Metastatic Cancer Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

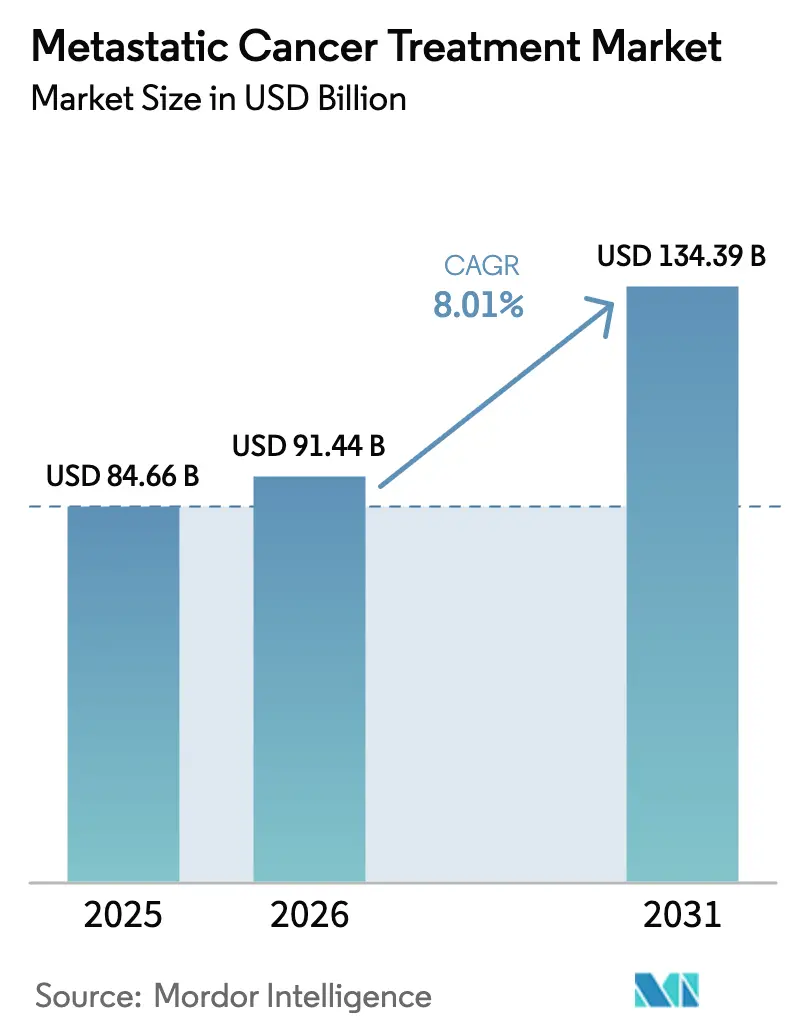

| Market Size (2026) | USD 91.44 Billion |

| Market Size (2031) | USD 134.39 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

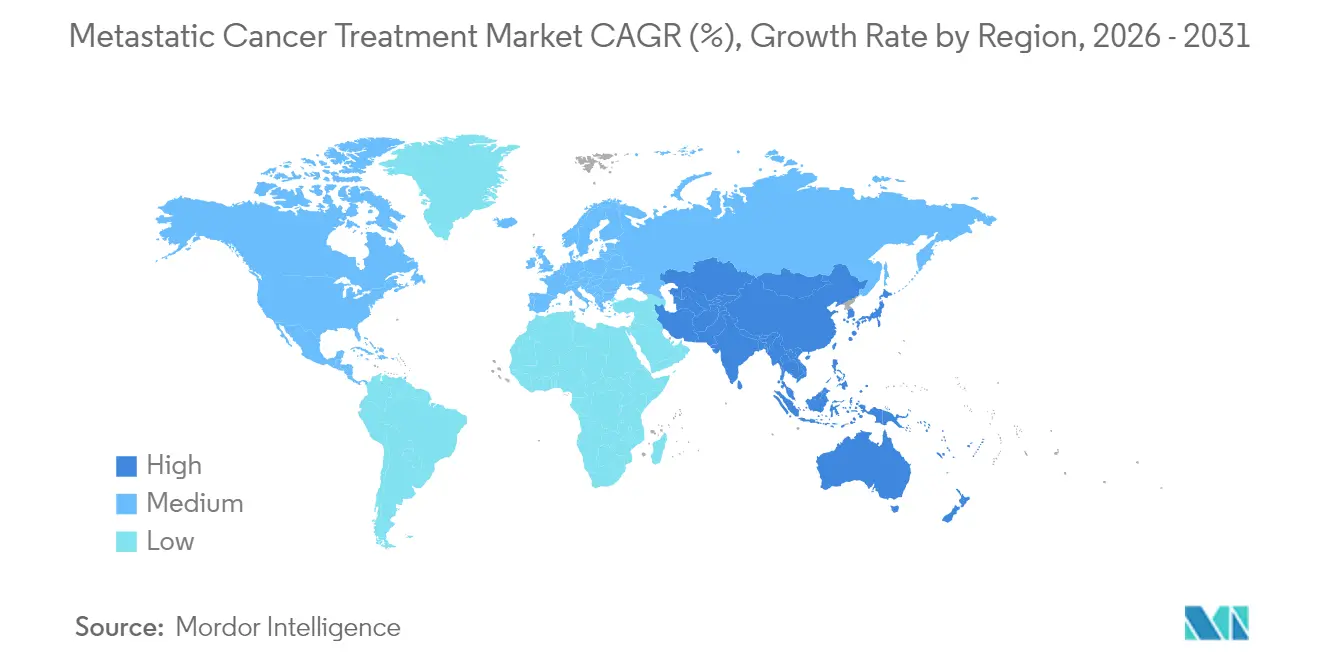

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metastatic Cancer Treatment Market Analysis by Mordor Intelligence

The metastatic cancer treatment market size in 2026 is estimated at USD 91.44 billion, growing from 2025 value of USD 84.66 billion with 2031 projections showing USD 134.39 billion, growing at 8.01% CAGR over 2026-2031. Rapid regulatory clearances, rising precision-guided therapy use, and wider health-system reimbursement underpin this expansion. Momentum stems from 55 U.S. Food and Drug Administration approvals in 2024—the second-highest oncology total in three decades—and 28 positive European Medicines Agency opinions that same year, underscoring the shift from cytotoxic regimens to pathway-targeted and immune-modulating approaches. Targeted therapy already leads the metastatic cancer treatment market with a 54.51% share, yet cell and gene therapy is advancing the fastest at an 18.25% CAGR on the back of CAR-T production scale-ups and tumor-infiltrating lymphocyte breakthroughs. Hospital networks remain the primary treatment venue, but specialty clinics are expanding swiftly, mirroring decentralised trial models that cut enrolment timelines by up to 50% versus conventional sites. Regionally, North America keeps its lead, Asia-Pacific shows the highest growth, and patent-driven dealmaking is reshaping competitive positions.

Key Report Takeaways

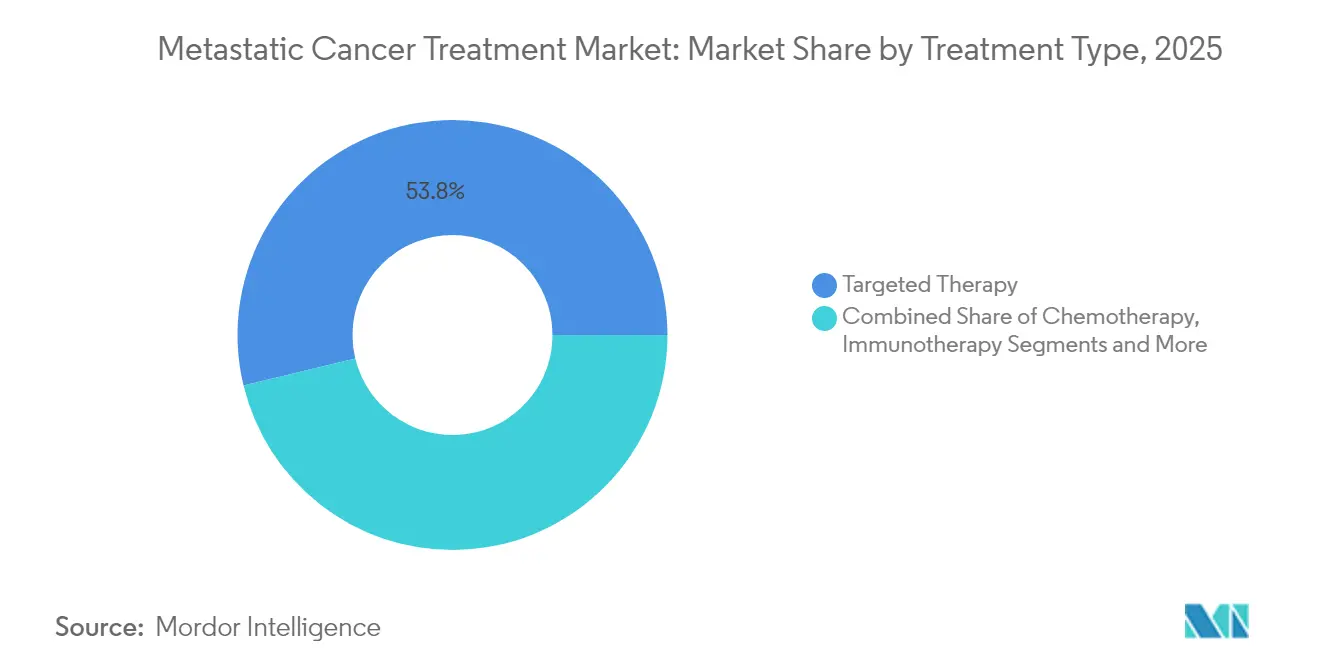

- By treatment type, targeted therapy commanded 53.78% of the metastatic cancer treatment market share in 2025; cell and gene therapy is projected to grow at an 17.35% CAGR to 2031.

- By cancer type, lung cancer led with 25.08% of the metastatic cancer treatment market size in 2025, while liver metastases will expand at a 12.14% CAGR through 2031.

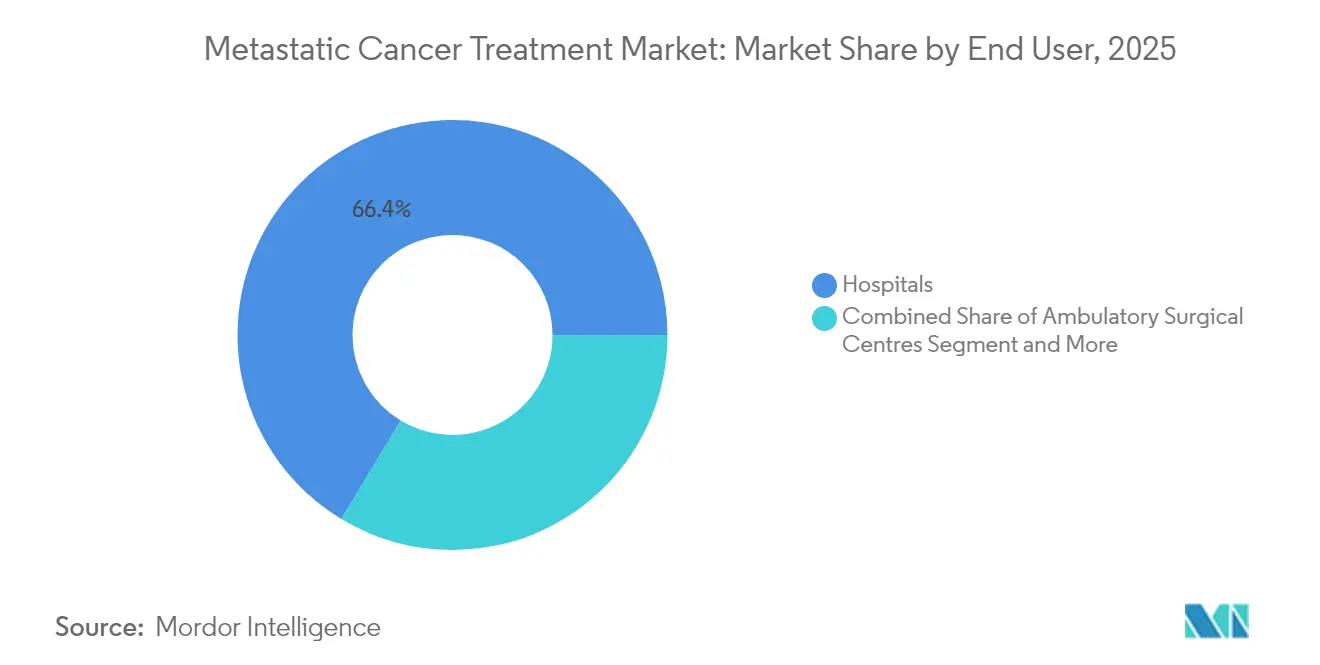

- By end user, hospital-based centres accounted for 66.35% of the metastatic cancer treatment market in 2025; specialty clinics post the highest forecast CAGR at 9.78% to 2031.

- By geography, North America captured 44.89% of the metastatic cancer treatment market in 2025, whereas Asia-Pacific is on track for a 10.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metastatic Cancer Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of metastatic cancers | +1.5% | Global, strongest in ageing North America & Europe | Long term (≥ 4 years) |

| Accelerated FDA/EMA approvals & label expansions | +1.2% | North America & Europe, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Surge in immunotherapy adoption | +0.8% | Global, earliest uptake in advanced markets | Medium term (2–4 years) |

| Precision-medicine & companion-diagnostic uptake | +0.6% | Core in North America & Europe, rising in Asia-Pacific | Long term (≥ 4 years) |

| Tumor-agnostic approvals expanding revenue | +0.4% | Regulatory-advanced markets first, then global | Medium term (2–4 years) |

| Decentralised clinical-trial models | +0.3% | Dependent on digital readiness worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated FDA/EMA approvals & label expansions

Breakthrough therapy designations now cut median U.S. review times to 6.1 months, while the EMA issued eight conditional approvals for oncology products in 2024, including tisotumab vedotin and linvoseltamab, showing regulatory flexibility for high-need indications[1]European Medicines Agency, “New EU rules for health technology assessments become effective,” ema.europa.eu. Streamlined CAR-T umbrella evaluations further trim filing burdens by 40%, advantaging sponsors with robust manufacturing and late-stage assets. Joint clinical assessments under the European Health Technology Assessment framework promise aligned value dossiers across member states, narrowing launch gaps and accelerating revenue capture.

Surge in immunotherapy adoption

Checkpoint inhibitors now span 15 approved tumour types, with biomarker-driven selection lifting overall response rates to 45% in PD-L1-positive populations. Combination regimens that convert “cold” tumours into inflamed phenotypes through radiation or oncolytic viruses broaden eligibility beyond the historical 30% responsive cohort, and early data with linvoseltamab shows a 70% objective response in heavily pre-treated myeloma. Such outcomes cement the metastatic cancer treatment market as an innovation engine for durable survival gains.

Precision-medicine & companion-diagnostic uptake

Eight tumour-agnostic therapies now mandate companion diagnostics, adding USD 2.3 billion in global testing revenue streams. Next-generation sequencing, liquid biopsy, and AI interpretation together reduced turnaround to 3 days, enabling same-clinic treatment decisions and making precision workflows mainstream. Diagnostic-therapeutic integrators enjoy 60% higher uptake than stand-alone drug developers, underscoring the business case for platform strategies.

Tumor-agnostic approvals creating new revenue pools

Broad molecular targeting triples the addressable base compared with single-indication launches. Pembrolizumab now holds clearances across 20 histologies, while larotrectinib treats any solid tumour harbouring NTRK fusions, giving sponsors multi-billion pipelines without de-novo discovery programmes. Flexible study designs also cut recruitment periods by 40%, concentrating capital efficiency and speeding time-to-break-even.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs & reimbursement hurdles | -0.9% | Global, highest pressure in emerging markets | Long term (≥ 4 years) |

| Severe immune-related adverse events (irAEs) | -0.7% | Advanced systems better equipped | Medium term (2–4 years) |

| Limited efficacy in cold tumours | -0.5% | Impacts 60–70% of solid tumour patients worldwide | Long term (≥ 4 years) |

| Radionuclide & cell-therapy supply bottlenecks | -0.4% | Manufacturing centred in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High treatment costs & reimbursement hurdles

Average CAR-T pricing near USD 450,000 per course and antibody-drug conjugates exceeding USD 180,000 annually create affordability barriers. Total care costs soar another 60–80% due to specialised administration and toxicity management. Forty percent of U.S. commercial payers require prior authorisation for combination regimens, delaying optimal initiation, while European HTA bodies push for cost per quality-adjusted life year below EUR 100,000. Value-based contracting and biosimilar entry offer partial relief.

Severe immune-related adverse events (irAEs)

Grade 3-4 toxicities occur in up to 30% of immunotherapy recipients and trigger discontinuation in roughly 15%. Long-term endocrinopathies and pneumonitis inflate per-patient costs by USD 75,000–150,000. Access to specialist immunotoxicity clinics is uneven outside major academic centres, constraining broader uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Precision regimens anchor demand while cell therapy accelerates

Targeted therapies commanded 53.78% of 2025 revenue, anchored by robust biomarker-led protocols that cut empirical failure rates nearly in half. The segment enjoys stable formulary positioning and benefits from progressive label extensions. Chemotherapy persists mainly as a backbone for new combination protocols, and immunotherapy continues its expansion. Cell and gene therapy, though starting from a low base, posts the highest 17.35% CAGR. Legend Biotech’s plan to double Carvykti slots to 10,000 in 2025 exemplifies the infrastructure build-out required to satisfy demand. Novartis is similarly scaling radioligand output to 250,000 annual doses, addressing historic supply shortages.

The metastatic cancer treatment market size for cell and gene therapy is projected to expand at 17.35% CAGR between 2026 and 2031 on the back of manufacturing advances and favourable reimbursement pilots. Targeted therapy, despite slower percentage growth, will still add the largest absolute revenue owing to its broad base and numerous upcoming small-molecule launches.

By Cancer Type: Lung cancer holds leadership and liver metastases surge

Lung malignancies represented 25.08% of the metastatic cancer treatment market share in 2025, supported by universal EGFR, ALK, ROS1, and KRAS G12C screening. Continuous detection initiatives and liquid biopsy adoption sustain this edge. Breast cancer follows, driven by HER2-directed and CDK4/6 regimens, while prostate oncology benefits from androgen-pathway and PARP innovations.

Liver metastases treatment clocked the fastest 12.14% CAGR, propelled by histotripsy and improved ablation devices that create minimally invasive options for previously inoperable cases. Consequently, the metastatic cancer treatment market size for liver metastases is expected to outpace colorectal and melanoma segments through 2031, offering device and drug makers a high-growth niche.

By End User: Hospital concentration endures but specialty clinics gain ground

Hospitals retained 66.35% revenue in 2025 due to complex procedure requirements, central pharmacy infrastructure, and higher reimbursement. The metastatic cancer treatment market share is likely to stay hospital-centric for CAR-T and radioligand infusions that demand round-the-clock monitoring. Academic centres inside the hospital group often act as early technology adopters.

Specialty clinics, however, are rising at a 9.78% CAGR. Consolidated oncology practices, tele-oncology, and remote monitoring allow sophisticated regimens to move outside tertiary centres, improving patient convenience and cutting indirect costs. Decentralised trials executed through these clinics have already reduced enrolment timelines by an average 40%, further supporting their momentum.

Geography Analysis

North America generated 44.89% of revenue in 2025, underpinned by robust Medicare reimbursement, multi-state early-access pathways, and a mature clinical-trial ecosystem that hosts 60% of active global oncology protocols. The United States enjoys rapid uptake thanks to breakthrough designations that shave 6–12 months off launch timelines. Canada provides universal coverage yet faces longer provincial negotiations.

Europe stands second, benefiting from the EMA’s eight conditional oncology approvals in 2024. Germany leads uptake through well-funded cancer centres, while the United Kingdom imposes stricter cost-effectiveness hurdles. Southern European nations such as Spain have become attractive trial hubs, aided by EU-level cross-border research networks.

Asia-Pacific delivers the strongest 10.22% CAGR. China slashed approval cycles to 12 months and expanded domestic biologic capacity, boosting access and price competition. Japan, with its rapidly ageing demographic, embraces novel regimens like tislelizumab. India leverages large generic plants and a vibrant medical-tourism economy, while South Korea and Australia supply sophisticated trial sites. Rising incidence—projected up 24% by 2035—keeps demand high.

Competitive Landscape

The metastatic cancer treatment industry remains moderately concentrated as diversified pharmaceutical majors battle agile biotechs. Bristol Myers Squibb, Roche, and Merck hold depth across checkpoints, antibody-drug conjugates, and radioligands. Pipeline gaps from looming patent cliffs prompt bolt-on M&A: Bristol Myers Squibb bought Mirati for USD 4.8 billion to secure KRAS G12C assets, and Merck spent USD 10.8 billion on Harpoon Therapeutics to access T-cell engagers[3]White & Case, “Oncology dealmaking fuels biotech M&A,” whitecase.com. Integrated diagnostic partnerships help incumbents defend share by embedding their medicines into testing algorithms.

Emerging players specialise in niche modalities. Novartis scales radioligand therapy, Legend Biotech focuses on BCMA-directed CAR-T, and Iovance pioneers TIL therapy for solid tumours, having filed Europe’s first application in 2024. Success hinges on manufacturing agility, payer alignment, and safety management infrastructure.

Digital health firms supply predictive algorithms for toxicity, adherence, and value tracking, positioning themselves as essential collaborators. The result is a dynamic marketplace where data, diagnostics, and drugs increasingly converge around the shared goal of durable control of advanced disease.

Metastatic Cancer Treatment Industry Leaders

Bristol Myers Squibb Company

Merck and Co Inc.

Johnson & Johnson Services Inc

Novartis AG

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: EMA issued a positive opinion for Tivdak (tisotumab vedotin) in recurrent or metastatic cervical cancer, evidencing superior survival versus chemotherapy.

- June 2024: Iovance Biotherapeutics filed for EU approval of lifileucel, the first TIL therapy targeting advanced melanoma, setting a precedent for solid-tumour cellular immunotherapy.

Global Metastatic Cancer Treatment Market Report Scope

As per the scope of the report, metastatic cancer is a type of cancer that spreads from its original site to another portion of the body. It is also known as stage IV cancer for a variety of cancer forms. Metastasis is the term used to describe the process by which cancer cells spread to different areas of the body. The goal of metastatic cancer treatment is to slow the disease's progression or growth. The metastatic cancer treatment market is segmented by Treatment Type (Chemotherapy, Immunotherapy, Hormone Therapy, and Other Therapies), Type of Cancer (Breast Cancer, Lung Cancer, Prostate Cancer, Melanoma, Colorectal Cancer, and Other Type of Cancer), End Users (Hospitals, Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Chemotherapy |

| Immunotherapy |

| Targeted Therapy |

| Hormone Therapy |

| Cell & Gene Therapy |

| Radiation Therapy |

| Breast |

| Lung |

| Prostate |

| Colorectal |

| Melanoma |

| Liver |

| Others |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Chemotherapy | |

| Immunotherapy | ||

| Targeted Therapy | ||

| Hormone Therapy | ||

| Cell & Gene Therapy | ||

| Radiation Therapy | ||

| By Cancer Type | Breast | |

| Lung | ||

| Prostate | ||

| Colorectal | ||

| Melanoma | ||

| Liver | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centres | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current metastatic cancer treatment market size?

The metastatic cancer treatment market size is USD 91.44 billion in 2026, with an 8.01% forecast CAGR through 2031.

Which treatment type dominates the metastatic cancer treatment market?

Targeted therapy leads, accounting for 53.78% of 2025 revenue thanks to widespread biomarker-guided use.

Why is cell and gene therapy growing rapidly?

Manufacturing expansions, favourable reimbursement pilots, and strong clinical responses drive an 17.35% CAGR for cell and gene therapy between 2026 and 2031.

Which region shows the fastest growth?

Asia-Pacific posts the highest forecast CAGR at 10.22% through 2031 due to faster approvals, manufacturing investment, and a rising incidence burden.

How are high treatment costs being addressed?

Manufacturers increasingly pursue value-based contracts and explore biosimilar or next-generation platforms aimed at lowering acquisition and total care costs.

Page last updated on: