Multi Cloud Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

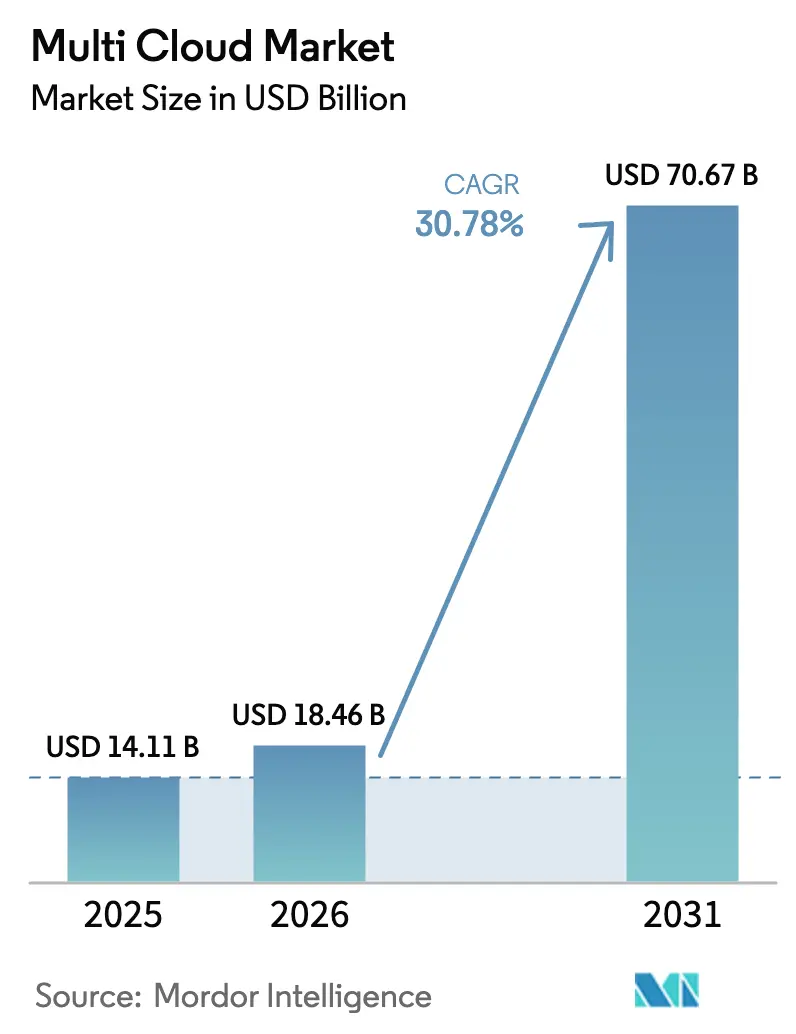

| Market Size (2026) | USD 18.46 Billion |

| Market Size (2031) | USD 70.67 Billion |

| Growth Rate (2026 - 2031) | 30.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi Cloud Market Analysis by Mordor Intelligence

The multi-cloud market size was valued at USD 14.11 billion in 2025 and estimated to grow from USD 18.46 billion in 2026 to reach USD 70.67 billion by 2031, at a CAGR of 30.78% during the forecast period (2026-2031). Spending momentum reflects the move from simple vendor-diversification toward coordinated workload orchestration that weighs cost, performance, and data sovereignty. Sovereign-cloud rules across the European Union and Middle East, large U.S. federal cloud budgets, and carbon-aware service placement all accelerate platform demand. Artificial-intelligence engines that resize and redeploy workloads in real time cut cloud expenses by double-digit rates while improving latency and uptime. Vendor ecosystems also evolve: hyperscalers embed management features within their stacks, while independent specialists add policy-based governance that works across providers. Skill shortages persist yet managed service partners and automation offset the talent gap.

Key Report Takeaways

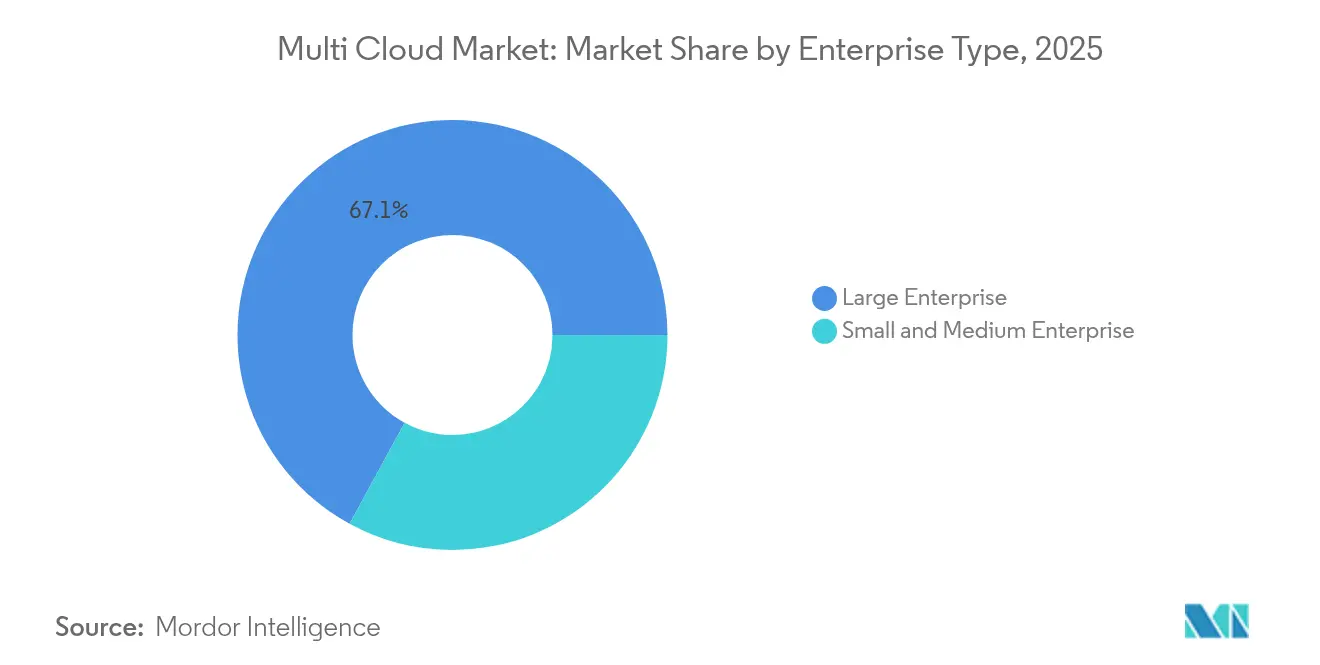

- By enterprise type, large enterprises led with 67.05% of the multi-cloud market share in 2025, while small and medium enterprises are set to grow at a 34.10% CAGR to 2031.

- By deployment model, hybrid setups captured 55.88% revenue share of the multi-cloud market size in 2025 and are projected to expand at a 37.95% CAGR through 2031.

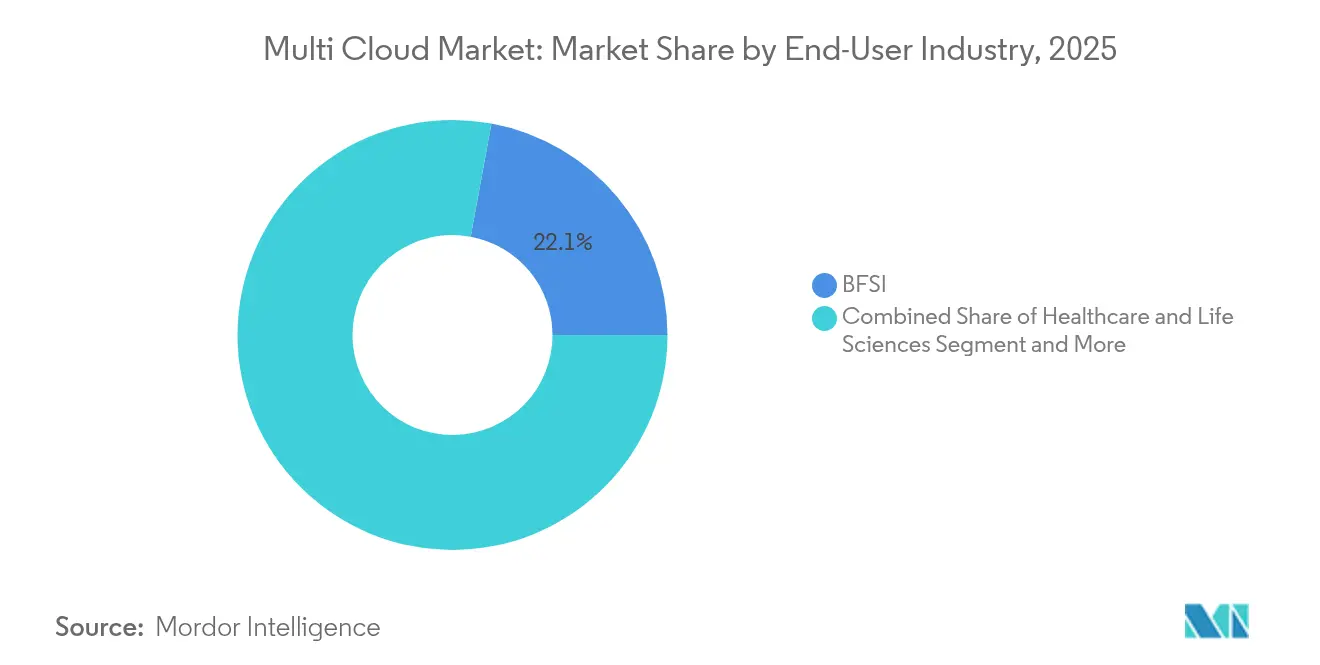

- By end-user industry, the BFSI sector held 22.10% share of the multi-cloud market size in 2025, whereas healthcare and life sciences are forecast to rise at a 37.10% CAGR to 2031.

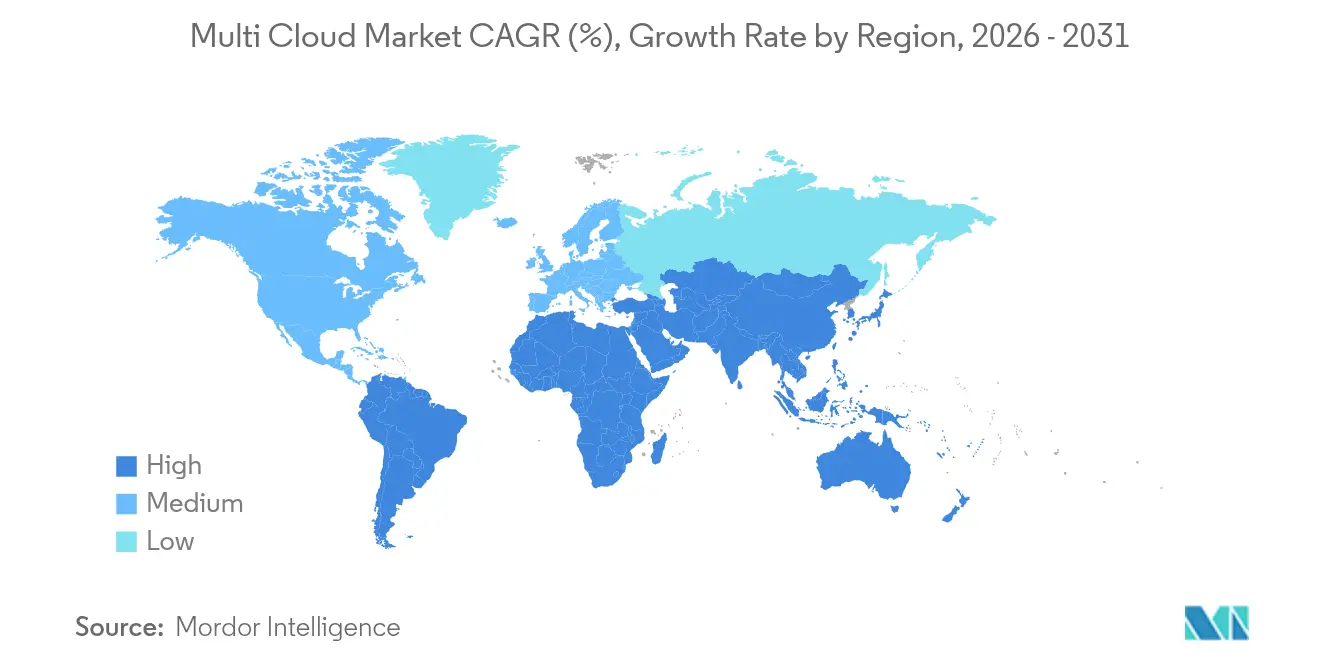

- By region, Asia-Pacific is the fastest-growing geography with a 36.95% CAGR to 2031, while North America remains the largest revenue contributor at 34.75% in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Multi Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid avoidance of vendor lock-in | + 8.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Demand for cloud-native disaster-recovery architectures | +6.2% | Global, concentrated in BFSI and Healthcare sectors | Short term (≤ 2 years) |

| AI-driven workload-placement engines | + 7.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Sovereign-cloud mandates in regulated sectors (EU, ME) | +5.4% | Europe and Middle East, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Hyperscaler interconnect fee optimisation | +4.7% | Global, with focus on high-traffic regions | Short term (≤ 2 years) |

| Carbon–aware orchestration requirements | +3.2% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Rapid avoidance of vendor lock-in | + 8.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid avoidance of vendor lock-in

Enterprises are rewriting procurement policies to ensure no single provider controls critical workloads. Subscription portability between Azure and on-premises VMware estates illustrates the new approach, giving teams leverage in price talks and resilience during provider outages.[1]Broadcom Press Room, “VMware Cloud Foundation Subscription Portability,” broadcom.comCloud-agnostic consoles that mask proprietary interfaces let developers redeploy applications without refactoring, lowering switching barriers and encouraging competitive bidding among hyperscalers.

Demand for cloud-native disaster-recovery architectures

Zero-downtime mandates in financial and healthcare environments are shifting recovery designs from nightly backups toward continuous replication across several clouds. Institutions now replicate databases in near real time and script automated failover that brings recovery objectives down to minutes. The design shields regional zones from outages and satisfies regulators who expect demonstrable secondary sites.

AI-driven workload-placement engines

Machine-learning schedulers study historical use, spot prices, latency, and carbon intensity before selecting a destination for every job. Enhanced TOPSIS algorithms running on Kubernetes cut response times by up to 36% and boost throughput by half, proving the value of predictive placement. Enterprises record 15–25% spending cuts as the engines right-size instances and shift batch jobs to low-cost regions during off-peak hours.

Sovereign-cloud mandates in regulated sectors

European and Middle-East regulators now require critical data to stay within national borders, forcing multinational firms to create region-bounded cloud zones. Azure Government and AWS GovCloud respond with ring-fenced infrastructure certified for public-sector workloads.[2]Bacancy Technology Analysts, “Sovereign Cloud Trends 2025,” bacancytechnology.com Companies split stacks: regulated data rests in local sovereign clouds, while customer experience layers run in global regions for scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent skill-set shortage in multi-cloud SRE talent pool | -4.8% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Inconsistent security postures across clouds | -3.2% | Global, concentrated in regulated industries | Short term (≤ 2 years) |

| Escalating egress-fee unpredictability | -2.7% | Global, high-impact in data-intensive sectors | Short term (≤ 2 years) |

| Limited workload portability for legacy monoliths | -2.1% | North America and EU, legacy-heavy industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent skill-set shortage in multi-cloud SRE talent pool

Sixty-two percent of firms report inadequate AI and cloud skills, and 41% cannot hire enough qualified engineers, inflating salaries and extending project timelines.[3]SoftwareOne Cloud Advisory, “2025 Cloud Skills Survey,” softwareone.com Managed service providers and upskilling programs ease pressure yet cannot fully offset the global gap, especially in emerging economies.

Inconsistent security postures across clouds

Each provider applies unique identity models, logging tools, and control planes, forcing security teams to juggle multiple dashboards. Three-quarters of enterprises admit that a patchwork of tools leaves blind spots that attackers exploit. Consolidated Cloud Native Application Protection Platforms promise relief, though integration complexity limits near-term adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Type: SMEs accelerate platform democratization

Small and medium enterprises represent the fastest-rising cohort with a 34.10% CAGR through 2031. Affordable SaaS consoles and managed services open enterprise-grade governance to resource-constrained IT teams, reducing the technical barrier once associated with multi-provider estates. The multi-cloud market size for SMEs is forecast to climb sharply as turnkey bundles include cost analytics, policy automation, and one-click migrations. Managed service partners supply expertise on demand, letting SMEs experiment with AI optimization without hiring deep SRE benches.

Large enterprises still anchor revenue because their estates span public clouds, on-premises clusters, and hundreds of distributed edge nodes. These organizations pilot AI-driven profilers that refactor monoliths during migration and fine-tune resource allocations by the hour. They influence product roadmaps and standards bodies, guiding tooling that later trickles down to smaller firms. Integration complexity and legacy debt temper their growth yet their budgets guarantee sustained platform spend, keeping the multi-cloud market in an innovation cycle.

By Deployment Type: Hybrid models command dual leadership

Hybrid topologies captured 55.88% share of the multi-cloud market size in 2025 and register the quickest expansion at a 37.95% CAGR. Firms place latency-critical or regulated assets in on-premises or colocation sites while bursting analytics or seasonal web loads into public regions. Automated connectors now render the boundary invisible, letting teams shift capacity without manual intervention.

Public cloud deployments keep expanding as provider compliance certifications multiply. Private clouds maintain presence where bespoke hardware, sovereign controls, or deterministic throughput is essential. The spectrum converges toward a unified control plane that discovers and manages any endpoint, a design goal highlighted by backup vendors that integrate hybrid visibility across snapshots, replication, and workload mobility.

By End-User Industry: Healthcare sets the growth pace

Healthcare and life sciences are on track for a 37.10% CAGR to 2031. Electronic health record vendors migrate to multi-region infrastructures that guarantee uptime and satisfy residency statutes. AI models for diagnostics demand GPU clusters that often exceed hospital data-center limits, so providers dispatch those tasks to cloud accelerators while holding sensitive identifiers on private nodes.

BFSI owns the largest revenue block with 22.10% share, having adopted multi-cloud early for disaster recovery and algorithmic trading resilience. Continuous integration pipelines, risk analytics, and customer-facing apps land on different providers to meet latency and regulation rules. Retail and manufacturing follow, embedding IoT telemetry in edge gateways connected back to regionally optimized analytic hubs.

Geography Analysis

North America contributed 34.75% of 2025 revenue after years of federal and enterprise investment. The U.S. government alone earmarked USD 8.3 billion for cloud in fiscal 2025, spurring contractors and integrators to upgrade orchestration expertise. Financial services, media, and technology firms advanced well-governed multi-cloud estates, leveraging a deep skill base and rich interconnect fabric. Canada enforces data-sovereignty controls that favor hybrid deployments, while Mexico’s near-shoring boom elevates demand for cross-border cloud coordination.

Asia-Pacific is the fastest-growing region at a 36.95% CAGR. China’s cloud-infrastructure spending hit USD 9.2 billion in 2024 as domestic players launched AI-optimized regions. India’s digital-public-goods initiatives bring government workloads online and create a downstream need for sovereign multicloud control planes. Japan and South Korea pair advanced manufacturing with real-time analytics that span domestic and global regions, requiring precise scheduler placement logic.

Europe grows steadily as regulators press for data-local guarantees. Germany, the United Kingdom, and France deploy sovereign nodes that route regulated datasets locally while still tapping global clouds for burst analytics. Vendors answer with “trusted cloud” labels, audited access paths, and encryption key escrow that the customer holds. The Middle East mirrors this pattern, adding sovereign capability to new hyperscale regions anchored by government cloud frameworks.

Competitive Landscape

The multi-cloud market features mid-level fragmentation. VMware combines virtualization, cost analysis, and sustainability dashboards. Microsoft, AWS, and Google layer cross-cloud governance into their suites, aiming to keep workloads within their wider ecosystems. Niche vendors differentiate on depth: Flexera focuses on license compliance, CoreStack on policy automation, and CloudBolt on template-driven self-service.

Strategic consolidation quickens. IBM closed a USD 6.4 billion HashiCorp deal, embedding Terraform and Vault into its automation catalog and signaling demand for integrated infrastructure-as-code with security defaults. Hewlett Packard Enterprise bought Morpheus Data to enrich its GreenLake platform, while Cisco added CloudBolt to advance single-pane management. Funding rounds also stay active: CloudZero secured USD 56 million to expand AI-led cost optimization

Horizontal moves include VMware’s sustainability claims that its virtualization stack helped users avoid 1.2 billion metric tons of carbon emissions, offering a green differentiator. Hyperscalers waive interconnect charges during promotional windows, encouraging cross-region architectures yet pulling workloads toward their fabrics. Overall, buyers weigh breadth of ecosystem, automation depth, and carbon-reporting features when selecting a platform.

Multi Cloud Industry Leaders

Dell Technologies Inc.

Microsoft Corp.

IBM Corp.

VMware Inc.

Oracle Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: IBM closed its USD 6.4 billion acquisition of HashiCorp, adding Terraform and Vault to IBM’s hybrid-cloud automation suite.

- August 2024: Hewlett Packard Enterprise acquired Morpheus Data, integrating multicloud orchestration and FinOps into GreenLake.

- January 2025: Google Cloud completed its purchase of CloudSimple, expanding Anthos with VMware migration capabilities.

- October 2024: Cisco finalized its acquisition of CloudBolt Software, enhancing governance and cost-optimization inside Cisco Intersight.

Global Multi Cloud Market Report Scope

Multicloud (also spelled as multi-cloud or multi cloud) describes a strategy where companies leverage multiple cloud computing services from diverse public vendors, all integrated within a unified, heterogeneous architecture. This strategy not only bolsters the capabilities of cloud infrastructure but also optimizes associated costs. Furthermore, it encompasses the distribution of cloud assets, software, applications, and more across various cloud-hosting environments. Typically, a multicloud architecture employs two or more public clouds alongside several private clouds. The primary goal of this multicloud setup is to reduce dependence on any single cloud provider, effectively mitigating the risk of vendor lock-in.

The Report Covers Multi Cloud Companies and the Market is Segmented by Deployment (Public, Private, Hybrid), by End-User Industry (BFSI, Healthcare, Manufacturing, Retail and E-Commerce, Government & Defense, Energy & Utility, Other End-User Industry), by Geography (North America, Europe, Asia-Pacific, Middle East and Africa, Rest of the World). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Large Enterprise |

| Small and Medium Enterprise |

| Public |

| Private |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| IT and Telecommunications |

| Government and Public Sector |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Enterprise Type | Large Enterprise | ||

| Small and Medium Enterprise | |||

| By Deployment Type | Public | ||

| Private | |||

| By End-User Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| IT and Telecommunications | |||

| Government and Public Sector | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the multi-cloud market?

The multi-cloud market is valued at USD 18.46 billion in 2026.

How fast is the multi-cloud market expected to grow?

It is forecast to expand at a 30.78% CAGR, reaching USD 70.67 billion by 2031.

Which deployment model leads the market?

Hybrid architectures lead with 55.88% revenue share and the highest growth trajectory at 37.95% CAGR.

Which industry segment is growing the fastest?

Healthcare and life sciences show the fastest growth, projected at a 37.10% CAGR through 2031.

What is the largest regional market?

North America holds the largest share at 34.75% of 2025 revenue, driven by public-sector and enterprise investment.

Page last updated on: