Cloud-Native Application Protection Platform (CNAPP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

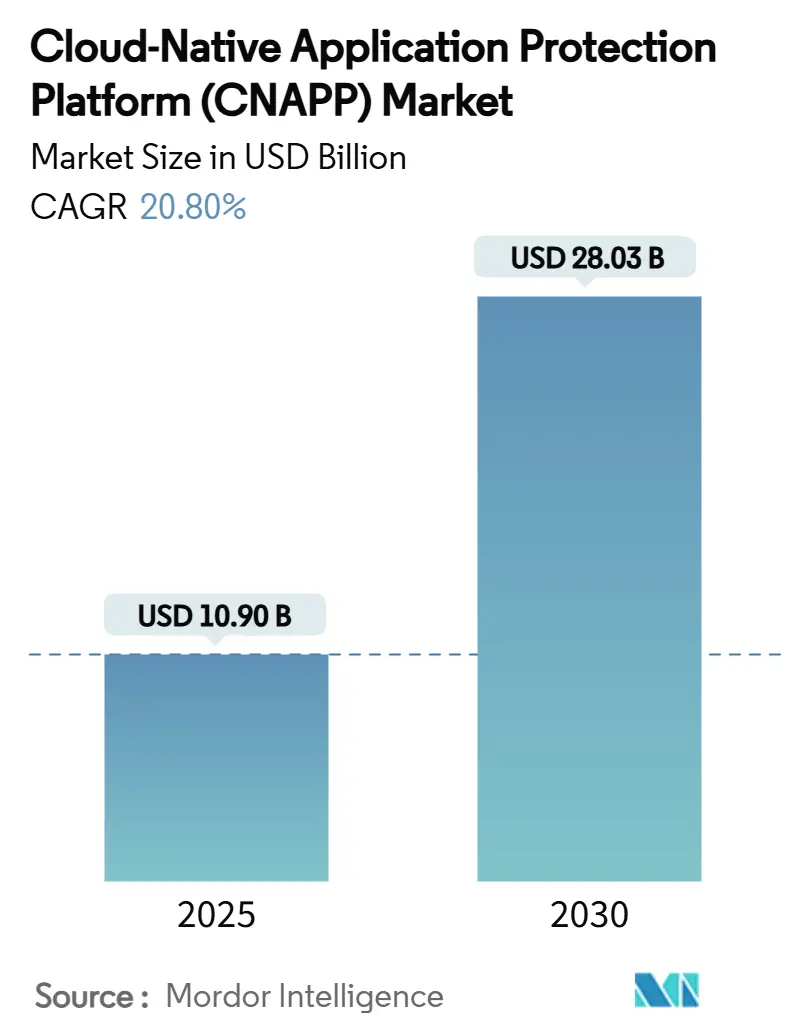

| Market Size (2025) | USD 10.90 Billion |

| Market Size (2030) | USD 28.03 Billion |

| Growth Rate (2025 - 2030) | 20.80% CAGR |

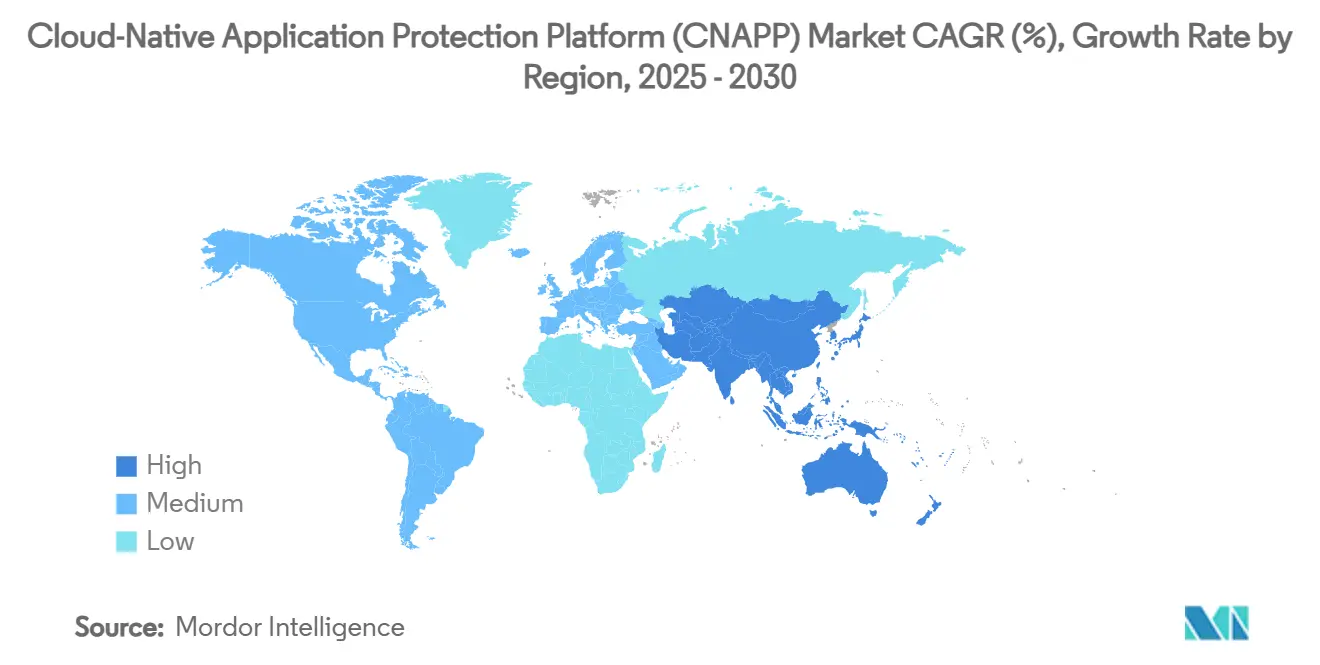

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-Native Application Protection Platform (CNAPP) Market Analysis by Mordor Intelligence

The Cloud-Native Application Protection Platform Market size is estimated at USD 10.90 billion in 2025, and is expected to reach USD 28.03 billion by 2030, at a CAGR of 20.80% during the forecast period (2025-2030). This growth stems from enterprise realization that fragmented cloud-security tooling limits visibility, inflates operating cost, and leaves exploitable gaps for advanced threat actors. Consolidation is accelerating: vendors are fusing Cloud Security Posture Management, Cloud Workload Protection, Kubernetes security, and entitlement management into single control planes, while strategic acquisitions—including SentinelOne, PingSafe, CrowdStrike, Bionic, and Fortinet, Lacework—underscore the shift toward platform breadth. Converged platforms now dominate procurement cycles, reinforced by tighter regulatory demands, a rapid move to hybrid architectures, and an expanding DevSecOps culture that embeds security earlier in development workflows.

Key Report Takeaways

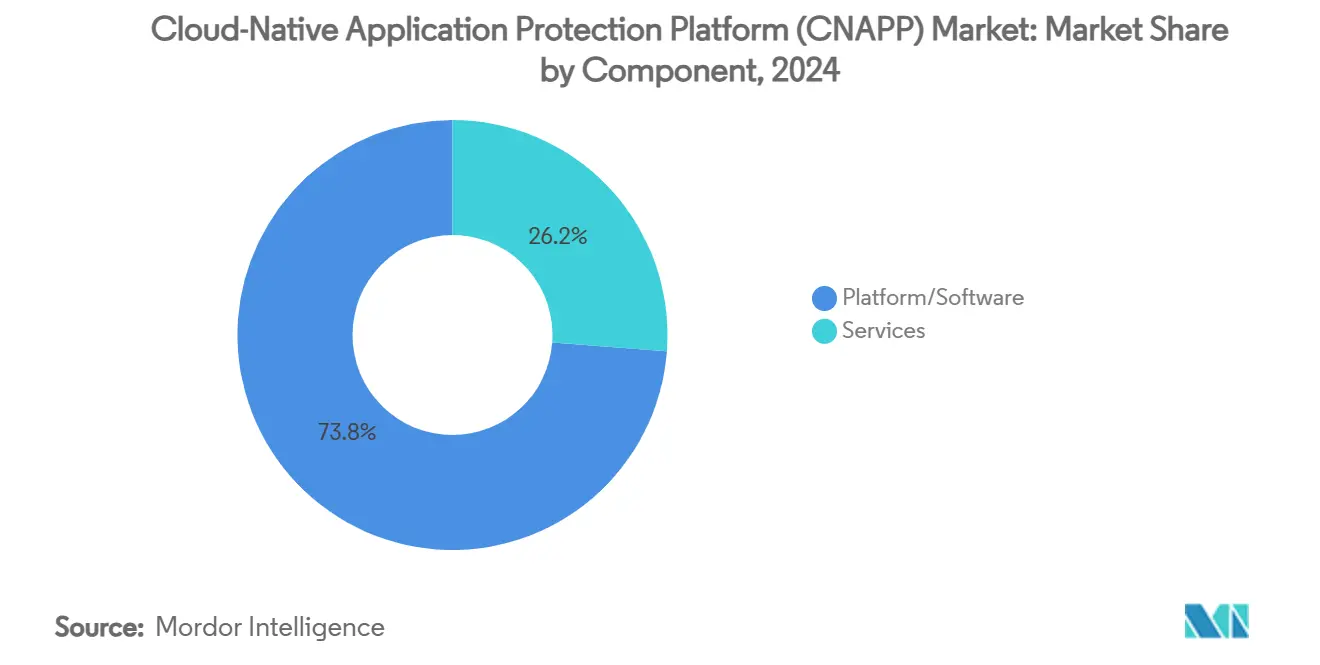

- By component, Platform/Software held 73.8% of the Cloud-Native Application Protection Platform market share in 2024, whereas Services is projected to advance at a 24.4% CAGR through 2030.

- By cloud-deployment mode, SaaS offerings captured 61.7% revenue share in 2024; PaaS-integrated solutions are forecast to expand at a 23.5% CAGR to 2030.

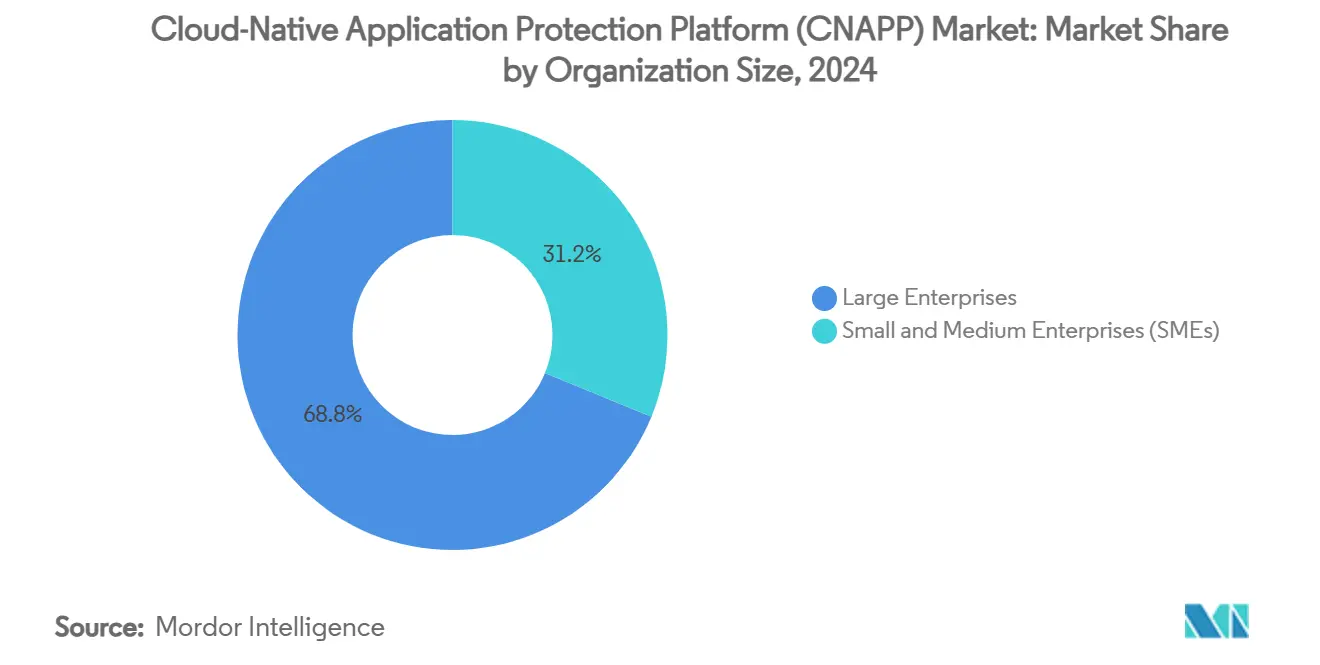

- By organization size, large enterprises commanded 68.8% of the Cloud-Native Application Protection Platform market in 2024, while small and medium enterprises represent the fastest-growing cohort at a 24.7% CAGR.

- By industry vertical, BFSI led with 27.8% revenue share in 2024; IT and Telecom are set to register the highest CAGR of 23.6% over the forecast window.

- By cloud environment, public-cloud deployments accounted for 57.8% revenue share in 2024, whereas hybrid/multi-cloud architectures are poised to climb at a 24.1% CAGR to 2030.

- By geography, North America contributed 38.3% revenue share in 2024, whereas Asia-Pacific is anticipated to record a 23.8% CAGR during 2025–2030.

Global Cloud-Native Application Protection Platform (CNAPP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of multi- and hybrid-cloud architectures | +4.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Increasing volume and sophistication of cloud-native breaches | +3.8% | North America and EU primary, APAC emerging | Short term (≤ 2 years) |

| Expanding regulatory and compliance mandates for cloud workloads | +3.5% | North America and EU core, spill-over to APAC | Long term (≥ 4 years) |

| DevSecOps shift-left integration across CI/CD pipelines | +3.1% | Global, with early gains in tech hubs | Medium term (2-4 years) |

| eBPF-based kernel observability enabling deeper runtime defense | +2.9% | Global, concentrated in advanced enterprises | Long term (≥ 4 years) |

| Standardization of policy-as-code (OPA) for entitlement management | +2.7% | Global, with financial services leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Multi- and Hybrid-Cloud Architectures

Hybrid strategies have matured from redundancy tactics to deliberate workload-placement models that optimize latency, sovereignty, and cost. This architectural pivot multiplies the number of control planes security teams must monitor, making point solutions untenable. Enterprises increasingly require one platform that ingests telemetry from public, private, and edge footprints, correlates risk, and applies uniform policies. Vendor roadmaps now prioritize agentless discovery, auto-classification of assets across clouds, and federated posture analytics. As hybrid prevalence grows, consolidated CNAPP platforms become critical for maintaining visibility at the pace of infrastructure dynamism.

Increasing Volume and Sophistication of Cloud-Native Breaches

Attackers are exploiting container registries, misconfigured serverless functions, and open-source dependency pipelines. Runtime attacks bypass build-time scanners by injecting malicious code into long-lived service meshes. Successful intrusions have pushed enterprises to demand real-time behavioral detection that recognizes sequence anomalies rather than static signatures. Market leaders incorporate context-rich graphs, kernel-level eBPF hooks, and ML-based profiling to surface threats in milliseconds. Heightened board-level scrutiny following high-profile supply-chain exploits accelerates budget allocation toward integrated runtime defense.

Expanding Regulatory and Compliance Mandates for Cloud Workloads

Frameworks such as CISA BOD 25-01 and NIST 800-171 r3 place explicit responsibility on agencies and contractors to protect cloud-resident information. [1]CISA, “Binding Operational Directive 25-01,” cisa.gov Financial institutions must evidence stringent access-control hygiene under evolving FFIEC guidance, while GDPR enforcement actions sustain European emphasis on data-in-use controls. Healthcare providers balance HIPAA guarantees against patient-experience digitization. These rules converge on the need for automated evidence collection, continuous control monitoring, and policy-as-code enforcement—all native functions within full-spectrum CNAPP suites.

DevSecOps Shift-Left Integration Across CI/CD Pipelines

Developers now own baseline security gates, embedding misconfiguration checks and compliance rules into build manifests. CNAPP vendors respond by exposing APIs and plugins that embed risk scoring into pull-request feedback loops. Generative-AI copilots recommend least-privilege IAM policies and auto-remediate infrastructure-as-code templates. Integration depth has become a critical buying criterion as engineering teams refuse tools that disrupt deployment velocity. The resulting culture change reduces mean time-to-remediate vulnerabilities and strengthens overall cloud posture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security-tool sprawl and integration complexity | -2.8% | Global, acute in large enterprises | Short term (≤ 2 years) |

| Shortage of skilled cloud-security professionals | -2.3% | Global, severe in emerging markets | Long term (≥ 4 years) |

| Ambiguous shared-responsibility in container-as-a-service | -1.9% | Global, concentrated in regulated industries | Medium term (2-4 years) |

| Vendor lock-in concerns around proprietary agent architectures | -1.7% | Global, prominent in multi-cloud environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security-Tool Sprawl and Integration Complexity

Large enterprises run dozens of security products that duplicate alerts and complicate incident response. Integrating disparate dashboards into a central SIEM increases overhead and delays triage. Although CNAPP consolidation promises relief, migration requires painstaking connector mapping and data-pipeline tuning. Budget holders weigh near-term integration cost against longer-term efficiency gains, occasionally slowing adoption cycles. Vendors responding with open APIs, pre-built SIEM exporters, and usage-based pricing ease transition pains, yet cannot fully eliminate migration friction.

Shortage of Skilled Cloud-Security Professionals

Global workforce studies estimate a 4-million-person cyber-skills deficit. Cloud security demands advanced knowledge of container orchestration, serverless event models, and infrastructure-as-code—a profile rarer than traditional perimeter expertise. Organizations without these specialists struggle to customize CNAPP policies, inadvertently leaving default configurations unchecked. Vendors are embedding low-code policy builders and AI-guided setup wizards, but effective oversight still hinges on human judgment. Talent scarcity, therefore, tempers the pace at which some regions deploy end-to-end protection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Depth Sustains Services Upswing

Platform/Software offerings accounted for 73.8% of Cloud-Native Application Protection Platform market revenue in 2024, reflecting buyer preference for unified consoles that span posture management, workload protection, container security, and entitlement governance. Integrated graph databases correlate identity, configuration, and runtime context, yielding faster root-cause analysis and measurable risk reduction. High-value enterprises view comprehensive coverage as essential insurance against sophisticated lateral-movement tactics. The Services component, while smaller, is registering a 24.4% CAGR as clients seek advisory, integration, and managed-response programs that maximize platform efficacy. Vendors augment professional offerings with runbook automation, enabling continuous optimization without proportionate headcount expansion.

Second-generation managed services appeal to mid-market firms lacking resident cloud-security expertise. Providers deliver 24/7 monitoring, threat-hunting, and compliance evidence generation, aligning outcomes with operational metrics. As platform complexity grows—incorporating eBPF telemetry, policy-as-code toolchains, and AI analytics—specialized service partners bridge skill gaps and accelerate time-to-value. Consequently, the symbiotic relationship between robust platforms and expert services reinforces market expansion.

By Cloud Deployment Mode: SaaS Leadership Faces Deep-Integration Pressure

SaaS deployments secured 61.7% of 2024 revenue, owing to rapid onboarding, elastic scalability, and provider-managed maintenance. Organizations seeking immediate visibility favor SaaS to eliminate infrastructure overhead and shorten proof-of-concept cycles. Nevertheless, PaaS-integrated offerings are outpacing at a 23.5% CAGR as enterprises embed controls alongside native cloud services. Tight coupling allows policy engines to act on resource-creation events in near real-time, enhancing preventative posture. APIs and service meshes weave CNAPP logic directly into platform workflows, reducing context switches for developers.

IaaS-hosted models persist where data-sovereignty statutes or existing private-cloud investments preclude SaaS adoption. These deployments ride customer-managed clusters and therefore grant deeper customization but demand heavier operational lift. The maturity curve indicates a lifecycle in which organizations pilot via SaaS, migrate to PaaS integrations for granularity, and reserve IaaS hosting for sensitive workloads, collectively broadening vendor TAM.

By Organization Size: Democratization Unlocks Mid-Market Momentum

Large enterprises retained a 68.8% share in 2024 thanks to complex estates that warrant full-spectrum protection and budgets to match. They often deploy multiple CNAPP modules, integrate with legacy SIEM platforms, and customize policies for granular compliance regimes. Yet small and medium enterprises (SMEs) are advancing at a 24.7% CAGR, signaling democratization of cloud-native defenses. Consumption-based pricing, agentless discovery, and wizard-driven setups lower adoption barriers. New digital-first businesses embed CNAPP controls at inception, avoiding costly retrofits later.

SME proliferation pressures vendors to streamline UX without sacrificing depth. Feature tiering, context-aware alerts, and marketplace automation extensions tailor complexity to customer sophistication. Vendors balancing enterprise-grade functionality with SME accessibility are positioned to capture outsized incremental revenue as global cloud adoption diffuses.

By Industry Vertical: BFSI Dominance Meets IT-Telecom Velocity

BFSI institutions controlled 27.8% of sector revenue in 2024, driven by stringent regulatory climates and high-value data. Zero-trust mandates and real-time transaction integrity drive deep investments in entitlement management and runtime defense. The IT and Telecom cohort, expanding at a 23.6% CAGR, benefits from native familiarity with cloud platforms and an imperative to secure sprawling developer ecosystems. Telecom operators additionally safeguard 5G edge workloads, broadening CNAPP use cases to carrier environments.

Healthcare, manufacturing, and retail each increase spend as digitization accelerates. Healthcare entities integrate automated HIPAA evidence collection, manufacturers secure connected-factory OT workloads, and retailers protect high-volume payment APIs. Vendor roadmaps that incorporate industry-specific compliance templates and reference architectures ease adoption, reinforcing vertical penetration.

By Cloud Environment: Public-Cloud Scale Evolves Toward Hybrid Complexity

Public-cloud deployments represented 57.8% of 2024 revenue, reflecting the dominant role of hyperscalers in digital transformation. Unified APIs streamline posture-management rollouts across regions. However, hybrid and multi-cloud strategies are expanding at a 24.1% CAGR, driven by cost arbitrage, resilience plans, and sovereignty mandates. A single enterprise may now distribute workloads across three CSPs, two private clouds, and multiple edge sites—all requiring one coherent risk model.

Private-cloud use cases endure for latency-critical or classified workloads. Yet even private environments increasingly expose standardized APIs, allowing CNAPP engines to normalize telemetry and apply centralized policy. The emerging equilibrium positions public cloud as an innovation ground, hybrid as an operational norm, and private as a specialized enclave, each reinforcing the need for converged protection.

Geography Analysis

North America contributed 38.3% of 2024 revenue, anchored by early enterprise cloud adoption, stringent regulatory frameworks, and a concentration of CNAPP innovators. Federal guidance, such as CISA BOD 25-01, obliges agencies to implement secure-by-design cloud architectures, catalyzing spend across the public sector. [2]CISA, “Binding Operational Directive 25-01,” cisa.gov Major financial institutions and technology giants extend this momentum by standardizing on entitlement-governance models and eBPF-enabled runtime defense, strengthening regional leadership and inspiring adjacent markets.

Asia-Pacific is projected to grow at a 23.8% CAGR to 2030, underpinned by data-localization statutes, sovereign-cloud programs, and a burgeoning digital-native SME sector. Governments in Japan, India, and Australia have introduced regulations paralleling GDPR, elevating mandatory control baselines. Enterprises navigating multiple jurisdictional rulesets are gravitating toward platforms capable of enforcing common policy while accommodating local residency constraints. As hyperscalers roll out region-specific availability zones, CNAPP vendors partner to deliver integrated compliance toolchains.

Europe maintains steady expansion fueled by ongoing GDPR enforcement and sector-specific directives such as DORA for financial services. Organizations reduce sensitive data residency in uncontrolled regions and adopt automated evidence templates to minimize audit fatigue. Middle East and Africa, and South America embark on cloud acceleration journeys, though limited cyber-talent pools temper full-suite CNAPP rollouts. Regional managed-security providers bridge gaps by offering subscription-based monitoring layered over vendor platforms, gradually seeding broader adoption.

Competitive Landscape

The Cloud-Native Application Protection Platform market is moderately consolidated, with leading vendors pursuing scale through platform breadth and inorganic expansion. Wiz, Palo Alto Networks, and CrowdStrike headline revenue rankings, each integrating CSPM, CWP, CIEM, and Kubernetes security under unified interfaces. CrowdStrike’s acquisition of Bionic and Fortinet’s purchase of Lacework highlight the premium placed on agentless posture assessment and infrastructure graph analytics. SentinelOne’s PingSafe deal further illustrates momentum toward single-pane solutions. [3]SentinelOne, “PingSafe Acquisition Announcement,” sentinelone.com

Technological differentiation now rests on context-rich risk modeling and low-overhead deployment. Graph-based schemas map relationships among identities, configurations, and runtime behaviors, enabling precise prioritization. eBPF instrumentation offers frictionless telemetry, while generative-AI engines translate complex policy logic into human-readable recommendations. Vendors that align feature velocity with compliance requirements gain traction in regulated sectors.

White-space opportunities persist in edge-compute and OT workload protection, serverless policy enforcement, and automated software-supply-chain assurance. Emerging specialists—such as AccuKnox with deterministic-AI policy builders—target these niches and form strategic alliances with SIEM, SOAR, and cloud-platform marketplaces. Ecosystem integration is increasingly vital: Wiz’s partnership with Exabeam exemplifies how combined analytics reduce mean-time-to-detect. [4]Wiz, “Press Releases,” wiz.io As buyers consolidate vendors, market share is likely to coalesce around platforms delivering end-to-end visibility with open-ecosystem connectors.

Cloud-Native Application Protection Platform (CNAPP) Industry Leaders

Wiz, Inc.

Orca Security Ltd.

Lacework, Inc.

Aqua Security Software Ltd.

Sysdig, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Wiz introduced Wiz Defend, adding real-time detection and automated incident response to its platform.

- January 2025: AccuKnox unveiled an AI-powered CNAPP that embeds generative security guidance into developer pipelines.

- January 2025: Wiz and Exabeam announced a technology alliance for unified cloud-threat detection.

- December 2024: Wiz acquired Dazz Inc. for USD 450 million to deepen its supply-chain remediation capabilities.

- December 2024: Tenable enhanced its CNAPP portfolio with automated governance modules for multi-cloud accounts.

- November 2024: Palo Alto Networks expanded Prisma Cloud with AI-driven alert-deduplication, lowering false positives.

Global Cloud-Native Application Protection Platform (CNAPP) Market Report Scope

| Platform/Software | CSPM |

| CWP | |

| CIEM | |

| Kubernetes and Container Security | |

| Serverless Security | |

| Services | Professional Services |

| Managed Services |

| SaaS CNAPP |

| PaaS-integrated CNAPP |

| IaaS-hosted CNAPP |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| IT and Telecom |

| Government and Defense |

| Manufacturing |

| Other Industry Verticals |

| Public Cloud |

| Private Cloud |

| Hybrid/Multi-Cloud |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Platform/Software | CSPM | |

| CWP | |||

| CIEM | |||

| Kubernetes and Container Security | |||

| Serverless Security | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Cloud Deployment Mode | SaaS CNAPP | ||

| PaaS-integrated CNAPP | |||

| IaaS-hosted CNAPP | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Industry Vertical | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| IT and Telecom | |||

| Government and Defense | |||

| Manufacturing | |||

| Other Industry Verticals | |||

| By Cloud Environment | Public Cloud | ||

| Private Cloud | |||

| Hybrid/Multi-Cloud | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and projected growth of the Cloud-Native Application Protection Platform market?

The market stands at USD 10.90 billion in 2025 and is forecast to reach USD 28.03 billion by 2030, expanding at a 20.8% CAGR.

Why are enterprises moving away from point cloud-security tools toward CNAPP platforms?

Fragmented tooling causes visibility gaps and higher operating cost, while consolidated CNAPP suites provide single-pane management and stronger defense against sophisticated cloud-native attacks.

Which deployment mode dominates CNAPP adoption today?

SaaS CNAPP deployments lead with 61.7% market share in 2024, thanks to fast onboarding and provider-managed maintenance.

Which industry verticals invest most in CNAPP solutions?

Banking, Financial Services, and Insurance accounts for 27.8% of 2024 revenue, followed by rapid uptake in IT & Telecom that is growing at a 23.6% CAGR.

What geographic region will grow fastest through 2030?

Asia-Pacific is projected to expand at a 23.8% CAGR, driven by sovereign-cloud mandates and accelerating enterprise cloud adoption.

How does the shortage of cloud-security talent influence CNAPP demand?

The global cyber-skills gap pushes organizations toward automated, all-in-one CNAPP platforms that reduce manual configuration and streamline compliance work.

Page last updated on: