Cardiovascular Repair and Reconstruction Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.37 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiovascular Repair and Reconstruction Devices Market Analysis by Mordor Intelligence

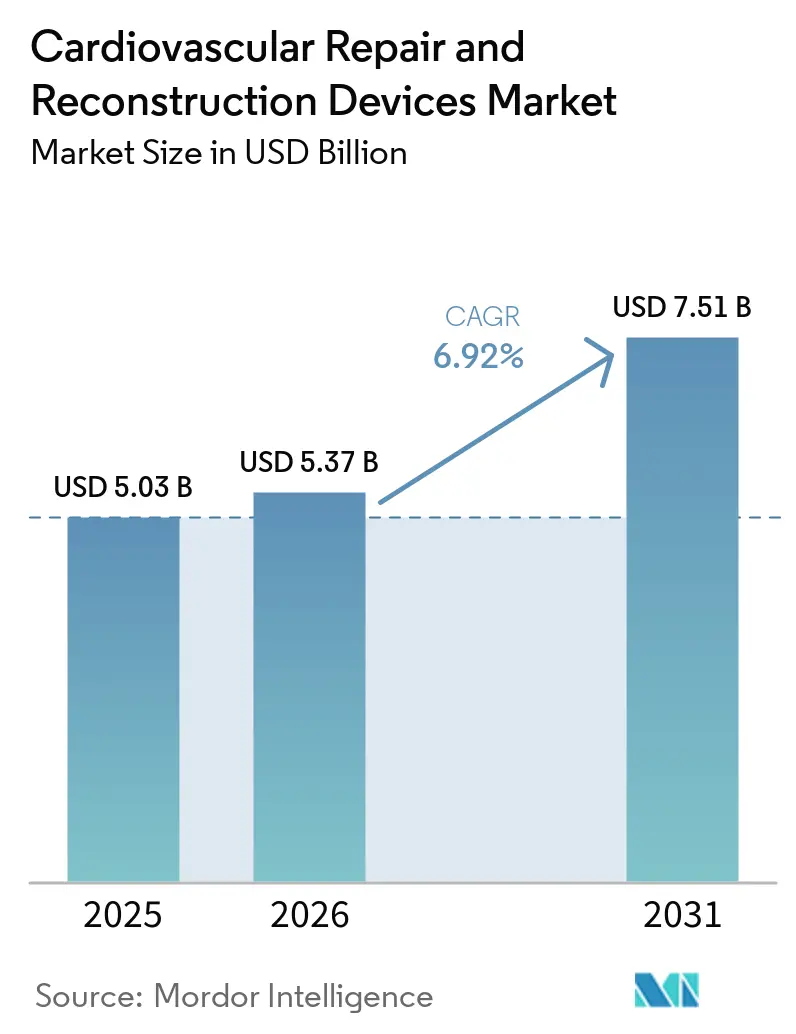

The Cardiovascular Repair And Reconstruction Devices Market size is projected to be USD 5.03 billion in 2025, USD 5.37 billion in 2026, and reach USD 7.51 billion by 2031, growing at a CAGR of 6.92% from 2026 to 2031.

The market is being pushed by the rising burden of structural heart and vascular disease, while older patient profiles are also increasing the need for less invasive treatment routes. The cardiovascular repair and reconstruction devices market is also expanding because transcatheter systems are moving into more complex mitral and tricuspid settings, which is widening the treatable population instead of only replacing existing surgery volumes. Imaging upgrades and bioabsorbable implant development are also changing procedure economics and long-term durability expectations, which supports broader use across hospital and catheter-based settings. Competition remains moderately consolidated at the platform level, with Abbott, Edwards Lifesciences, and Medtronic holding strong positions while targeted acquisitions and investments continue to reshape white-space areas such as aortic arch repair and TAVR platform expansion. At the same time, the cardiovascular repair and reconstruction devices market still faces limits from capital intensity, long Class III approval pathways, reimbursement friction for newer structural technologies, and the need for long-duration durability evidence before newer materials scale more widely.

Key Report Takeaways

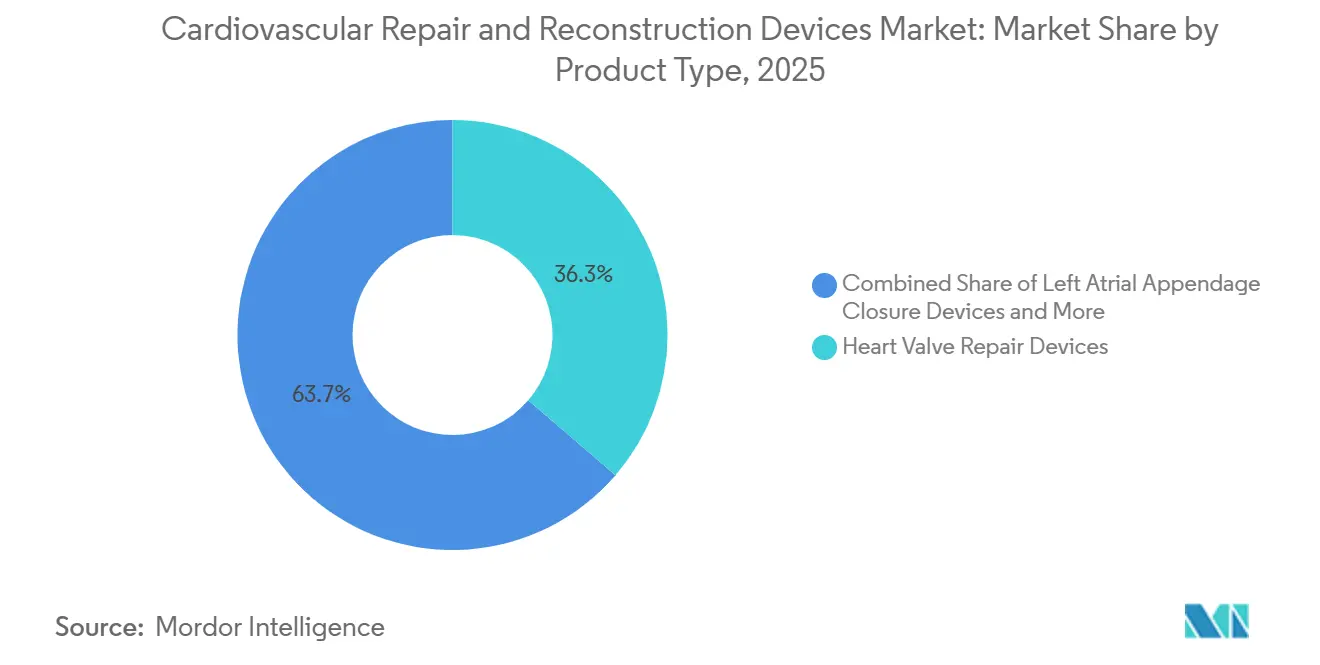

- By product type, Heart Valve Repair Devices led with 36.31% share in 2025, while Left Atrial Appendage Closure Devices are forecast to expand at a 7.38% CAGR through 2031.

- By material, Biological Tissue held 33.24% share in 2025, while Bioabsorbable and Hybrid Materials are expected to project a CAGR at 8.52% through 2031.

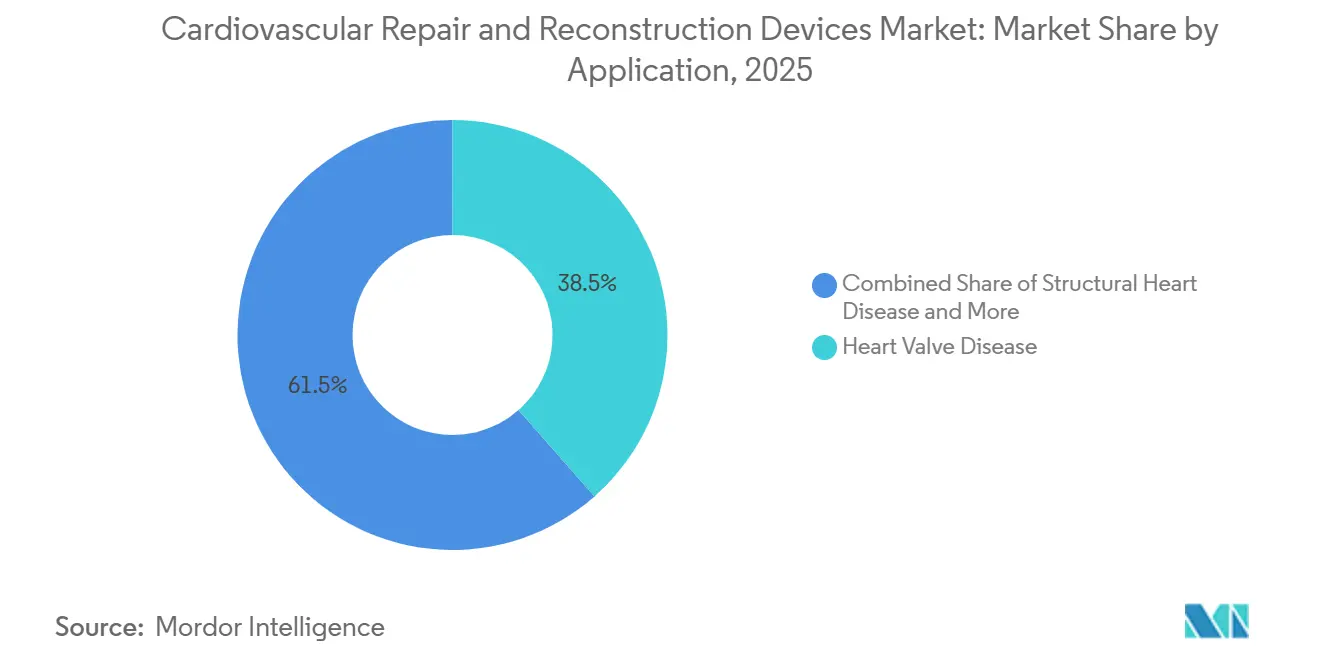

- By application, Heart Valve Disease accounted for 38.52% share in 2025, while Structural Heart Disease is expected to advance at a 7.25% CAGR through 2031.

- By end user, Hospitals captured 45.52% share in 2025, while Cardiac Catheterization Laboratories are projected to grow at an 8.25% CAGR through 2031.

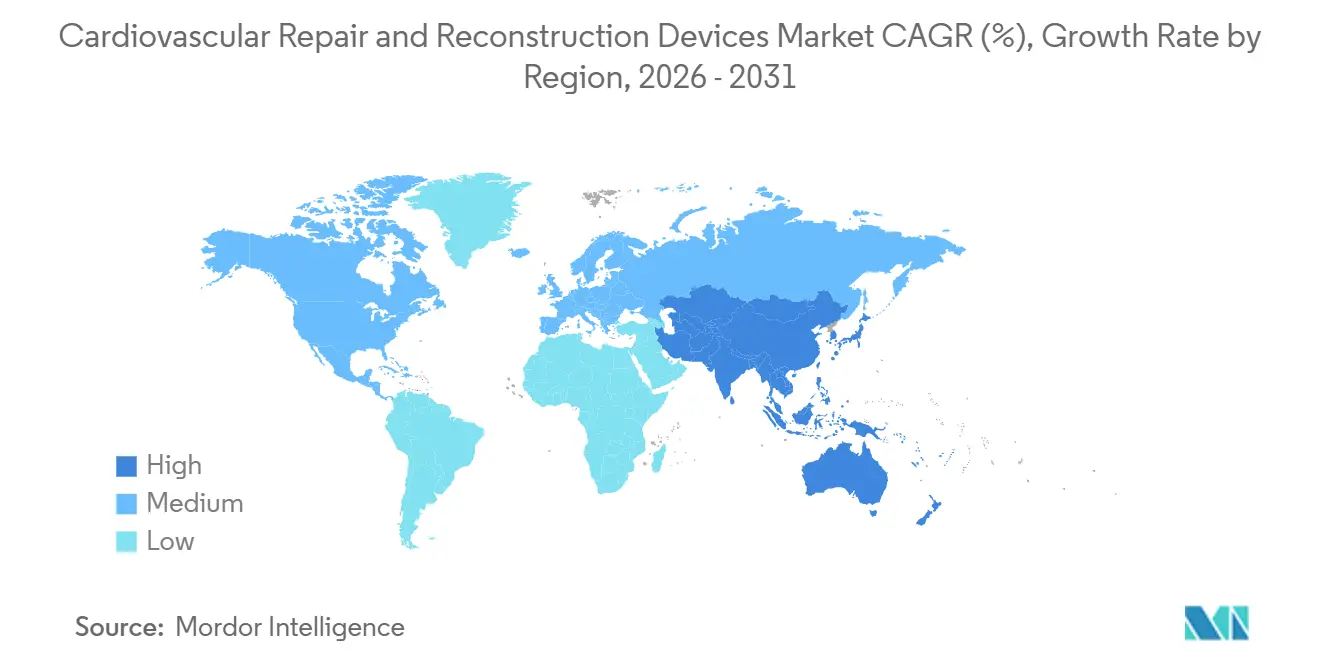

- By geography, North America held 38.22% share in 2025, while Asia-Pacific is forecast to expand at a 7.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiovascular Repair and Reconstruction Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Structural Heart and Vascular Disease | +2.1% | Global, concentrated in APAC, North America, and EU | Long term (≥ 4 years) |

| Shift Toward Transcatheter and Minimally Invasive Repair | +1.8% | Global, led by North America and Europe, accelerating in APAC | Medium term (2-4 years) |

| Aging and Frailty-Driven Surgical Risk Profile | +1.3% | North America, Europe, Japan, expanding in China and South Korea | Long term (≥ 4 years) |

| Imaging-Guided Device Navigation and Procedure Planning | +0.8% | North America and Europe, early adoption in APAC | Medium term (2-4 years) |

| Hospital Ambulatory Migration for Selected Cardiac Interventions | +0.5% | North America, with early signals in Western Europe | Short term (≤ 2 years) |

| Demand for Durable, Reintervention-Reducing Implants | +0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Structural Heart and Vascular Disease

The cardiovascular repair and reconstruction devices market is benefiting from a disease base that remains large and still rising in absolute volume. Non-rheumatic valvular heart disease recorded 28.4 million prevalent cases globally in 2021, and global incidence is projected to reach 20.28 per 100,000 by 2035. TAVI volumes reached 150,000 procedures annually by 2021, yet the treatable valve population remains much larger, which shows that access limits, not disease absence, still hold back volumes in many emerging settings. As PCI and EP ablation capacity expands across Southeast Asia and Latin America, structural heart programs are likely to follow the same hospital adoption path already seen in other interventional services. The gap between rising case counts and lower age-standardized mortality rates shows that device-based intervention is taking on a growing share of incremental patient management, which directly supports long-run demand in the cardiovascular repair and reconstruction devices market.

Shift Toward Transcatheter and Minimally Invasive Repair

The cardiovascular repair and reconstruction devices market is also being lifted by a clear clinical shift toward transcatheter and minimally invasive repair. In a 12-year Japanese cohort, 30-day TAVI mortality fell from 2.8% in 2013 to 0.4% in 2024, while annual case volume increased fourfold over the same period. This improvement in outcomes has supported guideline expansion into lower-risk patient groups and has given regulators a stronger basis for approving newer systems. Abbott received FDA approval in May 2025 for the Tendyne TMVR system for severe mitral annular calcification, which opened a patient group that had very limited surgical or transcatheter options before that point[1]Abbott Laboratories, “Abbott Receives FDA Approval for Tendyne, First-of-Its-Kind Device to Replace the Mitral Valve Without Open-Heart Surgery,” Abbott Newsroom, abbott.mediaroom.com. Edwards then received FDA approval in December 2025 for the SAPIEN M3 system as the first transseptal transcatheter mitral replacement therapy, showing that even difficult anatomical positions are moving toward percutaneous treatment. Germany also remains the highest-volume TAVI country in Europe, which indicates that established high-income systems are still generating new volume as indications widen.

Aging and Frailty-Driven Surgical Risk Profile

The cardiovascular repair and reconstruction devices market is being reinforced by population aging and by the higher frailty burden that comes with it. The global population aged over 70 years is projected to reach 2 billion by 2050, and ischemic heart disease, stroke, and hypertensive heart disease remain the leading causes of death in this age group. Older and frailer patients are less suitable for open surgical correction, which creates a steady need for lower-burden treatment pathways. Low-risk TAVI patients recorded 30-day mortality of 0.2% in 2024, which strengthens the case for broader use as lifetime valve planning becomes more important in clinical practice. Frailty-adjusted risk scoring and aging demographics together create a durable demand base that should continue to support the cardiovascular repair and reconstruction devices market over a long horizon.

Imaging-Guided Device Navigation and Procedure Planning

The cardiovascular repair and reconstruction devices market is also gaining from better imaging during planning and navigation. Three-dimensional intracardiac echocardiography is replacing transesophageal echocardiography in a growing set of structural heart procedures, which removes the need for general anesthesia in many cases and supports same-day discharge. A multicenter evaluation of the VeriSight Pro 3D ICE catheter showed safe and effective guidance across LAAC, mitral valve-in-valve, and PFO closure procedures, with no adverse events tied to the imaging platform. Philips launched DeviceGuide AI in Europe in 2025, and the platform combines live echocardiographic and X-ray images to create a real-time 3D model of the device inside the heart. The SCAI position statement published in 2025 also gives a more formal framework for ICE-guided structural interventions, which should shape future design expectations for transcatheter implants. Because ICE-guided procedures do not always need an anesthesia team, they can reduce cost and raise throughput in cath labs and outpatient settings, which supports broader use across the cardiovascular repair and reconstruction devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity of Advanced Valve and Graft Platforms | -0.9% | Global, most pronounced in APAC emerging markets and South America | Long term (≥ 4 years) |

| Lengthy Regulatory Pathways for Class III Cardiovascular Devices | -0.7% | Global, with distinct profiles in the United States and European Union | Medium term (2-4 years) |

| Reimbursement Friction for Newer Structural Heart Technologies | -0.6% | North America, secondary in Europe | Medium term (2-4 years) |

| Long-Term Evidence Requirements for Implant Durability and Patency | -0.4% | Global, most acute for novel biomaterial and first-in-class transcatheter platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Advanced Valve and Graft Platforms

The cardiovascular repair and reconstruction devices market still faces a clear funding barrier because advanced valve systems and graft platforms remain expensive to procure and deploy. Per-implant costs for advanced transcatheter valves and next-generation graft technologies range from USD 25,000 to USD 50,000, which can limit adoption in cost-sensitive health systems. Boston Scientific’s 2025 decision to discontinue global sales of Acurate neo2 and Acurate Prime after the platforms failed to secure FDA clearance shows how costly long development cycles can become, especially when clinical investment does not convert into commercial access. In middle-income markets, hospitals also need hybrid operating suites, advanced 3D imaging systems, and multidisciplinary structural heart teams, and these facility requirements often amount to USD 5 million or more. This cost structure strengthens the position of large manufacturers with broad portfolios and makes it harder for single-product entrants to disrupt the cardiovascular repair and reconstruction devices market.

Lengthy Regulatory Pathways for Class III Cardiovascular Devices

The cardiovascular repair and reconstruction devices market is also slowed by demanding approval pathways for Class III devices. Most repair and reconstruction implants require FDA Premarket Approval, and review periods can range from 1 to 5 years while submission costs can reach USD 1 million to USD 10 million or more[2]U.S. Food and Drug Administration, “Overview of Device Regulation,” FDA, fda.gov. Under MDUFA V for FY 2025 to FY 2027, the FDA average total time to a PMA decision is 285 days, but first-in-class structural heart systems often take longer because of extra clinical data requests and advisory review. In the European Union, the Medical Device Regulation has raised evidence expectations compared with the earlier MDD framework, and joint clinical assessments began in 2026 under the EU Health Technology Assessment Regulation. A Frontiers in Medical Technology review found that only 12.3% of 1,041 FDA Breakthrough Device-designated products received marketing authorization between 2015 and 2024, and the mean decision time for standard PMA cases was 399 days. These delays weigh most heavily on smaller innovators and are especially relevant for bioabsorbable conduits and hybrid platforms that lack direct predicate devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heart Valve Repair Devices Anchor Volume, LAAC Devices Define the Growth Frontier

Heart Valve Repair Devices held 36.31% of the cardiovascular repair and reconstruction devices market share in 2025, which made them the largest product category in the cardiovascular repair and reconstruction devices market. This position reflects strong procedure volumes across aortic stenosis, mitral regurgitation, and the developing tricuspid disease space. Edwards Lifesciences reported 97.9% freedom from structural valve deterioration and 97.8% freedom from reoperation due to structural valve deterioration at 10 years in the COMMENCE aortic trial for its RESILIA tissue bioprosthesis, which supports longer lifetime valve strategies and broader use in younger surgical patients. Left Atrial Appendage Closure Devices are the fastest-growing product type at 7.38% CAGR through 2031, supported by evidence that LAAC can act as a mechanical alternative to long-term anticoagulation in atrial fibrillation patients with high bleeding risk.

The OPTION trial published in 2024 showed LAAC was noninferior to oral anticoagulation after catheter ablation over 36 months and also delivered a lower rate of non-procedural major bleeding[3]Vivek Reddy Dukkipati, “Left Atrial Appendage Closure after Ablation for Atrial Fibrillation,” New England Journal of Medicine, nejm.org. Product innovation in LAAC is also accelerating, with Abbott reporting positive early VERITAS study results for Amulet 360 in February 2026 while Boston Scientific’s WATCHMAN Elite IDE trial is expected to begin enrolling in 2026. This competitive build-out is likely to lift procedure volumes and place more pressure on pricing over time. Vascular Grafts, Cardiovascular Patches, and Annuloplasty Systems continue to serve complementary anatomical needs, and vascular grafts are drawing more attention as bioabsorbable conduit platforms move through EU pivotal development.

By Material: Biological Tissue Leads on Precedent, Bioabsorbable Hybrid Materials Redefine Implant Longevity

Biological Tissue captured 33.24% share in 2025, which kept it as the leading material base in the cardiovascular repair and reconstruction devices market. Its lead rests on long clinical use across surgical valve bioprostheses, pericardial patches, and tissue-engineered vascular constructs. The RESILIA bovine pericardial tissue platform has now shown 97.9% freedom from structural valve deterioration at 10 years, which sets a high durability threshold for competing biological formulations. Bioabsorbable and Hybrid Materials represent the fastest-growing material category, and this cardiovascular repair and reconstruction devices market size for the segment is projected to expand at 8.52% CAGR through 2031 because clinicians are showing stronger interest in implants that support native tissue regeneration before resorption.

Xeltis reported 12-month pivotal data for its aXess restorative vascular access conduit in 2026, showing 79% secondary patency and 60% fewer reinterventions than conventional ePTFE arteriovenous grafts. Preclinical and early clinical work on Xeltis’ Xabg restorative coronary bypass conduit also points to future use in small-diameter bypass settings where no approved off-the-shelf option exists today. Synthetic Polymers and Metals and Alloys still remain essential in defined settings, with ePTFE and polyester serving peripheral bypass needs and nitinol or cobalt-chromium supporting self-expanding delivery frames. The shift toward hybrid and bioresorbable material systems is also visible in coronary scaffold research, where a PLLA and PLGA blend showed improved vessel healing versus conventional PLA platforms.

By Application: Heart Valve Disease Sustains Revenue Share, Structural Heart Disease Captures Incremental Volume

Heart Valve Disease accounted for 38.52% share in 2025, which kept it as the largest application area within the cardiovascular repair and reconstruction devices market. Aortic stenosis continues to generate the highest procedure volume, and TAVI has become the standard of care in Germany for patients aged 75 and older regardless of surgical risk. Tricuspid disease remains an underrecognized part of this application base, and Edwards received FDA approval in May 2026 for the Triformis Resilia valve, the first surgical valve designed specifically for tricuspid anatomy. Structural Heart Disease is the fastest-growing application at 7.25% CAGR through 2031 as more congenital, hypertrophic, mitral, and tricuspid conditions move toward catheter-based correction.

Abbott’s Tri.Fr trial data presented in 2026 showed that TriClip reduced heart failure hospitalization risk by 48% and major cardiovascular events by 44% versus medical therapy, which adds strong support for tricuspid transcatheter edge-to-edge repair. Coronary Artery Disease is also gaining from better vascular graft science, with Xeltis’ restorative bypass conduit in EU clinical investigation and 24-month follow-up showing maintained graft patency and strong flow in patients who need alternatives to vein harvesting. Peripheral Vascular Repair completes the application mix, and the Omniflow II biosynthetic prosthesis showed promising mid-term patency and low graft infection rates in a 2026 multicenter observational study in chronic limb-threatening ischemia patients. Better CT-based planning and imaging integration are especially useful in structural heart cases because they lower sizing errors and reduce intraoperative complications.

By End User: Hospitals Anchor Procedure Volume, Cardiac Catheterization Laboratories Capture the Growth Premium

Hospitals held 45.52% share in 2025, which kept them at the center of the cardiovascular repair and reconstruction devices market because complex open surgery, hybrid room use, and intensive monitoring still concentrate there. This lead is supported by a continued need for high-acuity care in aortic arch repair, multivalve surgery, and congenital heart reconstruction. Medtronic stated in 2026 that around 20,000 surgical mitral valve replacements take place annually in the United States, and that volume is likely to remain mostly hospital-based during the forecast period because of patient complexity and access requirements. Cardiac Catheterization Laboratories are the fastest-growing end-user segment at 8.25% CAGR through 2031 as more structural heart procedures move into catheter-based treatment pathways.

The cardiovascular repair and reconstruction devices market is also seeing a gradual migration of selected interventions toward outpatient and ambulatory settings, especially where same-day discharge is becoming more realistic. Imaging improvements, lower anesthesia needs, and stronger procedural safety are making cath labs better suited to absorb lower-complexity structural cases. At the same time, capital equipment costs and state-level certificate-of-need rules are likely to slow the pace of migration in some markets. The direction still favors cath labs and ambulatory expansion because payer policy, physician preference, and procedural evidence are increasingly aligned behind less intensive sites of care.

Geography Analysis

North America accounted for 38.22% share of the cardiovascular repair and reconstruction devices market size in 2025, making it the leading regional block in the cardiovascular repair and reconstruction devices market. The United States anchors this position because it performs more than half of all TAVR implants globally and continues to post strong growth in transcatheter repair volumes. The region also remains the first launch market for major platforms, with Abbott’s Tendyne TMVR approved in May 2025 and Edwards’ SAPIEN M3 mitral replacement system approved in December 2025 in the United States. Europe holds the second-largest position, and Germany performs the highest TAVI volumes on the continent. Under EU MDR, and with joint clinical assessments starting in 2026, commercialization timelines for novel structural implants are lengthening compared with the earlier framework, which is a larger burden for smaller innovators.

Asia-Pacific is the fastest-growing region at 7.65% CAGR over 2026-2031, and the cardiovascular repair and reconstruction devices market there is gaining from rising structural disease incidence, broader interventional infrastructure, and approvals for newer device classes. South Korea and Australia serve as important adoption anchors because both have established interventional cardiology networks and reimbursement structures that support technology uptake. India is also gaining procedural momentum as newer TAVR delivery systems reach local centers and broaden physician familiarity with advanced valve therapy. The regional opportunity remains large because procedure penetration still trails the underlying disease base in many Asia-Pacific countries.

South America and the Middle East and Africa contribute smaller shares to the cardiovascular repair and reconstruction devices market, but both regions offer meaningful long-term room for expansion. Brazil leads South American demand through its concentration of cardiac surgery hospitals and established TAVI programs. Argentina adds procedure volume through its private healthcare system, especially for higher-complexity structural interventions. In the Middle East, GCC countries are expanding catheterization capacity to reduce outbound medical travel, and UAE programs are handling more cases and greater complexity. South Africa remains the anchor in sub-Saharan Africa because it records the highest structural heart procedural volumes on the continent. Device pricing remains a barrier in both regions, which keeps adoption tied to hybrid procurement models and slows growth relative to Asia-Pacific or North America. Manufacturers are therefore leaning more on tiered portfolios and health-economics arguments to gain formulary access in constrained purchasing environments.

Competitive Landscape

The cardiovascular repair and reconstruction devices market remains moderately consolidated at the platform level, with Abbott, Edwards Lifesciences, and Medtronic holding the broadest overlap across aortic, mitral, and tricuspid repair and replacement. Specialized players still matter in defined niches, including Artivion in aortic arch repair, W. L. Gore and LeMaitre Vascular in peripheral vascular products, and Getinge and Terumo in coronary vascular surgery support. Edwards has strengthened its position through long-duration evidence, with 10-year COMMENCE trial data showing 97.9% freedom from structural valve deterioration for RESILIA tissue. That type of durability data helps create evidence-based differentiation and supports its role in lifetime valve management planning. The cardiovascular repair and reconstruction devices market therefore shows concentration in core transcatheter platforms, while still leaving room for focused players in anatomy-specific categories.

Strategic moves in 2025 and 2026 show that the cardiovascular repair and reconstruction devices market is still being reshaped through platform expansion rather than simple line extension. Artivion completed its acquisition of Endospan in May 2026 after FDA PMA approval for the NEXUS Aortic Arch System, which gave the company a broader aortic arch platform spanning AMDS, NEXUS, and Arcevo LSA. Boston Scientific announced a USD 1.5 billion strategic investment in MiRus LLC in May 2026, with an option tied to the Siegel TAVR platform, which shows how valuable scale remains in TAVR for reimbursement, evidence generation, and global distribution. These moves indicate that leading companies are still buying or backing platforms that can strengthen their position in structural heart therapy rather than relying only on incremental upgrades.

White-space opportunities in the cardiovascular repair and reconstruction devices market remain strongest in dedicated tricuspid systems, bioabsorbable small-diameter coronary conduits, and next-generation LAAC differentiation. Philips is also shaping competition indirectly through enabling tools, since DeviceGuide AI and 3D ICE can lower procedural complexity and support broader site-of-care migration. W. L. Gore received CE Mark approval in June 2026 for the GORE VIABAHN FORTEGRA Venous Stent, which shows how specialized graft players continue to defend targeted procedural niches with anatomy-specific designs. Competitive pressure is therefore likely to remain strongest where clinical evidence, procedural usability, and reimbursement readiness come together in the same platform. Smaller innovators can still build value, but their advantage is more likely to come from solving narrow unmet needs than from challenging the broad platform leaders across the full cardiovascular repair and reconstruction devices market.

Cardiovascular Repair and Reconstruction Devices Industry Leaders

Medtronic plc

Edwards Lifesciences Corporation

Abbott Laboratories

Terumo Corporation

Getinge AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: W. L. Gore & Associates has achieved CE Mark approval for its GORE VIABAHN FORTEGRA Venous Stent, following its recent US FDA approval. This stent is designed to treat symptomatic IVC and iliofemoral venous outflow obstructions. Featuring a self-expanding nitinol frame and a polymer lattice, it offers flexibility and durability to reduce the risk of fractures.

- June 2026: Edwards Lifesciences has received FDA approval for its Triformis Resilia surgical valve, marking a significant milestone as the first surgical replacement valve specifically designed for the tricuspid position. Using advanced RESILIA tissue technology, the valve earned approval based on strong preclinical performance data. It is set to launch commercially in the United States in the second half of 2026, addressing the needs of patients who have traditionally relied on off-label mitral prostheses.

Global Cardiovascular Repair and Reconstruction Devices Market Report Scope

As per the scope of the report, cardiovascular repair and reconstruction devices are medical devices designed to diagnose, treat, repair, or reconstruct parts of the cardiovascular system. This includes devices used in procedures to repair or replace damaged blood vessels, heart valves, or other cardiovascular structures.

The segmentation of the cardiovascular repair and reconstruction devices market is categorized by product type, material, application, end user, and geography. By product type, the market includes cardiovascular repair devices, heart valve repair devices, vascular grafts, cardiovascular patches, annuloplasty systems, and left atrial appendage closure devices. By material, it is segmented into biological tissue, synthetic polymers, metals and alloys, and bioabsorbable and hybrid materials. By application, the market covers coronary artery disease, heart valve disease, peripheral vascular repair, and structural heart disease. By end user, the segmentation includes hospitals, cardiac catheterization laboratories, ambulatory surgical centers, and specialty cardiac centers. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Cardiovascular Repair Devices |

| Heart Valve Repair Devices |

| Vascular Grafts |

| Cardiovascular Patches |

| Annuloplasty Systems |

| Left Atrial Appendage Closure Devices |

| Biological Tissue |

| Synthetic Polymers |

| Metals and Alloys |

| Bioabsorbable and Hybrid Materials |

| Coronary Artery Disease |

| Heart Valve Disease |

| Peripheral Vascular Repair |

| Structural Heart Disease |

| Hospitals |

| Cardiac Catheterization Laboratories |

| Ambulatory Surgical Centers |

| Specialty Cardiac Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Cardiovascular Repair Devices | |

| Heart Valve Repair Devices | ||

| Vascular Grafts | ||

| Cardiovascular Patches | ||

| Annuloplasty Systems | ||

| Left Atrial Appendage Closure Devices | ||

| By Material | Biological Tissue | |

| Synthetic Polymers | ||

| Metals and Alloys | ||

| Bioabsorbable and Hybrid Materials | ||

| By Application | Coronary Artery Disease | |

| Heart Valve Disease | ||

| Peripheral Vascular Repair | ||

| Structural Heart Disease | ||

| By End User | Hospitals | |

| Cardiac Catheterization Laboratories | ||

| Ambulatory Surgical Centers | ||

| Specialty Cardiac Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for cardiovascular repair and reconstruction devices?

The cardiovascular repair and reconstruction devices market is forecast to reach USD 7.51 billion by 2031 from USD 5.37 billion in 2026, with a 6.92% CAGR over 2026-2031.

Which product category currently leads revenue generation?

Heart Valve Repair Devices led product revenue with a 36.31% share in 2025, supported by high volumes in aortic, mitral, and tricuspid procedures.

Which product area is expanding the fastest through 2031?

Left Atrial Appendage Closure Devices are projected to grow at a 7.38% CAGR through 2031, helped by trial evidence that supports LAAC as an alternative to long-term anticoagulation in selected atrial fibrillation patients.

Why is Asia-Pacific drawing so much attention in this space?

Asia-Pacific is the fastest-growing region at a 7.65% CAGR through 2031 because structural disease incidence is rising and interventional infrastructure is improving across the region.

Why do hospitals still dominate procedure volumes?

Hospitals held 45.52% share in 2025 because they remain the main sites for complex open surgery, hybrid room use, and high-acuity follow-up care.

What are the main limits on faster adoption?

The main limits are high device and facility costs, long Class III approval pathways, reimbursement friction for newer structural therapies, and the need for longer durability evidence before novel materials scale broadly.

Page last updated on: