Spain Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.98 Billion |

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Folding Carton Market Analysis by Mordor Intelligence

The Spain folding carton market size is projected to expand from USD 1.03 billion in 2026 to USD 1.33 billion by 2031, registering a 5.17% CAGR over 2026-2031. Robust volume gains are tied to the single-use-plastic ban that becomes enforceable in August 2026, stricter design-for-recycling grades, and rising recycled-content mandates. Brand owners are pivoting toward mono-material fiber solutions, prompting sustained substrate and capacity investments across the Spain folding carton market. Integrated converters with back-ward integration into cartonboard and automation advantages are widening cost and compliance gaps versus smaller rivals, while volatility in recovered-paper pricing and elevated freight costs are testing converter margins. E-commerce adoption and chilled ready-meal growth are further raising demand for shelf-ready and microwave-safe carton formats, positioning the Spain folding carton market as a resilient growth pocket within the broader European packaging landscape.

Key Report Takeaways

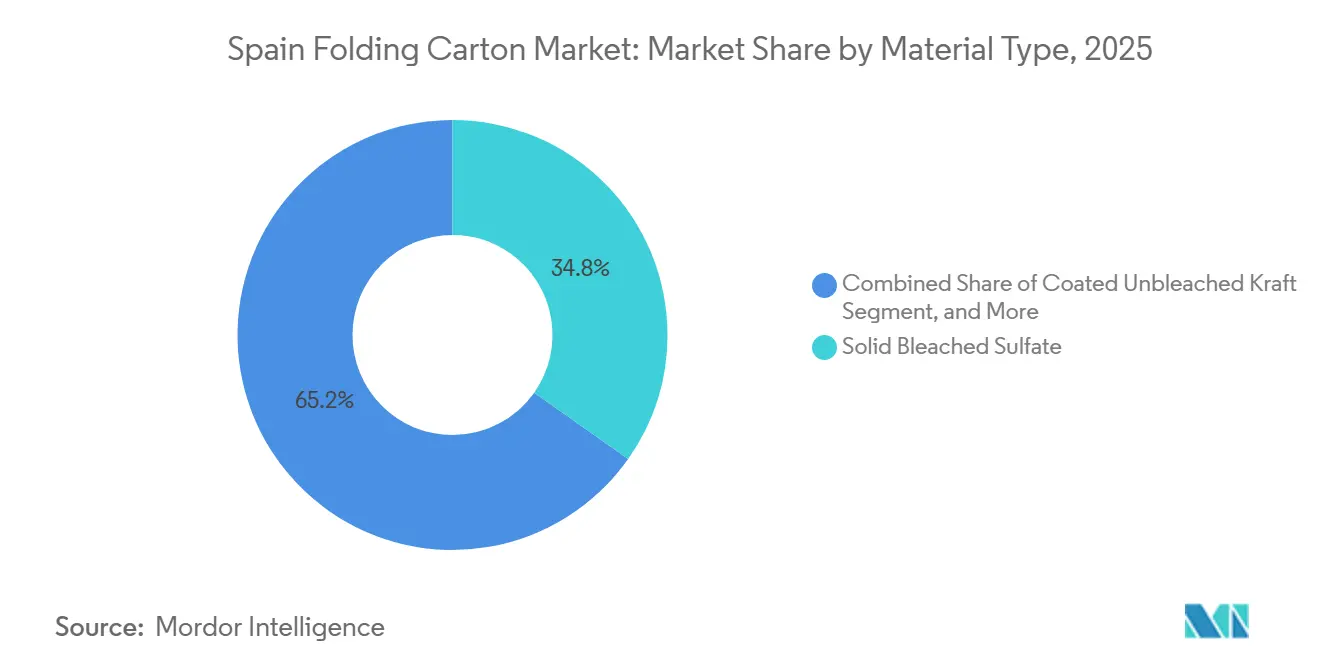

- By material type, solid bleached sulfate captured with 34.78% of the Spain folding carton market share in 2025.

- By printing technology, the Spain folding carton market size for digital platforms is projected to grow at a 6.73% CAGR to 2031.

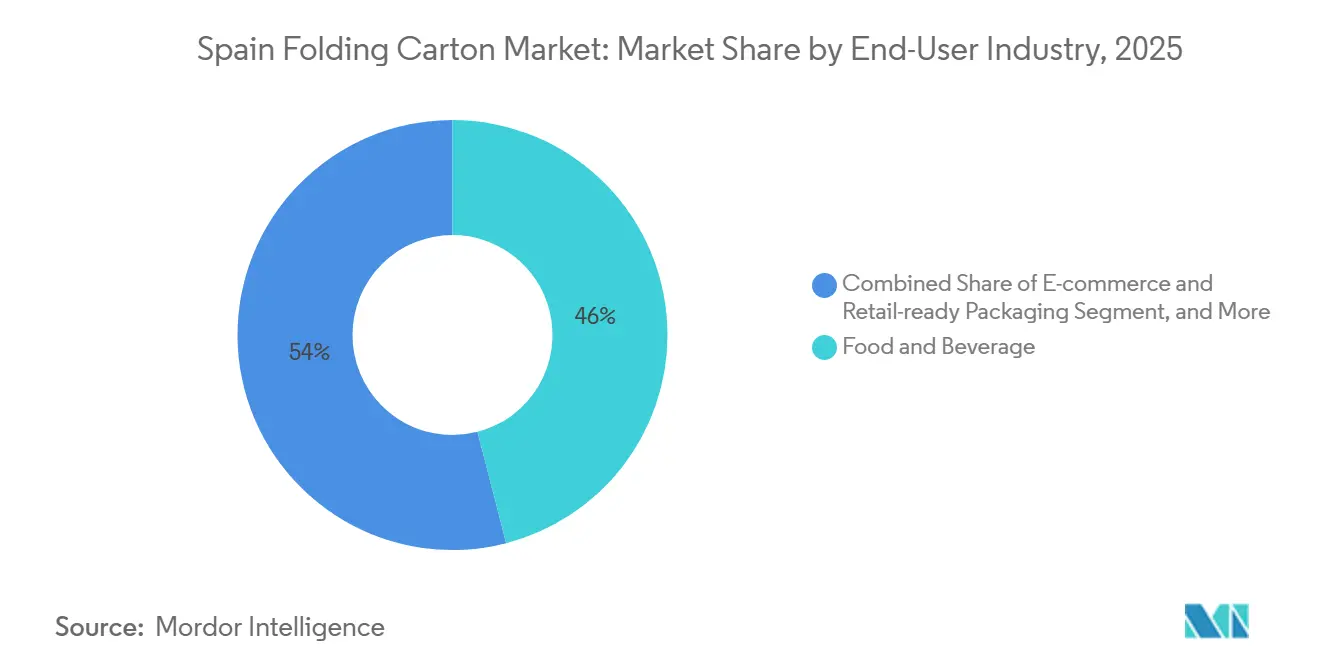

- By end-user industry, the food and beverage industry captured 45.98% of the Spain folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Packaging | +1.2% | National, Catalonia, Madrid, Valencia | Medium term (2-4 years) |

| Rising E-commerce Shipments Requiring Secondary Packaging | +0.9% | National, Barcelona, Madrid, Seville | Short term (≤ 2 years) |

| Stringent EU and Spanish Regulations on Single-Use Plastics | +0.8% | National, EU-wide compliance | Short term (≤ 2 years) |

| Cost Advantages of Lightweight Board for Logistics | +0.6% | National, export-oriented sectors | Medium term (2-4 years) |

| Rapid Expansion of Spain's Chilled Ready-Meals Segment | +0.7% | National, retail-concentrated regions | Medium term (2-4 years) |

| Digitization of Supply Chains Enabling Short Print Runs | +0.5% | National, pharmaceutical and cosmetics hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Packaging

Consumer preference for recyclable materials and retailer mandates are accelerating Spain’s shift toward fiber-based primary and secondary packs. The EU Packaging and Packaging Waste Regulation requires 35% post-consumer recycled content by 2030, pushing brand owners to redesign folding cartons for right-sized deliveries and to eliminate mixed-material barriers. Premium virgin-fiber grades such as ALASKA SMART and ALASKA KRAFT are marketed as lighter yet Braille-ready options that keep food-contact approvals intact. Upstream, coating start-ups like Papkot are securing capital to commercialize plastic-free barriers, signaling a deeper innovation cycle that reinforces the Spanish folding carton market’s sustainability narrative.[1]Fedrigoni Group, “FY 2024 Results,” fedrigoni.com

Rising E-commerce Shipments Requiring Secondary Packaging

Prepared-food volumes grew 7.6% in 2025, driving up retail-ready carton demand, particularly from Mercadona, whose ready-to-eat range expanded 24% and now reaches 40% shopper penetration. The EU regulation capping void space at 50% forces online merchants to replace corrugated shippers with compact folding cartons, spurring interest in integrated cushioning designs. Converters that can deliver rapid artwork changes through digital platforms are winning high-mix, low-volume contracts, as exemplified by Saica Fresh’s MAP-compatible carton solution launched in September 2025.

Stringent EU and Spanish Regulations on Single-Use Plastics

August 2026 is the hard stop for non-recyclable plastic food packs in Spain, with Royal Decree 1055/2022 adding disposal labeling, anti-greenwashing rules, and EPR fees that escalate when recyclability scores are low. Compliance audits by ENAC-accredited labs introduce fixed costs that smaller, more flexible converters struggle to absorb, accelerating share gains in the Spain folding carton market. Beverage DRS legislation, rolling out first in Barcelona and Madrid in November 2026, is expected to expand to composite packs by 2028, prompting early carton adoption among juice and dairy brands.

Cost Advantages of Lightweight Board for Logistics

Diesel averaged USD 1.37 per liter in Q1 2026, magnifying the logistics savings from lower-basis-weight boards. Smurfit WestRock’s kraftliner mills supply substrates that maintain compression strength at reduced grammage, enabling thinner retail cartons and freight cost relief. Equipment upgrades, such as ultrasonic strapping at Cartonajes Barco, cut energy use by up to 70% and strap consumption by 30%, reinforcing the business case for operational lightweighting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Recycled Paperboard Prices | -0.4% | National, EU-wide supply chains | Short term (≤ 2 years) |

| Competition from Flexible Packaging in Snack Formats | -0.3% | National, snack and confectionery sectors | Medium term (2-4 years) |

| Limited Domestic Hardwood Pulp Availability | -0.2% | National, import-dependent mills | Long term (≥ 4 years) |

| Brand Owner Reluctance Toward High-CapEx Digital Presses | -0.2% | National, mid-tier converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Recycled Paperboard Prices

April 2025 OCC spikes of EUR 20-30 per metric ton (USD 22-33 per metric ton) squeezed converter EBITDA, exposing the Spain folding carton market to upstream volatility. Declining office paper collection and geopolitical freight disruptions have tightened SOP supply, compelling mills to hedge by importing Scandinavian virgin fiber at higher freight premiums. This situation underscores the growing challenges in maintaining cost efficiency within the market.

Competition from Flexible Packaging in Snack Formats

Snack producers continue to favor stand-up pouches for nuts and confectionery, citing lower gram-per-pack costs and superior moisture barriers. Flexible suppliers are migrating to mono-material PE structures that now satisfy recyclability criteria, diluting cartonboard’s regulatory edge. Reusable PP trays for industrial glass transport, introduced by Cartonplast Ibérica, highlight alternative-material threats in B2B logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Virgin Fiber Consolidates Lead

Solid Bleached Sulfate held 34.78% of the Spain folding carton market share in 2025, a position secured by its white optics, odor neutrality, and pharmaceutical compliance credentials. The segment captures premium price points in cosmetics, confectionery, and blister folding cartons, cushioning converters against OCC price swings. Coated Unbleached Kraft is scaling fastest at a 7.34% CAGR through 2031, as organic food and artisan bakery brands adopt its natural-brown aesthetics and grease resistance. Folding Boxboard and White Line Chipboard satisfy high-volume frozen-food and cereal categories where cost efficiency prevails, even as regulatory recycled-content thresholds raise de-inking investments.

Large upstream projects, such as Stora Enso’s 750,000-metric ton PM6 rebuild, ensure a stable supply of coated grade for Spanish converters.[2]Stora Enso, “Oulu Mill PM6 Rebuild,” storaenso.com Coated specialty grades, micro-flute corrugated, and metalized boards serve luxury spirits and wine but face stricter demetallization requirements, slowing their momentum. The Spain folding carton market size for niche substrates remains modest, yet heightened demand for tamper-evident closures and smart-label integration is giving premium virgin fibers a defensible edge, particularly in high-growth GLP-1 therapy packaging.

By Printing Technology: Lithography Dominates, Digital Gains Strategic Relevance

Lithographic processes delivered 41.63% of the Spain folding carton market size in 2025 because they optimize cost per thousand impressions at run-lengths above 50,000. The method’s tight color tolerance meets cosmetic shelf appeal and pharmaceutical warning text clarity requirements. Digital printing, though less than 1% of national volume, is expanding at a 6.73% CAGR, driven by EU serialization, SKU proliferation, and the plate-less economics of sub-5,000-unit campaigns. Flexography remains relevant in kraftliner sleeves and shelf-ready carts that prioritize throughput over photo quality, while gravure remains confined to billion-unit cigarette cartons, though its share is in secular decline.

Digital adoption is uneven. Grupo La Plana’s EFI Nozomi and Kento Hybrid lines enable same-day artwork changes, supporting promotional refresh cycles aligned with Spanish supermarket flyers. Mid-tier converters often choose UV-LED retrofits to contain capex, delaying inkjet moves until press prices fall. De-inking compatibility debates may momentarily stall digital volumes, yet inkjet R&D from HP and EFI is closing recyclability gaps, ensuring long-term penetration across the Spain folding carton market.

By End-User Industry: Food Dominance, E-commerce Momentum

Food and Beverage accounted for 45.98% of the Spain folding carton market size in 2025, underpinned by fresh produce, frozen meals, and beverage multipacks. Chilled ready-meal volumes, especially at Mercadona, require grease-resistant dispersion coatings and MAP-compatible barriers, driving conversion from plastic trays to Coated Unbleached Kraft sleeves. E-commerce and Retail-ready Packaging is the fastest riser, expanding at a 7.05% CAGR, fueled by post-pandemic home dining and void-space restrictions that favor right-sized cartons.

Pharmaceutical demand is buoyant thanks to GLP-1 and biologics, with AEMPS serialization increasing variable-data carton requisites. Personal Care and Cosmetics adoption is shaped by compostability norms and anti-greenwashing rules that curb metalized windows in favor of embossed finishes. Electrical and Electronics packs are benefiting from e-commerce densification mandates, while tobacco remains a demand drag. Luxury wine and spirits volumes softened in late 2024 yet show signs of stabilization as tourist inflows rebound, presenting upside for premium SBS cartons.

Geography Analysis

Catalonia anchors the Spain folding carton market with dense converter clusters near Barcelona’s port, ample pharmaceutical manufacturing, and proximity to fresh-produce exporters. Saica’s Sant Esteve Sesrovires plant adds 45% national folding-carton capacity and supports rapid shifts away from flexible produce packs.[3]Alimarket, “Saica Pack and Grupo La Plana Investments,” alimarket.es Madrid’s central logistics role and high retailer concentration make it the primary market for retail-ready sleeves and promotional multipacks, with Mercadona dictating carton specifications through private-label dominance.

Valencia leverages its agribusiness links and houses Smurfit WestRock’s Ibi bag-in-box hub, supplying juice and olive oil brands targeting export channels. Regional compliance readiness diverges. Catalan converters lead on ENAC lab certification for recyclability testing, while Andalusian SMEs lag in capital expenditure schedules. Urban rollout of the beverage DRS favors early carton adoption in Barcelona and Madrid between 2026 and 2027, with rural implementations trailing into 2029.

When rail upgrades under Spain’s Recovery and Resilience Plan are set to be operational, inland mills grapple with elevated landed prices. This is largely due to freight corridors from the ports of Bilbao and Valencia, which play a pivotal role in determining the import costs of virgin fiber. These higher costs are expected to impact the competitiveness of inland mills in the short term. Which escalated costs are poised to affect the competitiveness of inland mills in the near future.

Competitive Landscape

70% of revenue is accounted for by 29 companies, indicating moderate concentration in the Spanish folding carton market. Integrated groups such as Smurfit WestRock and Saica Pack use a mill-to-converter model that protects them from OCC volatility and energy price spikes. Smurfit WestRock invested EUR 54 million (USD 57 million) to double Ibi bag-in-box output, capturing a share of the liquid-food market ahead of the plastic ban.

Saica’s EUR 100 million (USD 108 million) Sant Esteve greenfield site and EUR 17 million (USD 18.4 million) Amposta expansion champion fresh-produce and chilled-meal cartons, signaling a scale race. Mayr-Melnhof positions itself on specialty substrates and smart packaging know-how, supporting nineteen of the top twenty pharma firms. Its Fit-For-Future program yielded EUR 70 million (USD 75.6 million) in profit gains during 2025 and targets EUR 250 million (USD 270 million) by 2027, funding ongoing digitization and RFID pilots at Spanish plants.

Grupo La Plana leads in digital print agility, while Cartonplast Ibérica introduces reuse models that could divert some transport volume from single-use cartons.[4]Packnet, “Cartonplast Ibérica Inversiones,” packnet.es Mid-tier converters face capex dilemmas: adopt digital presses or double down on flexo and post-print enhancements. Regulatory complexity and fiber-sourcing audits accentuate fixed-cost burdens, nudging further consolidation. Entry barriers remain high, given ISO 14001, FSC, and ENAC laboratory requirements.

Spain Folding Carton Industry Leaders

Saica Pack SL

Stora Enso Oyj

Mayr-Melnhof Karton AG

Smurfit WestRock plc

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mayr-Melnhof reported FY 2025 consolidated sales of EUR 3,885.3 million (USD 4,215 million) with an adjusted operating margin of 5.0%. The Pharma and Healthcare division lifted Q4 2025 margin to 5.4%.

- February 2026: EU Packaging and Packaging Waste Regulation 2025/40 entered into force, triggering a countdown to August 2026 enforcement for recyclability grades and single-use-plastic bans.

- June 2025: Saica Pack opened its EUR 100 million (USD 108 million) Sant Esteve Sesrovires facility, adding 45% national folding-carton capacity and more than 100 jobs.

- May 2025: Saica Pack invested EUR 17 million (USD 18.4 million) to expand Amposta capacity 12%, aligned with Saica Fresh barrier-coated cartons for chilled meals.

Spain Folding Carton Market Report Scope

The Spain Folding Carton Market refers to the segment of the packaging industry that manufactures and applies folding cartons, paper-based packaging solutions. These cartons are extensively used across industries such as food and beverage, pharmaceuticals, personal care, and others due to their lightweight, recyclable properties, and ability to enhance branding while ensuring product protection. The scope of this study includes analyzing market trends, growth factors, challenges, and opportunities within the forecast period.

The Spain Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Spain folding carton market?

The Spain folding carton market size is estimated at USD 1.03 billion in 2026.

Which material type leads Spain’s folding-carton demand?

Solid Bleached Sulfate is the leading material, accounting for 34.78% of demand because of its printability and food-safety profile.

How fast is digital printing growing in Spanish folding cartons?

Digital printing is advancing at a 6.73% CAGR through 2031, driven by serialization and promotional short runs.

What regulation is reshaping Spanish folding-carton design?

EU Regulation 2025/40, enforceable from August 2026, mandates recyclability grades and bans many single-use plastics.

Which end-user segment is expanding quickest?

E-commerce and Retail-ready Packaging is the fastest segment, projected at a 7.05% CAGR thanks to ready-meal delivery growth.

How concentrated is Spain’s folding-carton supplier base?

The top 29 converters generate 70% of revenue, indicating moderate concentration with ongoing consolidation.

Page last updated on: