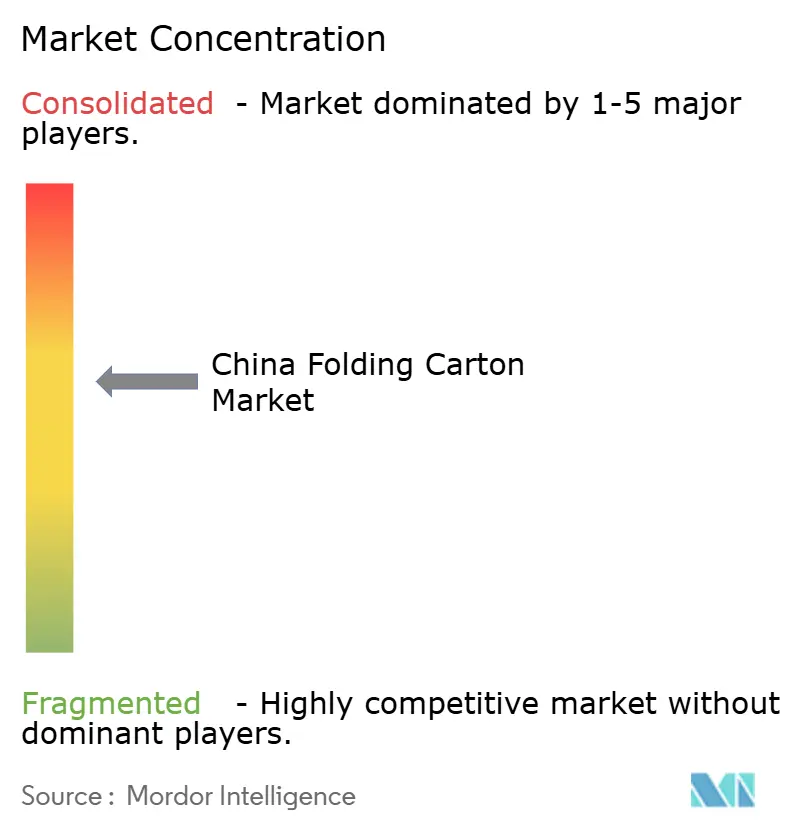

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Folding Carton Market Analysis by Mordor Intelligence

The China folding carton market size is expected to be USD 14.36 billion in 2025, USD 15.45 billion in 2026, and reach USD 22.28 billion by 2031, growing at a CAGR of 7.61% from 2026 to 2031. Multiple forces are reshaping demand, including e-commerce logistics that reward right-sized fiber boxes, government pressure to substitute single-use plastics, and premiumization in cosmetics, personal care, and ready-to-eat foods. Domestic integrated mills are adding virgin-fiber lines to comply with GB 4806 food-contact limits, while converters accelerate automation and digital printing to profit from shorter runs and seasonal campaigns. At the same time, pulp price deflation offers short-term relief on input costs but squeezes upstream mill margins, hinting at further consolidation across the China folding carton market.

Key Report Takeaways

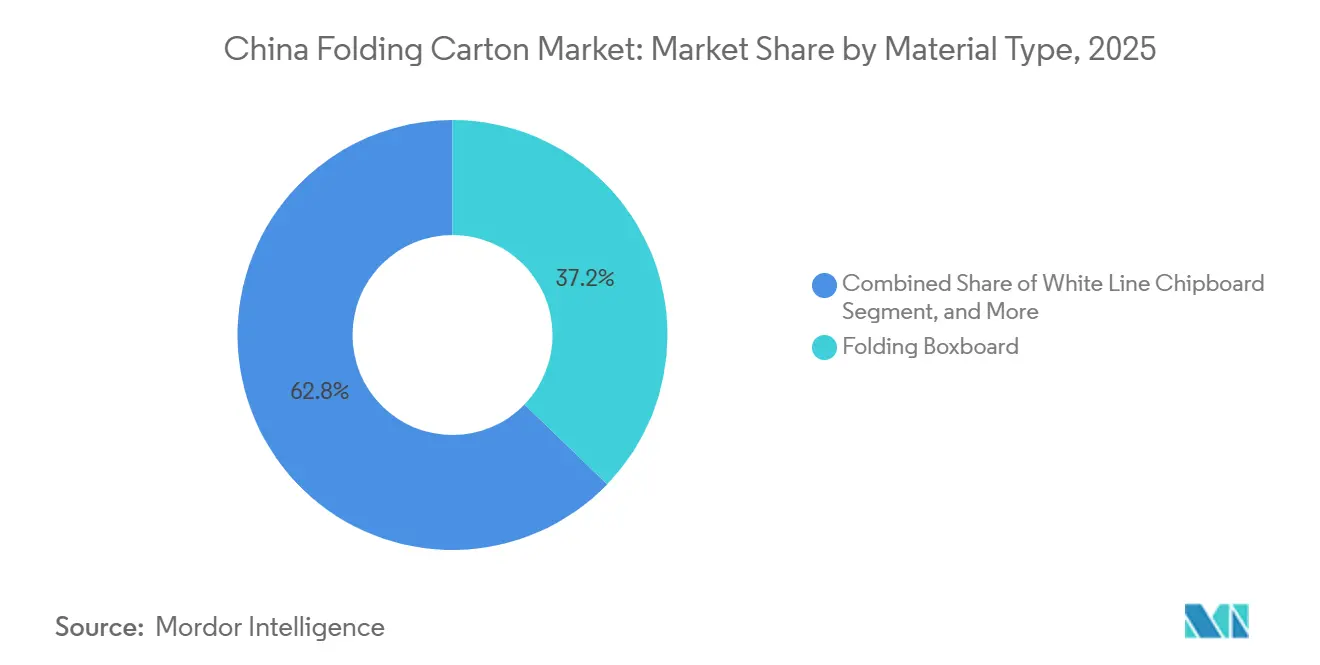

- By material type, folding boxboard captured 37.21% of the China folding carton market share in 2025.

- By printing technology, the China folding carton market size for the digital printing segment is forecast to advance at a 9.15% CAGR through 2031.

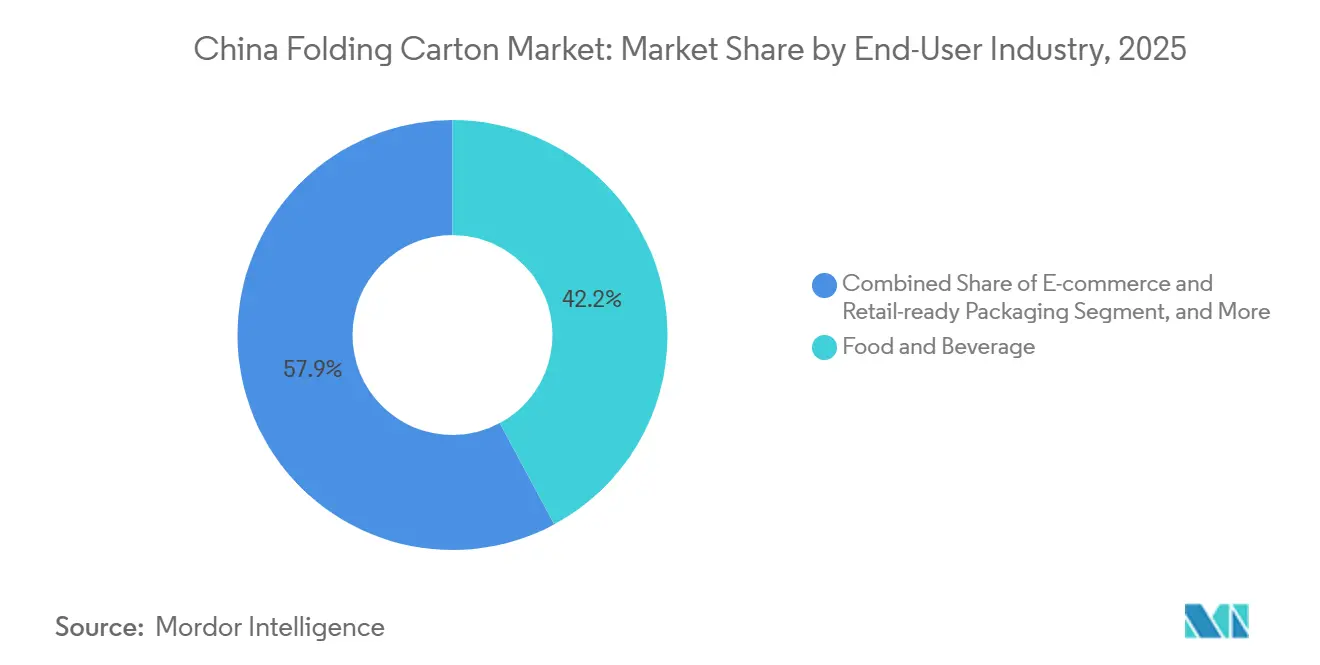

- By end-user industry, food and beverage captured 42.15% of the China folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Recyclable Fiber-Based Packaging | +2.0% | National, Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| E-Commerce Acceleration Driving Small-Run Carton Volumes | +1.8% | Yangtze River Delta, Pearl River Delta, Beijing-Tianjin-Hebei | Short term (≤ 2 years) |

| Rising Premiumization in Cosmetics and Personal Care | +1.3% | Shanghai, Beijing, Guangzhou, Shenzhen, Chengdu | Medium term (2-4 years) |

| Government Plastic-Reduction Mandates Boosting Paperboard | +1.6% | National, pilot enforcement in provincial capitals | Long term (≥ 4 years) |

| Automation Investments Lowering Conversion Costs | +1.0% | Guangdong, Zhejiang, Jiangsu, Shandong | Medium term (2-4 years) |

| Digital Printing Adoption Enabling Mass Personalization | +1.2% | National, early adoption in cosmetics and electronics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Recyclable Fiber-Based Packaging

Parcel volumes surpassed 120 billion in 2025, and the express delivery packaging green transition plan now requires 95% of materials to be recyclable, steering shippers toward folding carton.[1]National Development and Reform Commission, “Express Delivery Packaging Green Transition Plan,” GOV.CN Brands embrace Kraft aesthetics that cut ink coverage and simplify recycling, while integrated mills such as Nine Dragons expanded bleached boxboard capacity to 1.2 million t per year to secure a certified supply. Pilot reuse programs exist, yet hygiene and reverse-logistics hurdles keep single-use carton dominant.

E-Commerce Acceleration Driving Small-Run Carton Volumes

China's folding carton market orders placed through online channels reached an estimated 55% share in 2025, driven by flash sales and influencer-driven SKUs. Digital presses from HP Indigo and EFI enable profitable runs of 500 units with 97% PANTONE accuracy and embedded QR codes.[2]HP Inc., “HP Indigo Digital Printing Solutions for Corrugated and Folding Carton,” HP.COM Electronics brands in Shenzhen demand anti-static liners and custom die-cuts, pushing converters to invest in inline coating that integrates with digital workflows to achieve seven-day lead times.

Rising Premiumization in Cosmetics and Personal Care

High-end beauty carton exceeded CNY 8 billion (USD 1.15 billion) in 2025, expanding nearly 15% annually as domestic prestige labels mimic luxury houses with embossing and soft-touch varnishes. Solid Bleached Sulfate in the 250-350 gsm range provides stiffness and bright whiteness that meet GB 4806 migration limits.[3]Standardization Administration of China, “GB 4806.8-2022 National Food Safety Standard - Food Contact Materials and Articles - Paper and Board,” GB688.CN Nanocellulose-reinforced boards now under pilot raise tensile strength 40% and allow thinner gauges, reducing freight weight without sacrificing the unboxing experience.

Government Plastic-Reduction Mandates Boosting Paperboard

National bans on non-degradable plastics in food service have created an estimated 1.5 million tons of incremental demand for paperboard since 2025.[4]Ministry of Ecology and Environment, “Opinions on Further Strengthening Plastic Pollution Control,” MEE.GOV.CN Quick-service restaurant chains are increasingly specifying folding carton with food-grade barrier coatings to meet both safety and sustainability requirements. In response, Sun Paper has commissioned a 600,000-ton-per-year chemical pulp line to supply virgin fibers certified for low microbial content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Pulp and Energy Prices | -0.9% | Coastal mills reliant on imported pulp | Short term (≤ 2 years) |

| Competition from Flexible Plastic Packaging | -0.7% | Snack foods, confectionery, dry goods | Medium term (2-4 years) |

| Supply Gluts from Rapid Mill Capacity Expansions | -0.5% | Guangdong, Shandong, Zhejiang, Guangxi | Medium term (2-4 years) |

| Stringent Food-Contact Compliance Costs | -0.3% | Small and mid-sized converters nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Pulp and Energy Prices

Softwood pulp fell 11.98% in 2025 to CNY 5,633 (USD 790) per tonne and is forecast to dip another 8.81% in 2026. Converters welcome cheaper inputs, but integrated mills such as Shandong Bohui financed sizable pulp expansions that now face compressed returns. Energy can represent 70% of drying costs in papermaking, and fluctuating natural gas tariffs in coastal provinces further destabilize margins

Competition from Flexible Plastic Packaging

Laminated pouches retain superior barrier properties and lower freight weights, especially for snack foods. Baishen Pack offers digitally printed film with 10-day delivery and a 500-unit minimum, matching carton converters in terms of agility. Barrier-paper innovations from Mondi, achieving oxygen transmission below 0.5 cc/m²-day threaten to encroach on small sachet and stick-pack niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Expand on Sustainability Pull

Folding Boxboard captured 37.21% of the Chinese folding carton market share in 2025, supported by its smooth surface and consistent stiffness, which enable high-speed folder-gluers for snack, dairy, and pharmaceutical packaging. The segment benefits from integrated mills adding virgin fiber lines that ensure compliance with GB 4806 limits on heavy-metal migration. Coated Unbleached Kraft is forecast to outgrow the China folding carton market size at an 8.23% CAGR, propelled by organic food and craft beverage labels that showcase natural brown tones as an authenticity cue. Solid Bleached Sulfate remains the substrate of choice for prestige cosmetics where bright whiteness, embossability, and foil adhesion justify premium pricing, yet constrained hardwood pulp supply limits share gains. White Line Chipboard fills value tiers for detergents and dry goods, though its recycled content caps print fidelity and moisture resistance, limiting uptake in frozen and chilled foods.

Rising investor interest in virgin-fiber capacity is evident in Nine Dragons’ Dongguan upgrade, which will replace two legacy machines with a 620,000 tonne-per-year kraft liner line, signaling a pivot toward food-safe grades. Specialty boards fortified with nanocellulose are emerging, with pilot trials documenting 15% weight reductions that can lower logistics costs for multichannel e-commerce distribution. Mills that embed in-house labs to verify GB 4806 compliance increasingly partner with global brand owners that demand transparent sourcing, giving scaled producers a margin edge over spot-market traders in the China folding carton market.

By Printing Technology: Digital Inkjet Gains Personalization Premium

Lithography held 55.01% of 2025 volumes in the China folding carton market thanks to its cost efficiency on runs of 10,000 sheets or more and its compatibility with inline coating and die-cutting. However, digital presses are growing at 9.15% CAGR, capitalizing on cosmetics launches and influencer marketing that demand variable graphics, serial numbers, and region-specific languages. Digital setups slash make-ready time from 45 minutes to 18 minutes and cut scrap rates to 2%, letting converters profitably fulfill seven-day turnaround promises. Flexography serves mid-range household cleaner jobs, where graphics complexity is modest and water-based inks help meet VOC caps in Guangdong.

Gravure clings to tobacco and premium confectionery carton whose multi-million-unit runs amortize cylinder costs, yet its share erodes as hybrid litho-digital workflows approach gravure quality without long plate cycles. Ink prices for digital remain two to three times higher than litho, so converters often co-locate both technologies, routing long SKUs to litho and short SKUs plus late-stage localization to digital. Chinese converters installing HP Indigo 35K and EFI Nozomi lines report 30% higher utilization than in 2024, a step change that underscores the strategic role of digital in the China folding carton industry.

By End-User Industry: E-Commerce Reshapes Demand Mix

Food and beverage applications dominated with 42.15% of consumption in 2025, relying on grease-resistant coatings and consistent caliper for automated filling at 500 packs per minute. E-commerce and retail-ready formats are projected to expand at an 8.94% CAGR, underpinned by China’s rapid grocery delivery and live-stream flash sales that require compact carton shaped to product geometry. GB/T 45453-2025 now requires tamper-evidence on pharmaceutical packs, prompting converters to integrate tear strips and authentication labels validated by the National Medical Products Administration. Luxury cosmetics adopt rigid book-style carton with magnetic closures and tactile coatings that convey prestige in digital unboxing videos, supporting above-average price points within the China folding carton market.

Electronics brands specify anti-static liners and desiccant inserts inside folding carton for smartphones and drones, driving demand for multi-ply boards that balance cushioning with slim profiles suitable for parcel lockers. Household and industrial goods lean on recycled White Line Chipboard, where price takes precedence, while niche segments like craft beer favor Coated Unbleached Kraft sleeves that match artisanal branding. Collectively, these end-uses reinforce the diversification of the China folding carton market.

Geography Analysis

The eastern coastal provinces anchor production and consumption, with Guangdong, Zhejiang, and Jiangsu hosting clusters of converters that serve export-oriented electronics and cosmetics brands. The Yangtze River Delta accounts for over one-third of China's folding carton market, aided by dense courier networks that enable next-day delivery across megacities. Tier-1 cities attract premium orders for luxury cosmetics and limited-edition tech gadgets, supporting higher margins on Solid Bleached Sulfate grades.

Northern regions, such as Beijing-Tianjin-Hebei, are seeing rapid adoption of digital printing as micro-brands leverage social commerce to reach affluent consumers. The local share of China's folding carton market is also buoyed by pharmaceutical production in Hebei and Shandong, which demands tamper-evident carton that meet GB/T 45453-2025. Shandong’s coastal mills, however, feel pulp price swings acutely because they import long-fiber softwood, prompting vertical integration projects like Bohui Paper’s pulp line expansion.

Southwestern hubs, notably Chengdu and Chongqing, are emerging e-commerce fulfillment centers connecting to national express corridors. Converters here invest in mid-speed digital presses and modular folder-gluer systems that accommodate smaller lot sizes common to growing specialty food exports. Guangxi’s Guangxi Ping Qiaoyu and Valmet-supplied lines add 1.1 million t of testliner that will flow into regional corrugated and folding carton plants, mitigating freight costs associated with shipping board from the coast.

Competitive Landscape

Competition in China's folding carton market is moderate, with the five largest integrated suppliers accounting for roughly 35-40% of capacity. Nine Dragons Paper, Lee and Man Paper, and Sun Paper leverage captive pulp and energy to shield margins from raw-material swings, while simultaneously upgrading board machines for premium grades. Their scale facilitates investment in GB 4806 labs and traceable supply chains, qualities prized by multinational food and pharmaceutical clients.

Foreign groups, including Graphic Packaging and Huhtamaki, focus on niches that require flawless food-contact compliance and advanced finishing such as metallization and soft-touch coatings. These players import design expertise and deliver uniform quality across regions, enabling them to command higher price points. Mid-sized independents counter by adopting automation: retrofitted folder-glue systems lift throughput by 30% and pay back within 18 months, allowing faster lead times that appeal to e-commerce brands.

Emerging challengers blur rigid and flexible boundaries. Baishen Pack markets barrier paper laminates certified for curbside recycling, yet rival multilayer films outperform them in oxygen and moisture resistance, threatening Baishen Pack's share in coffee stick and snack bar sleeves. Consolidation is likely as mills seeking downstream integration acquire regional converters to secure carton outlets, while converters without captive board supply face margin squeeze amid capacity additions in 2026.

China Folding Carton Industry Leaders

Nine Dragons Paper Holdings Limited

Lee & Man Paper Manufacturing Limited

Shandong Sun Paper Industry Joint Stock Co., Ltd.

Shandong Bohui Paper Industry Co., Ltd.

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mondi closed three European converting plants and reported underlying EBITDA of EUR 212 million (USD 239 million), noting that Q1 pricing actions will flow through by Q3 2026.

- March 2026: Rengo’s Tri-Wall subsidiary started up Fengyuan Tri-Wall Packaging (Shandong) with a heavy-duty corrugator, expanding its northern China footprint.

- March 2026: Dongfang Precision agreed to sell corrugated line businesses to Brookfield-controlled entities for EUR 811 million (USD 916 million), sharpening its focus on water-jet propulsion equipment.

- February 2026: Yutong Technology acquired 60% of Gelbert Eco Print for EUR 6.54 million (USD 7.39 million) to establish a European beachhead serving global customers.

China Folding Carton Market Report Scope

The China folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The China Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-Commerce and Retail-Ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-Commerce and Retail-Ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current China folding carton market size and its projected value by 2031?

The market is valued at USD 15.45 billion in 2026 and is forecast to reach USD 22.28 billion by 2031, growing at a 7.61% CAGR between 2026 and 2031.

Which material type leads demand within China's folding carton?

Folding Boxboard led with 37.21% share in 2025, thanks to its smooth finish and high conversion speeds.

Why is digital printing gaining traction among Chinese carton converters?

Digital presses cut make-ready times by 60%, enable runs as low as 500 units, support variable data, and match up to 97% PANTONE colors, making them ideal for e-commerce promotions and cosmetics launches.

How are government plastic-reduction mandates affecting packaging choices?

National bans on non-degradable plastics in food service are shifting quick-service restaurants and grocery delivery platforms toward paperboard carton that comply with GB 4806 migration limits.

Which end-user segment is growing fastest in China's folding carton landscape?

E-commerce and retail-ready packaging is growing at an 8.94% CAGR as parcel volumes top 120 billion annually and brands demand right-sized, recyclable carton.

What risks could slow growth in the China folding carton industry?

Volatile pulp and energy prices, competition from flexible plastic pouches, and compliance costs tied to food-contact and pharmaceutical standards can limit profitability for converters and mills.

Page last updated on: