Institutional Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 244.65 Billion |

| Market Size (2031) | USD 333.59 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Institutional Furniture Market Analysis by Mordor Intelligence

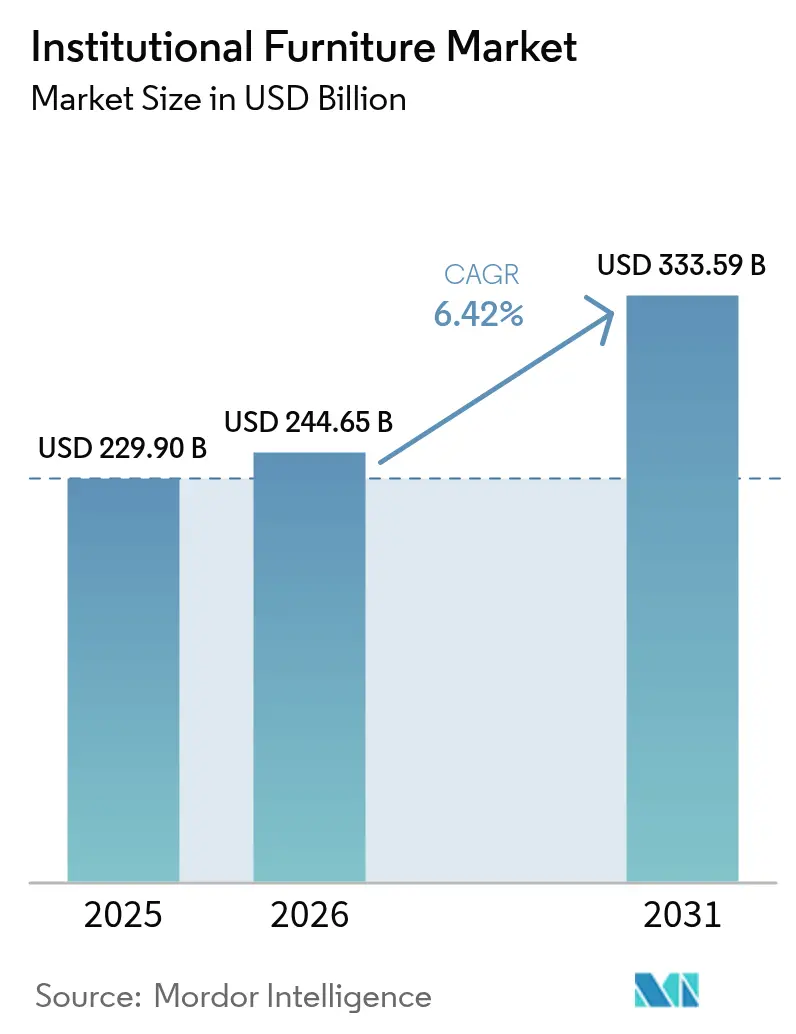

The institutional furniture market size is expected to grow from USD 229.9 billion in 2025 to USD 244.65 billion in 2026 and is forecast to reach USD 333.59 billion by 2031 at 6.42% CAGR over 2026-2031. Demand is buoyed by record student enrollments, enlarged healthcare capital budgets, and a widespread turn to hybrid work-learning formats that require furnishings able to shift from individual to group use within minutes. Buyers now insist on third-party sustainability labels, making FSC, GREENGUARD, and BIFMA LEVEL certifications baseline entry requirements. Heightened digital procurement activity, led by public e-tendering platforms, shortens buying cycles for standard lines yet raises expectations for rapid configuration support. Meanwhile, sensor-enabled seating and other connected products are opening a new data-driven services layer for manufacturers that can interpret utilization insights for clients.

Key Report Takeaways

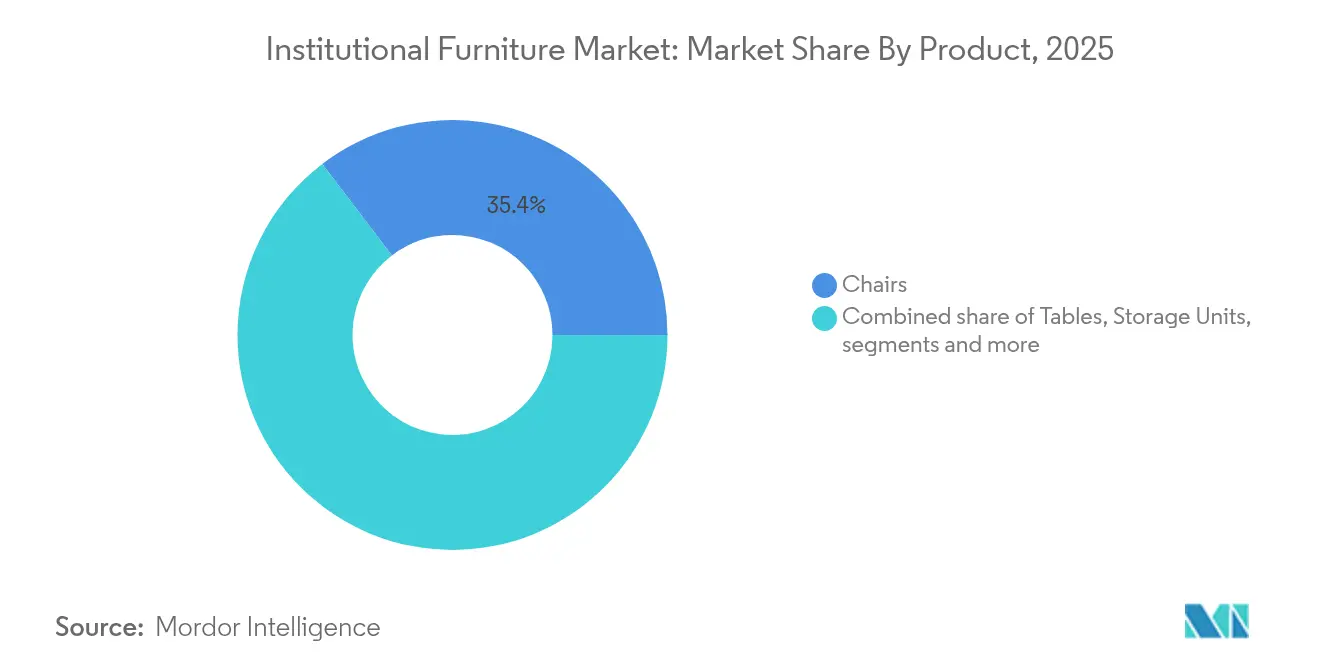

- By product, chairs led with 35.35% of the institutional furniture market share in 2025, while sofas and soft seating are on track for a 7.03% CAGR through 2031.

- By material, wood retained a 33.40% share of the institutional furniture market size in 2025; plastic and polymer materials are projected to climb to a 6.78% CAGR.

- By price range, economy lines held 42.35% of the institutional furniture market size in 2025, whereas premium furniture is expected to grow at 6.62% CAGR to 2031.

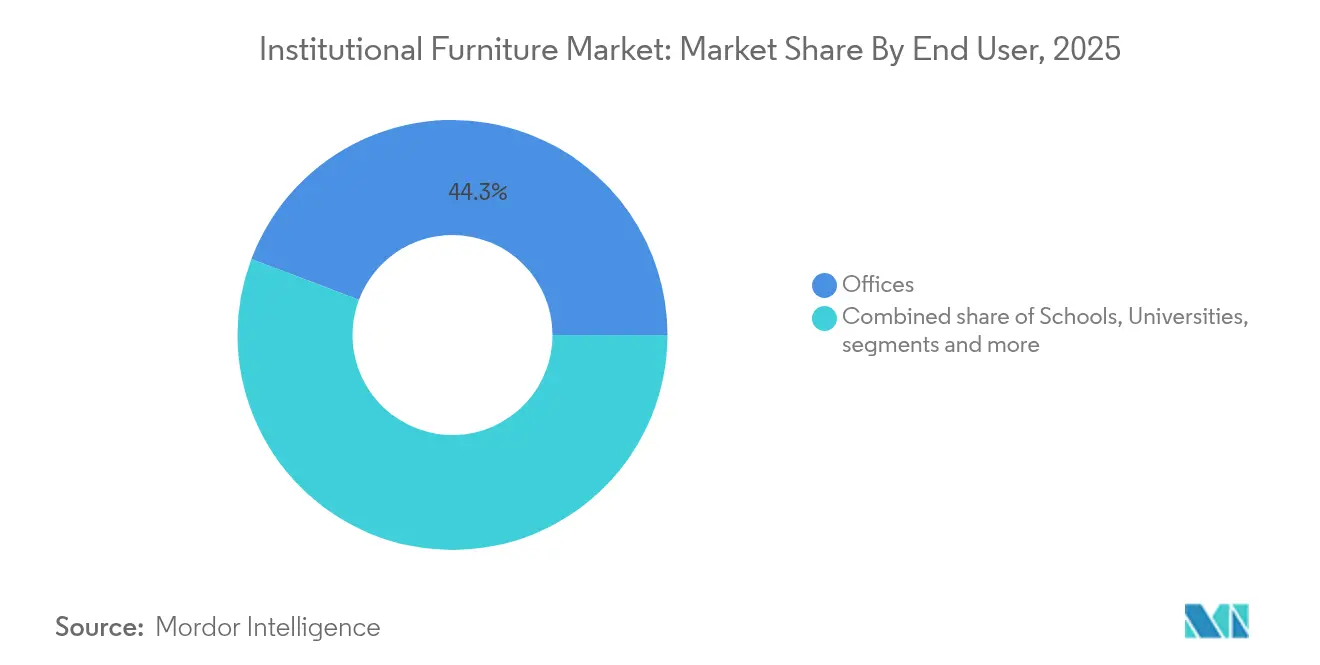

- By end user, offices captured 44.25% of the institutional furniture market size in 2025; healthcare facilities represent the fastest growing end user at 6.45% CAGR.

- By distribution channel, dealer networks accounted for 39.10% of 2025 sales, yet online platforms registered the fastest 7.48% CAGR.

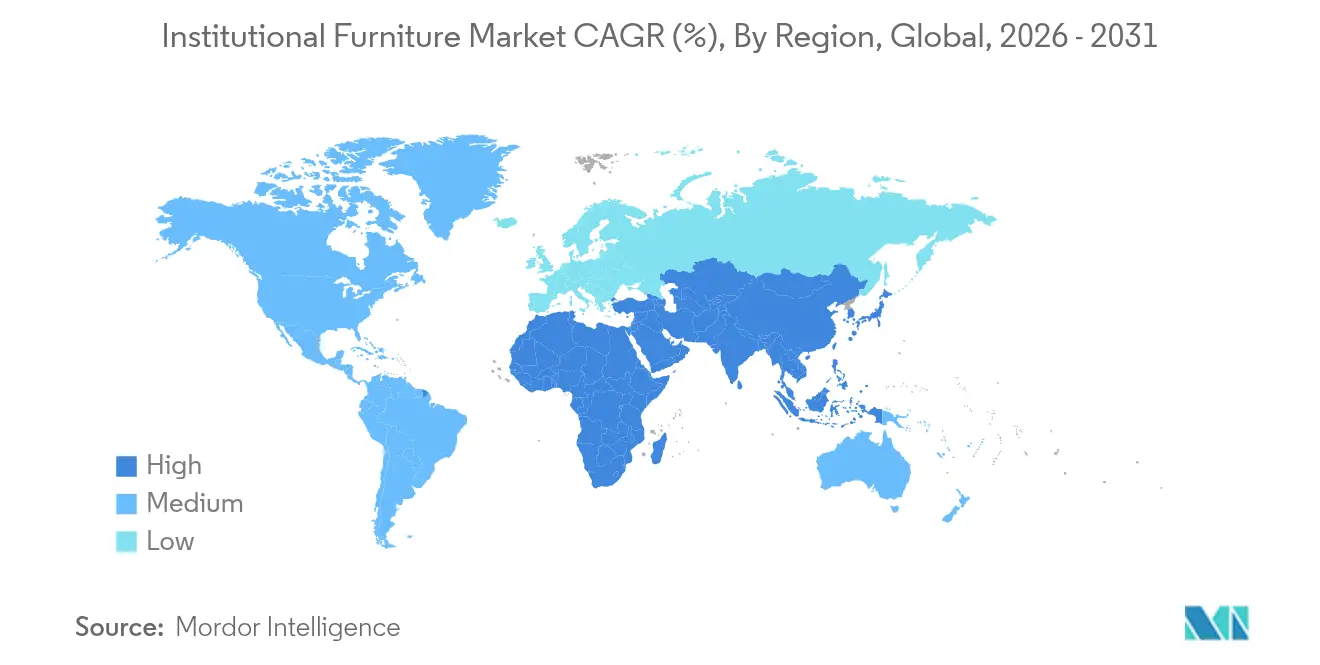

- By geography, North America dominated with 34.45% revenue in 2025; Asia-Pacific is forecast to post a 7.12% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Institutional Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Global Education Enrolments and Campus Construction | +1.8% | Global, with a concentration in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Growing Worldwide Spend on Healthcare Infrastructure and Patient-Centric Waiting Areas | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Hybrid Work-Learning Models Driving Demand for Re-Configurable Multi-Use Furniture | +1.2% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Rising Global Preference for Certified Sustainable Materials (FSC, GREENGUARD, BIFMA LEVEL) | +0.9% | North America, Europe, with a growing influence in Asia-Pacific | Long term (≥ 4 years) |

| Digital Procurement & E-Tendering Platforms Boosting Cross-Border B2B Furniture Sourcing | +0.7% | Global, with the strongest impact in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Global Education Enrolments and Campus Construction

Student populations are rising sharply, spurring the construction of new schools and universities that specify learning spaces able to morph from lectures to group tasks within the same period. In 2000, approximately 445 million children were enrolled in secondary education. By 2023, that figure surged to roughly 641 million [1]UNESCO Institute for Statistics, "Education Enrollment Data",unesco.org. As school enrollments surge, the construction of educational institutions ramps up, leading to a heightened demand for furniture solutions in schools and universities. Responding to the growing student population and the demand for contemporary, adaptable learning spaces, Shanghai Jiao Tong University broke ground on a new campus in Chenjiazhen Education Park, Chongming District, Shanghai, in October 2024. In September 2024, in a significant move to address the rising student population, Mayor Eric Adams unveiled 24 new public school buildings across New York City. This expansion, which added 11,010 K-12 seats in Brooklyn, the Bronx, Manhattan, and Queens, represents the most substantial increase in school seats since 2003 [2]The Office of the Mayor, “Mayor Adams Opens 24 New School Buildings Ahead of 2024-2025 School Year,” nyc.gov. Administrators now favor modular desks, mobile storage, and stackable seating that support open pedagogies, universal design, and technology-rich curricula. Demand for ergonomic adjustment features continues to climb as institutions address varied body sizes and accessibility mandates. Growth is strongest in Asia-Pacific and the Gulf Cooperation Council, where public budgets for K-12 and tertiary facilities remain intact despite wider fiscal pressures. As a result, the institutional furniture market sees larger bid sizes and longer call-off contracts tied to multi-phase campus projects.

Growing Worldwide Spend on Healthcare Infrastructure and Patient-Centric Waiting Areas

Hospitals and clinics are redirecting capital toward interiors that reduce stress and infection risks. Waiting zones increasingly mirror hospitality lounges, employing soft seating, calming palettes, and biophilic accents to raise patient satisfaction scores. For instance, the Asklepios Clinic in Schaufling, Germany, exemplified patient-centric design. The clinic collaborated with Appia Contract GmbH to redesign its reception area, focusing on enhancing patient comfort. The redesign featured spacious layouts, upgraded furniture, and modular seating. These improvements not only enhanced the clinic's aesthetics but also supported better hygiene practices. Furniture specifications now also include antimicrobial laminates, sealed foam cores, and fully welded frames such as those in Stance Healthcare’s Spry Seating line. Health-system mergers in the United States and Europe standardize design templates across networks, compressing decision timelines, and extending contract volumes. These trends keep healthcare the fastest-expanding end user within the institutional furniture market and reward suppliers able to verify cleanability and durability through real-time usage data.

Shift Toward Hybrid Work-Learning Models Driving Demand for Re-Configurable Multi-Use Furniture

Organizations revising real-estate footprints need furniture that lets one room become a private office in the morning and a team studio by afternoon. Height-adjustable tables, lightweight screens, and power-integrated seating are therefore moving from optional upgrades to base specifications. Manufacturers such as Steelcase report order uplifts linked directly to return-to-office programs. Early adopters in higher education are mirroring the approach, outfitting libraries and student hubs with mobile pods and touchdown benches. As hybrid policies stabilize, data-ready units that track occupancy support facility-management decisions, reinforcing the institutional furniture market’s pivot toward smart products.

Rising Global Preference for Certified Sustainable Materials

Environmental, social, and governance criteria feature prominently in tender scorecards, with many public agencies assigning minimum weights of 20-30% to sustainability credentials. Producers respond by expanding the use of recycled polymers, rapidly renewable wood such as bamboo, and low-VOC finishes. For instance, MillerKnoll’s pledge to eliminate added PFAS from all North American lines by May 2025 sets a milestone for chemical transparency in the institutional furniture market [3]MillerKnoll, “MillerKnoll is the First Office Furniture Manufacturer to Announce Elimination of PFAS from North American Brand Portfolio of Products,” millerknoll.com . Lifecycle assessments now influence not only materials but disassembly design, pushing factories toward mono-material components that simplify closed-loop recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Global Steel, Hardwood and Petrochemical Prices Impacting Input Costs | -0.8% | Global, with heightened impact in regions with limited raw material reserves | Medium term (2-4 years) |

| Intensifying Price Competition from Low-Cost Manufacturing Hubs (Vietnam, Malaysia, China) | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Lengthy Public-Sector Procurement Cycles and Compliance Certifications | -0.3% | Global, with particular impact in regions with complex regulatory frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Global Steel, Hardwood, and Petrochemical Prices Impacting Input Costs

Volatile costs for manufacturers are significantly restraining the growth of the market. In 2024 and early 2025, benchmark steel coil and hardwood indexes fluctuated by double-digit percentages quarter-to-quarter, eroding margin visibility for contract-linked projects. Because raw materials can account for three-quarters of furniture lifecycle impact, manufacturers hedge with forward-buy strategies and alternative material R&D. Yet, sudden cost spikes still force price renegotiations or scope reductions, tempering the institutional furniture market’s overall growth pace.

Intensifying Price Competition from Low-Cost Manufacturing Hubs

Low-cost manufacturing hubs, including China, Vietnam, India, and certain Eastern European regions, are reshaping the competitive landscape of the global institutional furniture market through intensifying price competition. These nations, with their access to cheaper raw materials, labor, and scalable production capacities, empower manufacturers to offer products at prices that undercut those from higher-cost areas, such as North America and Western Europe. European buyers report widening landed-cost gaps, prompting many regional brands to emphasize design, circularity, and quick-ship services over direct price matches. Consolidation within North America—illustrated by HNI Corporation’s USD 503.7 million acquisition of Kimball International—aims to unlock scale efficiencies that preserve competitiveness, yet downward pressure on average selling prices remains a drag on the institutional furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Soft Seating Redefines Collaborative Spaces

The institutional furniture market share for chairs reached 35.35% of total revenue in 2025, underscoring their universal role across campuses, clinics, and offices. Growing ergonomic awareness keeps task-chair refresh cycles short, sustaining volume even in mature regions. Sofas and other soft seating, though smaller in absolute terms, are projected to advance at a 7.03% CAGR to 2031 as institutions remodel lobbies, libraries, and break-out zones into informal collaboration areas.

A parallel trend boosts demand for acoustic pods, booths, and partition-integrated couches that mitigate noise without erecting permanent walls. Within open-plan schools, rolling ottomans and loveseat modules help educators reconï¬gure lessons swiftly, supporting inclusive pedagogy. Healthcare suites specify bariatric-rated lounge pieces that meet both durability and infection-control protocols, signaling that comfort-oriented design is becoming a clinical standard rather than a luxury. These shifts collectively steer incremental growth in the institutional furniture market, favoring vendors with broad upholstery fabrics and modular geometries.

By Material: Polymers Challenge Wood's Dominance

Wood held 33.40% of the institutional furniture market share in 2025, reflecting both aesthetic appeal and long-standing purchaser familiarity. Specifiers increasingly request chain-of-custody documentation, pushing mills toward FSC-certified timber and water-based finishing systems. Plastics and advanced polymers are the fastest-rising material class, expected to post a 6.78% CAGR through 2031. Their gains stem from recycled content innovation, reduced weight for shipping cost savings, and emerging bio-based resins that match structural requirements.

Metal frames remain critical for strength and reusability; aluminum and closed-loop steel benefit from indefinite recyclability and are championed in procurement guidance from several EU member states. Hybrid composites blending natural fibers with polypropylene now appear in student chair shells and hospital recliners, balancing impact resistance with lower embodied carbon. Such material experimentation widens choice yet obliges manufacturers to maintain multi-process capabilities, adding operational complexity across the institutional furniture industry.

By Price Range: Premium Segment Defies Economic Pressures

Economy lines commanded the largest slice of the institutional furniture market at 42.35% in 2025, serving price-sensitive public schools and regional government offices. Yet the premium tier is forecast for 6.62% CAGR as procurement teams embrace total cost-of-ownership metrics. Decision-makers now weigh extended warranties, upgrade paths, and ease of refurbishment against upfront outlay, often deciding that premium builds deliver lower lifetime expenses.

Manufacturers respond with high-pressure laminate edges, grade-A textiles, and service packages covering re-upholstery or component swap-outs. Mid-range products continue to sell on balanced specifications, but leakage to premium is evident in urban headquarters and magnet hospitals where interior branding and patient experiences tip budgets upward. As a result, the margin mix is drifting higher even while the broader institutional furniture market remains price-competitive at the entry level.

By End User: Healthcare Facilities Drive Innovation

Office environments represented 44.25% of the institutional furniture market size in 2025, anchored by ongoing space redesigns to accommodate hybrid attendance patterns. Reallocation of floorplates from dense benching to varied zones—focus nooks, social cafés, and training studios—sustains replacement cycles. In parallel, healthcare settings are forecast to outpace all other users at 6.45% CAGR as new clinics open and legacy hospitals retrofit for infection-prevention layouts.

Furniture for exam rooms and infusion bays integrate flush surfaces and easy-off upholstery covers, with several systems now offering embedded USB-C power and patient entertainment mounts. Educational bodies remain a stable demand pillar, though procurement windows often coincide with budget approvals, creating seasonal production spikes. Government ministries, courts, and civic centers continue to invest steadily, yet growth stems mainly from safety upgrades and accessibility compliance rather than square-footage expansion, moderating their contribution to overall institutional furniture market momentum.

By Distribution Channel: Online Platforms Disrupt Traditional Networks

Dealer networks controlled 39.10% of sales in 2025, leveraging installation crews and on-site design support to maintain relevance. However, web-based tendering and direct-to-client portals are scaling rapidly, reflected by a 7.48% CAGR outlook for online channels.

Manufacturers tread carefully to avoid channel conflict, often granting dealers region-exclusive finishes or bundled service agreements. Government entities increasingly utilize cooperative contracts such as OMNIA or Sourcewell, compressing bid paperwork and favoring suppliers with digital catalog syndication. Integration of 3-D visualizers and rapid quote engines on brand sites further accelerates the institutional furniture market’s online share, though complex turnkey projects still rely on dealer expertise for coordinated delivery and punch-list resolution.

Geography Analysis

North America accounted for 34.45% of the institutional furniture market revenue in 2025, supported by large-scale commitments to refresh K-12 classrooms and modernize hospital campuses. Adoption of sit-to-stand desks, active stools, and adjustable monitor arms continues as employers seek to reduce musculoskeletal claims and enhance retention. Canada mirrors these patterns, though capital outlays concentrate in higher education laboratories and public-sector workplaces.

Asia-Pacific is forecast to register a 7.12% CAGR through 2031, underpinned by urban migration, rapid school construction, and public-private investment in new hospitals. Chinese regulations now restrict precious hardwoods in state furnishing, nudging demand toward engineered timber, bamboo, and recyclable metals. India’s Production-Linked Incentive scheme should spur local manufacture of plastic injection and metal fabricated furniture, trimming delivery lead times for domestic projects. Southeast Asian producers, meanwhile, expand export capacity, reinforcing the region’s dual role as consumer and supplier within the institutional furniture market.

Europe maintains a deep design influence. Stringent Extended Producer Responsibility laws encourage take-back programs, prompting many brands to label components for easy recycling. Nordic governments already mandate public-sector furniture to include minimum recycled content percentages, setting precedents likely to spread across the bloc. The Middle East and Africa region pursues large university and hospital schemes financed by sovereign funds, while South America’s growth is tied to Brazil’s classroom digitization push and corporate headquarters openings in São Paulo and Santiago. Collectively, these dynamics sustain the institutional furniture market’s global expansion, even as regional mix shifts toward emerging economies.

Competitive Landscape

The institutional furniture market features a moderate concentration of leading suppliers balanced by vibrant regional specialists. Top players—Steelcase Inc., Haworth Inc., MillerKnoll, Inc., Okamura Corporation, and HNI Corporation—extend advantage through integrated R&D, vertically owned distribution, and expanding portfolios of technology-ready products. Haworth emphasizes circular design, as seen in the Breck task chair, composed of 55.6 kg CO₂e lifetime emissions, less than half typical equivalents.

Digital-first entrants differentiate via rapid product drops, configurable modules, and data dashboards delivered as software-as-a-service subscriptions. Many established brands respond by upgrading web visualization tools and piloting subscription models that bundle furniture, sensors, and analytics into monthly rates. Sustainability commitments, such as eliminating PFAS or achieving carbon-neutral factories, serve as key tender differentiators. Acquisition pipelines remain active, with mid-sized specialists in acoustic booths, antimicrobial laminates, or demountable walls viewed as attractive bolt-ons. Competition consequently hinges less on the lowest price and more on proof of impact—ergonomic, environmental, and operational—reinforcing value-focused segmentation within the institutional furniture market.

Institutional Furniture Industry Leaders

-

HNI Corporation

-

Steelcase Inc.

-

MillerKnoll, Inc.

-

Haworth Inc.

-

Okamura Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bentley Home expanded its collection at Milan Design Week, unveiling the Fenton Table, Ashford Modular Sofa, and Verve Coffee Tables to meet rising demand for customizable premium pieces.

- March 2025: HNI Corporation outlined a profit transformation plan targeting USD 80-85 million in savings and confirmed a new manufacturing site in Mexico.

- February 2025: Vietnam Kai Rui company introduced smart upholstery with integrated charging and home-system connectivity features.

- August 2024: Humanscale launched the first branded online store dedicated to refurbished office furniture, advancing circular business models.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the institutional furniture market as all purpose-built, moveable furnishings supplied to schools, colleges, healthcare facilities, government and religious premises, and corporate offices, designed for heavy-duty, multi-user cycles and certified to commercial fire, safety, and ergonomics codes. According to Mordor Intelligence, the market was valued at USD 229.90 billion in 2025 and is projected to reach USD 314.90 billion by 2030.

Scope Exclusions: Home-living décor, kitchen cabinetry, and single-use décor accessories are outside the study scope.

Segmentation Overview

-

By Product

- Chairs

- Tables

- Storage Units

- Sofas/Soft Seating

- Waiting Benches

- Other Products (stools, booths and partition, etc.)

-

By Material

- Metal

- Wood

- Plastic and Polymer

- Other Materials

-

By Price Range

- Economy

- Mid-range

- Premium

-

By End User

- Schools (K-12)

- Universities & Colleges

- Offices

- Healthcare Facilities (Hospitals, Clinics)

- Government & Public Administration

- Religious Institutions

- Others (Theaters & Auditoriums, etc.)

-

By Distribution Channel

- Direct Sales (from manufacturers to end-users)

- Dealer or Distributor Networks

- Online

- Other Distribution Channels (through government procurement portals, architectural firms or contractors, home centers, etc.)

-

By Geography

-

North America

- Canada

- United States

- Mexico

-

South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

-

Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with facilities managers at universities, procurement leads at hospital groups, government tender officials, and contract furniture dealers across North America, Europe, Asia-Pacific, and the Middle East. These conversations verified adoption rates for certified sustainable materials, average replacement intervals, and e-tender win prices, giving us confidence to triangulate the model outputs.

Desk Research

We first gathered macro indicators and baseline volumes from reputable, non-paywalled sources such as UNESCO Institute for Statistics, OECD Education at a Glance, WHO hospital bed density files, United States Census Bureau value-put-in-place tables, and BIFMA sales dashboards. Trade association newsletters, patent filings via Questel, and company 10-Ks or investor decks offered unit prices, refresh cycles, and pipeline projects that desk data alone could not reveal. D&B Hoovers and Dow Jones Factiva fed us historical revenue splits that helped peg supplier footprints across regions. The sources listed are illustrative only; many additional publications and datasets were reviewed for clarification and cross-checks.

Market-Sizing & Forecasting

A blended top-down build starts with institutional building floor-area additions, public-sector capex, and refurbishment allocations, which are then converted into furniture demand pools using spend-per-square-foot ratios sourced from dealer bids. Results are corroborated with selective bottom-up roll-ups of listed suppliers' contract sales and sampled average selling price × volume checks. Key variables feeding the engine include new student enrollment, hospital bed additions, hybrid-workspace penetration, average seating cost, and certified wood price indices. A multivariate regression aligns these drivers with historical furniture spend before an ARIMA overlay projects five-year scenarios. Gaps in bottom-up data are infilled by regional channel checks and validated with expert sentiment scores.

Data Validation & Update Cycle

Outputs undergo variance screens against independent building start data and BIFMA shipment signals, followed by a two-level peer review before sign-off. We refresh each model annually and trigger interim updates after material policy shifts or major mergers to keep clients current.

Why Mordor's Institutional Furniture Baseline Commands Reliability

Published estimates often diverge because firms select different end-user mixes, price conventions, and refresh cadences. Our disciplined scope selection and annual refresh rhythm reduce those swings and provide an anchor buyers can trace back to transparent variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 229.90 B (2025) | Mordor Intelligence | - |

| USD 255.77 B (2025) | Global Consultancy A | Combines retail office fixtures with institutional spend and converts revenues at purchasing-power parity rather than nominal USD. |

| USD 154.10 B (2024) | Trade Journal B | Focuses solely on contract furniture, omits school and healthcare segments, and extends totals via straight-line growth without macro driver linkage. |

The comparison shows that when scope boundaries or escalation methods shift, values swing widely. Mordor's step-wise build, variable alignment, and timely refresh deliver a balanced, decision-ready baseline.

Key Questions Answered in the Report

What is the current value of the institutional furniture market?

The institutional furniture market is valued at USD 244.65 billion in 2026 and is projected to reach USD 333.59 billion by 2031.

Which region is growing fastest?

Asia-Pacific posts the quickest trajectory with a forecast 7.12% CAGR driven by urbanization and government infrastructure spend.

What product segment is expected to grow most rapidly?

Sofas and other soft seating lead growth at a 7.03% CAGR as institutions redesign collaborative and waiting areas for comfort and flexibility.

How are sustainability requirements shaping procurement?

FSC, GREENGUARD, and BIFMA LEVEL certifications are now baseline tender requirements, and several manufacturers are eliminating chemicals such as PFAS to win bids.

Page last updated on: