Market Overview

| Study Period | 2020 - 2031 |

|---|---|

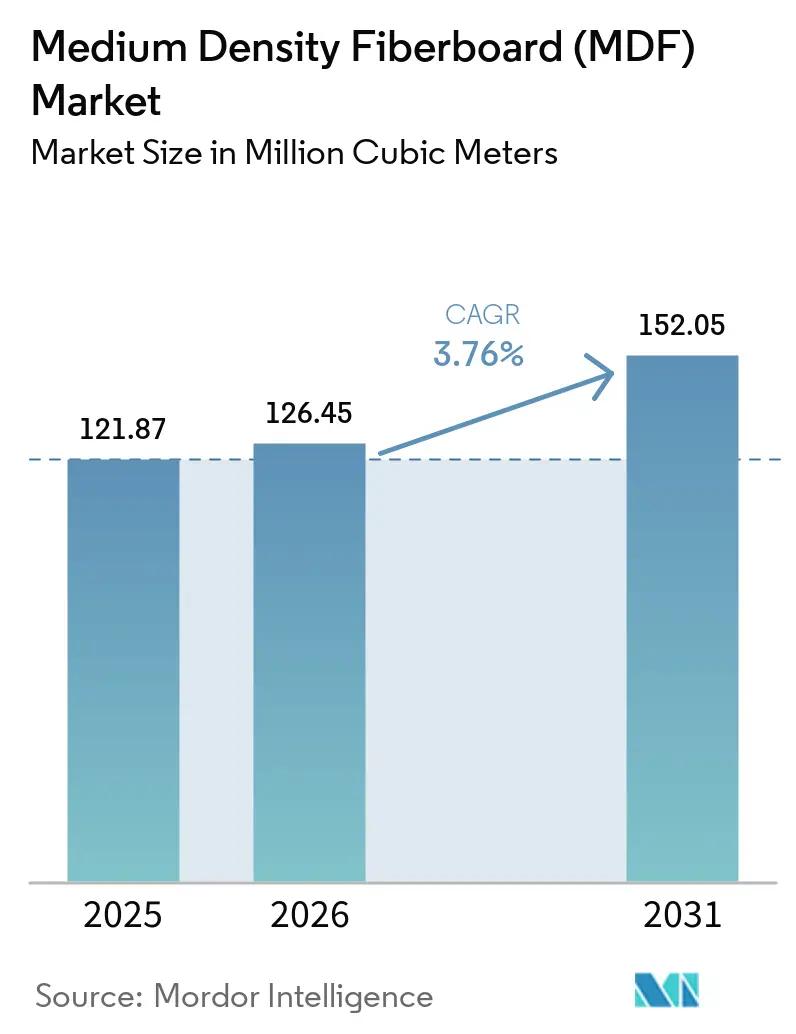

| Market Volume (2026) | 126.45 Million cubic meters |

| Market Volume (2031) | 152.05 Million cubic meters |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

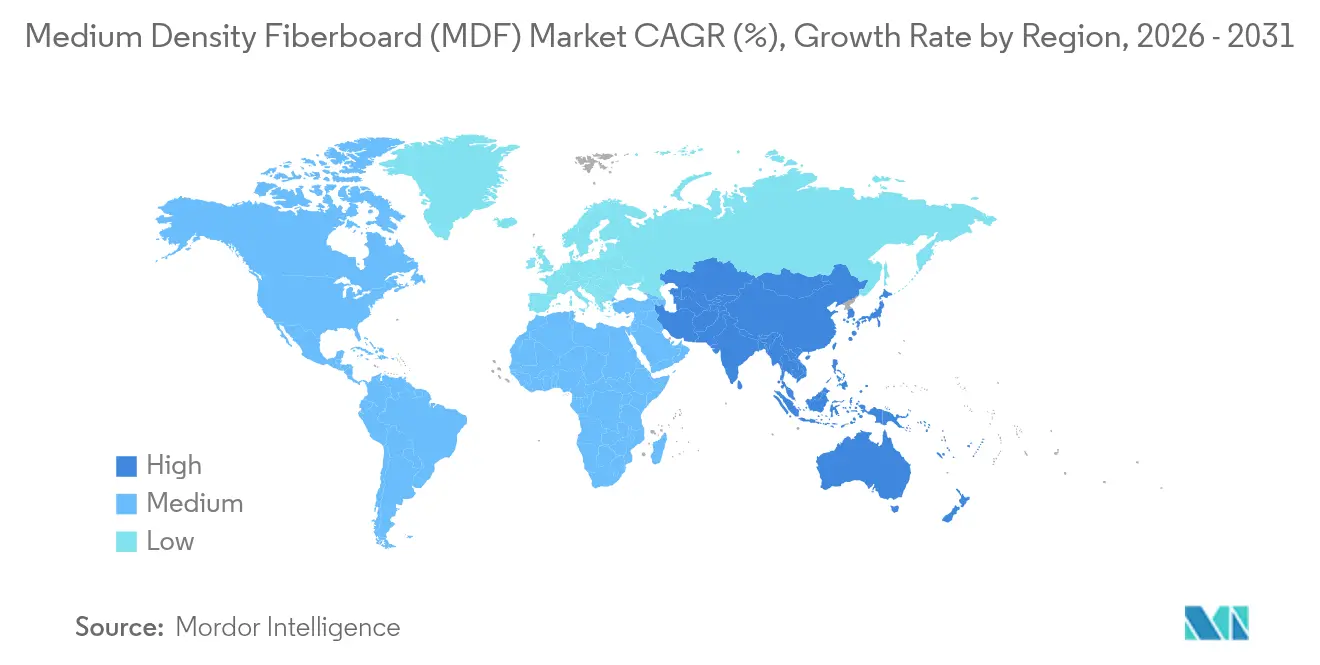

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medium Density Fiberboard (MDF) Market Analysis by Mordor Intelligence

The Medium Density Fiberboard market size is expected to grow from 121.87 million cubic meters in 2025 to 126.45 million cubic meters in 2026 and is forecast to reach 152.05 million cubic meters by 2031 at 3.76% CAGR over 2026-2031. This expansion continues even as global panel capacity grows more slowly, because producers increasingly rely on process upgrades, bio-based resins and circular manufacturing to lift output quality rather than pure tonnage. MDF’s superior machinability, uniform core and smooth face make it the preferred substrate for ready-to-assemble (RTA) cabinets, doors and shelving, allowing furniture makers to achieve consistent painted and laminated finishes. Asia-Pacific commands 60.72% of 2024 production as Vietnam, India and other cost-competitive hubs add lines to serve both domestic housing programs and offshore furniture contracts, while North America and Europe concentrate on premium low-VOC grades to satisfy tightening emission rules. Price volatility for wood fiber and urea-formaldehyde resin remains a short-term challenge, yet manufacturers are offsetting cost spikes through energy-efficient refining, backward integration in timberlands, and adoption of polymeric MDI binders that cut formaldehyde out-gassing.

Key Report Takeaways

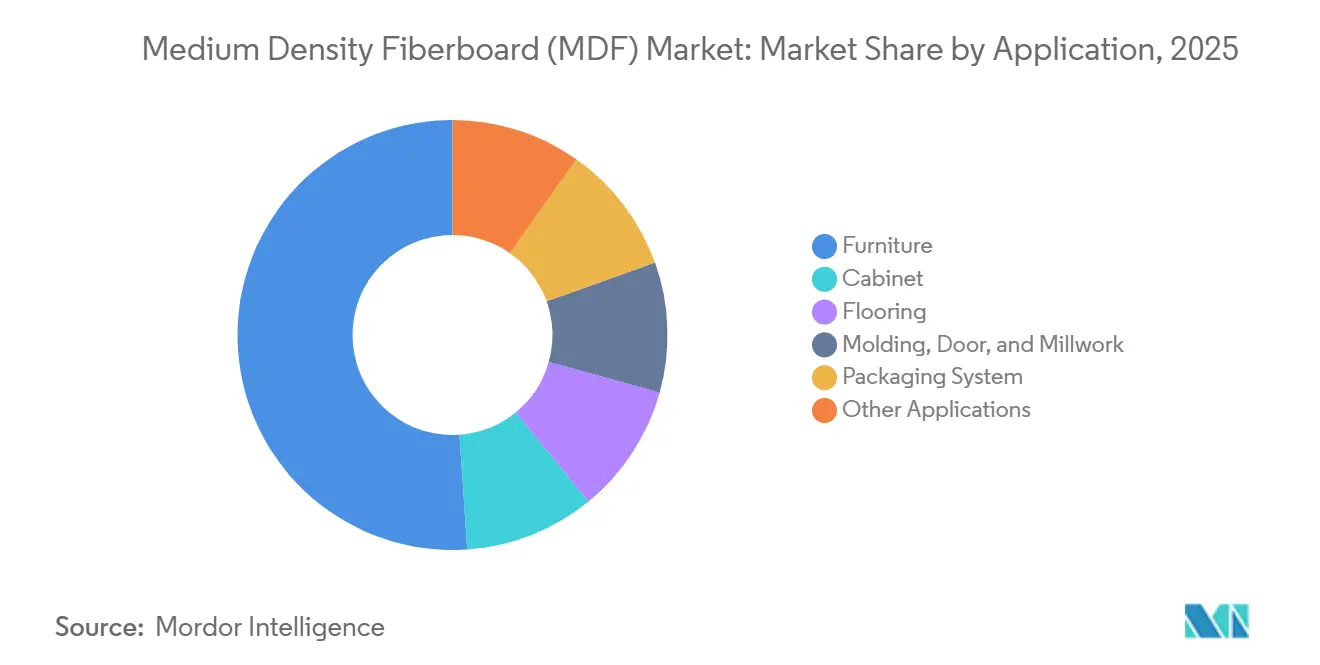

- By application, furniture led with 51.10% of 2025 volume and is advancing at fastest 4.04% CAGR outlook to 2031.

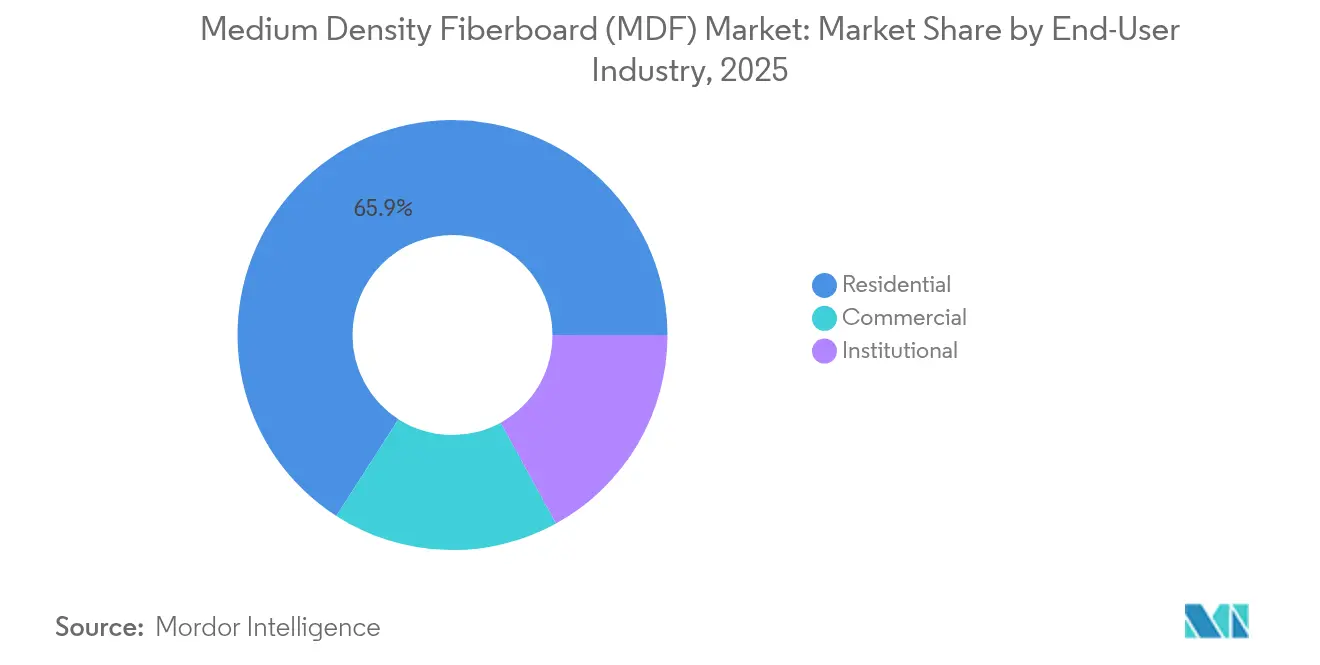

- By end-user industry, the residential segment captured 65.91% share of the medium density fiberboard market size in 2025 and is slated to expand at a 3.79% CAGR through 2031.

- By geography, Asia-Pacific accounted for 60.30% of the medium density fiberboard market share in 2025 and is projected to grow at a 4.05% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medium Density Fiberboard (MDF) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Capacity Additions in Asia-Pacific Furniture Manufacturing Hubs | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Recovery in Global Residential Renovation Spending Post-Pandemic | +0.8% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Shift From Plywood/Particleboard to Smoother MDF for RTA Furniture | +0.9% | Global, concentrated in furniture manufacturing regions | Long term (≥ 4 years) |

| Government-Backed Affordable Housing Programs in India and SE Asia | +0.7% | APAC core, national programs in India, Vietnam, Thailand | Medium term (2-4 years) |

| Adoption of PMDI/Bio-Based Resins Unlocking Premium Low-VOC Segments | +0.6% | North America and EU, regulatory-driven adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Capacity Additions in Asia-Pacific Furniture Manufacturing Hubs

Vietnam’s July 2024 start-up of a 600 m³ day line supplied by Siempelkamp underscores how exporters are back-integrating into panel production to secure feedstock and logistics certainty. Similar projects in Indonesia and the Philippines lift regional panel self-sufficiency, reduce freight exposure, and allow furniture OEMs to align substrate specs with customer finishing systems. Contractors expanding in Vietnam also establish satellite assembly lines in Cambodia and Laos to diversify labor and port risk, a pattern that multiplies MDF demand beyond the host country. Chinese producers, facing higher electricity tariffs, relocate incremental capacity to lower-cost Mekong provinces to protect margins while maintaining proximity to import customers. The medium density fiberboard market benefits as line debottlenecking and new-plant commissioning collectively add more than 6 million m³ of annual nameplate capacity in Southeast Asia between 2024 and 2026[1]Siempelkamp Maschinen- und Anlagenbau GmbH, “New MDF Line in Nghe An Starts Up,” siempelkamp.com .

Recovery in Global Residential Renovation Spending Post-Pandemic

Houzz’s 2025 homeowner sentiment survey shows kitchen and bath remodel intentions back at pre-pandemic highs, translating to heightened demand for cabinet-grade MDF panels in North America. Increased mortgage refinancing in the United States frees up discretionary funds, while energy-efficiency rebates spur window and door replacements that often specify MDF jambs and casings. In Europe, the pace is steadier because elevated energy prices delay bigger projects, yet MDF volumes hold as smaller tasks such as closet re-fronting favor thinner, paint-ready boards. Suppliers of water-repellent and fire-rated grades enjoy price premiums, offsetting resin cost inflation. The broader renovation upturn therefore underwrites baseline growth even if new housing starts soften in mature economies.

Shift From Plywood/Particleboard to Smoother MDF for RTA Furniture

Retailers selling flat-pack furniture online now mandate defect-free, uniform surfaces to minimize customer returns, tilting material choice toward MDF. Automated UV-curable coating lines in China and Poland achieve higher throughput on MDF because surface prep demands fewer filler passes than on particleboard. Brands focused on contemporary white and pastel finishes see fewer telegraphing defects when MDF is used for door and drawer fronts, driving conversion for value-oriented ranges as well. Particleboard makers answer with finer face chips and higher melamine press lines, yet cost differentials narrow once rework and paint consumption are factored in. Consequently, the medium density fiberboard market gains incremental share in décor-visible components while particleboard holds in hidden carcass structures.

Government-Backed Affordable Housing Programs in India and SE Asia

India’s Pradhan Mantri Awas Yojana targets 20 million urban homes by 2030, each requiring standardized wardrobes, kitchens and interior doors typically budgeted around 0.22 m³ of MDF per unit. The new IS 12440:2025 performance standard aligns domestic panel specs with global furniture buyers, boosting local sourcing and curbing imports. Vietnam’s social-housing blueprint likewise quotas locally made MDF in project procurement, channeling predictable volume into Mekong mills. Thailand restructures its EEC housing fund in 2025, earmarking MDF cabinetry for 45,000 low-cost units. These programs give producers long-term offtake contracts, supporting capacity-utilization rates above 85% even during private-sector slowdowns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Wood and Urea-Formaldehyde Prices Pressuring Margins | -0.6% | Global, acute in regions with limited wood fiber supply | Short term (≤ 2 years) |

| Competition from Substitute Decorative Panels (Melamine PB, WPC) | -0.4% | Global, concentrated in furniture and construction applications | Medium term (2-4 years) |

| Rising Chinese Electricity Tariffs Inflating Fibre-Refining OPEX | -0.4% | China core, spill-over to Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Wood and Urea-Formaldehyde Prices Pressuring Margins

Surging pulpwood demand from biomass energy plants in Germany and Japan tightens log supply, lifting delivered fiber costs by 9% between Q4 2024 and Q2 2025. Concurrently, natural-gas-linked methanol contracts spike, pushing urea-formaldehyde resin prices to a 15-month high. German MDF panel prices rose 1.26% in April 2024, yet producers failed to fully pass through hikes because RTA furniture buyers lock prices six months in advance. Mills mitigate volatility by shifting to in-house resin plants that blend urea with lower-cost soy flour extenders. Some Southeast Asian producers adopt longer-chip furnish to cut refining energy, but this approach risks lower face smoothness, underscoring the trade-off between cost and quality.

Competition From Substitute Decorative Panels (Melamine PB, WPC)

Melamine-faced particleboard underprices MDF by 25% in carcass applications where end users are less sensitive to telegraphing and edge-crush. Producers such as EGGER run double-decors and embossed-in-register synchronized laminates, narrowing the aesthetic gap. Wood-plastic composite (WPC) panels now offer Class B fire ratings and moisture stability, attracting door-core specifiers in humid climates. As a result, MDF loses share in exterior shutter assemblies, although WPC’s higher density limits adoption in weight-sensitive furniture. The medium density fiberboard market therefore centers its defense on specialty grades—lightweight MDF for thick doors and ultra-fine MDF for high-gloss finishes—to retain value share even where volume erodes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Furniture Drives Premium Segment Growth

The furniture segment captured 51.10% of 2025 volume, anchoring the medium density fiberboard market size near 62.28 million m³. Over 2026-2031, cabinet doors, drawer fronts and shelving sustain a 4.04% CAGR as consumers replace dated kitchens with painted shaker styles that rely on defect-free MDF cores. European builders favor moisture-resistant green-core panels for bath vanities, while North America shifts to thicker 18 mm boards for frameless cabinetry. Flooring uses, mainly laminate substrate, stabilize as luxury vinyl tile keeps displacing wood-look laminate, yet MDF remains pivotal in budget flooring where dimensional stability matters less than price.

Upgraded furniture lines integrate antibacterial laminates and super-matte lacquers, both demanding ultra-fine-sanded surfaces that particleboard struggles to provide at competitive cost. Producers in Brazil and Turkey advance value retention by co-laminating paper foil in-line, thereby shipping component blanks that reduce customer processing steps. Lightweight MDF variants leveraging poplar furnish penetrate premium interior doors by cutting leaf weight 20%, easing hinge load. These innovations reinforce the medium density fiberboard market as the substrate of choice whenever surface perfection and machinability underpin product differentiation.

By End-User Industry: Residential Renovation Sustains Demand Leadership

Residential construction and refurbishment consumed 65.91% of 2025 volume, equal to 80.33 million m³ of the medium density fiberboard market size. The sector grows 3.79% annually through 2031, propelled by aging housing stock upgrades in the United States and subsidy-driven apartment retrofits in Germany. Homeowners favor painted MDF baseboards and window stools for contemporary aesthetics. Pandemic-induced home office setups triggered desk and shelving purchases, a trend persisting as hybrid work normalizes.

Commercial and institutional applications absorb the remaining 34.09%, with office-furniture demand tempered by real-estate downsizing. However, hospitality renovations pivot toward quick-install MDF wall panels with integrated acoustic felt, shortening room turnaround times. Education and healthcare projects specify Class C flame-spread MDF for millwork, especially in nursing facilities where antimicrobial topcoats are specified. The European REACH deadline pushes both segments toward NAF and ultra-low-emitting formaldehyde grades, raising average selling prices.

Geography Analysis

Asia-Pacific solidified its lead with 60.30% of 2025 production, a position strengthened by policy-driven housing schemes in India and Vietnam that funnel predictable MDF offtake. China remains the single-largest producer, but rising electricity tariffs and stricter environmental audits encourage outbound investment to lower-cost ASEAN states. The region’s medium density fiberboard market share therefore rises in qualitative value even as incremental capacity growth disperses across multiple countries. Indian producers, aided by Biesse CNC localization hitting 80% domestic content, now meet cabinetmakers’ precision-routing needs and reduce lead times for export orders.

North America’s 20.15% share rests on renovation-heavy panel demand, especially for frameless kitchen cabinetry where MDF’s paintability justifies a price premium over plywood. U.S. mills in Georgia and North Carolina exploit abundant fast-growing pine and well-developed rail networks, sustaining competitive delivered pricing into the Midwest. Canadian suppliers capitalize on boreal fiber certification to win LEED projects while exporting surplus to the northeastern United States.

Europe emphasizes circular economy compliance. Germany and Poland install sander-dust briquette boilers and optical-sorting lines to reclaim fiber from production waste, thereby raising fiber recovery yield to 11% of intake by 2027. The EU’s 2026 formaldehyde cap compels upgrades to blow-line resin dosing and in-line press sealing, costs that many small mills cannot absorb, likely spurring consolidation. Southern Europe rebounds from earlier recessions, and Spain’s kitchen cabinet export surge lifts Iberian MDF utilization above 90%.

Competitive Landscape

The medium density fiberboard market exhibits moderate concentration; the top five producers control about 47% of global output. Industry leaders differentiate through vertical timberland integration, zero-added-formaldehyde resin technology, and closed-loop fiber recycling. Sonae Arauco’s 2025 start-up of the world’s first industrial MDF recycling line in Portugal demonstrates early-mover advantage in circular manufacturing. Swiss Krono’s acquisition of Collins Pine’s Oregon fiber operations in 2025 secures raw-material self-sufficiency ahead of Pacific Northwest log-export restrictions.

Cost pressures motivate rationalization: Roseburg shuttered its Missoula particleboard plant in 2024 to redirect resources to higher-margin MDF lines. West Fraser indefinitely curtailed its Florida sawmill in 2024, highlighting ongoing fiber scarcity. Disruptive entrants explore agro-waste fiber such as date-palm fronds; Dieffenbacher’s pilot plant in Saudi Arabia targets 100,000 m³ capacity, addressing desert-region fiber deficits.

Technological advances center on refining energy reduction; variable-speed motor upgrades and steam-recovery condensers cut electricity by 7% per m³. Inline X-ray thickness gauges, AI-driven surface-defect vision systems and automatic sanding optimize yield and quality. Market leaders funnel capital into such upgrades even as they slow greenfield expansion, prioritizing margin resilience over volume share grabs.

Medium Density Fiberboard (MDF) Industry Leaders

Kronoplus Limited

ARAUCO

EGGER

Swiss Krono Group

Kastamonu Entegre

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GREENPANEL INDUSTRIES LIMITED launched a new production line at its Srikalahasti facility in Andhra Pradesh, India. The expansion increased the company's annual MDF production capacity to 891,000 cubic meters. The company also introduced thin MDF products ranging from 1.5mm to 1.7mm.

- July 2024: MDF Mekong commenced MDF production at its new plant in Phu Tho Province, Vietnam. The facility features a Siempelkamp continuous press line with a ContiRoll press designed to process local acacia and eucalyptus wood. The plant has an annual production capacity exceeding 400,000 cubic meters.

Global Medium Density Fiberboard (MDF) Market Report Scope

Medium-density fiberboard (MDF) is produced with the help of a wide range of lignocellulosic fibers, including agrofibers, recycled wood, and other low-value wood by-products. Medium-density fiberboard (MDF) or dry-process fiberboards have a fiber moisture content of less than 20% at the stage of forming and a density 450 kg/m3. These boards are essentially produced under heat and pressure, with the addition of a synthetic adhesive. The medium-density fiberboard (MDF) market is segmented by application, end-user sector, and geography. By application, the market is segmented into a cabinet, flooring, furniture, molding, door and millwork, packaging system, and other applications. The end-user sector segments the market into residential, commercial, and institutional. The report also covers the market size and forecasts for the medium-density fiberboard (MDF) market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (million cubic meters).

By Application

| Furniture |

| Cabinet |

| Flooring |

| Molding, Door, and Millwork |

| Packaging System |

| Other Applications |

By End-Use Industry

| Residential |

| Commercial |

| Institutional |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Furniture | |

| Cabinet | ||

| Flooring | ||

| Molding, Door, and Millwork | ||

| Packaging System | ||

| Other Applications | ||

| By End-Use Industry | Residential | |

| Commercial | ||

| Institutional | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What volume will the medium density fiberboard market reach by 2031?

Supply is forecast to hit 152.05 million cubic meters by 2031, rising at a 3.76% CAGR.

Which region leads global MDF production?

Asia-Pacific holds 60.30% of 2025 output and should grow faster than the global average through 2031.

Why do furniture makers prefer MDF to particleboard?

Uniform density and smoother faces lower sanding and coating costs while improving painted finish quality.

How will new formaldehyde limits affect MDF?

EU rules effective 2026 favor polymeric MDI and bio-based resins, enabling price premiums for low-VOC boards.

Page last updated on: