Hip Reconstruction Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

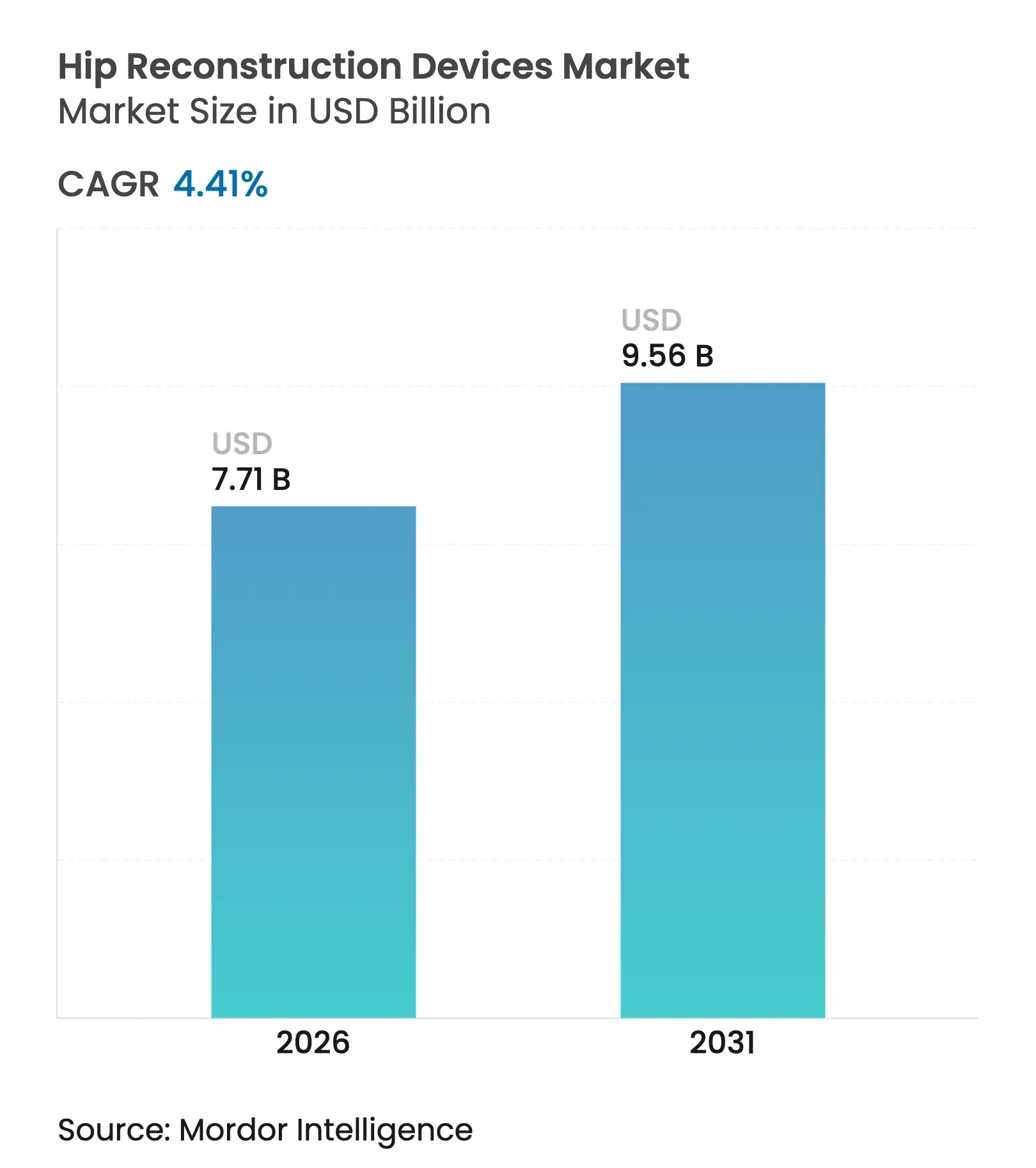

| Market Size (2026) | USD 7.71 Billion |

| Market Size (2031) | USD 9.56 Billion |

| Growth Rate (2026 - 2031) | 4.41 % CAGR |

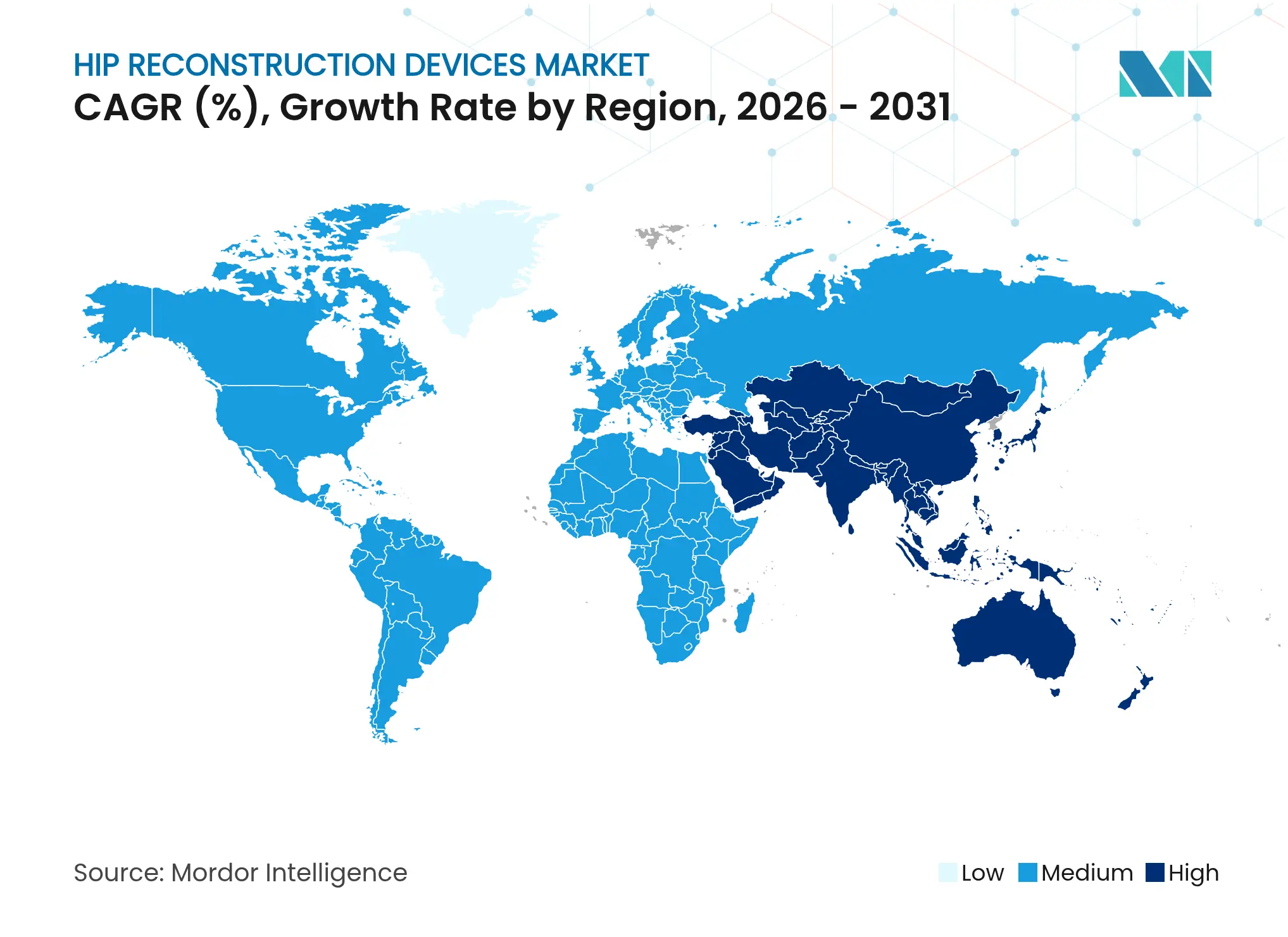

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

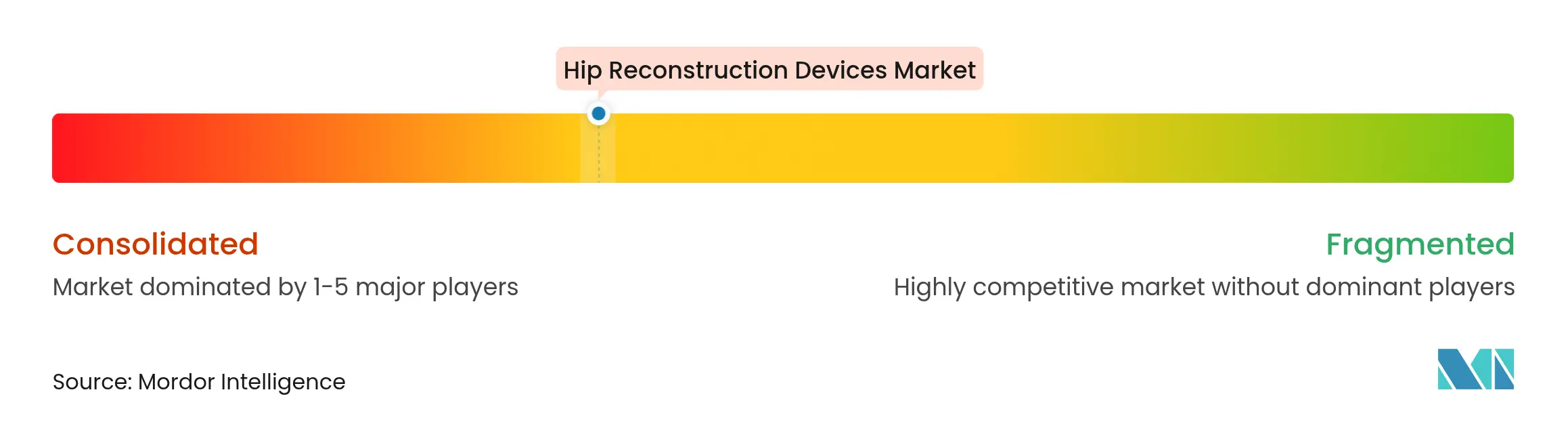

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hip Reconstruction Devices Market Analysis by Mordor Intelligence

Healthy procedure volumes, an aging population, and improved surgical eligibility from GLP-1 weight-loss therapy together lift demand, while cementless fixation and dual-mobility implants capture share through demonstrable outcome gains. Hospitals remain the dominant point of care, yet ambulatory surgical centers (ASCs) are scaling quickly as payers move complex orthopedic procedures to outpatient settings. North America preserves leadership on the back of high implant penetration and early robotic adoption, whereas Asia Pacific outpaces all regions as health-system investments and procurement reforms narrow affordability gaps. Moderate market concentration spurs a steady cadence of acquisitions, and digital surgery platforms create new competitive moats around data and workflow integration.

Key Report Takeaways

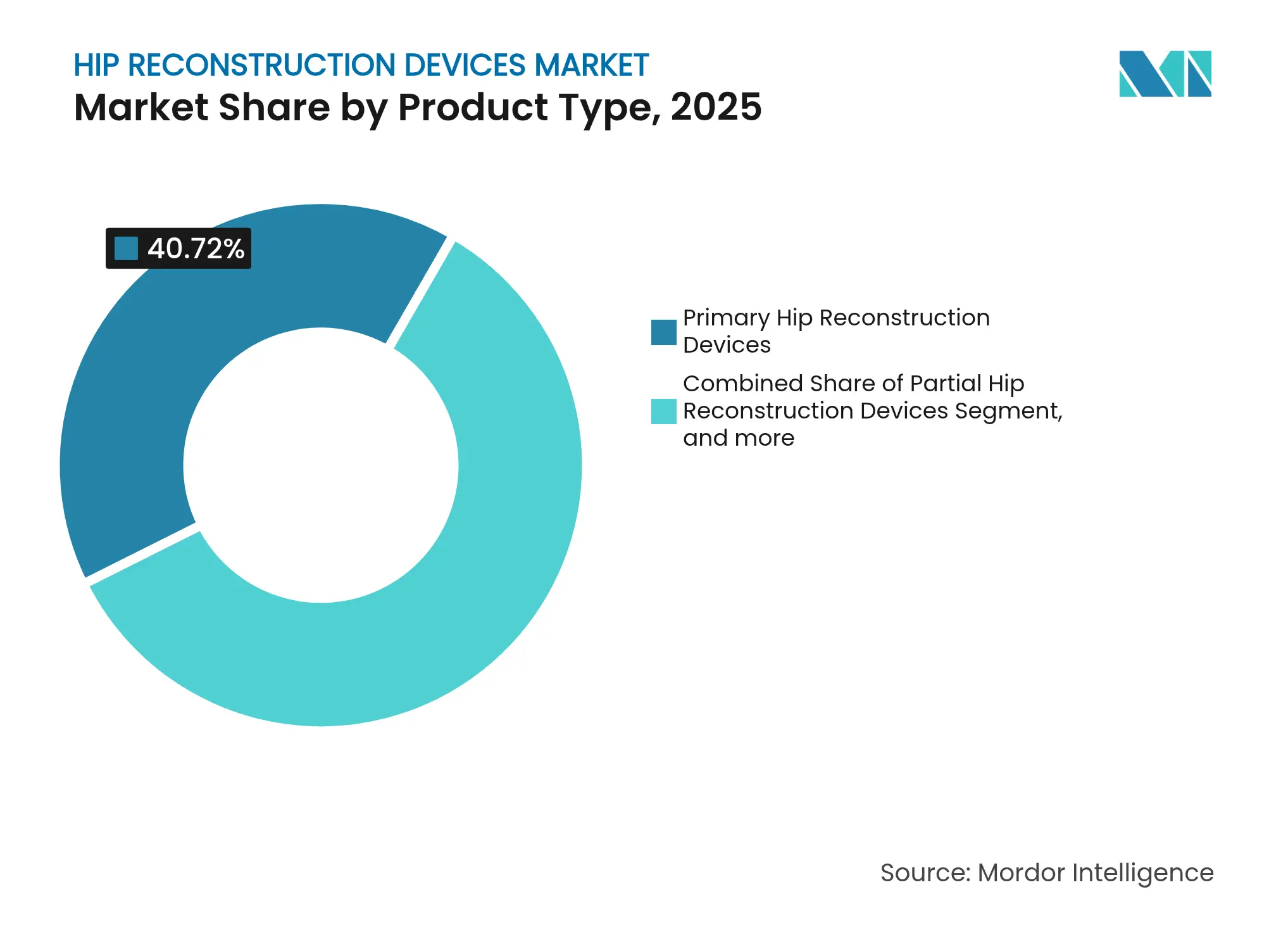

- By product type, primary hip devices held 40.72% of hip reconstruction devices market share in 2025, while dual-mobility systems are projected to expand at a 7.05% CAGR through 2031.

- By fixation technique, cementless solutions accounted for 52.68% of the Hip Reconstruction Devices market size in 2025 and are forecast to grow at a 6.32% CAGR to 2031.

- By end user, hospitals commanded 58.12% share of the hip reconstruction devices market in 2025, whereas ASCs record the fastest growth at 8.35% CAGR for 2026-2031.

- By geography, North America led with 43.25% revenue share in 2025; Asia Pacific is advancing at a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hip Reconstruction Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

Incidence of Hip Fractures & Osteoarthritis

Rising

Incidence of Hip Fractures & Osteoarthritis

| +1.4% | Global, with highest impact in aging populations of Europe, North America, and East Asia | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+1.4%

|

Geographic

Relevance

:

Global, with

highest impact in aging populations of Europe, North America, and East Asia

|

Impact

Timeline

:

Long term (≥

4 years)

|

Expanding

Geriatric Population

Expanding

Geriatric Population

| +0.8% | Global, particularly high-income regions with advanced healthcare systems | Long term (≥ 4 years) | |||

Rapid Uptake

of Minimally-Invasive & Robotic THA

Rapid Uptake

of Minimally-Invasive & Robotic THA

| +1.2% | North America & EU leading adoption, expanding to APAC | Medium term (2-4 years) | |||

Shift Toward

Outpatient & ASC Settings

Shift Toward

Outpatient & ASC Settings

| +0.9% | Primarily North America, with emerging adoption in Europe | Short term (≤ 2 years) | |||

AI-Driven

Surgical Planning & Patient-Specific Implants

AI-Driven

Surgical Planning & Patient-Specific Implants

| +0.7% | High-income markets with advanced digital infrastructure | Medium term (2-4 years) | |||

GLP-1-Induced

Obesity Decline Expanding Surgical Eligibility

GLP-1-Induced

Obesity Decline Expanding Surgical Eligibility

| +0.6% | North America & Europe where GLP-1 adoption is highest | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Hip Fractures & Osteoarthritis

Demographic aging intensifies the clinical burden: Asia alone is projected to record 6.3 million hip fractures and incur USD 130 billion in related costs by 2050.[1]Minh Ha Nguyen & Siew Kwaon Lui, “Holistic Management of Older Patients With Hip Fractures,” Orthopaedic Nursing, journals.lww.com/orthopaedicnursing The intersection of higher case complexity and better peri-operative optimization is elevating demand for both primary and revision Hip Reconstruction Devices market solutions. Advanced implants with dislocation-resistant designs and enhanced surface coatings increasingly suit patients with multiple comorbidities. Socio-economic development paradoxically elevates need as longer life expectancy exposes populations to degenerative musculoskeletal disease, reinforcing the Hip Reconstruction Devices market growth trajectory in both mature and emerging health systems.

Expanding Geriatric Population

Norway expects hip-fracture incidence to soar 91% in women and 131% in men by 2050 despite constant rates, highlighting the demographic swell facing affluent nations. Globally, nearly half of post-menopausal women are projected to suffer a musculoskeletal disorder by 2045, further widening the Hip Reconstruction Devices market’s addressable base. The baby-boomer cohort is entering peak joint-replacement age, a dynamic that simultaneously raises volumes and pushes device makers toward longer-lasting bearings. Revision procedures, already trending up, gain further momentum as earlier-generation implants reach end-of-life, driving uptake of modular and bespoke revision components. Health-system planners respond with expanded surgical capacity and geriatric-orthopedic protocols, fuelling sustained Hip Reconstruction Devices market demand over the long term.

Rapid Uptake of Minimally-Invasive & Robotic THA

Robotic-assisted total-hip arthroplasty (THA) delivers tighter acetabular-cup positioning, especially in obese patients, than manual approaches. More than 500,000 procedures have already been performed with the MAKO platform, underscoring fast clinical adoption. Nonetheless, elevated periprosthetic-fracture risk underlines a learning curve and the need for surgeon-training initiatives. As robotic workflows standardize and costs normalize, precision benefits resonate most with younger, physically active patients demanding extended implant survivorship, reinforcing premium-priced segments within the hip reconstruction devices market.

Shift Toward Outpatient & ASC Settings

CMS plans to fully retire the inpatient-only list for hip arthroplasty in 2026, paving the way for complex procedures in lower-acuity facilities and granting 2.4% payment hikes to compliant ASCs.[2]Centers for Medicare & Medicaid Services, “CY 2026 Hospital Outpatient Prospective Payment System Proposed Rule,” cms.gov Orthopedic cases in non-acute settings are on track to rise 13% this decade as payers rationalize episode-of-care costs. Device attributes now prioritize rapid ambulation, low blood loss, and streamlined instrumentation, fuelling innovation in cementless fixation and dual-mobility technology. ASCs, however, confront staffing constraints and stringent infection-control protocols, encouraging bundled-service models from implant vendors. The migration strengthens the Hip Reconstruction Devices market visibility in value-based-care negotiations, rewarding manufacturers that demonstrate day-of-surgery discharge safety and post-op resource efficiency.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

Procedure & Implant Costs

High

Procedure & Implant Costs

| -0.6% | Global, with highest impact in emerging markets and uninsured populations | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-0.6%

|

Geographic

Relevance

:

Global, with

highest impact in emerging markets and uninsured populations

|

Impact

Timeline

:

Long term (≥

4 years)

|

Stringent

EU-MDR & FDA Recall Risk

Stringent

EU-MDR & FDA Recall Risk

| -0.4% | EU and North America primarily, with spillover effects globally | Medium term (2-4 years) | |||

Reimbursement

Cuts Causing Implant Shortages

Reimbursement

Cuts Causing Implant Shortages

| -0.3% | North America and Europe, with Medicare and national health systems | Short term (≤ 2 years) | |||

Potential

Demand Dampening from Weight-Loss Drugs

Potential

Demand Dampening from Weight-Loss Drugs

| -0.2% | High-income markets with GLP-1 access, primarily North America and Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Procedure & Implant Costs

In 2024, Medicare reimbursed USD 12,553 per THA 5.5% above 2019 levels while China’s centralized procurement halved implant prices, demonstrating stark cost asymmetry. Limited GLP-1 drug coverage, affecting nearly two-thirds of eligible patients, further constrains surgical access in obesity-linked osteoarthritis. Elevated index-procedure costs magnify downstream burdens from complications such as periprosthetic infection, pressuring hospitals to prioritize value-based contracts. Device firms counter with additive-manufactured stems and streamlined instrument trays that compress sterilization and logistics expenses. Yet constrained public-sector budgets in emerging markets continue to temper Hip Reconstruction Devices market penetration, especially for premium implants.

Stringent EU-MDR & FDA Recall Risk

The 2024 FDA class II recall of Zimmer Biomet’s CPT stem affected 242,000 devices worldwide, spotlighting how safety lapses can abruptly disrupt supply chains.[3]U.S. Food & Drug Administration, “Class 2 Device Recall CPT,” fda.gov Parallel EU-MDR timelines impose fully compliant quality-management systems by 2024-2028, escalating regulatory costs and documentation burdens on manufacturers. Mid-sized firms face disproportionate impact, occasionally suspending SKUs or delaying new launches during conformity-assessment backlogs. Conversely, multinationals leverage deep regulatory resources to navigate audits and sustain portfolio breadth, reinforcing the moderate concentration within the Hip Reconstruction Devices market. Compliance demands also stimulate advisory-service niches and sophisticated post-market surveillance software.

Segment Analysis

By Product Type: Dual-Mobility Momentum within a Primary Device Core

Primary devices generated the largest revenue slice, representing 40.72% of 2025 hip reconstruction devices market share. Rising surgical volumes among aging yet active cohorts enhance preference for highly cross-linked polyethylene liners and advanced ceramic heads that extend implant longevity. Dual-mobility systems, while smaller today, are accelerating at a 7.05% CAGR to 2031, driven by superior dislocation resistance, especially in high-risk or revision patients. OXINIUM oxide-infused alloy heads achieved 94.1% survivorship at 20 years, translating into 35% fewer revisions versus conventional metal-on-polyethylene pairings. Partial devices preserve a role in hemiarthroplasty for frail femoral-neck–fracture patients, though comparative studies increasingly favor total hip with dual mobility on functional scores. Hip resurfacing retains niche appeal for young athletes due to bone-conserving benefits but faces narrowed indications following metal-ion surveillance.

Additive manufacturing and AI-based templating are enabling bespoke implant geometries, shrinking inventory and optimizing bone preservation. Modular neck-stem constructs cater to complex anatomies yet remain under scrutiny after past corrosion-related recalls. Revision-specific cages and augments see steady uptake as first-generation patients outlive implants, enlarging the hip reconstruction devices market size for revision solutions by the end of the decade. Competitive intensity hinges on differentiated surface treatments, advanced bearing couples, and digital planning workflows.

Note: Segment shares of all individual segments available upon report purchase

By Fixation Type: Cementless Ascendancy

Cementless fixation occupied 52.68% of the hip reconstruction devices market size in 2025 and is advancing at a 6.32% CAGR through 2031. Porous titanium and tantalum coatings generate early mechanical stability and long-term osseointegration, cutting aseptic-loosening revisions. LimaCorporate’s 3D-printed Trabecular Titanium cups exhibit 87% cortical bone ingrowth, underpinning broader confidence in additive-built surfaces. Cemented stems still dominate among osteoporotic elderly because low axial loading demands outweigh concerns on cement fatigue cracking. Hybrid techniques gain favor when acetabular bone quality diverges from femoral status, optimizing fixation per side while moderating cement mantle risks.

Broader adoption of robotic milling and intra-op imaging ensures precise press-fit seating, lowering early subsidence. However, cementless selection mandates thorough bone-density assessment to avert periprosthetic fracture. Suppliers invest in stiffness-matched lattices that mitigate stress shielding by approximating the elastic modulus of cancellous bone, an innovation trajectory likely to sustain cementless dominance in the hip reconstruction devices market.

By End User: ASC Growth Redesigns the Channel

Hospitals retained 58.12% revenue share of the Hip Reconstruction Devices market in 2025, benefiting from established trauma services and intensive-care capacity for complex revisions. Nonetheless, ASCs are forecast to grow at 8.35% CAGR, catalyzed by payer policies that reimburse same-day total-joint bundles. Zimmer Biomet logged nearly 4% volume growth in U.S. hip procedures by tailoring instrumentation kits for outpatient workflows. ASCs emphasize rapid-recovery protocols, driving demand for short-stay-friendly implant systems with minimal soft-tissue disruption. Orthopedic clinics and specialty joint centers complement the spectrum by managing revision outliers and high-complexity deformities.

ASC operators face constraints around sterilization throughput, supply-chain inventory, and peri-operative analgesia expertise. Consequently, implant vendors bundle analytics platforms and staff education to ensure protocol adherence. Hospitals, meanwhile, are redesigning inpatient programs around higher-acuity or multi-revision cases, intensifying capital expenditure on robotics and infection-prevention suites. The dual-channel dynamic broadens the Hip Reconstruction Devices market, rewarding suppliers able to customize value propositions across divergent care settings.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

Geography Analysis

North America accounted for 43.25% of 2025 Hip Reconstruction Devices market revenue, supported by more than 450,000 total-hip arthroplasties annually, mature reimbursement coverage, and early robotic penetration. Cementless stems constitute the standard of care, and dual-mobility adoption is expanding rapidly to curb instability complications. Regulatory vigilance remains elevated, as highlighted by the 2024 Zimmer Biomet recall, yet the depth of clinical data and surgeon familiarity preserves overall momentum.

Europe, although exposed to EU-MDR cost overheads, maintains high per-capita procedure rates and sophisticated revision capabilities. National joint registries fuel evidence-based purchasing, channeling demand toward implants with robust survivorship trajectories. Outpatient migration lags the United States but is accelerating in Scandinavia and the United Kingdom as payers prioritize day-case efficiency.

Asia Pacific is the fastest-growing region, advancing at a 5.12% CAGR thanks to expanding insurance coverage and aging demographics. China’s national volume-based procurement strategy trimmed total-hip implant prices by 50%, unlocking significant latent demand while pressuring supplier margins. Japan and South Korea demonstrate high robotic-surgery uptake, whereas India sees proliferation of mid-tier domestic manufacturers producing cost-optimized cementless stems. The Hip Reconstruction Devices market share in this region is set to widen further as tertiary hospitals scale capacity and clinical-outcome reporting improves.

South America and the Middle East & Africa collectively still represent a modest fraction of the Hip Reconstruction Devices market, yet their long-term potential grows with health-system investment and surgeon training exchanges. Colombia, for example, is projected to perform 13,902 hip replacements by 2050, mirroring broader regional orthopedic expansion. Import tariffs and currency volatility remain headwinds, prompting global vendors to weigh localized assembly or strategic partnerships to secure price competitiveness.

Competitive Landscape

Market Concentration

The hip reconstruction devices market is moderately concentrated, with Zimmer Biomet, Stryker, and Johnson & Johnson DePuy forming a triad commanding the bulk of global revenue. Each leverages comprehensive product lines spanning primary, revision, and cementless platforms, supported by dedicated digital-surgery ecosystems. Zimmer Biomet’s USD 1.1 billion purchase of Paragon 28 in 2025 signals a diversification push into faster-growing extremity implants while broadening cross-selling synergies.

Stryker continues to scale the MAKO robotic platform across hip, knee, and shoulder modules, reinforcing a data-flywheel advantage through cumulative procedure analytics. Johnson & Johnson DePuy accelerates smart-implant programs integrating RFID tracking for inventory automation and post-market surveillance. Smith+Nephew’s CORI system gains U.S. FDA clearances for AI-driven pre-operative planning, illustrating the competitive race toward workflow-embedded software.

Emerging challengers emphasize additive manufacturing, as evidenced by Enovis’ EUR 800 million acquisition of LimaCorporate and its Trabecular Titanium intellectual property, creating a USD 1 billion reconstruction division. Micro-multinationals concentrate on patient-specific implants and instrument sets tailored for ASC efficiency, occasionally licensing platforms to larger players seeking gap-fill options. The converging themes of regulatory compliance, digital-planning integration, and cost-out innovation collectively shape rivalry intensity in the hip reconstruction devices market.

Hip Reconstruction Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zimmer Biomet announced a definitive agreement to acquire Paragon 28 for approximately USD 1.1 billion, enhancing its portfolio in the foot and ankle orthopedic segment. This acquisition represents Zimmer Biomet's strategic diversification beyond core hip and knee markets into higher-growth specialty segments, expected to create cross-selling opportunities and accelerate revenue growth in the orthopedic reconstruction space.

- December 2024: Zimmer Biomet received FDA 510(k) clearance for the Persona SoluTion PPS Femur, a cementless total knee implant designed for patients with sensitivities to bone cement and metals. The implant features proprietary Tivanium alloy and porous coating technology, addressing growing concerns about metal hypersensitivity reactions and expanding treatment options for sensitive patient populations.

- December 2024: Smith+Nephew introduced CORIOGRAPH Pre-Op Planning and Modeling Services for total hip arthroplasty, cleared by the FDA. This software enables surgeons to create personalized surgical plans using X-rays or CT scans, enhancing accuracy and optimizing implant placement as part of the CORI Surgical System's integrated approach to hip reconstruction procedures.

- January 2024: Enovis Corporation completed its acquisition of LimaCorporate S.p.A. for EUR 800 million (USD 850 million), creating a USD 1 billion revenue reconstruction business. LimaCorporate's innovative 3D-printed Trabecular Titanium implant technologies and global presence in hip reconstruction complement Enovis's existing orthopedic portfolio, particularly strengthening capabilities in complex revision procedures and patient-specific solutions.

Table of Contents for Hip Reconstruction Devices Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence of Hip Fractures & Osteoarthritis

- 4.2.2Expanding Geriatric Population

- 4.2.3Rapid Uptake of Minimally-Invasive & Robotic THA

- 4.2.4Shift Toward Outpatient & ASC Settings

- 4.2.5Ai-Driven Surgical Planning & Patient-Specific Implants

- 4.2.6GLP-1-Induced Obesity Decline Expanding Surgical Eligibility

- 4.3Market Restraints

- 4.3.1High Procedure & Implant Costs

- 4.3.2Stringent EU-MDR & FDA Recall Risk

- 4.3.3Reimbursement Cuts Causing Implant Shortages

- 4.3.4Potential Demand Dampening from Weight-Loss Drugs

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Product Type

- 5.1.1Primary Hip Reconstruction Devices

- 5.1.2Partial Hip Reconstruction Devices

- 5.1.3Revision Devices

- 5.1.4Hip Resurfacing Devices

- 5.1.5Dual-mobility Systems

- 5.1.6Modular Neck/Stem Components

- 5.1.7Other Products

- 5.2By Fixation Type

- 5.2.1Cementless

- 5.2.2Cemented

- 5.2.3Hybrid

- 5.2.4Others

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Orthopedic Clinics

- 5.3.3Ambulatory Surgical Centers

- 5.3.4Specialized Joint-Replacement Centers

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Zimmer Biomet

- 6.3.2Johnson & Johnson (DePuy Synthes)

- 6.3.3Stryker

- 6.3.4Smith & Nephew

- 6.3.5B. Braun (Aesculap)

- 6.3.6MicroPort Orthopedics

- 6.3.7Exactech

- 6.3.8Waldemar Link

- 6.3.9LimaCorporate

- 6.3.10Surgival

- 6.3.11Hip Innovation Technology

- 6.3.12JointMedica

- 6.3.13Corin Group

- 6.3.14DJO Global

- 6.3.15Wright Medical (Tornier)

- 6.3.16Medacta

- 6.3.17Arthrex

- 6.3.18United Orthopedic Corp.

- 6.3.19Conformis

- 6.3.20OrthAlign

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Hip Reconstruction Devices Market Report Scope

As per the report's scope, hip reconstruction devices are used in surgeries that often occur after hip fractures. The hip reconstruction devices market is segmented by product type (primary hip reconstruction devices, partial hip reconstruction devices, hip resurfacing devices, and other products), end-user (hospitals, orthopedic clinics, and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.