Europe Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

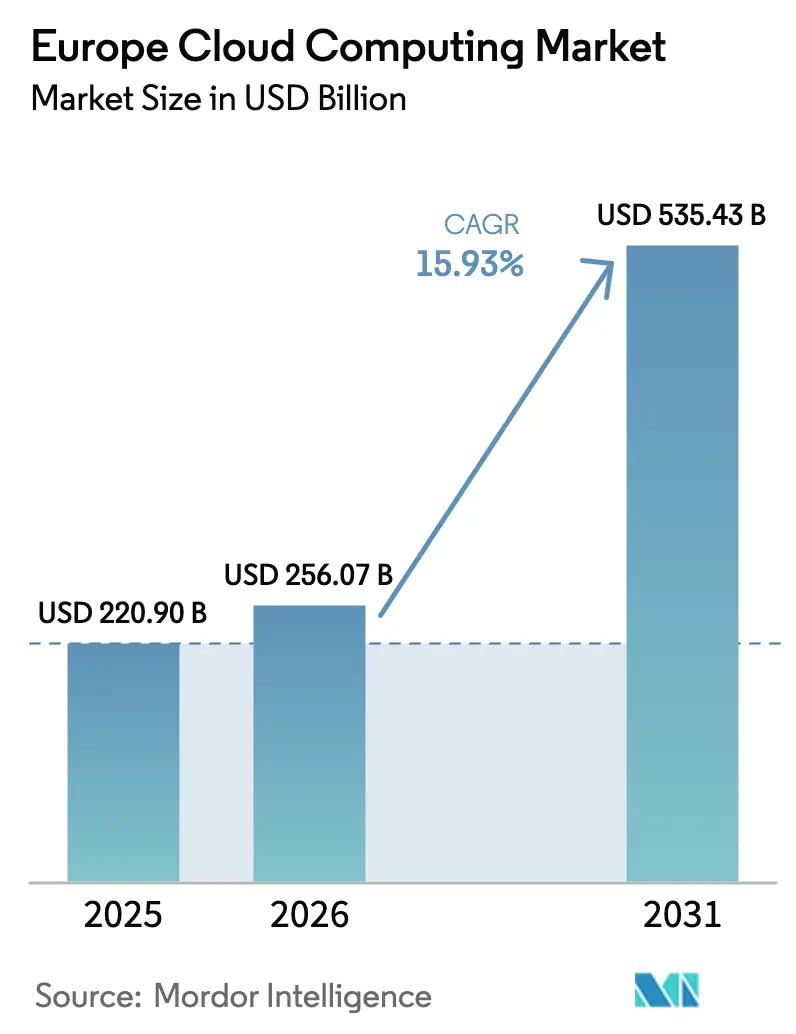

| Base Year Market Size (2025) | USD 220.90 Billion |

| Market Size (2026) | USD 256.07 Billion |

| Market Size (2031) | USD 535.43 Billion |

| Growth Rate (2026 - 2031) | 15.93% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cloud Computing Market Analysis by Mordor Intelligence

The Europe Cloud Computing market size is expected to grow from USD 220.90 billion in 2025 to USD 256.07 billion in 2026 and is forecast to reach USD 535.43 billion by 2031 at 15.93% CAGR over 2026-2031. This solid growth rests on escalating digital-sovereignty priorities, rising geopolitical tensions and an intricate regulatory environment that compels data to stay within European borders. A wave of sovereign-cloud programs ranging from Germany’s EUR 7.8 billion (USD 9.02 billion) AWS European Sovereign Cloud build-out to France’s Bleu platform launch has altered infrastructure deployment models across the region. Measured energy-efficiency targets, developer demand for compliant platforms and public–private funding mechanisms continue to lift service uptake, while mounting antitrust inquiries signal future adjustments in competitive conduct. Energy-supply constraints and cyber-risk exposures act as counterweights yet also spur innovation in greener architectures and advanced security controls, keeping the Europe cloud computing market on an innovation-led trajectory.

Key Report Takeaways

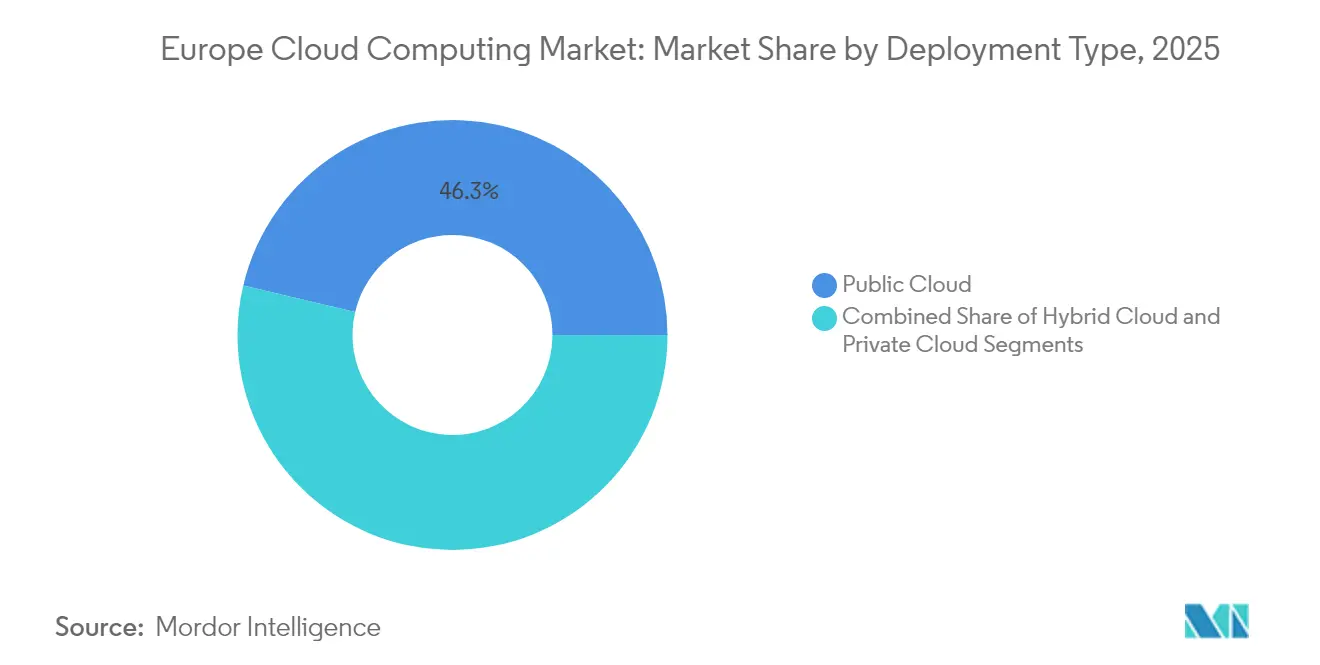

- By deployment type, Public Cloud led with 46.30% revenue share in 2025, while Hybrid Cloud is projected to expand at 18.68% CAGR through 2031.

- By service model, Software-as-a-Service held 40.65% of the Europe cloud computing market share in 2025, whereas Platform-as-a-Service is expected to post the fastest CAGR of 19.12% to 2031.

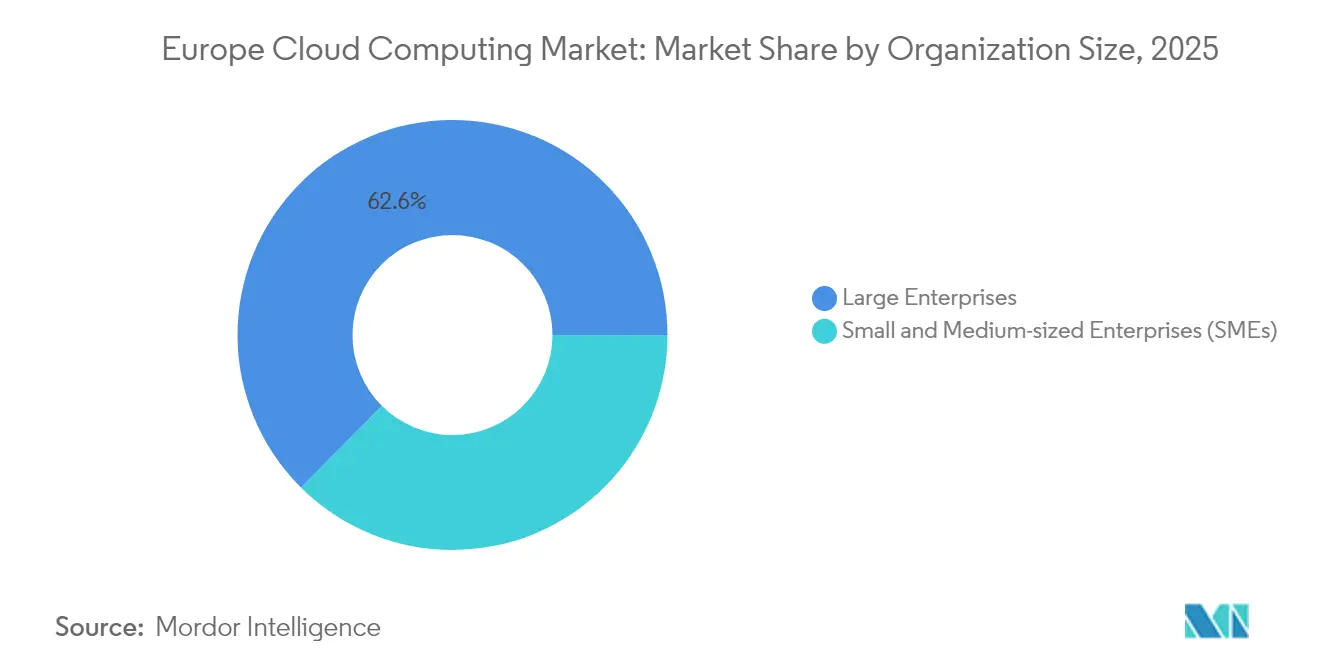

- By organization size, Large Enterprises commanded 62.55% of spend in 2025; the SME segment is accelerating at an 17.55% CAGR amid EU-backed skilling programs.

- By end-user industry, BFSI contributed 21.60% of demand in 2025, while Healthcare is on track to register a 19.05% CAGR to 2031.

- By geography, the United Kingdom retained 27.65% market share in 2025; Spain is forecast to lead growth at an 17.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple regions, with Europe contributing to the overall trajectory. The outlook on worldwide cloud computing market reflects how these are expected to evolve collectively.

Europe Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust government funding behind cloud-first digital agendas | +3.2% | EU-wide, especially Germany, France, Spain | Medium term (2-4 years) |

| Accelerated hyperscale build-outs in the FLAP-D corridor | +4.1% | Frankfurt, London, Amsterdam, Paris, Dublin | Short term (≤ 2 years) |

| SMEs pivoting from CapEx to OpEx IT spending | +2.8% | EU-wide, stronger momentum in Southern and Eastern Europe | Long term (≥ 4 years) |

| Gaia-X and sovereign-cloud programs nurturing local ecosystems | +2.9% | Germany, France, Netherlands with spill-over across the bloc | Medium term (2-4 years) |

| Green-computing mandates pushing energy-efficient cloud architectures | +1.7% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Post-Schrems II push for in-region data residency and edge clouds | +3.5% | EU-wide, most pronounced in regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong Government Incentives for Cloud-First Digital Agendas

Fiscal backing sits at the heart of the Europe cloud computing market’s acceleration. Spain has earmarked 28.2% of its National Recovery and Resilience Plan budget for digital projects, whereas Germany’s AI strategy targets 25% enterprise adoption of AI and Big Data by 2025.[1]Government of Canada, “Information and Communications Technologies (ICT) market in Spain,” tradecommissioner.gc.ca Direct capital subsidies now pair with streamlined permitting and preferential energy allocation for new data centers, cutting project lead times. The European Commission has channelled EUR 810 million (USD 937.12 million) into the Digital Europe Programme to help deploy the European Health Data Space, underscoring the region’s willingness to bankroll sector-specific clouds. In France, the Bleu platform’s SecNumCloud 3.2 qualification signals how national endorsement boosts local providers’ credibility. Parallel moves such as the Netherlands’ EUR 200 million (USD 231.39 million) AI factory reflect policy ambition to reduce foreign-tech dependence while nurturing sovereign infrastructure.

Rapid Hyperscaler Data-Center Build-Out Across FLAP-D Hubs

Capital spending by the large hyperscalers remains the single biggest catalyst for the Europe cloud computing market. AWS is ploughing GBP 8 billion (USD 10.54 billion) into new UK capacity through 2028. Google allocated USD 640 million for Dutch expansion during 2024. Yet the growth axis is shifting south as energy ceilings and planning moratoria bite in FLAP-D cities: Spain alone has attracted EUR 33 billion (USD 38.18 billion) in commitments, tripling anticipated capacity to 600 MW by 2028. Hyperscalers are responding to grid congestion by spreading sites into Nordic and Tier-2 regions endowed with renewables and cool climates. Ireland’s freeze on new data-center connections until 2028 further illustrates the need for geographic diversification.

SME Shift from CapEx to OpEx for IT Infrastructure

With compliance costs for digital regulations reaching an estimated EUR 53 billion (USD 61.32 billion), self-managed servers have become increasingly impractical for many small businesses, driving the European cloud computing market toward subscription-based models. Only 41% of SMEs used cloud in 2024, a sizeable gap vis-à-vis multinationals; EU-funded programs such as CloudCamp4SMEs now cover 90% of AWS certification costs, easing entry barriers. Early adopters in manufacturing run Palantir Foundry to automate shop-floor analytics, demonstrating that cloud platforms simultaneously meet efficiency and regulatory needs. The Slovenia case shows tighter buyer-supplier digital links when SMEs deploy cloud, highlighting an ecosystem-wide network effect.

EU Gaia-X and Sovereign-Cloud Programs Catalyzing Local Ecosystems

From concept to reality, Gaia-X has seeded pan-European collaboration. The EuroStack alliance convenes more than 100 partners to build interoperable, sovereignty-focused infrastructure. Deutsche Telekom’s 8ra program plans 10,000 edge nodes by 2030, delivering low-latency workloads without leaving EU soil. Private-sector moves mirror the theme: Schwarz Group teamed with Google to introduce StackIT’s client-side encryption for regulated German customers. Luxembourg’s DEEP-OVHcloud partnership proves that sovereign ambitions are not confined to Europe’s largest economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Cyber-Attack Surface and Headline Data-Breach Incidents | -2.1% | EU-wide, most acute in finance and public administration | Short term (≤ 2 years) |

| Complex Multi-Jurisdictional Compliance (GDPR and Country Add-Ons) | -1.8% | EU-wide, with uneven national requirements | Medium term (2-4 years) |

| Swings in electricity prices pushing up total cloud costs | -1.5% | Germany, Netherlands, Ireland, with knock-on effects across FLAP-D hubs | Short term (≤ 2 years) |

| Shortfall of cloud-native engineers outside major tech hubs | -1.2% | Eastern and Southern Europe, smaller markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Cyber-Attack Surface and Headline Data-Breach Incidents

ENISA recorded a sharp rise in DDoS and ransomware events during 2024, raising board-level anxiety within finance, transport and public administration.[2]ENISA, “ENISA THREAT LANDSCAPE 2024,” securitydelta.nl The NIS2 Directive demands significant-incident reporting within 24 hours, inflating compliance budgets but improving baseline security. Deutsche Bank, as part of its cloud migration strategy, has adopted advanced AI tools, including Google's Vertex AI platform and the state-of-the-art Gemini language models. These AI solutions are instrumental in streamlining critical operations, such as document management. The perceived exposure fuels demand for sovereign clouds that reduce foreign-law reach, though fragmented solutions may heighten operational complexity for multinational users.

Complex Multi-Jurisdictional Compliance (GDPR and Country Add-Ons)

While GDPR offers a baseline, member states overlay extra provisions that complicate scale-up plans. Amsterdam’s building pause and the Netherlands’ restrictive policies illustrate how local rules can override EU directives, forcing site-selection pivots.[3]Greenberg Traurig LLP, “Challenges in the Dutch Data Center Market,” gtlaw.com Spain now obliges hyperscalers to bid in formal tenders before constructing data centers, adding procedural delays. Divergent NIS2 transpositions only nine countries were compliant by early 2025 create uneven playing fields that impede providers looking for EU-wide coverage. For SMEs, the administrative load compounds existing skill gaps, elongating adoption cycles and tempering the otherwise rapid expansion of the Europe cloud computing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Architectures Gain Sovereignty Edge

Hybrid Cloud adoption grew at 18.68% CAGR through 2031, outpacing other models as enterprises blended private control with public scale. Hybrid’s momentum became visible when AWS revealed a EUR 7.8 billion (USD 9.02 billion) European Sovereign Cloud initiative designed to deliver isolated control planes and customer-chosen data locations. In parallel, Deutsche Bank migrated 260 applications to Google Cloud while retaining sensitive workloads on-premises, confirming that risk-heavy sectors can modernize without surrendering regulatory compliance.

Enterprises increasingly view hybrid architectures as a hedge against jurisdictional volatility, sustaining the Europe cloud computing market’s resilience. Energy-aware workload placement—processing low-latency AI inference near users while running archives in Nordic megasites—has widened the deployment palette. As a result, the Europe cloud computing market size attributed to hybrid solutions is expected to expand faster than the overall baseline, underscoring hybrid’s pivotal role in sovereign compliance strategies.

By Service Model: Platform Services Drive Developer Sovereignty

Platform-as-a-Service revenue registers the highest trajectory at 19.12% CAGR to 2031, signalling a developer push for managed runtimes located entirely within EU borders. Hopsworks and OVHcloud launched an AI PaaS that emphasises energy efficiency without exporting data, strengthening the Europe cloud computing market’s local value chain. Software-as-a-Service continues to dominate absolute spend thanks to office productivity and CRM suites, yet platform services introduce stickier developer ecosystems that anchor workloads regionally.

This narrative suggests a gradual pivot from application-only adoption to deeper platform loyalty. Companies integrating PaaS enjoy shorter innovation cycles, bolstering competitiveness while meeting complex compliance tests. Strong governance tooling embedded in local platforms limits legal exposures from extraterritorial demands, reinforcing demand intensity across the Europe cloud computing industry.

By Organization Size: SMEs Accelerate OpEx Transition

Large Enterprises still capture 62.55% of spend, but SMEs post an 17.55% CAGR as funding and training programs narrow the skills gap. CloudCamp4SMEs aims to qualify 1,000 professionals, lifting adoption in manufacturing and retail micro-segments. The resulting surge is reshaping procurement models: leasing cloud resources removes upfront server outlays, freeing cash for core operations and compliance upgrades.

The Europe cloud computing market size tied to SMEs could reach double-digit USD billion scale by the end of the period, though persistent talent shortages remain a risk. Country-level stimulus—such as voucher schemes in Eastern Europe—helps offset skill deficits, ensuring that smaller firms are no longer sidelined in the digital-sovereignty landscape. The transition also heightens demand for managed security services tailored to small budgets.

By End-User Industry: Healthcare Leads Digital Transformation

Healthcare’s 19.05% projected CAGR reflects the European Health Data Space mandate that requires interoperable yet sovereign-compliant data flows. Funding of EUR 810 million (USD 937.12 million) and anticipated EUR 11 billion (USD 12.73 billion) savings provide both carrot and stick for hospital systems moving clinical records to cloud services. BFSI remains the largest single vertical at 21.60%, leveraging cloud for real-time risk analytics and secure document processing.

Manufacturing’s uptake accelerates through Industry 4.0 proofs such as Palantir Foundry, which delivers production data into regulatory dashboards. Education, telecom and public administration follow, each constrained by sector-specific rules yet drawn by efficiency gains. Collectively, these verticals diversify demand, cushioning the Europe cloud computing market against cyclical shocks in any one industry.

Geography Analysis

The United Kingdom accounted for 27.65% of the Europe cloud computing market in 2025, supported by AWS’s GBP 8 billion (USD 10.54 billion) infrastructure infusion scheduled through 2028. Potential remedies arising from the Competition and Markets Authority probe into Amazon and Microsoft could diversify supplier options over the forecast horizon. Germany follows, anchored by the Brandenburg sovereign-cloud region and ongoing Gaia-X leadership. France benefits from the Bleu platform’s SecNumCloud accreditation, positioning Paris as a public-sector cloud hub, while Italy secures EUR 1.2 billion (USD 1.39 billion) AWS expansion that may inject USD 880 million into GDP and create 5,500 jobs.

Spain epitomises the market’s fastest ascent, recording an 17.98% CAGR to 2031 on the back of EUR 33 billion (USD 38.18 billion) hyperscale pledges and favourable renewable-energy economics. Madrid remains the primary colocation city, yet Aragon hosts five new AWS sites drawing 10,800 GWh, a figure surpassing regional electricity use in 2023. The Netherlands, historically part of the FLAP-D core, wrestles with zoning caps and parliamentary calls for reduced reliance on U.S. vendors, prompting some providers to redirect builds to neighbouring countries.

Nordic nations capture AI-centric workloads through low-carbon grids and natural cooling, while Eastern Europe’s cost-effective labour and high-growth SME base broaden adoption. Luxembourg’s sovereign-cloud rollout exemplifies small-state strategy to punch above weight in digital autonomy. Ireland faces grid bottlenecks after data centers reached 21% of national power draw, driving policy reassessment. Collectively, the geographic mosaic underlines how energy policy, land-use planning and sovereignty considerations now dictate the evolution path of the Europe cloud computing market.

Analysis of the cloud computing market by Mordor Intelligence spans multiple other regional evaluations across North America, Asia, and South America, supported by country-level insights for Spain, France, United Kingdom, Germany, Italy, and South Korea, wherein local market conditions keep varying from one country to another.

Competitive Landscape

A concentrated structure defines the Europe cloud computing market, with AWS and Microsoft Azure each approaching 40% share, followed by Google at low-double digits. OVHcloud leads indigenous providers, posting EUR 993 million (USD 1.15 billion) FY2024 revenue and capitalising on water-cooling plus local-data promises. Sovereign-cloud ventures like EuroStack and Virt8ra seek to erode hyperscaler hegemony by pooling European capacity and aligning with Gaia-X standards.

Strategic moves reveal a bifurcated playbook: hyperscalers embed locally segregated controls, while European vendors emphasise compliance and sustainable operations. Vodafone’s USD 1.5 billion, 10-year partnership will shutter its own data centers and migrate estates to Azure, illustrating a partnership-over-parity approach. Schwarz Group’s sovereign workplace partnership with Google shows demand for hybrid models that mix global scale and client-side encryption.

Regulatory oversight intensifies competition. The UK Digital Markets Act could impose conduct codes and functional-separation requirements once AWS and Microsoft gain “Strategic Market Status”. Parallel parliamentary inquiries in the Netherlands advocate favouring EU-origin software in public procurement. Such interventions aim to temper market lock-in and encourage home-grown alternatives, making compliance aptitude and sustainability metrics critical differentiators inside the Europe cloud computing market.

Europe Cloud Computing Industry Leaders

Alibaba Group Holding Limited

Amazon Web Services (AWS)

Google LLC

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: AWS established its European Sovereign Cloud as a separate company, strengthening regulatory independence.

- June 2025: Virt8ra Sovereign Cloud expanded with six new European providers.

- May 2025: BSO introduced DataOne, a 15 MW French AI hosting center scaling to 400 MW by 2028.

- May 2025: AWS planned EUR 15.7 billion (USD 18.16 billion) Spain investment through 2033.

Europe Cloud Computing Market Report Scope

Cloud computing provides on-demand access to computer resources, particularly data storage and processing power, without requiring direct management by the user. Computing resources, including physical and virtual servers, data storage, networking capabilities, application development tools, software, and AI-powered analytics, are accessible over the Internet with a pay-per-use pricing model.

The report covers European cloud computing companies, and the market is segmented by type (public cloud, private cloud, and hybrid cloud), organization type (SMEs and large enterprises), end-user industries (manufacturing, education, retail, transportation, and logistics, healthcare, BFSI, telecom, and IT, government and public sector), and country (the United Kingdom, Germany, France, Italy, and the Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Education |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance (BFSI) |

| Telecom and IT Services |

| Government and Public Sector |

| Utilities, Media and Entertainment, Others |

| Other End-user Industry |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Deployment Type | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organization Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Industry | Manufacturing |

| Education | |

| Healthcare and Life Sciences | |

| Banking, Financial Services and Insurance (BFSI) | |

| Telecom and IT Services | |

| Government and Public Sector | |

| Utilities, Media and Entertainment, Others | |

| Other End-user Industry | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe cloud computing market by 2031?

The Europe cloud computing market is expected to reach USD 535.43 billion by 2031.

Which deployment model is growing fastest in Europe?

Hybrid Cloud is forecast to advance at 18.68% CAGR as firms combine on-premises control with public scalability.

Why is Spain considered a rising cloud hub?

Spain has attracted EUR 33 billion in hyperscale commitments and offers renewable-energy access, low land costs and supportive regulation.

How will new EU regulations affect healthcare cloud adoption?

The European Health Data Space rules require sovereign storage of patient records, driving a 19.05% CAGR in healthcare cloud spending.

Which providers dominate the European market today?

AWS and Microsoft Azure each hold near-40% share, while OVHcloud leads indigenous competitors.

What role does energy sustainability play in future capacity planning?

EU mandates for carbon-neutral data centers by 2030 and grid congestion in key cities are pushing operators toward renewable-rich Nordic and Southern regions, shaping site selection.

Page last updated on: