Oncology Nutrition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 3.96 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oncology Nutrition Market Analysis by Mordor Intelligence

The Oncology nutrition market size is projected to expand from USD 2.77 billion in 2025 and USD 2.94 billion in 2026 to USD 3.96 billion by 2031, registering a CAGR of 6.12% between 2026 to 2031. Growing recognition that malnutrition compromises treatment tolerance and survival is pushing nutrition assessment into first-line oncology protocols, especially for cachexia-prone cancers. Rapid innovation in elemental and immunonutrition formulas, broadened Medicare coverage for home enteral feeding, and Asia-Pacific’s surging cancer incidence are shaping capital allocation, product design, and distribution pathways. At the same time, head-and-neck cancer remains the principal demand driver because dysphagia and xerostomia sustain long feeding periods, while immunotherapy-led lung-cancer regimens heighten metabolic needs. Competitive intensity is moderate: four global manufacturers dominate but agile entrants are capturing share with plant-based and organic alternatives that answer taste-aversion complaints.

Key Report Takeaways

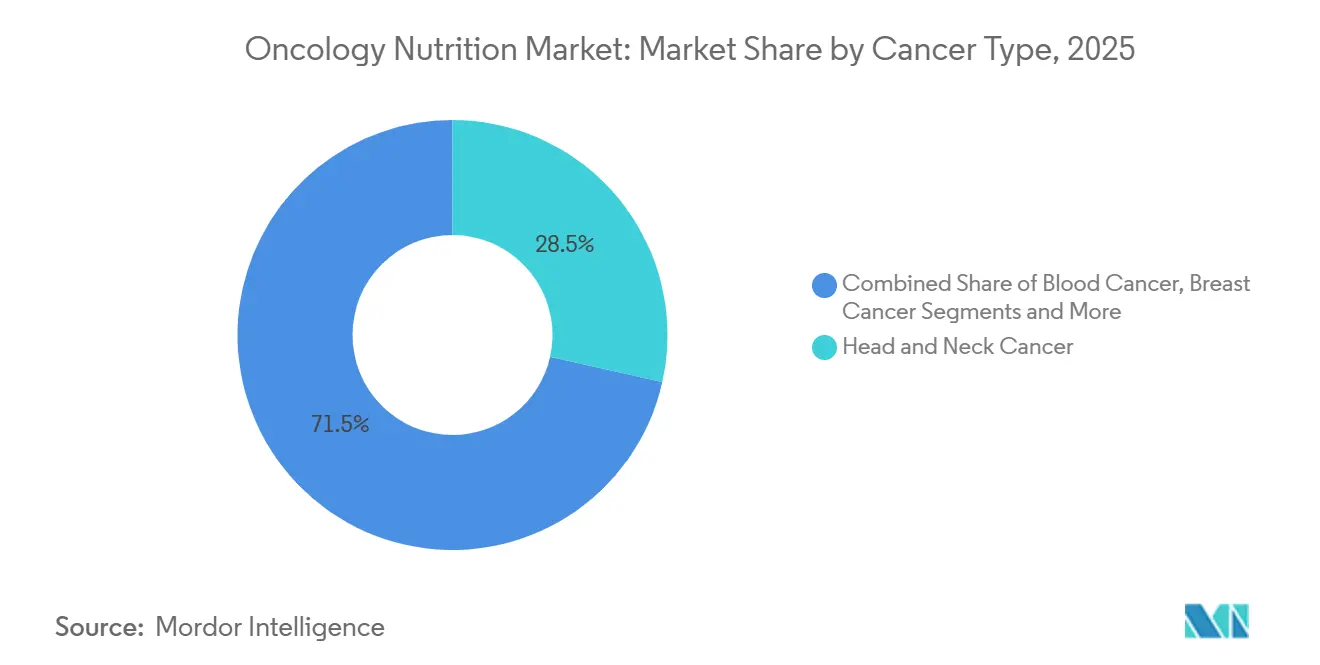

- By cancer type, head and neck cancer led with 28.54% of Oncology nutrition market share in 2025, while lung cancer is advancing at a 7.25% CAGR through 2031.

- By nutrition type, enteral formulas commanded 75.54% share of the Oncology nutrition market size in 2025; parenteral nutrition is forecast to post a 6.65% CAGR to 2031.

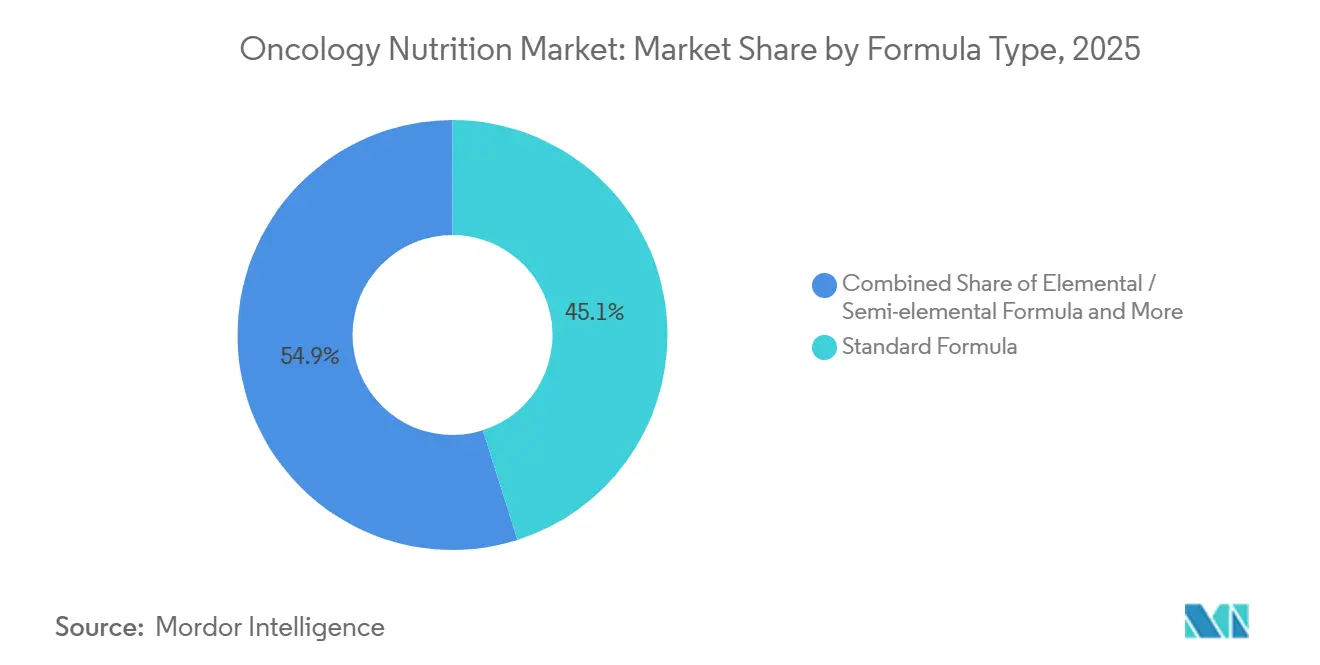

- By formula type, standard products captured 45.15% revenue in 2025, whereas disease-specific and immunonutrition lines are projected to grow at 7.82% CAGR over 2026-2031.

- By end user, hospitals held 58.23% share in 2025 but home care settings are pacing the field with an 8.42% CAGR to 2031.

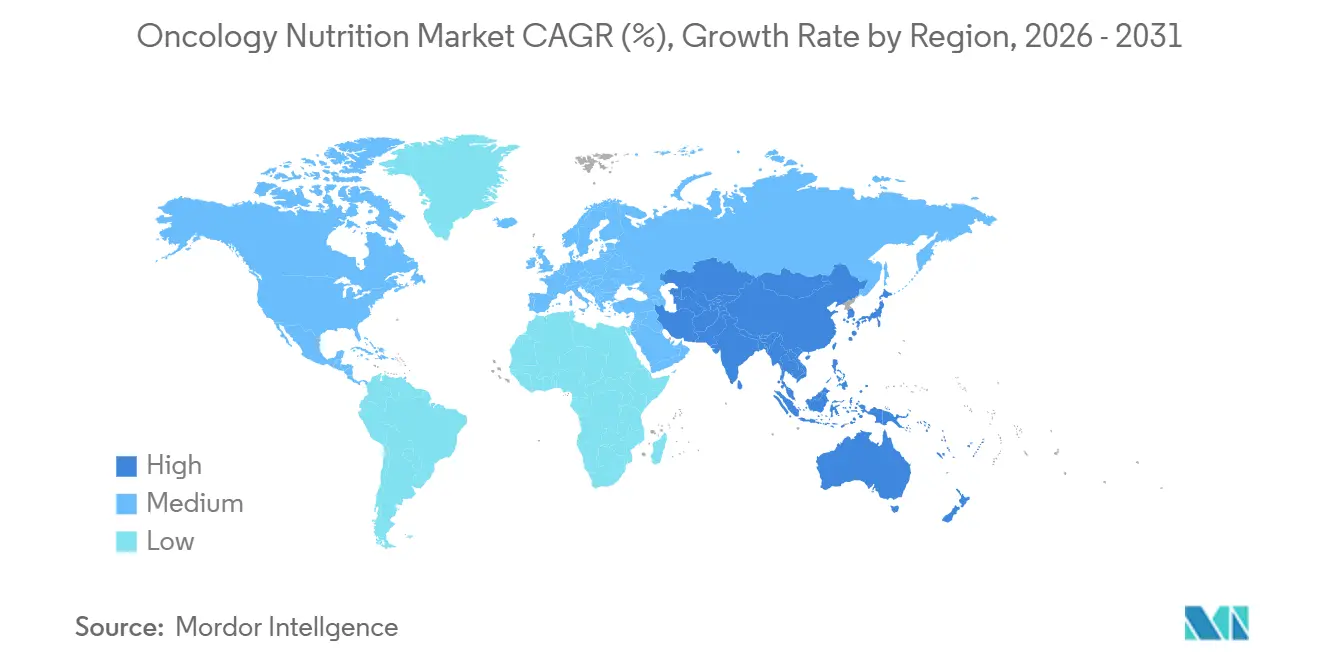

- By geography, North America retained 39.23% share in 2025, while Asia-Pacific is expected to record a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oncology Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cancer worldwide | +1.8% | Global, highest absolute growth in Asia-Pacific | Long term (≥ 4 years) |

| Shift from parenteral to enteral nutrition | +1.2% | North America and Europe lead | Medium term (2-4 years) |

| Growing adoption of home-based enteral devices | +1.4% | North America and Western Europe | Medium term (2-4 years) |

| Product innovation – elemental & immunonutrition | +0.9% | Global, fastest in North America and Japan | Short term (≤ 2 years) |

| AI-driven personalized nutrient planning | +0.5% | North America and select European centers | Long term (≥ 4 years) |

| Microbiome-modulating immunonutrition research | +0.6% | Global research, strong in North America, N. Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cancer Worldwide

Global cancer incidence stood at 20 million new cases in 2022 and is projected to soar to 35 million per year by 2050, a 75% upswing linked to aging populations, urban lifestyles, and broader screening programs. Forty-to-eighty percent of patients experience cancer-related malnutrition, which directly undermines chemotherapy completion and overall survival. Asia-Pacific is registering the fastest case growth, including sharp lung-cancer increases among never-smoking women exposed to air pollution. Head-and-neck cancers remain prevalent in South Asia because of tobacco and betel-nut habits, amplifying dysphagia-driven nutrition needs. Health systems are embedding screening tools such as the Patient-Generated Subjective Global Assessment to close the care gap.

Shift from Parenteral to Enteral Nutrition

Clinical evidence confirms that enteral routes cut catheter-related bloodstream infections by 40-50% compared with parenteral alternatives, a safety edge that is reshaping protocol templates in oncology wards. Enteral feeding maintains gut integrity and commensal microbiota, factors now linked to superior responses to immune-checkpoint inhibitors. Medicare dropped prior-authorization hurdles for home enteral nutrition in 2025, accelerating U.S. uptake[1]Centers for Medicare & Medicaid Services, “Medicare Coverage of Home Enteral Nutrition,” CMS, cms.gov . Device makers have introduced low-profile gastrostomy buttons and nasojejunal tubes that improve comfort and aesthetics, important for younger hematologic-oncology patients. Parenteral nutrition remains essential for severe mucositis and bowel obstruction, but its use is increasingly confined to specific complications.

Growing Adoption of Home-Based Enteral Feeding Devices

Payers and providers are prioritizing home nutrition support to reduce avoidable hospital days. A 2025 JAMA Oncology study documented USD 8,000-12,000 in six-month cost savings per patient when feeding was delivered at home rather than in the ward. Portable pumps now transmit usage data to dietitians, mitigating safety concerns and enabling prompt formula adjustments. Approximately 180,000 U.S. cancer patients used Medicare-funded home enteral services in 2025 and major private insurers aligned coverage soon after. Uptake is highest for head-and-neck and pancreatic cancers, which both impose protracted dysphagia and malabsorption challenges. Value-based payment contracts further incentivize rapid discharge once oncologic stability is achieved.

Product Innovation – Elemental & Immuno-Modulating Formulas

Manufacturers have shifted R&D toward elemental, semi-elemental, and immunonutrition lines that incorporate hydrolyzed proteins, arginine, glutamine, and omega-3 lipids. Elemental formulas improve tolerance for patients battling chemotherapy-induced mucositis, which affects up to 60% of pelvic-radiation recipients. A 2024 randomized trial showed perioperative immunonutrition cut postoperative infections by 30% and shortened hospital stays by two days in colorectal-cancer surgery, triggering guideline updates in Europe. Still, a 2025 lung-cancer study found no progression-free-survival benefit, suggesting tumor-specific protocols are required. U.S. FDA classifies these formulas as medical foods, enabling rapid launches yet constraining reimbursement options. Taste optimization is a new battleground, with plant-based and organic profiles winning favor with younger cohorts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium oncology nutrition products | -0.8% | Global, most acute in low- and middle-income markets | Short term (≤ 2 years) |

| Reimbursement gaps for outpatient therapy | -1.1% | North America and Europe; minimal public cover in Asia-Pacific | Medium term (2-4 years) |

| Feeding-tube infection and complication risk | -0.6% | Global, higher in resource-limited settings | Short term (≤ 2 years) |

| Supply-chain scarcity of specialized amino acids | -0.4% | Global, episodic shortages from China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium Oncology Nutrition Products

Immunonutrition formulas retail at USD 8-15 per serving, translating to USD 240-450 in monthly spending for patients requiring 1,500-2,000 kcal exclusively from enteral sources. In a 2024 U.S. survey, 38% of oncology patients reduced or discontinued supplements because of price, with Medicare beneficiaries in the coverage gap most affected. Generic polymeric formulas are cheaper but lack glutamine and omega-3 features that modulate inflammation, limiting their appeal to clinicians. In low-income regions, per capita health budgets of USD 50-200 make commercial products unattainable, forcing reliance on blenderized diets that frequently miss protein and micronutrient targets. Manufacturers wrestle with price-volume trade-offs: cutting prices widens access but dilutes margins on complex, quality-controlled supply chains.

Reimbursement Gaps for Outpatient Nutrition Therapy

Medicare funds home enteral and parenteral nutrition only for patients with permanent feeding access or severe malabsorption, excluding most chemotherapy recipients who would benefit from supplemental calories. Private insurers often label oral supplements as over-the-counter items and deny coverage, saddling patients with USD 200-400 monthly bills. In Europe, Germany reimburses comprehensively, but the United Kingdom requires prior authorization tied to specific tumor types, prolonging approval cycles[2]National Health Service, “Enteral Nutrition Service Specification,” NHS, nhs.uk . Asian markets exhibit minimal public reimbursement; only premium private plans in China and India cover specialized formulas for fewer than 10% of citizens. Without robust outcomes data demonstrating hospitalization savings, payers remain slow to broaden benefits, though ongoing health-economic studies aim to close this gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Head-and-Neck Dominance Meets Lung-Cancer Momentum

Head-and-neck malignancies captured 28.54% of Oncology nutrition market share in 2025, cementing their position as the largest revenue generator. Severe dysphagia, odynophagia, and xerostomia often last beyond the radiation window, driving extended gastrostomy dependence and sustained formula volumes. The Oncology nutrition market size allocated to lung cancer is projected to advance at a 7.25% CAGR through 2031, reflecting rising non-smoking-related incidence and the metabolic demands of PD-1/PD-L1 checkpoint combinations.

Radiation-induced mucositis affects up to 80% of head-and-neck patients, encouraging early prophylactic feeding-tube placement and elemental formula preference because of reduced digestive effort. Lung-cancer regimens elevate resting energy expenditure by 10-15%, and clinicians increasingly prescribe immunonutrition formulas to counter catabolism, though consensus on protocol specifics remains under debate. Stomach and gastrointestinal cancers add notable volume through long-term support needs after resections, while hematologic malignancies sustain parenteral demand during intensive chemotherapy phases.

By Nutrition Type: Enteral Preference Anchored by Clinical Evidence

Enteral products accounted for 75.54% of Oncology nutrition market size in 2025 as infection-avoidance benefits and lower costs underpin prescribing norms. Catheter bloodstream infections occur 40-50% less often with enteral routes, and gut-mediated immunity is thought to aid checkpoint-inhibitor efficacy. Parenteral nutrition, although holding only 24.46% share, is growing at 6.65% CAGR as advanced lipid emulsions cut inflammatory complications and home-infusion platforms broaden eligibility.

Reimbursement policy significantly influences modality choice. U.S. Medicare’s 2025 update waiving prior authorization for weight-loss cases above 10% boosted enteral discharges, whereas parenteral approvals still demand detailed malabsorption documentation. Cost remains a stark differential: USD 50-100 per day for enteral versus USD 150-300 for parenteral, steering hospital formularies toward enteral default except when contraindicated.

By Formula Type: Immunonutrition Innovation Outpaces Standard Products

Standard polymeric formulas maintained a 45.15% share in 2025 by offering balanced macronutrients at the lowest per-calorie cost, forming the backbone for routine hospital diets. Yet disease-specific and immunonutrition lines are forecast to expand at 7.82% CAGR through 2031 as clinicians test arginine- and omega-3-enriched variants against infection and inflammation metrics. Oncology nutrition market size for immunonutrition remains small today but could compound rapidly if positive surgical-oncology data translate into medical-oncology guidelines.

Elemental and semi-elemental formats, leveraging hydrolyzed proteins, are favored for mucositis or radiation enteritis patients because they reduce digestive workload. FDA’s medical-food classification speeds launches but constrains marketing claims, requiring manufacturers to invest in clinician education rather than direct-to-consumer promotion. Taste evolution is central: plant-based options from new entrants are winning share in young adult segments that report lactose intolerance and flavor fatigue.

By End User: Home Care Ascendance Reshapes Delivery Models

Hospitals generated 58.23% of end-user revenue in 2025 because they initiate cancer care, place feeding tubes, and manage acute complications. However, the Oncology nutrition market share flowing to home care is expanding quickly under an 8.42% CAGR as value-based reimbursement penalizes prolonged inpatient stays. Remote pump telemetry supports dietitian oversight, and courier networks enable direct-to-door deliveries that sustain adherence.

Specialty oncology clinics and infusion centers distribute oral supplements during chemotherapy visits, creating an integrated care loop that improves compliance. Telehealth dietitian appointments, sanctioned permanently in many U.S. states after pandemic waivers, further erode historical site-of-care barriers. Over the forecast horizon, hybrid models blending virtual consults with periodic in-person tube-care visits are expected to dominate.

Geography Analysis

North America held 39.23% of global revenue in 2025, anchored by Medicare coverage, two-million-plus annual cancer diagnoses, and entrenched clinical pathways that mandate nutrition screening at each chemotherapy cycle. The 2025 removal of prior-authorization requirements for home enteral therapy simplified discharge and swelled supplier order volumes. Canada’s coverage is province-specific, with Ontario and British Columbia offering the most generous benefits, while Mexico’s public systems lag, propelling private insurance uptake.

Europe ranked second, led by Germany, the United Kingdom, France, Italy, and Spain. Germany’s universal insurance reimburses home enteral nutrition comprehensively, driving per-capita consumption rates among the world’s highest. The United Kingdom’s National Health Service grants coverage to select tumor types only, making patient advocacy pivotal to policy expansion. Eastern European markets are rising as oncology infrastructure modernizes and EU funding improves supply chains.

Asia-Pacific is projected to deliver a 7.12% CAGR through 2031. China’s regulator approved multiple enteral products in 2024-2025, and its aging population is driving lung, gastric, and colorectal volume[3]National Medical Products Administration China, “Enteral Product Approvals 2024-2025,” NMPA, nmpa.gov.cn . India struggles with reimbursement gaps but flagship tertiary hospitals in metro areas are aligning with global nutrition guidelines. Japan’s universal payer system underwrites home enteral therapy, supporting stable demand even as total population contracts. Mature markets such as Australia and South Korea enjoy high adoption, while Southeast Asia remains nascent because of affordability barriers.

Competitive Landscape

Abbott Laboratories, Nestlé Health Science, Danone SA (Nutricia), and others collectively control a moderate share of the Oncology nutrition market, supported by global manufacturing, hospital purchasing contracts, and broad product portfolios spanning polymeric, elemental, and immunonutrition lines. Abbott’s nutrition division booked USD 8.1 billion in 2024 revenue, although oncology-specific figures remain undisclosed. Fresenius Kabi pledged EUR 50 million (USD 54 million) to expand Chinese production in 2025, underscoring Asia-Pacific growth ambitions.

Challenger brands such as Kate Farms are winning mindshare with dairy-free, organic formulas that target taste aversion and lactose intolerance. Strategic patterns across incumbents center on immunonutrition studies intended to differentiate premium lines, geographic expansion into high-growth Asian markets, and digital services that pair formulas with tele-dietitian counseling. The FDA’s medical-food pathway accelerates product launches but limits premium pricing potential, compelling firms to pursue cost leadership or clinical-evidence-backed differentiation. White-space opportunities include microbiome-modulating blends, AI-personalized packs, and low-cost SKUs tailored to emerging markets.

Oncology Nutrition Industry Leaders

Abbott Laboratories

Nestlé

B. Braun SE

Danone SA (Nutricia)

Reckitt Benckiser Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nutricia partnered with oncology societies worldwide to highlight the role of medical nutrition in cancer care.

- September 2025: University of Florida Health Cancer Center and Sylvester Comprehensive Cancer Center launched a food-pharmacy pilot to improve oncology patient access to nutrient-dense foods, backed by a Florida Department of Health grant.

Global Oncology Nutrition Market Report Scope

As per the scope of the report, oncology nutrition is a vital part of the entire process of recovering from cancer. Consuming a wide variety of foods and nutritious meals helps in coping with the heavy medication that is a part of cancer treatment. In well-balanced oncology, nutrition helps improve strength, maintain body weight, and assist the body in recovering from cancer.

The oncology nutrition market is segmented by cancer type into head and neck cancer, stomach and gastrointestinal cancer, blood cancer, breast cancer, lung cancer, and other cancers. By nutrition type, the market is divided into enteral nutrition and parenteral nutrition. Based on formula type, it is categorized into standard formula, elemental/semi-elemental formula, and disease-specific/immunonutrition formula. By end user, the market is segmented into hospitals, home care settings, and specialty oncology clinics. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Head & Neck Cancer |

| Stomach & Gastrointestinal Cancer |

| Blood Cancer |

| Breast Cancer |

| Lung Cancer |

| Other Cancers |

| Enteral Nutrition |

| Parenteral Nutrition |

| Standard Formula |

| Elemental / Semi-elemental Formula |

| Disease-specific / Immunonutrition Formula |

| Hospitals |

| Home Care Settings |

| Specialty Oncology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cancer Type | Head & Neck Cancer | |

| Stomach & Gastrointestinal Cancer | ||

| Blood Cancer | ||

| Breast Cancer | ||

| Lung Cancer | ||

| Other Cancers | ||

| By Nutrition Type | Enteral Nutrition | |

| Parenteral Nutrition | ||

| By Formula Type | Standard Formula | |

| Elemental / Semi-elemental Formula | ||

| Disease-specific / Immunonutrition Formula | ||

| By End User | Hospitals | |

| Home Care Settings | ||

| Specialty Oncology Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will Oncology nutrition market spending be by 2031?

It is projected to reach USD 3.96 billion by 2031, expanding at a 6.12% CAGR from 2026 to 2031.

Which cancer type currently drives the most nutrition demand?

Head-and-neck cancer leads, accounting for 28.54% of Oncology nutrition market share in 2025.

Which product route is preferred in clinical oncology nutrition?

Enteral feeding dominates with 75.54% share in 2025 because it lowers infection risk and preserves gut immunity.

What geography is expected to grow the fastest?

Asia-Pacific is forecast to post a 7.12% CAGR through 2031 as cancer incidence rises and insurance coverage expands.

What is the biggest obstacle to wider adoption of premium immunonutrition?

Fragmented reimbursement keeps many patients paying USD 200-450 monthly out-of-pocket, curbing adherence and uptake.

Are artificial-intelligence tools already used in oncology nutrition planning?

Yes, pilots at leading U.S. cancer centers showed 18% adherence gains and 12% fewer unplanned hospitalizations after launching AI-guided nutrient programs in 2025.

Page last updated on: