Bioresorbable Vascular Scaffold Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

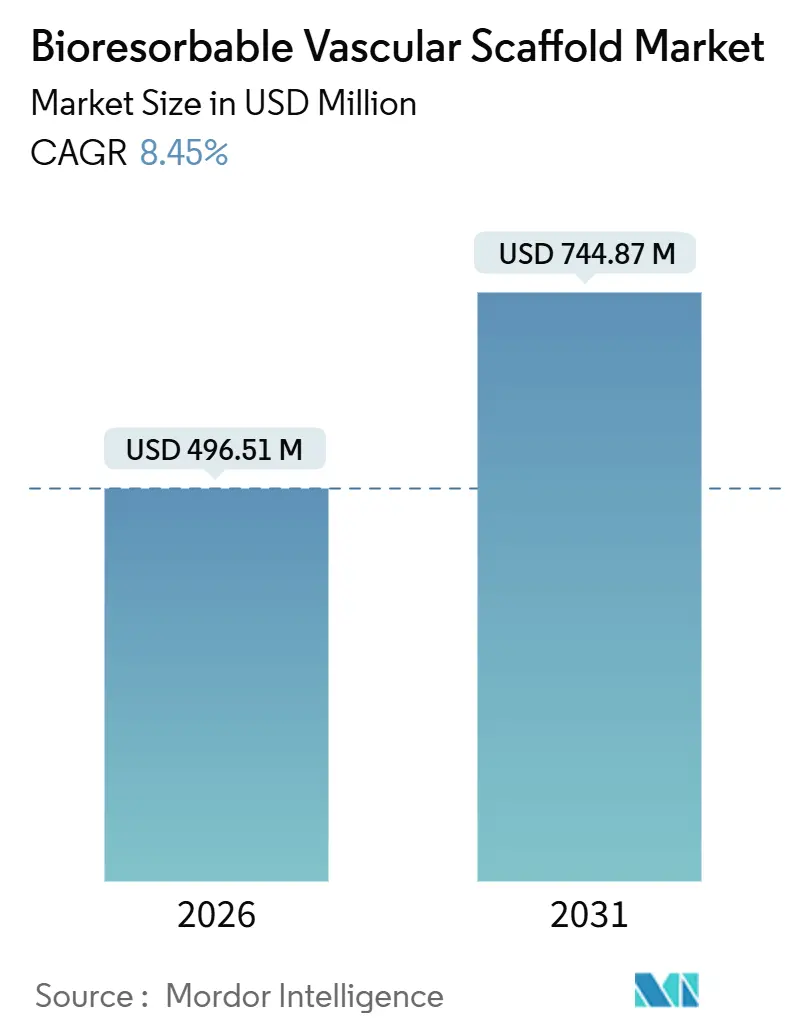

| Market Size (2026) | USD 496.51 Million |

| Market Size (2031) | USD 744.87 Million |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioresorbable Vascular Scaffold Market Analysis by Mordor Intelligence

The Bioresorbable Vascular Scaffold Market size is estimated at USD 496.51 million in 2026, and is expected to reach USD 744.87 million by 2031, at a CAGR of 8.45% during the forecast period (2026-2031).

This growth highlights a strategic transition from permanent metallic stents to advanced, fully resorbing platforms. The increasing volume of global percutaneous interventions, combined with the clinical benefits of avoiding permanent implants and expedited regulatory approvals in key markets such as the United States, China, and the United Kingdom, is driving demand. Magnesium alloy devices are gaining momentum due to their rapid 12-month resorption, while polymer platforms continue to dominate procedural volumes. Peripheral artery disease is emerging as a key application area, supported by FDA approval for below-the-knee use and clinical trial data demonstrating clear advantages over balloon angioplasty. However, market adoption is constrained by challenges such as elevated early thrombosis risks, high pricing, and the European Society of Cardiology’s 2025 advisory against routine use in coronary cases.

Key Report Takeaways

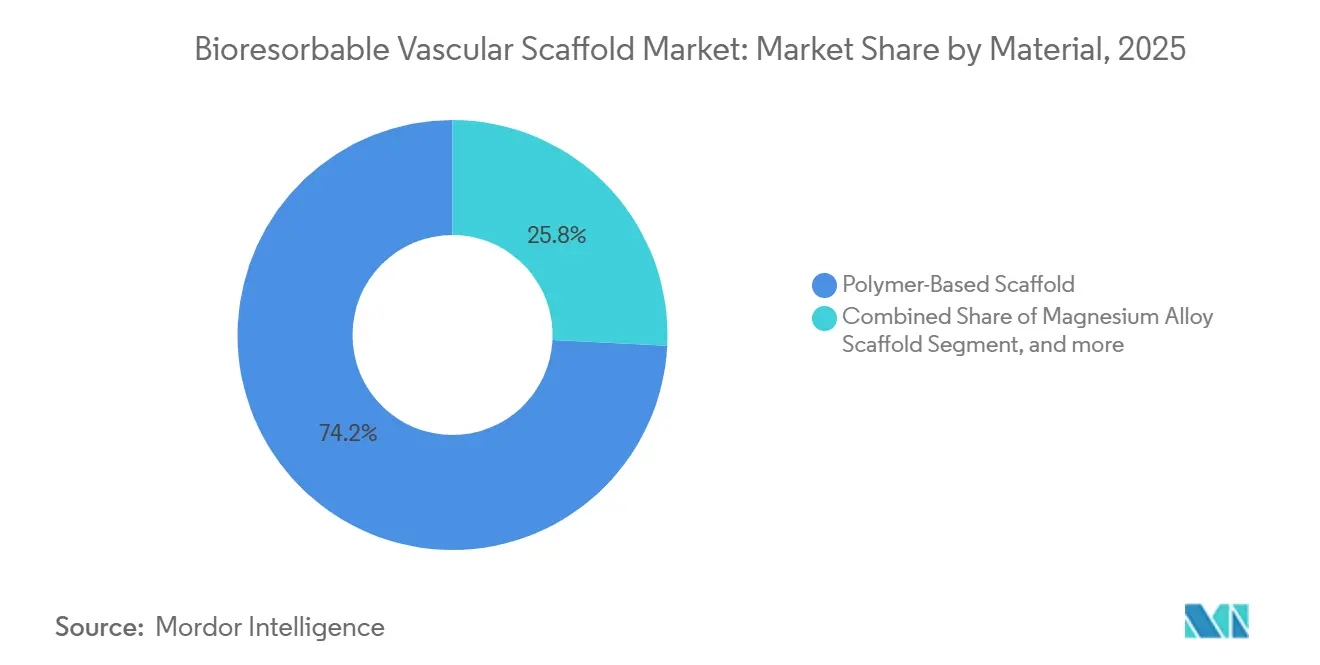

- By material, polymer scaffolds led with 74.21% of bioresorbable vascular scaffold market share in 2025; magnesium alloys are forecast to post the fastest 10.32% CAGR through 2031.

- By drug elution, drug-eluting platforms accounted for 55.76% of the 2025 revenue pool, while non-drug-eluting designs are set to expand at a 10.44% CAGR during 2026-2031.

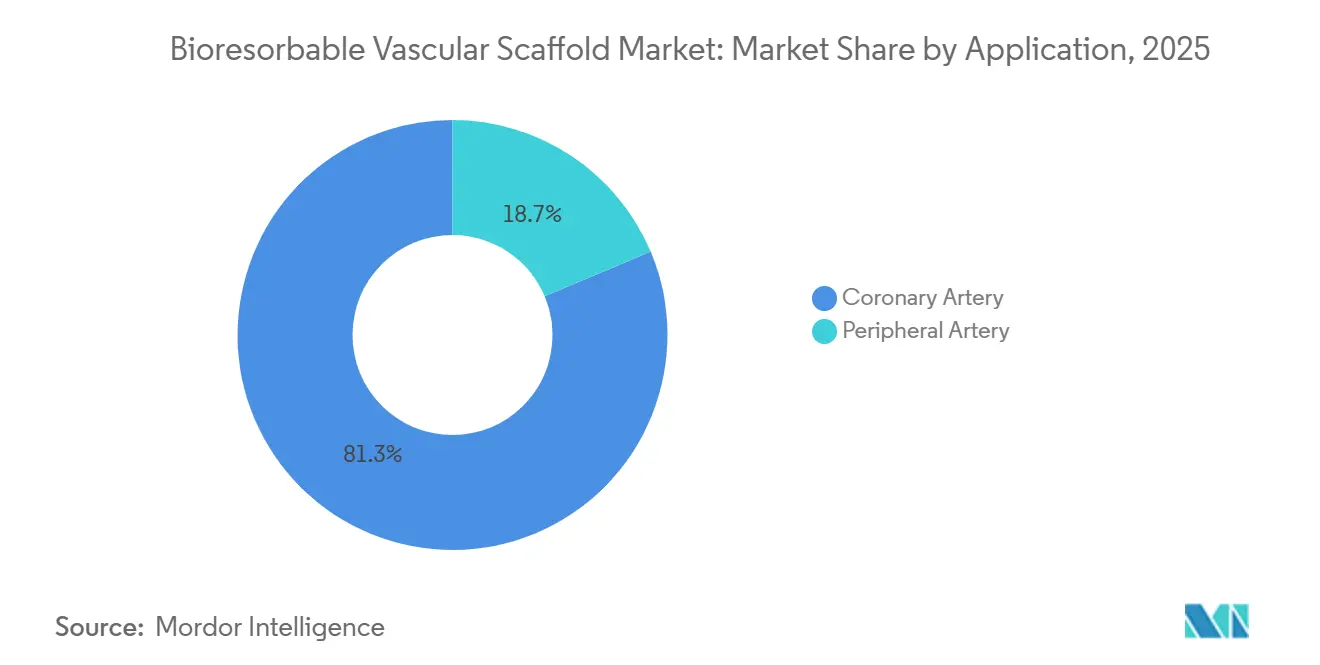

- By application, coronary arteries accounted for 81.34% of 2025 procedures; peripheral arteries are projected to have the highest 11.67% CAGR to 2031.

- By end user, hospitals controlled 58.65% of 2025 spending, whereas ambulatory care centers are on track for an 11.43% annual growth rate through the forecast horizon.

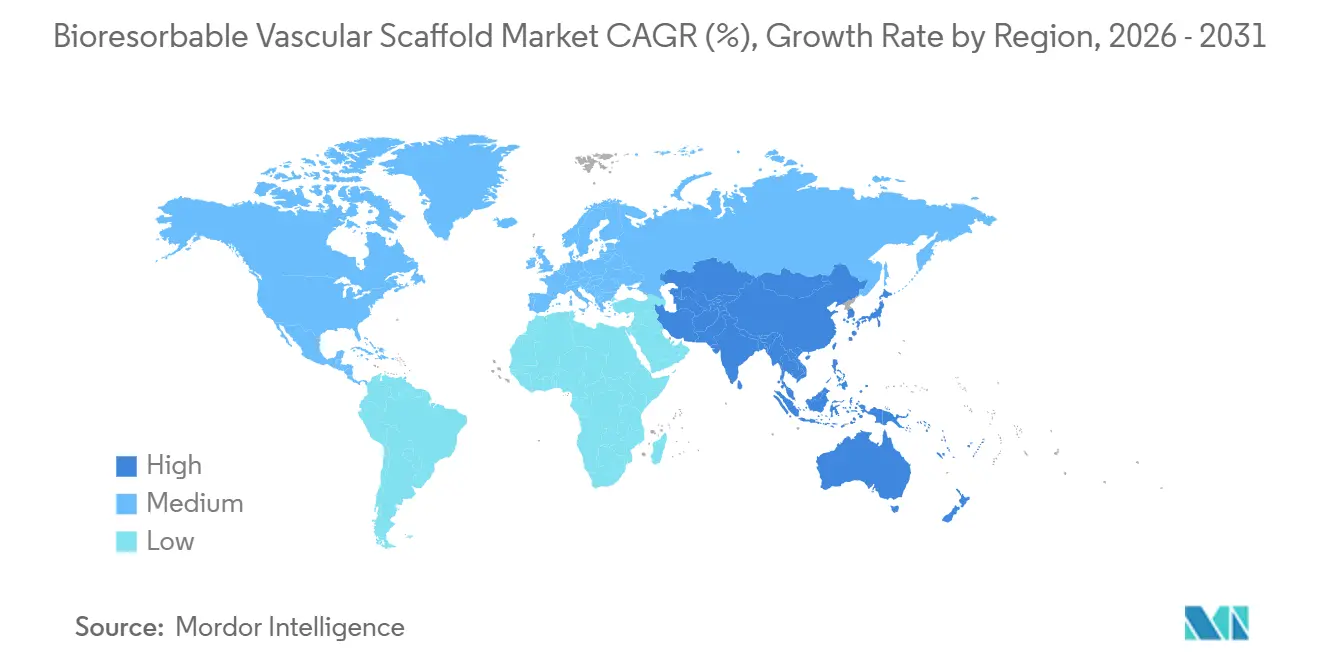

- By geography, North America accounted for 43.12% of 2025 turnover, and Asia-Pacific is projected to deliver the fastest 9.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bioresorbable Vascular Scaffold Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Cardiovascular Diseases | +2.1% | Global — highest burden in South-East Asia and Europe | Long term (≥ 4 years) |

| Shift Toward Minimally Invasive Percutaneous Interventions | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Continuous Technological Advancements in Resorbable Scaffold Materials | +1.5% | Global | Medium term (2-4 years) |

| Favorable Regulatory Initiatives for Novel Cardiovascular Devices | +1.2% | United States, Europe, China | Short term (≤ 2 years) |

| Growing Healthcare Expenditure in Emerging Economies | +1.0% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Intensifying Strategic Collaborations and R&D Investments | +0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cardiovascular Diseases

Cardiovascular disease caused 19.8 million deaths in 2022, or 32% of global mortality, with more than four-fifths of that burden in low- and middle-income nations where interventional capacity remains limited. The European Society of Cardiology Atlas 2024 reported over 3 million cardiac deaths annually across member states, equal to 37.4% of all deaths. South-East Asia logged 4.25 million cardiovascular deaths in 2021 and a hypertension prevalence of 32%, magnifying demand for percutaneous therapies. As catheterization-lab networks widen, operators are looking for devices that disappear once healing is complete, a proposition that the bioresorbable vascular scaffold market can uniquely deliver. Still, meticulous technique and prolonged dual-antiplatelet therapy remain prerequisites, potentially restraining uptake in resource-constrained settings.

Shift Toward Minimally Invasive Percutaneous Interventions

Spain’s national cath-lab registry noted that drug-coated balloons captured 14.3% of 2024 PCI cases and imaging guidance reached 10.6%, evidence of a broader pivot toward device strategies that reduce permanent metal burden[1]Spanish Society of Cardiology, “National Cardiac Catheterization Registry 2024,” secardio.es. Middle-income nations performed 1,355 PCI procedures per million people in 2024 versus 2,330 in high-income countries; the gap is closing as lab density increases. Ambulatory surgery centers now handle a growing share of elective PCI after U.S. Medicare instituted site-neutral payments, reinforcing the market advantage of temporary scaffolds that may eliminate future re-interventions. Routine use of optical coherence tomography and intravascular ultrasound helps operators size and optimize scaffold deployment, addressing malapposition, the key failure mode of first-generation devices. Mandated imaging in Biotronik’s ongoing 1,859-patient BIOMAG-II trial is likely to yield higher-quality outcomes data and could shift guidelines if favorable.

Continuous Technological Advancements in Resorbable Scaffold Materials

Magnesium alloy devices have reached 99.3% resorption at 12 months, effectively removing structural material before late adverse events accumulate. Strut thickness has fallen from 157 µm in early polymer devices to 95-120 µm in platforms such as Abbott’s Esprit BTK and Biotronik’s Freesolve, reducing flow disturbance. Iron-based designs offer 70 µm struts and stable late lumen loss over three years, balancing longevity and safety. Xeltis employs electrospun polycarbonate-urethane matrices that recruit endothelial progenitor cells for in-situ tissue formation, an approach awarded FDA Breakthrough Device status in 2024. MicroPort’s Firesorb achieved a 0.34% thrombosis rate and complete degradation within three years in pooled FUTURE trials, securing Chinese approval in 2024. Emerging consensus converges on sub-120 µm struts, 12- to 18-month resorption, and elution profiles tailored to neointimal hyperplasia.

Favorable Regulatory Initiatives for Novel Cardiovascular Devices

The FDA Breakthrough Devices Program shortened review timelines by six to 12 months for Biotronik’s Freesolve BTK and Xeltis’ aXess, underscoring U.S. commitment to innovation. China’s NMPA granted two separate approvals to MicroPort in 2024-2025, signaling a strategic tilt toward domestic innovation. The United Kingdom’s Innovative Devices Access Pathway provides conditional approvals linked to real-world evidence generation, slashing upfront trial costs. Conversely, the European Union Medical Device Regulation 2017/745 elevates evidentiary thresholds for Class III devices, extending time-to-market but offering strong post-approval differentiation. Japan’s 5-year post-market surveillance study achieved zero scaffold thrombosis by enforcing rigorous “predilate, size, post-dilate” protocols, a template that other regulators may adopt.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost Compared With Conventional Drug-Eluting Stents | -1.8% | Global — most acute in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Insufficient Long-Term Clinical Outcome Evidence | -1.5% | North America and Europe | Medium term (2-4 years) |

| Risk of Scaffold Thrombosis and Late Recoil | -1.2% | Global | Medium term (2-4 years) |

| Complex and Stringent Regulatory Approval Pathways | -1.0% | Europe, United States, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Cost Compared with Conventional Drug-Eluting Stents

Bioresorbable scaffolds can cost 30-50% more than top-tier metallic drug-eluting stents, a premium that is difficult to justify when payers focus on upfront acquisition price. China’s national procurement program has pushed coronary stent prices below USD 500, forcing scaffold makers either to accept sharp margin compression or exit the tender process. European payers bundle reimbursement for all stents in the same Diagnosis-Related Group, eliminating any price differential and reducing operator incentive to choose resorbable options. Outpatient labs, which operate on slim facility fees, often forgo stocking high-priced implants unless clear procedural advantages offset the cost delta. Pressure on list prices is set to intensify as domestic Asian suppliers scale up lower-cost magnesium and polymer lines.

Insufficient Long-Term Clinical Outcome Evidence

A pooled ABSORB analysis published in 2025 showed higher target-lesion failure and thrombosis through three years compared with everolimus-eluting metallic stents, reinforcing regulatory caution[2]Journal of the American College of Cardiology, “ABSORB Pooled Analysis 2025,” jacc.org. The AIDA trial’s five-year results found no late catch-up benefit for Absorb, challenging the premise that vessel restoration improves outcomes beyond scaffold resorption. Japan’s flawless five-year registry relied on mandatory pre- and post-dilation, plus optical coherence tomography, in 91.4% of cases, a protocol unlikely to be replicated in routine practice. BIOMAG-II will not report until 2027, leaving a multi-year evidence gap during which payers could harden restrictive coverage policies. Mandatory post-market follow-up under EU-MDR further burdens sponsors with surveillance costs and the risk of label changes if real-world events accumulate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Magnesium Alloys Narrow Polymer’s Lead

Polymer platforms captured 74.21% of the 2025 bioresorbable vascular scaffold market, buoyed by a long clinical track record, whereas magnesium alloys are projected to deliver the fastest 10.32% CAGR through 2031. Polymer scaffolds retain radial strength longer, helpful in calcified or recoil-prone lesions, yet their two- to three-year degradation prolongs exposure to thrombosis. Magnesium dissolves within 12 months, narrowing the risk window and aligning with vessel healing; Biotronik’s Freesolve showed 99.3% resorption at 1 year, with no new failures through year 3.

Iron-based devices featuring 70 µm struts sit between slow-degrading polymers and fast-resorbing magnesium, offering steady lumen maintenance over 3 years. MicroPort’s Firesorb polymer scaffold logged a 0.34% thrombosis rate across FUTURE trials and gained Chinese approval mid-2024. Xeltis’ polycarbonate-urethane matrix introduces a tissue-engineering mechanism rather than simple dissolution. Technology roadmaps across the bioresorbable vascular scaffold market converge on sub-120 µm struts, one-year resorption, and clinically proven anti-proliferative drug elution.

By Drug Elution: Non-Eluting Variants Gain in Peripheral Territories

Drug-eluting designs held 55.76% of 2025 revenue, dominating coronary practice. Still, non-drug-eluting scaffolds are poised for a 10.44% CAGR, driven by peripheral and below-the-knee uses that prioritize mechanical support. Abbott’s Esprit BTK, a non-drug platform, delivered 74% primary efficacy versus 44% for balloon angioplasty in LIFE-BTK, prompting FDA clearance in 2024[3]New England Journal of Medicine, “LIFE-BTK Trial,” nejm.org. Coronary applications still rely on sirolimus- or everolimus-eluting stents to curb neointimal hyperplasia, yet Europe’s 2025 ESC statement discourages routine coronary use of resorbables due to elevated thrombosis rates.

Biotronik’s Freesolve BTK, also drug-free, secured Breakthrough Device status in March 2024 and targets critical limb ischemia. Japan’s registry achieved zero thrombosis through disciplined technique rather than pharmacology, bolstering confidence in non-drug variants where meticulous deployment is practical. As the bioresorbable vascular scaffold market matures, manufacturers may sustain dual portfolios—drug-eluting for coronaries, drug-free for peripheral arteries—to serve divergent clinical philosophies.

By Application: Peripheral Arteries Outpace Coronary Growth

Coronary arteries accounted for 81.34% of 2025 procedures, but peripheral indications are forecast to grow at a 11.67% CAGR, outpacing coronary growth. FDA’s first-in-class approval of Esprit BTK ignited physician interest in below-the-knee critical limb ischemia, a segment with limited durable options. The LIFE-BTK trial’s number needed to treat of 4 underscores a compelling payer value proposition.

Peripheral operators face fewer deployment constraints than coronary specialists, making rapid adoption of techniques plausible in community hospitals and ambulatory centers. Reva Medical’s MOTIV scaffold reported 90% six-month patency, and R3 Vascular’s MAGNITUDE achieved 93% efficacy, adding momentum to a widening pipeline. Coronary adoption remains hampered by clinical society caution and stringent imaging requirements, illustrating the bifurcation within the bioresorbable vascular scaffold market.

By End-User: Ambulatory Centers Capture Elective Volume

Hospitals generated 58.65% of 2025 revenue, anchored in acute myocardial infarction care, yet ambulatory centers are forecast to grow by 11.43% as site-neutral U.S. payment policies spur migration of elective PCI. Imaging utilization rose by two percentage points in Spain during 2024, illustrating how improved visualization streamlines complex scaffolding in lower-acuity settings.

Cardiac specialty centers sit between hospitals and ambulatory labs, often running pivotal trials such as BIOMAG-II, and supplying experienced operators for high-end device launches. Manufacturers will need segmented commercial strategies: in-depth training and outcome tracking for hospitals, streamlined inventory, and rapid case-turnover support for outpatient facilities.

Geography Analysis

North America accounted for 43.12% of 2025 turnover, as the FDA issued landmark approvals for Abbott’s Esprit BTK and granted Breakthrough status to multiple next-generation platforms, providing predictable, expedited pathways. Early-adopter physician networks, mature cath-lab infrastructure, and payer acceptance of premium technology support continued leadership, although Europe’s conservative guidance tempers coronary enthusiasm.

Europe contends with EU-MDR Class III stringency, which demands robust clinical and post-market evidence but affords a competitive edge to compliant innovators. Biotronik’s CE-marked Freesolve showcases strong 12-month resorption and favorable three-year outcomes. Cath-lab density disparities are narrowing as regional governments fund cardiac-care capacity, enhancing future volume potential.

Asia-Pacific is projected for the swiftest 9.54% CAGR, propelled by China’s dual NMPA approvals for Firesorb and a rapamycin-eluting scaffold, underscoring Beijing’s pivot toward self-sufficiency. Price ceilings under volume-based procurement intensify competition but broaden accessibility. Japan’s impeccable five-year outcomes confirm that disciplined implantation can overcome early-generation safety concerns. India, Australia, and South Korea are expanding reimbursement codes, while emerging markets in the Middle East, Africa, and South America await infrastructure build-out and payer reform to unlock latent demand.

Competitive Landscape

Market concentration is moderate, anchored by Abbott, Biotronik, and Shanghai MicroPort, each leveraging distinctive material science and regional regulatory wins. Strategy clusters around material choice (polymer, magnesium, iron), anatomical focus (coronary versus peripheral), and regulatory acceleration (Breakthrough designations, CE marking, or NMPA priority). Abbott’s Esprit BTK validates peripheral opportunity; Biotronik’s magnesium portfolio targets both coronary and below-the-knee arteries; MicroPort’s rapid Chinese approvals underscore a domestic champion model.

Disruptors include Xeltis, whose tissue-engineering matrix secured U.S. Breakthrough status and entered pivotal enrollment in 2024. U.S. and Chinese players invest aggressively in thinner struts, faster degradation, and predictive imaging protocols to match Japan’s zero-thrombosis registry. The bioresorbable vascular scaffold market will pivot decisively once one or more platforms achieve sustained sub-1% thrombosis and non-inferior late outcomes compared with best-in-class metallic drug-eluting stents.

Bioresorbable Vascular Scaffold Industry Leaders

Abbott

Biotronik

Terumo Corporation

Elixir Medical

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: StentIt launched first-in-human trial of bioresorbable stent to treat below-the-knee chronic limb-threatening ischaemia (CLTI).

- February 2024: BIOTRONIK announced tCE approval and the launch of the he CE approval and launch of Freesolve Resorbable Magnesium Scaffold (RMS). This third-generation RMS has been engineered to provide optimized vessel support, yet achieves magnesium resorption within 12 months.

- February 2023: Zeus, one of the global leaders in advanced polymer solutions, developed Absorv XSE oriented tubing, the newest member of the company’s family of bioabsorbable products. Available in a variety of resins and expanded size ranges, Absorv XSE provides a highly customizable platform for design and offers an alternative to metallic products implanted permanently in the human body.

Global Bioresorbable Vascular Scaffold Market Report Scope

As per the scope of the report, a bioresorbable vascular scaffold (BVS) is a temporary stent made from biodegradable materials that supports a blood vessel after angioplasty. It gradually dissolves or is absorbed by the body, reducing the risk of long-term complications. BVS is used to restore blood flow in patients with coronary artery disease while minimizing the permanent presence of a device.

The Bioresorbable Vascular Scaffold Market is Segmented by Material (Polymer-Based Scaffold, Magnesium Alloy Scaffold, and Other Metal Scaffold), Drug Elution (Drug-Eluting Scaffold and Non-Drug-Eluting Scaffold), Application (Coronary Artery and Peripheral Artery), End-User (Hospitals, Ambulatory Care Centers, Cardiac Centers, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Polymer-Based Scaffold |

| Magnesium Alloy Scaffold |

| Other Metal Scaffold |

| Drug-Eluting Scaffold |

| Non-Drug-Eluting Scaffold |

| Coronary Artery |

| Peripheral Artery |

| Hospitals |

| Ambulatory Care Centers |

| Cardiac Centers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Material | Polymer-Based Scaffold | |

| Magnesium Alloy Scaffold | ||

| Other Metal Scaffold | ||

| By Drug Elution | Drug-Eluting Scaffold | |

| Non-Drug-Eluting Scaffold | ||

| By Application | Coronary Artery | |

| Peripheral Artery | ||

| By End-User | Hospitals | |

| Ambulatory Care Centers | ||

| Cardiac Centers | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the bioresorbable vascular scaffold market in 2026?

The bioresorbable vascular scaffold market size stands at USD 496.51 million in 2026.

What is the growth outlook for magnesium alloy scaffolds?

Magnesium platforms are forecast to expand at a 10.32% CAGR through 2031 on the strength of rapid one-year resorption and favorable mid-term outcomes.

Which region is set to grow fastest through 2031?

Asia-Pacific is projected to record a 9.54% CAGR, propelled by dual Chinese regulatory approvals and expanding cath-lab infrastructure.

Why are ambulatory surgery centers important for future adoption?

Site-neutral reimbursement and simplified imaging protocols favor outpatient labs, where scaffold procedures can capitalize on same-day discharge efficiency.

What data gap still limits broad coronary adoption?

Long-term randomized evidence demonstrating non-inferiority to metallic drug-eluting stents beyond three years remains limited; key trials will report after 2027.

How does EU-MDR affect new scaffold launches?

EU-MDR Class III classification imposes stricter clinical and post-market requirements, extending timelines but offering differentiation to compliant devices.

Page last updated on: