Chile Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

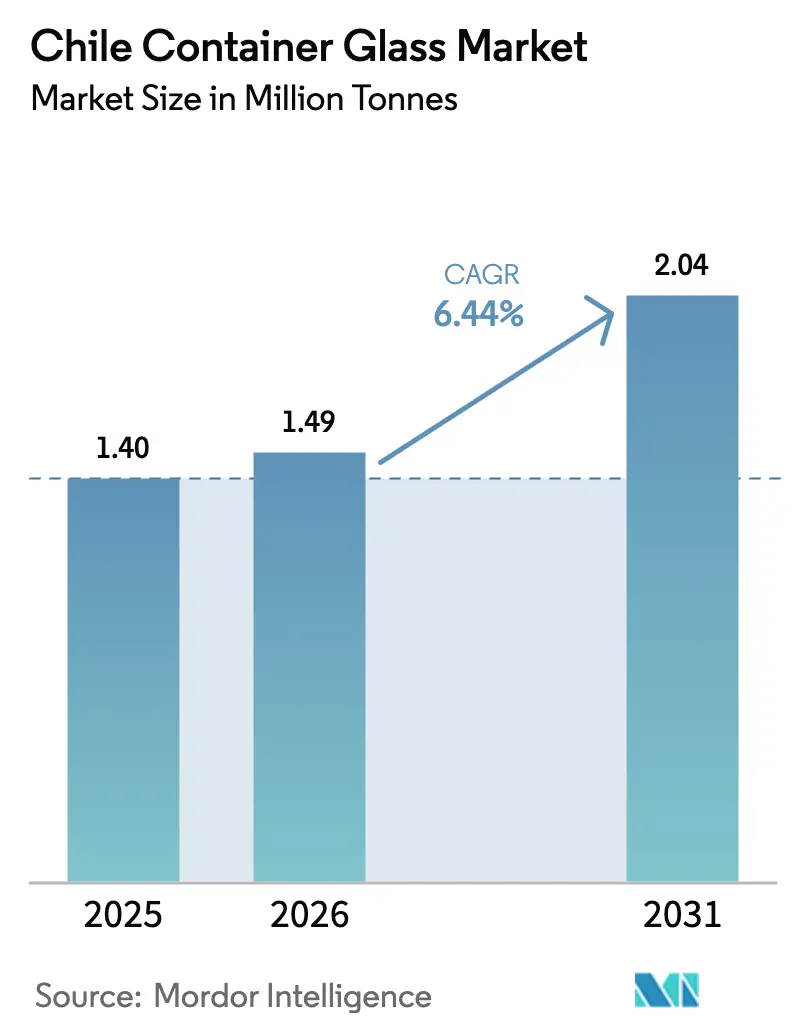

| Base Year Market Size (2025) | 1.40 Million tonnes |

| Market Volume (2026) | 1.49 Million tonnes |

| Market Volume (2031) | 2.04 Million tonnes |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Container Glass Market Analysis by Mordor Intelligence

The Chile Container Glass Market size was valued at 1.40 million tonnes in 2025 and estimated to grow from 1.49 million tonnes in 2026 to reach 2.04 million tonnes by 2031, at a CAGR of 6.44% during the forecast period (2026-2031). Strong momentum arises from mandatory extended producer responsibility (EPR) obligations, premium demand for alcoholic beverages, and export-oriented bottling requirements. Chile's container glass market also benefits from pending rules on single-use plastics, which encourage food-service outlets to adopt reusable vessels, as well as announced furnace modernization programs that reduce fuel intensity. Competitive headwinds stem from the substitution of aluminum and PET; however, regulatory incentives, rising recycled-content goals, and trade-barrier relief help offset material losses.

Key Report Takeaways

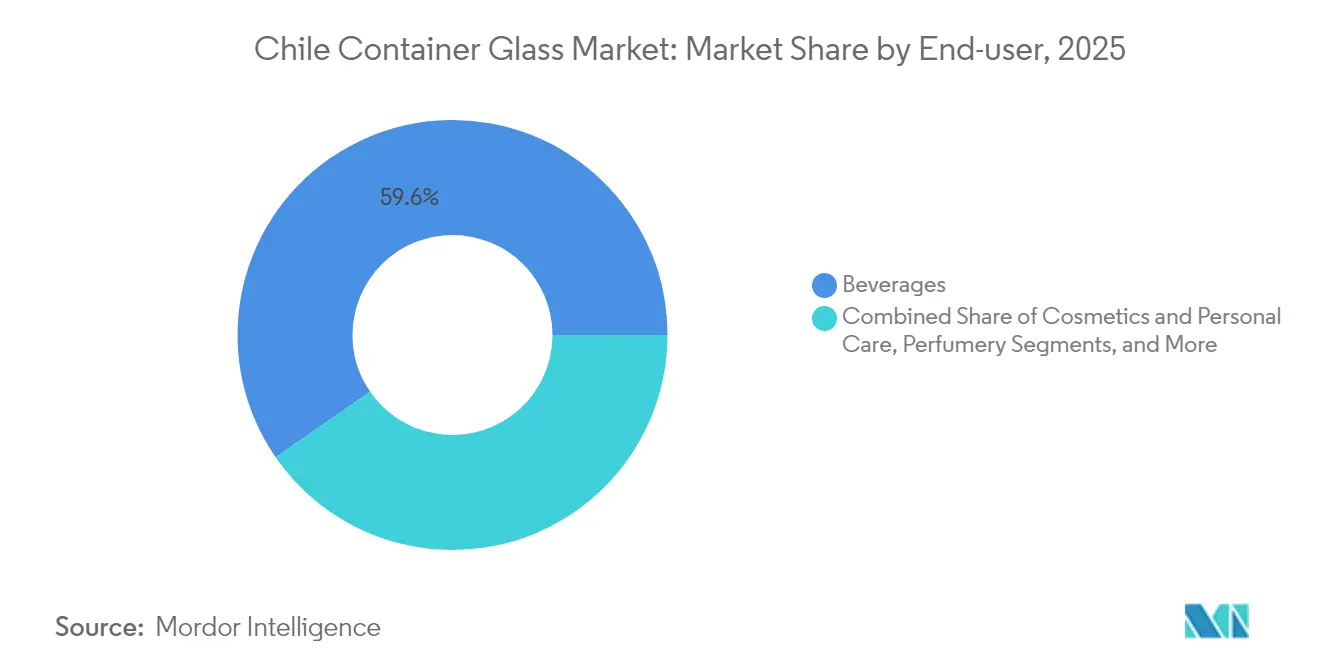

- By end user, beverages accounted for 59.62% of the Chilean container glass market share in 2025.

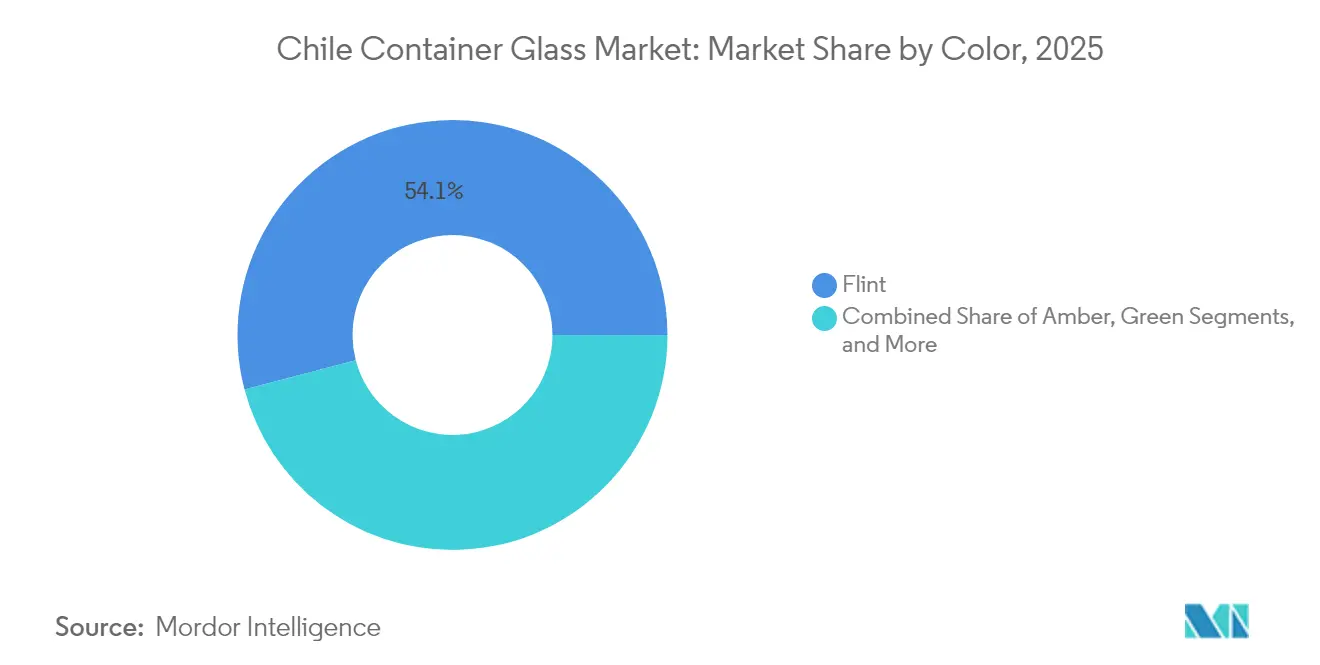

- By color, the Chile container glass market size for amber is projected to expand at a 7.86% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand for alcoholic beverages | +2.1% | Central Valley, national | Medium term (2-4 years) |

| Surge in sustainable, eco-friendly packaging adoption | +1.8% | Santiago metro, export corridors | Long term (≥ 4 years) |

| Premiumization of domestic wine and craft spirits | +1.2% | Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Rising exports require high-quality glass | +1.0% | Maipo, Colchagua, Casablanca | Short term (≤ 2 years) |

| Impending cannabis-beverage legalization | +0.3% | National | Long term (≥ 4 years) |

| EPR law accelerating closed-loop recycling | +0.7% | Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Demand for Alcoholic Beverages

Premium wine producers rely on heavier flint and green bottles to signal quality, and most export destinations require certified packaging integrity that glass fulfills. Domestic craft spirits start-ups grew at double-digit volumes in 2024 and continue to specify customizable shapes that differentiate their shelf presence. Wineries also report higher fill-line efficiencies when using standardized 750ml glass, which lowers unit costs for bulk export preparations.[1]International Trade Administration, “Preliminary Determinations in the AD Investigations of Certain Glass Wine Bottles,” trade.gov Sustainability certifications, a prerequisite for 80% of bottled shipments, further solidify glass as a recyclable, inert container that aligns with importer ESG requirements.

Surge in Sustainable Eco-Friendly Packaging Adoption

EPR Law 20.920 obligates producers to finance collection networks targeting a 30% glass recycling rate by 2030, up from the present 1% baseline. Producer-responsibility organizations formed since 2023 have begun contracting material-recovery facilities and integrating informal recyclers, bolstering cullet availability for domestic furnaces. Ambipar Environment committed USD 23 million to recovery infrastructure capable of 90% throughput, creating predictable secondary-glass supply lines. Brand owners in the beverage and cosmetics segments are increasingly specifying minimum-recycled-content clauses that favor local suppliers offering certified cullet streams, thereby widening the moat for compliant incumbents.

Premiumization of Domestic Wine and Craft Spirits

Total vinification decreased in 2024 amid extreme weather, yet revenue rose as wineries redirected their efforts toward higher-margin bottled formats. Premiumization increases the average bottle weight, favors embossed or specialty finishes, and requires color differentiation, such as antique green, for reserve labels. New alcohol-labeling rules, effective July 2024, require health warnings and energy statements in set typefaces, prompting container redesigns with larger label panels that accommodate glass surfaces without structural compromise.[2]Foreign Agricultural Service, “Chile’s New Alcohol Labeling Law in Force on July 7,” fas.usda.gov The regulation indirectly increases the value of glass units and encourages limited-edition runs produced in specialty molds.

Rising Exports Requiring High-Quality Glass

The removal of U.S. antidumping risks in December 2024 eliminated provisional margins that threatened Chilean bottle pricing, stabilizing procurement for export wineries. Diversification into Asian markets imposes tougher packaging tests for pressure, impact, and finish-dimension tolerances; glass suppliers winning long-term contracts have invested in automated inspection lines and tighter SPC regimes. Enhanced border inspection protocols in China and Canada underscore the need for defect-free containers, reinforcing demand for premium domestic output over cheaper imports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from PET and metal containers | -1.4% | Beverage and food segments | Short term (≤ 2 years) |

| Volatile energy costs are elevating furnace Opex | -0.8% | All manufacturing centers | Medium term (2-4 years) |

| Skilled-labor shortage and wage inflation | -0.6% | Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Limited rural cullet collection | -0.4% | Rural districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Competition From PET and Metal Containers

Ball Corporation’s Santiago plant forms part of its South America division that shipped 19 billion aluminum cans in 2023, marketing infinite recyclability and lightweight logistics that appeal to beverage fillers.[3]Ball Corporation, “Form 10-K Fiscal Year Ended December 31, 2023,” sec.gov Coca-Cola’s venture into refillable PET bottles boosted recovery rates to 40%, eroding demand for single-use glass in carbonated soft-drink channels. Rising mandates for recycled content in plastic bottles impose cost penalties on PET producers, yet they also spur rapid innovation in lightweight, multilayer bottles that partially cannibalize glass market shares in the water and juice categories.

Volatile Energy Costs Elevating Furnace Opex

Furnace fuel comprises up to one-third of variable plant cost, and Chile’s spot-natural-gas price rose steeply in 2024. O-I Glass shuttered 7% of its global capacity under its Fit-to-Win program to cut USD 100 million in annual costs, signaling a broader shift toward asset rationalization. Domestic producers face similar pressures; line-shut incentives threaten smaller batch-colored runs, potentially limiting the availability of specialty amber and cobalt bottles unless efficiency upgrades, such as hybrid-electric furnaces, materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Remain Core, Cosmetics Fastest Rising

Beverages contributed 59.62% to Chile's container glass market size in 2025, anchored by export-driven wine bottling and by domestic beer volumes that rebounded alongside tourism. Within the beverage industry, premium wine represents the largest tonnage, as most exporters prefer 600-gram flint or green bottles with BVS finishes. Spirits command smaller volumes but higher unit values, and craft distillers increasingly specify amber or antique-green tints for ultraviolet protection. Chile container glass market share growth for beverages is expected to be modest, 4.99% CAGR, given substitution risks from PET in low-alcohol RTD lines.

Cosmetics and personal care posted the fastest trajectory at 7.16% CAGR, capturing demand for luxury skincare housed in heavy flint jars that convey purity and recyclability. Multinational brands such as L’Oréal now mandate post-consumer-recycled (PCR) content, prompting local glassmakers to secure color-sorted cullet streams. Domestic boutique cosmetics also adopt mini-format flacons, leveraging glass’s compatibility with organic formulations that are free of leachates. The high-margin profile of this vertical offsets furnace base-load gaps during the wine off-season, stabilizing capacity utilization.

Food jars account for a resilient mid-single-digit share, supported by fruit-preserve and condiment exports. Pharmaceutical, though smaller, benefits from syrup bottles that require Type III flint containers and are insulated from PET due to strict barrier requirements. Perfumery remains a niche market, but it influences design innovation that later migrates into mainstream beverage packaging.

By Color: Flint Dominates Yet Amber Accelerates

Flint glass retained 54.08% of the Chilean container glass market share in 2025, as wine bottlers value clarity for rosé and white varieties, and cosmetics brands favor transparent aesthetics. Flint’s versatility enables fast line changes and accommodates embossed branding without visible defects. However, amber glass leads growth at 7.86% CAGR as craft-spirit distillers and pharmaceutical syrup fillers switch to amber for UV shielding. Some premium beers also revert to amber after can-brightness issues with hop-sensitive recipes.

Green glass maintains a solid foothold in red-wine exports aimed at European importers, where the color connotes tradition. Specialty tints such as cobalt or emerald blue remain small but command price premiums and serve as brand-differentiation tools in limited-edition runs. Vineyard carbon audits increasingly influence color selection. Heavier, darker bottles hinder lightweighting efforts, so producers balance aesthetics, protection, and carbon intensity when finalizing procurement.

Geography Analysis

Central Valley viticulture, encompassing Maipo, Colchagua, and Casablanca, accounts for nearly two-thirds of Chile's container glass market demand, as these districts host the bulk of the country's export wineries. Proximity to Santiago’s bottle-making facilities minimizes freight cost and breakage risk on heavy flint shipments. The metropolitan region also concentrates food-processing and cosmetics filling lines, creating a dense demand cluster that sustains multi-color furnace campaigns year-round.

Northern macrozones, such as Atacama and Antofagasta, rely on imported containers for mining-camp food service and water packaging; however, rising desalination projects present localized opportunities for beverage production. Recycling coverage in these sparse regions lags often below 50% limiting cullet availability and prompting interest in mobile crushing units under EPR frameworks.

Southern territories, including Los Lagos, are witnessing a rise in bottle uptake from salmon canneries that are adopting glass for value-added smoked products targeting the East Asian gourmet segment. Port cities Valparaíso and San Antonio act as logistics nodes, funneling outbound wine bottles; capacity expansions in container terminals support smoother export flows. Regional disparities in cullet collection incentivize public-private partnerships to site beneficiation plants closer to high-volume bottle return centers, thereby reducing reverse logistics costs and CO₂ footprints.

Competitive Landscape

The Chilean container glass market exhibits moderate consolidation, with the top five suppliers controlling roughly 68% of the output capacity. Verallia Chile leverages global process know-how and European financing strength; its Latin America unit generated EUR 198.1 million (USD 213.9 million) in revenue for H1 2024, partially offset by favorable exchange rates. Domestic peer Cristalerías de Chile retains entrenched winery relationships, whereas O-I Glass focuses on rationalizing any underperforming lines.

Strategy gravitates toward higher recycled content and lightweighting. Verallia’s 2024 issuance of EUR 600 million (USD 648 million) eight-year bonds earmarks capex for hybrid-electric furnace pilots and cullet-processing assets. Smaller players pursue niche differentiation, such as engraved-shoulder bottles for craft mezcal, but face capital constraints when meeting EPR obligations. Bulk buyers increasingly sign multi-year cullet-content contracts, effectively tying up supply and raising barriers for late entrants.

The competitive threat from cans and PET suppliers intensifies. Ball touts closed-loop aluminum logistics and invests in digital printing to woo craft-beer brands, while Coca-Cola’s refillable PET success story pressures single-use glass in CSD channels. Nevertheless, the regulatory risk facing plastics including the escalating recycled-content thresholds under Chile’s single-use law works in glass’s favor, encouraging converters to promote reusable bottle programs aligned with circular economy pledges.

Chile Container Glass Industry Leaders

Verallia SA

Cristalerias de Chile S.A.

Titanio Sa

TricorBraun South America SAS

Cristalerías Toro S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Verallia reaffirmed full-year guidance, citing volume recovery in Chile after a weak Q1.

- December 2024: The U.S. Department of Commerce terminated the antidumping probe on Chilean wine bottles following the petitioner's withdrawal.

- October 2024: Verallia placed EUR 600 million (USD 648 million) bonds at 3.875% coupon to finance furnace upgrades.

- October 2024: O-I Glass extended its Fit-to-Win plan with additional 2025 capacity cuts targeted at high-cost sites.

Chile Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. The Chile glass containers market tracks the shipment volume of different types of glass containers across end-user industries in the market.

Chile Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the projected volume for the Chile Container Glass Market in 2031?

The market is forecast to reach 2.04 million tonnes by 2031, expanding at a 6.44% CAGR during 2026-2031.

How does EPR Law 20.920 influence glass packaging demand?

The law mandates producer-funded collection systems that target a 30% recycling rate, thereby boosting cullet supply and favoring glass over less recyclable substrates.

Which end-user segment shows the fastest growth in Chile?

Cosmetics and personal care are projected to lead with a 7.16% CAGR through 2031, as consumers trade up to premium packaging.

Why is amber glass gaining popularity in Chile?

Amber offers superior UV protection essential for craft spirits and pharmaceuticals, driving its 7.86% forecast CAGR.

What are the competitive threats facing Chilean bottle makers?

PET and aluminum containers from multinationals like Ball and Coca-Cola compete on weight and recyclability, pressuring single-use glass volumes.

How are Chilean producers coping with energy-cost volatility?

Leading firms invest in hybrid furnaces, lightweighting, and capacity rationalization programs to offset higher fuel expenses.

Page last updated on: