Cardiac Sutures Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

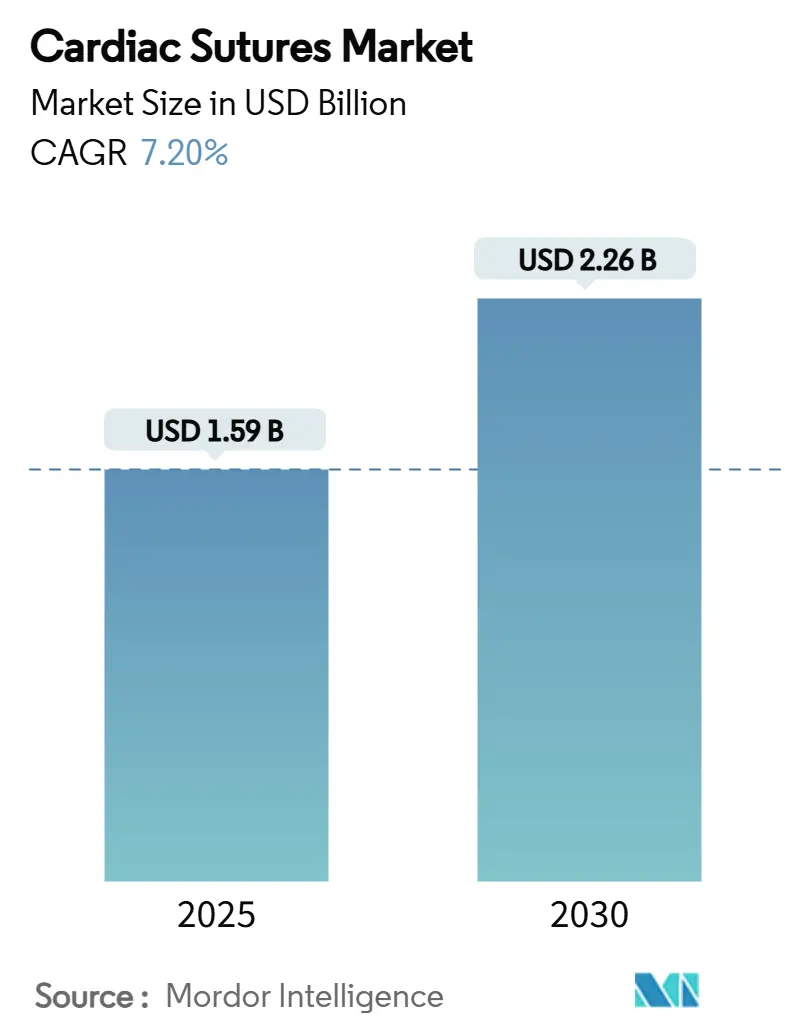

| Market Size (2025) | USD 1.59 Billion |

| Market Size (2030) | USD 2.26 Billion |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

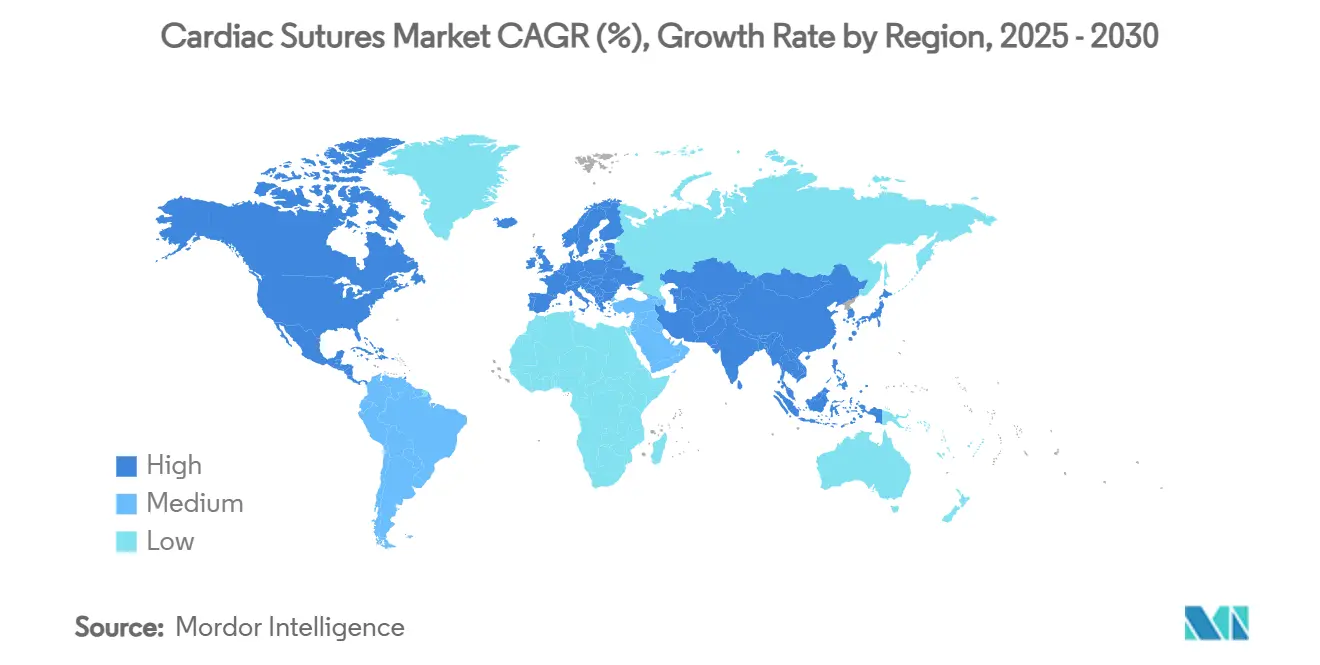

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Sutures Market Analysis by Mordor Intelligence

The cardiac sutures market size stands at USD 1.59 billion in 2025 and is projected to reach USD 2.26 billion by 2030, reflecting a 7.2% CAGR. Robust demand arises from the growing global cardiovascular disease burden, swift adoption of minimally invasive and robotic-assisted procedures, and continuous advances in absorbable and smart bio-resorbable materials. Hospitals continue to account for the bulk of surgical volumes, yet ambulatory surgery centers (ASCs) are capturing complex cases as reimbursement structures mature. Suppliers also benefit from the material shift toward ultra-fine ePTFE and drug-eluting bio-resorbable yarns that command premium pricing. In parallel, regulatory scrutiny around high-risk devices is tightening, raising both entry barriers and product quality expectations.

Key Report Takeaways

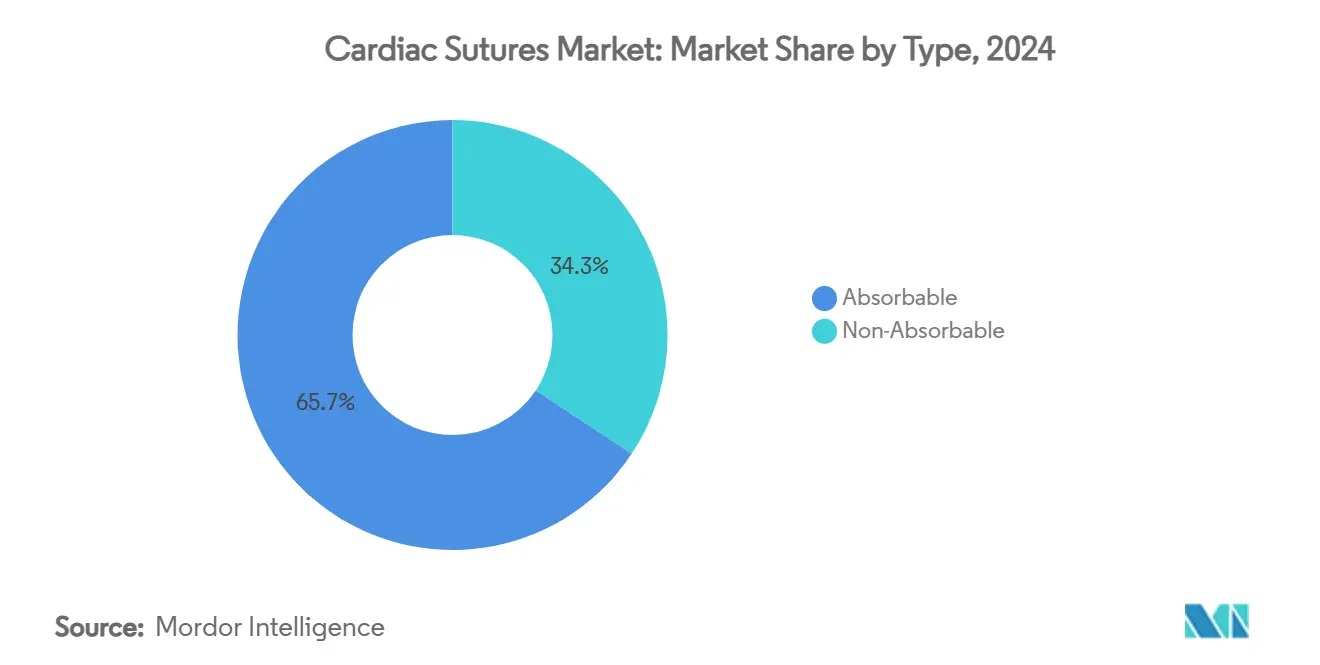

- By type, absorbable sutures led with 65.7% revenue share in 2024, while smart bio-resorbable sutures are advancing at a 9.4% CAGR through 2030.

- By material, polyester retained 28.6% share in 2024; ePTFE is the fastest-growing material at a projected 10.1% CAGR to 2030.

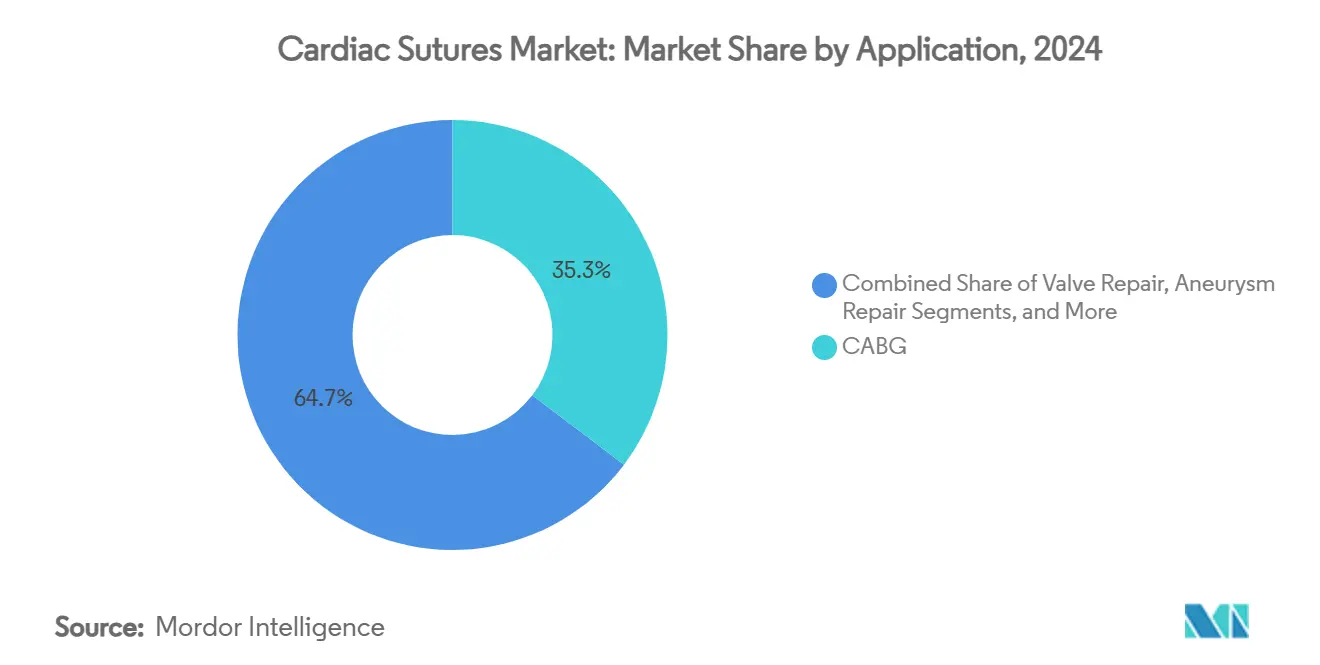

- By application, coronary artery bypass grafting accounted for a 35.3% share of the cardiac sutures market size in 2024, whereas aneurysm repair and valve surgery are forecast to expand at an 8.7% CAGR between 2025-2030.

- By end user, hospitals represented 80.2% of total consumption in 2024, while ASCs are on track for a 7.9% CAGR over the same period.

- By region, North America led with 48.5% revenue share in 2024, while Asia Pacific is projected to expand at a 7.2% CAGR between 2025-2030.

Global Cardiac Sutures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Cardiovascular Diseases & Surgical Volumes | +1.80% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Aging Population Driving Higher Open-Heart Procedures | +1.50% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Technological Advances In Absorbable & Barbed Cardiac Sutures | +1.20% | North America & EU leading, Asia Pacific following | Medium term (2-4 years) |

| Shift Toward Minimally Invasive & Robot-Assisted Cardiac Surgery | +1.00% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Emergence Of Smart Bio-Resorbable Sutures With Micro-Sensors | +0.80% | North America & Europe early adoption, global expansion | Medium term (2-4 years) |

| Off-Pump CABG Growth Requiring Ultra-Fine EPTFE Sutures | +0.50% | Global, with concentration in advanced cardiac centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular Diseases

Clinical cardiovascular disease is projected to affect 45 million U.S. adults by 2050, up from 11.3% to 15.0% prevalence.[1]Dominique Vervoort, “Global Cardiac Surgical Volume and Gaps,” Annals of Thoracic Surgery Short Reports, atssr.org Coronary artery bypass grafting already exceeded 160,000 isolated procedures in 2019, and global surgical demand in high-income countries averages 123.2 interventions per 100,000 population. Rising hypertension rates and diabetes prevalence further enlarge the candidacy for complex cardiac repair. In low- and middle-income economies, public health planning now targets 61.6 procedures per 100,000 population, signaling sizable untapped volume. The result is consistent upward pressure on the cardiac sutures market as every open or minimally invasive repair requires multiple strands for anastomosis and tissue approximation.

Aging Population Elevating Open-Heart Procedures

Patients aged 65 and above will represent more than half of cardiovascular admissions by 2035, with valve interventions growing 106% in this cohort. A tertiary European center projects 51-67 additional surgical aortic valve replacements annually by 2041, underscoring mounting caseloads.[2]Rafael Maniés Pereira, “Predicting the Burden for Surgical Aortic Valve Replacement in a Tertiary Centre: The Impact of Aged Populations for the Next Decades,” Journal of Clinical Medicine, mdpi.com Elderly physiology brings fragile tissue and comorbidities, driving the selection of sutures that minimize inflammatory response and accelerate endothelialization. Specialized heart-valve teams in Europe increasingly standardize premium absorbable and barbed sutures, further enlarging high-value demand.

Advances in Absorbable & Barbed Sutures

Next-generation filaments integrate antimicrobial coatings, drug-eluting layers, or real-time sensors for infection monitoring. Researchers at MIT have 3D-printed bioadhesive leads that remove the need for knot tying altogether, demonstrating the convergence of electronics and suture science. Bioabsorbable mechanoelectric fibers also create micro-electrical stimulation that promotes cell migration and angiogenesis before degrading inside the body. Combined, such innovations are steering surgeons toward smart bio-resorbable lines that command higher average selling prices and expand the cardiac sutures market.

Shift to Minimally Invasive & Robotic-Assisted Surgery

Robotic coronary artery bypass grafting records 0.6% 30-day mortality and hospital stays of 3.8 days, improving on conventional techniques.[3]Bridget Hwang, “Systematic Review and Meta-Analysis of Robotic CABG Outcomes,” Annals of Cardiothoracic Surgery, annalscts.com Uptake of robotic mitral repair now captures 15% of U.S. volumes, and global programs are scaling training to reduce learning curves. Robots require ultra-fine ePTFE or 7-0 polypropylene suture packs that can pass through limited port access and sustain complex graft geometry. High procedural precision elevates demand for equal precision in suture manufacturing, driving a mix shift toward advanced materials within the cardiac sutures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Suture-Less Valves & Tissue Adhesives | -0.80% | North America & Europe leading adoption | Medium term (2-4 years) |

| Regulatory Recalls & Stringent Approval Pathways | -0.60% | Global, with strictest impact in US & EU | Short term (≤ 2 years) |

| Price Pressure From Generic Suture Manufacturers | -0.40% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| PFAS-Linked Supply-Risk For High-Performance Fluoropolymers | -0.30% | Europe leading, North America following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Suture-Less Valves & Tissue Adhesives

Transcatheter aortic procedures rose from 4,666 cases in 2012 to nearly 98,504 in 2022, whereas surgical valve replacements shrank by 36%. Edwards Lifesciences’ RESILIA tissue shows 99.3% freedom from deterioration at eight years, lowering the revision burden that typically requires multiple sutures. Catheter-based tricuspid and peripheral scaffolds from Abbott further bypass suturing altogether, tightening the addressable segment for traditional lines.

Regulatory Recalls & Stringent Approval Pathways

Class I recalls for cardiovascular devices—such as the Varipulse ablation catheter—highlight a 3% stroke incidence versus the expected 1% benchmark, spurring heightened oversight. The FDA has already instructed providers to halt use of certain heart devices over safety concerns. Manufacturers must now deliver more extensive post-market surveillance data, prolonging time-to-market for new suture innovations and inflating compliance costs across the cardiac sutures market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Absorbable Retains Scale as Smart Resorbables Accelerate

Absorbable sutures represented 65.7% of revenue in 2024, reflecting surgeon preference for materials that do not require removal and reduce infection risk. Smart bio-resorbable lines are projected to grow 9.4% annually to 2030, fueled by embedded sensors and antimicrobial coatings that transform closure threads into active therapeutic platforms. Non-absorbable filaments remain indispensable for pediatric and transplant settings that demand enduring tensile strength. The cardiac sutures market share commanded by absorbable products is therefore secure in volume, although premium value growth shifts to sensor-enabled formats.

Electrospinning and 3D printing now allow custom yarn diameters for minimally invasive robotic ports, creating differentiated supply chains. Drug-eluting versions deliver hemostatic agents directly into the anastomosis, reducing intraoperative bleed-back and elevating surgeon confidence. As clinical evidence mounts, procurement committees increasingly approve higher unit prices, reinforcing revenue per procedure. Meanwhile, non-absorbables such as PTFE and polypropylene continue to serve re-operations where permanent support is essential, ensuring portfolio breadth across the cardiac sutures market.

By Material: ePTFE Challenges Polyester Leadership

Polyester maintained a 28.6% foothold in 2024 owing to proven biocompatibility and broad procedural familiarity. Surgeons, however, are gravitating toward ultra-fine ePTFE that enables delicate threading through calcified vessels and small port sites, driving a 10.1% CAGR forecast. PFAS-related regulation in Europe introduces supply-chain uncertainty, prompting R&D into fluorine-free alternatives without sacrificing pliability or knot security. In procedures such as robotic minimally invasive direct CABG, 7-0 polypropylene Prolene sutures remain the standard of care, illustrating the heterogeneous material needs within the cardiac sutures market.

Polyglactin and nylon occupy niche roles in patch closure and pediatric septal repair, while albumin-based composites in early trials promise improved endothelial integration. Johnson & Johnson’s HEMO-SEAL technology, which reduces anastomotic bleeding, demonstrates how incumbent vendors refresh legacy lines to defend their share. As hospitals tighten supplier qualification criteria, reliable traceability in material sourcing is becoming a competitive differentiator.

By Application: CABG Leads, Valve and Aneurysm Work Gains Tempo

Coronary artery bypass grafting held a 35.3% revenue slice in 2024 and continues to anchor demand as multivessel disease persists despite improvements in stenting. Aneurysm and valve repairs, however, are poised for the fastest 8.7% CAGR due to aging demographics and complementary transcatheter strategies that enlarge the surgical candidate pool rather than cannibalize it. Smart bio-resorbable sutures deliver localized drug therapy that shortens healing times in valve-sew-on pledgets, creating a secondary upsell in high-value cases.

Congenital heart defect repair and transplantation remain smaller but critically important segments characterized by intricate anatomies. Here, the cardiac sutures market size for pediatric grafts is forecast to rise steadily as long-term survival rates improve. Surgeon preference for low-memory, high-knot-security yarns means suppliers must sustain R&D investment to address diverse structural demands across procedures.

By End User: Hospitals Dominate but ASCs Emerge

Hospitals consumed 80.2% of cardiac sutures in 2024 because advanced imaging, perfusion support, and post-operative care remain largely inpatient. Yet ASCs are registering the sharpest 7.9% CAGR, buoyed by Medicare’s decision to reimburse higher-acuity cardiovascular procedures in outpatient settings. Five new cardiology ASCs opened in 2024 alone, each anchoring demand for sterilized single-use suture kits. Direct-pay models adopted by private equity-backed centers could compress pricing, requiring vendors to create tiered portfolios balancing cost with performance.

Cardiac specialty hospitals and academic institutes act as incubators for smart bio-resorbable trials and niche materials. Their feedback loops inform broader commercial roll-outs. Over the next five years, suppliers expect revenue diversification as procedure migration blurs historic boundaries between inpatient and outpatient consumption patterns within the cardiac sutures market.

Geography Analysis

North America retained leadership in 2024 due to 96% graft patency for robotic CABG, reduced average stays of 3.8 days, and comprehensive insurance coverage for high-complexity surgeries. The United States alone has 127.9 million adults living with some form of heart disease, driving a stable flow of open and minimally invasive procedures. Stringent FDA oversight, however, continues to delay certain launches, compelling vendors to strengthen clinical dossiers before commercialization.

Europe benefits from structured Heart Team protocols and aging demographics that sustain procedure volumes. PFAS regulation is prompting accelerated R&D spending in Ireland and Germany as manufacturers hedge against potential ePTFE shortages. Multi-center robotic programs across Germany, France, and the United Kingdom are fueling demand for ultra-fine barbed sutures compatible with wristed instruments.

Asia Pacific is the fastest-growing territory, propelled by the surging prevalence of heart failure in China, Indonesia, and Malaysia. Increasing healthcare spending and medical tourism initiatives in India and Thailand bolster investment in cardiac theaters. Hospitals in these markets are leapfrogging older material generations, moving straight to sensor-enabled and drug-eluting lines, thereby accelerating value growth across the cardiac sutures market.

Competitive Landscape

The global playing field is moderately consolidated: the top five companies command just under 70% share, leaving room for regional specialists. Johnson & Johnson has earmarked USD 31.35 billion of a USD 148 billion MedTech budget specifically for cardiology platforms, signaling a long-run commitment to suture innovation. Teleflex’s EUR 760 million purchase of Biotronik’s vascular arm adds drug-coated balloon and scaffold technologies that complement high-margin suture offerings. KKR’s USD 838.6 million acquisition of Healthium MedTech highlights private equity's appetite for scale in emerging markets.

Product differentiation now centers on smart sutures with bioresorbable matrices, embedded diagnostics, and localized drug delivery. MIT’s bioadhesive pacing lead introduces a suture-free paradigm for select implantable devices, emphasizing disruptive threats from academic spin-offs. Meanwhile, traditional players refine portfolio resilience by adding hemostatic coatings and barbed variants that cut closure time.

Supply-chain risk tied to PFAS regulation is forcing dual-sourcing of fluoropolymers and accelerated testing of non-fluorinated alternatives. Vendors that can demonstrate compliant production while sustaining knot security are poised to gain share as regulatory headwinds intensify.

Cardiac Sutures Industry Leaders

Johnson & Johnson

Medtronic plc

B. Braun Melsungen AG

Teleflex Incorporated

W. L. Gore & Associates

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed the acquisition of Biotronik’s Vascular Intervention business for EUR 760 million, adding resorbable scaffold assets.

- April 2025: Abbott secured FDA approval for the Esprit BTK resorbable scaffold, the first dissolving stent for below-knee arteries.

- March 2025: Johnson & Johnson MedTech launched the DUALTO energy system with adaptive tissue response features.

Global Cardiac Sutures Market Report Scope

| Absorbable Cardiac Sutures |

| Non-Absorbable Cardiac Sutures |

| Polypropylene |

| ePTFE (Expanded PTFE) |

| Polyester |

| Polyglactin 910 (Vicryl) |

| Nylon |

| Coronary Artery Bypass Grafting (CABG) |

| Valve Repair & Replacement |

| Aneurysm & Aortic Repair |

| Congenital Heart Defect Repair |

| Heart Transplantation & Assist Devices |

| Hospitals |

| Cardiac Specialty Centers |

| Ambulatory Surgery Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Absorbable Cardiac Sutures | |

| Non-Absorbable Cardiac Sutures | ||

| By Material | Polypropylene | |

| ePTFE (Expanded PTFE) | ||

| Polyester | ||

| Polyglactin 910 (Vicryl) | ||

| Nylon | ||

| By Application / Procedure | Coronary Artery Bypass Grafting (CABG) | |

| Valve Repair & Replacement | ||

| Aneurysm & Aortic Repair | ||

| Congenital Heart Defect Repair | ||

| Heart Transplantation & Assist Devices | ||

| By End User | Hospitals | |

| Cardiac Specialty Centers | ||

| Ambulatory Surgery Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the cardiac sutures market in 2025?

The cardiac sutures market size is USD 1.59 billion in 2025 with a 7.2% CAGR projected through 2030.

Which suture type is growing the fastest?

Smart bio-resorbable sutures are expanding at a 9.4% CAGR because they integrate sensors and drug-eluting properties.

What material will lead growth through 2030?

EPTFE is forecast to grow 10.1% annually as surgeons favor ultra-fine filaments for robotic and minimally invasive procedures.

Why are ASCs important for cardiac sutures suppliers?

ASCs are registering a 7.9% CAGR as more complex cardiovascular procedures shift to outpatient settings, broadening demand beyond hospitals.

How do PFAS regulations impact supply?

Planned PFAS restrictions in Europe could limit ePTFE availability, prompting manufacturers to develop alternative materials to ensure uninterrupted suture production.

Page last updated on: