Philippines Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

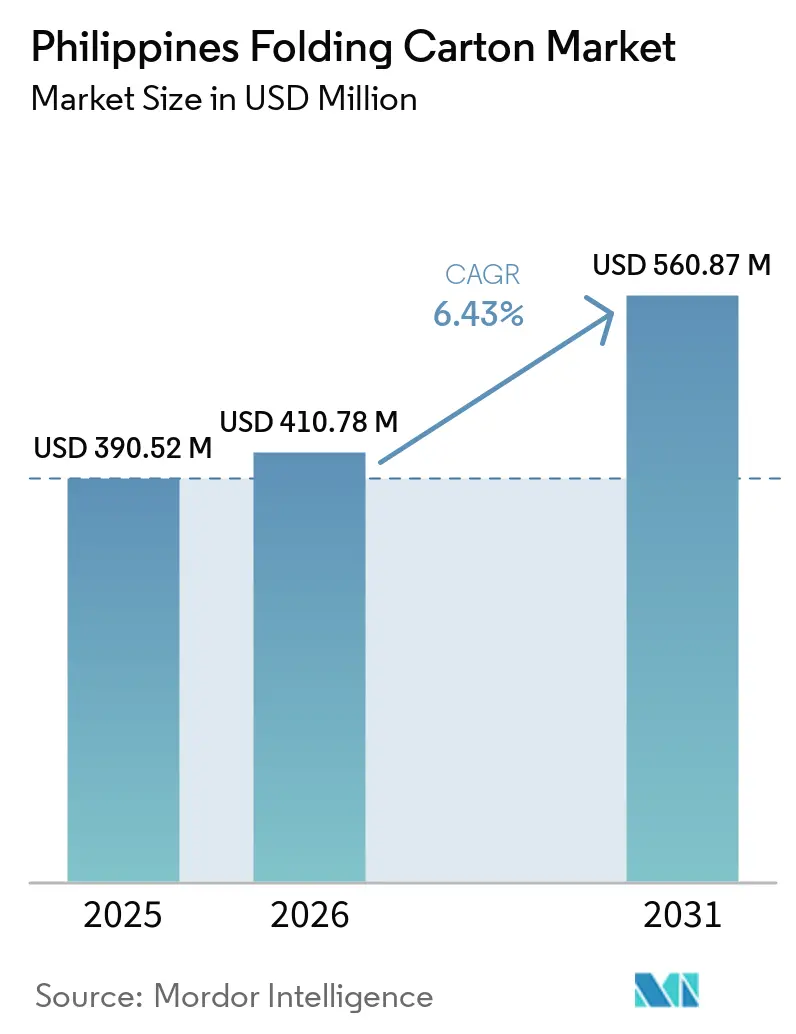

| Base Year Market Size (2025) | USD 390.52 Million |

| Market Size (2026) | USD 410.78 Million |

| Market Size (2031) | USD 560.87 Million |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

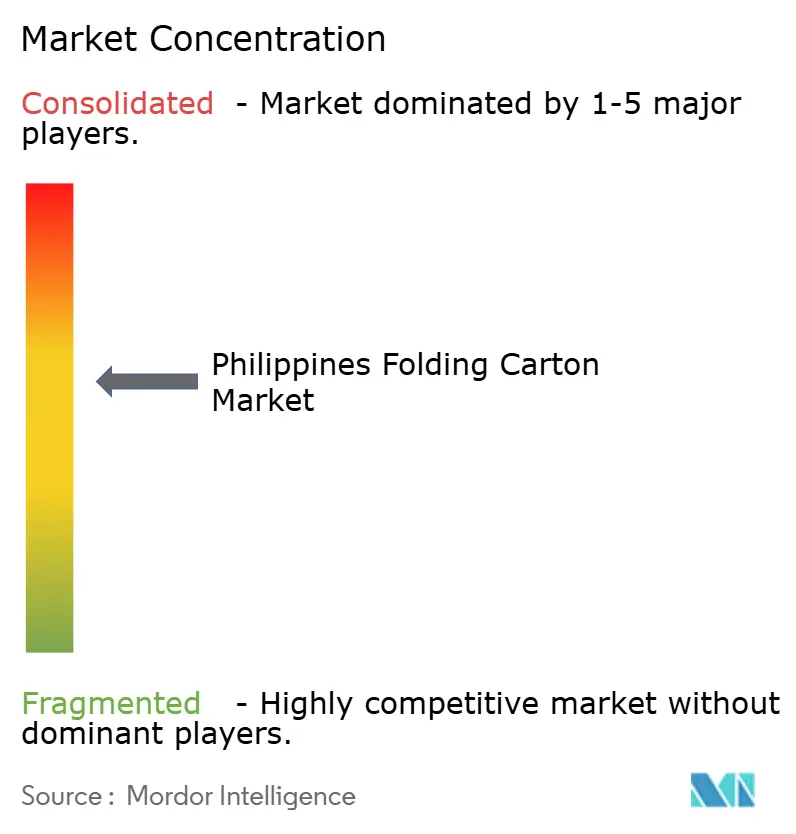

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Folding Carton Market Analysis by Mordor Intelligence

The Philippines folding carton market size is projected to expand from USD 410.78 million in 2026 to USD 560.87 million by 2031, registering a 6.43% CAGR over 2026-2031. Strengthening single-use plastic legislation, expanding e-commerce penetration, and aggressive capital spending by multinational food processors are the principal forces behind this trajectory. Converter investment in hybrid offset-flexo presses and digital workflow upgrades is lowering set-up waste and enabling rapid SKU rotation for cloud kitchens, while excise-tax-driven substitution keeps paperboard demand resilient despite pulp price volatility. Multinationals such as Smurfit WestRock and Mondi are leveraging regional to service high-volume accounts, yet domestic specialists continue to win on turnaround speed and localized design support, preserving a moderately fragmented competitive landscape. Rising household incomes and an ongoing shift toward organized retail underpin further growth as brand owners seek tamper-evident, traceable, and curbside-recyclable packaging solutions.

Key Report Takeaways

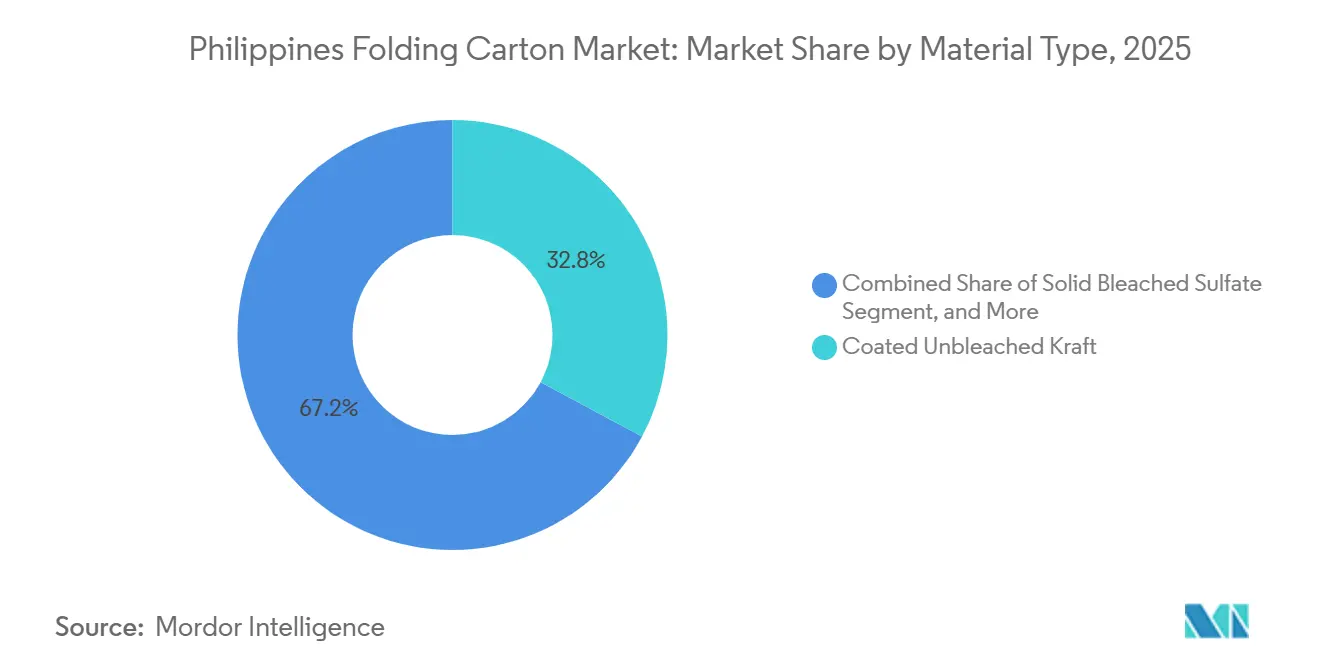

- By material type, coated unbleached kraft captured with 32.83% of the Philippines folding carton market share in 2025.

- By printing technology, the Philippines folding carton market size for digital printing is projected to grow at a 8.34% CAGR to 2031.

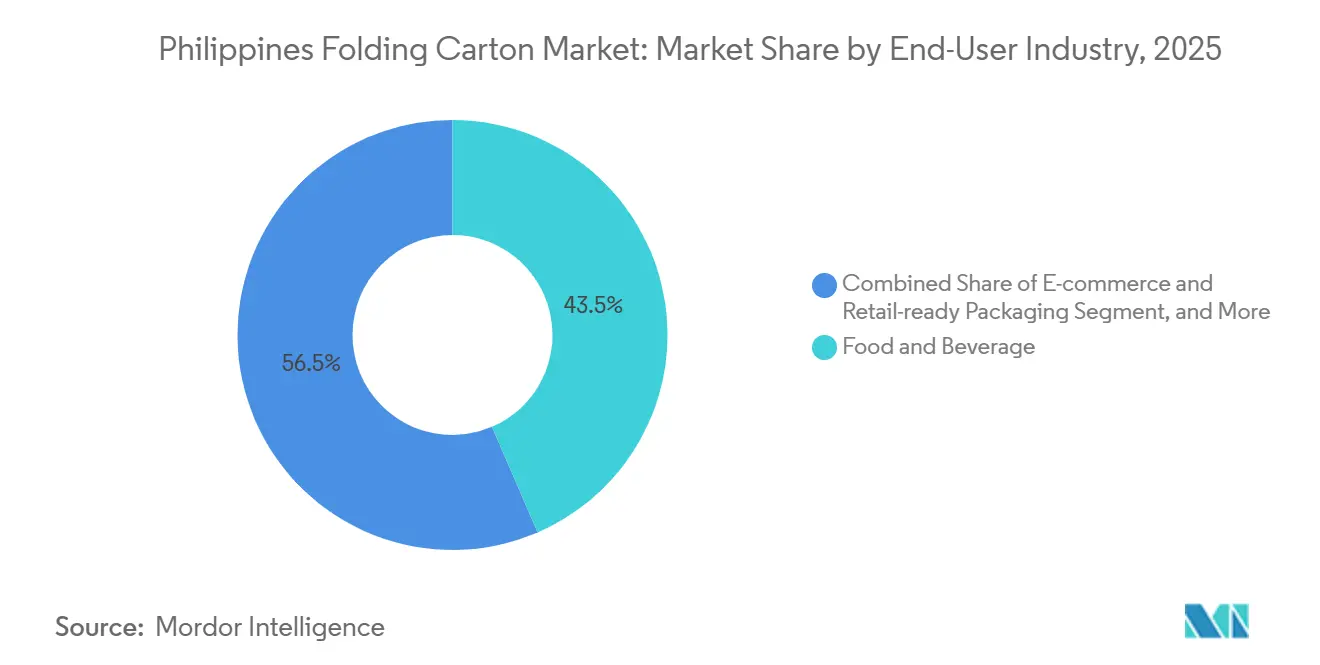

- By end-user industry, the food and beverage industry captured 43.52% of the Philippines folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of E-commerce Packaging Demand | +1.8% | Metro Manila, CALABARZON, Central Luzon | Medium term (2-4 years) |

| Expansion of Food and Beverage Processing | +1.5% | Luzon provinces of Batangas, Tarlac, Laguna | Medium term (2-4 years) |

| Rising Demand for Sustainable Packaging | +1.2% | National, led by multinational FMCG chains | Long term (≥ 4 years) |

| Increased Adoption of Digital Printing | +0.9% | Metro Manila and Cebu converters | Short term (≤ 2 years) |

| Government Excise Tax on Plastic Packaging | +0.7% | National | Medium term (2-4 years) |

| Rapid Growth of Cloud-Kitchen Start-ups | +0.6% | Metro Manila, Cebu, Davao | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of E-commerce Packaging Demand

Online grocery services and direct-to-consumer brands request tamper-evident seals and variable-data printing that personalize unboxing experiences. Cloud-based restaurant chains have secured fresh investment and rely on short-run cartons that can be sourced within days rather than weeks. The Department of Trade and Industry reports that 78% of Filipino consumers value sustainability when shopping online, encouraging fulfillment centers to specify recyclable paperboard in place of plastic pouches.[1]Department of Trade and Industry, “E-Commerce Consumer Survey 2025,” dti.gov.ph Logistics providers highlight that fiber-based cartons lower dimensional-weight charges and offer 79% curbside recycling access in mature markets, a persuasive argument as domestic fuel costs remain volatile.

Expansion of Food and Beverage Processing Sector

More than PHP 20 billion (USD 352 million) has been deployed between 2024 and 2026 to enlarge domestic capacity for frozen foods, biscuits, coconut products, and seasonings. These projects cluster around cold-chain infrastructure in Luzon, locking in steady volumes of FDA-compliant, coated, unbleached kraft cartons with moisture barriers. Converters that certify substrates for food contact gain preferred-supplier status as processors tighten audit protocols. Adoption of electronic Certificates of Product Registration starting October 2025 increases traceability expectations, benefitting plants equipped with digital lot-coding.

Rising Demand for Sustainable Packaging Solutions

The Extended Producer Responsibility (EPR) law compels large enterprises to recover 60% of their plastic output by 2026, incentivizing a switch to recyclable fibers. Multinational converters are investing in capacity in Southeast Asia to meet this surge, while local printers are expanding their offerings of FSC-certified substrates. Government consultations on using excise tax revenue to fund material recovery facilities promise improved segregation and higher-quality recovered paper streams. Brands in personal care and home care categories adopt premium bleached board with compostable coatings to align with corporate carbon targets.

Increased Adoption of Digital Printing

Hybrid offset-flexo presses and roll-to-sheet inkjet lines shorten make-ready from hours to minutes, cutting spoilage by up to 40%. Converters servicing cloud kitchen and meal-kit operators now adjust artwork batches overnight, embedding QR codes and promotional messages without plate changes. Brands exporting to neighboring ASEAN members demand multilingual cartons, a requirement best met through digital workflows. Early adopters in Metro Manila and Cebu secure premium margins in exchange for just-in-time delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Paperboard Prices | -1.2% | Nationwide | Short term (≤ 2 years) |

| Limited Domestic Pulp Production | -0.9% | Nationwide | Long term (≥ 4 years) |

| Competition From Flexible Packaging | -0.7% | Food and beverage segments | Medium term (2-4 years) |

| Power Supply Interruptions | -0.5% | Luzon and Visayas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Paperboard Prices

Benchmark pulp climbed to USD 740 per ton in February 2026, a 15% jump in six months, tightening converter margins and triggering quarterly price-adjustment clauses.[2]Board of Investments, “Philippine Packaging Industry Report 2025,” boi.gov.ph Philippine converters import nearly all virgin fiber, leaving them exposed to freight spikes and foreign-exchange swings. Inventories now run higher, but carrying extra stock strains working capital, especially for small printers whose credit lines are capped. Those conditions complicate converters' ability to offer fixed-price contracts, which many consumer-goods companies prefer. Until regional pulp supply stabilizes, cost pass-through will remain uneven.

Limited Domestic Pulp Production Increasing Import Dependence

The country lacks commercial forestry plantations, and environmental rules restrict large-scale logging projects, leaving converters reliant on containerized pulp shipments with four-to-six-week lead times. Imported fiber can add 15% to landed substrate cost, eroding competitiveness against Indonesian and Vietnamese suppliers operating integrated mills. Recycled-fiber quality is inconsistent because household segregation remains weak, pushing mills to operate below full capacity. Converters diversify sourcing, but spot markets remain sensitive to geopolitical tensions in key supplier nations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Dominance Meets Bleached Premium

Coated unbleached kraft captured 32.83% of the Philippines folding carton market share in 2025 on the strength of its recyclability and suitability for food-contact applications. Solid bleached sulfate is forecast to outpace all other materials at a 7.76% CAGR, buoyed by premium cosmetics and pharmaceutical launches that require high-brightness substrates and tamper-evident seals. The Philippines folding carton market size attributed to coated unbleached kraft will rise in parallel with frozen food and quick-service restaurant growth. Pharmaceutical producers sourcing cartons for oral solids already specify child-resistant designs that favor premium bleached board.

Solid bleached sulfate benefits further from rising demand for deluxe finishes such as embossing and metallic accents in skin-care lines distributed through department stores and e-commerce platforms. Folding boxboard provides a cost-effective option for dry groceries and mid-tier household goods, while white-lined chipboard persists in shoe boxes and industrial packs where aesthetics rank below price. Recycled-content grades make incremental headway as EPR compliance drives brand owners to publish recyclability scores on front-of-pack graphics.

By Printing Technology: Flexo Volume, Digital Agility

Flexographic systems accounted for 39.53% of 2025 output thanks to fast line speeds and water-based inks that meet food safety rules, but the Philippines folding carton market, driven by digital presses, is expanding the fastest, in line with the 8.34% projected CAGR. Converters leverage a fixed-color palette in flexo to reduce wash-ups on high-volume snack and beverage cartons, while reserving digital lines for subscription boxes and limited-edition runs.

Digital’s share hovering at 20-30% in short-run niches thrives on demand for variable QR codes and dynamic promotions used by cloud kitchens and direct-to-consumer brands. Hybrid offset-flexo presses allow printers to combine photographic imagery with high-speed varnishing in one pass, preserving flexo’s cost advantage on long jobs while matching offset quality. Lithographic presses remain credible for ultra-premium categories, whereas gravure rarely appears because few local projects exceed half-million-unit thresholds.

By End-User Industry: Food Anchors, E-commerce Accelerates

Food and beverage producers delivered 43.52% of 2025 demand, making them the backbone of the Philippines folding carton industry. Cartons enclosing canned fish, biscuits, and powdered seasonings increasingly incorporate moisture-barrier coatings that help preserve shelf life in humid climates. The Philippines folding carton market size for e-commerce and retail-ready packaging is set to rise faster than any other vertical at a 7.96% CAGR, supported by cloud kitchens, meal-kit operators, and online grocery portals.

Healthcare spending lifts pharmaceutical carton volumes as the Department of Health expands oncology and vaccine programs. Personal care brands migrate to premium bleached board to convey sustainability credentials, yet some mass-market SKUs continue to rely on flexible pouches for cost reasons. Electronics and small appliances require anti-static liners, whereas tobacco packaging remains subject to strict excise and health-warning rules that require serialized traceability.

Geography Analysis

Greater Metro Manila, and Central Luzon account for more than 70% of national demand because they host the largest clusters of food processors, pharmaceutical plants, and fulfillment centers. The proximity of Batangas and Cavite industrial zones to Manila’s ports cuts transit times for converters delivering just-in-time cartons. However, recurring grid alerts in April 2026 forced plants to install backup generators, adding 8-12% to energy costs and pressuring working capital for small printers.

Cebu anchors Visayas demand, supplying regional exporters of dried mangoes and processed seafood, yet yellow alerts in early 2026 capped production growth. Mindanao’s coconut processors order cartons from Luzon converters, absorbing extra freight costs because local capacity remains limited. Inter-island shipping adds 10-15% to logistics expenses, but consolidating orders through Manila hubs mitigates part of this disadvantage.

Government enforcement of EPR and forthcoming excise taxes on single-use plastics encourage retailers in urban centers to replace plastic carry-outs with folding cartons. Municipalities collecting USD 1.2 fees on disposable plastic items channel revenues toward material-recovery facilities, improving waste segregation and boosting recycled-fiber quality.[3]Meralco, “Maintenance Advisories April 2026,” meralco.com.ph Those measures underpin longer-term carton penetration even in outlying provinces once collection infrastructure matures.

Competitive Landscape

The Philippines folding carton market exhibits moderate fragmentation, with the ten largest players accounting for roughly 55-60% of national volume. Smurfit WestRock has already realized more than USD 400 million in merger and is upselling board solutions to multinational clients across Asia-Pacific.[4]Smurfit WestRock, “Q1 2026 Earnings Release,” smurfitwestrock.com Mondi’s EUR 1.2 billion (USD 1.32 billion) expansion in Southeast Asia underlines the strategic pivot toward fiber-based packaging in the region. Amcor’s USD 8.43 billion acquisition of Berry Global strengthens cross-selling into accounts that buy both flexible and rigid formats.

Domestic leaders such as Printwell, VJ7 Printing, and Papercon possess deep ties with quick-service restaurants and FMCG brands, winning on design agility and drop-in deliveries for rush promotions. Printwell’s eight-station fusion line cuts set-up waste by up to 40%, while VJ7’s Heidelberg Speedmaster CX 104 handles specialty halal cartons destined for Middle East markets. Papercon leverages a six-decade track record and ISO 9001 certification to anchor large-volume accounts such as Jollibee and Procter & Gamble.

Growth white space centers on digital micro-runs for cloud kitchens, pharmaceutical serialization, and compostable barrier coatings ahead of the Bureau of Philippine Standards’ forthcoming compostability guidelines. Rengo’s incremental equity stakes in Indonesian packaging firms hint at a scenario where additional Southeast Asia assets could feed Philippine demand should local converters struggle to scale. Competitive intensity remains elevated as multinationals chase high-growth segments while niche local players differentiate through geographic proximity and customized service.

Philippines Folding Carton Industry Leaders

Cr8tive Boxes & Labels Corporation

Oji Holdings Corporation

Tetra Pak (Philippines), Inc.

The House Printers Corporation

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The National Grid Corporation of the Philippines issued yellow alerts for Luzon and Visayas, taking 5,137.2 MW offline and forcing converters to reschedule production

- April 2026: Meralco performed maintenance outages in key industrial parks, disrupting just-in-time deliveries for food processors.

- February 2026: Pulp benchmark reached USD 740 per ton, a six-month rise of 15%, triggering renegotiation of converter contracts.

- January 2026: The Bureau of Customs implemented excise-tax hikes on tobacco, accelerating demand for traceable folding cartons.

Philippines Folding Carton Market Report Scope

The scope of the report covers the analysis of the folding carton market in Philippines, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton market in Philippines.

The Philippines Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Philippine folding carton market, and how fast is it growing?

The Philippines folding carton market size stands at USD 410.78 million in 2026 and is forecast to reach USD 560.87 million by 2031, advancing at a 6.43% CAGR over the period (Mordor Intelligence).

Which material commands the largest share of folding carton demand in the Philippines?

Coated unbleached kraft led the 2025 market with 32.83% share owing to its strength and recyclability.

What printing technology is growing the fastest?

Digital printing is projected to post an 8.34% CAGR through 2031 as cloud kitchens and D2C brands request short-run, variable-data cartons.

How will proposed plastic excise taxes influence carton demand?

Taxes of up to PHP 150 per kg (USD 2.65) on single-use plastics will make paperboard alternatives more cost competitive, encouraging brand owners to adopt folding cartons for retail-ready packaging.

Which end-user segment offers the greatest growth upside?

E-commerce and retail-ready packaging is forecast to expand at a 7.96% CAGR to 2031, outpacing food, personal care, and pharmaceuticals.

What are the main challenges facing converters?

Volatile pulp prices, limited domestic fiber supply, intermittent power outages, and competition from flexible packaging all pressure converter margins and planning cycles.

Page last updated on: