Heart Pump Device Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.67 Billion |

| Market Size (2030) | USD 8.03 Billion |

| Growth Rate (2025 - 2030) | 16.96% CAGR |

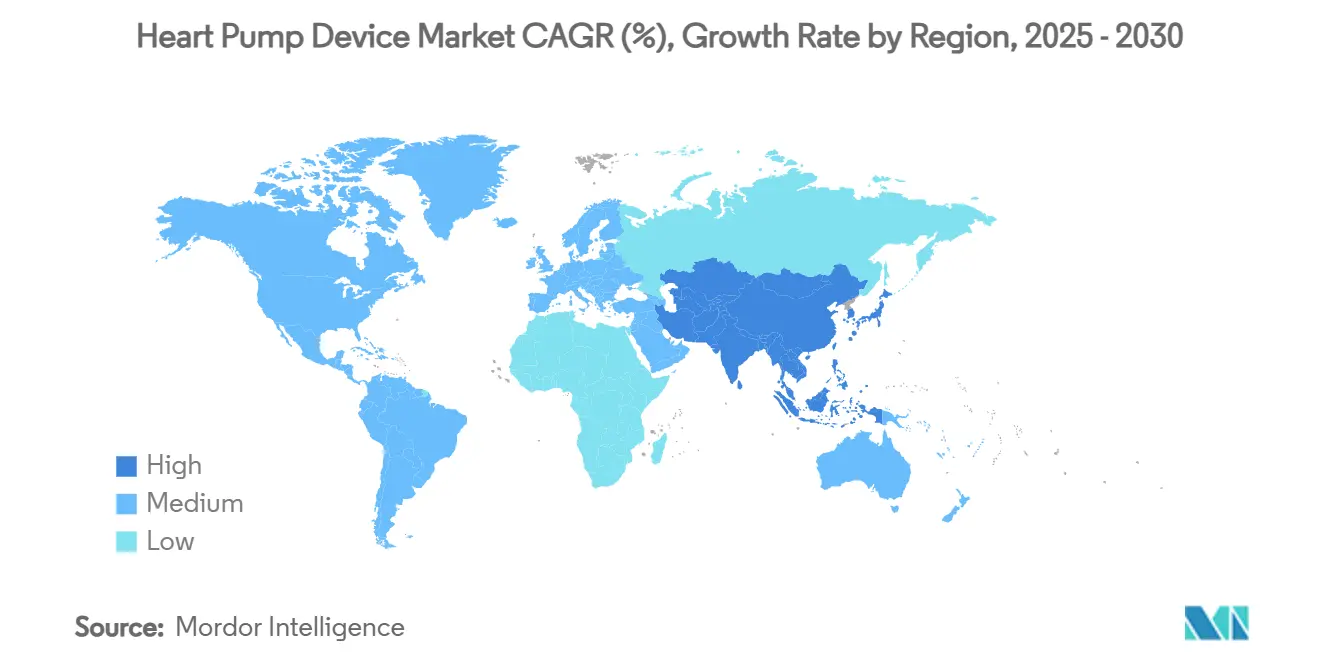

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

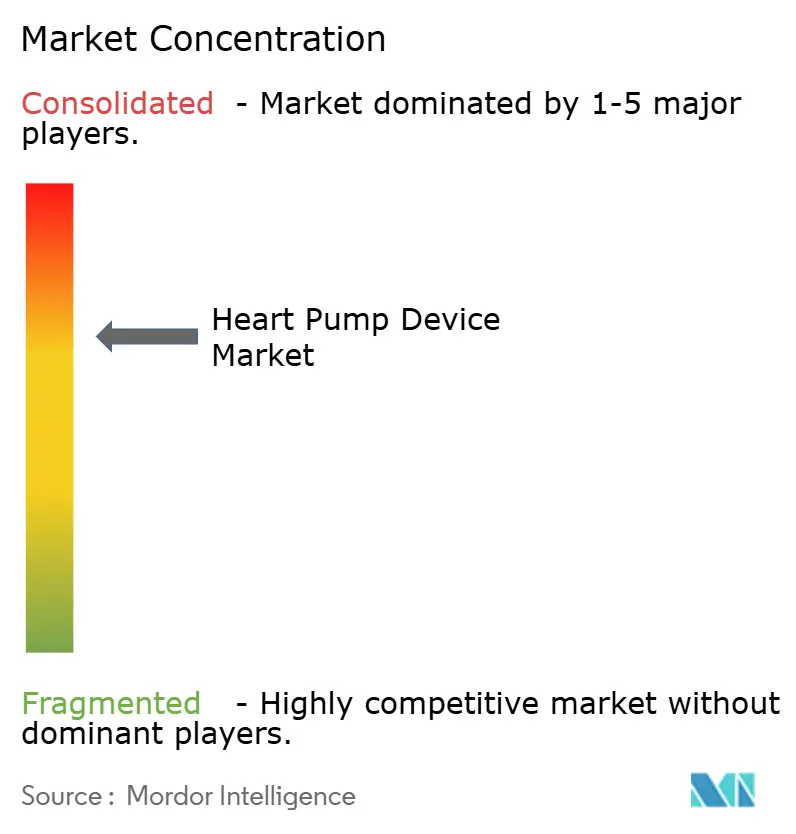

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heart Pump Device Market Analysis by Mordor Intelligence

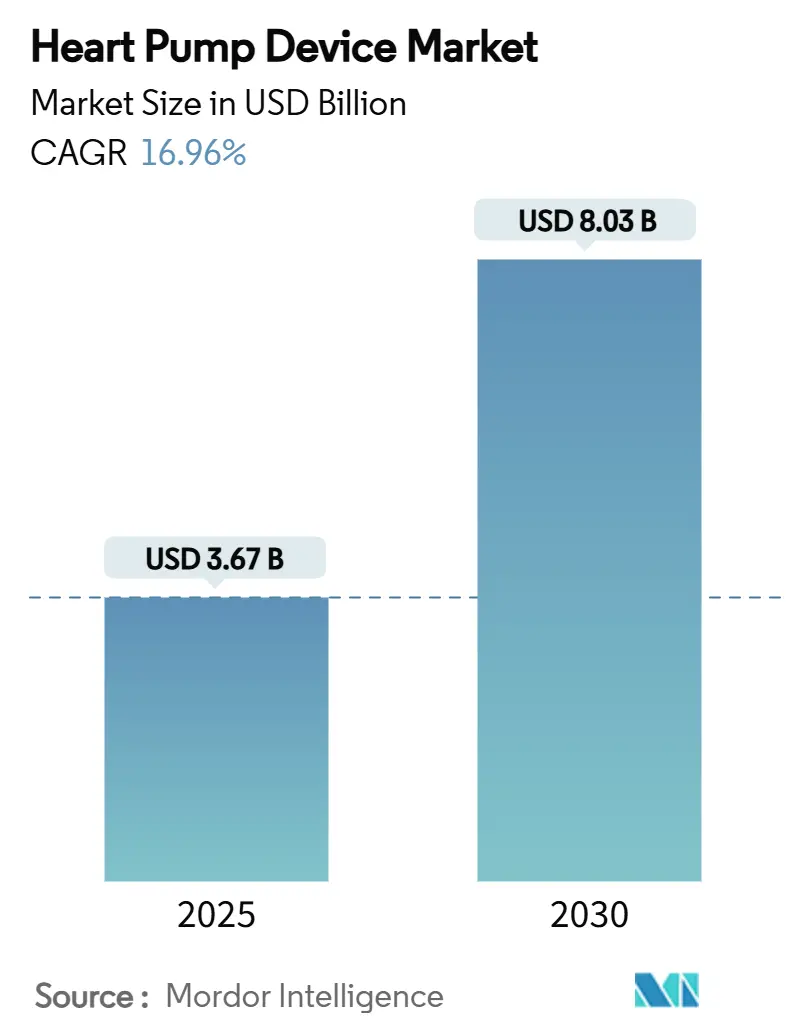

The heart pump device market is valued at USD 3.67 billion in 2025 and is forecast to reach USD 8.03 billion by 2030, advancing at a 16.96% CAGR. The figures underline a clear upward trajectory in market size supported by aging populations, widening transplant waiting lists, and steady improvements in mechanical circulatory support technology.[1]Centers for Medicare & Medicaid Services, “2025–05–29 MLNC,” cms.gov Continued North American dominance and rapid Asia-Pacific uptake shape a competitive global landscape, while reimbursement expansions in the United States and Europe accelerate patient access. Technological pivots—from large implantable systems to percutaneous pumps—enable minimally invasive procedures, broaden the treatable cohort, and lower the cost of care. At the same time, supply-chain sensitivities around rare-earth magnets and heightened regulatory scrutiny after several Class I recalls remind manufacturers that quality management and sourcing resilience remain pivotal. Consolidation, highlighted by Johnson & Johnson’s acquisition of Abiomed, underlines the race for clinical data leadership and end-to-end platform control in the heart pump device market.[2]Abbott, “Momentum 3 Trial Publications,” cardiovascular.abbott

Key Report Takeaways

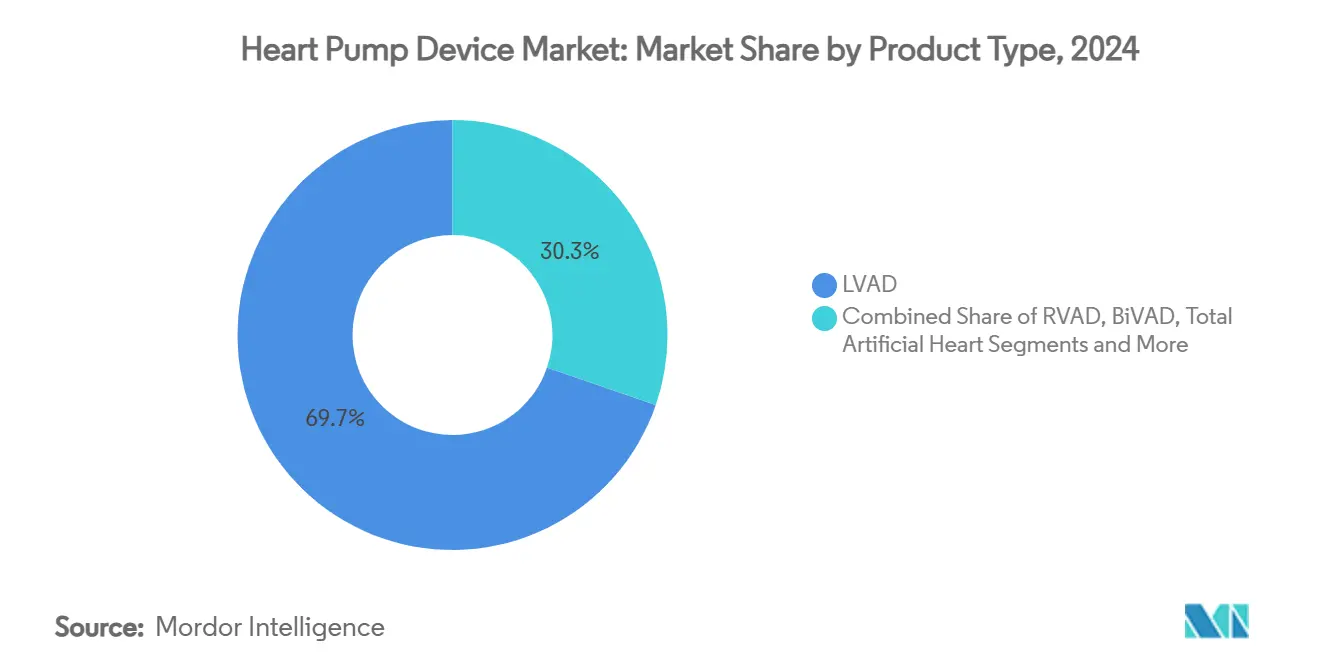

- By product type, Left Ventricular Assist Devices (LVADs) led with 69.73% of heart pump device market share in 2024, whereas percutaneous VADs are set to expand at 19.78% CAGR through 2030.

- By device type, implantable systems accounted for 68.72% of the heart pump device market size in 2024; extracorporeal devices record the swiftest growth at an 18.34% CAGR to 2030.

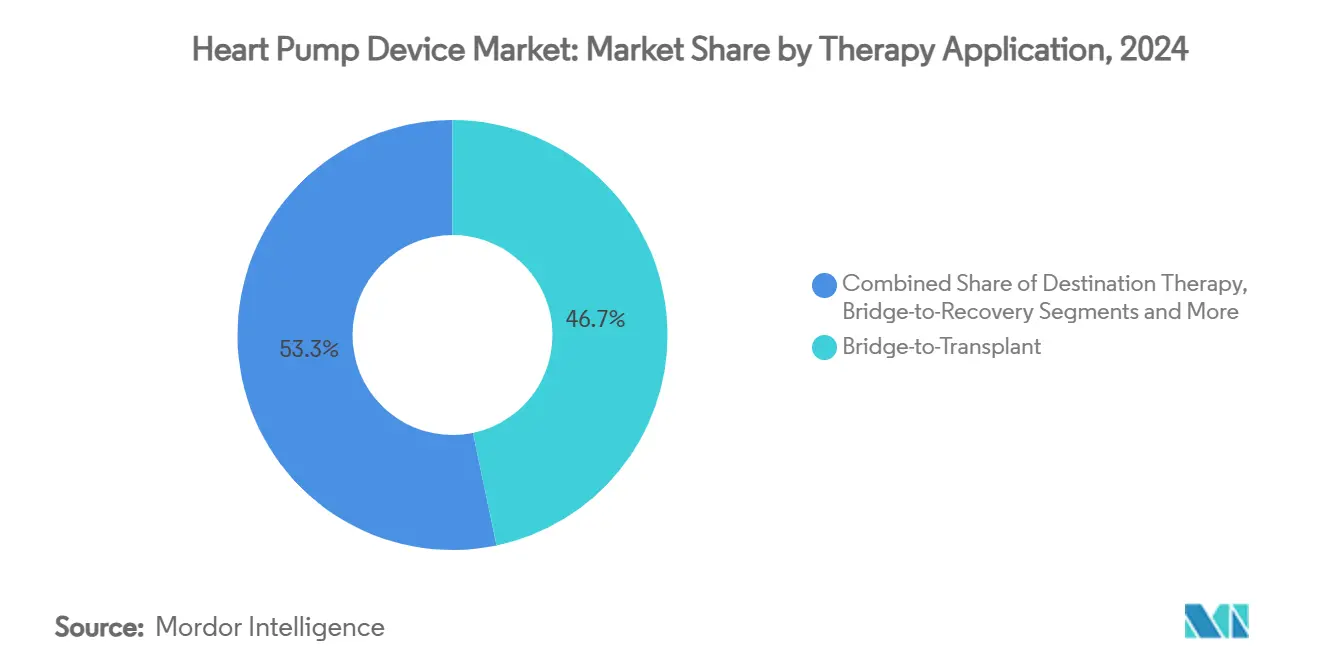

- By therapy application, bridge-to-transplant contributed 46.72% revenue share in 2024; destination therapy is on course to rise at an 18.53% CAGR, reflecting broader payer acceptance.

- By end user, tertiary care hospitals held 83.41% share of the heart pump device market in 2024, while home healthcare settings are poised for 19.02% CAGR growth.

- By geography, North America dominated with 38.77% share in 2024; Asia-Pacific represents the fastest-growing region with an 18.53% CAGR until 2030.

Global Heart Pump Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of end-stage HF & donor-organ shortage | +3.5% | Global; acute in North America & Europe | Long term (≥ 4 years) |

| Continuous-flow LVADs improve survival & QoL | +2.8% | Core North America & EU; extending to APAC | Medium term (2-4 years) |

| Reimbursement expansion for destination therapy | +1.9% | North America & Europe | Short term (≤ 2 years) |

| Growth of minimally invasive percutaneous VADs | +2.1% | Developed markets worldwide | Medium term (2-4 years) |

| Magnetically levitated fully implantable LVAD trials | +1.7% | North America & Europe; global roll-out | Long term (≥ 4 years) |

| Pediatric-size VAD miniaturization | +1.2% | Global; focused in specialty centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of End-Stage HF & Donor-Organ Shortage

Heart failure affects more than 6.2 million Americans, yet donor hearts remain limited at roughly 3,500 annually. As incidence doubles each decade after age 65, demand outstrips supply and positions mechanical circulatory support as a core therapy. December 2024 FDA clearance of the Impella platform for children shows how technology is filling age-group gaps in a strained transplant ecosystem. Five-year LVAD survival rates now approximate 63%, encouraging clinicians to recommend long-term support even for transplant-ineligible seniors. Together, these demographic and clinical realities reinforce long-run growth in the heart pump device market.

Continuous-Flow LVADs Improve Survival & Quality of Life

Five-year data from the MOMENTUM 3 trial reveal 54% survival with HeartMate 3 versus 29.7% for axial-flow pumps, cementing continuous-flow systems as standard of care.[3]Linda Wanjiku Njoroge and Navin Rajagopalan, “Sustained Superiority of the HeartMate 3 LVAD,” American College of Cardiology, acc.org Average 6-minute walk distances tripled post-implant, underscoring functional gains that justify premium pricing. ELEVATE registry results confirm 63.3% survival in real-world cohorts. Reduced thrombosis (0.01 events per patient-year) and low rehospitalization rates enable 85% of patients to live at home, easing burdens on health systems and caregivers.

Reimbursement Expansion for Destination Therapy in US/EU

CMS coverage for implantable pulmonary artery pressure sensors, effective January 2025, directly supports permanent LVAD programs by lowering hospitalization risk 30% and cutting costs. CLEAR-LVAD data show USD 10,722–USD 17,947 lower Medicare outlays for HeartMate 3 compared with alternatives. Similar cost-effectiveness findings in Dutch registries drive wider European reimbursements. New remote-monitoring codes create recurring revenue for clinics, accelerating uptake of destination therapy.

Growth of Minimally Invasive Percutaneous VADs

Johnson & Johnson’s USD 16.6 billion Abiomed purchase confirmed market appetite for catheter-based pumps. While MAUDE data report bleeding in 38% of Impella cases, the devices allow intervention in high-risk coronary patients once deemed untreatable. Investor funding—USD 105 million for Magenta’s palm-sized pump—signals confidence in next-gen miniaturization. Rapid, sub-15-minute insertion makes percutaneous devices invaluable in emergency shock, propelling the heart pump device market toward less invasive therapy models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & surgical costs in emerging markets | −1.8% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Device-related adverse events (bleeding, stroke, infection) | −1.4% | Global | Short term (≤ 2 years) |

| HeartMate 3 Class I recalls heighten scrutiny | −1.1% | North America & Europe | Short term (≤ 2 years) |

| Rare-earth magnet & titanium supply constraints | −0.9% | Global manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device-Related Adverse Events (Bleeding, Stroke, Infection)

A systematic review shows 78% of LVAD recipients encounter infections, with drivelines accounting for 22% of cases. Bloodstream infection and bleeding (0.43 events per patient-year in HeartMate 3) still demand resource-intensive management. Stroke, though reduced to 0.05 events per patient-year, remains a life-altering risk. Such complications limit program expansion to centers possessing multidisciplinary expertise.

HeartMate 3 Class I Recalls Heighten Regulatory Scrutiny

Multiple FDA Class I actions during 2024–2025—covering graft obstruction and power-unit failures—compelled heightened post-market surveillance across manufacturers. Extended review timelines and mandatory registries inflate compliance costs and dampen smaller entrants’ enthusiasm, weighing on the heart pump device market’s near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LVAD Dominance Faces Percutaneous Challenge

LVADs captured 69.73% of 2024 revenue, securing the highest heart pump device market share, whereas percutaneous VADs post a 19.78% CAGR outlook through 2030. The heart pump device market size for LVADs reflects clinical confidence built on HeartMate 3’s 58.4% five-year survival advantage. Axial-flow decline continues as magnetically levitated centrifugal pumps reduce thrombosis and hemolysis. RVADs and BiVADs serve right-sided and biventricular failure niches, while total artificial hearts offer a lifeline to complex anatomical cases, highlighted by BiVACOR’s 2024 first-in-human implant. Emerging percutaneous platforms extend support into cath-lab settings, enabling high-risk PCI and rapid-response shock therapy.

A second wave of miniaturized pumps is readying for market entry, with venture-backed start-ups focusing on sheath sizes below 10 Fr and battery-free operation. These innovations may compress procedural times, expand outpatient indications, and diversify the heart pump device market.

By Device Type: Implantable Systems Lead Despite Extracorporeal Growth

Implantable solutions represented 68.72% of 2024 revenue, underpinning USD 2.52 billion of the heart pump device market size, while extracorporeal models are projected to swell at 18.34% CAGR through 2030. Median survival beyond five years and 85% home-discharge rates make implantables indispensable for destination therapy. Wireless energy transfer studies aim to eradicate drivelines altogether, further amplifying patient quality of life.

Extracorporeal pumps, by contrast, thrive as bridge-to-decision tools. CentriMag’s 51.8% one-year survival in refractory shock underpins demand where rapid stabilization is critical. Portability upgrades—lighter consoles and smaller priming volumes—let clinicians mobilize patients during support, a feature that accelerates recovery and hospital throughput.

By Therapy Application: Bridge-to-Transplant Leads While Destination Therapy Accelerates

Bridge-to-transplant held 46.72% share in 2024, mirroring ongoing dependence on donor organs, yet destination therapy is climbing at an 18.53% CAGR as payer acceptance broadens. ROADMAP showed 80% twelve-month survival for LVAD recipients compared with 63% on optimal medical therapy. Growing clinician confidence and streamlined reimbursement erode historical reluctance to implant LVADs as permanent solutions.

Bridge-to-recovery applications flourish in myocarditis and peripartum cohorts, where reversible pathology enables eventual explantation, while bridge-to-decision use cases offer critical time for candidacy evaluation. This multi-track framework ensures mechanical support adapts to clinical uncertainty, expanding the heart pump device market’s scope.

By End User: Hospital Dominance Challenged by Home Healthcare Growth

Tertiary hospitals contributed 83.41% of 2024 revenue, reflecting surgical complexity and intensive follow-up needs. However, home healthcare settings exhibit a 19.02% CAGR, spurred by remote pressure sensors and AI-enabled monitoring that flag early decompensation. CardioMEMS’ decade-long dataset shows 35,000 implants with 30% hospitalization reductions, validating decentralized care.

Ambulatory surgical centers increasingly host percutaneous VAD procedures, offering cost savings and same-day discharge. Specialty cardiac centers retain a research and training edge, ensuring high-risk cases remain centralized while routine management migrates outward. This redistribution of care sites reshapes resource allocation within the heart pump device industry.

Geography Analysis

North America held 38.77% revenue share in 2024, buoyed by more than 3,000 annual implants and robust Medicare coverage for destination therapy. Canadian provinces coordinate LVAD programs under single-payer funding, while Mexico’s private hospitals attract cross-border patients seeking affordable surgery. Clinical registries such as MOMENTUM 3 and ELEVATE emanate from U.S. centers, reinforcing the region’s innovation leadership and global guideline influence.

Europe remains a mature yet opportunity-rich arena. Germany, the United Kingdom, and France run high-volume LVAD centers under publicly funded systems, while CE-mark processes and real-world cost-effectiveness data support steady adoption. Southern and Eastern European countries report double-digit growth as reimbursement pathways unlock.

Asia-Pacific delivers the fastest regional CAGR at 18.53%, powered by China’s domestic manufacturing push and Japan’s aging demographic. Beijing’s policy drive to onshore magnetically levitated pump production mitigates rare-earth supply concerns and trims cost barriers. India’s burgeoning private sector and medical tourism expand patient throughput, while South Korea and Australia leverage advanced cardiac hubs to serve regional demand. Middle East & Africa, although nascent, show promise as Gulf states invest in cardiac centers of excellence.

Competitive Landscape

Market structure is moderately concentrated. Abbott’s HeartMate 3 commands clinical mindshare despite recent recalls, which intensified oversight but also spurred device-quality improvements. Johnson & Johnson, post-Abiomed, controls a leading percutaneous VAD portfolio and directs capital toward miniaturization and evidence generation. Medtronic competes across pump classes, leveraging global distribution channels.

Emerging innovators—BiVACOR, FineHeart, CorWave—pursue disruptive total artificial hearts and membrane pumps. Venture capital flows target wireless energy transfer and AI-enabled home monitoring, reflecting the sector’s pivot beyond pure hardware. Strategic imperatives center on head-to-head outcomes trials and post-market surveillance excellence, both essential for maintaining or winning share in the heart pump device market.

Heart Pump Device Industry Leaders

Abbott Laboratories

Johnson & Johnson

Medtronic plc

Terumo Corporation

Berlin Heart

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CorWave implanted the first wave-membrane LVAS in a human patient, ushering a new propulsion modality.

- December 2024: FDA broadened Impella’s label to include pediatric indications, expanding the minimally invasive heart pump device market.

- July 2024: BiVACOR achieved first-in-human total artificial heart implantation at Texas Heart Institute, backed by USD 13 million funding.

Global Heart Pump Device Market Report Scope

| LVAD | Continuous-flow LVAD |

| Pulsatile-flow LVAD | |

| RVAD | |

| BiVAD | |

| Total Artificial Heart (TAH) | |

| Percutaneous VAD | |

| Intra-aortic Balloon Pump (IABP) | |

| Extracorporeal Centrifugal Pump |

| Implantable |

| Extracorporeal |

| Bridge-to-Transplant |

| Destination Therapy |

| Bridge-to-Recovery |

| Bridge-to-Decision / Candidacy |

| Tertiary Care Hospitals |

| Specialty Cardiac Centers |

| Ambulatory Surgical Centers |

| Home-Healthcare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | LVAD | Continuous-flow LVAD |

| Pulsatile-flow LVAD | ||

| RVAD | ||

| BiVAD | ||

| Total Artificial Heart (TAH) | ||

| Percutaneous VAD | ||

| Intra-aortic Balloon Pump (IABP) | ||

| Extracorporeal Centrifugal Pump | ||

| By Device Type | Implantable | |

| Extracorporeal | ||

| By Therapy / Application | Bridge-to-Transplant | |

| Destination Therapy | ||

| Bridge-to-Recovery | ||

| Bridge-to-Decision / Candidacy | ||

| By End User | Tertiary Care Hospitals | |

| Specialty Cardiac Centers | ||

| Ambulatory Surgical Centers | ||

| Home-Healthcare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the heart pump device market?

The heart pump device market is valued at USD 3.67 billion in 2025 and is on track to reach USD 8.03 billion by 2030.

Which product segment generates the highest revenue?

LVADs account for 69.73% of 2024 revenue, making them the largest contributor to the heart pump device market.

Which segment is growing the fastest?

Percutaneous VADs are forecast to post a 19.78% CAGR through 2030, the quickest among all product categories.

How dominant is North America in this market?

North America holds 38.77% market share, sustained by robust reimbursement policies and high procedural volumes.

Why is destination therapy gaining momentum?

Improved five-year survival, expanded CMS coverage, and lower total Medicare costs are driving wider adoption of permanent LVAD support.

Page last updated on: