Distributed Cloud Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

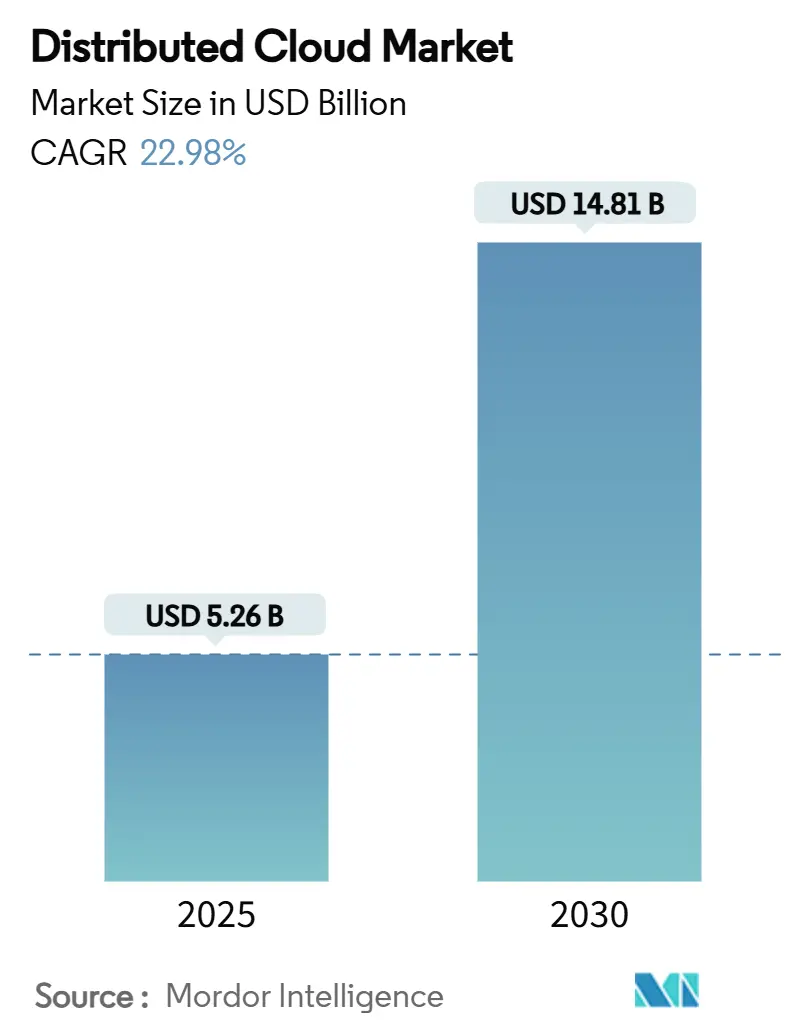

| Market Size (2025) | USD 5.26 Billion |

| Market Size (2030) | USD 14.81 Billion |

| Growth Rate (2025 - 2030) | 22.98% CAGR |

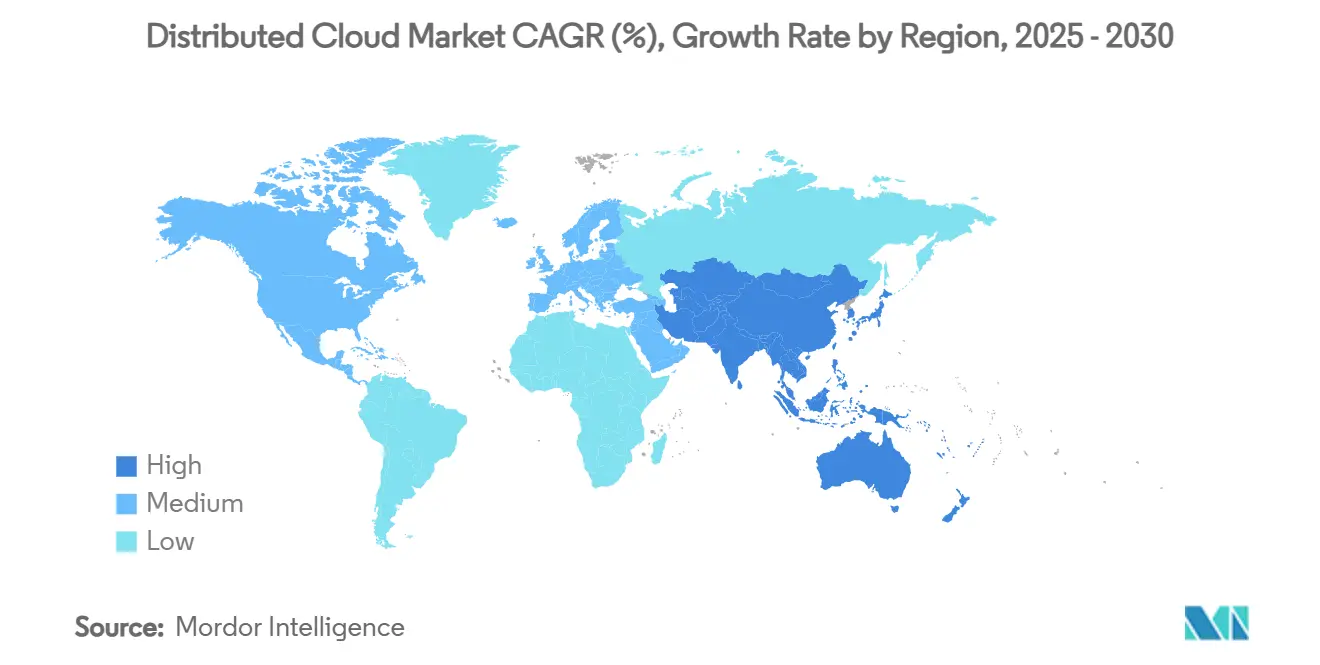

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Distributed Cloud Market Analysis by Mordor Intelligence

The distributed cloud market size stands at USD 5.26 billion in 2025 and is forecast to expand to USD 14.81 billion by 2030, translating into a 22.98% CAGR. Broader adoption is anchored in the shift toward edge-native architectures that process data near where it is generated, a necessity for latency-sensitive IoT, 5G and AI workloads. Strong regulatory pressure for data-sovereignty compliance, along with rising cloud egress fees, drives enterprises toward hybrid-IT operating models that mix core, regional and edge nodes for optimal cost–performance balance. Intensifying competition among hyperscalers and infrastructure specialists accelerates product innovation, while modular subscription pricing lowers entry barriers for small and medium enterprises (SMEs). These trends collectively sustain robust investment momentum in the distributed cloud market, positioning it as a foundational layer for Industry 4.0, intelligent retail and smart-health initiatives.

Key Report Takeaways

- By deployment model, provider-managed offerings captured 63.71% of distributed cloud market share in 2024; edge-managed services are advancing at 24.71% CAGR through 2030.

- By organisation size, large enterprises held 56.31% of the distributed cloud market size in 2024, while SMEs are expanding at 23.45% CAGR to 2030.

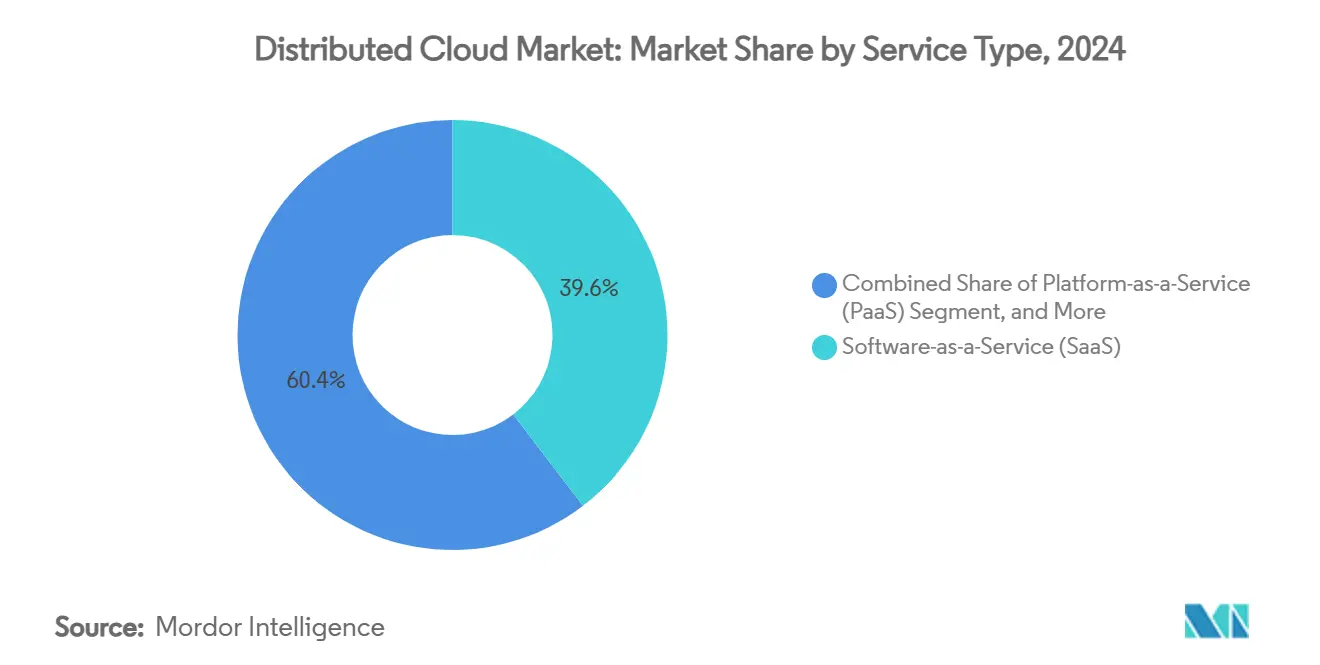

- By service type, Software-as-a-Service secured 39.61% revenue share in 2024; Infrastructure-as-a-Service is projected to grow at 25.64% CAGR through 2030.

- By industry vertical, IT and telecom accounted for 25.97% share of the distributed cloud market size in 2024, whereas healthcare and life sciences are forecast to progress at 24.91% CAGR to 2030.

- By geography, North America led with 37.69% revenue share in 2024; Asia-Pacific is expected to chart the fastest expansion at 26.73% CAGR through 2030.

Global Distributed Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of latency-sensitive edge workloads in IoT and 5G | +4.2% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Need for data-sovereignty compliance | +3.8% | Europe, APAC core, with regulatory spill-over to MEA | Long term (≥ 4 years) |

| Cost optimisation via hybrid-IT and lower egress fees | +3.1% | Global, particularly cost-sensitive SME segments | Short term (≤ 2 years) |

| Distributed AI model training across multi-region GPU clusters | +4.7% | North America, Europe, China, with emerging adoption in India | Medium term (2-4 years) |

| Rise of collaborative multi-cloud orchestration toolchains | +2.9% | Global enterprise segments, led by North America and Europe | Long term (≥ 4 years) |

| Monetisation of idle on-prem compute via federated exchanges | +2.1% | Developed markets with mature IT infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Latency-Sensitive Edge Workloads in IoT and 5G

Semiconductor manufacturers deploy private 5G networks to achieve sub-10 millisecond response times for autonomous production lines, underscoring why distributed cloud market adoption is pivotal for real-time analytics and machine vision.[1]Manufacturers Alliance, “Why Semiconductor Manufacturer Chose 5G for New Factory,” manufacturersalliance.org Factory-floor data streaming through Google Cloud’s Manufacturing Data Engine cuts deployment cycles from weeks to hours while maintaining audit-grade security.[2]Google Cloud, “Manufacturing Data Engine,” cloud.google.com Telecom operators also monetise edge footprints; CelcomDigi shortened new service roll-outs by 95% via AWS edge nodes, proving that distributed architectures deliver measurable agility benefits. These operational wins reinforce executive confidence and advance capital allocation toward distributed edge build-outs across manufacturing, retail and transport.

Need for Data-Sovereignty Compliance

Singapore’s Infocomm Media Development Authority released guidelines in February 2025 that prioritise resilient, compartmentalised cloud deployments, directly bolstering distributed cloud market demand. The Asia Cloud Computing Association warns that conflicting legislation across 14 economies stalls cross-border data flow, hence regulated enterprises view geo-fenced edge nodes as a compliance accelerator. Europe’s forthcoming Digital Operational Resiliency Act amplifies a similar shift, encouraging regional processing centers that integrate seamlessly with global hyperscale cores. Organizations consequently reassess architecture roadmaps to ensure every workload has a clearly defined residency domain.

Cost Optimisation via Hybrid-IT and Lower Egress Fees

A Ugandan banking cohort achieved 15–20% annual IT savings after migrating critical workloads to distributed nodes; every 1% migration step correlated with a 0.4-unit cost reduction. Cisco and Equinix have responded with pay-as-you-go middle-mile networking that aligns expenditure with episodic demand and pushes distributed cloud market economics further in favour of SMEs.[3]Cisco, “Cisco Streamlines Middle-Mile Networking with Pay-As-You-Go,” blogs.cisco.com Processing data locally dramatically shrinks egress traffic, allowing CFOs to redeploy savings toward innovation budgets rather than overhead.

Distributed AI Model Training Across Multi-Region GPU Clusters

Enterprises face GPU scarcity and soaring training costs; distributed architectures that schedule workloads across multiple regions unlock idle capacity and accelerate iteration cycles. Techniques such as low-communication training cut gradient exchange frequency, trimming network costs by double digits while preserving accuracy. Aramco’s collaboration with Microsoft and Armada operationalised the first industrial distributed cloud, enabling AI-driven safety analytics across remote oil fields through edge data centers. Healthcare pioneers adopt federated learning to refine models without moving patient data off-site, as illustrated by Kakao Healthcare’s multi-hospital breast-cancer initiative. These proofs validate distributed AI at scale and broaden the use-case portfolio for the distributed cloud market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded cyber-attack surface in dispersed nodes | -2.8% | Global, with heightened concerns in regulated sectors | Short term (≤ 2 years) |

| Governance and observability complexity | -2.1% | Enterprise segments globally, particularly in North America and Europe | Medium term (2-4 years) |

| Shortage of edge-site skilled workforce | -1.9% | Global, with acute shortages in North America and developed APAC markets | Long term (≥ 4 years) |

| Carbon-accounting gaps across heterogeneous nodes | -1.4% | Europe and North America leading sustainability mandates, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanded Cyber-Attack Surface in Dispersed Nodes

Each edge instance represents a discrete threat vector yet often lacks the compute headroom for sophisticated intrusion detection, magnifying vulnerability across sprawling footprints. Researchers note that a breach at one site can cascade laterally through poorly segmented overlays. The United States has 700,000 unfilled cyber-security roles, producing an immediate talent bottleneck for distributed deployments. Boards therefore rank edge-specific security investment and managed detection services as critical mitigations, even though the added controls inflate near-term operating spend.

Governance and Observability Complexity

Heterogeneous hardware stacks across retail outlets, cell towers and micro-data centers complicate uniform policy enforcement. Carbon reporting, incident response and software patch orchestration demand unified dashboards that many enterprises still lack. IBM’s sovereign cloud framework promotes integrated controls yet reiterates that distributed paradigms require above-average DevSecOps maturity. Frequent tool fragmentation drives CIOs toward vendor-managed solutions despite the desire for bespoke configurations, tempering some cost-savings momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Provider-Managed Dominance Faces Edge Disruption

Provider-managed configurations held 63.71% of distributed cloud market share in 2024 as organisations prioritised turnkey orchestration and 24×7 support. This status quo is increasingly contested by edge-managed frameworks forecast to grow 24.71% CAGR, propelled by real-time manufacturing, retail point-of-sale and telco-core demands. Microsoft’s Azure Local demonstrates how centrally controlled services can be projected into branch sites to satisfy low-latency targets while retaining uniform governance. Over the outlook, hybrid patterns-mixing managed and self-directed nodes-are likely to reshape procurement criteria as buyers weigh agility versus autonomy.

Self-managed deployments remain niche, supported by digitally mature conglomerates that possess in-house Site Reliability Engineering (SRE) teams. Such adopters often cite proprietary compliance or algorithmic IP as reasons to retain full stack control. The distributed cloud market sees these capabilities converging into unified control planes that allow workload-level policy choices, suggesting interoperability rather than exclusivity will define future architectural blueprints.

By Organisation Size: SMEs Drive Democratisation Through Accessible Platforms

Large companies captured 56.31% of distributed cloud market size in 2024, leveraging global footprints to align production, disaster recovery and data-residency goals across continents. Their enterprise agreements with multiple hyperscalers often include volume discounts and co-innovation labs. SMEs, however, are set to outpace with 23.45% CAGR as low-code and AI-assisted DevOps slash onboarding complexity. Consumption-based billing, free tier credits and regional marketplace ecosystems increasingly remove capital hurdles previously faced by smaller firms.

Start-ups benefit from edge services packaged as plug-and-play stacks that integrate payment, telemetry and security out of the box. Municipal utilities, boutique retailers and telehealth clinics now stand up compliant edge nodes within hours, a dynamic that broadens total addressable demand and cements the distributed cloud market as an equaliser across company sizes.

By Service Type: IaaS Acceleration Challenges SaaS Supremacy

Software-as-a-Service sustained 39.61% revenue leadership in 2024 because it delivers immediate productivity with minimal configuration. Yet Infrastructure-as-a-Service is projected to vault ahead at 25.64% CAGR through 2030, largely due to containerised microservices and data-intensive AI pipelines that require bespoke GPU, FPGA or DPU instances. The distributed cloud market size for IaaS-backed deployments is expected to exceed USD 8 billion by 2030, underscoring the swing toward infrastructure flexibility.

Platform-as-a-Service and Function-as-a-Service unlock faster code release cycles but face developer hesitation around cold-start latency at micro-sites. Edge Services, a nascent category, packages network acceleration, AI inferencing and local storage to satisfy sub-20 millisecond thresholds. Interoperability between these service types will matter more than rigid taxonomy as vendors converge offerings to deliver unified developer experiences within the distributed cloud market.

By Industry Vertical: Healthcare Acceleration Transforms Medical Data Processing

IT and telecom retained 25.97% share of distributed cloud market size in 2024, driven by 5G core virtualisation, content delivery and network slicing. Healthcare is forecast to grow 24.91% CAGR, propelled by imaging analytics, hospital-at-home services and federated learning that keeps patient data in-country. Distributed nodes inside radiology departments enable instant inferencing while offloading bulk archival to regional hubs.

Manufacturing utilises predictive maintenance and automated quality inspection, while BFSI leverages geo-specific nodes to satisfy stringent residency rules. Retail experiments with computer-vision-enabled checkout and dynamic pricing that need edge responsiveness to uphold customer experience. Government smart-city pilots deploy traffic optimisation and public safety analytics atop sovereign cloud stacks, illustrating cross-sector reliance on distributed designs.

Geography Analysis

North America commanded 37.69% revenue share in 2024, anchored by mature data-center penetration, early 5G roll-out and sophisticated enterprise digital strategies. AWS committed more than USD 1 billion in new partnerships to proliferate Outposts and Local Zones, ensuring diverse industries can meet sub-single-digit latency demands. Federal programmes that address cyber-skills gaps and critical-infrastructure resilience offer policy support, enhancing the distributed cloud market’s commercial sustainability.

Asia-Pacific is advancing at 26.73% CAGR, buoyed by over USD 15 billion in new data-center investment. Singapore surpassed its 70% cloud migration target by moving more than 80% of government systems to cloud, demonstrating public-sector proof at scale. The Asian Development Bank forecasts cloud-first strategies could lift regional GDP by up to 0.7 percentage points by 2028, creating a virtuous cycle for distributed cloud market demand.

Europe emphasises sovereignty and compliance, stimulating hybrid architectures with in-region processing enclaves. South America and the Middle East & Africa remain emerging yet dynamic; Saudi Arabia’s USD 1.5 billion (USD 1.5 billion) Oracle cloud investment underscores state-backed commitment to diversified digital economies. Regional carriers and energy majors increasingly partner with hyperscalers to co-locate edge infrastructure, accelerating the global diffusion of distributed best practices.

Competitive Landscape

The distributed cloud market is moderately fragmented. AWS, Microsoft and Google combine hyperscale footprints with partner ecosystems to deliver turnkey edge plus core solutions. Each extends proprietary operating models-Outposts, Azure Arc, Anthos-into telco points-of-presence and enterprise campuses. Equinix leverages interconnection hubs and global platform reach to bundle colocation with sovereign cloud zones, while VMware, now backed by Broadcom, positions Cloud Foundation as a private-cloud control plane integrated natively with public services.

Strategic alliances form a keystone of competitive play. AWS collaborates with Booz Allen to tailor secure government workloads; Kyndryl pairs with Databricks to streamline AI pipelines; IBM introduces multizone regions for regulated clients. Edge specialists such as Cloudflare, Akamai, and Vapor IO target microsecond content delivery and 5G offload, carving a niche in latency-critical applications. Sovereign providers in Europe and Asia differentiate via compliance certifications, giving regulated entities alternative sourcing options without sacrificing cloud-native elasticity.

Capital allocation trends confirm rising entry barriers. Leaders commit multibillion-dollar sums to expand GPU capacity, renewable energy sourcing and liquid-cooling technologies, placing smaller rivals under scale pressure. However, vertical-specific solution stacks-industrial AI, healthcare diagnostics, energy asset management-offer pathways for specialists to insert high-value services on top of shared infrastructure.

Distributed Cloud Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FairPrice Group partnered with Google Cloud to launch its Store of Tomorrow, integrating cloud-connected carts and AI operations portals to elevate in-store analytics. The strategy reinforces Google’s retail vertical focus and demonstrates a tangible edge use-case that validates distributed architectures in high-footfall environments.

- June 2025: Kyndryl entered a global alliance with Databricks to modernise enterprise data estates. The deal combines Kyndryl’s managed services with Databricks’ Lakehouse platform, positioning both to capture AI-driven migrations in the distributed cloud market.

- May 2025: IBM Cloud unveiled new GPU partnerships and sovereign cloud regions, a move that aligns its portfolio with rising AI demand and regulatory scrutiny, thereby strengthening stickiness among compliance-sensitive clients.

- March 2025: Singapore’s IMDA issued comprehensive cloud guidelines that prioritise resilience and security, effectively endorsing distributed topologies over monolithic data-centers. Providers will need to align service blueprints with these national benchmarks to partake in public-sector contracts.

Global Distributed Cloud Market Report Scope

| Self-Managed Distributed Cloud |

| Provider-Managed Distributed Cloud |

| Edge-Managed Distributed Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Function-as-a-Service (FaaS) |

| Edge Services |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and eCommerce |

| Government and Public Sector |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Turkey | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Deployment Model | Self-Managed Distributed Cloud | ||

| Provider-Managed Distributed Cloud | |||

| Edge-Managed Distributed Cloud | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Service Type | Infrastructure-as-a-Service (IaaS) | ||

| Platform-as-a-Service (PaaS) | |||

| Software-as-a-Service (SaaS) | |||

| Function-as-a-Service (FaaS) | |||

| Edge Services | |||

| By Industry Vertical | IT and Telecom | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and eCommerce | |||

| Government and Public Sector | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Turkey | |||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected revenue for distributed cloud solutions by 2030?

The distributed cloud market is forecast to reach USD 14.81 billion by 2030, driven by a 22.98% CAGR across edge, core and hybrid deployments.

How are enterprises using distributed cloud to meet data-sovereignty rules?

Organisations place edge nodes within national borders to process regulated data locally while linking non-sensitive workloads to global regions, aligning with Singapore IMDA and EU DORA requirements.

Which service layer is expected to grow fastest through 2030?

Infrastructure-as-a-Service leads at a 25.64% CAGR as companies modernise legacy systems with containerised, GPU-enabled edge environments.

Why are SMEs adopting distributed architectures more rapidly than before?

Consumption-based pricing, low-code orchestration and managed security bundles let SMEs access enterprise-grade cloud capabilities without heavy capital investment, supporting 23.45% CAGR adoption.

How does distributed cloud support real-time manufacturing operations?

Private 5G and local processing enable sub-10 millisecond latency for machine vision and predictive maintenance, eliminating round-trip delays to distant data-centers.

What security challenges accompany distributed cloud expansion?

A wider attack surface across dispersed nodes requires advanced zero-trust frameworks and skilled cyber-talent; shortages in the workforce add complexity to defence strategies.

Page last updated on: