Peru Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

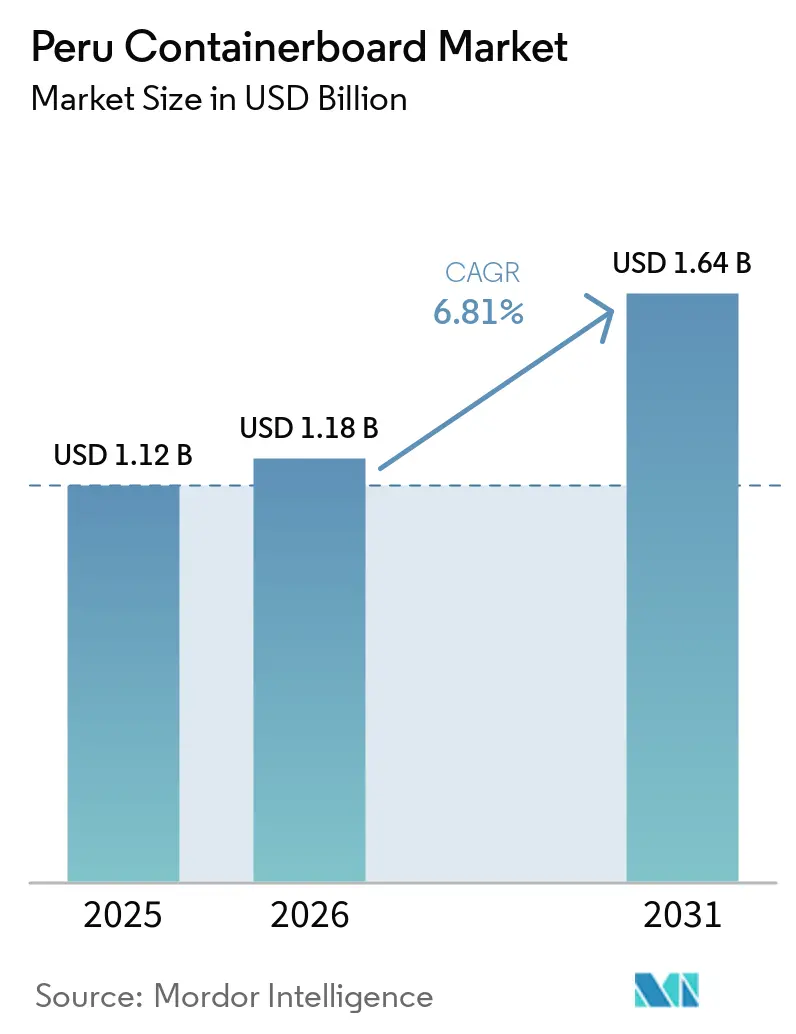

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

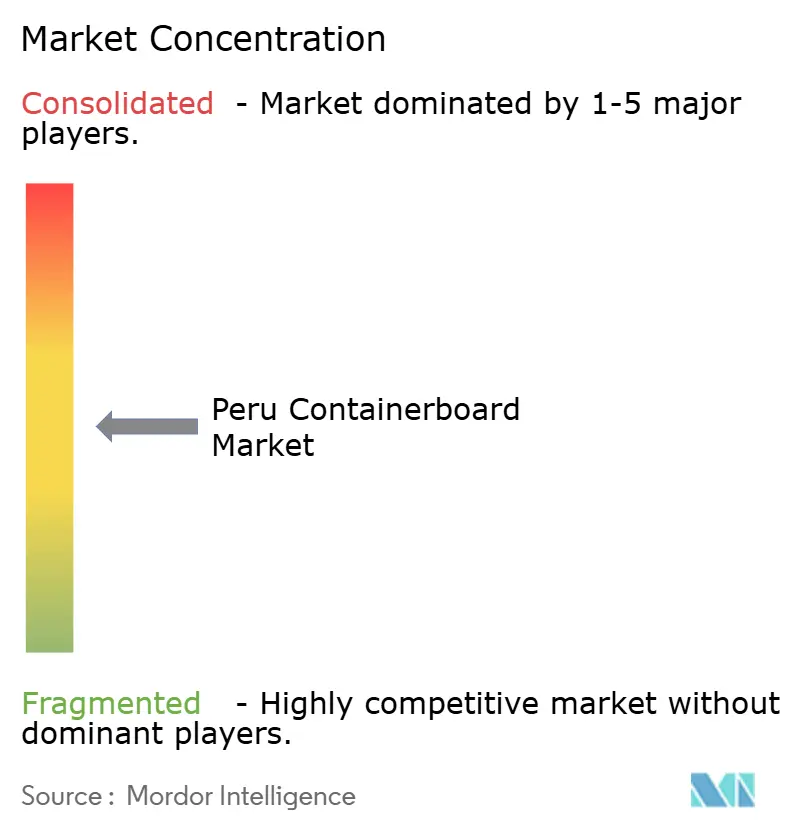

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Containerboard Market Analysis by Mordor Intelligence

The Peru containerboard market size is projected to expand from USD 1.12 billion in 2025 and USD 1.18 billion in 2026 to USD 1.64 billion by 2031, registering a CAGR of 6.81% between 2026 to 2031. The Peru containerboard market is supported by the country’s role as an exporter of blueberries, table grapes, and avocados, as these products rely on corrugated cartons that can withstand long sea routes and cold-chain handling. Agro-export revenues reached USD 15.013 billion in 2025, and that scale keeps carton demand tied to a structural export base rather than only to short-cycle industrial activity. The market is also benefiting from stronger food processing output and wider use of secondary packaging in modern retail, which adds a steadier domestic layer of demand beyond produce exports. Competitive conditions remain moderate rather than highly consolidated, with domestic scale, access to imported kraftliner, converting quality, and proximity to coastal export corridors shaping supplier advantage. Near-term pressure still comes from weather-linked crop swings, imported input costs, and inland delivery constraints, but the Peru containerboard market is positioned to keep expanding as export throughput and cold-chain capacity continue to improve through the forecast period.

Key Report Takeaways

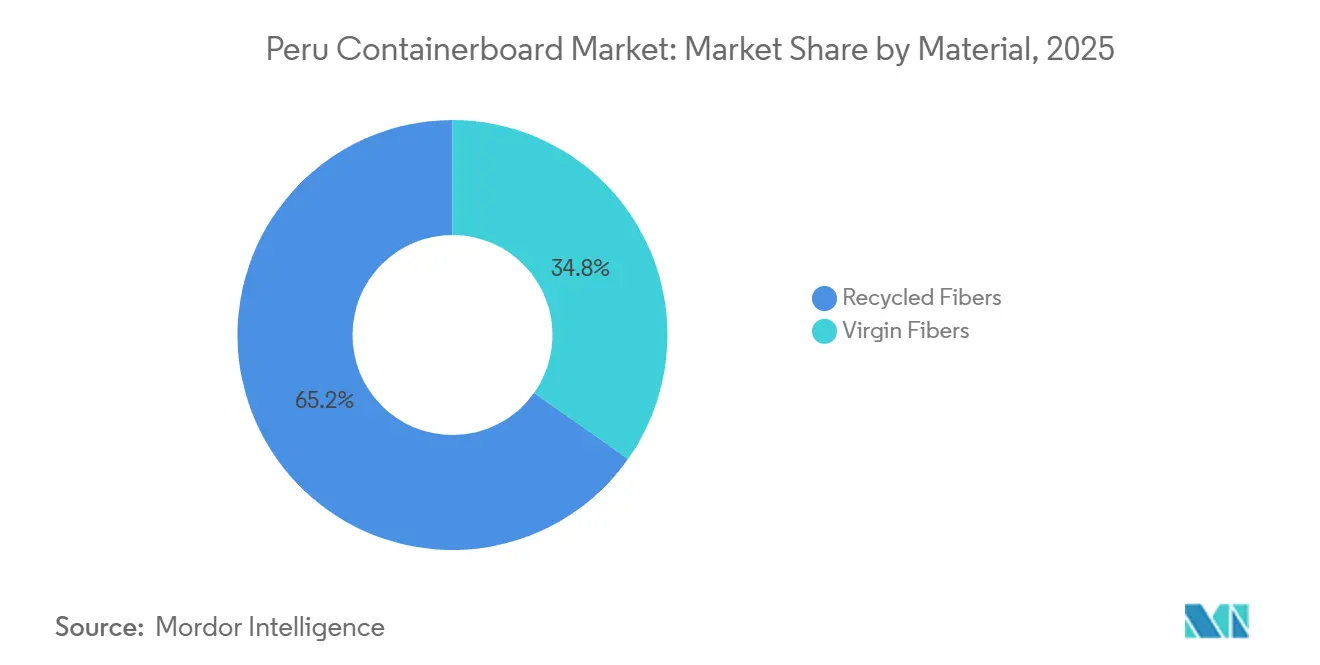

- By material, recycled fibers captured 65.21% of the Peru containerboard market share in 2025.

- By product type, the Peru containerboard market size for the kraftliners segment is forecast to advance at a 7.38% CAGR through 2031.

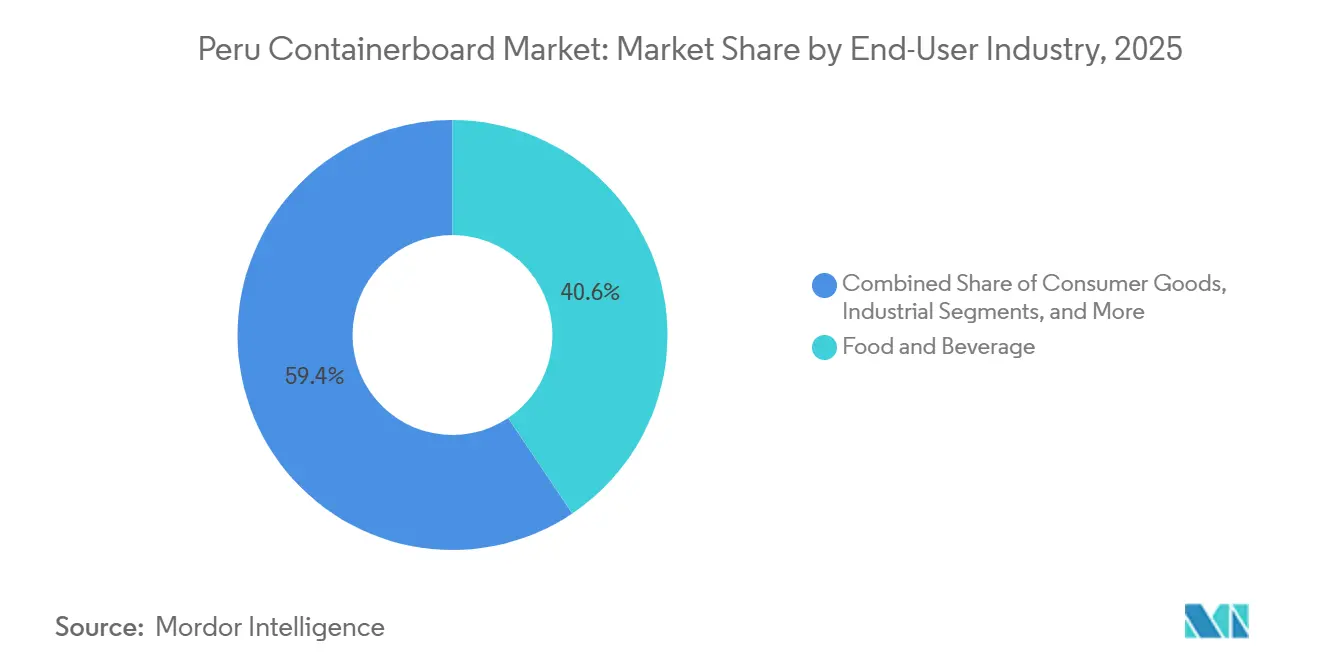

- By end-user industry, food and beverage captured 40.59% of the Peru containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Peru Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Agro-Export Expansion In Blueberries, Grapes, And Avocados | +2.3% | Coastal agro-export corridor, La Libertad, Lambayeque, and Ica, with spill-over to Lima converting hubs | Short term (≤ 2 years) |

| Cold-Chain Export Carton Upgrades For Long-Haul Routes | +1.1% | Northern Peru, Piura, Lambayeque, and La Libertad, and Callao port logistics zone | Medium term (2-4 years) |

| Food Processing And Modern Retail Packaging Demand | +0.8% | Lima metropolitan area, and secondary cities including Arequipa, Trujillo, and Piura | Medium term (2-4 years) |

| Rising Recycled-Fiber Adoption And Plastic-to-Paper Substitution | +0.7% | Global, with strongest near-term uptake in Lima and coastal cities | Short term (≤ 2 years) |

| E-Commerce And Home-Delivery Parcelization | +0.5% | Lima metro core, expanding to Arequipa and Trujillo | Medium term (2-4 years) |

| Food-Contact Recycled-Packaging Rulemaking | +0.2% | National, with early regulatory activity concentrated in Lima under MINSA and DIGESA oversight | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Agro-Export Expansion In Blueberries, Grapes, And Avocados

Agro-export volume remains the main demand anchor for the Peru containerboard market because fresh produce shipments require corrugated boxes at nearly every stage of harvest consolidation, cold storage, and export loading. Peru’s agro-export revenues reached USD 15.013 billion in 2025, up 17.3%, and fresh blueberries, grapes, and avocados together represented 44.2% of the non-traditional agricultural export value.[1]Ministry of Agrarian Development and Irrigation, “Peru: Agro-exports Up 17.3%, Totaled US$15.013 Billion in 2025,” Andina, andina.pe That commodity mix matters because these are not low-specification shipments; exporters need cartons with ventilation, moisture control, stack strength, and surface quality that meet retail and logistics requirements in Europe and North America. The export calendar is also spread across much of the year, so converters are not exposed to a single harvest window as they would be in a narrower produce economy. That steadier flow supports plant utilization, seasonal stock planning, and better recovery of conversion costs throughout the year. With agro-export revenues expected to exceed USD 16 billion in 2026, the Peru containerboard market will continue to draw support from a broad, high-value, packaging-intensive shipment base.

Cold-Chain Export Carton Upgrades For Long-Haul Routes

Cold-chain investment is changing the quality mix of demand in Peru's containerboard market, as exporters increasingly need cartons that retain strength after refrigerated handling and long ocean transit. In July 2025, Maersk launched a 17,500 m² integrated packing and cold storage hub in Olmos, Lambayeque, with processing capacity above 38 tonnes per hour, 7 rapid cooling tunnels, and 420 integrated refrigerated container slots. When cold-chain infrastructure is placed close to plantations, converters must supply boxes that tolerate longer dwell times and tighter handling standards rather than basic transit packaging. That shift raises demand for higher-performance liners, better fluting combinations, and heavier board grades for produce that spends multiple weeks in transit before reaching destination shelves. The upcoming impact of Chancay’s deep-water logistics buildout points in the same direction, as lower freight costs and stronger cold-chain links tend to favor greater export throughput rather than weaker packaging specifications. As a result, the Peru containerboard market is seeing quality-led growth alongside volume growth, and that improves the position of suppliers that can meet stricter carton standards.

Food Processing And Modern Retail Packaging Demand

Domestic packaging demand has become a more durable second layer of support for the Peru containerboard market, because food processing and modern retail both require corrugated solutions beyond direct export boxes. Peru’s food processing sector grew 6.3% in 2025 and accounted for roughly 24% of industrial GDP, underscoring the importance of packaged foods, beverages, dairy, snacks, and canned products to the industrial base.[2]USDA Foreign Agricultural Service, “Peru: Food Processing Ingredients Annual,” USDA FAS, fas.usda.gov This matters for board demand because processed goods move through secondary packaging, shelf-ready cases, and distribution units that are less exposed to farm-level seasonality than fresh produce. Retail chains have also pushed for more display-ready formats, better print quality, and boxes that can move from transport to shelf with limited repacking. That trend supports a wider use of die-cut formats and higher-value converting work rather than plain transport cartons alone. The Peru containerboard market, therefore, benefits from a broader demand base, where export agriculture still leads, but food processing and retail packaging now add more continuity across the year.

Rising Recycled-Fiber Adoption And Plastic-To-Paper Substitution

Recycled fiber remains central to the Peru containerboard market because domestic cost structures favor recovered feedstocks for standard grades, and Lima’s recovery networks are more established than any domestic virgin-fiber base. Recycled fibers led the material mix in 2025, and that position reflects both price discipline among buyers and the operating maturity of local paper collection and reprocessing channels. The push away from single-use plastics is also supporting paper-based packaging choices in parts of the supply chain where substitution is technically feasible, especially in secondary packaging and transport formats. At the same time, the shift is not uniform across all applications, because high-value fresh exports still require tighter performance and moisture resistance than lower-grade recycled inputs can consistently deliver. That is why recycled adoption is expanding alongside, not instead of, demand for premium virgin-based liners in export cartons. In practical terms, the Peru containerboard market is becoming more segmented, with recycled grades retaining their scale role while fiber-substitution policies and customer expectations keep paper solutions relevant in more packaging decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Kraftliner Dependence And Foreign Exchange Exposure | -1.0% | National, with greatest converter exposure concentrated in Callao and Lima industrial districts | Short term (≤ 2 years) |

| Weather Disruptions And Crop-Linked Demand Volatility | -0.7% | Northern and coastal agro-export corridors, La Libertad, Lambayeque, and Ica | Short term (≤ 2 years) |

| Andean Inland Logistics Raise Delivered Box Costs And Damage Risk | -0.4% | Andean highlands and inland Amazonian regions | Long term (≥ 4 years) |

| Skilled Flexo And Digital Press Labor Gaps | -0.3% | National, with the sharpest pressure in secondary cities outside Lima | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported Kraftliner Dependence And Foreign Exchange Exposure

Imported kraftliner remains a structural pressure point for the Peru containerboard market because the country does not have domestic virgin-fiber kraftliner mill capacity. That means converters depend on imported supply for applications where strength, print finish, and moisture resistance rule out lower-grade alternatives. This dependence becomes harder to manage when box prices are committed under seasonal export contracts, because converters cannot always pass through higher input costs when foreign exchange conditions turn against them. The risk is uneven across the market, and it weighs most heavily on mid-tier operators that do not have the same sourcing scale or customer leverage as the largest players. The Peru containerboard market therefore faces a margin constraint even when demand is healthy, because earnings can tighten faster than volumes improve. This issue also shapes competition, since firms with stronger procurement relationships and more flexible supply chains are better placed to protect profitability during imported cost swings.

Weather Disruptions And Crop-Linked Demand Volatility

The Peru containerboard market remains highly exposed to agricultural output, as much of its carton demand is tied to produce exports and harvest conditions. Containerboard consumption fell from 427,000 tonnes in 2022 to 303,000 tonnes in 2023, before recovering to 310,000 tonnes in 2024 and an estimated 319,000 tonnes in 2025, underscoring how quickly demand can shift when weather and political conditions disrupt export flows. In Q1 2026, Peru’s agro-exports rose 6.4%, but the pace was lower than the 16% growth recorded in Q1 2025, and the slowdown reflected declines in grape and mango shipments.[3]Association of Exporters, “Peru: Agro-exports Reach US$2.935 Billion, Up 6.4% in 1Q 2026,” Andina, andina.pe That matters because a few perishable commodity groups still account for a large share of carton offtake, so a weak season can quickly outweigh the steadier support coming from domestic food and consumer packaging. Even when long-term export prospects remain positive, converters still need to plan for short-cycle volume swings that are hard to smooth out with normal capacity decisions. For the Peru containerboard market, weather is therefore not just an agricultural issue; it is a direct operating variable for production planning, stock levels, and pricing discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Scale Meets Virgin-Fiber Quality Pull

Recycled fibers accounted for 65.21% of the Peru containerboard market in 2025, and that lead came from the clear cost advantage of recovered feedstocks in a market that still values price discipline in standard-grade box production. The segment’s position also reflects the maturity of Lima-centered recovery and reprocessing, providing domestic mills and converters with a more reliable stream of paper inputs than they have with virgin-fiber sourcing. In practical terms, recycled material remains the default choice for common testliner and fluting applications where buyers prioritize availability and competitive box pricing. This keeps a large part of the Peru containerboard industry tied to local recovery economics rather than to imported pulp or virgin kraft systems. It also helps explain why recycled grades remain dominant even while premium export applications move toward higher specifications.

The second side of this story is that virgin fiber production is growing faster, with the Peru containerboard market for virgin fibers projected to expand at a 7.24% CAGR through 2031. That growth is being driven by export-carton requirements, where burst strength, smoother print surfaces, and better moisture resistance matter more than the input-cost advantage of recycled content. European and North American retail supply chains also push exporters toward cartons that can support stronger certification and more consistent physical performance. This creates a split structure within the Peru containerboard market, where recycled grades keep the volume base while virgin-based liners gain weight in higher-value applications. Over time, converters that serve fresh produce exports will likely deepen their use of imported premium liners, even if the broader material mix remains led by recovered fiber. The result is not a replacement of recycled board, but a more defined separation between commodity-grade and export-grade packaging demand.

By Product Type: Testliner Volume Leadership And Kraftliner Upgrade Momentum

Testliners held 43.15% of the Peru containerboard market by value in 2025, which reflects their role as the standard lining material in cost-sensitive corrugated box production. Their strong position comes from the fit between recycled-fiber manufacturing and everyday domestic packaging needs, especially for food distribution, consumer staples, and general transport cases. Testliners remain central to the Peru containerboard market because they offer adequate strength for a wide range of standard applications without the imported cost burden attached to virgin kraftliner. Fluting follows a similar logic, as it supports the core corrugated structure used by medium- and large-scale converters supplying Lima and other commercial centers. Together, these grades form the operating base of the domestic box system and still account for much of the routine converting activity.

Kraftliners, however, are the fastest-growing product type, with the Peru containerboard market size for kraftliners expected to rise at a 7.38% CAGR through 2031. That growth is tied to the export-packaging upgrade cycle, in which fresh produce and long-haul refrigerated shipments require stronger, more stable liners than those used in standard domestic applications. The shift is also commercial, because high-value exporters are more willing to pay for fiber performance when packaging failure can put shipment quality, retailer compliance, or brand presentation at risk. This is why the Peru containerboard market is gradually moving toward a richer mix of performance-grade liners, even though exposure to imported kraftliner remains a cost challenge. As that mix changes, suppliers with stronger access to premium base papers and better converting consistency will likely gain share in export-linked accounts. Testliners will keep the broad volume lead, but kraftliners are set to capture more of the value added at the export margin.

By End-User Industry: Food And Beverage Leadership With Consumer Goods Building Faster

Food and beverage accounted for 40.59% of the Peru containerboard market in 2025, making it the largest end-user industry by a clear margin. This leadership reflects the combined effect of export cartons for fresh produce, secondary packaging for processed foods, and the wider use of corrugated formats in retail distribution. The category is broad enough to support different board grades, from transit cartons for agro-exports to higher-quality display-ready packs for packaged foods. That breadth gives the Peru containerboard market a strong base in an end-use market linked to both external trade and domestic consumption. It also means demand is not dependent on a single packaging format, because product handling, distribution, and shelf requirements differ across the segment.

Consumer goods are the fastest-growing end-user segment, with the Peru containerboard market size for this segment projected to advance at a 7.46% CAGR through 2031. The gain comes from online fulfillment, parcel shipping, expansion of personal care, and the move toward more rigid corrugated packaging in categories that previously relied more heavily on flexible formats. Food processing still supports the overall demand floor, as the sector grew 6.3% in 2025 and remains a large part of the industrial economy.[4]USDA Foreign Agricultural Service, “Peru: Food Processing Ingredients Annual,” USDA FAS, fas.usda.gov This interplay between packaged food demand and faster-growing consumer goods channels gives the Peru containerboard market a more balanced growth profile than one based only on produce exports. Industrial and other end users still contribute demand in mining, chemicals, and construction-linked packaging, but their growth profile is less structurally strong. For that reason, food and beverage will remain the volume anchor, while consumer goods will continue to gain relevance as format needs diversify across the broader Peru containerboard industry.

Geography Analysis

The Peru containerboard market is geographically centered on the coastal export corridor, with Lima serving as the main converting, recovery, and logistics hub for national demand. Lima’s dominance comes from its concentration of paper mills, corrugated converting capacity, commercial demand, and export staging activity through Callao. This makes the city both a domestic consumption center and the core redistribution point for produce consolidated from farming regions before shipment. The Peru containerboard market, therefore, does not follow a purely local consumption map, because board demand rises where industrial capacity and export logistics intersect rather than only where crops are grown. That structure favors scale players with access to Lima-based infrastructure and strong links to coastal freight channels.

Northern Peru has become more important as agro-export volumes and cold-chain investment have moved closer to production zones in Piura, Lambayeque, and La Libertad. Maersk’s launch of its integrated packing and cold storage hub in Olmos during July 2025 reinforced that shift by adding high-capacity export infrastructure near key fruit-growing areas. This matters because local access to packing and cooling activities creates stronger demand for cartons near harvest points rather than only in Lima. It also supports investment logic for converters that want to place more equipment in the north and serve seasonal peaks with shorter lead times. In the Peru containerboard market, northern geography is now a performance advantage as much as a freight advantage, since carton quality and timing both matter in export handling.

Southern Peru forms a secondary corridor, led by Ica and supported by export-oriented agriculture and longer shipping routes that favor stronger board grades. These southern flows often need heavier-gauge cartons because longer transit windows raise the penalty for packaging failure. Inland Andean and Amazonian regions still face a structural disadvantage because steep terrain, long delivery routes, and a higher risk of box damage push up delivery costs and limit wider corrugated adoption. The Peru containerboard market also sits within a wider South American supply chain where Peru imports key base papers, especially for premium grades, while local converters compete on the production of finished corrugated solutions. That keeps sourcing economics linked not only to domestic demand, but also to freight conditions and exchange-rate movements with regional suppliers. Over the forecast period, the strongest geographic gains will remain tied to coastal export corridors, while inland development is likely to lag because logistics friction is harder to solve than core demand availability.

Competitive Landscape

The Peru containerboard market is moderately concentrated at the top and more fragmented across the mid-tier, with Trupal S.A. holding the strongest domestic production position and Smurfit Westrock plc standing out as the main multinational converting presence. Trupal’s advantage comes from mill capacity, recovered-fiber access, and a plant footprint that extends from Lima to northern Peru, which gives it both scale and regional reach. Smurfit Westrock competes differently, using global procurement, design capability, and compliance-oriented carton offerings that suit exporters serving demanding overseas buyers. The wider field includes domestic converters such as EcoPacking Cartones S.A., Cartones Villa Marina S.A., and Packingtech Perú S.A.C., which tend to compete on regional access, price, and shorter response times during harvest peaks. This gives the Peru containerboard market a layered structure where scale matters, but specialized service and location still shape customer decisions.

Strategic moves in 2025 and 2026 show that competition is centered on capacity, quality, and logistics rather than on price alone. Trupal’s S/100 million investment plan, equivalent to USD 27 million, and its acquisition of a new corrugating machine for Piura strengthened its position in the northern agro-export corridor. The company also reported production records at its Sullana and Evitamiento plants and added a new printing and die-cutting press at Sullana to support cold-chain export cartons. Smurfit Westrock, meanwhile, reported 25% corrugated box volume growth in Peru in Q3 of fiscal 2025, which indicates that the company was gaining traction in accounts that value performance-grade packaging and supply reliability. These moves matter in the Peru containerboard market because they show where suppliers believe the next margin pool will sit, namely in export packaging quality, regional proximity, and converting consistency rather than only in commodity board output.

Regional producers are also trying to improve their position in Peru through wider South American logistics and export strategies. Empresas CMPC S.A. announced a BRL 1.5 billion (USD 280 million) port terminal investment in Rio Grande do Sul during January 2026, and that step can improve freight economics for kraft paper movement into markets such as Peru. Competitive white space remains in digital print, inline die-cutting, and more advanced display-ready formats, because many mid-tier converters still rely on outsourced finishing for higher-specification work. The Peru containerboard market is also likely to see a gradual shift toward more performance-based differentiation as moisture barriers, modified atmosphere packaging components, and tighter certification demands become more relevant in export cartons. That will favor companies with technical support and steady access to premium liners, while smaller firms remain more exposed to input volatility and seasonal demand swings. Even so, the presence of several mid-tier and regional players means the market is not tightly controlled by a small group, and customer choice remains meaningful across domestic and export-focused accounts.

Peru Containerboard Industry Leaders

Smurfit Westrock plc

Trupal S.A.

Cartones Villa Marina S.A.

EcoPacking Cartones S.A.

Packingtech Peru S.A.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: MINSA (Peru's Ministry of Health) published Resolución Ministerial N° 388-2026/MINSA, initiating a 90-day public consultation on a draft Supreme Decree to expand approved recycled raw materials in food-contact packaging beyond PET, signaling a forthcoming regulatory opening for recycled containerboard in direct food-contact applications under DIGESA oversight.

- April 2026: Smurfit Westrock announced a second containerboard price increase of USD 50 per ton effective June 1, 2026, following a USD 50 per ton increase implemented in April, signaling sustained cost pressure on Peruvian converters reliant on imported kraftliner from global producers.

- January 2026: Empresas CMPC S.A. announced a BRL 1.5 billion (USD 280 million) investment in a port terminal in Rio Grande do Sul, Brazil, as part of its "Projeto Natureza" program, a development that is expected to improve logistics economics for CMPC's kraft paper exports into South American markets including Peru.

- January 2026: Peru's Ministry of Agrarian Development announced the country exported over 3 million tonnes of agricultural products to 115 destinations in 2025, with avocados (767,230 tonnes), table grapes (555,524 tonnes), and blueberries (343,537 tonnes) comprising the top 3 export commodities by volume, driving record carton demand across major converting hubs.

Peru Containerboard Market Report Scope

The Peru Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Peru Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and future size of the Peru containerboard market?

The Peru containerboard market size stood at USD 1.12 billion in 2025, is valued at USD 1.18 billion in 2026, and is projected to reach USD 1.64 billion by 2031, at a CAGR of 6.81% over 2026-2031.

What is driving demand for containerboard in Peru?

The strongest demand driver is agro-export growth in blueberries, grapes, and avocados, supported by cold-chain expansion, stronger food processing output, and wider use of corrugated packaging in modern retail and consumer goods distribution.

Which material segment leads containerboard demand in Peru?

Recycled fibers led with 65.21% share in 2025, supported by cost competitiveness and established recovery networks, while virgin fibers are projected to grow faster at a 7.24% CAGR as export cartons shift toward higher specifications.

Which product type is growing the fastest in Peru?

Kraftliners are expected to post the fastest growth at a 7.38% CAGR through 2031, even though testliners remained the largest product type with 43.15% share in 2025.

Which end-user industry accounts for the largest share of demand?

Food and beverage led with 40.59% share in 2025, because it combines fresh produce export cartons, processed food packaging, and growing retail-ready corrugated formats.

What are the main risks facing suppliers in Peru?

The main risks are imported kraftliner dependence, foreign exchange exposure, weather-driven crop volatility, and higher inland transport costs, all of which can pressure margins even when export demand remains healthy.

Page last updated on: