Chile Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

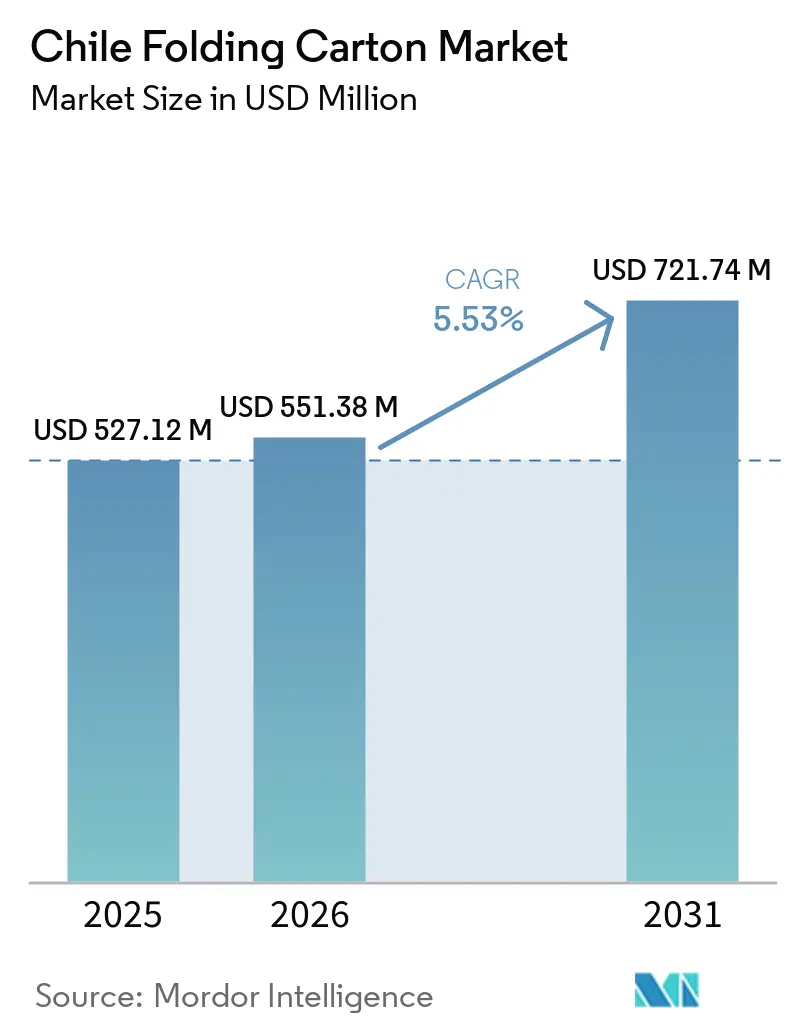

| Base Year Market Size (2025) | USD 527.12 Million |

| Market Size (2026) | USD 551.38 Million |

| Market Size (2031) | USD 721.74 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

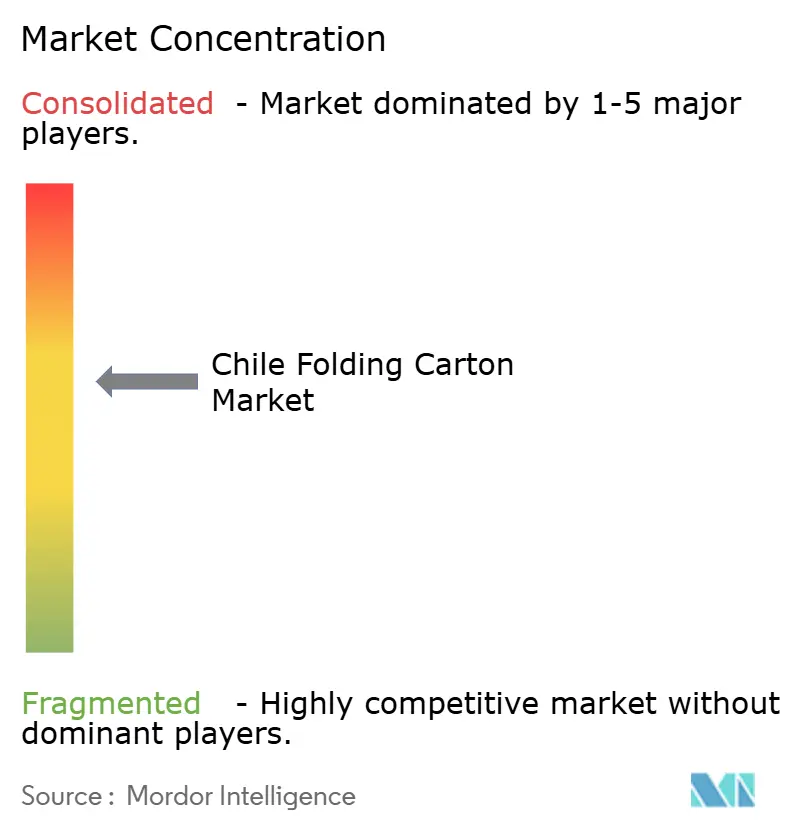

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Folding Carton Market Analysis by Mordor Intelligence

The Chile folding carton market size is expected to be USD 527.12 million in 2025, USD 551.38 million in 2026, and reach USD 721.74 million by 2031, growing at a CAGR of 5.53% from 2026 to 2031. Demand is expanding as Santiago consolidates its role as a regional packaging hub that serves Chile’s export-oriented agro-industry and a fast-growing e-commerce ecosystem. Extended Producer Responsibility rules are pushing brand owners toward recyclable substrates, while the single-use plastics law is accelerating fiber substitution in food-service, grocery, and last-mile delivery channels. Integrated players are investing in moisture-resistant kraft grades, digital printing, and automation to navigate pulp price swings, warehouse robotics, and retailer shelf-ready requirements. At the same time, independent converters face margin pressure from pulp volatility, currency shifts, and the capital costs of variable-data presses, prompting a gradual consolidation toward vertically integrated mills that can guarantee supply security and circular-economy compliance.

Key Report Takeaways

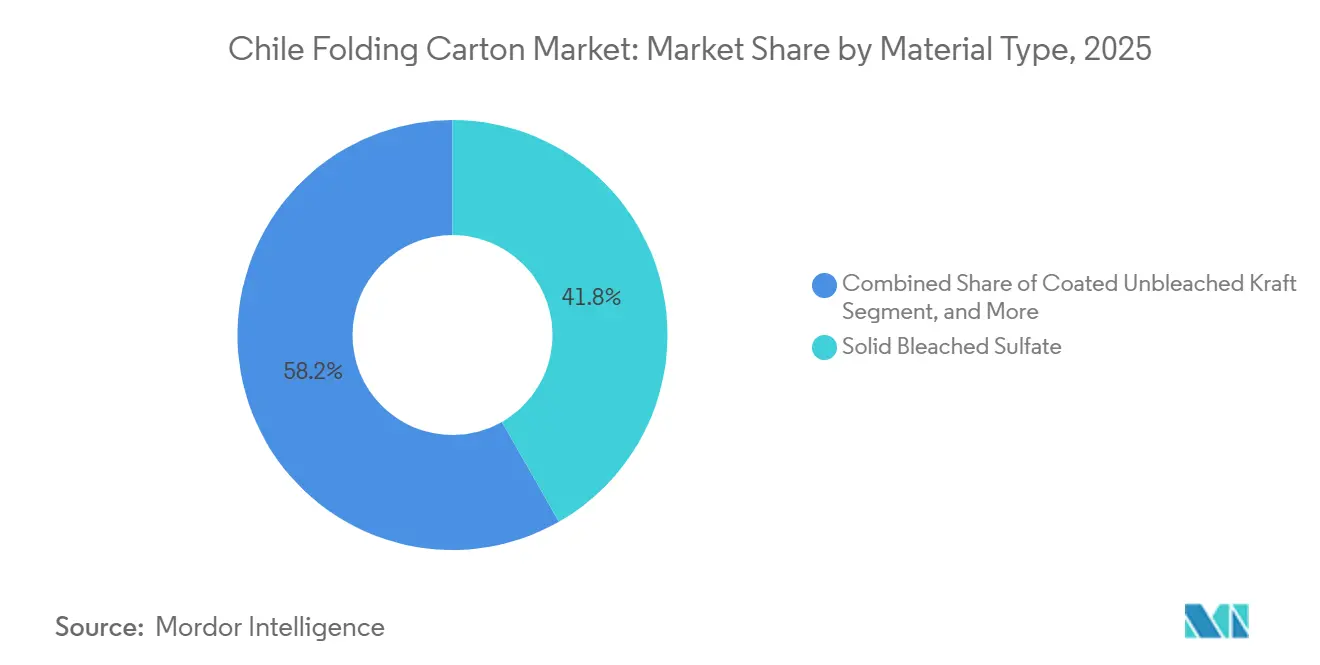

- By material type, solid bleached sulfate captured with 41.76% of the Chile folding carton market share in 2025.

- By printing technology, the Chile folding carton market size for digital printing is projected to grow at a 7.17% CAGR to 2031.

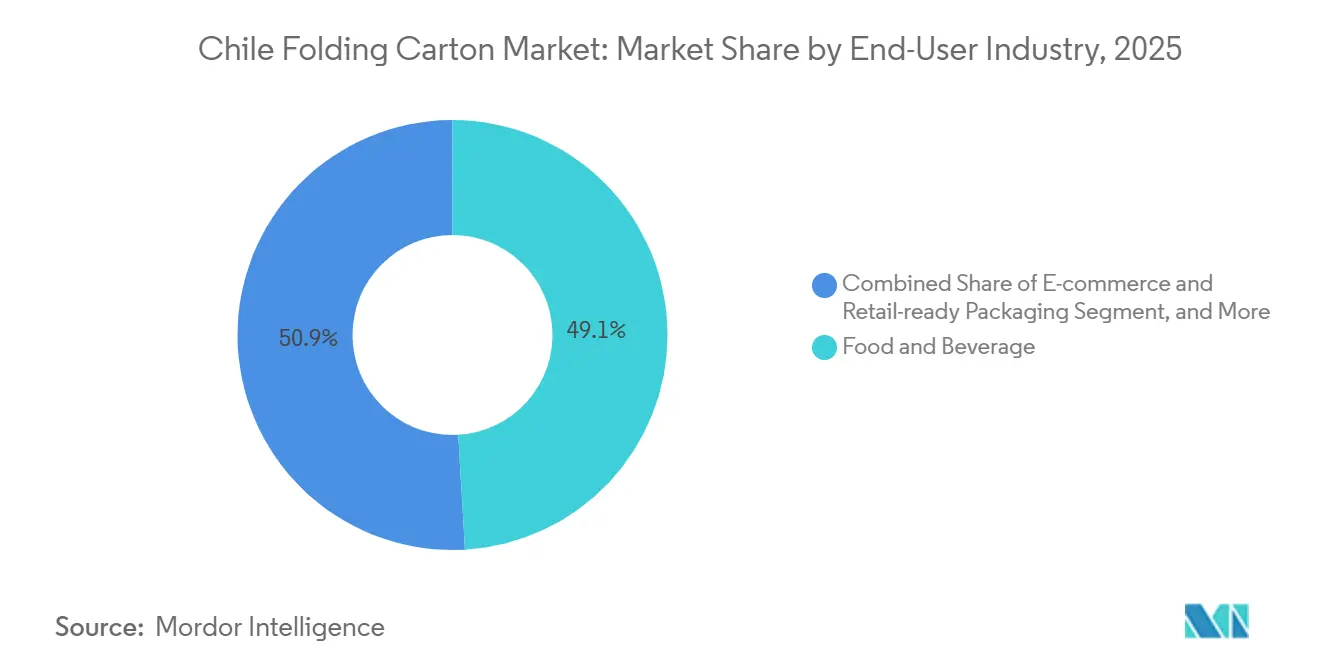

- By end-user industry, the food and beverage industry captured 49.07% of the Chile folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Packaging Solutions | +1.2% | National, early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Expansion of Chile's Processed Food Export Sector | +1.1% | National, export-oriented regions (Maule, O'Higgins, Biobío) | Long term (≥ 4 years) |

| Rising E-commerce Volumes Requiring Secondary Packaging | +0.9% | Metropolitan Santiago, urban centers | Short term (≤ 2 years) |

| Increasing Adoption of Shelf-Ready Packs by Retail Chains | +0.6% | National, concentrated in Santiago metro | Medium term (2-4 years) |

| Surge in Small-Batch Digital Printing for Personalization | +0.5% | Santiago, Valparaíso, craft beverage hubs | Medium term (2-4 years) |

| Government Incentives for Circular Economy Practices | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging Solutions

Decreto 12, issued in 2024 under Chile’s Extended Producer Responsibility framework, sets cardboard collection targets that rise from 30% in 2026 to 60% by 2030, thereby lowering compliance fees for brands that adopt recyclable cartons rather than multi-material laminates. Law 21.368 bans non-recyclable food-service containers and enforces minimum recycled-content thresholds that narrow the cost gap between virgin plastics and fiber-based substrates. CMPC’s Pulp-T egg cartons, produced from recycled fibers and tea residues, illustrate how converters are aligning product design with circular mandates. Walmart Chile’s robotic distribution center demands cartons that combine recyclability with compression strength, proving that sustainability must coexist with performance. Cencosud’s cardboard-reuse machines for e-commerce fulfillment reinforce the extent to which large retailers internalize circular costs and specify fiber-based void-fill.

Expansion of Chile's Processed Food Export Sector

Agro-industrial exports hit USD 3.392 billion in 2025, up 33% year-on-year, while cherry shipments soared to 625,000 tonnes, 91% of which moved to China in refrigerated containers. Coated Unbleached Kraft cartons withstand condensation during trans-Pacific transits, explaining their outperformance versus the overall Chile folding carton market. Wine exporters still rely on high-graphics SBS gift boxes to protect USD 1.26 billion in shipments.[1]Wines of Chile, “Exportaciones de Vino 2025,” Winesofchile.org Nut exports worth USD 643 million require tamper-evident cartons with moisture barriers. Phytosanitary rules from SAG mandate variable-data traceability labels, spurring the adoption of digital presses.

Rising E-commerce Volumes Requiring Secondary Packaging

Online retail exceeded USD 10 billion in 2025 and is expanding 7-10% annually, with food e-commerce alone reaching USD 1.9 billion. Folding cartons are favored for barcode legibility and stackability in automated fulfillment centers. Walmart Chile’s 64-robot facility imposes strict dimensional tolerances that reward converters who invest in precise die-cutting and scoring. Cencosud’s cardboard reuse initiative shows retailers substituting bubble wrap with carton-based void-fill. The e-commerce packaging segment, valued at USD 0.61 billion in 2024, is projected to grow at 17.42% CAGR through 2033, well ahead of the broader Chile folding carton market.

Increasing Adoption of Shelf-Ready Packs by Retail Chains

Major supermarkets now standardize on shelf-ready formats that reduce in-store labor. Walmart Chile reports 99.9% order accuracy, a metric that hinges on cartons engineered for robotic handling. Retail pack adoption is rising in Santiago and secondary cities as chains seek faster replenishment, prompting converters to combine micro-flute inserts with high-graphics exteriors for simultaneous protection and promotion. Shelf-ready acceptance also dovetails with government sustainability targets by minimizing stretch film and shrink wrap in back-of-store operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Virgin Fiber Pulp Prices | -0.7% | National, linked to global pulp markets | Short term (≤ 2 years) |

| Limited Domestic Recycling Infrastructure Capacity | -0.5% | National, acute in rural regions | Medium term (2-4 years) |

| High Initial Cost of Digital Printing Equipment | -0.3% | National, affects small and mid-sized converters | Medium term (2-4 years) |

| Competitive Pressure from Flexible Plastic Alternatives | -0.4% | National, concentrated in the snack and pet-food segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Fiber Pulp Prices

Global long-fiber pulp prices fell 18% year-on-year in Q1 2025, yet Chilean converters still faced cost spikes due to currency swings and freight bottlenecks. Integrated multinationals such as Smurfit WestRock mitigate volatility through captive pulp, including a USD 150 million capacity lift at Brazil’s Três Barras mill scheduled for completion in 2027. Independent converters lack hedging options, must renegotiate supply every quarter, and often absorb 10-15% cost shifts that squeeze margins and delay capital upgrades.

Limited Domestic Recycling Infrastructure Capacity

Chile valorized only 48.3% of cardboard and 3.2% of beverage cartons in 2025. Rural municipalities have minimal curbside coverage, so converters pay premiums for scarce recycled pulp. While Integrity’s Quilicura plant and Tetra Pak’s San Bernardo line add capacity, the combined 27,000-tonne output covers less than 6% of the estimated 500,000-plus tonnes of cartons consumed annually. The supply gap forces reliance on imported recovered fiber, exposing converters to freight and exchange-rate risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Substrates Gain on Cold-Chain Exports

Solid Bleached Sulfate dominated the Chile folding carton market share with 41.76% in 2025, thanks to cosmetics, pharmaceuticals, and premium wine boxes that demand high whiteness and print fidelity. Coated Unbleached Kraft, favored for moisture resistance, outpaces the Chile folding carton market size average with a 6.71% CAGR by 2031, mirroring cherry exports that rely on cartons able to survive humid refrigerated voyages to China. Folding Boxboard benefits from Sorepa’s recovered fiber flow, while White Line Chipboard finds price-sensitive buyers in household goods.

Amcor’s AmFiber trays, unveiled in 2026, showcase hybrid fiber-plus-barrier structures that blur lines between carton and molded pulp and could redirect growth toward specialty grades.[2]Amcor, “AmFiber Tray Launch,” Amcor.com Recycled-content mandates embedded in law 21.368 further tip the balance toward kraft and boxboard grades that deliver circularity credentials without sacrificing structural integrity. Integrated mills are tweaking furnish recipes to balance virgin and recycled pulp, thereby stabilizing costs during pulp upcycles and improving life-cycle assessments presented to export buyers in Europe and North America.

By Printing Technology: Digital Personalization Scales Up

Lithographic presses still account for 46.12% of the printed volume, especially among large food brands that demand Pantone accuracy and spot Varnishes. Yet digital printing has the fastest 7.17% CAGR through 2031, as craft breweries, specialty coffee roasters, and DTC snack brands request runs of under 2,000 units with individualized QR codes or influencer artwork. South America’s digital print equipment market crossed USD 159.22 million in 2024, and Santiago captures a disproportionate share due to its start-up ecosystem.

Hybrid flexo-digital lines are emerging, offering variable SKUs without exceeding the Chile folding carton industry’s tight lead-time windows. High press costs, ranging from USD 500,000 to USD 2 million, deter small converters, but leasing and contract-print models are lowering entry barriers. Walmart Chile’s robotics requires perfect barcode placement, nudging converters toward digital correction workflows. Gravure’s footprint shrinks each year, limited to cigarettes and high-volume snacks, while screen and foil embellishment remain niche but vital for luxury cosmetics and holiday gift packs.

By End-User Industry: E-Commerce Speeds Ahead

Food and beverage dominated demand in 2025, but e-commerce and retail-ready packs are the breakout star, growing at 7.85% CAGR on the back of Chile’s USD 10 billion online retail market. Cartons designed for frustration-free unboxing, easy returns, and automated detection deliver value well above their tonnage share, boosting margins for converters who specialize in this niche. Healthcare and cosmetics demand SBS for tamper seals and tactile finishes, while electronics require anti-static liners and cushioned inserts.

Tobacco, though shrinking, still uses high-security cartons with holographic threads dictated by Chilean tax rules. Flexible plastics remain a formidable rival in snack foods and pet-food pouches, yet the plastics ban and recycled-content thresholds are gradually pushing volumes toward fiber alternatives. Converters that integrate moisture barriers or combine carton sleeves with mono-PET liners can capture switch-over volumes without sacrificing protection.

Geography Analysis

The Chile folding carton market demand is heavily concentrated in Metropolitan Santiago, which houses roughly 40% of national consumption and most converter capacity. Valparaíso’s port complex anchors export flows, especially for wine bound for the United States and Europe. Biobío, Maule, and O'Higgins host pulp and paper mills plus agro-export pack-houses that require just-in-time sleeve supply. The geographic concentration creates logistics efficiencies for large converters but also exposes the market to Santiago-centric risks, including seismic vulnerability, labor disputes, and infrastructure bottlenecks during peak export seasons

This clustering creates freight efficiencies for large integrated mills but exposes the supply chain to seismic risk and occasional port congestion during peak cherry season. Export orientation distinguishes Chile from its larger South American peers. Cherry exports grew 51% to 625,000 tonnes in 2025 and rely on kraft cartons with high stacking strength. Even when domestic wine volume slipped 1.3%, premium carton demand held up due to brand-building needs in Asia and Europe.

Regional pulp oversupply means Asian boxboard may flood Andean markets as Mexican tariffs divert Chinese supply southward, pressuring prices in Chile. Smurfit WestRock’s 2026 purchase of Ecuador’s Cartomanabí signals a race for regional scale that allows cross-border balancing of demand surges. Chile’s stringent Ley REP and plastics law act as non-tariff barriers, since imported packs meet the same recycled-content tests, leveling the field in favor of local converters already aligned with circular targets.

Competitive Landscape

Competition is moderate to high, led by multinationals Smurfit WestRock, Amcor, and Mondi alongside domestic names Cartones del Pacífico and Envases del Pacífico. Smurfit WestRock posted USD 2.113 billion in South American packaging sales in 2025 and is boosting Três Barras pulp output by up to 10% to hedge against external pulp shocks.[3]Smurfit WestRock, “Annual Report 2025,” Smurfitkappa.com Envases del Pacífico swung to a USD 1.06 million net loss in 2024, illustrating how scale and integration dictate profitability in the Chile folding carton industry.

CMPC’s USD 65 million investment wave covers molded-pulp, water-based varnishes, and moisture-separable salmon liners, targeting premium export niches.[4]CMPC, “Innovaciones de Empaques 2025,” CMPC.com Mondi’s EUR 1.2 billion (USD 1.3 billion) capex program, largely completed by end-2024, adds corrugated and flexible capacity in Eastern Europe to feed global networks, enabling price competition in Chile. Amcor’s April 2026 tie-up with Metsä and G. Mondini brings fiber trays with more than 80% recyclability, positioning the firm for growth in chilled foods.

Smaller converters without digital presses or closed-loop fiber sources risk margin erosion as retailers push EPR pass-through costs and demand audit trails on recycled content. Strategic moves focus on e-commerce-specific formats, variable-data personalization, and hybrid cartons that blend barrier liners with kraft outers. Access to recycled fiber and capital for automation now define competitive moats more than pure converting capacity.

Chile Folding Carton Industry Leaders

Smurfit WestRock plc

Amcor plc

International Paper Company

Mondi plc

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Amcor, Metsä Group, and G. Mondini unveiled an integrated fiber-tray system with >80% fiber recovery demonstrated live at Interpack, aimed at chilled-food producers.

- March 2026: Smurfit WestRock acquired Ecuador’s Cartomanabí, adding 50,000 tonnes of folding carton capacity to its South American portfolio.

- March 2025: Klabin started up the BRL 1.56 billion (USD 312 million) Piracicaba II project in Brazil, boosting corrugated supply to Chile.

- February 2025: Integrity opened Chile’s largest board recycling plant in Quilicura, a CLP 6 billion (USD 6.64 million) investment that adds 20,000 tonnes of capacity.

Chile Folding Carton Market Report Scope

The folding carton market is the industry that produces, distributes, and uses paperboard-based packaging solutions, commonly used for consumer goods, food, beverages, and other products. This report analyzes the market trends, growth drivers, challenges, and opportunities specific to Chile folding carton market.

The Chile Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Chile folding carton market size and its expected growth?

The Chile folding carton market size reached USD 551.38 million in 2026 and is forecast to attain USD 721.74 million by 2031, reflecting a 5.53% CAGR.

Which material type is expanding fastest in Chile’s carton sector?

Coated Unbleached Kraft is projected to grow at a 6.71% CAGR through 2031 as exporters seek moisture-resistant, cold-chain-ready cartons.

How is e-commerce influencing carton design requirements?

Online retail sales exceeding USD 10 billion are driving demand for secondary cartons optimized for robotic handling, easy-open features, and friction-free returns.

What regulatory measures are shaping packaging decisions?

Ley REP and the single-use plastics law impose collection targets and recycled-content thresholds that favor recyclable fiber cartons over plastic alternatives.

Why are pulp price swings a major risk for converters?

Virgin fiber cost volatility, amplified by currency shifts, can move input costs by 10-15% per quarter, squeezing margins for converters without captive pulp.

Which printing technology is gaining share in Chile?

Digital printing is advancing at a 7.17% CAGR as craft beverage and DTC brands require short runs with personalized graphics and QR-based traceability.

Page last updated on: