Data Virtualization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

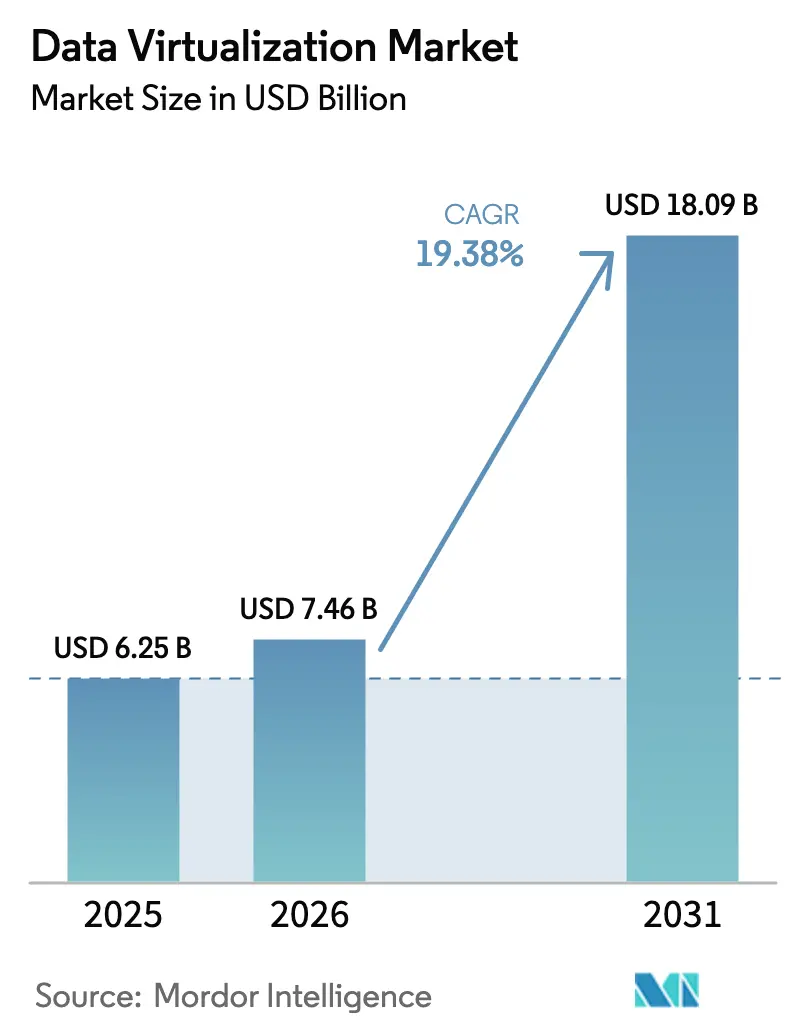

| Market Size (2026) | USD 7.46 Billion |

| Market Size (2031) | USD 18.09 Billion |

| Growth Rate (2026 - 2031) | 19.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Virtualization Market Analysis by Mordor Intelligence

The data virtualization market size is expected to grow from USD 6.25 billion in 2025 to USD 7.46 billion in 2026 and is forecast to reach USD 18.09 billion by 2031 at 19.38% CAGR over 2026-2031. Robust AI-centric infrastructure spending, tighter data-sovereignty regimes, and the spread of edge computing architectures are accelerating adoption. Vendors that streamline query optimization across hybrid and multi-cloud environments continue to gain traction as enterprises favor logical data fabrics over data lakes. The shift toward consumption-based licensing, evidenced by fully managed offerings on hyperscaler marketplaces, is widening penetration among small and midsize enterprises. Meanwhile, consolidation moves by platform leaders signal intensifying competition to deliver AI-ready data pipelines at scale.

Key Report Takeaways

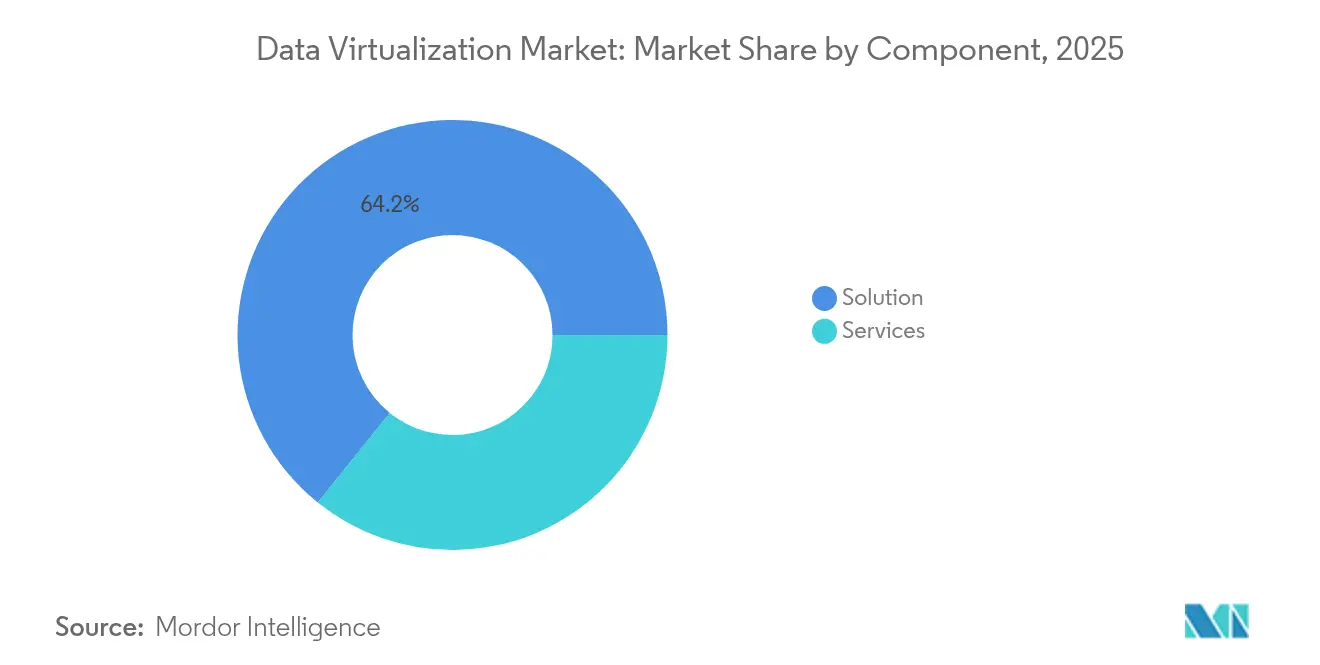

- By component, Solutions led with 64.22% of data virtualization market share in 2025, while Services exhibit the fastest CAGR at 24.05% through 2031.

- By deployment mode, Cloud captured 69.85% revenue in 2025; Hybrid Cloud is projected to expand at a 27.62% CAGR to 2031.

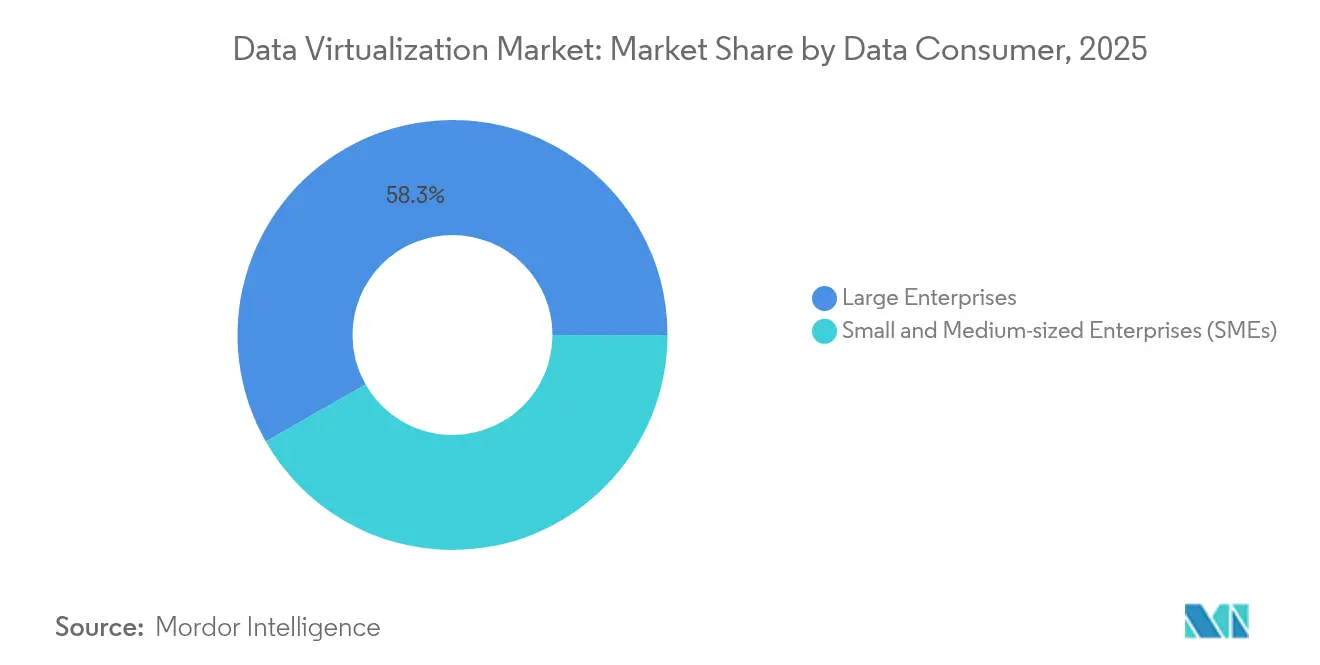

- By data consumer, Large Enterprises held 58.25% of the data virtualization market in 2025; SMEs are growing fastest at 25.45% CAGR.

- By end-user, the BFSI segment contributed 31.12% revenue in 2025, whereas Retail and E-commerce is poised for a 21.05% CAGR to 2031.

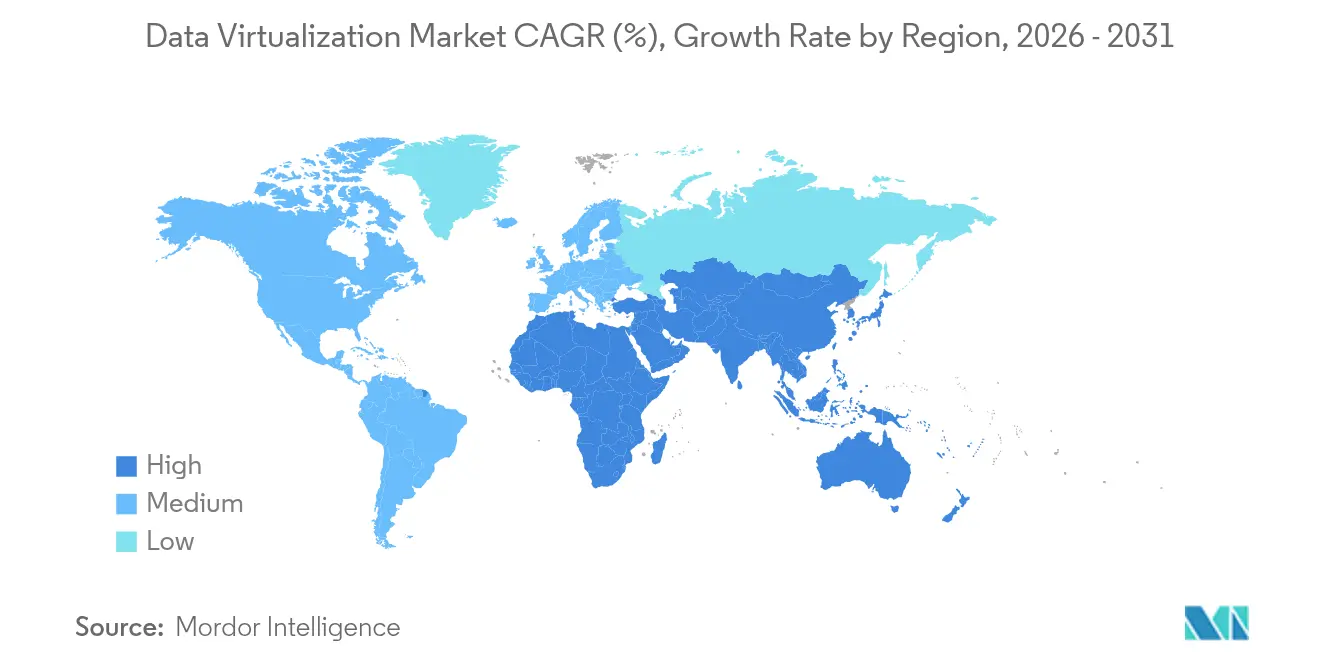

- By geography, North America accounted for 38.25% of global revenue in 2025; Asia-Pacific is the fastest-growing region at a 25.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Virtualization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-centric cloud infrastructure spending surge | +4.2% | Global, high in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing demand for real-time analytics in regulated industries | +3.8% | North America and EU | Short term (≤ 2 years) |

| Shift to data-mesh and logical data fabric architectures | +3.1% | Global, led by North America | Medium term (2-4 years) |

| Rise of industry-specific data marketplaces | +2.7% | Early adoption in North America | Long term (≥ 4 years) |

| Investor push for GenAI-ready data pipelines | +3.5% | Tech hubs worldwide | Short term (≤ 2 years) |

| Edge-to-cloud latency reduction requirements | +2.9% | Asia-Pacific core, global spill-over | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-centric cloud infrastructure spending surge

Hyperscaler capital expenditure on AI-optimized servers rose sharply in 2025, with enterprises allocating 35% of annual IT budgets to accelerated compute; this share is projected to hit 41% by 2029.[1]Network World Staff, “AI hardware spending explodes as rack power tops 100 kW,” networkworld.com Higher rack-level power densities drive organizations to adopt virtualization layers that minimize data movement and maximize cache efficiency across GPU clusters. Oracle reported a 115% quarter-over-quarter jump in MultiCloud database revenue, highlighting how cloud providers monetize this surge by offering virtualized, low-latency data access for AI workloads investor. [2]Oracle Corporation, “Oracle Fiscal 2025 Q4 Results,” investor.oracle.com

Growing demand for real-time analytics in regulated industries

Financial firms now spend 10% of annual revenue on compliance, prompting adoption of virtualization engines that aggregate risk data in real time for Basel III and FRTB reporting. Healthcare providers follow suit, using logical fabrics to merge imaging, lab, and patient-reported outcomes data while meeting HIPAA and GDPR mandates for data residency. The urgency to deliver instant insights under stringent oversight positions data virtualization as a default integration layer.

Shift to data-mesh and logical data fabric architectures

Enterprises are moving away from centralized lakes toward domain-owned data products managed under a mesh model, improving data quality and governance at scale. Logical data fabrics built on virtualization allow real-time delivery without duplicating datasets, supporting multi-cloud and edge scenarios. Denodo reports rising demand from federal agencies that combine mesh principles with centrally governed fabrics for sensitive workloads.[3]Acceldata, “Data observability for healthcare compliance,” acceldata.io

Rise of industry-specific data marketplaces

The market for data marketplaces is growing at a 25% CAGR, creating new revenue streams that rely on virtualization to expose secure, governed access to proprietary datasets. Snowflake’s expansion of its marketplace to AI-ready data underlines the structural role of virtualization in data commerce by abstracting location and format barriers.[4]Snowflake, “Introducing Snowflake Marketplace for GenAI,” snowflake.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data governance program failures | -2.8% | Global, large enterprises | Short term (≤ 2 years) |

| Skill shortages in virtualization query optimization | -2.1% | North America and EU | Medium term (2-4 years) |

| Unpredictable egress fees in multi-cloud topologies | -1.7% | Cloud-first organizations | Short term (≤ 2 years) |

| Fragmented global data-sovereignty legislation | -1.9% | Multi-region enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data governance program failures

Up to 75% of governance initiatives falter due to weak executive sponsorship, poor metrics, and limited alignment with business value, delaying virtualization rollouts and eroding stakeholder trust. Fragmented lineage and policy management across virtual layers compel organizations to revamp governance playbooks before scaling logical fabrics.

Skill shortages in virtualization query optimization

Ninety percent of organizations report critical talent gaps that add 3-10 months to digital projects. Expertise that blends distributed database design with cloud-native tuning remains scarce, creating deployment bottlenecks and constraining the realized benefits of the data virtualization market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions maintain revenue leadership

Solutions accounted for 64.22% of data virtualization market share in 2025, underscoring the foundational need for core software to federate and cache distributed datasets. Standalone virtualization software remains the largest sub-category as enterprises seek granular control, while data-integration tooling gains because hybrid environments demand extensive connector libraries. Services are projected to grow at 24.05% CAGR as enterprises transition from deployment to optimization. Professional services dominate the services mix, yet managed services adoption is climbing as organizations offload operational complexity. Denodo’s fully managed Agora service exemplifies vendor response to this trend.

By Deployment Mode: Hybrid Cloud advances fastest

Cloud deployments held 69.85% revenue in 2025, reflecting a clear preference for elastic scale and consumption billing. Within the cloud cohort, Hybrid Cloud leads growth at 27.62% CAGR since it lets firms keep sovereign data on-premises while running analytics in the public cloud. VMware found that 84% of European enterprises plan to adopt sovereign cloud frameworks within the next year. On-premises models persist in defense and critical-infrastructure sectors but show slower expansion as cloud security assurances mature.

By Data Consumer: SMEs narrow the gap

Large enterprises controlled 58.25% of 2025 revenue, leveraging sizeable IT budgets to integrate virtualization into AI pipelines and data fabrics. Yet SMEs represent the fastest-growing cohort at 25.45% CAGR as user-friendly, consumption-based offerings remove entry barriers. Awareness of advanced analytics among US SMEs has surpassed 70%, particularly in marketing and customer experience use cases. This democratization is reshaping vendor go-to-market strategies toward simplified interfaces and preconfigured connectors.

By End-User: BFSI retains dominance; Retail accelerates

BFSI led adoption with 31.12% of 2025 revenue, propelled by real-time risk modeling and regulatory pressure for granular data lineage. Retail and e-commerce is forecast to grow at 21.05% CAGR through 2031 as merchants strive for sub-second personalization across channels. Manufacturing, healthcare, energy, and public-sector users likewise expand adoption, integrating operational technology streams with enterprise records to improve decision accuracy and compliance.

Geography Analysis

North America represented 38.25% of 2025 revenue due to mature cloud infrastructure, deep AI investment, and supportive regulatory sandboxes that encourage innovation. The data virtualization market size in the region is expanding steadily, with financial services and tech sectors driving large contractual wins. Europe benefits from GDPR-mandated data-protection frameworks and sovereign cloud initiatives, sustaining a healthy growth trajectory in markets such as Germany, France, and the Nordics.

Asia-Pacific is the fastest-growing geography at 25.05% CAGR, propelled by large-scale digital transformation programs in China, India, and Southeast Asia. Regional hyperscalers are building new data centers that shorten latency and comply with local residency laws, making virtualization appealing for cross-border analytics. The Middle East and Africa are emerging growth pockets where governments fund smart-city and e-government programs that depend on virtual data layers. South America’s momentum is led by Brazil, where financial-sector modernization and open-banking regulations create demand for secure, real-time data integration.

Competitive Landscape

The market remains moderately fragmented, with technology giants and pure-play vendors competing on performance, governance, and deployment flexibility. Denodo, IBM, and Microsoft leverage extensive partner ecosystems and RandD scale to protect share. Salesforce’s USD 8 billion purchase of Informatica underscores the strategic value of virtualization in AI-driven CRM workflows. Funding rounds, such as CData’s USD 350 million investment, fuel product innovation in high-performance connectors and low-code interfaces. Emerging challengers focus on domain-specific verticals—healthcare interoperability, IoT telemetry, and federal secure clouds—where compliance intricacies create entry barriers for generalist vendors.

Edge integration and AI-assisted query optimization have become focal points for differentiation. Vendors file patents around adaptive caching and cost-based optimizers that respond to fluctuating network conditions. Strategic alliances between cloud platforms and virtualization specialists, notably ClickHouse’s five-year partnership with AWS, expand global reach and embed virtualization deeper into cloud data stacks. Market leaders continue to invest in open-standards contributions to lock in developer mindshare while reducing switching friction for customers.

Data Virtualization Industry Leaders

Microsoft Corporation

Denodo Technologies

Oracle Corporation

TIBCO Software

Informatica LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Salesforce completed its USD 8 billion acquisition of Informatica to enhance CRM-embedded data management.

- January 2025: Qlik acquired Upsolver to bolster real-time data lakehouse performance.

- January 2025: Snowflake agreed to purchase Datavolo, widening its data virtualization toolkit.

- October 2024: Denodo launched Agora, a fully managed deployment of its platform with consumption pricing.

Global Data Virtualization Market Report Scope

Data virtualization serves as the fundamental technology that facilitates logical data management functionalities.

The study tracks the revenue accrued through the sale of data virtualization solutions and services by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. It further analyses the aftereffects of COVID-19 and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

Data virtualization market report is segmented by component (solution [standalone software, data integration solution, and application tool solution), and services), by deployment mode (cloud and on-premises), by data consumer (large enterprises and SMEs), by end-user (BFSI, healthcare, manufacturing, IT and telecom, education, government and defense, retail and e-commerce, and others), and by geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solution | Standalone Software |

| Data Integration Software | |

| Application Tool Solution | |

| Services | Professional Services |

| Managed Services |

| Cloud | Public Cloud |

| Private Cloud | |

| On-premises |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| BFSI |

| Healthcare |

| Manufacturing |

| IT and Telecom |

| Government and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Solution | Standalone Software | |

| Data Integration Software | |||

| Application Tool Solution | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | Cloud | Public Cloud | |

| Private Cloud | |||

| On-premises | |||

| By Data Consumer | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By End-User | BFSI | ||

| Healthcare | |||

| Manufacturing | |||

| IT and Telecom | |||

| Government and Defense | |||

| Retail and E-commerce | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the data virtualization market?

Expanding AI workloads, stricter data-sovereignty laws, and the need for real-time analytics across hybrid environments underpin the 19.38% CAGR forecast to 2031.

Which segment contributes the largest data virtualization market size today?

Solution software holds the highest revenue, accounting for 64.22% of 2025 spending, while services are growing fastest at 24.05% CAGR.

Why is Hybrid Cloud the fastest-growing deployment mode?

Hybrid models balance regulatory data-residency obligations with the elasticity of public clouds, resulting in a projected 27.62% CAGR through 2031.

How significant is Asia-Pacific to future expansion?

Asia-Pacific is expected to post a 25.05% CAGR, led by digital transformation projects in China, India, and Southeast Asia that rely on logical data fabrics.

What key obstacle could stall adoption?

A global shortage of specialists in virtualization query optimization delays projects by up to ten months and reduces ROI for many organizations.

Page last updated on: