Interventional Cardiology Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

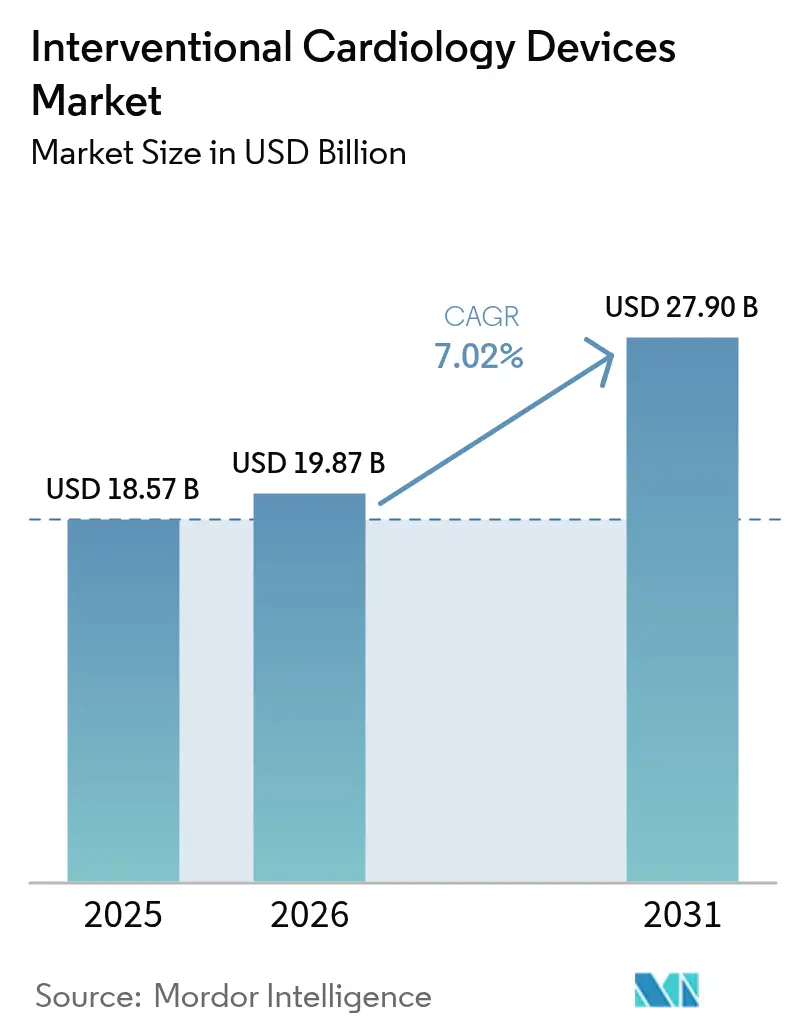

| Market Size (2026) | USD 19.87 Billion |

| Market Size (2031) | USD 27.9 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interventional Cardiology Devices Market Analysis by Mordor Intelligence

The interventional cardiology devices market size was valued at USD 18.57 billion in 2025 and estimated to grow from USD 19.87 billion in 2026 to reach USD 27.9 billion by 2031, at a CAGR of 7.02% during the forecast period (2026-2031). Current growth is anchored by brisk uptake of minimally invasive procedures that rely on drug-eluting stents, intravascular lithotripsy (IVL) systems and AI-enhanced imaging. The expanding global burden of coronary artery disease (CAD), together with same-day discharge pathways and ambulatory surgical center (ASC) adoption, continues to enlarge the addressable patient pool. Product pipelines are shifting toward thinner-strut, bio-resorbable platforms as regulators and providers place greater emphasis on long-term safety and sustainability. Competitive intensity is rising as large manufacturers pursue acquisitions that add differentiated technologies and shore up supply chains. Escalating regulatory scrutiny, workforce shortages and material legislation present headwinds but have not derailed the market’s upward trajectory.

Key Report Takeaways

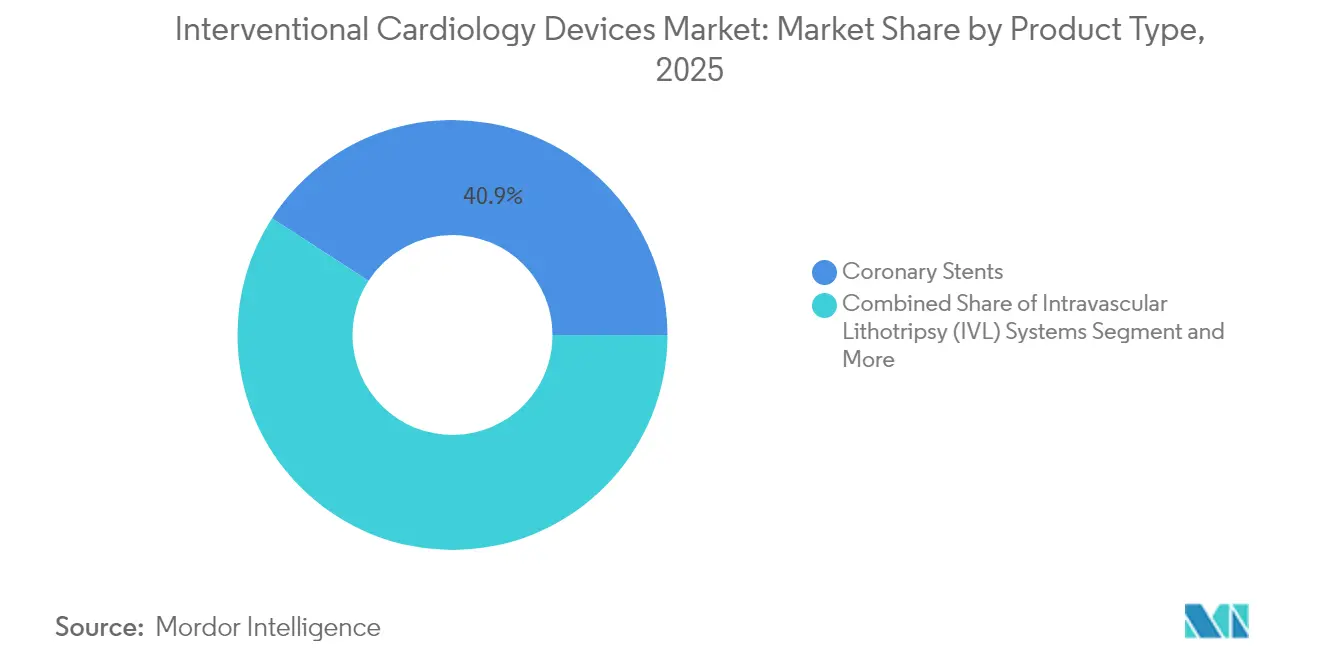

- By product type, coronary stents led with 40.86% of the interventional cardiology devices market share in 2025, while IVL systems are projected to grow at 10.75% CAGR through 2031.

- By end-user, hospitals commanded 66.88% share of the interventional cardiology devices market size in 2025; ASCs exhibit the fastest growth at 10.35% CAGR to 2031.

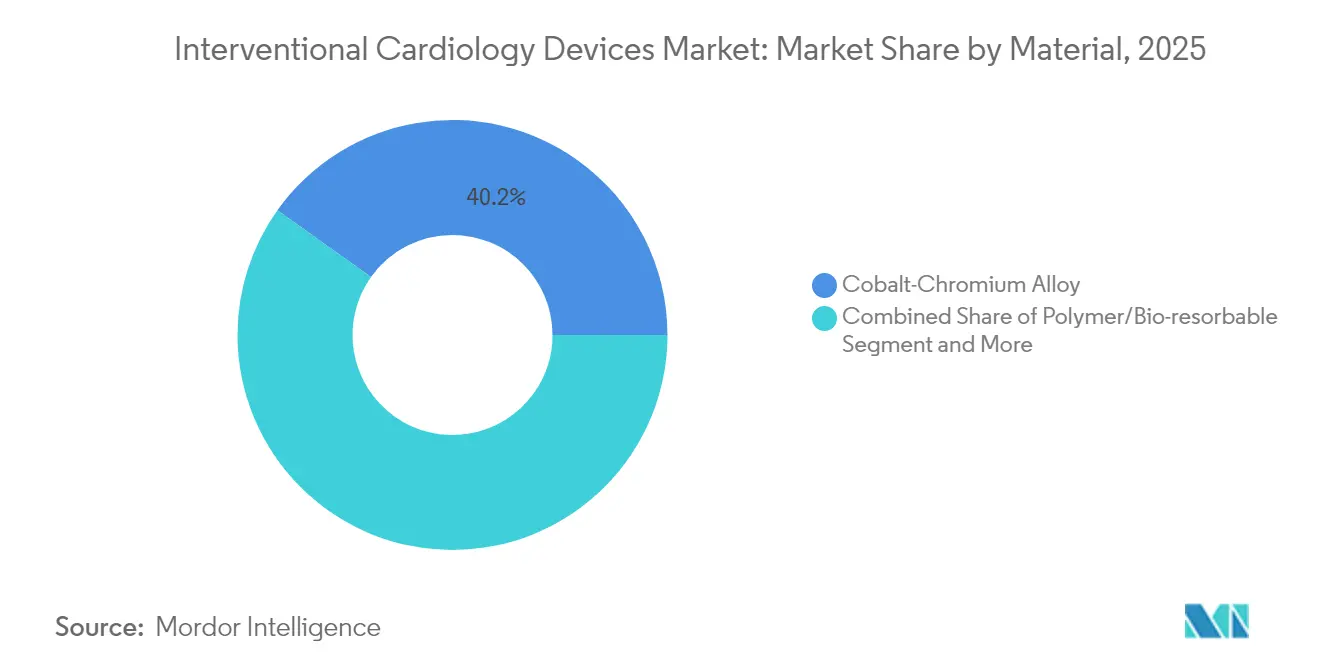

- By material, cobalt-chromium alloys accounted for 40.15% revenue share in 2025, whereas polymer and bio-resorbable platforms are advancing at 11.85% CAGR.

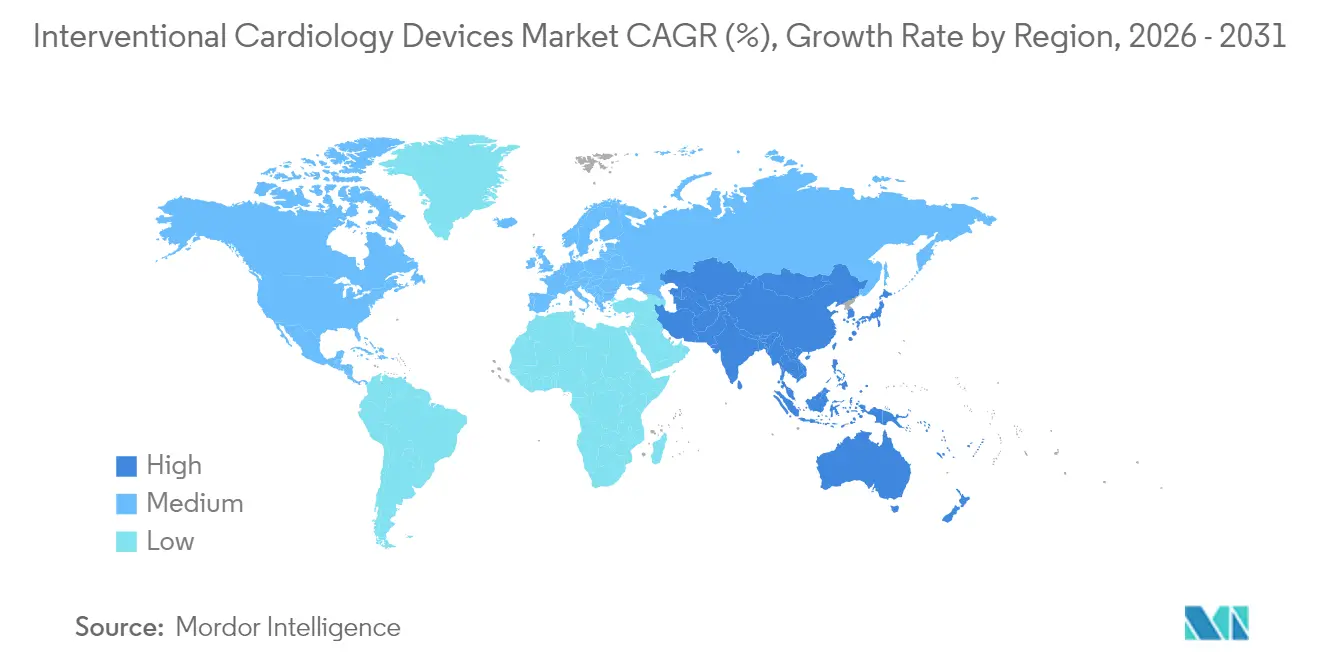

- By geography, North America held 41.25% of the interventional cardiology devices market in 2025, but Asia-Pacific is expanding at 12.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Interventional Cardiology Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing CAD prevalence & PCI volume | +1.8% | North America, Europe, APAC | Long term (≥ 4 years) |

| Shift to minimally invasive therapies | +1.5% | Developed markets | Medium term (2-4 years) |

| Drug-eluting stent (DES) price erosion | +1.2% | APAC, Latin America | Medium term (2-4 years) |

| AI-augmented imaging & decision support | +0.9% | North America, EU, APAC | Short term (≤ 2 years) |

| Same-day discharge and ASC migration | +0.7% | North America, Europe | Short term (≤ 2 years) |

| Sustainability push for bio-resorbables | +0.4% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of CAD & PCI Procedures

CAD remains the leading global cause of mortality, affecting more than 20 million adults in the United States alone. Aging populations, obesity and sedentary lifestyles are increasing procedural demand, particularly for multivessel disease and complex calcified lesions that benefit from IVL therapy. Asia-Pacific markets show the steepest rise as urbanization alters dietary and activity patterns. Re-interventions now constitute a larger portion of procedural volume because CAD is managed as a chronic condition, sustaining device utilization beyond single-episode care.

Accelerating Shift to Minimally Invasive Therapies

Hospitals and payers favor percutaneous approaches that shorten admissions and reduce complications. The COVID-19 pandemic reinforced this preference and catalyzed adoption of drug-eluting balloons and bio-resorbable scaffolds[1]JACC, “Same-Day Discharge Principles,” jacc.org. AI-assisted imaging enhances precision, lowers contrast load and expands eligibility for elderly or comorbid patients once deemed high risk for open surgery.

Continuous DES Price Erosion Expanding Addressable Pool

Generic entrants and manufacturing scale are lowering DES unit prices by up to 40% in emerging markets, enabling hospitals to broaden PCI programs without compromising outcomes. Value-based purchasing incentives further accelerate the shift toward cost-effective platforms, especially ultra-thin strut and biodegradable-polymer designs that maintain clinical performance[2]EuroIntervention, “Medical Device Regulation in Europe,” eurointervention.pcronline.com.

AI-Augmented Pre-PCI Imaging & Decision Support Adoption

HeartFlow’s CT-derived fractional flow reserve reduced unnecessary invasive angiography in more than 90,000 NHS patients, validating AI-enabled triage at national scale. Partnerships between image-analysis firms and device companies are integrating plaque characterization and 3-D visualization into routine workflow, improving first-pass success rates and reducing radiation exposure.

Restraints Impact Analysis of Interventional Cardiology Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region regulatory pathways | −1.1% | EU, United States, Japan | Medium term (2-4 years) |

| Global shortage of cath-lab personnel | −0.8% | Rural North America, developing regions | Long term (≥ 4 years) |

| First-line pharmacotherapy effectiveness | −0.6% | High-income markets | Long term (≥ 4 years) |

| Anti-plastic legislation on polymer supply | −0.4% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Regulatory Pathways

EU Medical Device Regulation demands more rigorous clinical data and post-market surveillance, increasing time-to-market and compliance costs. Concurrently, the United States has heightened recall oversight after several Class I events[3]U.S. FDA, “Class I Recall VARIPULSE Catheter,” fda.gov. Divergent regional requirements force manufacturers to run parallel approval programs, straining smaller innovators.

Global Shortage of Cath-Lab Personnel & Interventional Cardiologists

A projected deficit of 8,650 U.S. cardiologists by 2037 threatens capacity, with rural areas lacking full-time coverage for 22 million residents. Cath-lab nurse and technician training pipelines lag behind demand, leading to longer scheduling backlogs and under-utilization of installed capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Interventional Cardiology Devices Market Segment Analysis

By Product Type:

IVL Systems Drive InnovationCoronary stents generated the largest revenue, holding 40.86% of the interventional cardiology devices market in 2025, supported by durable demand for percutaneous interventions. IVL platforms, although nascent, are forecast to advance at 10.75% CAGR through 2031. The interventional cardiology devices market size for IVL technology is expected to expand markedly as heavily calcified lesions become more frequently treated percutaneously. Ultra-thin-strut drug-eluting stents and next-generation bio-absorbable scaffolds reduce restenosis and facilitate physiologic vessel healing. Bare-metal stents are now reserved for patients requiring abbreviated dual antiplatelet therapy. PTCA balloons and guidewires maintain steady volume growth, with drug-coated balloons gaining attention for in-stent restenosis management following FDA approval of the Agent platform in 2024.

Procedural adjuncts such as IVUS and OCT catheters benefit from AI overlays that refine lesion assessment and optimize device sizing. Hemostasis devices that enable immediate ambulation are integral to same-day discharge protocols. Collectively, these innovations bolster procedural efficiency and extend the clinical reach of PCI.

By End-user:

ASCs Accelerate Market ShiftHospitals represented 66.88% of market revenue in 2025 owing to infrastructure that supports high-risk interventions and 24-hour backup. ASC volumes, however, are climbing at 10.35% CAGR as Medicare reimbursement expands and clinical evidence affirms safety parity with inpatient settings. If penetration reaches half of eligible cases, health systems could save USD 200–500 million each year without compromising outcomes. The interventional cardiology devices market size for ASC procedures is poised to widen as cath-lab efficiencies and standardized protocols lower operating costs.

Hybrid cardiac catheterization laboratories blend hospital resources with ASC efficiency, offering an intermediate option for moderate-risk cases. Same-day discharge, endorsed by the American College of Cardiology, underpins this migration strategy and drives procurement of closure devices that minimize recovery time.

By Material:

Bio-resorbable Platforms Gain MomentumCobalt-chromium alloys retained 40.15% revenue share in 2025 for their strength and fluoroscopic visibility. Platinum-chromium and nitinol alloys dominate specialized niches requiring radiopacity or self-expansion. Polymer-based and fully bio-resorbable materials are projected to grow 11.85% annually, encouraged by the “leave-nothing-behind” paradigm. Abbott’s Esprit BTK scaffold secured FDA approval in 2024, demonstrating superior limb-salvage outcomes. The interventional cardiology devices market share of eco-friendly platforms is expected to expand further as California’s impending DEHP ban compels manufacturers to reformulate plastics. Iron-based scaffolds now exhibit complete resorption within 18 months while preserving radial force, addressing earlier mechanical limitations.

Geography Analysis

North America and Europe Interventional Cardiology Devices Market

North America led the interventional cardiology devices market with 41.25% revenue in 2025 on the back of broad insurance coverage, robust clinical research networks and rapid uptake of AI-guided imaging. The region is also pioneering ASC adoption and same-day discharge for complex PCI, although FDA recall vigilance and cath-lab staffing gaps temper growth. Europe follows as a mature yet innovation-friendly arena where sustainability initiatives encourage bio-resorbable scaffolds and lower-carbon supply chains. MDR compliance costs weigh on small manufacturers, but Germany and France continue to pilot early human use of next-generation devices.

APAC Interventional Cardiology Devices Market

Asia-Pacific is the standout growth engine with a 12.05% forecast CAGR. China’s public insurance expansion and hospital construction boom are scaling PCI volumes, while India’s price-capped environment favors cost-effective DES platforms anchored by local production. Japan’s stringent approval process slows rollouts but commands premium pricing once clearance is secured. South Korea and Australia showcase high procedural quality and early AI integration, positioning them as secondary innovation hubs. Together these trends are set to re-shape regional competitive dynamics and redistribute future revenue pools within the interventional cardiology devices market.

Competitive Landscape

The interventional cardiology devices market is moderately consolidated. Abbott, Medtronic, Boston Scientific and Johnson & Johnson collectively dominate through comprehensive portfolios and global distribution. Johnson & Johnson closed its USD 13.1 billion purchase of Shockwave Medical in 2024, gaining a leadership position in IVL technology. Teleflex announced a EUR 760 million acquisition of Biotronik’s vascular intervention unit in 2025, adding drug-coated balloons and DES capability.

R&D pipelines emphasize AI-enabled imaging, thinner-strut stents and fully absorbable materials. Medtronic’s equity option in CathWorks underscores strategic convergence between diagnostics and therapy. Smaller regional manufacturers compete on price and local regulatory agility, particularly in China and India, while private-equity roll-ups of cardiology practices in the United States are beginning to influence purchasing decisions through centralized contracting. Persistent recall events elevate reputational risk and can swiftly reshape share positions, reinforcing the importance of post-market surveillance and proactive quality management across the interventional cardiology devices industry.

Interventional Cardiology Devices Industry Leaders

Cook Medical Inc.

Abbott Laboratories

Boston Scientific Corporation

Terumo Medical Corporation

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Interventional Cardiology Devices Market Companies Covered in this Report

- Abbott Laboratories

- Medtronic

- Boston Scientific

- B. Braun

- Terumo Corp.

- Biosensors International

- BIOTRONIK

- Cardinal Health

- Cook Group

- Koninklijke Philips

- Edwards Lifesciences Corp.

- Nano Therapeutics Pvt. Ltd.

- Shockwave Medical Inc.

- Merit Medical Systems

- Siemens Healthineers

- AngioDynamics

- C. R. Bard (BD)

- MicroPort Scientific Corp.

- Alvimedica

Read Analysis of Interventional Cardiology Devices Companies

Recent Industry Developments in Interventional Cardiology Devices Market

- March 2025: Abbott initiated a 335-patient U.S. clinical trial evaluating its coronary IVL system.

- February 2025: Teleflex agreed to acquire Biotronik’s vascular intervention business for EUR 760 million, with deal closure expected in Q3 2025.

Interventional Cardiology Devices Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global interventional cardiology devices market as all catheter-based therapeutic products, including coronary stents, PTCA balloons, atherectomy and thrombectomy systems, intravascular imaging/physiology catheters, guidewires, vascular closure, and adjunct accessories, used to diagnose or treat coronary or structural heart lesions in cath-lab or hybrid-OR settings.

Scope exclusion: purely diagnostic non-invasive imaging modalities such as cardiac CT, MRI, and echocardiography systems remain outside the scope.

Segments Covered in This Report

- By Product Type

- Coronary Stents

- Bare-metal Stents

- Drug-eluting Stents

- Bio-absorbable Scaffolds

- Catheters

- Angiography Catheters

- IVUS/OCT Catheters

- PTCA Guiding Catheters

- PTCA Balloons

- Guidewires

- Hemostasis & Vascular Closure Devices

- Intravascular Lithotripsy (IVL) Systems

- Coronary Stents

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Cardiac Catheterization Labs

- By Material

- Cobalt-Chromium Alloy

- Platinum-Chromium Alloy

- Nitinol

- Polymer/Bio-resorbable

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed interventional cardiologists, cath-lab managers, regional distributors, reimbursement consultants, and materials scientists across North America, Europe, Asia-Pacific, and the Gulf. These conversations validated stent ASP erosion rates, emerging IVL adoption curves, ASC penetration, and post-COVID PCI rebound figures, closing gaps left by secondary data.

Desk Research

We began with structured reviews of major public datasets such as the World Health Organization's Global Health Estimates, American Heart Association Heart Disease & Stroke Statistics, Eurostat hospital discharge files, and OECD Health Expenditure data, which quantify disease burden, PCI procedure volumes, and cath-lab density across 60+ nations. Trade bodies, including the Cardiovascular Research Foundation, Medical Device Manufacturers Association, and China Association for Medical Devices Industry, provided shipment trends and regulatory timelines. Company 10-Ks, FDA 510(k)/PMA databases, and select paid platforms (D&B Hoovers for revenue splits, Dow Jones Factiva for deal flow) added competitive and pricing color. This list is illustrative; many additional open and paid sources informed our desk research.

Market-Sizing & Forecasting

We anchor 2025 market value through a top-down reconstruction. National PCI counts are multiplied by device usage factors and blended average selling prices, then reconciled with import-export sheet data and sampled supplier revenues to create a calibrated baseline. Select bottom-up checks, including supplier roll-ups and channel surveys, test the totals and flag anomalies. Key model drivers include (i) CAD prevalence trends, (ii) elective-to-emergency PCI mix, (iii) drug-eluting stent ASP trajectories, (iv) hospital cath-lab expansion, and (v) reimbursement policy shifts. Forecasts to 2030 employ multivariate regression combined with scenario analysis, allowing sensitivity to stent price caps and same-day discharge legislation. Gaps in bottom-up detail are bridged using regional proxy ratios agreed upon with our expert panel.

Data Validation & Update Cycle

Outputs pass a three-layer review, including algorithmic variance checks, senior-analyst peer review, and research manager sign-off. We re-contact sources when deviations exceed preset thresholds. The dataset refreshes annually, with interim updates triggered by major regulatory or M&A events, ensuring clients always receive the latest vetted view.

How Mordor Intelligence's Interventional Cardiology Devices Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose different device baskets, price assumptions, and refresh cadences.

By tying volumes to verified PCI counts and adjusting ASPs for regional tender data, Mordor minimizes these scope and currency skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.57 B (2025) | Mordor Intelligence | - |

| USD 11.28 B (2025) | Global Consultancy A | Narrow scope, excludes imaging/FFR catheters and vascular closure devices |

| USD 27.80 B (2024) | Industry Association B | Uses list prices, inflates value, and applies single-year growth proxy for forecasts |

The comparison shows that under-scoping can understate opportunity while unvalidated ASP multipliers can overstate it. By blending procedure-linked volumes with transaction-level pricing, Mordor Intelligence delivers a balanced, transparent baseline that executives can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the interventional cardiology devices market?

The market was valued at USD 19.87 billion in 2026 and is projected to reach USD 27.9 billion by 2031.

Which product segment is expanding the fastest?

Intravascular lithotripsy systems are forecast to grow at 10.75% CAGR through 2031, the highest among all product categories.

Why are ambulatory surgical centers gaining market share?

ASC growth is fueled by Medicare reimbursement for PCI, same-day discharge protocols and potential annual cost savings of USD 200–500 million once penetration reaches 50%.

How are regulatory changes in Europe affecting device availability?

The Medical Device Regulation requires more clinical evidence and post-market surveillance, extending approval timelines and increasing compliance costs for manufacturers.

What materials are expected to dominate future stent platforms?

Polymer and fully bio-resorbable scaffolds are advancing at 11.85% CAGR, driven by favorable clinical outcomes and sustainability mandates such as California’s DEHP ban.

How significant is the workforce shortage in interventional cardiology?

The United States alone is projected to face a shortfall of 8,650 cardiologists by 2037, with rural regions experiencing the most acute gaps in catheterization lab coverage.

Page last updated on: