Hairy Cell Leukemia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

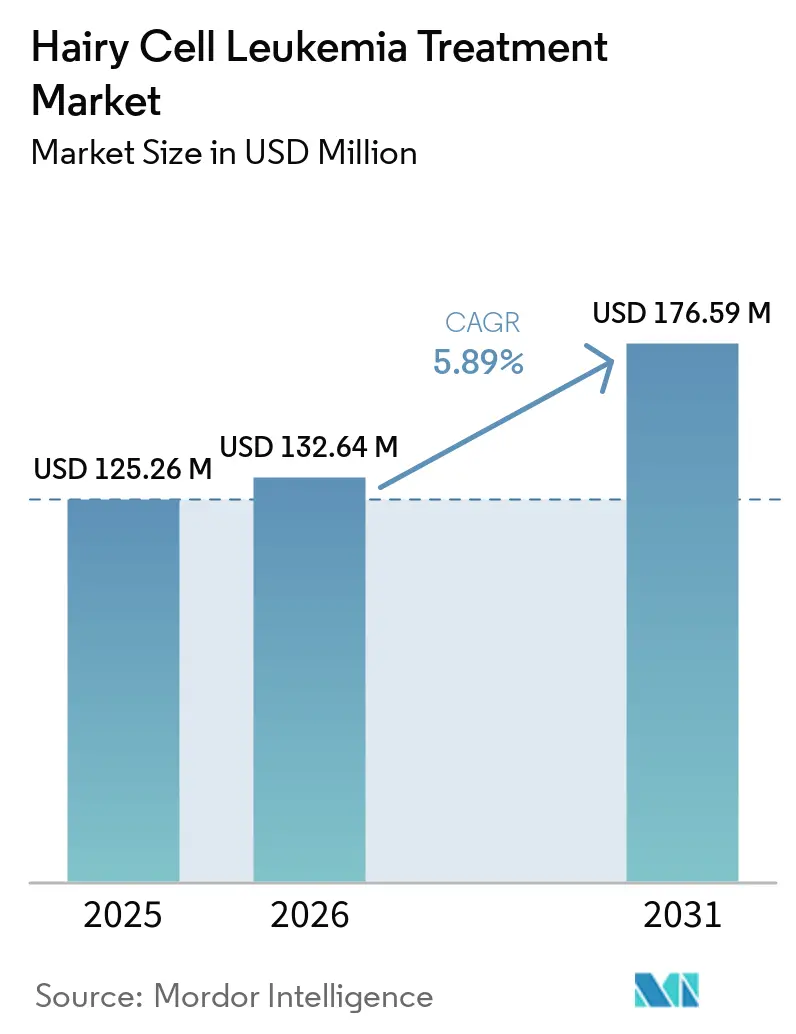

| Market Size (2026) | USD 132.64 Million |

| Market Size (2031) | USD 176.59 Million |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hairy Cell Leukemia Treatment Market Analysis by Mordor Intelligence

The Hairy Cell Leukemia Treatment Market size is expected to increase from USD 125.26 million in 2025 to USD 132.64 million in 2026 and reach USD 176.59 million by 2031, growing at a CAGR of 5.89% over 2026-2031.

The upward curve emerges from rapid uptake of precision therapies that directly target the BRAF V600E mutation, early diagnostic confirmation through flow cytometry and molecular panels, and the continued regulatory commitment to orphan‐drug innovation by the FDA and EMA. Improved life expectancy among treated patients intensifies the need for long-term monitoring solutions, while broader telemedicine coverage moves specialist knowledge beyond academic centers to underserved geographies. Competitive activity focuses on combination protocols that couple purine analogues with monoclonal antibodies or kinase inhibitors, aligning efficacy with tolerability. Meanwhile, oral and subcutaneous formulations challenge the dominance of infusion-center care, fostering home-based treatment pathways that lower systemic costs.

Key Report Takeaways

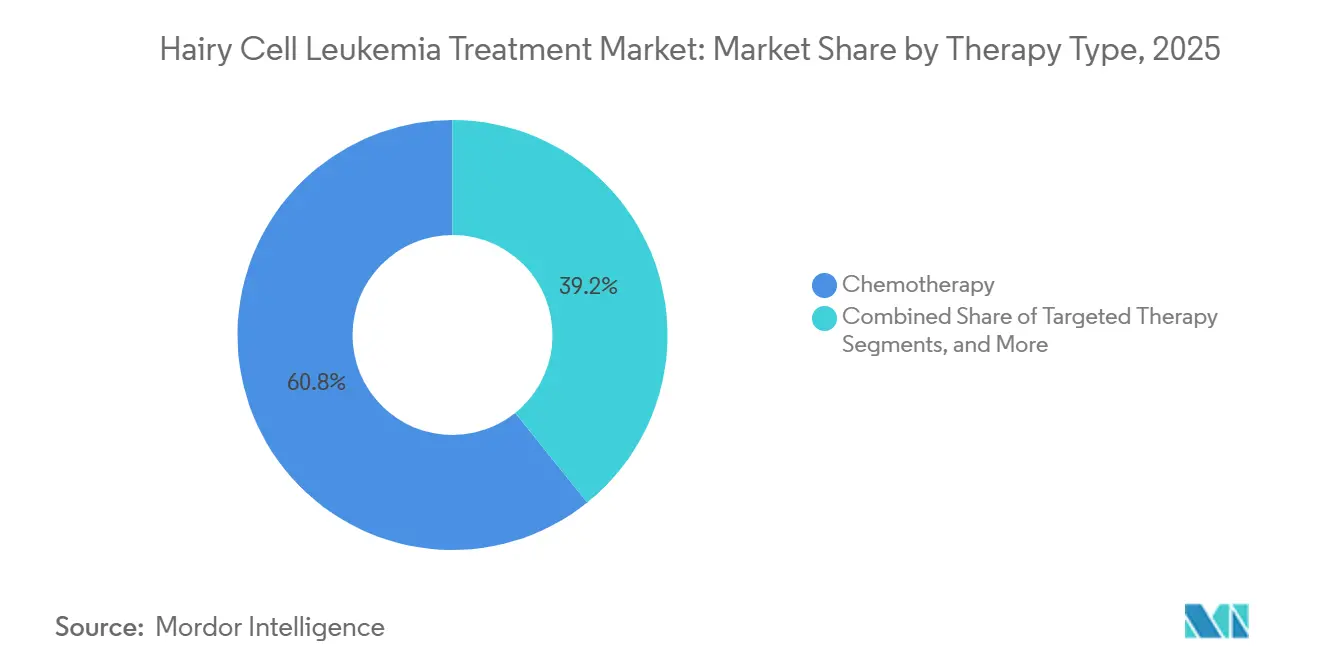

- By therapy type, chemotherapy commanded 60.78% of the hairy cell leukemia treatment market share in 2025, whereas targeted therapy is forecast to grow at an 8.21% CAGR to 2031.

- By patient type, classic hairy cell leukemia held 81.67% share of the hairy cell leukemia treatment market size in 2025; the variant subtype is poised to expand at a 7.52% CAGR through 2031.

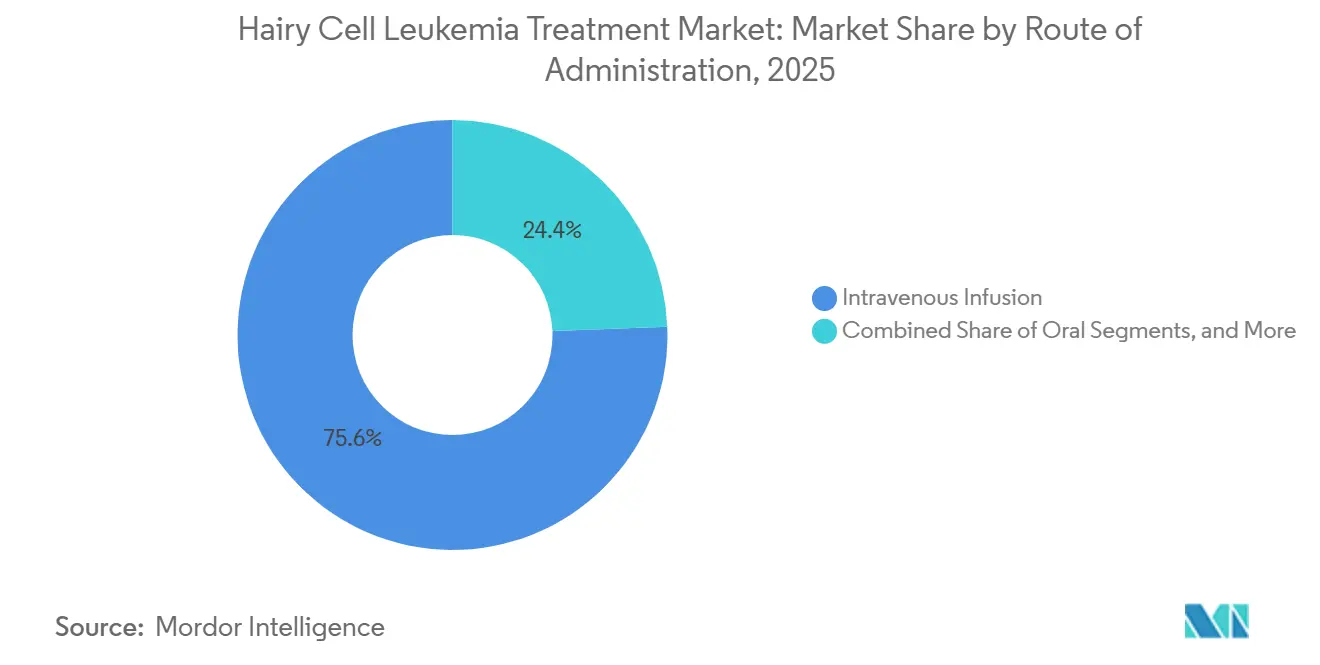

- By route of administration, intravenous delivery accounted for 75.62% of the hairy cell leukemia treatment market in 2025, while oral routes are projected to scale at a 9.05% CAGR to 2031.

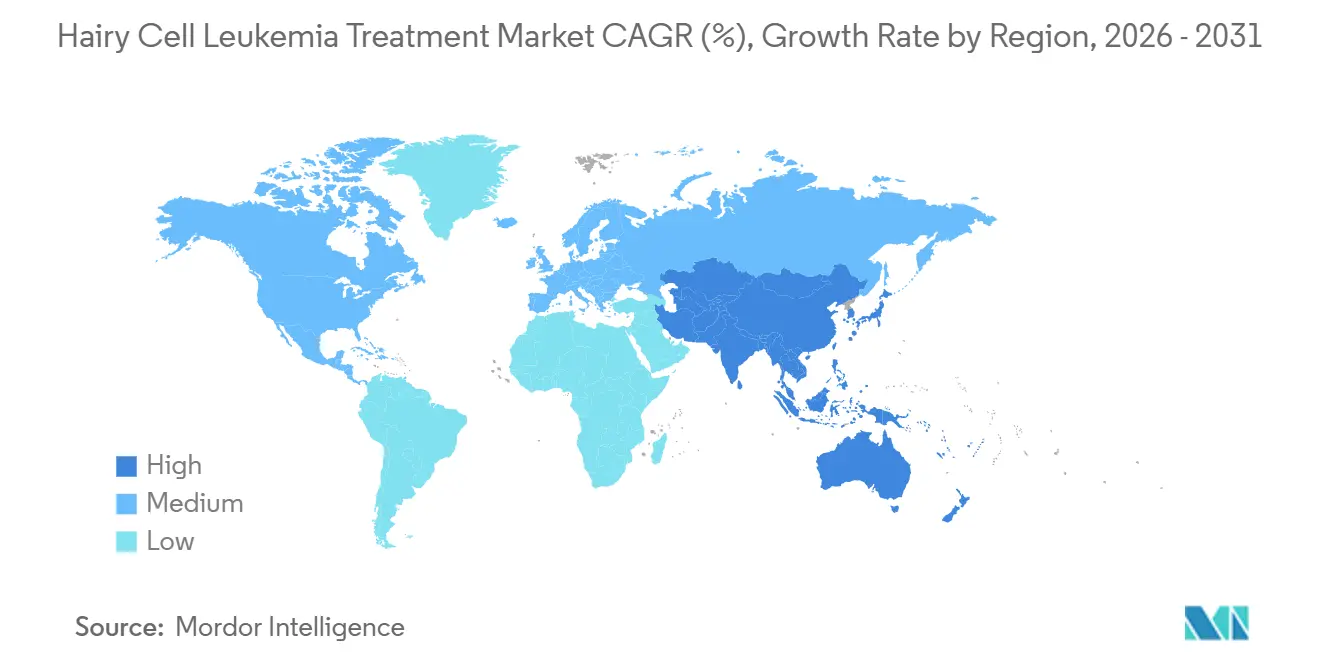

- By geography, North America led with a 41.95% revenue share in 2025; the Asia-Pacific region is expected to record the fastest growth, at an 8.55% CAGR, up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hairy Cell Leukemia Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing burden of leukemia cases & higher diagnosis rates | 1.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rising geriatric population | 0.80% | Global, particularly developed markets | Long term (≥ 4 years) |

| Rapid uptake of next-generation targeted therapies | 1.50% | North America & EU leading, APAC following | Short term (≤ 2 years) |

| MRD-guided retreatment algorithms | 0.70% | Advanced healthcare systems globally | Medium term (2-4 years) |

| Home-based sub-cutaneous cladribine protocols | 0.90% | Developed markets with robust home healthcare | Medium term (2-4 years) |

| Support of Regulatory Authorities | 1.10% | Global, with FDA & EMA leadership | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Leukemia Cases & Higher Diagnosis Rates

Flow cytometry and immunophenotyping now uncover cases that previously slipped under clinical radar, raising confirmed incidence counts and enabling prompt therapeutic intervention. AI-enabled pattern recognition archives a 97.5% concordance with manual reads while trimming processing time by 60.3%, increasing throughput and standardizing quality. Telemedicine links provincial laboratories with metropolitan reference centers, accelerating second opinions for atypical findings. Refinement of morphological scoring has also clarified epidemiology; the near-universal BRAF V600E hallmark provides a single-gene anchor that removes diagnostic ambiguity. These advances collectively swell treatment-eligible populations and shorten lead times to first treatment.

Rising Geriatric Population

Median presentation age remains between 50 and 55 years, yet prevalence rises sharply in octogenarian cohorts. Bone marrow biopsy audits in individuals aged 85 plus revised initial diagnoses in 44.1% and reshaped therapy plans in 25.4% without added complications.[1]U.S. Food and Drug Administration, “FDA Approves Acalabrutinib with Venetoclax for CLL,” fda.gov Older patients push demand for regimens that offer deep responses without myelosuppressive intensity, tilting prescribing toward BRAF or BTK inhibition. Subcutaneous dosing schedules reduce hospital stays, align with mobility constraints, and thus resonate with senior lifestyle preferences. Prolonged post-remission survival further necessitates structured surveillance and retreatment triggers.

Rapid Uptake of Next-Generation Targeted Therapies

Combination of vemurafenib and rituximab delivered 96% complete responses and 83% progression-free survival at 29.5 months median follow-up, outstripping purine analog comparators. Covalent-independent BTK blockers such as pirtobrutinib furnish durable activity even after C481-variant resistance emerges, widening salvage options.[2]American Cancer Society, “Cancer Facts & Figures 2026,” cancer.org MEK inhibition with trametinib brings clinically meaningful benefit to BRAF-negative or relapsed patients. Regulators expedite filing reviews under breakthrough designations, narrowing bench-to-bedside lags for pipeline entrants.

MRD-Guided Retreatment Algorithms

Next-generation sequencing detects residual disease down to 1 cell in one million, well below flow cytometry thresholds.[3] The Lancet Haematology, “CLL Burden in China 2020–2025,” thelancet.com Early signals of molecular relapse trigger pre-emptive therapy, permitting shorter upfront cycles and reducing cumulative toxicity without compromising remission durability. Payors also appreciate decreased drug wastage when therapy stops at MRD clearance.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited awareness & specialist access in rural areas | -0.90% | Global, particularly emerging markets | Long term (≥ 4 years) |

| High cost of novel targeted agents | -1.10% | Price-sensitive markets globally | Medium term (2-4 years) |

| Orphan-drug exclusivity expiries post-2028 | -0.70% | Developed markets with generic competition | Long term (≥ 4 years) |

| Severe immunosuppression & infection risk with purine analogues | -0.60% | Global, affecting treatment selection | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Awareness & Specialist Access in Rural Areas

Resource limitations confine immunophenotyping and molecular labs to tertiary centers. Case series from low-income regions reveal splenectomy still substituted for cladribine because supply chains do not consistently stock purine analogues. Hematologist shortages persist, with 113 radiation oncologists serving 110 million citizens in the Philippines, a ratio that illustrates systemic gaps. Tele-oncology mitigates but does not yet erase these disparities, as patchy internet coverage curtails video consultation reliability in remote districts.

High Cost of Novel Targeted Agents

Economic reviews show annual treatment spending escalating from USD 29,080 for legacy regimens to USD 371,393 for advanced cellular interventions in allied hematologic settings. Out-of-pocket spending exceeds 75% of total care costs in many middle-income economies, throttling uptake rates. Reimbursement decision lags average 4 years after approval in some countries, prolonging inequity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Precision Expansion Shapes the Landscape

Targeted modalities are registering the swiftest momentum, as the segment is expected to grow at an 8.21% CAGR through 2031. Near-universal BRAF V600E positivity provides a clear biomarker, and the vemurafenib–rituximab pair achieves a 96% complete response, solidifying the proof of concept. BTK inhibition furnishes an alternative axis for relapsed or mutation-resistant subsets, and early-line integration trials are underway. Immunotoxin therapy, such as CD22-directed moxetumomab pasudotox, remains reserved for multiply relapsed disease because of capillary leak risk and price considerations.

Chemotherapy maintains a significant presence, accounting for 60.78% of the hairy cell leukemia treatment market share in 2025. Cladribine and pentostatin remain frontline standards, thanks to 80% or higher complete remission rates and decades of clinician familiarity. Rituximab co-administration enhances the depth of response while reducing relapse frequency, thereby maintaining the relevance of chemotherapy. Emerging subcutaneous formulations support outpatient or home deployment, helping to fend off share erosion.

By Patient Type: Diagnostic Refinement Accelerates Variant Recognition

Classic disease predominated in 2025, accounting for 81.67% of the overall volume, due to its well-characterized symptom triad of splenomegaly, cytopenia, and marrow fibrosis. Standard purine analogue care protocols ensure high and durable response, preserving segment heft.

Variant disease, however, is the fastest climber at 7.52% CAGR. Immunophenotypic nuance and advanced sequencing now differentiate variant disease from splenic diffuse red pulp lymphoma and other mimickers. Resistance to purine analogues in this cohort prompts prescribers to consider combinations involving rituximab or targeted kinase blockade. Ongoing BAFF-pathway research promises further tailored therapeutics.

By Route of Administration: Convenience Drives Oral Uptake

Oral regimens progress at a 9.05% CAGR as adherence initiatives push completion rates to 85% under pharmacist stewardship. Tablet or capsule delivery alleviates travel and chair-time burdens, fits telehealth follow-up models, and aligns with patient lifestyle expectations.

Intravenous infusion still maintains 75.62% of 2025 revenue because infusion-center oversight remains essential for combination cycles and for high-acuity cases. Subcutaneous formulations bridge both worlds by trimming infusion times and enabling at-home nursing support. Large-volume wearable injectors now trial 5-15 ml dose delivery without loss of efficacy.

Geography Analysis

North America steered 41.95% of 2025 global sales, anchored by dense networks of specialty hematology centers that facilitate rapid adoption of innovative regimens and real-time MRD surveillance. FDA decisions continue to influence worldwide standard-setting, with breakthrough labels cutting development timelines from years to months. Tele-oncology services have grown rapidly; the Mayo Clinic reports oncology virtual-care completion rates above 90%, broadening specialist reach.

Asia-Pacific is set to grow at an 8.55% CAGR owing to expanding tertiary care capacity and policy frameworks that encourage clinical trial hosting. Chinese leukemia incidence stabilizes, yet survival metrics improve as technology diffusion continues. India’s updated trial guidelines now align with ICH-GCP, accelerating start-up timelines and enhancing safety governance. This ecosystem invites multinational sponsors to enroll previously unserved patients, bolstering early access.

Europe benefits from the EMA’s centralized approval mechanism, permitting simultaneous market entry across member states once reimbursement dossiers clear national HTA bodies. Pan-regional cooperative research groups sustain high enrollment for investigator-initiated trials, particularly those comparing novel kinase inhibitors against purine analog benchmarks.

Latin America, the Middle East, and Africa record gradual uptake, yet supply chain gaps and reimbursement constraints hinder pace. Splenectomy persists in certain low-resource pockets, reflecting therapy access shortfalls. International partnerships that supply subsidized drug, diagnostic kits, and telepathology teaching promise to narrow disparity margins over the coming decade.

Competitive Landscape

Competition remains moderate, shaped by the rare-disease status that dissuades head-to-head promotion wars. The pipeline favors targeted pathway stacking—BRAF plus BTK or MEK—to deepen remission or overcome resistance. Biotechnology innovators with a single-asset focus secure orphan-drug incentives, then co-license commercialization to larger groups once phase II proof emerges. Academic alliances dominate trial design, ensuring access to the relatively small global patient pool.

Digital capabilities evolve into strategic differentiators. AI-driven diagnostic support tools speed oncologist decision-making, while remote monitoring dashboards feed real-time adherence and toxicity data back to clinics. Recent patent documentation highlights long-acting subcutaneous depots intended to consolidate multi-day infusion schedules into once-monthly at-home shots, trimming hospital resource strain.

White-space opportunities include extended-wear on-body injector technology, combination regimens that suppress multiple escape pathways, and tailored MRD assay services. Firms that integrate therapeutic and diagnostic platforms stand to command bundle pricing and deepen customer lock-in.

Hairy Cell Leukemia Treatment Industry Leaders

Pfizer Inc.

Gilead Sciences Inc.

AstraZeneca plc

F. Hoffmann-La Roche Ltd

Amgen Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Blood Cancer United, formerly recognized as The Leukemia & Lymphoma Society, announced new scientific grants and investments to drive progress toward cures and improve the quality of life for individuals with blood cancer, including hairy cell leukemia, and their families.

- June 2025: The Leukemia Research Foundation has revealed the recipients of its 2025-2027 New Investigator Research Grant Program. A total of 13 early-career researchers from across the nation will each receive a grant of USD 150K, allocated over a two-year period.

Global Hairy Cell Leukemia Treatment Market Report Scope

According to Mordor Intelligence, the Hairy Cell Leukemia (HCL) market refers to worldwide prescription revenues from drugs that treat classic or variant HCL, including purine-analog chemotherapy (cladribine, pentostatin), BRAF and BTK targeted agents, monoclonal antibodies, and recombinant immunotoxins, captured at ex-manufacturer prices and allocated to the year in which patients receive therapy. We count every labeled line of therapy but stop where use is purely off-label for other malignancies.

Scope Exclusions: Supportive care products, diagnostic assays, bone-marrow procedures, and hospital service fees sit outside this market.

| Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) |

| Antimalarials |

| Corticosteroids |

| Immunosuppressants / DMARDs |

| Biologics |

| Stem-cell & Gene-based Therapies |

| Oral |

| Intravenous |

| Subcutaneous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) | |

| Antimalarials | ||

| Corticosteroids | ||

| Immunosuppressants / DMARDs | ||

| Biologics | ||

| Stem-cell & Gene-based Therapies | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Subcutaneous | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current market size?

The market is valued at USD 132.64 million in 2026 and projected to reach USD 176.59 million by 2031, growing at a 5.89% CAGR.

Which therapy type dominates the market?

Chemotherapy held 60.78% share in 2025, while targeted therapy is the fastest-growing segment with an 8.21% CAGR.

Which patient type is most common?

Classic HCL accounted for 81.67% of cases in 2025, but variant HCL is expanding at a 7.52% CAGR due to improved diagnostics.

What is the fastest-growing route of administration?

Oral therapies are projected to grow at a 9.05% CAGR, driven by convenience and telehealth integration.

Which region leads the market?

North America led with 41.95% share in 2025, while Asia-Pacific is the fastest-growing region at 8.55% CAGR.

What are the main growth drivers?

Growth is fueled by precision therapies targeting BRAF V600E, early diagnostics, and regulatory support from FDA & EMA.

Page last updated on: