Chemotherapy At Home Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 7.64% CAGR |

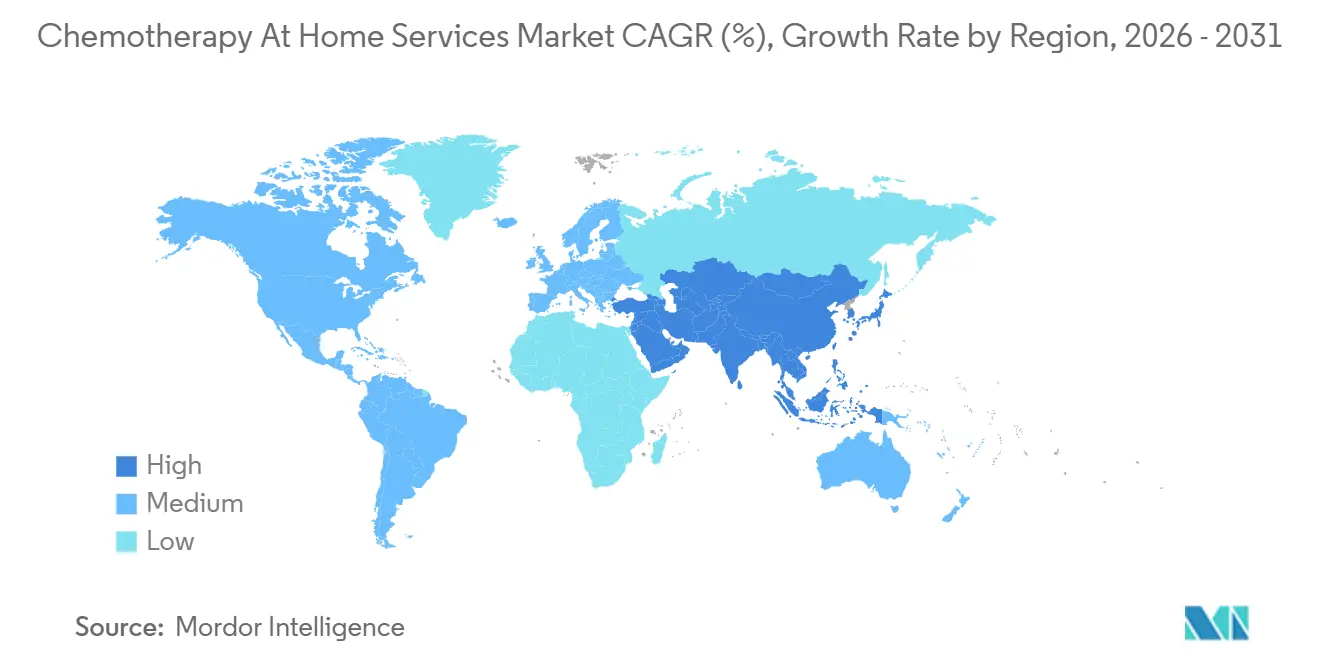

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

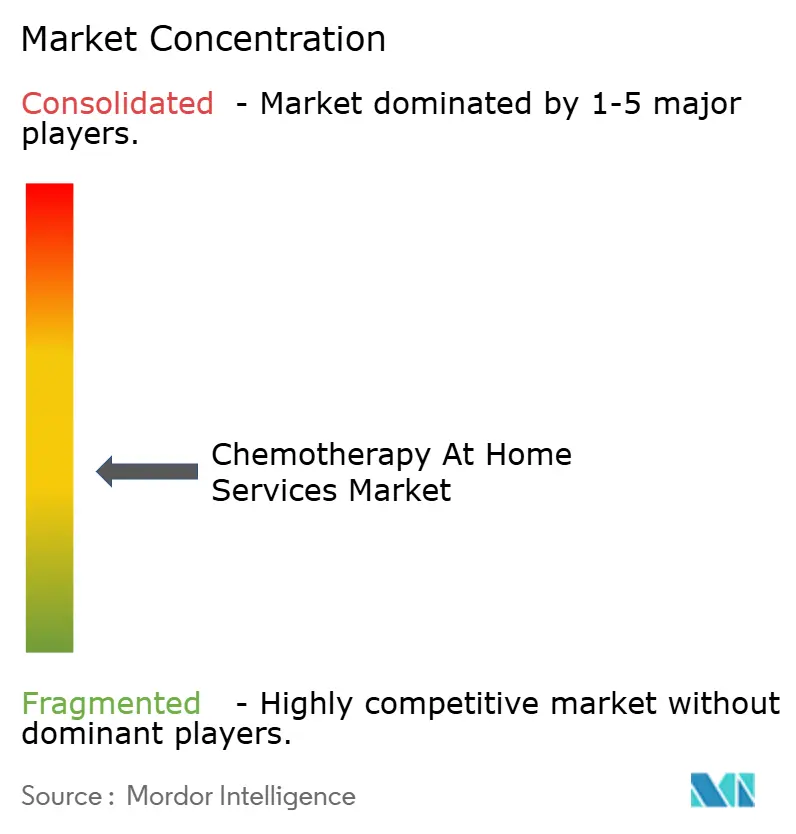

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemotherapy At Home Services Market Analysis by Mordor Intelligence

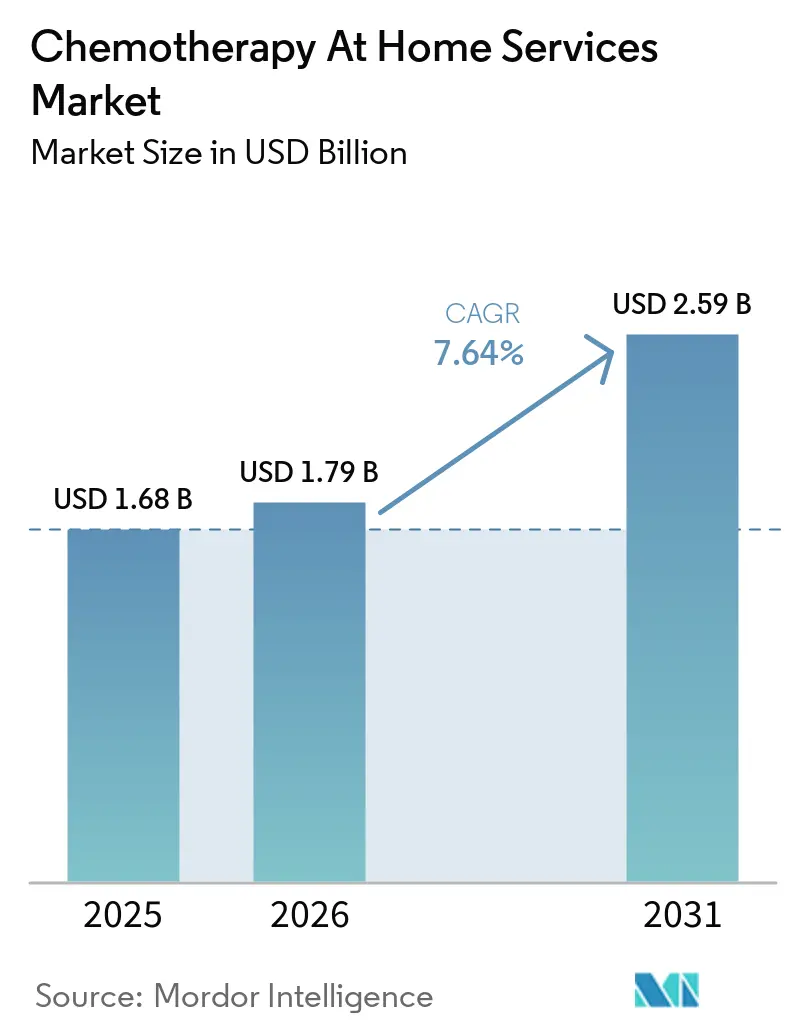

The Chemotherapy At Home Services Market size is expected to grow from USD 1.68 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.59 billion by 2031 at 7.64% CAGR over 2026-2031.

The chemotherapy at home services market is expanding because cancer incidence remains high, the number of patients living for years after diagnosis continues to rise, and many of these patients require repeated treatment cycles or maintenance therapy. The chemotherapy at home services market is also benefiting from stronger clinical comfort with home administration, as Mayo Clinic reported safe delivery of 93 intravenous chemotherapy infusions at home with no infusion reactions and no catheter-related infections. Payer economics are reinforcing this shift, because UnitedHealth Group found that moving cancer drug administration from hospital outpatient settings to home or physician office settings can reduce costs by 32%-39% and create annual savings of USD 12 billion if hospital infusion share declines from 60% to 30%. Better logistics, smart pump adoption, and more organized nurse dispatch networks are widening the range of regimens that can be handled outside hospitals, especially in mature markets with scale operators and stronger payer coverage. Growth still faces limits from reimbursement uncertainty, hazardous drug handling rules, and shortages of oncology-trained staff, which keep supply expansion below the level of underlying demand.

Key Report Takeaways

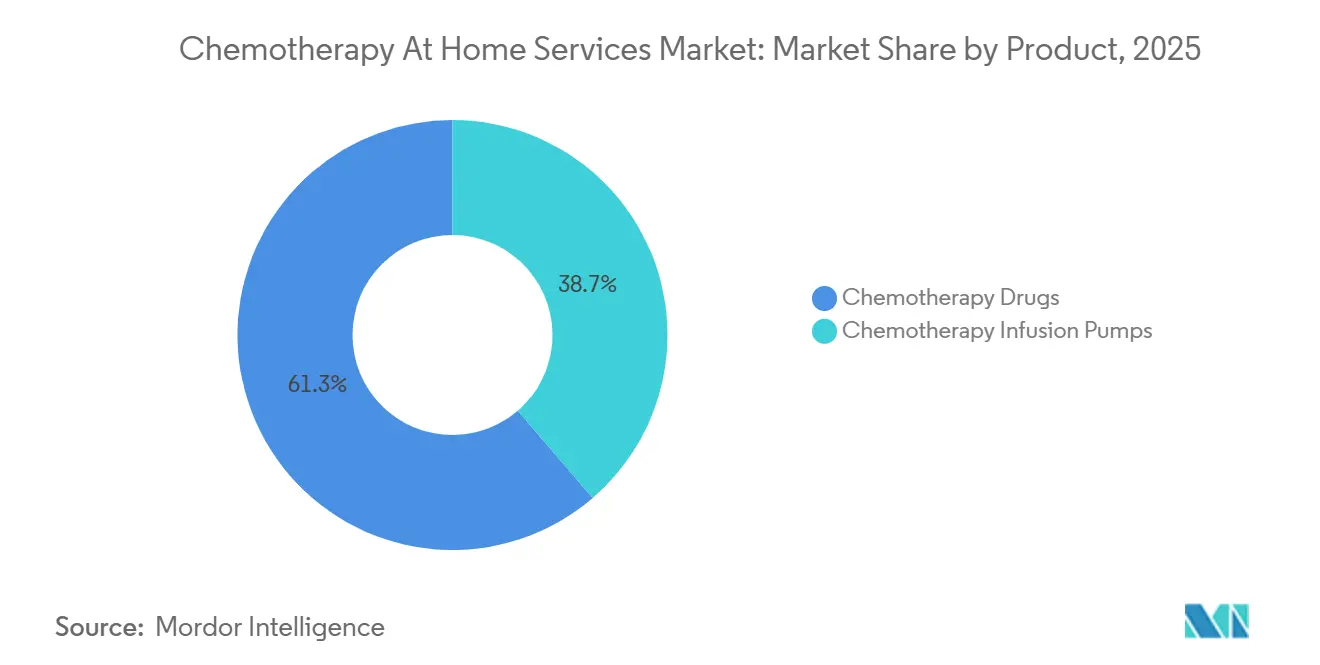

- By product, chemotherapy drugs led with 61.31% revenue share in 2025 in the chemotherapy at home services market, while chemotherapy infusion pumps are projected to expand at an 8.36% CAGR through 2031.

- By route of administration, intravenous held 82.68% of the chemotherapy at home services market share in 2025 and is advancing at a 9.74% CAGR through 2031.

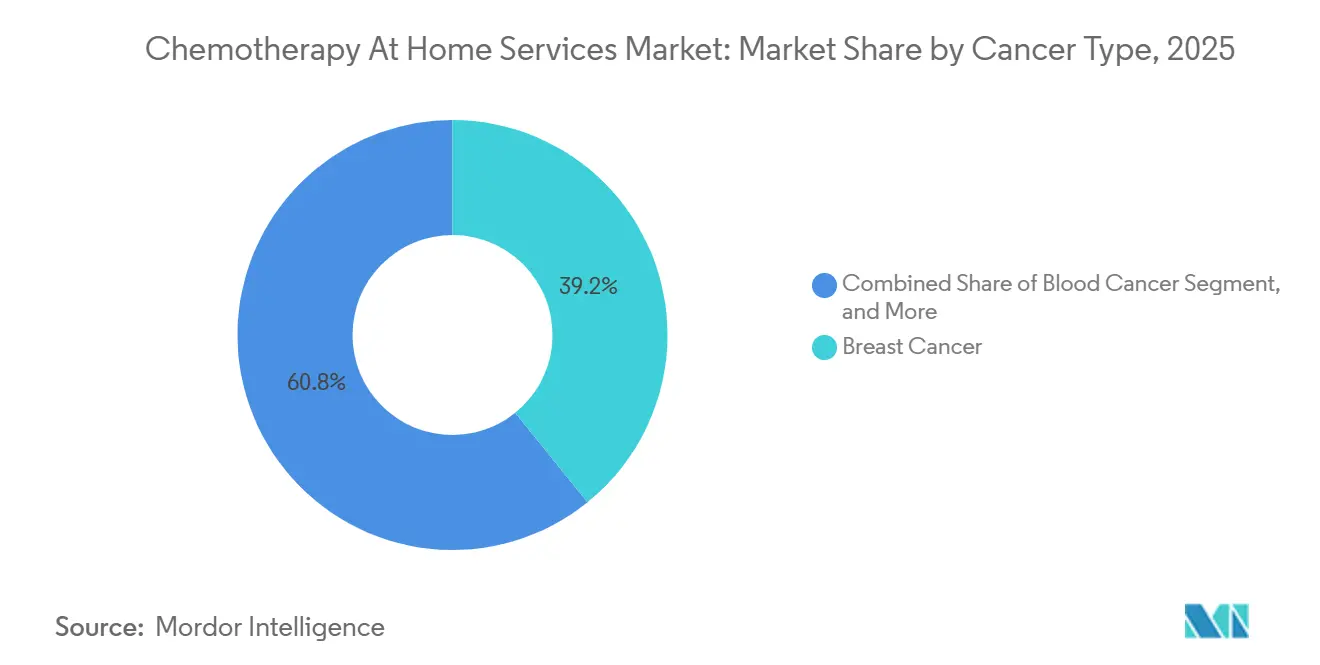

- By cancer type, breast cancer accounted for 39.16% share of the chemotherapy at home services market size in 2025, while blood cancer is forecast to grow at a 8.99% CAGR through 2031.

- By geography, North America captured 45.64% of global revenue in 2025 in the chemotherapy at home services market, while Asia-Pacific is projected to expand at a 9.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chemotherapy At Home Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cancer Incidence and Treatment Volumes | +1.8% | Global | Long term (≥ 4 years) |

| Preference Shift From Facility-Based Care to Home-Based Oncology Delivery | +1.5% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Remote Monitoring and Tele-Oncology Support Models | +0.9% | North America, Asia-Pacific, and Europe | Medium term (2-4 years) |

| Home Infusion Logistics and Nurse Dispatch Networks Improving Treatment Feasibility | +0.8% | North America and Europe, with early gains in Asia-Pacific urban centers | Medium term (2-4 years) |

| Portable Infusion Devices and Drug Stability Protocols Broadening Home Eligibility | +0.7% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Value-Based Care Incentives Supporting Site-of-Care Shift | +1.0% | North America, with spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cancer Incidence and Treatment Volumes

The chemotherapy at home services market is gaining a larger patient base because global cancer volumes remain high and are still increasing.[1]World Health Organization, “Global Cancer Burden Growing, Amidst Mounting Need for Services,” World Health Organization, who.int The World Health Organization reported 20 million new cancer cases and 9.7 million deaths in 2022, and it expects annual new cases to rise above 35 million by 2050. This rise matters for home-based care because hospital infusion capacity does not expand as quickly as case volumes in many health systems. The same pressure is being amplified by the large survivorship pool, with 53.5 million people alive within 5 years of a cancer diagnosis as of 2022. Many of these patients remain on adjuvant, maintenance, or repeat-cycle treatment plans that fit recurring home service models. That gives the chemotherapy at home services market a steady demand base that is not tied only to new diagnoses in a single year.

Preference Shift From Facility-Based Care to Home-Based Oncology Delivery

The chemotherapy at home services market is moving forward as providers, patients, and payers become more comfortable with treatment outside the hospital. Mayo Clinic’s Cancer CARE Beyond Walls program reported 93 home intravenous chemotherapy infusions with no infusion reactions and no catheter-related infections, which supports confidence in care quality and delivery safety.[2]R. Dronca et al., “Cancer CARE Beyond Walls, Safety, Feasibility, and Patient Experience of Home-Based Chemotherapy,” NEJM Catalyst, catalyst.nejm.org The economic case is also strong, as UnitedHealth Group estimated that shifting cancer drug administration from hospital outpatient settings to home or physician office settings can reduce costs by 32%-39% per commercially insured patient. The same analysis estimated USD 12 billion in annual savings if the hospital infusion share drops from 60% to 30%. Those savings are encouraging payers to favor lower-cost settings more actively than before. As a result, the chemotherapy at home services market is being shaped not only by patient convenience, but also by deliberate site-of-care redirection.

Expansion of Remote Monitoring and Tele-Oncology Support Models

The chemotherapy at home services market is becoming easier to scale because remote monitoring is improving how providers supervise patients between visits. Digital home-based monitoring models are being used to track side effects during breast cancer therapy and support clinical decisions without requiring constant in-person review. These tools help care teams decide when a patient can continue treatment at home and when escalation is needed. They also reduce unnecessary routine interactions because nurse visits can be triggered by symptom alerts instead of fixed schedules. This matters most for oral and lower-acuity regimens, where safety depends more on fast visibility into symptoms than on continuous physical presence. That shifts the chemotherapy at home services market toward more selective, data-supported home eligibility rather than simple geographic proximity to an infusion site.

Home Infusion Logistics and Nurse Dispatch Networks Improving Treatment Feasibility

The chemotherapy at home services market depends heavily on logistics, because safe delivery requires pharmacy coordination, cold-chain movement, nurse dispatch, and dependable scheduling. Option Care Health reported more than 5,000 clinicians, more than 190 locations, and service coverage for over 315,000 patients annually across all 50 U.S. states, which shows the scale needed to manage complex home infusion demand.[3]Option Care Health, “Annual Report 2025,” U.S. Securities and Exchange Commission, sec.gov Larger networks can absorb referral shifts more effectively because they already have staff, dispatch systems, and compounding links in place. They can also support broader payer relationships, which improves consistency in patient intake and authorization handling. Logistics depth becomes even more important when treatment requires multi-day ambulatory infusion or hazardous drug handling. For that reason, the chemotherapy at home services market is favoring operators with wide service footprints and more standardized operating models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology Nurse and Pharmacist Capacity Gaps | -0.5% | North America and Europe, acute in rural United States | Long term (≥ 4 years) |

| Reimbursement Variability and Payer Authorization Friction | -0.6% | North America, with spillover to Western Europe | Medium term (2-4 years) |

| Hazardous Drug Handling, Cold Chain, and Home Safety Compliance Burden | -0.3% | Global, with acute regulatory influence in the United States and Europe | Short term (≤ 2 years) |

| Limited Suitability of High-Risk Regimens for Home Administration | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oncology Nurse and Pharmacist Capacity Gaps

The chemotherapy at home services market faces a basic supply problem because oncology-trained nurses and pharmacists remain hard to recruit and retain. The Lancet Oncology Commission identified the global cancer workforce as a critical resource gap and linked care quality directly to staffing levels across countries and care settings. Home administration adds another layer of difficulty because general home health capabilities are not always enough for chemotherapy toxicity assessment and rapid response. Staff must distinguish treatment side effects from disease progression and make correct escalation decisions during visits or remote review. That raises training needs well above standard infusion support in lower-acuity services. Until that workforce base deepens, the chemotherapy at home services market will continue to expand more slowly than patient demand would otherwise allow.

Reimbursement Variability and Payer Authorization Friction

The chemotherapy at home services market also faces uneven financial support, which makes providers cautious about expanding programs too quickly. ASCO noted that the U.S. Acute Hospital Care at Home waiver, which supports hospital-at-home models under expanded Medicare rules, did not have permanent authorization in 2025. That uncertainty matters because investment in oncology-at-home capacity requires confidence that reimbursement pathways will remain stable over several years. A peer-reviewed Belgian study found that home hospitalization in oncology costs more than standard hospital-based care and that insurer reimbursement did not fully cover operating costs. When that gap appears, providers face margin pressure even if patient acceptance and clinical feasibility are both strong. This keeps the chemotherapy at home services market from moving at the same speed as the underlying clinical and cost case.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Drug Volume Dominates but Pump Economics Accelerate

Chemotherapy drugs held 61.31% of revenue in 2025 in the chemotherapy at home services market, which kept the revenue profile centered on drug spending rather than equipment or logistics fees. That position reflects how most patient episodes are still built around the therapy itself, with devices and home support layered around it. Multi-day intravenous regimens such as fluorouracil-based treatment for colorectal cancer reinforce this structure because the drug and the delivery setup are used together in a single care cycle. The pump segment is still the fastest-growing product category, with an 8.36% CAGR projected through 2031. That growth is coming from broader use cases rather than from a decline in drug importance. The chemotherapy at home services industry still depends on drugs as the primary billing driver, but devices are becoming more important for enabling a larger share of those therapies to move out of clinics.

Pump adoption is rising because product formats are widening, and providers can choose between lower-cost elastomeric systems and more connected smart platforms. Fresenius described its Ivenix smart infusion platform as a meaningful growth driver for 2026, and it highlighted advanced connectivity and a 97% drug library compliance rate in its investor communication. KORU Medical also moved to widen home eligibility when it submitted a 510(k) notification in January 2026 for the FreedomEDGE infusion system to administer pertuzumab, trastuzumab, and hyaluronidase subcutaneously at home for HER2-positive breast cancer. Medicare coverage support also improved, as the CMS LCD revision effective January 25, 2026 confirmed home coverage for ambulatory infusion pumps used with continuous antineoplastic drugs including fluorouracil, cytarabine, and vincristine. These changes are pushing the chemotherapy at home services market toward a larger installed pump base without changing the central role of chemotherapy drugs in total revenue.

By Route of Administration: IV Infrastructure Sustains Leadership While Oral Gains Strategic Relevance

Intravenous administration retained 82.68% of route revenue in 2025 and is projected to grow at a 9.74% CAGR through 2031 in the chemotherapy at home services market. This means the largest route is also the fastest-growing route, which reflects the scale of existing IV-dependent regimens and better home delivery support. Improved drug stability protocols and the spread of ambulatory pump platforms have made more IV treatment cycles practical outside hospitals. A 2024 patient satisfaction study in colorectal cancer found higher daytime and outdoor use satisfaction with soft-shelled elastomeric pumps, which supports continued preference for portable IV delivery formats in suitable regimens. These factors keep IV treatment central to the chemotherapy at home services market share even as care settings change. They also explain why route diversification is happening through home delivery models rather than through a rapid fall in IV use.

Oral chemotherapy still represented a smaller route base in 2025, but its strategic role is increasing because it removes the need for pump setup and routine nurse administration. Remote monitoring programs are becoming the main clinical oversight tool for these therapies, especially when treatment can be paired with side-effect tracking and direct patient reporting. The FDA approved Inqovi plus venetoclax in May 2026 as the first all-oral acute myeloid leukemia regimen for adults aged 75 years and older or for patients unable to tolerate intensive induction chemotherapy. BeOne Medicines also received FDA approval in June 2025 for a tablet formulation of BRUKINSA for all approved indications, which expanded portable oral treatment options in blood cancers. These approvals do not displace IV volume in the near term, but they widen the path for selected patients to receive full treatment courses at home with lighter infrastructure needs.

By Cancer Type: Breast Cancer's Volume Base Versus Blood Cancer's Momentum

Breast cancer accounted for 39.16% of revenue in 2025 in the chemotherapy at home services market, which made it the largest cancer type by service use. Its position reflects both high diagnosis volume and the broader set of regimens that can be managed safely in the home setting for selected patients. Global cancer statistics for 2022 continued to show breast cancer among the highest-incidence malignancies, which supports a large and recurring treatment base for home-compatible programs. Home eligibility in breast cancer is also widening because subcutaneous biologic formats are expanding beyond conventional clinic delivery. KORU Medical’s January 2026 filing for home subcutaneous delivery of Phesgo is a clear example of this shift toward easier home administration pathways.

Blood cancer is the fastest-growing indication, with a 8.99% CAGR projected through 2031 in the chemotherapy at home services market. Its growth pattern is different because it relies more on oral and subcutaneous innovation than on traditional ambulatory infusion workflows. AACR reported that, as of June 2025, the FDA had approved 4 BTK inhibitors for non-Hodgkin lymphoma and other hematologic malignancies, which points to a deeper treatment bench in blood cancers. The May 2026 approval of an all-oral AML regimen and the June 2025 approval of a BRUKINSA tablet support home treatment continuity for patients who would otherwise depend more heavily on facility visits. That keeps breast cancer as the largest base today, while blood cancer adds some of the strongest forward momentum in the chemotherapy at home services industry.

Geography Analysis

North America accounted for 45.64% of revenue in 2025 in the chemotherapy at home services market, and that lead rests on a combination of scale operators, payer support, and value-based oncology policy. Option Care Health reported more than 190 locations, more than 5,000 clinicians, and service across all 50 U.S. states, which illustrates the network depth available in the region. CMS also strengthened the operating backdrop through the Enhancing Oncology Model, which increased Monthly Enhanced Oncology Services payments and supported more patient-centered oncology workflows. The chemotherapy at home services market share in North America is also supported by stronger administrative ability to manage authorization, compounding, dispatch, and compliance at scale.

Europe remains the second-largest regional cluster in the chemotherapy at home services market, but growth is less uniform than in North America. Progress is strongest where hospital oncology teams, homecare providers, and public payment systems already work through linked operating pathways. At the same time, a peer-reviewed Belgian study showed that oncology treatment at home can cost more than standard hospital care when reimbursement is not designed to cover operating reality. That gap slows expansion because clinical feasibility alone does not guarantee provider investment or routine program scale.

Asia-Pacific is forecast to grow at a 9.59% CAGR through 2031 in the chemotherapy at home services market, making it the fastest-growing regional block. The region has a large untreated opportunity because cancer volumes are high and hospital capacity remains uneven across urban and non-urban settings. Growth is strongest where digital coordination, urban nurse availability, and payer openness are improving at the same time. South Korea and Australia already have established home infusion provider networks, while other countries are moving through earlier stages of structured oncology-at-home development. South America and the Middle East and Africa remain smaller in revenue terms, but the chemotherapy at home services market is gaining relevance there as health systems search for more flexible ways to deliver treatment outside major hospitals.

Competitive Landscape

The chemotherapy at home services market is moderately fragmented, with activity spread across independent infusion networks, integrated specialty pharmacy operators, and specialist home oncology providers. Option Care Health remained the largest independent position by scale, reporting USD 5.6 billion in net revenue for 2025 and a network of more than 190 locations. Optum Infusion Pharmacy and Fresenius Kabi also hold important positions, though their strengths differ across care delivery, payer linkage, and infusion product exposure. The top 3 independent infusion operators were estimated to hold 35%-40% of combined revenue, which leaves substantial space for regional and specialist competitors.

A major competitive reset came in October 2024 when CVS Health exited its acute home infusion business through Coram, closing or selling 29 regional pharmacies and redistributing referral flow across the U.S. home infusion field. Option Care Health used this period to extend its footprint, complete the integration of Intramed Plus, add more than 80 infusion suites, and improve claims processing efficiency with AI support that automated 40% of claims processing. Fresenius Kabi took a different route by joining the NHIA Future of Infusion Advisory Council in April 2026, which strengthened its role in policy and operating alignment with home infusion providers. Manufacturers are shaping the chemotherapy at home services market through pump placement, drug formulation access, and technology integration rather than by competing directly in service delivery. This gives large service operators an incentive to build closer ties with equipment and drug partners that can expand safe home eligibility.

The chemotherapy at home services market is also separating providers by compliance strength and staffing depth. USP Chapter <800> has increased the value of operators who can document hazardous drug handling protocols, engineering controls, and workforce training at a higher level. That creates a practical barrier for smaller providers that want to move into higher-acuity oncology cases without major operating investment. Regional specialists such as Sciensus in the United Kingdom, Portea Medical and Jivika Healthcare in India, and View Health in Australia are still gaining ground where payer coverage for home oncology is expanding and hospital-to-home referral models are becoming more routine. Competition therefore remains active, but scale, compliance, and clinical staffing are becoming the clearest markers of advantage.

Chemotherapy At Home Services Industry Leaders

Amgen Inc.

Baxter International Inc.

ICU Medical, Inc.

Medtronic

Optum, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The FDA approved Inqovi (decitabine/cedazuridine) plus venetoclax as the first all-oral acute myeloid leukemia regimen for adults aged 75+ or those unable to tolerate intensive therapy. The 28-day home-administered protocol requires no scheduled infusion clinic visits for drug delivery, converting a previously IV-dependent indication to a home-suitable format.

- April 2026: Fresenius Kabi joined the NHIA’s Future of Infusion Advisory Council, aligning its infusion pump and drug portfolio with U.S. home infusion policy strategy and advancing its position in the home-based oncology care delivery ecosystem.

- March 2026: KORU Medical Systems received EU Medical Devices Regulation certification for the Freedom60 infusion pump with prefilled syringe compatibility, enabling commercialization across EU markets and expanding the home subcutaneous infusion access point in European oncology care.

- December 2025: CMS implemented the NOPAIN Act through its final 2026 OPPS and ASC payment rule, providing separate Medicare reimbursement for qualifying ambulatory infusion pumps, including the CADD-Solis used by InfuSystem and Eitan Medical’s Sapphire, effective January 1, 2026, supporting the financial viability of home-based infusion therapy programs.

Global Chemotherapy At Home Services Market Report Scope

The Chemotherapy at Home Services Market is defined as the global industry providing cancer patients with access to chemotherapy treatments in home-based settings, rather than traditional hospital or clinic environments.

The Chemotherapy at Home Services Market is segmented by product, route of administration, cancer type, and geography. By product, it includes Chemotherapy Drugs and Chemotherapy Infusion Pumps. By route of administration, treatments are delivered through Oral and Intravenous methods. By cancer type, the market covers Breast Cancer, Blood Cancer, Ovarian Cancer, Colorectal Cancer, and Other Cancer Types.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of MEA), and South America (Brazil, Argentina, Rest of South America).

| Chemotherapy Drugs |

| Chemotherapy Infusion Pumps |

| Oral |

| Intravenous |

| Breast Cancer |

| Blood Cancer |

| Ovarian Cancer |

| Colorectal Cancer |

| Other Cancer Types |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Chemotherapy Drugs | |

| Chemotherapy Infusion Pumps | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| By Cancer Type | Breast Cancer | |

| Blood Cancer | ||

| Ovarian Cancer | ||

| Colorectal Cancer | ||

| Other Cancer Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for chemotherapy at home services?

The chemotherapy at home services market is forecast to reach USD 2.59 billion by 2031, up from USD 1.79 billion in 2026, at a 7.64% CAGR.

Which route is most important in home chemotherapy delivery?

Intravenous remains the leading route, with 82.68% share in 2025, and it is also the fastest-growing route at a 9.74% CAGR through 2031.

Why are payers pushing treatment into home settings?

Cost savings are the main reason. UnitedHealth Group found that shifting eligible cancer drug administration away from hospital outpatient settings can reduce costs by 32%-39%.

Which cancer type creates the largest demand base for home chemotherapy services?

Breast cancer leads with 39.16% of revenue in 2025 because diagnosis volume is high and more regimens are considered suitable for home use.

What is driving faster growth in blood cancer treatment at home?

Blood cancer is projected to grow at a 8.99% CAGR through 2031 because more oral and subcutaneous therapies are reducing dependence on clinic-based infusion.

Which region offers the strongest expansion opportunity through 2031?

Asia-Pacific has the fastest projected growth at a 9.59% CAGR, while North America remains the largest regional base with 45.64% share in 2025.

Page last updated on: