Cloud-based Apps Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

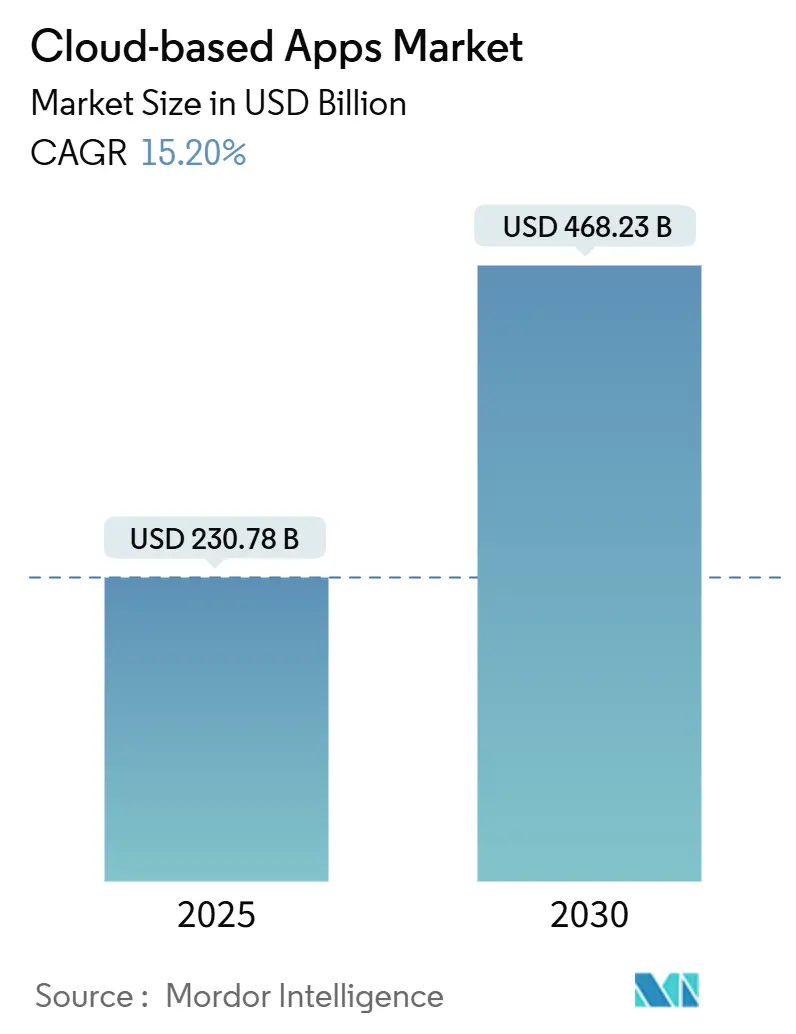

| Market Size (2025) | USD 230.78 Billion |

| Market Size (2030) | USD 468.23 Billion |

| Growth Rate (2025 - 2030) | 15.20% CAGR |

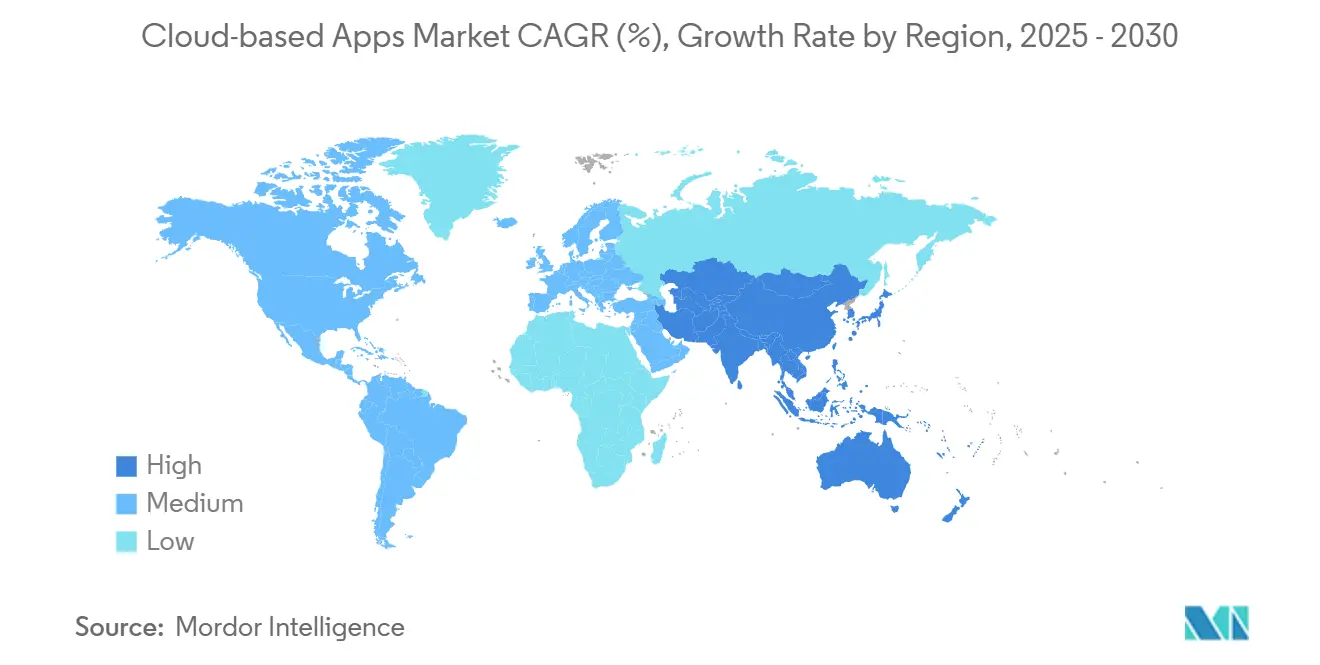

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-based Apps Market Analysis by Mordor Intelligence

The cloud-based apps market size is projected to reach USD 468.23 billion by 2030, advancing at a 15.2% CAGR from USD 230.78 billion in 2025. This vigorous expansion reflects enterprises shifting away from rigid, on-premise software toward composable cloud architectures that support constant business model adaptation.[1]Microsoft Corporation, “Azure Application Innovation Platform,” microsoft.com Key growth forces include sovereign AI regulations that drive hybrid deployments, API-first strategies that encourage microservice composition, and vertical compliance mandates that transform traditional SaaS delivery. North America leads with a 37.31% revenue share in 2024, while the Asia Pacific records the highest 17.44% CAGR through 2030, underscoring the differing maturity curves of developed and emerging regions. CRM holds the largest 29.7% application share, yet Collaboration and Productivity Suites expand fastest at 17.5% CAGR as hybrid work and AI-enabled automation gain permanence. Public-cloud SaaS remains dominant at 72.8%, but Hybrid-cloud SaaS grows at a 16.3% CAGR amid demands for sovereignty and latency. Large enterprises still account for 65.1% of spending, although SME adoption accelerates at a 16% CAGR, driven by consumption-based pricing and turnkey vertical bundles. BFSI sustains a 38.02% vertical lead, yet Retail and E-commerce surge at 17.81% CAGR on omnichannel imperatives, signaling a re-balancing of end-market influence within the cloud-based apps market.

Key Report Takeaways

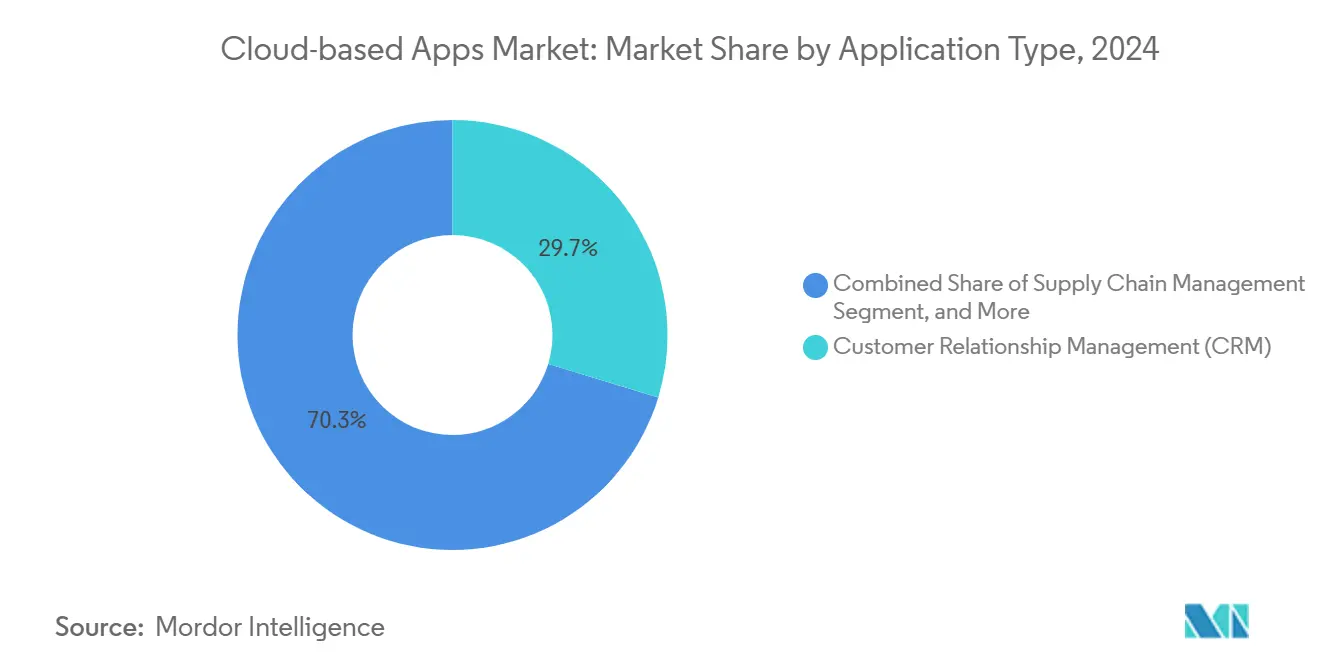

- By application, CRM captured 29.7% of the cloud-based apps market share in 2024, while Collaboration and Productivity Suites are projected to post the highest 17.5% CAGR to 2030.

- By deployment model, Public-cloud SaaS secured 72.8% of the cloud-based apps market size in 2024; Hybrid-cloud SaaS is forecast to expand at a 16.3% CAGR through 2030.

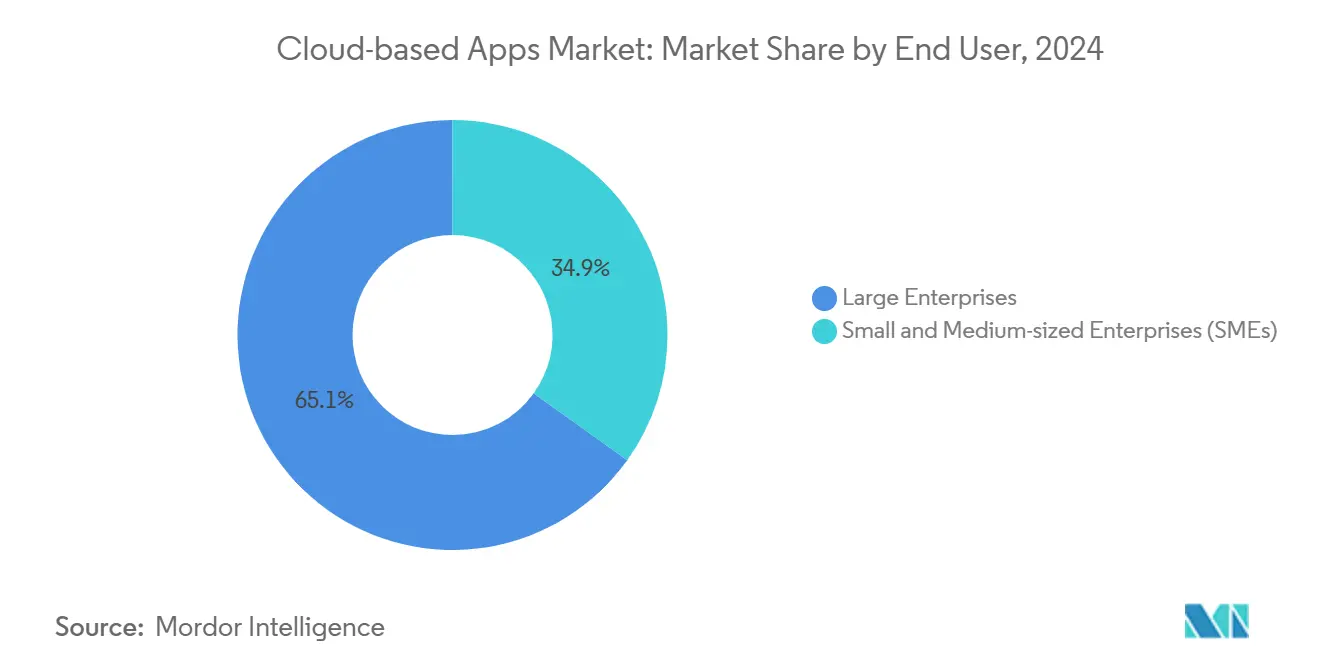

- By end user, large enterprises controlled 65.1% of spending in the cloud-based apps market in 2024, whereas SMEs are expected to rise at a 16% CAGR to 2030.

- By industry vertical, BFSI commanded a 38.02% share of the cloud-based apps market in 2024, while Retail and E-commerce are expected to grow at a 17.81% CAGR during 2025-2030.

- By geography, North America led the cloud-based apps market in 2024, accounting for 37.31% of the revenue, while the Asia Pacific is projected to grow at a 17.44% CAGR through 2030.

Global Cloud-based Apps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise digitization and SaaS adoption | +3.2% | Global with APAC and Latin America acceleration | Medium term (2-4 years) |

| SME demand for scalable solutions | +2.8% | Global; strongest in emerging markets | Short term (≤ 2 years) |

| AI and ML integration into SaaS | +3.5% | North America and Europe leading, APAC following | Long term (≥ 4 years) |

| Expansion of API ecosystems | +2.1% | North America and Europe core, spillover to APAC | Medium term (2-4 years) |

| Vertical-specific cloud apps | +2.4% | Global, higher in regulated regions | Medium term (2-4 years) |

| Low-code and no-code customization | +1.8% | Global, SME-dense regions faster | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Enterprise Digitization and SaaS Adoption

Organizations accelerated cloud migration when 85% of SAP’s 2024 new customers opted for cloud deployments, up from 45% in 2020.[2]SAP SE, “Q4 2024 Earnings Release,” sap.com Replacement cycles were shortened to 3-5 years due to legacy architectures constraining competitiveness. Manufacturers deploying Industry 4.0 programs relied on cloud ERP and SCM systems with embedded IoT capabilities to connect their supply chains in real-time. Enterprises now view cloud apps as agility enablers rather than cost reducers, prompting providers to bundle migration services and hybrid connectors. This driver adds consistent upside to the cloud-based apps market by prompting both back-office reinvention and front-office modernization.

Rapid Integration of AI and ML into SaaS Offerings

Salesforce Einstein delivered more than 1 trillion weekly AI predictions in 2024, demonstrating how embedded intelligence has evolved from an add-on feature to a core workflow. AI-first architectures sharpen competitive moats through predictive customer insights and automated decision support. Vertical apps in healthcare, legal, and finance combine domain models with machine learning to raise accuracy and throughput. Compliance burdens created by the EU AI Act channel enterprise spending toward vendors capable of providing audit trails and ethics governance. Consequently, AI enrichment significantly enhances perceived value, driving premium-priced renewals and expanding the cloud-based apps market.

Expansion of API Ecosystems Enabling Composable App Architectures

Stripe surpassed USD 1 trillion in 2024 payment volume through API integrations, signaling enterprise comfort with assembling solutions from specialized components.[3]Stripe Inc., “Annual Letter 2024,” stripe.com OpenAPI standards and developer marketplaces ease interoperability, letting midsize firms orchestrate sophisticated processes without large internal IT staffs. Vendors that invest in robust documentation, sandbox environments, and pre-built connectors secure integration stickiness. Composability, therefore, expands the addressable customer base and increases the average revenue per account, further driving the growth of the cloud-based apps market.

Vertical-specific Cloud Solutions Driving New Revenue Streams

Healthcare cloud revenues grew 23% annually as providers sought HIPAA-compliant EHR, telehealth, and decision support systems. Financial services platforms incorporate real-time fraud detection and regulatory reporting, thereby sidestepping the limitations of generic CRM systems. Deep workflow embedding raises switching costs and cushions margins against horizontal commoditization. Regulatory barriers in pharmaceuticals, aerospace, and energy protect incumbents yet leave room for specialists versed in sector nuance. Vertical focus thus redirects future growth to compliance-heavy niches within the cloud-based apps market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SaaS subscription fatigue and vendor sprawl | -2.1% | Global; most in mature markets | Short term (≤ 2 years) |

| Data residency and sovereignty laws | -1.8% | Europe, China and strict-law markets | Medium term (2-4 years) |

| Hyperscaler price competition | -1.3% | Global; smaller vendors affected | Long term (≥ 4 years) |

| Rising cloud security breaches | -1.5% | Global; high-security industries hit harder | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising SaaS Subscription Fatigue and Vendor Sprawl

Enterprises ran an average of 254 SaaS applications in 2024, which inflated management overhead and license spending. Duplication, integration drift, and fragmented analytics prompted consolidation toward suite providers offering unified billing, SSO, and shared data models. Point product vendors lacking a clear ROI experienced elevated churn. Procurement teams now weigh total platform value over feature depth, tempering growth in some sub-segments of the cloud-based apps market.

Data Residency and Sovereignty Regulations Limiting Adoption

GDPR in Europe and China’s Cybersecurity Law obligate local data processing, compelling vendors to build in-region infrastructure. Compliance raises costs, lengthens launch timelines, and occasionally disqualifies foreign providers that lack a local presence. Highly regulated industries must vet providers for jurisdictional fit, which reduces the global scalability benefits that have historically powered cloud adoption. While hybrid SaaS partly mitigates risk, sovereignty constraints shave momentum from the cloud-based apps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: CRM Dominance Faces AI-Enhanced Collaboration Challenge

CRM held a 29.7% market share of cloud-based apps in 2024, confirming its centrality in revenue orchestration. Collaboration and Productivity Suites, however, are set to outpace every category with a 17.5% CAGR, reflecting permanent hybrid work patterns and conversational interfaces that boost workforce efficiency. HRM adoption remains steady as employee-centric analytics gain favor, and ERP systems revive through cloud-native deployments that eliminate legacy complexity.

Heightened supply-chain disruptions prompted organizations to adopt cloud SCM platforms that incorporate IoT telemetry and AI forecasting, thereby intensifying competition among vendors that embed blockchain provenance and predictive logistics. Specialized vertical apps, ranging from telemedicine portals to regulatory reporting engines, appeal to enterprises that cannot afford the customization debt associated with horizontal suites. This functional rebalance steers incremental revenues across the cloud-based apps market.

By Deployment Model: Hybrid Architectures Reshape Cloud Strategy

Public-cloud SaaS accounted for 72.8% of the cloud-based apps market size in 2024. Yet, Hybrid-cloud SaaS, forecasted at a 16.3% CAGR, embodies the emerging norm of locating sensitive data on-premise while harnessing cloud elasticity for analytics. Private-cloud SaaS fulfills strict compliance needs and legacy bind-ins but cedes growth to hybrid versatility.

Edge computing reinforces hybrid ascendancy, enabling latency-sensitive workloads to process locally while synchronizing with central analytics. Financial institutions host core ledgers on private nodes while deploying customer engagement modules in cloud regions. Container orchestration eases portability among infrastructures, shrinking switching friction and broadening options. These dynamics expand both deployment flexibility and the potential of the cloud-based apps market.

By End User: SME Acceleration Challenges Enterprise Dominance

Large enterprises still generated 65.1% of 2024 revenue, but SME uptake is rising at a 16% CAGR due to the appeal of pay-as-you-grow pricing and turnkey vertical templates. Integrated suites better match SME capacity constraints than point tools, thereby heightening demand for all-in-one bundles that reduce administrative burden.

In emerging regions, SMEs leapfrog legacy IT by implementing mobile-first cloud systems, expanding the geographic reach of providers with localized currencies and language packs. Conversely, saturated enterprise segments are now focusing on platform consolidation and AI extension rather than new deployment, recalibrating their sales strategies across the cloud-based apps market.

By Industry Vertical: BFSI Leadership Faces Retail Innovation Pressure

BFSI retained a 38.02% share in 2024 thanks to stringent compliance and the premium banks pay for secure, audited workflows. Retail and E-commerce, advancing at 17.81% CAGR, capitalize on omnichannel analytics and real-time inventory orchestration to enhance customer experience. Healthcare continues to undergo steady digitization through the expansion of telehealth reimbursement.

Manufacturing’s Industry 4.0 momentum integrates predictive maintenance and digital twins, blending ERP, MES, and IoT analytics into unified cloud frameworks. Telecom and IT firms serve as dual users and suppliers, commercializing internal tools as external products, adding layered growth vectors to the cloud-based apps market size.

Geography Analysis

North America maintained a 37.31% revenue lead in 2024, driven by mature IT budgets and robust hyperscaler ecosystems. U.S. enterprises emphasize AI-infused, composable architectures, whereas Canadian firms prioritize compliance with sovereignty, and Mexican manufacturers adopt bilingual cloud SCM to integrate near-shoring supply chains.

The Asia Pacific region posts the fastest 17.44% CAGR through 2030, driven by government digitization, Industry 4.0 mandates, and fintech innovation. Chinese vendors thrive under localization rules and integration with domestic payment rails, while Singapore and Hong Kong serve as regional cloud hubs for cross-border enterprises. India’s software sector drives both supply and demand, reinforcing regional dynamism within the cloud-based apps market.

Europe continues to grow steadily amid the GDPR-driven demand for privacy-by-design applications. Germany’s manufacturers adopt secure Industry 4.0 suites, U.K. financial firms seek post-Brexit multi-jurisdictional compliance, and France’s digital sovereignty program boosts regional cloud providers. South America, the Middle East, and Africa exhibit leapfrog patterns, where mobile-first cloud solutions bypass desktop legacies, thereby diversifying revenue streams.

Competitive Landscape

The cloud-based apps market exhibits moderate fragmentation, with platform giants expanding their reach through acquisitions while specialists secure niche markets. CRM and ERP segments remain leader-heavy, yet AI-powered analytics, vertical compliance suites, and low-code platforms are fragmented with numerous entrants. Providers are increasingly differentiating themselves through AI scale, domain expertise, and adherence to evolving data laws, rather than relying solely on feature counts.

Patent submissions for cloud workflow optimization and predictive analytics increased by 34% in 2024, reflecting the rising competitive intensity.[4]United States Patent and Trademark Office, “Technology Trends Report 2024,” uspto.gov Acquisition activity, such as Salesforce’s purchase of Slack and Adobe’s acquisition of Figma, illustrates suite-building aimed at consolidation-minded enterprises. Hyperscaler pricing pressure challenges pure-play vendors, prompting alliances like Oracle and Microsoft that pool infrastructure strengths to shield their margins.

White space persists in heavily regulated sectors where certification hurdles deter newcomers, yet reward incumbents with resilient pricing. Simultaneously, emerging-market localization gaps invite regional challengers who are fluent in language, payments, and compliance nuances. These converging dynamics keep rivalry lively while steering the overall growth of the cloud-based apps market.

Cloud-based Apps Industry Leaders

Salesforce Inc.

ServiceNow Inc.

Workday Inc.

Atlassian Corporation Plc

Shopify Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft announced a USD 15 billion investment in AI infrastructure expansion across its Azure cloud platform, specifically targeting enterprise AI workloads and generative AI integration across its business applications suite, including Dynamics 365 and Power Platform, positioning the company to compete with emerging AI-native cloud providers.

- September 2026: Salesforce completed its USD 12.8 billion acquisition of MuleSoft's remaining integration platform assets and announced the launch of Einstein GPT Enterprise, a comprehensive AI assistant that integrates across all Salesforce clouds to provide automated customer service, sales forecasting, and marketing campaign optimization capabilities.

- August 2025: ServiceNow launched its Now Platform Vancouver release, featuring embedded AI agents capable of autonomous IT service management. This represents a USD 2.3 billion R&D investment over 18 months to create self-healing enterprise systems that reduce manual intervention requirements by up to 75%.

- July 2025: Oracle and Google Cloud announced a USD 8.5 billion strategic partnership to integrate Oracle Autonomous Database with Google's AI and machine learning services, enabling enterprises to run Oracle applications on Google Cloud infrastructure while leveraging advanced analytics and AI capabilities for real-time business insights.

- June 2025: Workday acquired Adaptive Insights competitor Anaplan for USD 13.2 billion, creating the largest cloud-based enterprise planning and analytics platform that combines human capital management with financial planning and supply chain optimization in a unified interface.

- May 2025: Adobe completed its USD 4.9 billion acquisition of collaboration platform Frame.io and launched Adobe Experience Cloud AI, which uses generative AI to create personalized customer experiences across digital touchpoints, targeting enterprises seeking to automate content creation and customer engagement workflows.

Global Cloud-based Apps Market Report Scope

| Customer Relationship Management (CRM) |

| Human Resource Management (HRM) |

| Enterprise Resource Planning (ERP) |

| Collaboration and Productivity Suites |

| Supply Chain Management |

| Other Application Types |

| Public Cloud SaaS |

| Private Cloud SaaS |

| Hybrid Cloud SaaS |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Healthcare |

| Retail and E-commerce |

| Manufacturing |

| IT and Telecom |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Application Type | Customer Relationship Management (CRM) | |

| Human Resource Management (HRM) | ||

| Enterprise Resource Planning (ERP) | ||

| Collaboration and Productivity Suites | ||

| Supply Chain Management | ||

| Other Application Types | ||

| By Deployment Model | Public Cloud SaaS | |

| Private Cloud SaaS | ||

| Hybrid Cloud SaaS | ||

| By End User | Small and Medium-sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | BFSI | |

| Healthcare | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| IT and Telecom | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the cloud-based apps market in 2025?

The cloud-based apps market size is USD 230.78 billion in 2025 and is projected to grow at a 15.2% CAGR to USD 468.23 billion by 2030.

Which application segment grows fastest through 2030?

Collaboration and Productivity Suites lead growth with a 17.5% CAGR, reflecting hybrid work permanence and AI-enhanced workflows.

Why are hybrid-cloud deployments gaining traction?

Hybrid-cloud SaaS grows at 16.3% CAGR as firms balance latency, sovereignty and security by keeping sensitive data on-premise while scaling analytics in public clouds.

What drives SME adoption of cloud-based apps?

SMEs embrace consumption-based pricing and all-in-one vertical bundles, resulting in a 16% CAGR that challenges enterprise spending dominance.

Which region offers the highest growth opportunity?

Asia Pacific shows the steepest trajectory at 17.44% CAGR thanks to government digitization, manufacturing automation and fintech innovations.

Page last updated on: