Cabinet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

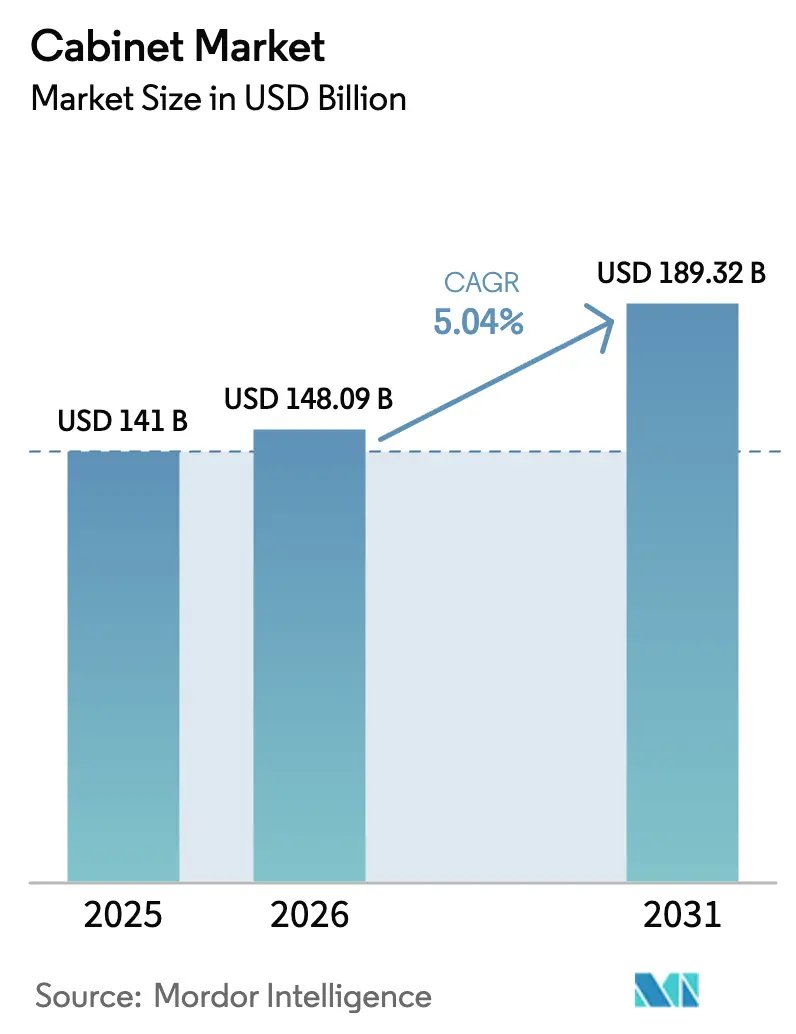

| Market Size (2026) | USD 148.09 Billion |

| Market Size (2031) | USD 189.32 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

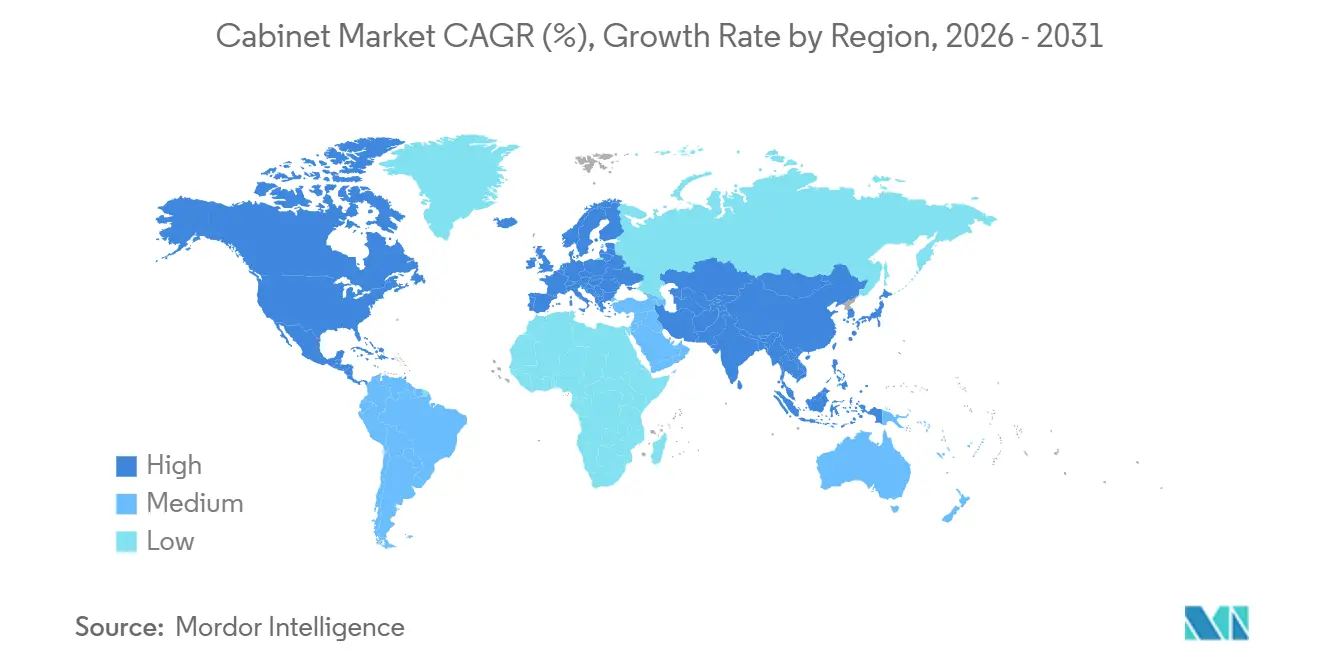

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cabinet Market Analysis by Mordor Intelligence

The cabinet market size is expected to grow from USD 141 billion in 2025 to USD 148.09 billion in 2026 and is forecast to reach USD 189.32 billion by 2031 at a 5.04% CAGR over 2026-2031. The cabinet market includes kitchen cabinets, bathroom vanities, and other storage systems for residential and commercial settings, with growth underpinned by product mix shifts, channel realignment, and regulatory and design influences that shape purchasing behavior and competitive positioning. Demand is being pulled forward by remodel activity, modular and frameless adoption in constrained urban layouts, and a rising share of online discovery and purchase journeys that are reshaping the cost-to-serve curve for manufacturers and retailers. Mix effects are visible in the faster growth of ready-to-assemble lines, the sustained dominance of wood materials alongside a catch-up in metal-based outdoor installations, and the ongoing pivot of commercial buyers toward standardized, durable solutions that shorten installation cycles. Global supply chains remain sensitive to tariffs, input cost swings, and certification requirements, which collectively steer the cabinet market toward compliant materials, energy-efficient processes, and verifiable chain-of-custody documentation for wood inputs.

Key Report Takeaways

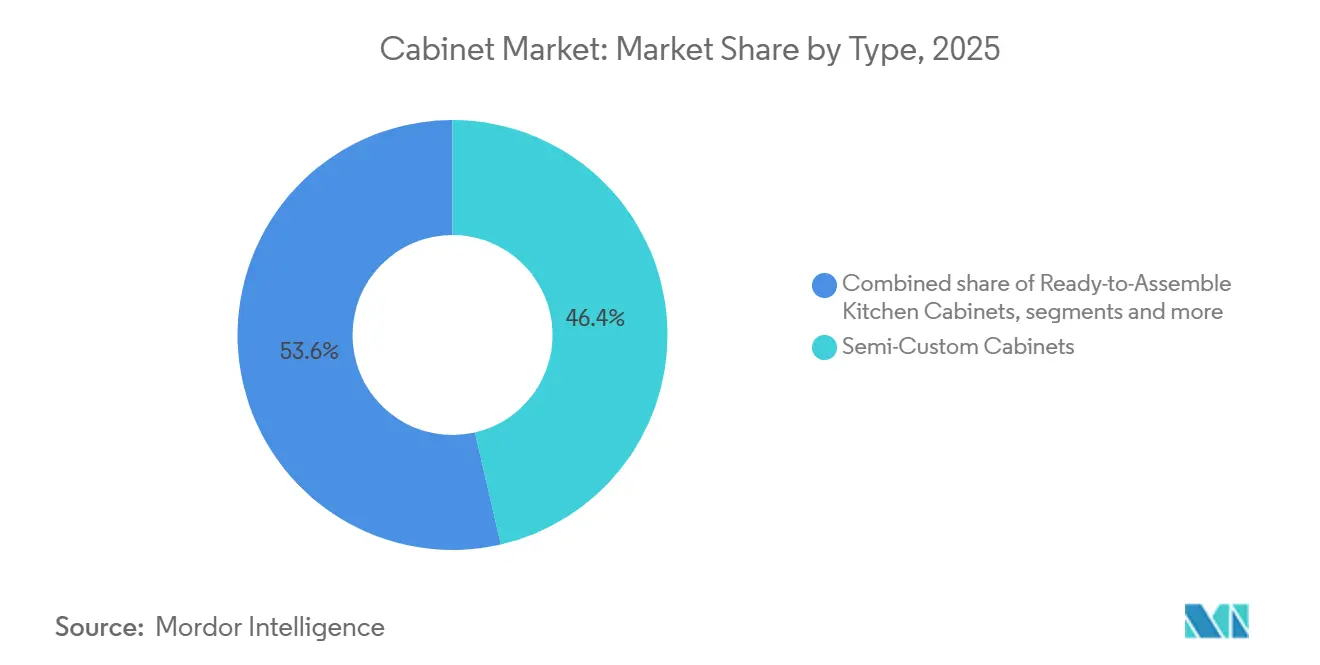

- By type, semi-custom configurations led with a 46.39% market share in 2025, the highest cabinet market share among product types. The cabinet market size for ready-to-assemble configurations is projected to expand at a 7.26% CAGR through 2031.

- By application, kitchen cabinets accounted for a 69.39% share in 2025, the largest cabinet market share by application. The cabinet market size for bathroom cabinets is forecast to grow at a 7.87% CAGR through 2031.

- By material, wood held a 71.84% share in 2025, the leading cabinet market share by material. The cabinet market size for metal cabinetry is projected to grow at a 6.37% CAGR through 2031.

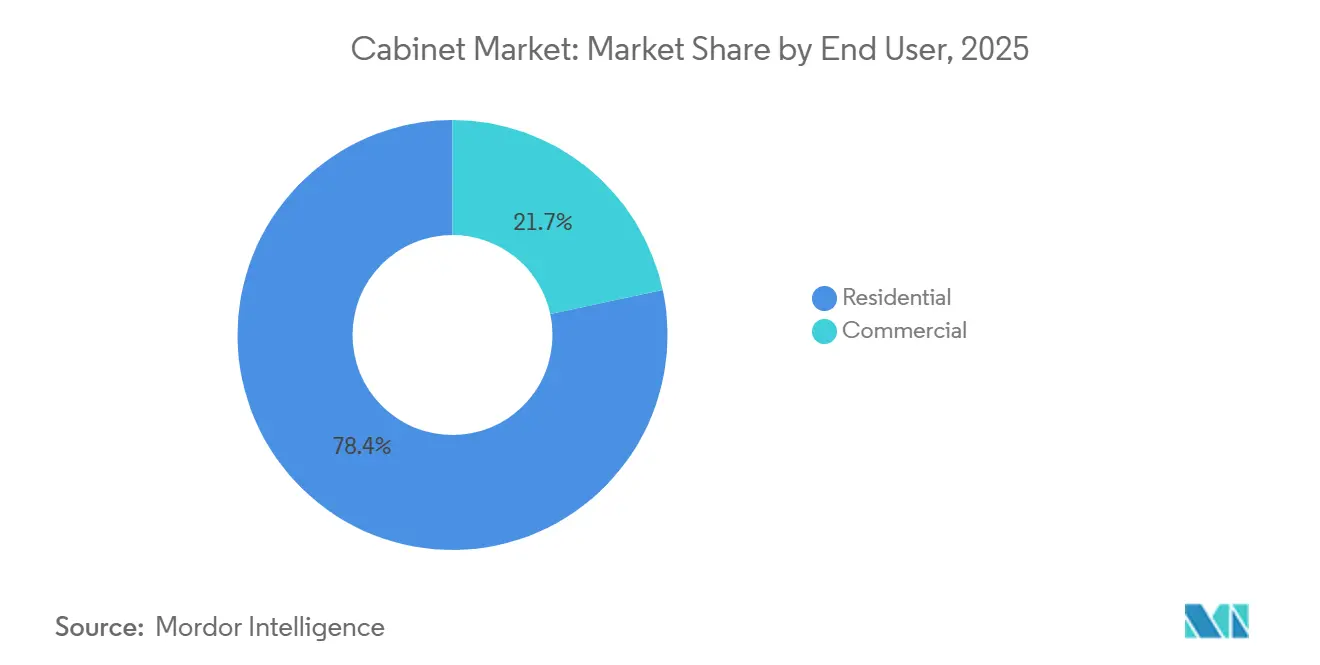

- By end user, residential accounted for a 78.35% share in 2025, the largest cabinet market share by end user. The cabinet market size for commercial projects is expected to grow at an 8.24% CAGR through 2031.

- By distribution channel, offline held a 66.36% share in 2025, the highest cabinet market share by channel. The cabinet market size for online channels is projected to grow at a 9.39% CAGR through 2031.

- By geography, North America led with a 38.39% share in 2025, the largest cabinet market share by region. The cabinet market size for Asia-Pacific is forecast to expand at an 8.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cabinet Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread shift toward frameless and modular kitchen layouts | +1.3% | Europe, North America, APAC | Medium term (2–4 years) |

| Multifamily construction boom and renovation uptick favoring stock and RTA lines | +1.0% | North America, Europe, Urban APAC | Short term (≤2 years) |

| Quickening e-commerce growth across kitchen and bath furnishings | +0.8% | North America, Western Europe, Global | Medium term (2–4 years) |

| Outdoor living and hospitality upgrades spurring weatherproof cabinetry | +0.6% | North America, Europe, Resort APAC/MEA | Medium term (2–4 years) |

| Policy-driven push for certified wood and recycled inputs | +0.4% | Europe, North America, Urban APAC | Long term (≥4 years) |

| Emergence of IoT-enabled smart cabinet solutions | +0.7% | China, North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Widespread shift toward frameless and modular kitchen layouts

Frameless cabinets, featuring full-access construction, are gaining market share by eliminating the face frame. This design allows wider drawers, full-overlay fronts, and increased interior yield, offering nearly double-digit gains in storage within the same footprint. The cabinet market has expanded frameless options, focusing on urban apartments and smaller homes where space optimization and minimalist aesthetics are key. European design influence remains strong, with modular planning tools enabling homeowners and installers to configure frameless setups with integrated storage accessories. Global retailers are scaling plan-and-order formats for kitchens and bath storage, streamlining decisions through visualization, digital design, and curated assortments. Large-format retailers are opening new plan-and-order points, enhancing awareness and access to frameless and modular configurations.

Multifamily construction boom and renovation uptick favoring stock and RTA lines

The cabinet market is benefiting from resilient renovation activity and multifamily construction pipelines that favor standardized, repeatable specifications suited to stock and ready-to-assemble formats. Replacement cycles for cabinets typically fall in the 15 to 20 year range, which maintains a steady cadence of demand in repair and remodel channels and supports product refreshes that emphasize function, storage, and workflow improvements in kitchens and baths. RTA lines that meet tighter budgets and faster installation windows continue to scale, helped by growing digital discovery and configurators that simplify layout and ordering through guided choices and visualization. Remodel activity in North America stayed supportive heading into 2026, with pro-led projects stabilizing even as homeowners recalibrate budgets for cabinets, surfaces, and fixtures[1]NAHB.ORG Multifamily Housing Market Will Decline in 2024 while Remodeling Market Will Hold Steady | NAHB. The mix shift toward stock and RTA configurations is reinforced by delivery speed, installation simplicity, and broad availability across home centers, dealer networks, and direct-to-consumer websites that together extend reach into price-sensitive cohorts.

Quickening e-commerce growth across kitchen and bath furnishings

E-commerce penetration accelerates in bathroom and kitchen furniture categories globally, complementing traditional channels as observed by the National Kitchen & Bath Association in industry outlook reports[2]NKBA Trademarks https://kb.nkba.org/research/2025-kitchen-bath-market-outlook-july-update/. Digital platforms enhance accessibility for cabinet products, with North American retail segments reporting conservative growth tied to online trends. European cross-border sourcing supports bathroom cabinet distribution. Asian-Pacific markets lead in volume for home furniture e-tail. Association insights note price transparency influencing cabinet sales through hybrid models. Middle Eastern digital infrastructure growth aids penetration in emerging areas. Kitchen Cabinet Manufacturers Association members highlight complementary e-commerce amid showroom reliance.

Outdoor living and hospitality upgrades spurring weatherproof cabinetry

Hospitality and outdoor living trends elevate demand for weather-resistant outdoor cabinets globally, supported by sustained tourism growth with international arrivals up 5% in the first nine months of 2025 per UN Tourism data. Over 1.1 billion tourists traveled internationally through September 2025, boosting resort and venue enhancements requiring durable cabinetry[3]UN Tourism International Tourist https://www.untourism.int/news/international-tourist-arrivals-up-5-in-the-first-nine-months-of-2025. North American coastal developments prioritize resilient materials for outdoor spaces. Middle Eastern hospitality expansions focus on luxury weather-proof integrations. European eco-tourism incorporates sustainable outdoor cabinets. Asia-Pacific coastal regions emphasize modular, durable units. UN Tourism barometer indicates resilient demand driving commercial outdoor cabinet applications across climates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Swings in lumber and panel costs squeezing producer margins | −0.9% | Global, highest exposure in North America | Short term (≤2 years) |

| Persistent skilled carpentry labor gap lengthening delivery schedules | −0.6% | North America, Europe | Medium term (2–4 years) |

| Tariffs and anti-dumping rulings unsettling RTA supply chains | −0.4% | North America, Europe, Asian manufacturing hubs | Medium term (2–4 years) |

| High mortgage rates curbing homeowner renovation spend | −0.3% | North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Swings in lumber and panel costs squeezing producer margins

Input price volatility has weighed on the cabinet market because lumber and panels account for a significant share of finished product cost structures, which squeezes margins or forces pass-through price adjustments that can dampen demand. The United States framing lumber price indices saw month-to-month declines in late 2025, yet remained higher than the prior year, which illustrates the uncertainty that procurement teams must manage across quarters. Canadian softwood lumber duties rose during 2025 and, when combined with anti-dumping rates, raised the effective cross-border burden on key wood inputs that flow into many cabinet components shipped to the United States plants. In parallel, cabinet producers cited resin and adhesive cost pressures for particleboard and MDF substrates and reduced price-lock windows on bids to limit exposure to rapid swings in input prices and surcharges. In this environment, the cabinet market is emphasizing design-to-value alternatives, mix optimization, and inventory discipline, while also reinforcing compliance with CARB and TSCA Title VI emissions limits for composite wood, which remain non-negotiable market access requirements.

Persistent skilled carpentry labor gap lengthening delivery schedules

Skilled labor scarcity in carpentry, millwork, and installation continues to stretch lead times for premium and custom projects, which drives some buyers toward semi-custom and stock options that can be delivered faster. In 2025, a majority of kitchen and bath firms reported moderate to severe labor shortages, reflecting recruitment challenges that directly influence scheduling, throughput, and customer satisfaction. The cabinet market is responding with investments in training, digital design workflows, and factory automation to reduce bottlenecks, stabilize quality, and improve installation consistency at the job site. Companies across the building products ecosystem have highlighted the need for expanded apprenticeship pipelines and retention efforts to bring new talent into the trades, which remains critical as experienced workers retire. Over the near term, elevated wage requirements for experienced installers and extended backlogs in custom shops continue to reinforce demand for well-specified, modular offerings that can be installed efficiently by smaller crews.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: RTA Configurations Lead Growth Despite Semi-Custom Dominance

Semi-custom cabinets dominate the market with a 46.39% market share in 2025, offering a balance of personalization and cost efficiency that suits remodel budgets and builder standards. Their variety in door styles, finishes, and storage options appeals to design professionals and installers, balancing aesthetics with availability. Custom cabinets remain a niche for premium projects despite labor and lead-time challenges, while stock cabinets support large-scale builder programs focused on speed and uniformity. Modularity is gaining traction in semi-custom and custom segments as manufacturers streamline platforms to enhance scalability, interchangeability, and cost efficiency. Semi-custom cabinets are expected to retain their leadership, while ready-to-assemble (RTA) cabinets grow rapidly, driven by delivery speed and cost considerations.

RTA cabinets are forecasted to grow at a 7.26% CAGR through 2031, supported by online assortments, visual planners, and home-center footprints targeting cost-conscious buyers and small contractors. Retailers are adopting plan-and-order formats, design support, and pick-up points to reduce costs and lead times. RTA’s simple installation reduces skilled labor needs, addressing labor shortages. Leading brands are enhancing digital tools for layout configuration, finish exploration, and purchase-ready lists compatible with RTA packaging. These advancements are expected to boost RTA’s market share, while semi-custom cabinets remain central in remodel-heavy regions.

By Application: Kitchen Dominance with Bath Vanities Accelerating

Kitchen cabinets accounted for 69.39% of the applications market size in 2025, highlighting their central role in remodel spending and new-home specifications. Kitchens require more linear footage, deeper storage, and greater hardware and accessory usage than other rooms, resulting in higher revenue per project. The growing adoption of full-height pantries, concealed storage, and integrated organizational systems increases the materials tied to cabinet lines and accessories. Integrated appliance panels and panel-ready features enhance cabinetry's aesthetic appeal, supporting premium pricing in mid to high tiers. These factors keep kitchens dominant in the cabinet market, even as other rooms expand their cabinet usage.

Bathroom cabinets are projected to grow at a 7.87% CAGR through 2031, driven by demand for vanities with integrated power, drawer organizers, and wood grain or textured finishes. Storage within arm’s reach remains a priority, encouraging deeper drawers, pull-outs, and better vertical utilization around sinks and mirrors. Personalized storage solutions for grooming routines, haircare appliances, and concealed device charging are gaining traction. Durability and low-VOC compliance are critical in bathrooms, influencing product development alongside design trends. As renovation cycles progress through primary and secondary bathrooms, suppliers are aligning offerings to capture upgrades in single-family and multifamily homes.

By Material: Wood Retention with Metal Gains in Outdoor Segments

Wood holds a 71.84% market share in 2025, driven by its natural textures, varied finishes, and certified options meeting emissions and chain-of-custody standards. Consumers favor visible wood grain on doors and drawer fronts, especially in warm, natural finishes for modern and transitional spaces. Cabinet makers increasingly source certified wood under FSC and PEFC programs and ensure compliance with CARB and TSCA Title VI emission standards. Companies with North American and European sourcing emphasize traceability and responsible forestry, aligning with green building programs preferred by developers and institutional buyers, while reducing regulatory risks.

Metal cabinetry is projected to grow at a 6.37% CAGR through 2031, supported by outdoor kitchens, hospitality venues, and high-durability applications. Stainless steel, including marine-grade variants, is valued for corrosion resistance, easy cleaning, and longevity in seaside and pool-adjacent installations. Polymer options like HDPE outdoor cabinets are expanding due to water and UV resistance, low maintenance, and recyclability. The rise of outdoor living spaces with integrated storage, sinks, and refrigeration boosts demand for metal and polymer cabinets alongside stone and composite surfaces. Metal’s market share is expected to grow in high-end outdoor projects, while wood remains dominant in interior residential and commercial applications.

By End User: Residential Majority with Commercial Expansion

Residential end users accounted for 78.35% of cabinet demand in 2025, highlighting the importance of single-family and multifamily homes in the market. Homeowners prioritize kitchen and bath upgrades for resale value and daily functionality, driving consistent demand for cabinets. Aging homes in North America and Europe sustain replacement cycles, even during slowdowns in new home construction, keeping dealer networks and home centers active. Manufacturers maintained steady retail and builder channel flows in 2025, despite normalized product mixes and disciplined pricing post-pandemic. Accessible design support and project planning services enable residential buyers to align upgrades with budgets and timelines while meeting functional and compliance needs.

Commercial projects, including hospitality, office, retail, healthcare, and education, are expected to grow at an 8.24% CAGR through 2031. Developers and facility owners focus on durable finishes, standardized components, and quick installations. The cabinet industry addresses these needs with solutions that balance aesthetics and replaceable parts, reducing lifecycle costs in high-traffic areas. Green building goals and indoor air quality standards influence specifications, with low-VOC coatings and compliant composite wood frequently cited. Large multifamily developments drive growth by using uniform cabinet packages for efficient installations and turnovers. The cabinet market is well-positioned to deliver scalable, compliant systems across portfolios and regions.

By Distribution Channel: Offline Dominance with Online Surge

Offline channels dominate the cabinet market with a 66.36% share, driven by specialty showrooms, dealer networks, and home centers offering tactile product experiences, professional design, and installation services. These channels benefit from manufacturer training, display investments, and co-op marketing, enabling designers and sales teams to manage complex kitchen and bath projects. Manufacturers with strong retail and builder partnerships emphasize the importance of offline routes for high-complexity projects and custom solutions. Integrated in-store services, such as measurement, layout, and logistics support, streamline project management from planning to installation. Offline channels remain vital for service-intensive projects and buyers seeking in-person design collaboration.

Online platforms are projected to grow at a 9.39% CAGR through 2031, driven by configurators, visualization tools, and direct ordering for RTA and semi-custom lines. Retailers and brands are blending digital and physical experiences with virtual planning tools and appointment scheduling, reducing friction in research and purchasing. Investments in user-friendly product finders, AR visualization, and clear content enhance consumer understanding of construction, finishes, and storage options. Large retailers are expanding online-offline hybrids with plan-and-order points and localized pick-up sites, cutting costs and improving buyer confidence. These advancements reshape cabinet selection, reaching budget-conscious consumers while maintaining compliance and service standards.

Geography Analysis

North America accounted for 38.39% of the cabinet market size in 2025, with the United States leading due to strong remodeling activity and a well-established dealer and home-center network. Monthly sales fluctuated as price normalization, tariff concerns, and inventory management prompted cautious purchasing. Sales trends across stock, semi-custom, and custom cabinets reflected macroeconomic conditions, seasonality, and regional project variations. Lumber price volatility and Canadian softwood tariffs complicated planning, while formaldehyde emission standards influenced composite wood sourcing. The market remained driven by repair and remodeling projects, steady semi-custom demand, and increased use of online tools for RTA and stock packages.

Europe serves as a key manufacturing and design hub for cabinets, with high demand for frameless and modular designs supported by advanced suppliers and machinery partners. Germany leads in storage categories, while sustainability standards, circularity, and energy-efficient production shape regional demand. Manufacturers focus on certified wood, low-emission composites, and waterborne finishes to meet regulations and consumer expectations. Retailers with European manufacturing bases invest in capacity and automation for kitchens and storage systems, leveraging scale and compliance. Stabilizing macroeconomic conditions are expected to drive moderate growth in remodeling and selective new construction, with a focus on premium and sustainable designs.

Asia-Pacific is projected to grow at an 8.38% CAGR through 2031, driven by urbanization, rising incomes, and the adoption of Western-style kitchens adapted to smaller spaces. China’s furniture sector experienced revenue and profit variability in 2025 due to mixed demand and cost conditions. Regional suppliers are expanding into Southeast Asia and the Middle East, incorporating digital planning and modular platforms in showrooms. The market emphasizes value, compact storage, and quick installation, alongside compliance with certified wood and emissions standards. Investments in retail infrastructure are expected to boost online-assisted cabinet sales and RTA adoption in the forecast period.

Competitive Landscape

The cabinet market in North America and parts of Europe is moderately to highly consolidated, with brand portfolios, dealer networks, and retail partnerships offering significant scale advantages. Leading manufacturers streamlined product platforms and improved plant utilization in 2025, reinvesting savings into automation, digital tools, and services. A major all-stock merger between two prominent North American cabinet brands focused on procurement, manufacturing optimization, and overhead efficiencies. Large-format home furnishings retailers expanded their cabinet offerings through plan-and-order formats, prioritizing kitchen and bath system planning in new U.S. metro locations. Certification bodies and regulators continued to drive competitive differentiation by rewarding early investments in chain-of-custody, low-emission materials, and energy efficiency.

MasterBrand reported FY2024 net sales of USD 2,700.4 million and adjusted EBITDA of USD 363.6 million. A 2024 cabinet brand acquisition expanded its channel reach and contributed to net sales. American Woodmark, with FY2025 net sales of USD 1,709.6 million, optimized its operations, including closing a Virginia facility as part of a cost and service initiative. In August 2025, the two companies announced an all-stock merger targeting USD 90 million in annual revenue within three years and adjusted diluted EPS growth by year two post-close[4]American Woodmark Corporation, “AWC 2025 Annual Report,” American Woodmark, americanwoodmark.com. These strategies emphasize platform standardization, network optimization, and digital enablement to enhance service and reduce unit costs.

Global retailers sustained cabinet-related growth in 2025, with online sales exceeding a quarter of turnover for the largest home furnishings brand. This retailer opened 66 new sales locations, focusing on kitchen, bathroom, and closet systems in the United States, supported by a multibillion-dollar omnichannel investment. The United States maintained a 25% Section 232 tariff on certain cabinet imports, delaying a planned increase to 50% until January 2027, adding complexity for importers and price-sensitive buyers. Compliance with TSCA Title VI and CARB Phase 2 influenced material strategies, particularly for composite wood products and finishes. Manufacturers and retailers focused on channel optimization, digital planning, and certified materials to drive differentiation and resilience in the cabinet market.

Cabinet Industry Leaders

IKEA

Masco Corporation

American Woodmark Corp.

Cabinetworks Group

Oppein Home Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: KraftMaid Cabinetry introduced seven new finish colors, broadening its standard palette and the ColorCast™ Collection. Trend-forward additions like Vanilla Smoke, Muted Moss, and Ember are at the forefront of this update. This move seeks to rejuvenate the brand and offer homeowners and designers enhanced avenues for personalizing kitchen and bath spaces.

- August 2025: MasterBrand, Inc. acquired Supreme Cabinetry Brands, Inc., enhancing its 2024 net sales while expanding its product portfolio and distribution channels.

- July 2024: MasterBrand, Inc. acquired Supreme Cabinetry Brands, Inc., enhancing its 2024 net sales while expanding its product portfolio and distribution channels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cabinet market as factory-built storage units covering stock, semi-custom, custom, and ready-to-assemble formats that are intended for permanent installation in kitchens, bathrooms, utility rooms, offices, and other interior spaces. Values are captured at manufacturer selling price and include the carcass, doors, drawer fronts, hardware, and applied finishes.

Scope Exclusion: Laboratory biosafety hoods, telecom or outdoor equipment enclosures, and site-built millwork are outside the study scope.

Segmentation Overview

- By Type

- Ready-to-Assemble (RTA) Kitchen Cabinets

- Pre-Assembled/Stock Cabinets

- Semi-Custom Cabinets

- Custom Cabinets

- By Application

- Kitchen Cabinets

- Bathroom Cabinets

- Other Applications

- By Material

- Wood

- Metal

- Other Raw Materials

- By End User

- Residential

- Commercial

- By Distribution Channel

- Online

- Offline

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cabinet producers, hardware suppliers, buying groups, and distributor chains in North America, Europe, and Asia-Pacific. These conversations clarified material yield losses, regional ASP spreads, online channel share, and likely renovation budgets, allowing us to plug data gaps and stress-test desk findings.

Desk Research

We begin with public datasets such as UN Comtrade export codes 9403 and 4412, FAOSTAT wood-panel output, US Census housing starts, Eurostat building permits, KCMA shipment indices, and NKBA renovation-spend trackers, which give broad demand signals across regions. News archives, housing dashboards, and trade journals add context on style shifts and channel mix.

Financial filings and investor presentations accessed through D&B Hoovers and Dow Jones Factiva help our team benchmark average selling prices and material cost swings. The sources named here are illustrative; many additional publications, databases, and statistical yearbooks supported data extraction, validation, and clarification.

Market-Sizing & Forecasting

A blended top-down model converts residential construction completions, renovation outlays, and furniture-expenditure pools into cabinet demand, then cross-checks results with sampled supplier revenues and shipment audits. Key variables include new housing starts, median kitchen size, wood-panel price indices, e-commerce furniture penetration, and renovation-loan disbursements. Multivariate regression projects each driver, while scenario analysis adjusts for lumber price shocks; selective bottom-up roll-ups spot outliers and anchor regional splits.

Data Validation & Update Cycle

Model outputs face automated anomaly flags, peer cross-checks, and senior sign-off. We refresh core datasets annually and issue interim updates if tariffs, raw-material spikes, or housing-policy shifts alter demand patterns, ensuring clients receive the latest calibrated view.

Why Mordor's Cabinet Market Baseline Commands Confidence

Published numbers often differ because firms choose unique product mixes, pricing points, and refresh rhythms. By aligning scope tightly to finished factory cabinets and keeping our base year current, Mordor minimizes such drift.

Key gap drivers include inclusion of worktops, differing ASP escalation curves, or reliance on outdated shipment ratios. Our annual refresh and dual-side validation keep the figure balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 141 B (2025) | Mordor Intelligence | |

| USD 141.4 B (2025) | Global Consultancy A | Counts outdoor equipment enclosures, inflating total |

| USD 131.5 B (2024) | Trade Journal B | Uses 2020 ASPs without adjusting for lumber inflation |

| USD 63.2 B (2023) | Industry Association C | Focuses only on kitchen cabinets, excludes bath and utility |

Taken together, the comparison shows that when scope, price year, and refresh cadence are standardized, our measured baseline sits logically between narrow product tallies and broad furniture aggregates, giving decision makers a dependable starting point.

Key Questions Answered in the Report

What is the 2026 cabinet market size and how fast is it expected to grow through 2031?

The cabinet market is estimated USD 148.09 billion in 2026 and is projected to reach USD 189.32 billion by 2031 at a 6.18% CAGR.

Which product types lead demand in the global cabinet market and which are growing the fastest?

Semi-custom led with 46.39% share in 2025, while ready-to-assemble lines are projected to grow the fastest at a 7.26% CAGR through 2031.

What applications are most important to cabinet demand today?

Kitchen cabinets accounted for 69.39% of 2025 demand and remain the anchor application, while bathroom cabinets are forecast to grow at a 7.87% CAGR through 2031.

How are materials shifting in cabinet production and specification?

Wood remained dominant at 71.84% share in 2025, while metal cabinets are gaining with outdoor living trends and are projected to grow at 6.37% CAGR.

Which sales channels are driving cabinet purchases now?

Offline channels held 66.36% in 2025 driven by showroom design support and installation services, while online is projected to grow at a 9.39% CAGR through 2031.

What regional trends define current cabinet demand and growth prospects?

North America led with 38.39% share in 2025 on remodel strength, while Asia-Pacific is expected to be the fastest growing region at an 8.38% CAGR through 2031.

Page last updated on: