United States Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

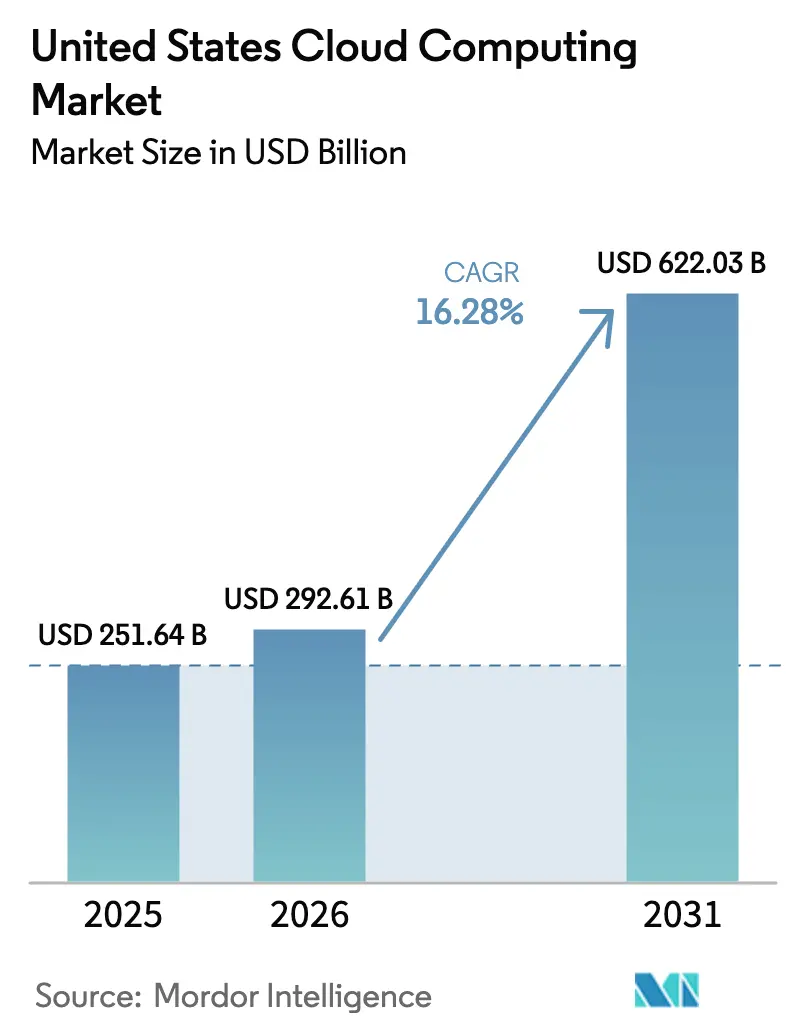

| Base Year Market Size (2025) | USD 251.64 Billion |

| Market Size (2026) | USD 292.61 Billion |

| Market Size (2031) | USD 622.03 Billion |

| Growth Rate (2026 - 2031) | 16.28% CAGR |

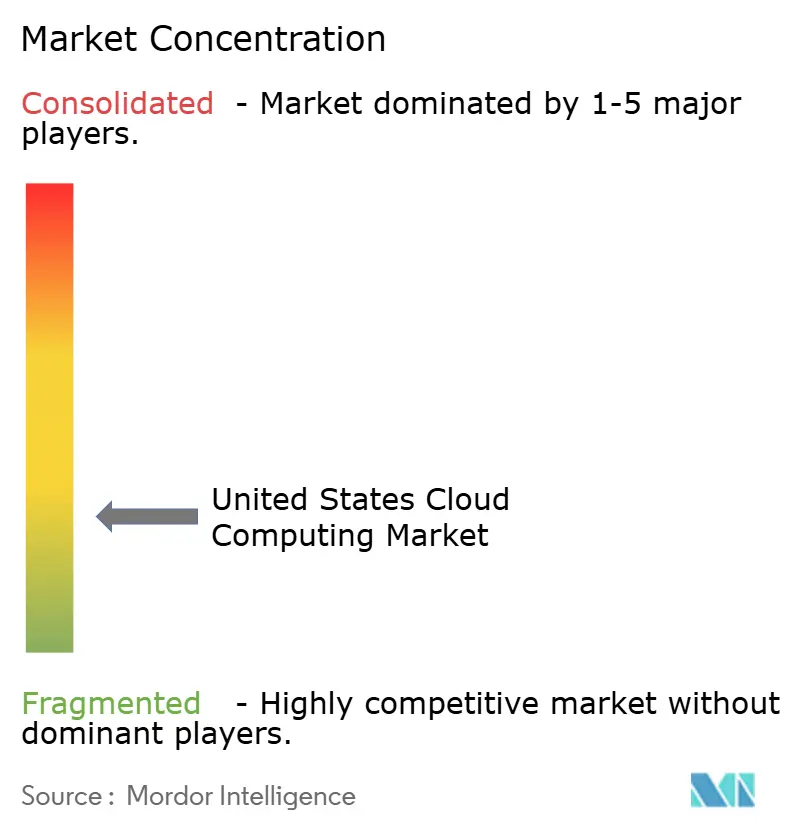

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cloud Computing Market Analysis by Mordor Intelligence

The United States Cloud Computing Market size was valued at USD 251.64 billion in 2025 and estimated to grow from USD 292.61 billion in 2026 to reach USD 622.03 billion by 2031, at a CAGR of 16.28% during the forecast period (2026-2031). The United States cloud computing market continues to benefit from unmatched hyperscale capital spending, an unrivaled domestic data-center footprint, and the rapid institutionalization of artificial-intelligence workloads across every major industry vertical. Strong federal incentives, robust venture funding, and deep enterprise demand keep the United States cloud computing market well ahead of global peers in both absolute value and growth velocity. Power-grid bottlenecks and an escalating cyber-threat landscape temper the outlook but are not expected to derail the overall expansion trajectory as long as grid upgrades and Zero-Trust security frameworks keep pace. Together, these demand-side and supply-side forces reinforce a positive long-term outlook for the United States cloud computing market.

Key Report Takeaways

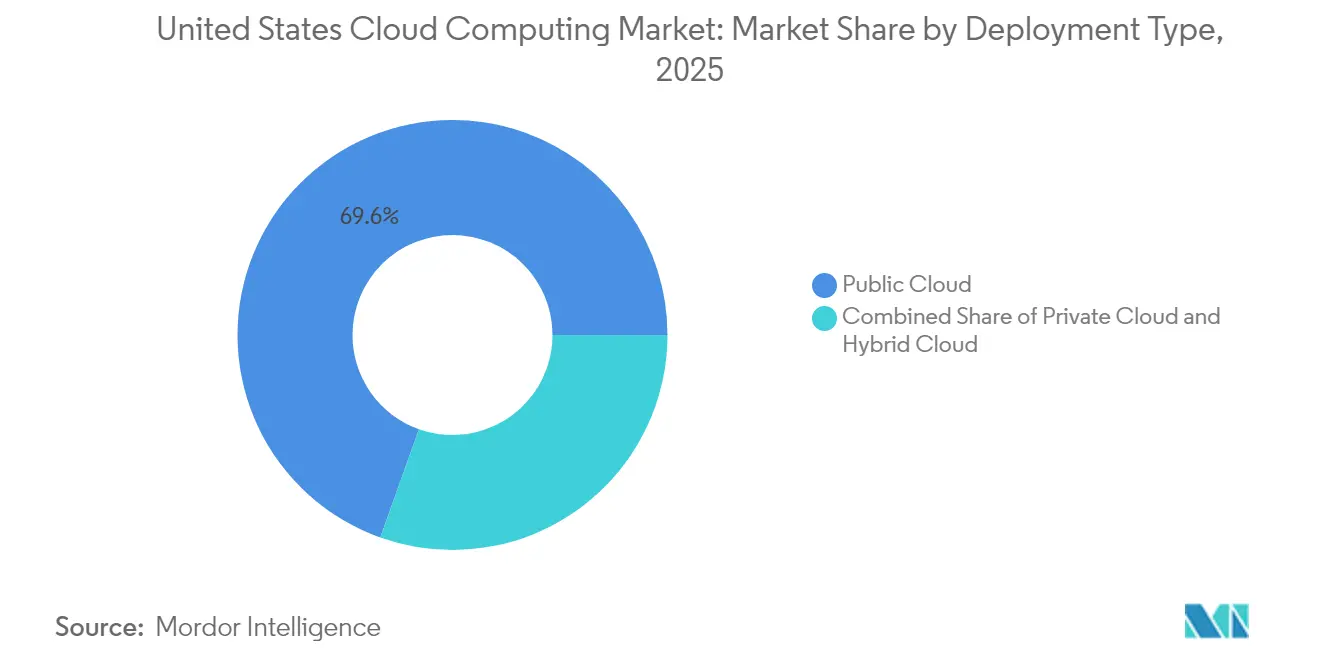

- By deployment type, Public Cloud led with a 69.55% revenue share in 2025, while Hybrid Cloud is projected to expand at a 22.24% CAGR through 2031.

- By service model, Software-as-a-Service held 46.95% of the United States cloud computing market share in 2025; Platform-as-a-Service posts the fastest growth at 26.74% CAGR.

- By organization size, Large Enterprises captured 60.85% share of the United States cloud computing market size in 2025, whereas SMEs are advancing at a 18.90% CAGR.

- By end-user vertical, IT & Telecom commanded 24.35% share of the United States cloud computing market in 2025 while Healthcare records the highest forecast CAGR at 20.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United states contributes to a system defined not by any single country or region but by the interaction of many. The global cloud computing market data by Mordor Intelligence represents that combined structure.

United States Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated digital transformation across U.S. enterprises | +3.2% | National, with concentration in tech hubs | Medium term (2–4 years) |

| AI / ML & big-data workload boom | +4.8% | West Coast, Northeast corridors | Short term (≤2 years) |

| Cost-optimisation & flexibility over on-premise IT | +2.1% | National, strongest in SME segment | Long term (≥4 years) |

| Federal & state green-tax incentives for energy-efficient data-centres | +1.7% | Regional, focused on renewable-energy states | Medium term (2–4 years) |

| FinOps-driven cost governance & ESG reporting demands | +1.9% | National, enterprise-focused | Medium term (2–4 years) |

| Edge-to-cloud orchestration for latency-sensitive use-cases | +2.3% | Urban centers, manufacturing regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital Transformation Across U.S. Enterprises

Rising cloud maturity is reshaping procurement patterns. Ninety-five percent of banking executives now classify cloud as pivotal to digital-strategy execution, a view validated by Capital One’s full cloud migration that shortened product-launch cycles and improved cross-channel agility. Manufacturers such as Procter & Gamble deploy cloud-based manufacturing-execution platforms that integrate shop-floor assets with ERP data, cutting process-implementation times by up to 50%. These shifts push more workloads into the public cloud, driving platform-based operating models that, in turn, reinforce the growth path of the United States cloud computing market.

AI/ML and Big-Data Workload Boom

A surge in AI workloads exerts significant capacity pressure. Microsoft reports a tenfold rise in Copilot demand, while Google acknowledges ongoing supply-demand imbalances for AI infrastructure. The AI infrastructure market is forecast to reach USD 309.4 billion by 2031, and 96% of enterprises plan additional GPU capacity, pointing to sustained upside risk for the United States cloud computing market. Because generative AI adoption among U.S. firms remains below 10%, incremental demand is likely to stay elevated for several planning cycles.

Cost-Optimisation and Flexibility Over On-Premise IT

FinOps practices give enterprises granular control over usage-based charges and enable SMEs to match IT spending with cash flow. Ultra Tool & Manufacturing saved USD 128,000 per year by migrating to cloud-based manufacturing software, underscoring how variable pricing models reduce capex exposure. As 99.9% of U.S. businesses qualify as SMEs, scalable pay-as-you-go services expand the total addressable base, strengthening the mid-term outlook for the United States cloud computing market.

Federal and State Green-Tax Incentives for Energy-Efficient Data Centers

Digital Realty reached 100% renewable-energy use for its North American colocation portfolio in 2024, a milestone achieved through green-tax credits and utility partnerships. Amazon is on pace to run 100% on renewables by 2025, backing USD 150 billion in data-center capex with 1.5 GW of contracted clean-power capacity. These incentives tilt new-build economics in favor of the United States cloud computing market while advancing decarbonization goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex regulatory & data-sovereignty compliance | −2.8% | National, with sector-specific variations | Long term (≥4 years) |

| Escalating cyber-security & ransomware threats | −1.9% | National, concentrated in critical infrastructure | Short term (≤2 years) |

| Acute cloud-skills gap amid rapid GenAI stack changes | −2.3% | National, most severe in emerging tech hubs | Medium term (2–4 years) |

| Power-grid constraints in key U.S. hyperscale clusters | −3.1% | Regional, focused on Northern Virginia, Dallas, Silicon Valley | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Complex Regulatory and Data-Sovereignty Compliance

Financial institutions must reconcile FFIEC cloud guidance with Gramm-Leach-Bliley privacy rules, while healthcare providers negotiate HIPAA-mandated business-associate agreements even for encrypted storage. Defense contractors bear additional obligations under DoD regulations requiring domestic data residency. Fragmented jurisdictional requirements raise compliance costs and lengthen procurement cycles, dampening some demand within the United States cloud computing market.

Escalating Cyber-Security and Ransomware Threats

Fifty-nine percent of organizations endured ransomware attacks in 2024. AI-enabled voice-phishing and intermittent encryption elevate risk severity, particularly in healthcare and public infrastructure. Cloud misconfigurations add further exposure, compelling enterprises to invest in Zero-Trust architectures and managed detection services. The added cost burden could limit short-term net-new migrations, though robust security offerings from hyperscale providers may mitigate longer-term impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Architectures Drive Enterprise Modernization

The United States cloud computing market size for deployment models shows Public Cloud at USD 174.97 billion in 2025, representing 69.55% of value. Hybrid Cloud’s 22.24% CAGR reflects sovereign-data mandates and the need for local latency control. Telecommunications firms leverage hybrid cores to anchor 5G performance, while manufacturers route IoT data to nearby edge nodes before central analytics. These patterns establish Hybrid Cloud as the architectural default for regulated and latency-sensitive workloads within the United States cloud computing market.

In parallel, Private Cloud remains relevant for highly regulated sectors such as financial services and defense. However, the growing interplay between edge and centralized compute creates a continuum rather than a dichotomy. Enterprises increasingly adopt policy-based orchestration that auto-moves workloads across environments, underscoring how workload portability will shape the long-run structure of the United States cloud computing market.

By Service Model: Platform Services Accelerate AI Development

Software-as-a-Service captures the largest slice at 46.95%, translating to a United States cloud computing market size of USD 118.13 billion in 2025. Adoption spans productivity suites, CRM, and sector-specific applications. The spotlight now shifts to Platform-as-a-Service, whose 26.74% CAGR underscores a decisive turn toward integrated AI development stacks. Enterprises favor managed Kubernetes and serverless databases to speed experimentation, while avoiding infrastructure chores. These dynamics enlarge the addressable base for Platform services, reinforcing top-line growth across the United States cloud computing market.

Infrastructure-as-a-Service underpins both SaaS and PaaS movements. Hyperscalers allocate outsized capital to GPU-rich clusters that host foundation models and inference workloads. The resulting specialization differentiates providers on the basis of chip availability, network throughput, and framework integrations. Consequently, service-model boundaries blur as customers purchase holistic solution bundles that span compute, data, and machine-learning tools all of which drive incremental value back into the United States cloud computing market.

By Organisation Size: SME Cloud Adoption Democratizes Enterprise Capabilities

Large Enterprises held 60.85% of 2025 spend, equal to a United States cloud computing market share of roughly USD 153.11 billion. These customers migrate mission-critical ERP, analytics, and collaboration suites, layering AI services on top to unlock productivity gains. Yet growth momentum tilts toward SMEs, posting a 18.90% CAGR thanks to consumption-based billing and a flourishing ecosystem of no-code tools. For firms with fewer than 500 employees, the cloud eliminates the historical fixed-cost barrier, allowing them to adopt cybersecurity, analytics, and e-commerce solutions on par with larger competitors.

Policy makers view SME digitization as an engine for job creation and supply-chain resilience. Federal grant programs and localized venture funds provide onboarding credits and technical guidance. As digital-skills training catches up, SMEs will contribute an outsized share of incremental revenue, cementing their role as a primary growth lever for the United States cloud computing industry.

By End-User Vertical: Healthcare AI Drives Sector Transformation

IT and Telecom contributed 24.35% of 2025 revenue, reflecting heavy self-consumption by carriers deploying network-cloud cores and by software vendors distributing SaaS offerings. Healthcare, however, rises as the growth pacesetter at 20.45% CAGR, propelled by AI-based diagnostics, electronic medical-record modernization, and strict uptime targets. Seattle Children’s Hospital achieved five-nines availability for its Epic EHR after migration to a managed cloud environment. This reliability standard sets a new benchmark across the United States cloud computing market.

Manufacturing, BFSI, and Government also advance cloud penetration but at lower CAGRs. Manufacturers exploit cloud analytics for predictive maintenance, while banks focus on open-banking compliance and real-time risk analytics. Public-sector adoption accelerates under the FedRAMP 20x initiative, which shrinks authorization windows from months to weeks. Collectively, vertical diversification buffers macro-cyclical risk and reinforces total addressable demand within the United States cloud computing market.

Geography Analysis

Regional dispersion follows power availability, land cost, and industry density. The West leads due to Silicon Valley’s concentration of hyperscale campuses and proximity to AI start-ups, yet power-grid congestion in Northern California compels providers to secure supplemental capacity in desert states. The South gains momentum as AWS stakes USD 10 billion each in Mississippi and North Carolina, citing renewable-energy abundance and supportive tax policies. Such commitments elevate the South’s role inside the United States cloud computing market.

The Midwest offers stable power grids and central location, making it a preferred region for disaster-recovery zones and cold-storage data lakes. Chicago and Columbus hubs benefit from fiber cross-connect density, supporting multicloud interconnect strategies. Meanwhile, the Northeast sustains robust demand from financial-services firms despite tighter real-estate markets and higher electricity rates. Collectively, these patterns confirm that regional growth hinges less on user proximity than on energy resilience and permitting timelines.

Secondary cities emerge as alternative growth nodes as primary metros near saturation. Atlanta and Phoenix register double-digit absorption, while local utilities fast-track transmission-line upgrades. Onsite microgrids are expected to supply 30% of U.S. data-center power by 2030, reducing dependency on congested bulk-power systems. This decentralized energy trend is poised to enhance long-term supply stability for the United States cloud computing market size allocated to regional builds.

The cloud computing market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Asia, and South America. This is complemented by country-specific insights for Canada, Brazil, United Kingdom, India, Germany, and Italy, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Capital intensity remains the defining entry barrier. Amazon leads with a USD 100 billion FY 2025 U.S. capex plan aimed at GPU-dense clusters for foundation-model training. Microsoft follows at USD 80 billion, directing more than half to domestic campuses. Google commits USD 75 billion, pairing hardware advances with in-house TPU development. Collectively, the trio accounts for most incremental supply, yet competitive space exists for specialists in network security, data-integration, and edge orchestration.

Oracle secured a USD 30 billion multi-year cloud services agreement focused on AI workload hosting, signaling appetite for alternative platforms outside the Big Three. GPU-focused providers such as CoreWeave win contracts by guaranteeing shorter lead times and offering flexible leasing. Interconnection specialists like Equinix and Cloudflare position themselves as neutral hubs, enabling multicloud strategies without directly challenging compute incumbents. These dynamics illustrate a maturing ecosystem characterized by coopetition rather than pure rivalry.

Partnerships across power infrastructure also redefine competitive boundaries. Microsoft, BlackRock Infrastructure Partners, and MGX joined forces to co-invest in data-center power assets, easing grid stress and ensuring predictable energy pricing. Similar alliances are spreading to other hyperscale clusters, suggesting that control over power generation will soon rival network reach as a determinant of market leadership inside the United States cloud computing market.

United States Cloud Computing Industry Leaders

Amazon.com Inc. (AWS)

Google LLC

Microsoft Corporation

Salesforce Inc

Adobe Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon announced USD 10 billion investment in North Carolina data centers to enhance AI infrastructure, expected to create 500 jobs in the state.

- March 2025: The General Services Administration introduced the FedRAMP 20x program to reduce federal cloud authorization times from months to weeks through automated controls.

- February 2025: AWS committed USD 10 billion to build hyperscale facilities in Mississippi, marking the state’s largest private technology investment.

- January 2025: Microsoft outlined an USD 80 billion fiscal-year budget for U.S. AI-enabled data-center expansions.

United States Cloud Computing Market Report Scope

Cloud computing offers a vast range of computing services over the Internet. These services include servers, storage, databases, networking, software, analytics, and intelligence. Key advantages of cloud computing are accelerated innovation, flexible resource allocation, and economies of scale. Customers generally pay only for the services they use. This approach not only cuts operational costs but also boosts infrastructure efficiency and enables scaling to meet changing business demands.

The US Cloud computing market is segmented by type (public cloud [IaaS, Paas, Saas], private cloud, and hybrid cloud), organization size (SMEs and large enterprises), end-user verticals (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and it, government and public sector, and other end-user verticals (utilities, media & entertainment, etc.)). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium Enterprises (SME's) |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail |

| Transportation and Logistics |

| Telecom and IT |

| Government and Public Sector |

| Utilities |

| Media and Entertainment |

| Others |

| By Deployment Type | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organisation Size | Small and Medium Enterprises (SME's) |

| Large Enterprises | |

| By End-user Vertical | Manufacturing |

| Education | |

| Retail | |

| Transportation and Logistics | |

| Telecom and IT | |

| Government and Public Sector | |

| Utilities | |

| Media and Entertainment | |

| Others |

Key Questions Answered in the Report

What is the current size of the United States Cloud Computing Market?

The United States Cloud Computing Market is valued at USD 292.61 billion in 2026 and is forecast to reach USD 622.03 billion by 2031, reflecting a 16.28% CAGR during the forecast period (2026-2031).

Which deployment model is growing fastest?

Hybrid Cloud is expanding at a 22.24% CAGR as organizations balance sovereign-data mandates with edge performance requirements.

How large is the Platform-as-a-Service opportunity?

PaaS is projected to grow at 26.74% CAGR through 2031, propelled by demand for AI development tooling and container orchestration.

Why is healthcare expected to outpace other verticals?

Healthcare posts a 20.45% CAGR due to AI-powered diagnostics, regulatory automation, and the need for near-zero downtime electronic medical records.

What is the main constraint on new data-center builds?

Power-grid congestion in major hubs such as Northern Virginia and Silicon Valley poses the primary supply-side limitation, prompting investment in onsite generation and secondary markets.

How are federal initiatives influencing cloud adoption?

Programs like FedRAMP 20x accelerate authorization processes, enabling agencies to move workloads to the cloud in weeks instead of months, which boosts overall federal demand.

Page last updated on: