Spain Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.96 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 1.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Containerboard Market Analysis by Mordor Intelligence

The Spain containerboard market size was valued at USD 1.96 billion in 2025 and estimated to grow from USD 2.02 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 1.53% during the forecast period (2026-2031). The Spain containerboard market remains shaped by a mature demand base, but its demand mix is shifting as food exports, parcel growth, and regulatory change alter grade selection and price realization. Spain’s role as Europe’s third-largest corrugated cardboard producer keeps the Spain containerboard market tied more to downstream consumption patterns than to tight domestic capacity. The operational rollout of the EU Packaging and Packaging Waste Regulation in August 2026 is strengthening the position of recyclable fiber formats, even where that effect is not fully visible in headline volume growth. Competitive behavior in the Spain containerboard market is also moving toward integration and selective consolidation, as larger producers use scale, recovered-fiber access, and logistics reach to widen their advantage. The main pressure on the Spain containerboard market over 2026-2031 comes from input costs, especially recovered fiber and natural gas, rather than from an underlying weakening in end-use demand.

Key Report Takeaways

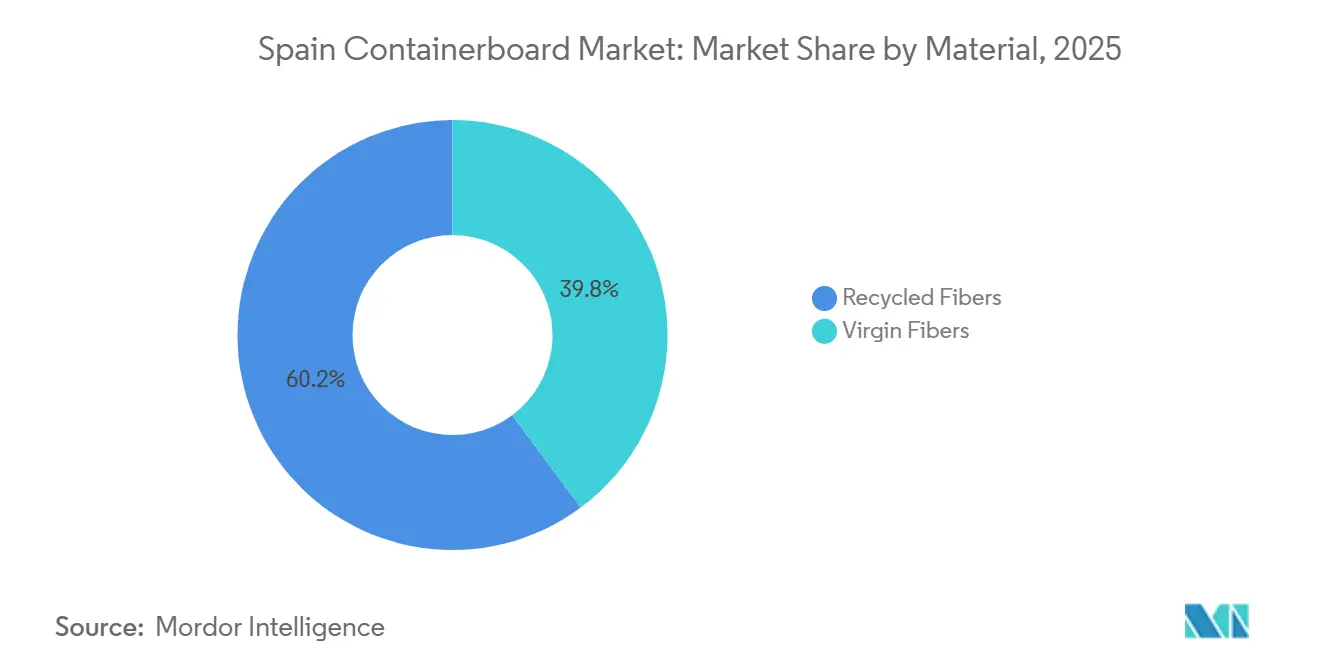

- By material, recycled fibers captured 60.18% of the Spain containerboard market share in 2025.

- By product type, the Spain containerboard market size for the kraftliners segment is forecast to advance at a 2.03% CAGR through 2031.

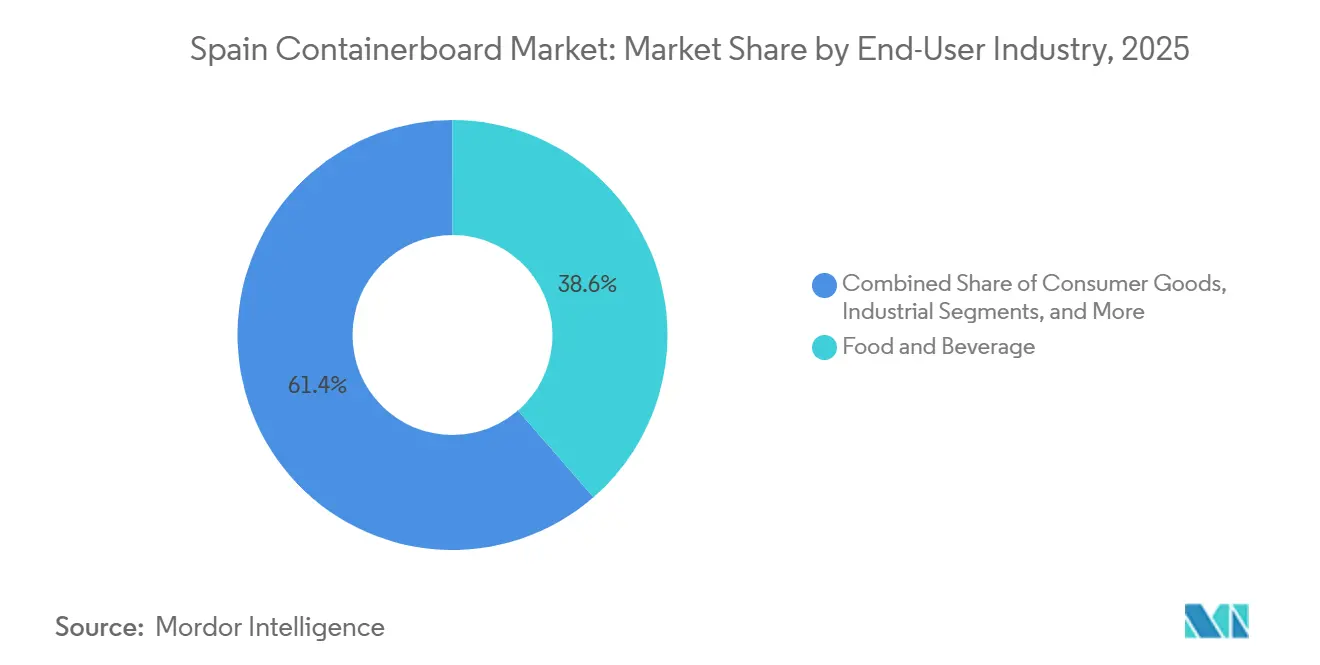

- By end-user industry, food and beverage captured 38.62% of the Spain containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food Export And Fresh-Produce Corrugated Demand | +0.4% | National, with concentrated gains in Andalusia, Valencian Community, and Murcia | Short term (≤ 2 years) |

| E-Commerce Parcel And Right-Sizing Growth | +0.35% | National, with early intensity in Madrid, Barcelona, and Valencia logistics zones | Short term (≤ 2 years) |

| Recyclability Rules Favor Fiber Packaging | +0.3% | EU-wide compliance pressure with intensity in Spanish food and FMCG supply chains | Medium term (2-4 years) |

| Strong Recovered-Fiber And Recycling Infrastructure | +0.2% | National, with Aragon, Catalonia, and Basque Country as fiber-processing anchors | Medium term (2-4 years) |

| Automation-Ready Packaging Demand In Iberian Logistics | +0.15% | National, concentration in Zaragoza and Barcelona logistics corridors | Medium term (2-4 years) |

| Agricultural-Residue Nanocellulose For Stronger Recycled Linerboard | +0.1% | National, early-stage gains in Andalusia and Aragon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food Export And Fresh-Produce Corrugated Demand

Spain’s agrifood export base keeps the Spain containerboard market closely linked to fresh-produce trade flows. Fresh fruit and vegetable exports generated EUR 18.666 billion in 2025 (USD 20.2 billion), even as shipped volume declined by 4%, indicating that higher-value categories lifted packaging value intensity per unit moved.[1]FEPEX, “La Exportación De Frutas Y Hortalizas En 2025 Desciende Un 4% En Volumen Y Sube El Mismo Porcentaje En Valor Alcanzando 12 Millones De Toneladas Y 18.666 Millones De Euros,” FEPEX Andalusia accounted for 33% of national fruit and vegetable export volume in 2025, while the Valencian Community contributed 28%, making both regions central ordering points for corrugated demand. As exporters shift from lower-value produce to berries, stone fruits, and specialty vegetables, packaging specifications become tighter and average board grades rise. Spain’s agrifood exports to China reached USD 7.7 billion in 2024, which lengthens logistics distances and raises crush resistance and stacking requirements for corrugated formats serving export chains. The EU-Mercosur agreement, signed in December 2024, is expected to boost Spain’s trade by 0.6%-1.4%, supporting further demand for export-ready boards suited to multi-modal handling. This keeps the Spain containerboard market tied not only to export volumes, but also to the changing value mix of what Spain ships abroad.

E-Commerce Parcel And Right-Sizing Growth

Parcel activity is providing the Spain containerboard market with a steady source of incremental demand for converted board. Spain handled a record 1.303 billion e-commerce shipments in 2024, up 240% from 538 million in 2019, while logistics package volumes are running at 3.3 million per day in 2026. ICEX projected 5.4% e-commerce growth for 2025, which supports continuing parcel throughput into the current period. The material change is not only in box count but also in format precision, as logistics networks move toward right-sized, variable-geometry packaging that better fits parcel lockers and automated handling lines. Spanish logistics operators have adopted route optimization and warehouse automation at high rates, which favors packaging inputs that can support automated fulfillment and efficient cube utilization. Demand is also broadening into grocery and quick-commerce channels, where corrugated secondary packaging remains the standard transport choice across dense urban distribution networks. That pattern gives the Spain containerboard market more support from value-added converted formats than from simple commodity volume alone.

Recyclability Rules Favor Fiber Packaging

Regulatory change is now working through the Spain containerboard market as a practical purchasing factor rather than as a distant policy theme. Regulation (EU) 2025/40 entered into force in February 2025 and became generally applicable on August 12, 2026, requiring all packaging on the EU market to be recyclable by January 1, 2030.[2]European Parliament and Council, “Regulation (EU) 2025/40 On Packaging And Packaging Waste,” Official Journal of the European Union Paper and cardboard must achieve an 85% recycling rate by 2030, while Spain’s corrugated sector was already operating at a 90% recovery rate in 2025, placing local fiber formats in a favorable compliance position. The same regulation bans single-use plastic packaging for fresh fruit and vegetables weighing less than 1.5 kg from January 1, 2030, redirecting attention toward fiber-based trays and wraps. Eco-modulated Extended Producer Responsibility fees also matter, because weaker recyclability grades can carry higher fee burdens before outright bans take effect.[3]EUROPEN, “PPWR Survival Guide,” EUROPEN That shifts total packaging cost calculations in favor of mills and converters that can document design-for-recycling credentials. For the Spain containerboard market, this means regulatory alignment is increasingly becoming a source of pricing resilience and customer preference.

Strong Recovered-Fiber And Recycling Infrastructure

Recovered paper collection remains one of the main structural supports for the Spain containerboard market. Spain’s corrugated sector achieved a 90% recovery and recycling rate in 2025, while the European benchmark for corrugated reached 95%, which confirms that Spain already operates close to best-practice circularity levels.[4]AFCO, “El Cartón Ondulado En España 2025,” AFCO Integrated operators are extending that advantage, and Saica Natur completed the acquisition of FCC Ámbito’s paper recovery operations in Spain, adding 7 facilities and bringing its plant count in Spain to 36. This kind of network reduces exposure to abrupt OCC sourcing disruptions and gives integrated mills more stable throughput when market conditions weaken. Spain’s legal ban on the open burning of agricultural residues is also opening a longer-term path for feedstock diversification, as residues such as horticultural waste and wheat straw are being studied as reinforcement inputs for recycled paperboard. Research in Spain has already shown that agricultural-residue-derived nanocellulose can improve performance properties in recycled linerboard systems. This does not change near-term raw material dependence, but it strengthens the medium-term operating base of the Spain containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Fiber And Energy Cost Volatility | -0.25% | National, with highest exposure at recycled-linerboard and testliner mills in Aragon and Basque Country | Short term (≤ 2 years) |

| Reusable Transport Packaging Mandates | -0.15% | EU-wide, with compliance pressure concentrated in Spanish grocery retail and beverage distribution | Medium term (2-4 years) |

| Fresh-Produce Shift Toward Reusable Plastic Crates | -0.1% | Andalusia, Valencian Community, and Murcia, Spain’s primary fresh-produce export corridors | Medium term (2-4 years) |

| Mill-Outage Risk In Spain’s Recycled Containerboard Base | -0.05% | National, concentrated at integrated single-site mill complexes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recovered Fiber And Energy Cost Volatility

The main risk to the Spain containerboard market remains cost transmission rather than a collapse in end demand. Recycled fibers accounted for 60.18% of demand in 2025, indicating that a large part of the market remains exposed to swings in OCC prices and energy costs. European OCC benchmark prices moved down from EUR 120 (USD 135.4) per tonne in early autumn 2025 to EUR 105 (USD 118.5) per tonne by year-end, reflecting weak downstream demand, China’s suspension of dry-ground recycled pulp imports, and excess inventories in Western Europe. That price decline did not eliminate risk, as unstable fiber pricing continues to disrupt margin planning and inventory strategy for non-integrated producers. Energy exposure adds another layer, with 68% of energy consumed in EU recycled containerboard production derived from natural gas, and a EUR 10 (USD 11.2) per MWh rise in gas prices lifting variable production costs by up to EUR 20 (USD 22.5) per tonne for recycled packaging paper. For the Spain containerboard market, this pressure is strongest at recycled-grade mills that lack captive power, biomass support, or long-term energy hedging.

Reusable Transport Packaging Mandates

Reusable transport rules create a more targeted headwind for the Spain containerboard market. The PPWR requires that at least 40% of transport packaging operate within reuse systems by January 1, 2030, and that can favor rigid plastic pooling systems in some logistics applications if buyers interpret reuse as the priority criterion. Cardboard boxes are exempt from those reuse targets under Article 29.4, which limits direct mandatory displacement of corrugated formats. The pressure, therefore, comes less from a legal ban and more from procurement behavior, retailer sustainability targets, and packaging system redesign. Spain’s logistics profile complicates large reuse loops because road transport accounts for more than 95% of goods movement, and return logistics costs can dilute the advantage of washable reusable systems. That matters most in grocery and beverage distribution, where high circulation density is required for pooled systems to operate efficiently. The effect on the Spain containerboard market is therefore selective and gradual, but it remains relevant in transport-heavy fresh distribution chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Linerboard Dominance Holds, While Virgin Fiber Gains At The Margin

Recycled fibers accounted for 60.18% of the Spain containerboard market in 2025, giving this segment the leading position across the feedstock mix. That share reflects Spain’s established paper mill base, high corrugated recovery rates, and the cost advantage of recovered-paper sourcing over imported virgin kraft in many standard applications. Saica’s PM9 at El Burgo de Ebro produces more than 400,000 metric tons per year of lightweight recycled containerboard from 100% recovered fiber, and the machine completed a planned upgrade in March 2026 to improve efficiency and sustainability. Spain’s 90% corrugated recovery rate supports stable feedstock access, although mills without captive collection remain exposed when OCC prices fluctuate within the EUR 105-120 (USD 118-135) per tonne range seen in 2025.

Virgin fibers are forecast to grow at a 1.79% CAGR through 2031, making them the faster-growing feedstock base even from a smaller starting point. That growth reflects stronger demand from premium fresh-produce exports and e-commerce applications, where burst strength and crush resistance still favor higher-performance fiber inputs. In segment terms, virgin fibers are the faster-moving part of the Spanish containerboard market size, where performance specifications matter more than raw material cost alone. Ence’s planned bleached-recycled-fiber bioplant at As Pontes, backed by EUR 24.7 million (USD 27.8 million) in provisional government funding and supported by an integrated environmental authorization issued in August 2025, shows how producers are trying to narrow the performance gap between recycled and virgin-style grades. The Spain containerboard industry therefore remains led by recycled fiber, but the commercial pull toward stronger and more specialized grades is giving virgin-linked solutions a modest growth edge.

By Product Type: Testliners Remain Core, While Kraftliners Benefit From Premium Demand

Testliners held 41.76% of the Spain containerboard market share in 2025, which kept them as the largest product category. Their scale reflects Spain’s broad food supply chains and the depth of its recycled-fiber manufacturing system, where standardized demand still favors high-volume recycled liner grades. Saica’s Zaragoza paper complex, with PM6 capacity of 235,000 metric tons per year and PM7 capacity of up to 330,000 metric tons per year, illustrates the production scale that supports testliner availability in Spain. Fluting remains an important part of the mix, but its growth is more closely tied to total corrugated output than to a distinct end-use shift.

Kraftliners are forecast to advance at a 2.03% CAGR through 2031, making them the fastest-growing product segment in the Spain containerboard market. Their momentum comes from fresh-produce exporters shipping on longer-haul routes and from e-commerce users who require stronger stacking under mixed logistics conditions. In product terms, kraftliners represent the fastest-growing segment of the Spanish containerboard market as customers move toward stronger top-liner performance and better packaging presentation. Smurfit Westrock’s launch of the fully recyclable Nertop Stretch Kraft paper pallet wrap from its Nervión plant in January 2025 also signaled commercial traction for higher-specification kraft-based logistics formats inside Spain’s own supply chain. The PPWR’s PFAS restrictions from August 2026 further support fiber-based food-contact packaging choices, adding another layer of support to the grade-mix shift toward stronger, cleaner kraft-derived solutions.

By End-User Industry: Food And Beverage Provides Scale, While Consumer Goods Expands Faster

Food and beverage accounted for 38.62% of the Spain containerboard market size in 2025, making it the largest end-user segment by value. This position aligns with AFCO data showing that food accounted for 61% of all corrugated board consumed in Spain in 2025, keeping agrifood shipment volumes closely linked to mill order patterns. Spanish law, under Real Decreto 888/1988, also supports single-use packaging for fresh, unwrapped perishable goods, thereby limiting substitution risk in a significant part of domestic food distribution. The segment also carries a higher density of food-grade linerboard and multi-ply corrugated structures, which supports value even when shipment units move unevenly across categories.

Consumer goods are projected to grow at a 1.87% CAGR through 2031, making it the fastest-growing end-user segment in the Spanish containerboard market. That expansion is tied to parcel-intensive retail categories such as fashion, electronics, and household goods, along with continued growth in online order volumes and fulfillment activity. Hinojosa’s BottleClip Carrier, a recyclable cardboard alternative to plastic film for beverage multipacks, shows how substitution within packaged consumer products is widening fiber demand beyond standard shipping cases. Logistics and e-commerce together accounted for 9.14% of corrugated board demand in 2025, up sharply from 4.3% in 2023, which shows how quickly end-use demand is shifting toward fulfillment-led packaging needs. The Spain containerboard market therefore remains anchored in food and beverage, while consumer goods is becoming the clearer source of incremental growth.

Geography Analysis

Spain’s position as Europe’s third-largest corrugated cardboard producer in 2025 shaped the geographic pattern of the Spain containerboard market around manufacturing clusters, export agriculture, and logistics corridors. Aragon remains the core containerboard production base, led by Saica’s twin-mill footprint at El Burgo de Ebro and Zaragoza, where combined recycled containerboard capacity exceeded 1 million metric tons per year. That location works because it sits close to the Ebro Valley agricultural chain and retains efficient road and rail links to Mediterranean ports and central European routes. Catalonia represents the country’s most advanced converting base, and Saica Pack’s Sant Esteve Sesrovires facility in Barcelona began operations in early 2025 following a EUR 100 million (USD 112.8 million) investment that increased combined capacity by up to 45%. The Basque Country also remains important through containerboard converting and recovery activity tied to industrial supply chains and cross-border demand cycles.

The Mediterranean produce corridor is the main regional demand engine for the Spain containerboard market. The Valencian Community and Murcia together generated 48% of Spain’s fresh fruit and vegetable export volume in 2025, which makes this arc the central destination for agricultural corrugated demand. Companies such as Vegabaja Packaging and Cartonajes de la Plana are positioned inside this corridor, and Grupo La Plana invested EUR 14 million (USD 15.8 million) in automated high-rack storage at Castellón in February 2026 to improve logistics efficiency and service speed. Andalusia is the largest single fresh-produce region, accounting for 33% of export volume and greenhouse-vegetable export value of EUR 4.262 billion (USD 4.81 billion) in the 2024/25 campaign. Research based on Andalusian horticultural residues has also shown that agricultural waste can improve recycled linerboard performance, including a 62.68% increase in burst index from a 4.5% addition of TEMPO-oxidized eggplant-derived nanofibers in tested systems.

Central and inland regions are becoming more relevant as logistics balancing points within the Spain containerboard market. Extremadura and Castile-La Mancha are gaining attention because their central-peninsular position lowers distribution costs for agricultural and industrial customers serving both Spain and Morocco. Ondupack’s greenfield facility in Navalmoral de la Mata became operational in 2025 with a EUR 49 million (USD 55.3 million) investment and total capacity of 200 million m² per year, designed partly around Morocco-bound fresh-produce flows. Madrid strengthens demand from the logistics side, as the region handles a meaningful share of Spain’s 3.3 million daily e-commerce packages in 2026 and therefore favors standardized, automation-ready corrugated formats. La Rioja and Navarre add a smaller but steady stream of demand tied to wine, food processing, and higher-graphics secondary packaging for branded goods.

Competitive Landscape

The Spanish containerboard market is moderately fragmented, with 2 to 3 vertically integrated multinationals leading the standardized board segment, while a wide range of regional producers compete on speed, location, and customization. More than 66 corrugating companies operated 89 factories in Spain in 2025, which kept the mid-tier dispersed even as scale advantages strengthened at the top. Smurfit Westrock and Saica remain the clearest reference points because both combine paper, packaging, and network reach with stronger access to downstream demand. Smurfit Westrock’s Iberian and Moroccan operations generated EUR 1.2 billion (USD 1.3 billion) in revenue in 2025, and 70% of its customers were in food and beverage, which makes it a useful indicator of where structural demand is concentrated in Spain.

Consolidation is becoming one of the defining competitive themes in the Spain containerboard market. Smurfit Westrock stated in May 2026 that it plans to pursue acquisitions in Spain and Europe as part of its 2026-2030 strategy, reflecting a view that Europe's packaging sector remains far more fragmented than the United States' packaging sector. Saica is reinforcing a different but related advantage through vertical integration, and the January 2026 addition of FCC Ámbito’s 7 recovery facilities expanded its domestic recovered-paper collection platform. That matters because feedstock security has become a more durable competitive moat than simple mill scale during periods of OCC and energy volatility. Smurfit Westrock also entered this phase with strong financial capacity after the earlier Smurfit Kappa-Westrock merger, which reportedly generated more than USD 400 million in synergies and widened its room for further deal activity.

Technology and process investment are also separating stronger players from the rest of the Spain containerboard market. Hinojosa committed more than EUR 60 million (USD 67.7 million) in 2025 to capacity, automation, and energy recovery at its Alquería paper mill, showing that circular energy systems are becoming a strategic tool rather than a side project. The LIFE-NANOPAP work, in which Hinojosa participated as an industrial partner, also showed an active push to bring cellulose nanofibers into recycled containerboard applications at a commercial scale. Smaller groups such as Ondupack, Vegabaja, and Cartonajes companies are responding by focusing on export niches, automated warehousing, and local service responsiveness rather than direct price competition with the largest integrated suppliers. This leaves the Spain containerboard market competitive at the regional level, but increasingly tilted toward integrated producers in the most scale-sensitive parts of the value chain.

Spain Containerboard Industry Leaders

SAICA Pack, S.L.

Smurfit Westrock plc

International Paper Company

Hinojosa Packaging Group, S.L.

Cartonajes de la Plana, S.L.U.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit Westrock's CEO for Spain, Portugal, and Morocco publicly confirmed plans to pursue acquisitions in Spain and Europe as part of the company's 2026-2030 strategic plan, citing the fragmented European packaging market as a consolidation opportunity. The Iberian and Morocco region generated approximately EUR 1.2 billion (USD 1.36 billion) in 2025 revenue, with 90% originating from Spain, the group also noted that the Smurfit Kappa-Westrock merger had generated more than USD 400 million (EUR 354 million) in operating synergies.

- April 2026: Hinojosa Packaging Group reported 2025 consolidated revenue of EUR 847.5 million (USD 915.3 million), a 6% increase, confirming completion of the full integration of French packaging group ASV and an investment of more than EUR 60 million (USD 64.8 million) in capacity, automation, and the Alquería paper mill's energy-recovery system in 2025, the group now operates 24 plants across Spain, France, Portugal, and Italy, with over 3,000 employees.

- March 2026: Saica Group completed a planned upgrade of its PM9 paper machine at El Burgo de Ebro, Zaragoza, in collaboration with Voith, targeting further efficiency and sustainability improvements for a machine that produces more than 400,000 metric tons per year of lightweight recycled containerboard from 100% recovered fiber.

- February 2026: A fire broke out at Saica Group's Zaragoza paper production and recycling site on February 14, 2026, severely damaging machinery in one of two buildings, paper production was interrupted but partially restarted on February 16 under operating limitations, with the site hosting PM6 (235,000 metric tons/year) and PM7 (up to 330,000 metric tons/year) capacity, making this one of the most significant single-site production disruptions in Spain's containerboard sector in recent memory.

Spain Containerboard Market Report Scope

The Spain Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The Spain Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Spain containerboard market size?

The Spain containerboard market was valued at USD 1.96 billion in 2025 and is valued at USD 2.02 billion in 2026. It is forecast to reach USD 2.18 billion by 2031 at a 1.53% CAGR, according to Mordor intelligence.

Which material segment leads demand in Spain?

Recycled fibers led with a 60.18% share in 2025, supported by Spain's strong recovered-paper network and a 90% corrugated recovery rate.

Which product type is growing fastest through 2031?

Kraftliners are projected to grow the fastest at a 2.03% CAGR, helped by export packaging needs and demand for better strength in e-commerce and fresh produce.

Why does food and beverage remain so important for containerboard demand?

Food and beverage accounted for 38.62% of value in 2025, and food represented 61% of all corrugated board consumed in Spain, keeping agrifood shipments central to demand.

How is regulation changing packaging choices in Spain?

The PPWR is pushing brands toward recyclable formats, and paper and cardboard already fit the direction of the new rules better than many alternative packaging materials.

Which regions matter most for production and demand?

Aragon remains the main production hub, while Andalusia, Valencia, and Murcia are the strongest demand centers because of fresh-produce exports and packaging-intensive agricultural flows.

Page last updated on: