Cloud-Based VDI Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

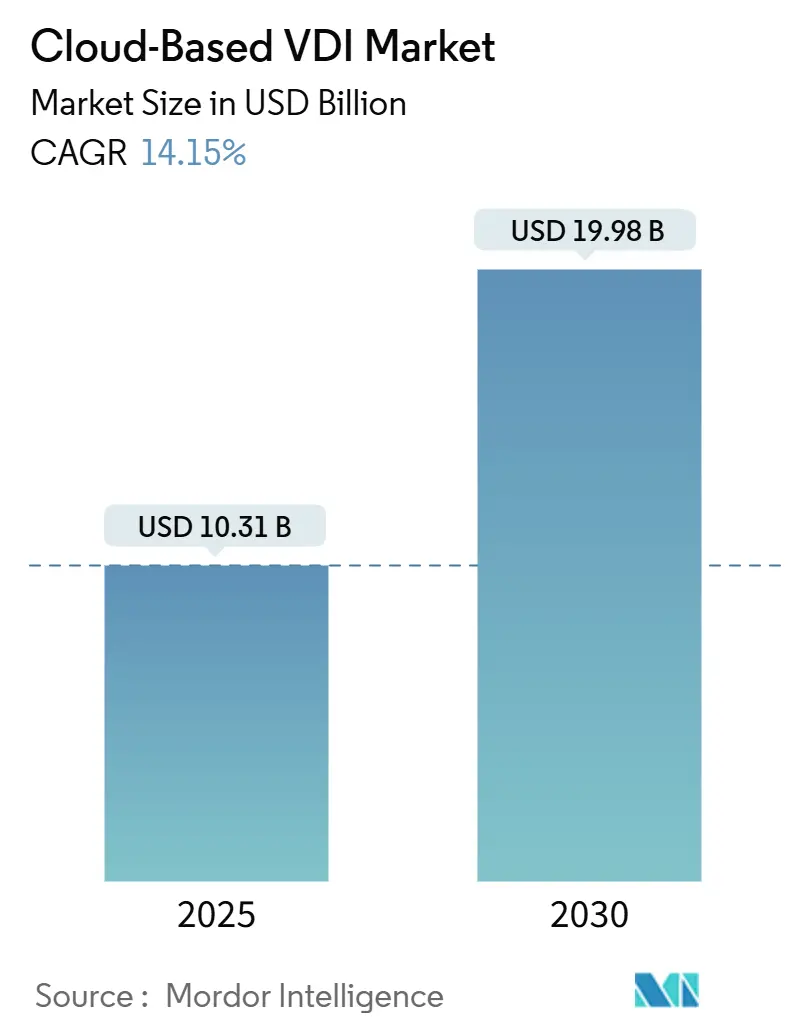

| Market Size (2025) | USD 10.31 Billion |

| Market Size (2030) | USD 19.98 Billion |

| Growth Rate (2025 - 2030) | 14.15% CAGR |

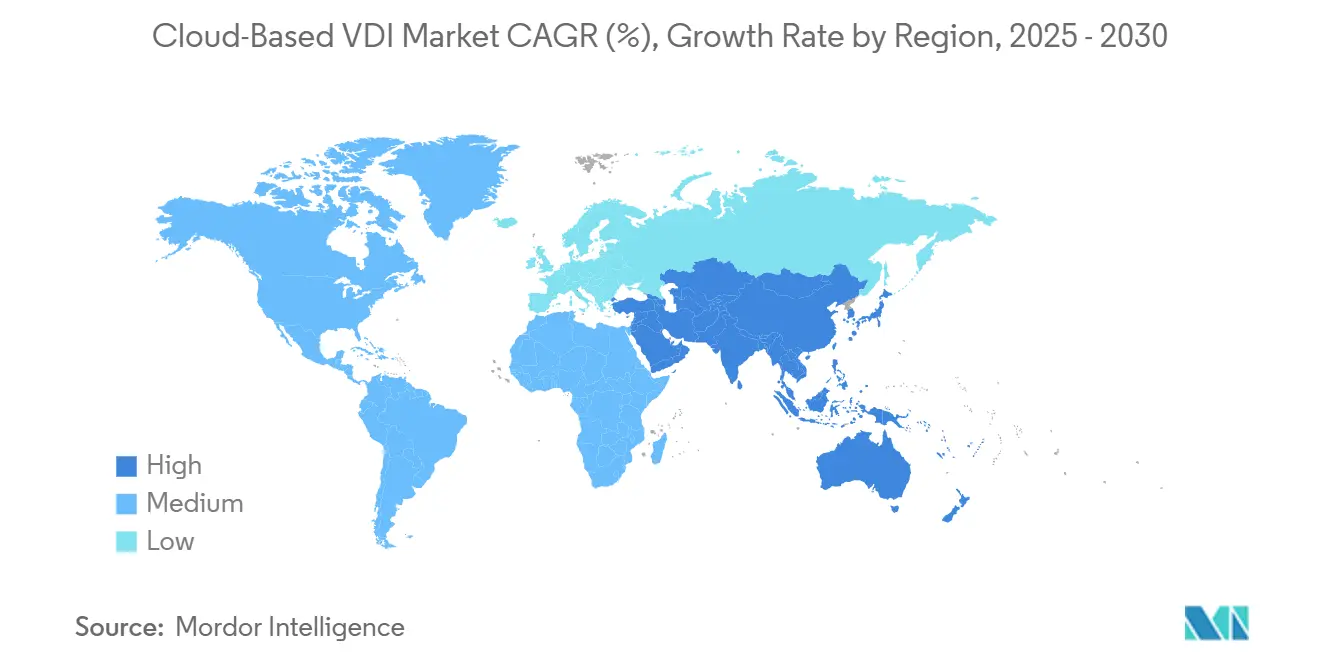

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

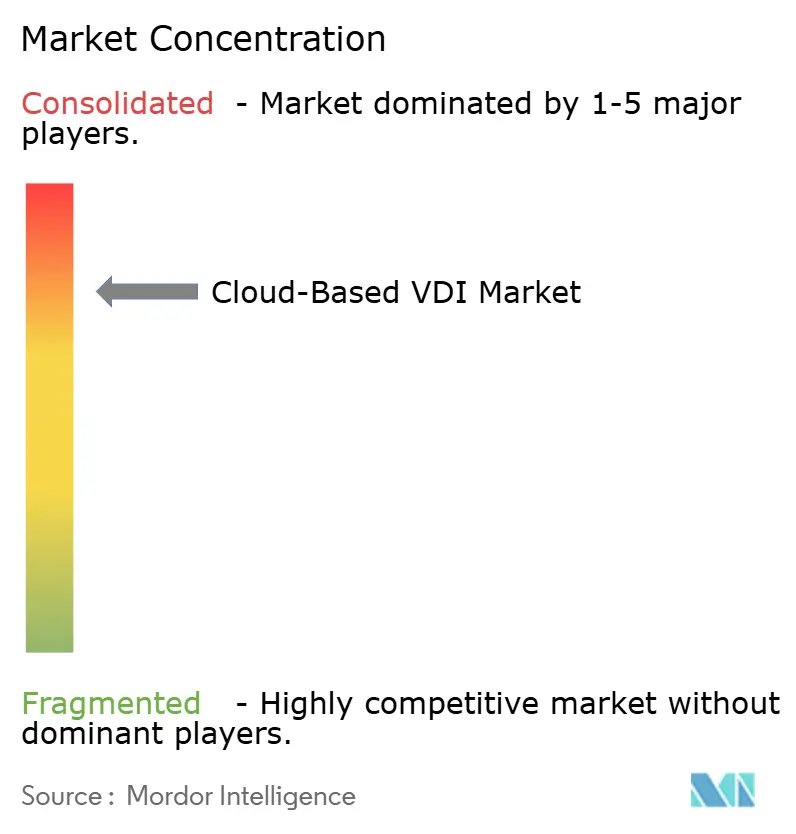

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-Based VDI Market Analysis by Mordor Intelligence

The Cloud-Based VDI Market size is estimated at USD 10.31 billion in 2025, and is expected to reach USD 19.98 billion by 2030, at a CAGR of 14.15% during the forecast period (2025-2030).

Momentum reflects the sweeping shift from on-premises virtualization to cloud-delivered desktops, propelled by hybrid-work normalization, zero-trust security mandates, and hyperscaler capital spending. Growing reliance on GPUs for graphics-dense workloads, rapid AI adoption for user-experience analytics, and region-specific data-sovereignty laws further shape demand. Intensifying competition among Microsoft Azure Virtual Desktop, Citrix DaaS, Amazon WorkSpaces, and Google Cloud’s ChromeOS Flex keeps pricing in check while accelerating feature innovation. Enterprises lean on non-persistent architectures to cut storage costs and reduce attack surfaces, and managed service providers broaden access for small and mid-sized firms, lifting the overall cloud-based VDI market trajectory.

Key Report Takeaways

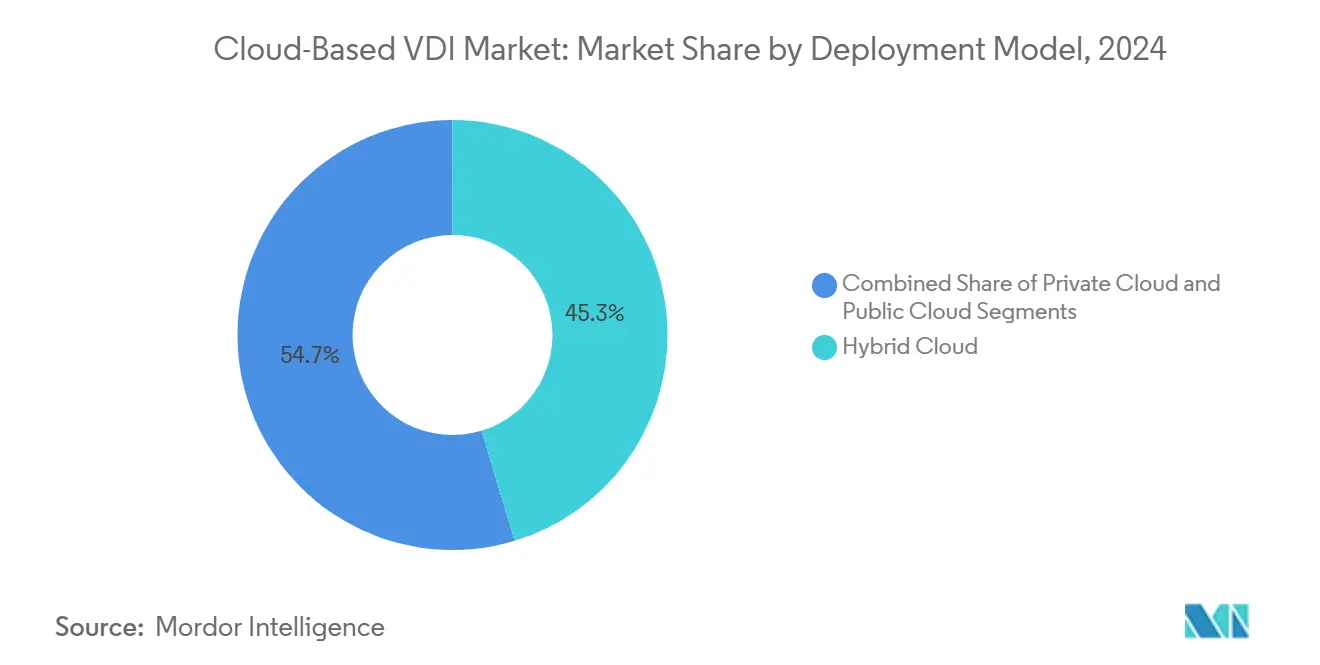

- By deployment model, hybrid cloud captured 45.32% of the cloud based VDI market share in 2024, while public cloud deployments are projected to advance at a 16.43% CAGR through 2030.

- By organization size, large enterprises accounted for 45.76% revenue share in 2024, whereas small and medium enterprises are expanding at a 16.71% CAGR to 2030.

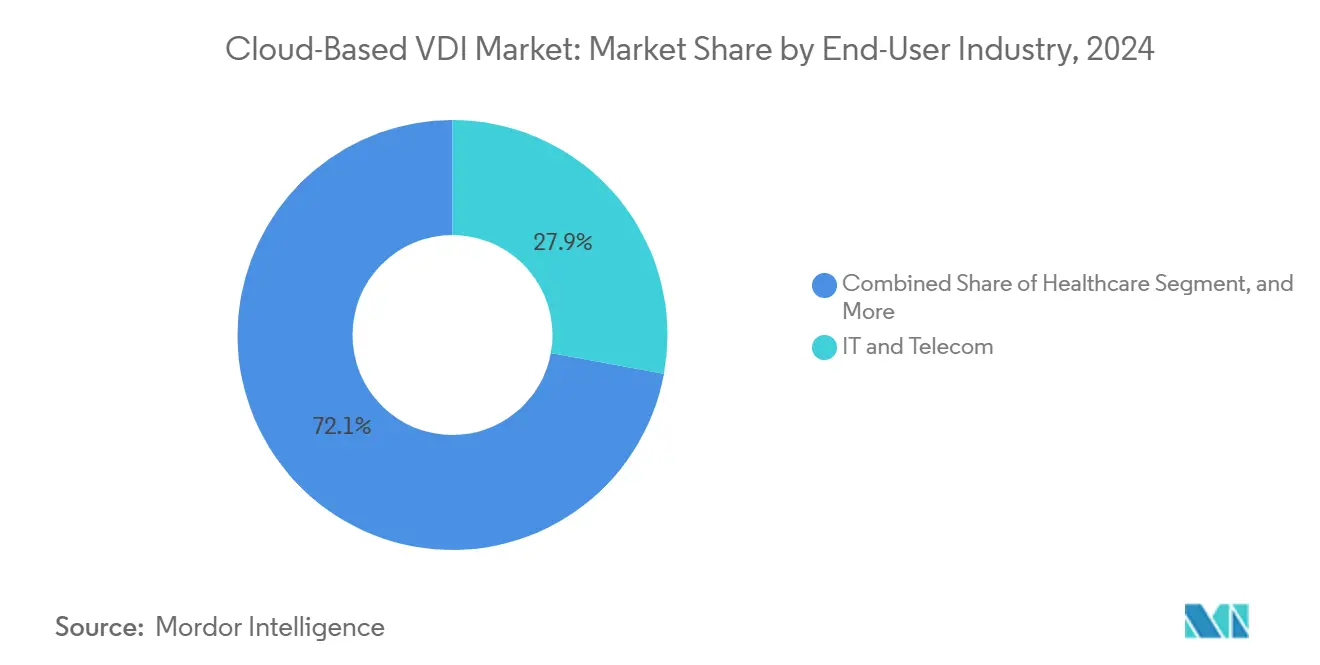

- By end-user industry, IT and telecommunications led with 27.89% revenue share in 2024, while healthcare is forecast to record the fastest 14.57% CAGR through 2030.

- By desktop persistence, non-persistent configurations commanded 59.93% share in 2024 and are also projected to post the highest 15.83% CAGR during the forecast period.

- By geography, North America led with 37.43% revenue share in 2024, whereas Asia-Pacific is poised to grow at a 14.82% CAGR through 2030.

Global Cloud-Based VDI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-work and BYOD proliferation | +3.2% | North America, Europe, scaling globally | Medium term (2-4 years) |

| Centralized cost-saving architecture | +2.8% | Global SMEs | Short term (≤ 2 years) |

| Hyperscaler scalability and global reach | +2.1% | Asia-Pacific, emerging markets | Medium term (2-4 years) |

| Security and compliance imperatives | +2.4% | Europe, healthcare verticals | Short term (≤ 2 years) |

| AI-driven user-experience analytics | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Edge-PoP GPU deployments | +1.3% | Urban manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid-work and BYOD proliferation

Corporate acceptance of hybrid work has turned secure anytime-anywhere desktop access into a baseline requirement. Hackensack Meridian Health migrated 31,000 employees to ChromeOS-based endpoints and Citrix DaaS, achieving sub-five-second logins while keeping PHI off devices. Similar rollouts at Bolton NHS cut login times to 2-3 seconds on thin clients and ensured diagnostic-image fidelity across 30 facilities. BYOD uptake complicates endpoint control, so vendors embed real-time device-posture checks and contextual authentication, broadening the addressable cloud based VDI market.

Centralized cost-saving architecture

Moving desktops to the cloud reduces refresh cycles, trims local IT headcount, and slashes energy use. Gateway Technical College’s pivot from an ailing on-prem VMware environment to V2 Cloud cut support tickets tenfold and freed staff for strategic work. [1]V2 Cloud Solutions, “Gateway Technical College Customer Story,” v2cloud.com St. Joseph’s Health now supports up to 1,800 concurrent Citrix sessions on 200 servers managed by a two-person team, evidencing the opex efficiencies feeding cloud-based VDI market growth. Annual power savings also reinforce sustainability targets, strengthening the business case.

Hyperscaler scalability and global reach

Microsoft earmarked USD 80 billion for AI-ready datacenters in 2025, expanding Azure regions that host Azure Virtual Desktop. Southern District Health Board tapped Citrix Cloud to stage workloads close to clinicians while meeting New Zealand data-residency rules. Public-cloud footprint expansion lowers latency, enables burst capacity, and brings GPU instances near edge users, widening the cloud based VDI market addressable base.

Security and compliance imperatives

Ransomware spikes and stringent privacy laws push organizations toward centrally governed desktops. Citrix’s 2024 acquisitions of deviceTRUST and Strong Network layered real-time posture analysis and secure developer workspaces onto its platform. Opava Psychiatric Hospital employs Citrix watermarking and encrypted channels to safeguard patient data across 20 buildings. Better audit trails and zero-trust alignment fuel confidence in the cloud-based VDI industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bandwidth and latency constraints | -2.1% | Rural and developing regions | Medium term (2-4 years) |

| Opex sticker-shock vs. amortized CapEx | -1.8% | Cost-sensitive SMEs worldwide | Short term (≤ 2 years) |

| Data-residency / sovereignty mandates | -1.5% | Europe, ASEAN, regulated industries | Medium term (2-4 years) |

| Proprietary protocol vendor lock-in | -1.2% | Global enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bandwidth and latency constraints

High-definition streaming desktops falter on sub-optimal links. Edge appliances with local GPU cache help, yet rural broadband rollouts lag. Users subject to jitter report productivity dips, curbing some cloud-based VDI market adoption. Vendors now embed adaptive codecs and predictive pre-fetching, but last-mile upgrades remain critical.

Opex sticker-shock vs. amortized CapEx

Subscription invoices can exceed depreciation schedules on legacy hardware. After Broadcom’s VMware license resets, some firms faced 3-6× cost jumps and shifted to Citrix or open platforms. Total-cost models that factor in power, space, and staff savings mitigate concern, yet sticker shock temporarily slows migrations among budget-tight SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Strategies Drive Flexibility

Hybrid implementations captured 45.32% of the cloud-based VDI market in 2024 as firms fused on-prem compliance with public-cloud elasticity. Southern District Health Board blended local datacenters with Citrix Cloud to maintain sovereignty while staging future Azure expansions. Public-cloud services are accelerating at 16.43% CAGR, supported by Microsoft’s AI datacenter surge and Citrix DaaS for Amazon WorkSpaces Core launch. Private-cloud remains critical for sensitive workloads-Opava Psychiatric Hospital hosts Citrix in its own datacenter to maintain full data control.

Public-cloud momentum stems from region launches, flat-rate GPU instances, and ISO/FedRAMP certifications. The cloud based VDI market size for public deployments is forecast to add more than USD 4 billion between 2025-2030. Vendor alliances-Citrix-Microsoft’s eight-year pact and NetApp’s CloudJumper buy-simplify lift-and-shift paths. Hybrid flexibility ensures business continuity, explaining why enterprises allocate fresh budgets toward multi-cloud VDI orchestration.

By Organization Size: SME Uptake Redefines Demand

Large enterprises retained 45.76% revenue share, underpinned by rollouts like Hackensack Meridian Health’s 17-hospital deployment. Yet SMEs are the fastest risers at 16.71% CAGR, benefiting from managed service models that remove architectural complexity. Foundation IT leveraged Parallels RAS to serve remote engineers without full-time VDI admins. [2]Parallels International, “Foundation IT Case Study,” parallels.com

Lower entry costs, consumption-based billing, and browser-only clients shrink onboarding hurdles, broadening the cloud-based VDI market. Vendors launch migration incentives targeting post-VMware-license sticker shock. MSPs bundle security, backup, and monitoring, positioning the cloud-based VDI industry as an attainable tool for 50-seat firms, not just global conglomerates.

By End-User Industry: Healthcare Accelerates Digital Care

IT and telecom accounted for 27.89% revenue, capitalizing on rapid application testing and secure developer sandboxes. Healthcare, however, is projected to outpace all sectors with a 14.57% CAGR to 2030. Queensland Health integrates Pexip video with Citrix desktops to enable virtual consults under HIPAA-aligned security. Bolton NHS’s thin-client rollout delivered image fidelity for radiology and cut energy waste.

Telemedicine, e-prescription portals, and 24/7 clinician mobility push hospitals toward cloud-based VDI market adoption. Anunta’s 1,500-seat deployment for a medical BPO confirmed the scalability of secure virtual clinics. [3]Anunta Technology, “Scaling 1,500 Virtual Desktops,” anuntatech.com Retail, manufacturing, and education continue steady uptake for graphics design stations, quality assurance dashboards, and hybrid classrooms.

By Desktop Persistence: Stateless Wins on Security

Non-persistent images held a 59.93% share and will sustain a 15.83% CAGR. Stateless desktops vanish at logoff, aligning with zero-trust and GDPR. Opava Psychiatric Hospital’s memory-only instances limit breach blast radius. Centralized golden images lower patch overhead, fueling the cloud-based VDI market.

Persistent desktops remain for engineers needing local CAD caches or creatives relying on personalized plug-ins. Storage deduplication and user-environment management ease cost pain, yet security-first boards increasingly default to non-persistent pools for mainstream staff. Hybrid mixes of both models are emerging as best practice.

Geography Analysis

North America commanded 37.43% of 2024 revenue on the back of mature hybrid-work norms, deep hyperscaler presence, and aggressive zero-trust adoption. Healthcare giants like Hackensack Meridian Health showcase multi-cloud, multi-vendor orchestration at scale. Federal and state mandates around data protection also sharpen demand.

Asia-Pacific registers the fastest 14.82% CAGR to 2030. Hyperscalers opened new regions in India, Indonesia, and New Zealand, easing data-localization obstacles. Southern District Health Board’s low-latency Citrix Cloud rollout exemplifies compliance-aware architecture. Nevertheless, differing ASEAN data-residency statutes force vendors to offer granular location controls, nudging further hybrid designs.

Europe shows steady growth, boosted by GDPR. Thin-client energy savings resonate in carbon-reduction strategies, as evidenced by Bolton NHS. Middle East and Africa and South America are nascent but rising; national 5G deployments and public-sector digitization plans spur pilot VDI proofs of concept. Economic headwinds and patchy connectivity temper full-scale conversions, yet managed services help bypass capex, widening the cloud-based VDI market footprint.

Competitive Landscape

Competition is moderate. Microsoft, Amazon, Google, and Citrix collectively hold a sizable slice, yet emerging vendors differentiate via vertical specialization and edge computing. Citrix’s 2025 acquisition of Unicon added 2.5 million eLux endpoints, deepening endpoint control. KKR’s purchase of VMware’s EUC unit resets strategy for Horizon Cloud under new ownership.

Investment in AI telemetry is the new arms race. Microsoft placed USD 80 billion into AI datacenters, driving low-latency analytics for Azure Virtual Desktop. Citrix couples deviceTRUST and a Strong Network to extend zero-trust out to the code repository. NetApp’s CloudJumper buy pushes storage giants into the cloud-based VDI industry.

Channel alliances also intensify. Scale Computing teamed with Leostream to ship turnkey VDI clusters installable in under four hours. Apporto joined the IGEL Ready program for browser-first classrooms. Price competition stays balanced as vendors counter VMware pricing shifts by touting predictable flat-rate compute.

Cloud-Based VDI Industry Leaders

Broadcom Inc.

Citrix Systems, Inc.

Microsoft Corporation

Amazon Web Services, Inc.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ZEDEDA integrated NVIDIA Jetson support for edge-AI desktops.

- January 2025: Citrix closed its Unicon buy, adding eLux endpoint OS.

- December 2024: Citrix acquired deviceTRUST and Strong Network to bolster zero-trust.

- November 2024: Citrix DaaS launched for Amazon WorkSpaces Core with fixed pricing.

Global Cloud-Based VDI Market Report Scope

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecom |

| BFSI |

| Healthcare |

| Education |

| Government and Public Sector |

| Manufacturing |

| Retail and E-commerce |

| Other End-User Industry |

| Persistent VDI |

| Non-Persistent VDI |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare | |||

| Education | |||

| Government and Public Sector | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Other End-User Industry | |||

| By Desktop Persistence | Persistent VDI | ||

| Non-Persistent VDI | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How big is the cloud-based VDI market today?

The cloud-based VDI market size reached USD 10.31 billion in 2025 and is projected to nearly double to USD 19.98 billion by 2030.

What CAGR is expected for cloud VDI through 2030?

A 14.15% CAGR is forecast for the period 2025-2030, driven by hybrid work, zero-trust mandates, and hyperscaler expansion.

Which deployment model is growing the fastest?

Public-cloud VDI leads with a 16.43% CAGR thanks to new regional datacenters and fixed-price GPU instances.

Why is healthcare adopting cloud VDI so quickly?

Telemedicine, 24/7 clinician mobility, and strict compliance needs push hospitals to stateless, centrally managed desktops.

What is the main restraint to broader VDI adoption?

Limited bandwidth in rural zones and subscription cost shock for SMEs remain the largest hurdles, though mitigations are improving.

Who are the leading vendors?

Microsoft, Citrix, Amazon, and Google hold prominent positions, with NetApp, Scale Computing, Apporto, and others expanding via niche strategies.

Page last updated on: