Cardiac Prosthetic Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.2 Billion |

| Market Size (2031) | USD 13.73 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

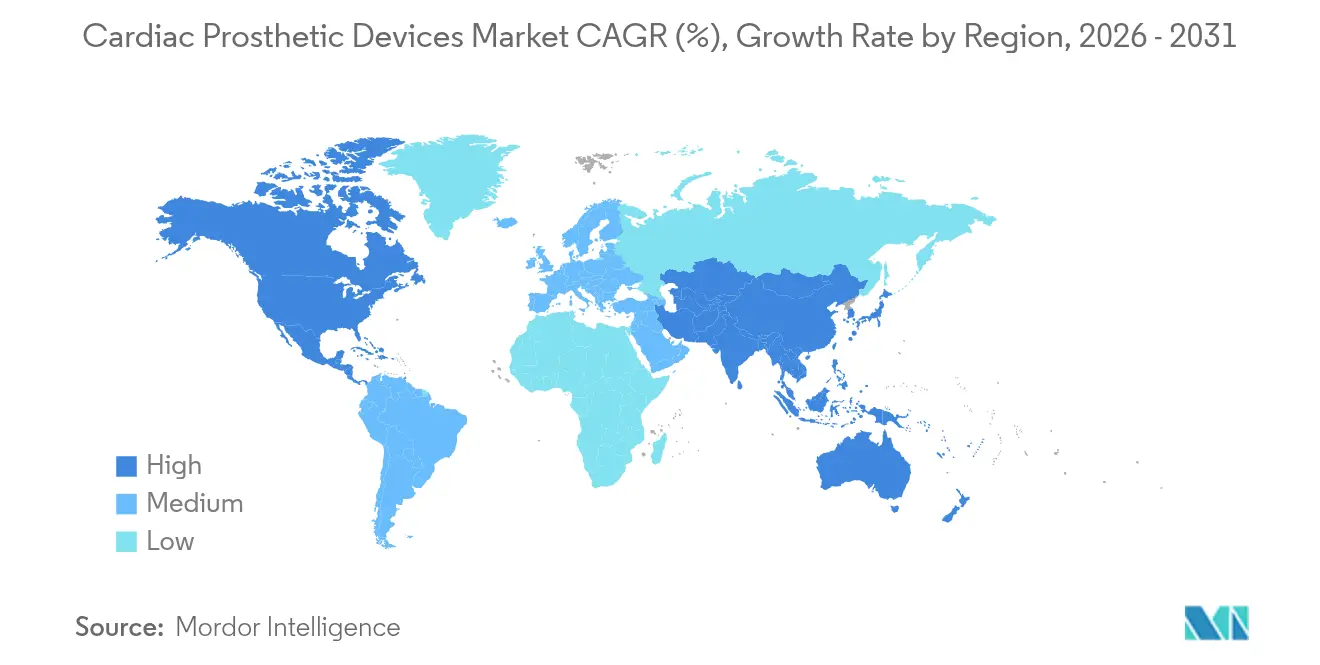

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

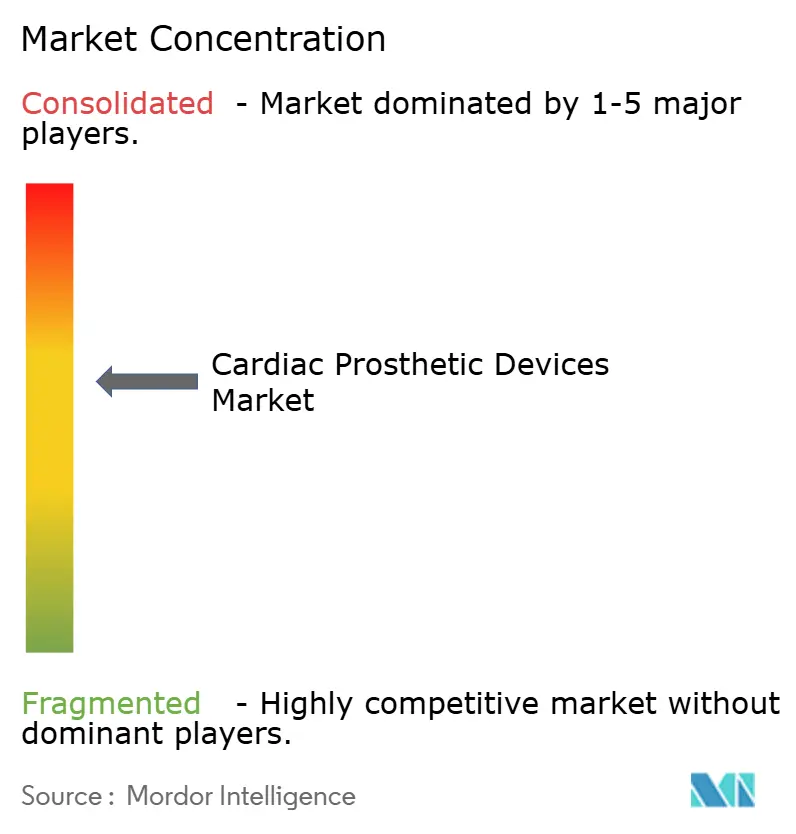

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cardiac Prosthetic Devices Market Analysis by Mordor Intelligence

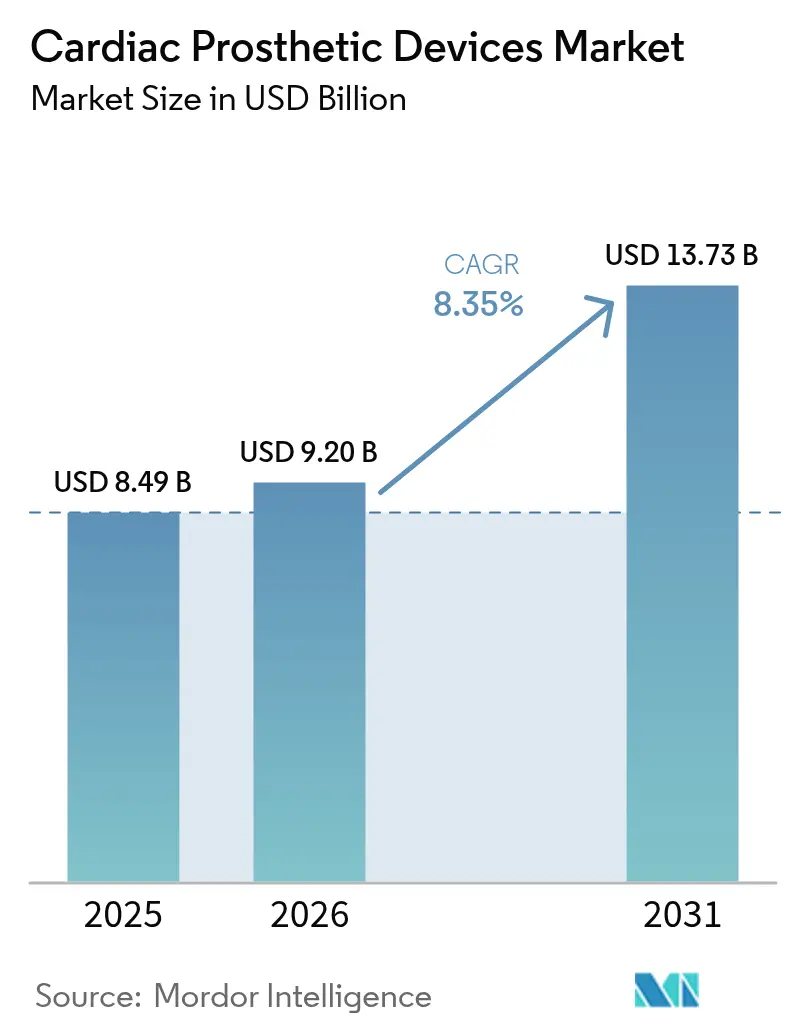

The cardiac prosthetic devices market size was valued at USD 8.49 billion in 2025 and estimated to grow from USD 9.2 billion in 2026 to reach USD 13.73 billion by 2031, at a CAGR of 8.35% during the forecast period (2026-2031). Rising life expectancy, expanding indications for transcatheter procedures, and continuous device miniaturization collectively underpin this steady advance. Manufacturers are capitalizing on the rapid uptake of catheter-based aortic and mitral valve replacements, which enable treatment of elderly or high-risk patients who previously lacked surgical options [1]Edwards Lifesciences, "Edwards’ EVOQUE Valve Replacement System First Transcatheter Therapy to Earn FDA Approval for Tricuspid Valve," edwards.com. At the same time, remote monitoring software embedded in next-generation pacemakers is unlocking subscription-type revenues for device makers while reducing follow-up burdens on cardiology clinics. Competitive pressure is intensifying around pulsed-field ablation platforms that promise shorter treatment times and fewer complications, forcing incumbents to accelerate R&D road-maps. Finally, hospitals and ambulatory centers alike are benefiting from payer support for same-day discharge, a policy trend that amplifies procedure volumes without proportionally raising facility overheads.

Key Report Takeaways

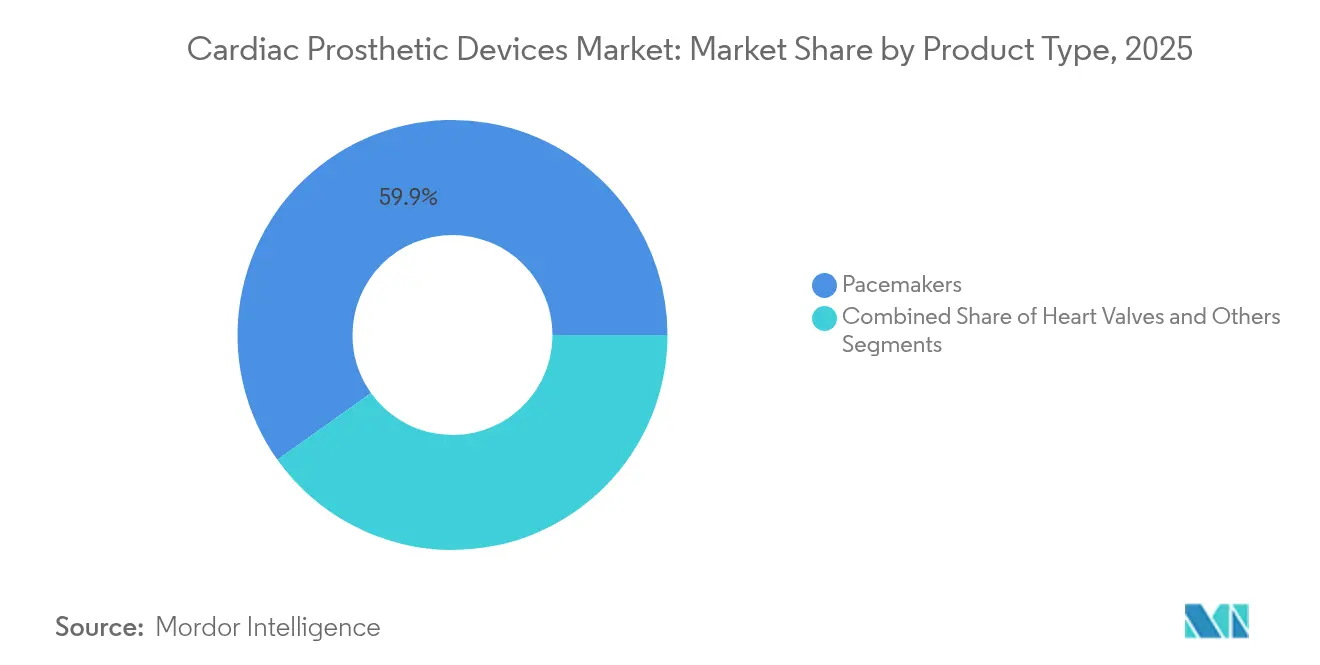

- By product type, pacemakers led the cardiac prosthetic devices market share with 59.85% in 2025, whereas heart valves are projected to post the fastest 9.12% CAGR through 2031.

- By material, metal alloys accounted for 57.12% of the cardiac prosthetic devices market size in 2025, while biological tissue is set to advance at a 9.27% CAGR to 2031.

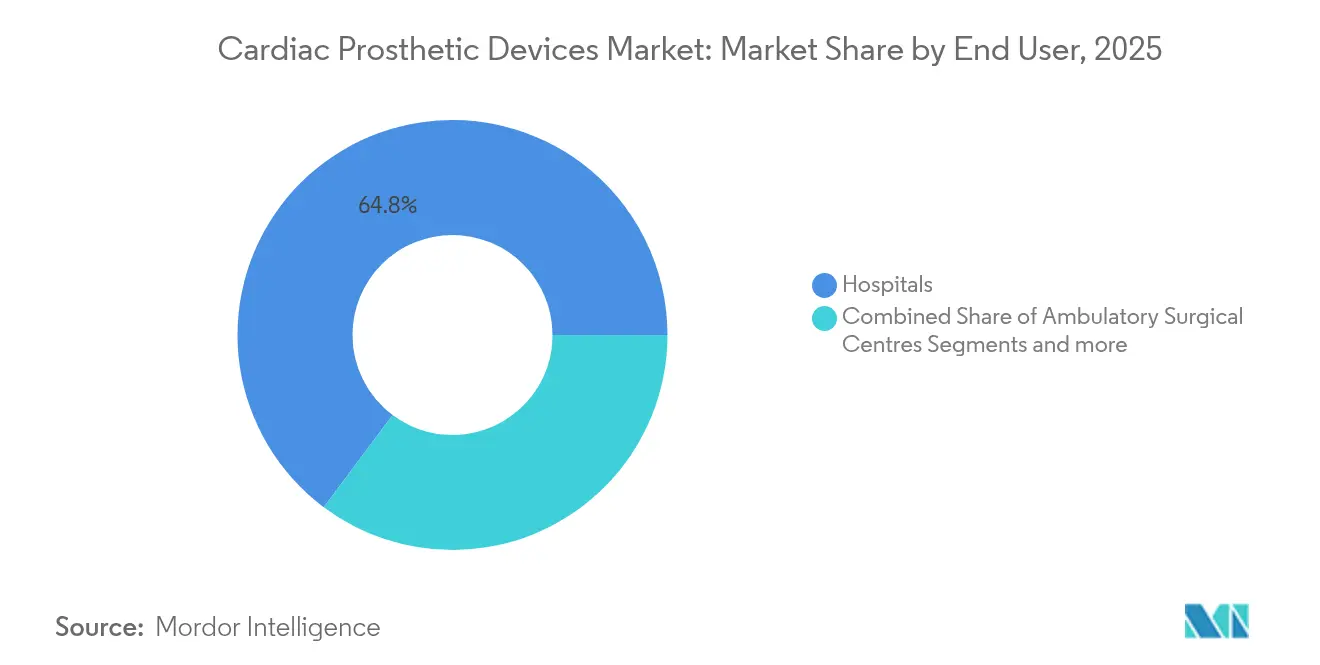

- By end user, hospitals handled 64.78% of total implant volume in 2025; ambulatory surgical centers are expected to record the highest 9.18% CAGR over the forecast horizon.

- By geography, North America captured 40.92% revenue share in 2025, whereas Asia-Pacific is on track for a 9.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Prosthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in prevalence of cardiac diseases & ageing population | +1.8% | Global, most acute in North America & Europe | Long term (≥ 4 years) |

| Rapid adoption of minimally-invasive TAVR procedures | +2.1% | North America & EU lead, Asia-Pacific follows | Medium term (2-4 years) |

| Continuous technology upgrades in leadless & MRI-safe pacemakers | +1.2% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Favourable reimbursement pathways in US, EU & Japan | +0.9% | North America, Europe, Japan | Short term (≤ 2 years) |

| AI-driven remote programming & monitoring of pacemakers | +1.1% | North America & EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Polymeric RESILIA-like valves extending durability beyond 25 years | +0.7% | Premium global segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in prevalence of cardiac diseases & ageing population

Cardiovascular disease incidence climbs steeply after age 65, and the share of citizens in that age bracket now exceeds 17% in the United States, 21% in Japan and 20% across Western Europe. Higher life expectancy therefore enlarges the pool of patients living long enough to develop severe aortic stenosis, atrial fibrillation or heart failure that necessitate implant therapy. Longer survivorship also raises clinical expectations for device longevity, which pushes vendors to engineer valves that can last decades without re-operation. Geriatric patients tend to favor minimally-invasive therapies that shorten hospital stays, reinforcing demand for transcatheter solutions. Together these demographic forces are expanding procedure volumes as well as unit prices, supporting sustained revenue growth for the cardiac prosthetic devices market.

Rapid adoption of minimally-invasive TAVR procedures

Rapid adoption of minimally-invasive TAVR proceduresTranscatheter aortic valve replacement (TAVR) has shifted from a high-risk niche therapy to a mainstream option endorsed for low-risk patients after robust five-year data confirmed comparable survival versus open surgery. Hospitals gain operational efficiencies because typical length of stay falls below two days, freeing capacity in crowded cardiac wards. Valve-in-valve techniques further widen the addressable pool by treating degenerated bioprostheses without sternotomy, a capability especially valued by elderly patients. Next-generation platforms now feature enlarged commissural alignment and easier coronary access, ensuring future percutaneous coronary interventions remain feasible. As payer policies increasingly reimburse TAVR outside tertiary centers, procedure counts accelerate, amplifying the positive impact on the cardiac prosthetic devices market CAGR.

Continuous technology upgrades in leadless & MRI-safe pacemakers

Traditional transvenous leads are implicated in nearly 55% of long-term pacemaker complications, including fracture, infection and venous occlusion. Leadless systems eliminate these risks by positioning the pulse generator directly inside the ventricle and anchoring via nitinol tines. Dual-chamber variants, now commercially available in Europe, replicate physiologic pacing while preserving the cosmetic and infection advantages of their single-chamber predecessors. MRI-conditional designs allow full-body scans at 1.5 T and 3 T fields, a feature increasingly critical because over 70% of cardiac device patients will need magnetic resonance imaging within their lifetime. Collectively, these iterative upgrades refresh the mature pacemaker segment and sustain premium price points within the cardiac prosthetic devices market.

Favourable reimbursement pathways in US, EU & Japan

Medicare expanded coverage of TAVR to low-surgical-risk patients in 2024, instantly enlarging the billable population by an estimated 30%. Parallel decisions by the German G-BA and the French HAS confirmed public payment for transcatheter mitral and tricuspid valves that meet strict clinical-evidence thresholds. In Japan, the Ministry of Health, Labour and Welfare provides separate reimbursement for AI-enabled pacemaker remote monitoring services, thereby transforming what was once a cost center for hospitals into an attractive revenue stream. These policy endorsements compress adoption curves for innovative implants, reinforcing topline growth across every major regional slice of the cardiac prosthetic devices market.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region regulatory approvals | –0.8% | Global, acute in EU under MDR | Medium term (2-4 years) |

| High procedure & device cost, limited access in LMICs | –1.2% | Primarily LMICs, knock-on effects in emerging markets | Long term (≥ 4 years) |

| Dependency on bovine & porcine tissue supply chains | –0.6% | Global, concentrated among biological valve makers | Short term (≤ 2 years) |

| Catheter-based ablation therapies delaying implant need | –0.4% | North America & EU, gradual Asia-Pacific uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent multi-region regulatory approvals

The European Medical Device Regulation (MDR) enforces clinical-evidence requirements that roughly triple the documentation burden relative to the former CE-mark process, adding 18-24 months to typical approval timelines and inflating pre-market costs by USD 12 million per high-risk device according to company filings [2]Bijaya Chettri, "A comparative study of medical device regulation between countries based on their economies," Expert Review of Medical Devices, tandfonline.com. Simultaneously, the U.S. FDA’s requirement for long-term post-approval studies places ongoing resource demands on manufacturers. Smaller innovators struggle to finance these obligations, leading several to out-license promising technologies or exit the field entirely. Multinational players can absorb the expense, but the longer path to revenue delays return on R&D spending, marginally dampening the CAGR of the cardiac prosthetic devices market during the forecast window.

High procedure & device cost, limited access in LMICs

A TAVR implantation package, including diagnostics, valve, delivery catheter and hospitalization, typically exceeds USD 40,000 in the United States, a figure beyond the reach of many healthcare systems in low- and middle-income countries. Even where public insurance exists, co-payments can equal several months of household income, forcing patients to defer treatment until symptom escalation mandates emergency care. Hospitals in these regions also face capital constraints that limit acquisition of hybrid operating rooms and advanced imaging modalities needed to run transcatheter programs efficiently. Consequently, penetration rates remain low in populous territories such as India, Nigeria and Indonesia, capping the global revenue potential of the cardiac prosthetic devices market despite its compelling clinical value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heart Valves Drive Premium Growth

Heart valves contributed 9.12% CAGR through 2031, outpacing every other category even though pacemakers retained a 59.85% cardiac prosthetic devices market share in 2025. TAVR, TMVR and emerging transcatheter tricuspid systems have expanded the treatable patient pool while commanding high average selling prices that lift overall revenue. Hospitals prize the rapid recovery dynamics of these implants, and patients value the avoidance of sternotomy, fueling sustained double-digit annual procedure growth. Pacemaker sales remain resilient due to the sheer size of the bradyarrhythmia population, yet their mature status and pricing compression restrain segment expansion. The others segment, including ventricular assist devices, continues to receive breakthrough-device designations, suggesting a long-term upswing that could diversify revenue beyond the core rhythm-management base, but near-term contribution remains modest.

Second-generation tissue valves integrating anti-calcification chemistry now capture share from mechanical valves, especially in patients aged 50-65 who prefer to avoid lifelong anticoagulation. Simultaneously, leadless pacemakers with AI-enabled analytics are carving a premium sub-segment even within a plateauing category. The combined effect is a gradual tilt of the product mix toward higher-margin, technology-rich solutions that sustain the broader cardiac prosthetic devices market growth trajectory.

By Material: Biological Tissue Innovation Accelerates

Biological tissue recorded a 9.27% CAGR, eclipsing the growth of metal alloys that still represent 57.12% of 2025 revenue. The shift is linked to improved leaflet preservation processes that extend implant life and broaden clinical eligibility down to younger patients. Polymeric-hybrid valves under development may further accelerate biologic displacement by delivering both durability and hemodynamic excellence. However, pacemaker generators and ICD cans will continue to rely on titanium alloys because of their superior corrosion resistance and electromagnetic shielding, ensuring metals retain a large absolute share of the cardiac prosthetic devices market size. Advanced surface coatings that reduce biofilm formation could bolster the competitiveness of metallic implants, but the primary growth spotlight will stay on biologic innovations.

Metal component suppliers face margin pressure as competition from lower-cost contract manufacturers in Southeast Asia intensifies. To differentiate, leading firms are integrating additive-manufacturing techniques that shorten development cycles for complex delivery-system parts. Composite materials are gaining traction in delivery catheters where stiffness and flexibility must coexist, illustrating that material-science progress is permeating every corner of the cardiac prosthetic devices market .

By End User: ASCs Capture Procedural Migration

Ambulatory surgical centers (ASCs) registered the fastest 9.18% CAGR, riding policy waves that reimburse same-day TAVR and leadless pacemaker procedures outside traditional hospital walls. Purpose-built catheter suites foster high throughput with lean staffing, allowing ASCs to price competitively while maintaining attractive margins. Hospitals still command 64.78% of volume because they manage complex multi-valve cases, emergent situations and patients with significant co-morbidities. Nevertheless, administrators are redesigning inpatient programs to emulate ASC efficiency, creating a blended care continuum that shares clinical protocols and data platforms. Specialty clinics focusing on heart-rhythm disorders or valve disease are also proliferating and act as referral hubs that funnel well-optimized candidates into ASC pipelines, further amplifying outpatient growth momentum.

The procedural migration exerts design pressure on device makers to simplify deployment and shorten learning curves. Companies that embed step-by-step imaging guidance into delivery handles or integrate hemostatic sealing into introducer sheaths gain a competitive edge in resource-constrained ASC environments. Over time, the outpatient shift is expected to redistribute capital-equipment spending toward compact fluoroscopy units and cloud-connected monitoring stations, extending ripple effects beyond the core implant devices within the cardiac prosthetic devices market.

Geography Analysis

North America leads global revenue, accounting for 40.92% in 2025 as Medicare broadened TAVR coverage to low-risk cohorts and approved ambulatory billing codes. The presence of vast clinical-trial networks facilitates first-in-human studies, often granting U.S. facilities 12-18-month lead time over international peers in new-technology adoption. Regulatory programs such as the FDA Breakthrough Device pathway shorten time-to-market for transformative platforms, further cementing the region’s leadership. Yet margin compression is inevitable as value-based purchasing agreements and bundled payments expand; leading manufacturers hedge by bundling digital services and extended warranties into pricing proposals to preserve ASPs.

Asia-Pacific is the fastest climber at 9.39% CAGR, supported by governmental push to modernize tertiary care and a burgeoning middle class able to self-pay for advanced interventions. Chinese Centers for Excellence grants subsidize the capital expenditure for hybrid operating suites, unlocking latent demand. Japan’s revised reimbursement schedule recognizes AI-driven remote monitoring codes, creating recurring revenue that stabilizes vendor cash flows. Although per-patient spend is lower than in North America, population scale compensates, and local manufacturing partnerships reduce import tariffs, improving affordability.

Europe demonstrates steady mid-single-digit expansion as universal-payer models shield procedure volumes from economic volatility. Germany’s DRG system rewards shorter length of stay, directly benefiting transcatheter approaches. The MDR imposes up-front costs but enhances patient confidence in device safety, indirectly supporting adoption. Meanwhile, the United Kingdom’s Medicines & Healthcare products Regulatory Agency is piloting an expedited review for implantables post-Brexit, offering an alternate fast-track to market for companies willing to invest in localized evidence generation. Collectively, these regional dynamics shape a balanced growth mosaic that underpins the upward trajectory of the cardiac prosthetic devices market.

Regulatory Landscape

EU MDR 2017/745 remains the governing framework for implantable cardiovascular devices. In June 2026, the European Commission published Delegated Regulations (EU) 2026/1359 and 2026/1451, expanding the MDR Well-Established Technology list to include cardiovascular device categories such as catheters, guidewires, leads, and snares. This reduces the need for new premarket clinical investigations for eligible legacy technologies, while maintaining requirements for documented clinical evaluation.

US regulatory oversight continues to emphasize lifecycle evidence and design-control rigor for structural-heart systems. In March 2026, the FDA issued final guidance on incorporating voluntary patient preference information across the total product life cycle, formalizing how preference data can be used in benefit-risk evaluations. Separately, FDA PMA supplement activity indicates ongoing regulatory focus on controlled manufacturing changes for approved implant systems, including an April 2026 approval of a PMA supplement for process and cleanroom modifications related to Edwards Lifesciences SAPIEN M3. Alongside core regulatory pathways, trade-policy uncertainty emerged in 2026, as additional duty proposals under U.S. Section 301 were discussed for some imports, increasing cost-planning and sourcing complexity for globally integrated supply chains used in cardiac prosthetic components.

Competitive Landscape

The market is moderately concentrated: top five suppliers account for roughly 72% of global revenue, creating meaningful entry barriers yet leaving room for nimble innovators. Incumbents deploy full-line portfolios spanning valves, rhythm products and heart-failure solutions, enabling multiproduct contracts that lock in provider loyalty. Edwards Lifesciences deepens its moat with continuous valve-platform evolution, evidenced by the 2025 CE-mark approval of its SAPIEN M3 mitral system. Medtronic answers with the Evolut FX+ valve featuring oversized coronary access ports that appeal to interventional cardiologists planning future PCI procedures. Abbott and Boston Scientific continue to invest in leadless and battery-less pacing concepts, hoping to leapfrog competitors in miniaturization and longevity.

Meanwhile, Chinese players such as MicroPort are scaling aggressively at home and submitting dossiers to Western regulators, introducing price tension in tender markets. Strategic collaboration between western OEMs and contract manufacturers in Malaysia and Vietnam aims to sharpen cost positions without compromising quality. Start-ups specializing in polymeric valves or wirelessly powered CRT devices often seek licensing deals rather than solo commercialization, reinforcing incumbent dominance. The data-analytics layer is emerging as a new battleground, with proprietary algorithms delivering predictive alerts that differentiate devices beyond raw hardware metrics, tightening vendor lock-in across the cardiac prosthetic devices market.

Cardiac Prosthetic Devices Industry Leaders

-

Abbott Laboratories

-

LivaNova PLC

-

Medtronic plc

-

Boston Scientific Corporation

-

Edwards Lifesciences Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is concentrated in structural-heart indications where standard surgical options are limited, or where high-risk populations were historically undertreated, particularly across mitral, tricuspid, and aortic regurgitation therapies. In 2026, regulatory and clinical developments point to specific product spaces expanding: JenaValve Technology received FDA PMA for the Trilogy transcatheter heart valve system for symptomatic, severe aortic regurgitation in high-risk patients (March 2026), and the PULSTA CE-approval trial reported 98.2% freedom from reintervention at five years for a transcatheter pulmonary valve (June 2026).

Durability and tissue-design differentiation are also practical levers for share gains as centers prioritize longer-lasting performance. Clinical evidence for SAPIEN 3 Ultra RESILIA, citing improved hemodynamics, has supported premium positioning of advanced tissue and sealing designs in transcatheter valves (May 2026). At the same time, Edwards Lifesciences' Triformis Resilia surgical tricuspid valve replacement and related SAPIEN M3 manufacturing enhancements are expanding adoption across surgical and catheter-based pathways (June 2026, April 2026).

Recent Industry Developments

- June 2026: Edwards Lifesciences received FDA clearance for the Triformis Resilia surgical tricuspid valve replacement, advancing a dedicated tricuspid solution as a discrete product category. The clearance supports portfolio differentiation and reinforces lifetime management of right-sided valvular disease.

- April 2026: Edwards Lifesciences won FDA PMA supplement approval for process and cleanroom modifications related to the SAPIEN M3 system. The approval allows manufacturing flexibility to support broader clinical adoption of next-generation transcatheter valves.

- March 2026: JenaValve Technology secured FDA PMA for the Trilogy transcatheter heart valve system addressing symptomatic severe aortic regurgitation in high-risk patients. The approval expands transcatheter options for complex valvular disease and increases competitive pressure in the aortic regurgitation space.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cardiac prosthetic devices market is defined as the revenue generated from implantable devices and prostheses used to replace, repair, or provide long-term support to cardiac structures and rhythm, and then used in clinical care across major regions.

Scope exclusions: We exclude procedure fees, physician services, standalone imaging systems, and routine consumables that are not integral to the implanted prosthetic device.

Segmentation Overview

-

By Product Type

-

Heart Valves

- Mechanical Valves

- Tissue Valves

- Transcatheter Valves

-

Pacemakers

- Leaded

- Leadless

- Others

-

Heart Valves

-

By Material

- Metal Alloys

- Biological Tissue

- Polymeric and Hybrid

-

By End User

- Hospitals

- Specilaty Clinics

- Ambulatory Surgical Centres

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and utilization backdrop before the model was built. We relied on public health and regulatory signals, such as CDC cardiovascular disease statistics, WHO mortality datasets, and OECD health indicators, to understand diagnosis and treatment volumes by geography.

To anchor device adoption and technology direction, we reviewed sources such as FDA device databases and safety communications, plus CMS reimbursement and coding references, and peer-reviewed cardiology journals that track valve replacement trends and pacing practice. This desk list was supported with company filings, investor presentations, reputed press, and selective use of paid subscriptions for company financials and intelligence plus patent databases, which helped validate product pipeline timing. This desk list is illustrative only, and many other public and paid sources were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what the desk work could not fully show, especially the real-world mix shift between surgical and transcatheter valves and the pace of leadless pacing uptake. We spoke with a mix of manufacturers, distributors, hospital procurement teams, and clinicians across APAC, EMEA, and the Americas, then used follow-up questions to reconcile gaps in pricing ranges, replacement cycles, and short-term demand shocks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 32% |

| Smaller Players: 15% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

The sizing model starts with a top-down build where procedure volumes and treated patient pools are reconstructed by region, and then translated into device demand using adoption and replacement-rate assumptions. For cardiac prosthetic devices, the most important demand anchors were valve replacement and repair procedure counts (including transcatheter volumes), pacemaker implant volumes, and the split between first-time implants and replacements.

Next, the value layer was estimated using average selling price (ASP) bands that reflect mix shifts across device types and settings, rather than relying on one blended price. Inputs that were checked and refreshed include the transcatheter share progression, leadless pacing penetration, aging population growth, diagnosis and referral patterns for structural heart disease, and reimbursement stability that influences hospital purchasing cycles. To keep totals realistic, we corroborated results with selective bottom-up approximations, including sampled ASP times volume checks from channel feedback and a limited supplier and geography roll-up, and then adjusted where gaps appeared.

For forecasting, scenario analysis was used so we could reflect different adoption curves for newer technologies and different procedure recovery paths after disruption years. Assumptions were finalized only after being stress-tested with primary feedback, and where bottom-up visibility was weak in smaller countries, we used proxy indicators such as procedure density per million population and hospital capacity markers to avoid overstating demand.

Data Validation & Update Cycle

Validation is done in layers so individual assumptions do not quietly distort the final number. We compare model outputs against independent signals such as procedure trend direction, import and device registration signals where available, and announced capacity or program expansions in major cardiac centers.

Variance checks are run across regions and across device families, and outliers are reviewed again before sign-off. If a key metric moves sharply, such as a reimbursement change or a major guideline update affecting valve or pacing use, the team triggers re-contacts and re-runs the most sensitive parts of the model. Reports are refreshed annually, and interim updates are made for material events, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Cardiac Prosthetic Devices Market Estimate Compared With Other Published Estimates

Published numbers for cardiac prosthetic devices do not always match because the market boundary is not treated the same way across studies, and because procedure and pricing assumptions can be updated at different times. In practice, the biggest differences come from what is counted as a cardiac prosthetic device, the year used for currency conversion, and how fast transcatheter adoption is assumed to ramp.

By tracking procedure volumes and refreshing mix and ASP assumptions, Mordor Intelligence keeps the total tied to valves and pacemakers as the core counted categories, while some estimates expand the definition to include more structural-heart accessories and related implant leads that lift the headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.49 B (2025) | |

| Industry Publisher A | USD 7.60 B (2025) | Uses a narrower value build with more conservative adoption and price bands for transcatheter valves and newer pacing formats, which reduces the near-term market capture. |

| Industry Publisher B | USD 9.78 B (2025) | Uses a wider product scope that includes additional structural-heart related implants (for example, certain rings, patches, and lead categories), which increases the counted revenue pool versus a valves-and-pacemakers anchored view. |

The spread in the table is mainly explained by scope edges and how quickly mix shifts are assumed to happen, rather than by a single data point. When definitions and pricing logic are made explicit, the resulting market size becomes easier to trace back to procedure volumes, device mix, and practical purchasing behavior, which helps decision-makers compare years consistently.

Key Questions Answered in the Report

How large is the cardiac prosthetic devices market in 2026?

The cardiac prosthetic devices market size reached USD 9.2 billion in 2026.

What is the expected growth rate for cardiac prosthetic implants to 2031?

Revenue is projected to rise at an 8.35% CAGR, taking the market to USD 13.73 billion by 2031.

Which product category leads in revenue?

Pacemakers held 59.85% of 2025 revenue, making them the largest cardiac prosthetic segment.

Which region is expanding fastest?

Asia-Pacific is forecast to post a 9.39% CAGR through 2031, the highest among all regions.

What driver most affects future demand?

The rapid shift toward catheter-based valve replacements adds 2.1% to the forecast CAGR.

How strong is competition among suppliers?

The top five companies control roughly 72% of revenue, giving the market a moderate concentration score of 7.

Page last updated on: