Peru Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

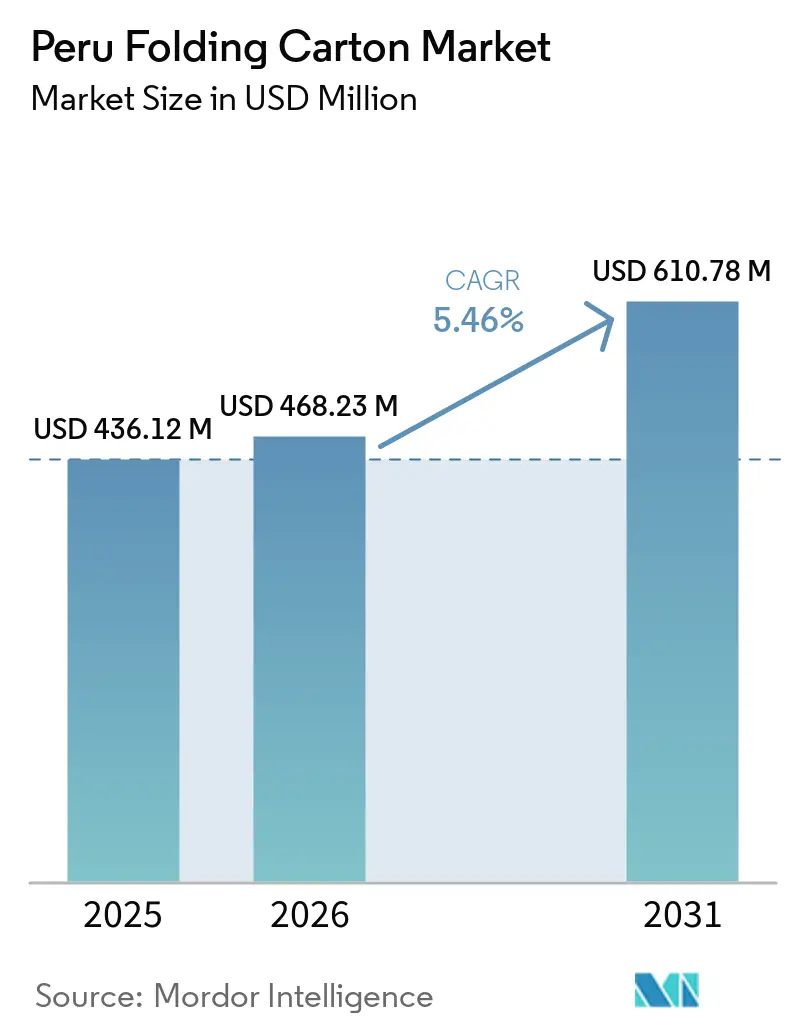

| Base Year Market Size (2025) | USD 436.12 Million |

| Market Size (2026) | USD 468.23 Million |

| Market Size (2031) | USD 610.78 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

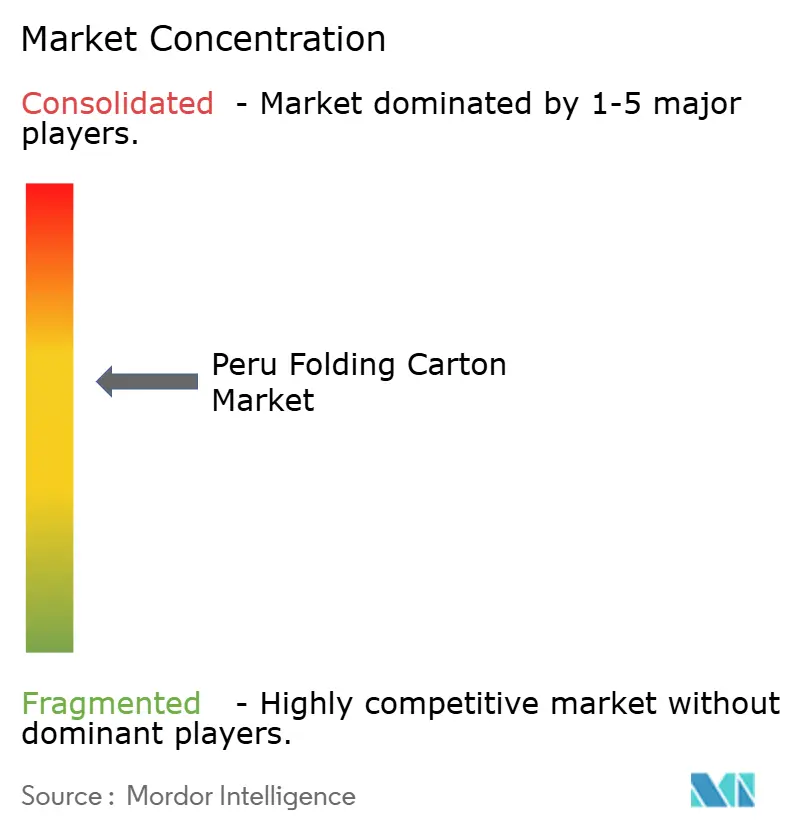

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Folding Carton Market Analysis by Mordor Intelligence

The Peru folding carton market size is projected to expand from USD 436.12 million in 2025 and USD 468.23 million in 2026 to USD 610.78 million by 2031, registering a CAGR of 5.46% between 2026 to 2031. Sustained export growth for blueberries, avocados, and table grapes keeps large runs of ventilated microflute cartons moving through ports, while rising urban income stimulates demand for premium cosmetics and pharmaceuticals packaged in high-graphics cartons. Government circular-economy mandates are accelerating the shift to recycled-core substrates and pushing converters toward low-carbon operations, even as e-commerce is driving the need for lightweight, tamper-evident formats that protect products during last-mile delivery. Converters able to certify recycled content, provide lifecycle data, and offer short-run digital printing are capturing share from slower rivals. Input-cost volatility in virgin pulp and persistent congestion at Callao port continue to test margin resilience across the Peru folding carton market.

Key Report Takeaways

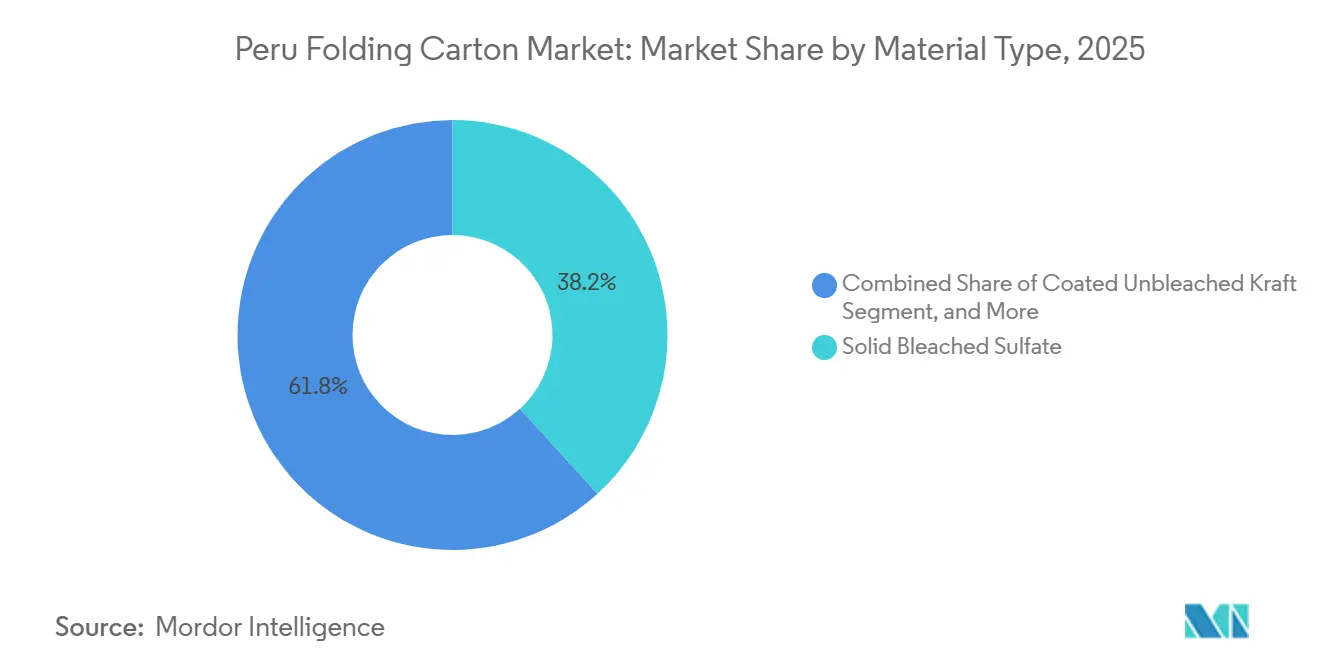

- By material type, solid bleached sulfate captured with 38.21% of the Peru folding carton market share in 2025.

- By printing technology, the Peru folding carton market size for digital printing is projected to grow at a 6.82% CAGR to 2031.

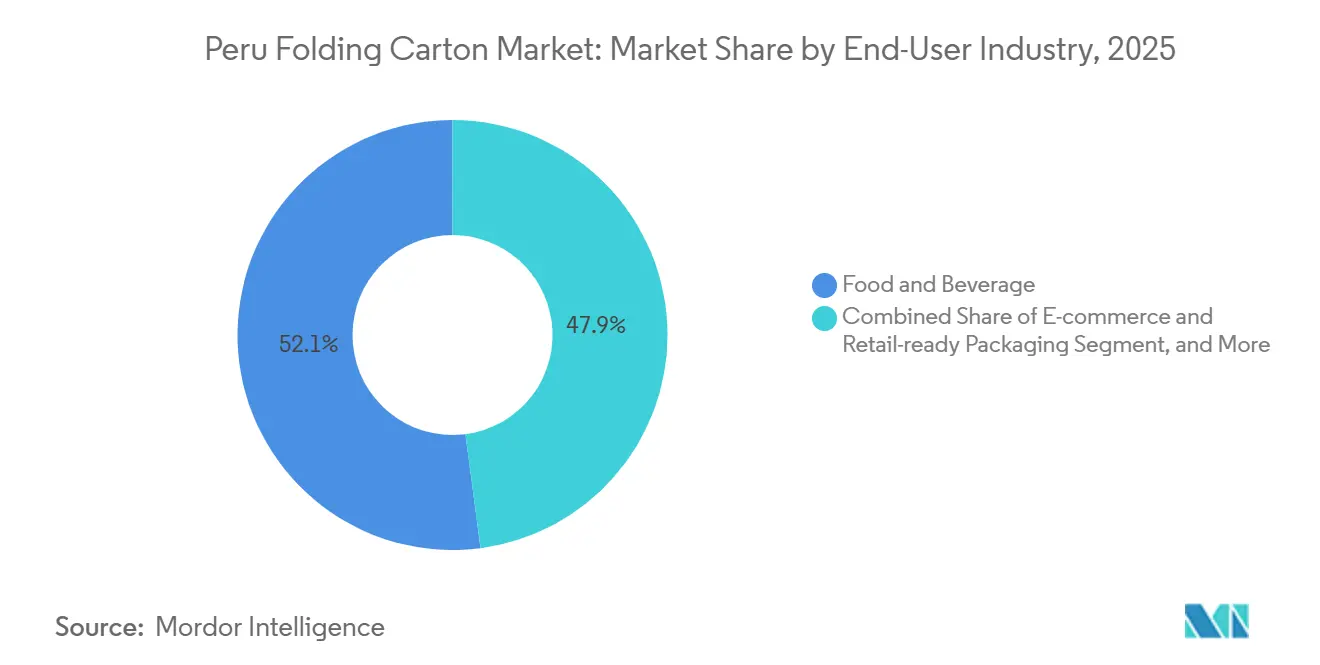

- By end-user industry, the food and beverage industry captured 52.07% of the Peru folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Peru Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Packaging From Food and Beverage Brands | +1.2% | National, Lima, Callao, coastal export zones | Medium term (2-4 years) |

| Expansion of E-Commerce Requiring Lightweight Secondary Packaging | +1.0% | National, early gains in Lima Metropolitana, Arequipa, Trujillo, Piura | Short term (≤ 2 years) |

| High-Graphics Microflute Cartons Penetrating Coastal Produce Exports | +0.9% | Ica, La Libertad, Piura, Lambayeque export corridors | Medium term (2-4 years) |

| Government Incentives for Recycling and Circular Economy Initiatives | +0.8% | National, pilot programs in five priority regions | Long term (≥ 4 years) |

| Rising Disposable Income Boosting Personal Care Carton Consumption | +0.7% | National, with Lima holding 45% of consumption | Medium term (2-4 years) |

| Nearshoring of Pharma Assembly Driving Shelf-Ready Carton Needs | +0.5% | Lima and Callao industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging from Food and Beverage Brands

Export-oriented confectionery and dairy producers now include lifecycle assessments and carbon-footprint clauses in purchasing specifications, prompting converters to certify recycled content and chain-of-custody compliance.[1]Machu Picchu Foods, “2024 Sustainability Report,” mpf.com.pe Draft sanitary regulations issued in 2026 to allow more recycled materials in food-contact applications are expected to unlock demand for food-grade recycled paperboard once DIGESA approvals begin. Local champions such as Carvajal Empaques have already reached Level 3 Huella de Carbono Perú status and operate closed-loop PET recycling lines that feed sustainable carton programs. Mandatory circular-economy roadmaps published for manufacturing set a clear precedent that comparable targets will be imposed on packaging firms, reinforcing the strategic value of low-carbon board and waste-heat recovery investments. A 7% growth in Peru’s cosmetics market in 2025 further illustrates the pull for premium, responsibly sourced cartons that align with brand storytelling at the point of sale.

Expansion of E-Commerce Requiring Lightweight Secondary Packaging

Online retail surpassed USD 15.6 billion in 2024 and is projected to climb another 35% by 2026, creating a surge in small-parcel shipments that rely on compact folding cartons engineered for both outbound and reverse logistics. Same-day delivery expectations in Lima Metropolitana reward converters that can supply tamper-evident formats with optimized dimensional weight. Exituno’s USD 980,000 equipment upgrade increased capacity by 30% to serve dark kitchens and delivery platforms, showing how regional converters are pivoting toward fast-cycle e-commerce work. Social commerce flash campaigns elevate the value of digital presses that can run variable graphics without plates, while low return-rate targets incentivize designs with integrated reseal features.

High-Graphics Microflute Cartons Penetrating Coastal Produce Exports

Agricultural exports exceeded 3 million tonnes in 2025, driving year-round demand for ventilated microflute cartons that can withstand three-week transoceanic cold chains. EcoPacking Perú operates a fully automated plant in La Libertad that delivers lightweight, high-definition cartons directly into nearby agricultural valleys, cutting lead times for growers shipping to the United States and European supermarkets. Blueberry export value has multiplied more than tenfold since 2019, pressuring converters to innovate lighter substrates with barrier coatings that meet EU recyclability thresholds. Importers now request covert digital watermarks for end-to-end traceability, forcing carton suppliers to integrate data-matrix printing during converting runs. With growers racing to new African markets, converters who can customize board strength for longer-haul times will capture the incremental tonnage.

Government Incentives for Recycling and Circular Economy Initiatives

Supreme Decree 018-2025-PRODUCE codifies a national circular-economy roadmap that directs tax incentives toward waste-valorization technologies and mandates sectoral recyclability targets by 2030. The Ruta MYPE Sostenible program channels free audits and microgrants, lowering payback periods for energy-efficient dryers and ink-capture systems among regional carton shops. Formal recycler networks across eleven cities recovered over 537 tonnes of sorted paper monthly by late 2025, slightly easing mill dependence on imported recovered fiber. Nationwide producer-responsibility regulations will soon require converters to co-finance collection hubs, prompting early movers to sign joint ventures with municipal cooperatives. Firms already running internal pulper loops and water-recovery lines will therefore sidestep future compliance levies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Pulp Prices | -0.9% | National, import-reliant converters | Short term (≤ 2 years) |

| Port Congestion at Callao Disrupting Export Carton Lead Times | -0.6% | Callao and neighboring ports | Short term (≤ 2 years) |

| Substitution Threat From Flexible Plastic Pouches in Beverages | -0.4% | National, liquid condiment segment | Medium term (2-4 years) |

| Limited Recovered Fiber Quality From Fragmented Collection Network | -0.3% | Major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Pulp Prices

Latin American pulp fell 18% in early 2025 as oversupply from new mills collided with muted Asian demand, wiping earnings at major forestry groups and raising uncertainty for Peruvian converters tethered to spot import contracts. Cartones del Pacífico routinely imports Colombian kraft linerboard, exposing finished-box margins to both freight premiums and exchange-rate swings. Asian board producers redirected volumes to Peru once Mexico imposed antidumping duties, sparking localized price wars that undercut smaller domestic mills. Some converters hedge by shifting orders toward bagasse-based substrates supplied under multiyear contracts denominated in PEN rather than USD. Yet sudden pulp rallies can still compress EBITDA margins by more than 200 basis points within a single quarter.

Port Congestion at Callao Disrupting Export Carton Lead Times

Berth delays reached 15 days during overlapping fishmeal and fruit-export peaks, forcing packers to truck cartons to secondary ports or pay air-freight premiums when vessel cutoffs were missed. Authorities built a temporary 3.6-hectare antepuerto and APM Terminals invested USD 95 million in yard expansion, yet long-haul truck queues stretched 12 kilometers during 2025 harvest peaks, increasing fuel theft risks. COSCO’s Chancay greenfield port offers faster gate turns, luring truckers away from Callao and intensifying capacity imbalances on traditional corridors. Retailers now pressure converters to store safety stock near farms, raising working-capital needs and amplifying financing costs. Unless planned rail links materialize, structural congestion threatens to shave 0.6 percentage points from the long-term market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled-Core Substrates Gain Share

Solid Bleached Sulfate retained 38.21% of the Peru folding carton market share in 2025, leveraging pristine whiteness and direct-food compliance to dominate confectionery and pharmaceutical niches. White Line Chipboard is expected to grow 7.61% annually as brand owners embrace recycled cores with bleached liners that reduce costs while preserving shelf impact. Folding Boxboard supports lightweight FMCG applications, while coated unbleached kraft secures frozen-food cartons that are exposed to freezer condensation during export. Carvajal Empaques’ bagasse-based board illustrates the potential of non-wood fibers to dampen exposure to pulp-price shocks and meet corporate emissions targets.

Converters therefore invest in multi-grade machines that can toggle between virgin and recycled blends according to pulp arbitrage windows, sharpening resilience in a volatile raw-material landscape. Premium point-of-sale marketing further accelerates coating innovations across these substrates. Trupal reports that up to 80% of purchase decisions happen at retail, so UV spot varnish, holography, and soft-touch laminations increasingly appear on everyday cartons, even holiday panettone boxes.[2]Trupal, “Impresión Offset y Digital,” trupal.com.pe Regulatory pressure on plastic clamshells nudges produce exporters toward paper-based alternatives, expanding total addressable tonnage for moisture-resistant WLC microflute.

By Printing Technology: Digital Gains on Short-Run Demand

Lithographic presses accounted for 44.32% of the Peru folding carton market size in 2025, valued for color consistency, fine linework, and competitive unit costs at runs above 10,000 sheets. However, influencer-driven limited editions and distributor-specific SKUs now launch with order sizes below 5,000 units, catalyzing a 6.82% CAGR in digital press adoption. ZFlex Perú markets hybrid workflows that merge variable data with flexo spot-color decks, cutting lead times from 2 weeks to 48 hours while maintaining ink density suitable for holographic foils. Flexographic printing holds a share of microflute produce cartons, where inline coating and die-cutting speed matter more than four-color fidelity. Gravure remains restricted to ultra-long beverage runs because the high cost of cylinder engraving deters frequent art changes, especially amid SKU proliferation.

Packaging 4.0 discussions spotlight QR-led consumer engagement and anti-counterfeiting as revenue-protecting features. Perú shows how augmented-reality triggers integrated into carton panels raise time-on-page metrics for cosmetics launches. Yet digital printing’s share is capped by the advent of Amcor’s machine-direction-oriented polyolefin films, which threaten litho cartons in sauces and liquid condiments by delivering lower carbon footprints while retaining high clarity. Forward-thinking carton converters therefore bundle digital print capability with recyclable coatings to keep value propositions competitive vis-à-vis flexible pouches.

By End-User Industry: Export Produce Anchors Demand

Food and beverage applications captured 52.07% of the Peru folding carton market size in 2025 as fruit exports alone hit USD 904 million in January 2026, requiring continuous carton output that aligns with staggered harvest calendars. E-commerce shipments, projected to grow at a 7.34% CAGR, demand branded unboxing experiences that withstand drop tests while still fitting high-speed sorters. Pharmaceutical imports from India rose 27% in 2025, and prospective nearshoring will boost GxP-compliant secondary-carton volumes as firms localize blister-card assembly in Lima free-trade zones. Meanwhile, board suppliers in the electronics and household-chemical categories must tailor grease-resistant coatings that withstand tropical humidity along inter-Andean trucking routes.

Electrical and electronics, household cleaners, tobacco, and industrial spares collectively serve a fragmented long-tail user base, primarily from Lima and Trujillo warehouses. Trade partners increasingly enforce recycled-content rules, so converters supplying this long-tail must integrate FSC or PEFC chains of custody to avoid border delays. Flexible-pouch competition remains fiercest in beverages and condiments, yet micro-retail shops still favor tuck-end cartons that stack sturdily on limited shelf real estate. Consequently, end-user diversity cushions the market against cyclical downswings in any single industry.

Geography Analysis

Lima Metropolitana and neighboring Callao concentrate the majority of Peru’s folding-carton converting horsepower, benefiting from proximity to a port that handled more than two million TEU in 2025, which equates to over eighty percent of the nation’s foreign trade throughput.[3]WorldCargo News, “DP World Callao surpasses 2m TEU in 2025,” worldcargonews.com The dense industrial belt hosts multinational plants such as Smurfit WestRock, Carvajal Empaques, and Exituno, supported by laminating, ink-mixing, and die-manufacturing ecosystems located within a sixty-kilometer radius. Large domestic retailers operate distribution centers along the Lima bypass roads, enabling overnight truck runs that deliver printed cartons directly into omnichannel fulfillment hubs. Nonetheless, road congestion from Metro Line 2 construction often disrupts just-in-time transit, forcing converters to keep higher finished-goods inventory buffers. These buffers elevate working-capital requirements, prompting mid-tier converters to seek short-term credit lines indexed to PEN rather than USD.

Northern coastal regions, particularly La Libertad, Piura, and Lambayeque, have emerged as high-growth nodes because they sit adjacent to blueberry and table-grape mega-farms that require continuous microflute box supply during harvest months. EcoPacking Perú’s automated corrugator in Chao district ships ventilated cartons to packhouses within ninety minutes, cutting lead times that otherwise stretch three days from Lima hubs. Regional governments have co-funded feeder road upgrades that reduce truck turnaround times, thereby encouraging converters to install satellite printing and finishing units near packhouse clusters. Formal recycling programs under the PISo strategy now operate in Paita, Ferreñafe, and Sechura, slightly increasing recovered-fiber availability, but contamination rates remain above 8%, limiting its suitability for food-grade board. As Port Chancay comes online with a dedicated underground truck tunnel, logistics planners foresee a partial freight shift northward, which may redistribute carton-plant investment toward Piura over the next five years.

Southern corridors anchored by Ica also generate substantial carton pull because they supply 30% of Peru’s avocado exports, shipping primarily through Callao and occasionally via Pisco’s multipurpose terminal. To mitigate Callao delays, some exporters trial rail-truck intermodal moves that load refrigerated containers directly at farm gates before routing them to the port, reducing box handling and damage. Lima-based converters respond by storing semi-knocked-down cartons at third-party warehouses in Ica, thereby balancing freight efficiency with the need for just-in-time erection near packing lines. Over the forecast horizon, shifting freight patterns, combined with regional sustainability incentives, are expected to diversify carton supply away from an over-reliance on the Lima-Callao axis, thereby improving national resilience against single-node bottlenecks.

Competitive Landscape

The Peru folding carton market is moderately concentrated, with the five largest converters accounting for roughly sixty percent of installed capacity, leaving room for agile specialists to capture niche volumes. Smurfit WestRock’s South America division generated USD 2.099 billion in sales and USD 485 million in EBITDA during 2025, after closing 600,000 tons of high-cost capacity and realizing USD 400 million in savings.[4]Smurfit WestRock plc, “Full Year 2025 Results,” investors.smurfitwestrock.com Its Peruvian plant focuses on export-grade white-lined chipboard and agricultural microflute cartons, leveraging integration with regional kraft liner mills to cushion raw-material swings. Carvajal Empaques, under the Pamolsa banner, manufactures about 400 million PET fruit clamshells annually and holds FSC, ISO 14001, and BRCGS certifications that appeal to multinational grocery chains. These certifications position Carvajal as a primary supplier for export blueberries that must clear EU and U.S. recyclability audits.

Domestic challenger, Exituno invested USD 980,000 in modern presses and die-cutters to lift annual output to 4,500 tonnes, targeting fast-turn e-commerce SKUs and food-delivery formats for dark kitchens in Lima and Arequipa. Grupo Comeca plans USD 8 million for Carvimsa and Epinsa in 2026, including a twenty-percent capacity hike at its paper mill to guarantee in-house liner supply for downstream box plants. Amcor’s September 2025 start-up of an MDO line delivers AmPrima Plus films with twenty-six-percent lower carbon emissions, heightening competitive tension by offering retailers a flexible-pouch alternative to small liquid-food cartons. Smaller converters respond by bundling carton-and-printed-insert kits that speed e-commerce fulfillment and reinforce brand integrity during unboxing. Digital-print partnerships with international press vendors enable them to match Amcor’s agility and reduce minimum order quantities for niche beauty brands.

Certification races now define market entry thresholds, with buyers demanding FSC, PEFC, ISO 9001, ISO 14001 and BRCGS coverage before approving vendor codes, effectively sidelining unaccredited job shops. Multinationals also favor suppliers that provide carbon accounting dashboards and real-time inventory portals that feed directly into their ERP systems, driving industry digitalization. Family-owned converters in Trujillo and Chiclayo leverage regional proximity by signing exclusivity pacts with agro-export packers, ensuring steady volumes during peak harvest months in exchange for off-season promotional-carton runs. Some mid-market players explore smart-label technology co-developments with local universities, aiming to differentiate via anti-counterfeit features embedded in box board.

Peru Folding Carton Industry Leaders

Smurfit WestRock plc

Amcor plc

Klabin S.A.

Graphic Packaging Holding Company

Carvajal Empaques S.A.S.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smurfit WestRock posted full-year 2025 Latin America sales of USD 2.099 billion and EBITDA of USD 485 million, surpassing targets after capacity rationalization.

- December 2025: PRODUCE launched the PRODUCE-AECID fund of PEN 1 million (USD 265,000) to accelerate circular-economy projects among micro-enterprises in five priority regions.

- September 2025: Amcor inaugurated a Machine Direction Orientation line in Lima to manufacture AmPrima Plus recyclable films for South American markets.

- August 2025: The government enacted the 2030 Circular Economy Roadmap for manufacturing and domestic trade, defining standards and incentives for packaging circularity.

Peru Folding Carton Market Report Scope

The Peru Folding Carton Market encompasses the production, distribution, and application of folding cartons, paper-based packaging solutions designed for a variety of consumer and industrial goods. This report includes an analysis of key market dynamics, trends, and forecasts specific to Peru.

The Peru Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Peru folding carton market size and how fast is it growing?

The Peru folding carton market size reached USD 468.23 million in 2026 and is forecast to climb to USD 610.78 million by 2031, reflecting a 5.46% CAGR.

Which material type leads demand in Peru’s folding carton sector?

Solid Bleached Sulfate governs the segment with 38.21% of Peru folding carton market share thanks to its food-contact compliance and premium printability.

How is e-commerce influencing folding carton design in Peru?

Rapid growth in online retail is lifting demand for lightweight, tamper-evident cartons that fit automated fulfillment and support resealable returns, driving a 7.34% CAGR in the e-commerce packaging segment.

What regulatory trends will shape folding carton sustainability?

National circular-economy roadmaps, upcoming DIGESA rules for recycled food-grade board and extended producer-responsibility schemes will oblige converters to certify recycled content and fund collection programs.

Which printing technology is growing fastest?

Digital printing is expanding at a 6.82% CAGR as brands seek short-run, variable-data campaigns without the setup costs of lithographic plates.

How exposed are Peruvian converters to pulp price swings?

Roughly half of virgin fiber is imported, so fluctuations in regional pulp markets and freight rates can trim margins by up to 0.9 percentage points on projected CAGR.

Page last updated on: