Kitchen Cabinets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 95.95 Billion |

| Market Size (2031) | USD 124.42 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kitchen Cabinets Market Analysis by Mordor Intelligence

The kitchen cabinets market size was valued at USD 91.07 billion in 2025 and estimated to grow from USD 95.95 billion in 2026 to reach USD 124.42 billion by 2031, at a CAGR of 5.36% during the forecast period (2026-2031). Steady renovation outlays in North America and Europe, rapid apartment construction in the Asia-Pacific, and accelerating e-commerce adoption collectively anchor demand. Regulatory requirements for low-emission substrates, rising home-equity levels, and automation investments further reinforce growth momentum. Meanwhile, skilled-labor shortages and input-price swings encourage manufacturers to standardize components and embrace prefabricated designs. Consolidation among leading players lifts operational scale yet keeps room for regional specialists, sustaining healthy rivalry across the kitchen cabinets market through 2030.

Key Report Takeaways

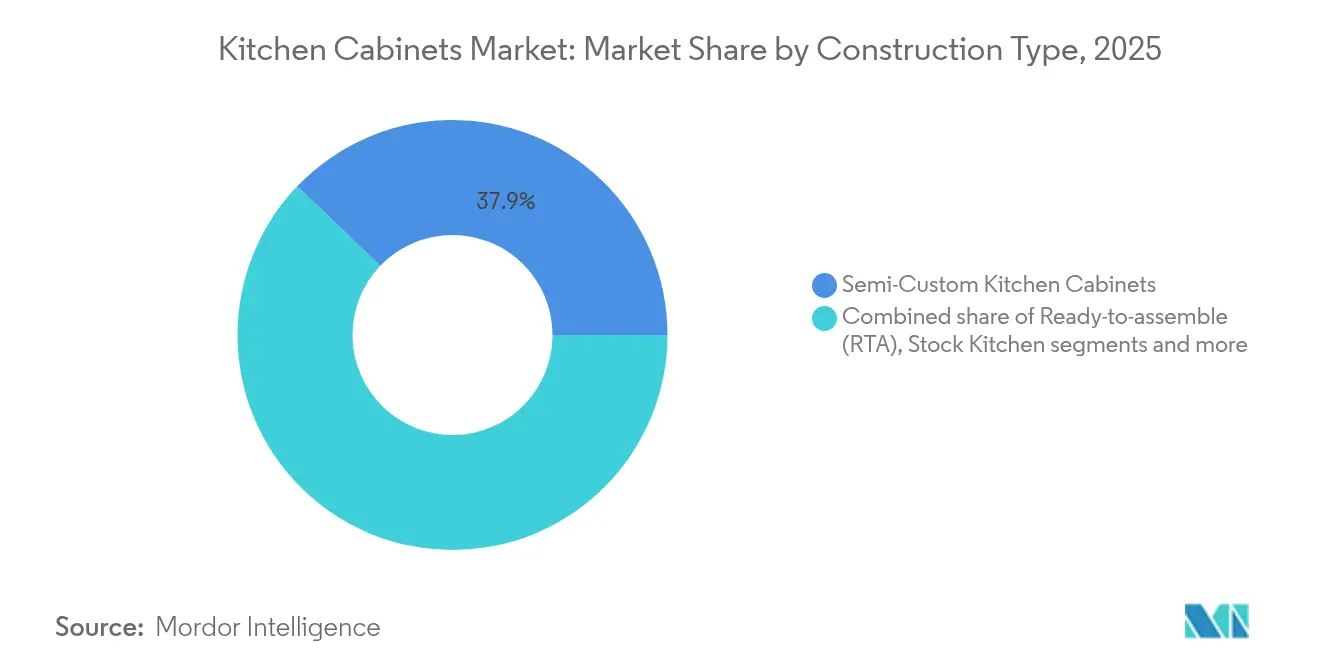

- By construction type, semi-custom cabinets led with 37.85% of the kitchen cabinets market share in 2025, while ready-to-assemble units are projected to post the fastest 6.36% CAGR through 2031.

- By material, wood retained 60.15% of global revenue in 2025, whereas other raw materials, principally bamboo and recycled composites, are advancing at a 5.72% CAGR on tightening emissions rules.

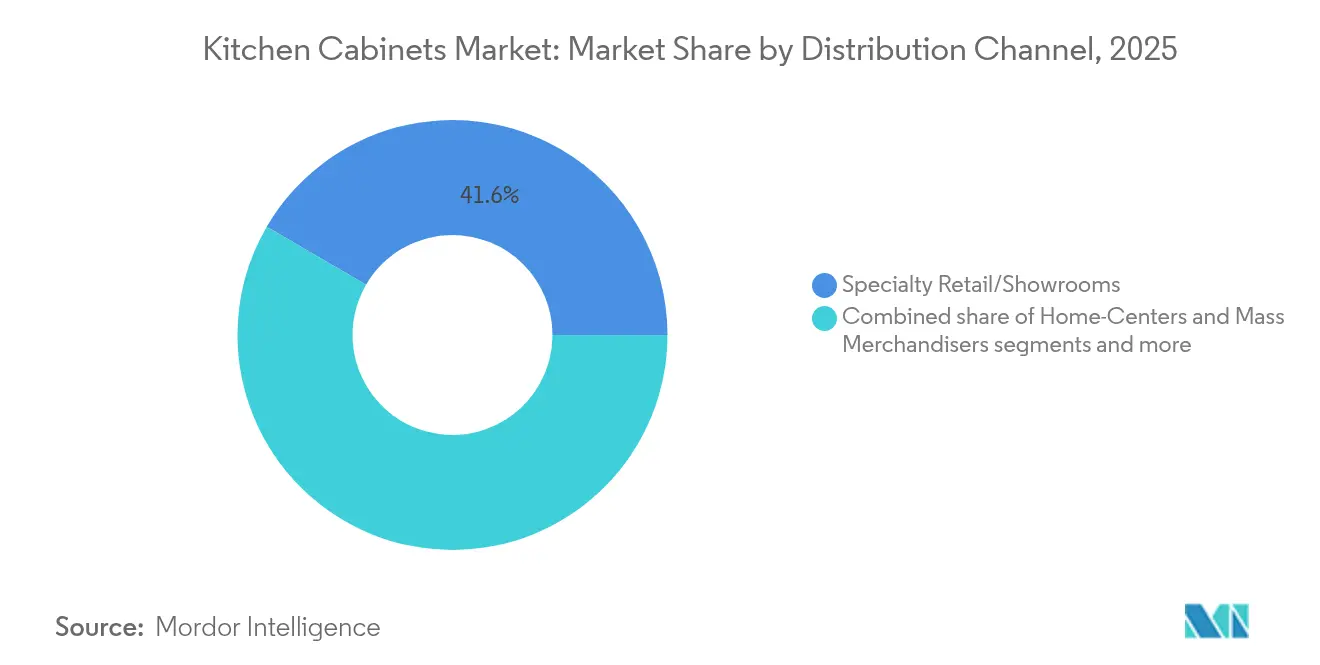

- By distribution channel, specialty retail and showrooms captured 41.60% of sales in 2025, yet contractor/trade direct pipelines are expanding at a 6.50% CAGR as builders push for negotiated pricing and timed deliveries.

- By end user, residential installations generated 82.35% of 2025 revenue, whereas commercial applications are forecast to climb at a 7.65% CAGR through 2031 on hospitality and office fit-out growth.

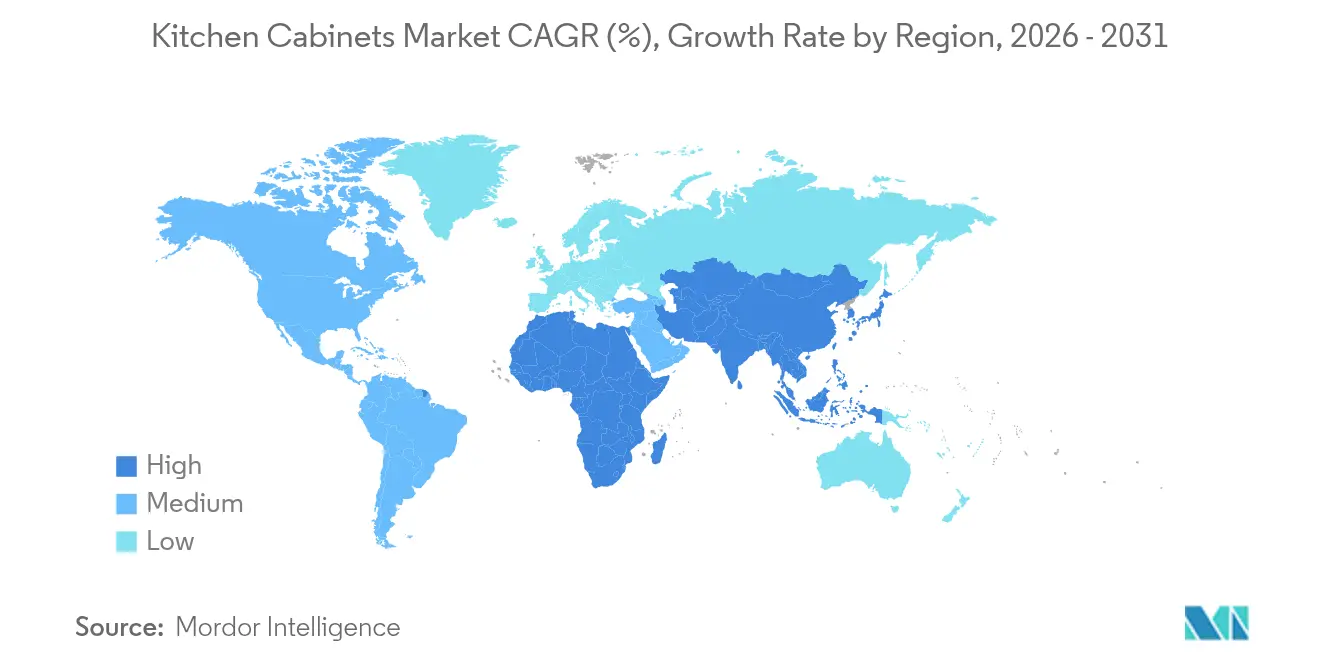

- By geography, North America held 34.55% of the 2025 value, while Asia-Pacific is set to outpace all other regions with a 6.07% CAGR through 2031 on sustained urban apartment construction.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kitchen Cabinets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential renovation boom in mature economies | +1.2% | North America & Europe | Medium term (2-4 years) |

| Urban apartment growth in Asia-Pacific | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| E-commerce-driven RTA cabinet penetration | +0.9% | Global, early gains in North America & Europe | Short term (≤ 2 years) |

| Frameless cabinetry uptake in micro-apartments | +0.7% | Asia-Pacific core, European urban centers | Medium term (2-4 years) |

| Bamboo & fast-renewable materials compliance | +0.5% | Global, led by California & the EU | Long term (≥ 4 years) |

| AI-enabled mass-customization platforms | +0.4% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Residential Renovation Boom in Mature Economies

Solid labor markets and record home-equity levels give homeowners the financial latitude to upgrade kitchens rather than relocate. Harvard researchers foresee a 1.2% uptick in owner-occupied remodeling outlays for 2025[1]Joint Center for Housing Studies, “Modest Gains in 2025 Outlook for Home Remodeling,” jchs.harvard.edu. The National Association of Home Builders anticipates a 5% lift in overall remodeling, citing a surge in homes aged 20-39 years that will peak at 24.2 million by 2027. Kitchen projects consistently deliver top “Joy Scores,” motivating discretionary spending on semi-custom fixtures and smart storage. Homeowners also value energy-efficient lighting and soft-close hardware that elongate lifecycle and curb noise. These factors keep average selling prices firm, sustaining margin strength for suppliers in the kitchen cabinets market. Furthermore, renovation incentives tied to aging-in-place programs spur accessibility upgrades such as pull-down shelves and wider drawer rails, expanding demand for tailored solutions.

Urban Apartment Growth in Asia-Pacific

Asia-Pacific’s demographic shift drives an unparalleled pipeline of compact units that rely on modular cabinetry. China’s urban population surpassed 930 million in 2024, while renovation subsidies have upgraded 44.34 million dwellings since 2019. India must erect up to 100 million homes this decade as 70 million households cross ownership thresholds. Large cities such as Guangzhou and Chengdu plan to absorb millions more residents by 2035, anchoring long-term installation volume. Developers favor frameless boxes that maximize cubic inches without expanding footprints. Height-adjustable wall cabinets and pull-out pantries cater to ergonomic needs in tight quarters, elevating functionality. Rising disposable incomes translate into a willingness to pay for premium finishes, pushing per-unit revenue higher and reinforcing regional outperformance within the kitchen cabinets market.

E-Commerce-Driven RTA Cabinet Penetration

Digital retail removes geographic barriers and opens price-transparent marketplaces for cabinetry. Asia-Pacific will capture 61% of global retail e-commerce by 2025, with cross-border orders expanding at a 29% CAGR[2]Asian Development Bank, “E-Commerce Evolution in Asia and the Pacific,” adb.org. IKEA’s USD 2.2 billion omnichannel push adds 900 pickup sites, illustrating how click-and-collect smooths bulky-item logistics. Standardized RTA SKUs allow carriers to consolidate shipments, lowering freight expense and carbon footprint. Younger buyers appreciate transparent lead times and online configuration tools that visualize finishes in augmented reality. Influencer-led tutorials demystify self-assembly, expanding DIY adoption. As fulfillment networks mature, online volume steadily carves share from traditional showrooms, raising competition and price transparency across the kitchen cabinets market.

Frameless Cabinetry Uptake in Micro-Apartments

Eliminating face frames enlarges interior clearances by 10-15%, a crucial benefit where kitchens average less than 70 square feet in high-density Asian cities. European minimalist styling influences global taste, encouraging sleek slab doors and concealed hinges. Frameless boxes simplify robotic manufacturing because fewer frame components and wider tolerances suit line automation. Builders specify full-access designs to differentiate projects marketed toward young urban professionals. Upselling frameless hardware, such as soft-close slides and integrated lighting, elevates average ticket size while satisfying premium aesthetics. As architects prioritize continuous sight lines, frameless layouts become a default blueprint in emerging apartment developments, driving sustained unit demand in the kitchen cabinets market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.8% | Global, acute in North America | Short term (≤ 2 years) |

| High upfront cost of custom cabinetry | -0.6% | North America & Europe | Medium term (2-4 years) |

| Skilled-installer shortages | -0.5% | Global, severe in North America | Long term (≥ 4 years) |

| Stricter IAQ emissions standards | -0.3% | Global, led by California & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Softwood prices spiked 23% year-over-year in April 2025, and prospective duty hikes on Canadian imports from 14.5% to 34.5% threaten further escalation[3]CNBC, “How Lumber Duties Could Worsen Home Affordability in the U.S.,” cnbc.com. Canada supplies 85% of U.S. softwood imports, making the tariff lever a potent disruptor. Engineered-wood antidumping duties on Vietnamese plywood cost American Woodmark USD 4.9 million in fiscal 2024. Volatile pricing complicates bid validity periods, pushing contractors to insert escalation clauses that dampen customer confidence. Manufacturers hedge through forward contracts and diversify sourcing, yet pass-through timing lags depress margins when spikes hit suddenly. Persistent swings therefore trim volume growth and muddy forecasting for the kitchen cabinets market.

High Upfront Cost of Custom Cabinetry

Custom lines can cost 2-3 times more than stock equivalents, stretching project budgets and tempering adoption among mid-income homeowners. Lengthy lead times averaging 25 days add financing strain, especially when interest rates rise, forcing remodelers to stage payments over longer horizons. Price sensitivity channels many buyers toward semi-custom or RTA kits, constraining premium-segment expansion. Builders of mid-range tract homes often cap kitchen allowances, making full custom unattainable in standard packages. While affluent consumers sustain demand at the luxury end, broad-based penetration remains limited, shaving a modest 0.6 percentage point from forecast CAGR in the kitchen cabinets market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Construction Type: Semi-Custom Leads While RTA Accelerates

Semi-custom cabinets accounted for 37.85% of the kitchen cabinets market share in 2025, reflecting consumer appetite for tailored door styles and finishes that still meet mid-range budgets. The segment benefits from dealer showrooms that use design software to translate homeowner mood boards into buildable specs within hours, holding customer attention during a crucial decision window. At the opposite end of the speed spectrum, ready-to-assemble lines can ship in four to seven days versus the 25-day average for made-to-order products, enabling rapid renovation cycles that appeal to younger, time-pressed buyers. Stock formats remain relevant for entry-level buyers, yet their flat pricing leaves little room for upsell, pushing many retailers to migrate floor space toward semi-custom displays that drive higher margins. Custom cabinetry, while the smallest slice of the kitchen cabinets market size, retains a loyal luxury clientele willing to wait months for hand-finished craftsmanship and exotic veneers.

Ready-to-assemble demand is climbing at a 6.36% CAGR due to e-commerce marketplaces that simplify price comparison and doorstep delivery. IKEA’s network of roughly 900 U.S. pickup lockers eases last-mile barriers, encouraging shoppers to order flat-packs online and collect them at neighbourhood hubs. Traditional manufacturers counter by launching “quick-ship” frameless series and investing in robotic dowel insertion that mimics RTA efficiency while keeping semi-custom flexibility. Builders also value RTA for multifamily projects because standardized carcasses streamline installation sequencing and reduce punch-list callbacks. As labor shortages persist, construction crews gravitate toward cabinet systems pre-fitted with clip-on rails and adjustable legs, reinforcing the growth runway for the RTA format within the broader kitchen cabinets market.

By Material: Wood Dominance Faces Sustainable Alternatives

Wood captured 60.15% of global revenue in 2025, buoyed by its warm aesthetics, familiar machining techniques, and ease of on-site touch-up. Oak, maple, and birch remain the staples for North American buyers, whereas European consumers gravitate toward painted MDF with smooth edges that suit frameless furniture trends. Despite raw-material volatility, wood vendors leverage domestic lumber contracts to reduce tariff exposure, maintaining reliable lead times for volume builders. Stain-grade doors offer refinishability that prolongs service life, a trait homeowners factor into total-cost-of-ownership calculations. These attributes keep wood the keystone substrate for premium and mid-tier price points across the kitchen cabinets market.

The fastest growth sits in the “other raw materials” bucket, advancing at 5.72% CAGR as bamboo, recycled composites, and ultra-low-emitting particleboard satisfy stricter emission caps. California Air Resources Board Phase 2 formaldehyde limits push factories to adopt no-added-formaldehyde adhesives and water-borne lacquers that shrink off-gassing windows. Manufacturers pursuing ISO 14001 certification document carbon savings from bamboo, which matures in one-tenth the time of hardwoods and sequesters more CO₂ per hectare. Recycled PET-wood hybrids divert plastic from landfills while providing moisture resistance favoured in coastal installations. Commercial specifiers now mandate Environmental Product Declarations, accelerating alternative-material adoption in office, hospitality, and health-care projects. These dynamics gradually rebalance the kitchen cabinets market share mix without displacing wood’s cultural cachet.

By Distribution Channel: Showrooms Retain Influence, Contractor Direct Scales

Specialty retail and design showrooms secured 41.60% of 2025 sales, offering tactile door samples, lighting mock-ups, and in-house designers who walk clients through software-based renderings. Demonstration kitchens let homeowners test drawer glides and hinge soft-close action, anchoring higher conversion rates for semi-custom and custom orders. Home centers appeal to DIY shoppers who value one-stop trips for cabinets, paint, and hardware, although their product depth skews toward entry-level lines. Online platforms extend reach to rural customers, providing 3-D planners and augmented-reality apps that overlay cabinets onto smartphone photos. Despite digital advances, complex renovation buyers still prefer at least one in-person consultation before placing a five-figure order, preserving brick-and-mortar relevance.

Contractor and trade-direct programs are growing at a 6.50% CAGR as builders seek competitive rebates and synchronized deliveries that align with tight critical-path schedules. American Woodmark reports that builders and independent dealers now account for nearly 60% of revenue, confirming the segment’s clout. Large multifamily developers negotiate project-bundled pricing, cutting administrative overhead and minimizing change-order risk. Digital portals let contractors track order status, arrange staggered drop shipments, and download installation guides that reduce job-site errors. IKEA’s Plan & Order studios illustrate omnichannel fusion, where consumers design layouts online, finalize picks with an advisor, and collect flat-packs curbside within days. As the reliability of delivery remains paramount, factory-direct and hybrid models will continue carving share from traditional stocking distributors within the kitchen cabinets market.

By End User: Residential Core Stable, Commercial Upside Strengthens

Residential projects contributed 82.35% of total revenue in 2025, buoyed by remodels that transform dated galley kitchens into open-concept hubs for work and socializing. High “Joy Scores” assigned to kitchen makeovers fuel homeowners’ willingness to invest in upgraded storage accessories, integrated LED strips, and contrasting island colors. Mortgage-rate volatility steers many households toward renovate-rather-than-relocate decisions, stabilizing baseline cabinet demand. Aging-in-place retrofits like pull-down upper-cabinet shelves and soft-close lifts open new pockets of growth among baby boomers. These features command modest premiums that lift average selling prices and strengthen profitability across the residential slice of the kitchen cabinets market.

Commercial installations are projected to rise at a 7.65% CAGR through 2031, driven by hospitality renovations, quick-service restaurant rollouts, and office amenity upgrades that include staff kitchens. Designers specify fire-rated, antimicrobial carcasses and metal toe kicks that endure heavy traffic, raising unit values well above residential equivalents. Open-kitchen restaurant concepts showcase chef stations, prompting demand for durable yet visually striking fronts that align with brand aesthetics. Corporate wellness programs add fully equipped break rooms to attract and retain talent, generating steady retrofit opportunities. Institutional buyers universities, hospitals, and military housing, lean on KCMA Severe-Use certification to vet products for long service cycles, creating a moat for compliant suppliers. Collectively, these factors diversify revenue streams and buffer the kitchen cabinets market against residential cyclicality.

Geography Analysis

North America captured 34.55% of global revenue in 2025, undergirded by robust remodeling and aging inventory. Owner-occupied improvement outlays will inch 1.2% higher in 2025, while Canada’s high-value markets, such as Toronto and Vancouver, chase premium finishes. Affluent consumers’ willingness to pay for customization keeps margin profiles attractive, sustaining leadership for the region within the kitchen cabinets market size metrics.

Asia-Pacific is progressing at a 6.07% CAGR through 2031, propelled by mega-city programs and surging middle-class consumption. China’s 66.16% urbanization rate and 44.34-million-unit renovation drive highlight deep renovation potential. India’s demand outlook, pegged at 100 million incremental homes, multiplies cabinet opportunities. Rising apartment towers elevate volume, while aspirational tastes lift per-unit spend, cementing Asia-Pacific as the fastest growth vector in the kitchen cabinets market.

Europe contributes steady replacement demand anchored in design leadership and environmental compliance. Frameless systems pioneered in Germany and Italy shape global aesthetics, while stringent VOC limits push innovation toward water-borne finishes. Middle Eastern and African markets enjoy greenfield potential linked to tourism megaprojects and social-housing budgets. Latin America’s currency volatility tempers immediate growth yet offers upside as macro stability returns. Diversified regional demand underpins broad resilience for the kitchen cabinets market.

Regulatory Landscape

Indoor air quality and emissions compliance remains a core requirement for cabinet substrates and finishes, particularly where engineered wood is used. In the United States, the Environmental Protection Agency administers the Formaldehyde Emission Standards for Composite Wood Products under TSCA (40 CFR Part 770), shaping material selection (including no-added-formaldehyde resins) and driving tighter factory quality-control practices across MDF, particleboard, and plywood inputs.

In Europe, product compliance is being reframed by the Construction Products Regulation, Regulation (EU) 2024/3110, which applies from January 8, 2026. For cabinet systems sold through construction-led channels, the shift toward harmonized performance assessment and expanded sustainability-related requirements raises the documentation and traceability bar for manufacturers and their component suppliers, affecting how products are specified for projects and tendered through building supply chains.

Value Chain Analysis

The kitchen cabinet value chain starts with upstream suppliers of hardwood lumber and softwood, engineered wood panels (MDF, particleboard, hardwood plywood), resins and adhesives, decorative surfaces (laminates, veneers, PET films), and hardware such as hinges, slides, drawer systems, and pulls. Cabinet manufacturers convert these inputs through panel processing, CNC routing/drilling, edging, finishing (paint, lacquer, laminations), and assembly into stock, semi-custom, custom, and ready-to-assemble (RTA) formats. Packaging design becomes especially important for RTA and e-commerce shipments because it affects both damage rates and freight efficiency.

Downstream routes include specialty retail and showrooms with design services, home-centers and mass merchandisers, online platforms, and contractor/trade-direct programs serving builders and multifamily projects. Installation contractors and carpenters complete the last mile, where skilled-labor shortages lift the value of standardized, easy-to-install systems. Standards and certification programs from bodies such as KCMA (ANSI/KCMA A161.1), AMK, and CKCA influence procurement, while tariffs and wood-panel price volatility encourage dual sourcing and support regional manufacturing clusters (including the Southeast United States and China manufacturing hubs) to reduce lead-time risk.

Competitive Landscape

The global kitchen cabinets market exhibits moderate consolidation with increasing merger and acquisition activity reshaping competitive dynamics. Mergers and acquisitions are redrawing competitive lines as manufacturers chase raw-material leverage, automated capacity, and distribution reach. MasterBrand’s USD 520 million purchase of Supreme Cabinetry Brands and its subsequent all-stock merger with American Woodmark, creating a USD 2.4 billion equity entity, demonstrates the scale thesis now driving boardroom agendas. The combined company expects USD 120 million in three-year costs from procurement pooling and plant consolidation, signaling intensified price competition for mid-tier dealers and builders.

Technology investments form the second battleground. Nobia AB’s asset-light restructuring closes under-performing U.K. showrooms and redirects capital to a lights-out factory in Jönköping featuring robotic dowel insertion and AI-driven quality scans. American Woodmark’s new North Carolina and Mexico plants add 15% capacity with automated assembly cells that cut cycle times and reduce labor dependency, directly addressing installer shortages that plague North American job sites.

Channel innovation rounds out the competitive playbook. IKEA’s USD 2.2 billion omnichannel expansion layers nine Plan & Order studios and roughly 900 pickup lockers onto its existing footprint, marrying digital configurators with curbside convenience to siphon volume from independent showrooms. Traditional cabinet firms respond by launching web-based design portals, quick-ship frameless lines, and sustainability-badged collections that target eco-aware millennials. As the top five suppliers now control just over half of the global revenue, competitive intensity remains moderate, leaving viable niches for regional specialists that excel in bespoke craftsmanship or local-code compliance.

Kitchen Cabinets Industry Leaders

IKEA

American Woodmark

Nobilia

Oppein

Nobia AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sustainability-led product differentiation is a clear opportunity as emissions limits and environmental documentation requirements tighten. Demand signals already point to wider use of bamboo, recycled composites, and ultra-low-emitting boards in the material mix, supported by compliance needs tied to formaldehyde controls under US EPA TSCA Title VI (40 CFR Part 770) and Europe's sustainability-driven compliance direction under Regulation (EU) 2024/3110 applying from January 8, 2026. Manufacturers that can deliver consistent low-emission performance, documented chain-of-custody, and repeatable finishes can strengthen positioning across both residential remodeling and commercial specification workflows.

Channel and operating-model opportunities are concentrated in RTA and hybrid semi-custom programs that simplify installation and improve delivery predictability for contractors and e-commerce customers. IKEA's USD 2.2 billion US omnichannel expansion plan, including additional Plan & Order points and roughly 900 pickup lockers, illustrates how fulfillment infrastructure and click-and-collect can move bulky cabinetry orders into faster, more standardized pipelines. On the manufacturing side, automation and quality-scanning investments align with frameless and modular designs that reduce part complexity and help stabilize output where labor is constrained, supporting faster-ship assortments for builders and multifamily timelines.

Recent Industry Developments

- May 2026: MasterBrand completed its all-stock merger with American Woodmark, making American Woodmark a wholly owned subsidiary and consolidating operations under the MasterBrand name. The combination increases scale across North American cabinet manufacturing and distribution, supporting broader portfolio coverage across stock and semi-custom tiers. Integration priorities such as procurement pooling and footprint rationalization raise competitive pressure on mid-tier suppliers that rely on builder and dealer channels.

- February 2026: Nobilia released its 2026 kitchen collection with system updates such as new 762 mm wide units, standardized 110-degree hinges on access doors, and new modular storage concepts like the FurnSpin swivel base unit. The refresh supports planning flexibility for compact kitchens while improving installation consistency through standardized fittings. This strengthens Nobilia's ability to serve both showroom-led design projects and repeatable developer specifications that favor modularity.

- June 2024: IKEA committed USD 2.2 billion to expand its US footprint over three years, adding new stores, Plan & Order points, and roughly 900 pickup lockers to support omnichannel fulfillment of large-format home goods including RTA cabinetry. The initiative improves last-mile convenience and lead-time transparency for online-first cabinet purchases. It also increases competitive pressure for traditional showrooms by pairing digital planning tools with lower-friction pickup and delivery options.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market covers kitchen cabinets sold for residential and commercial kitchens, measured in revenue terms across common cabinet types and materials, and tracked through offline and online routes to market. Values reflect what customers pay for cabinet units and built-in kitchen storage systems supplied into the market.

Scope exclusions: We exclude non-kitchen furniture items such as tables and chairs, kitchen appliances, and stand-alone storage that is not sold as a kitchen cabinet solution.

Segmentation Overview

- By Construction Type

- Ready-to-assemble (RTA) Kitchen Cabinets

- Stock Kitchen Cabinets

- Semi-Custom Kitchen Cabinets

- Custom Kitchen Cabinets

- By Material

- Wood

- Metal

- Other Raw Materials

- By Distribution Channel

- Specialty Retail/Showrooms

- Home-Centers & Mass Merchandisers

- Online

- Contractors/Trade Direct

- By End User

- Residential

- Commercial (Hospitality, Offices, Others)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX

- NORDICS

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base demand story and to anchor the model with repeatable, public signals that track housing and remodeling activity. We leaned on sources such as the US Census Bureau (housing starts and permits), Eurostat (construction output and housing), UN Comtrade (cabinet and furniture trade flows), and the International Trade Administration for country-level construction context. When we needed a sharper view on product innovation and material shifts, we also reviewed patent databases and peer-reviewed papers on wood panels, coatings, and cabinetry finishes.

We then compared these signals with company filings, investor presentations, and reputable press coverage to understand channel mix changes and pricing pressure from inputs like wood panels and metals. A paid subscription for company financials and news was also used to speed up cross-checks on revenue exposure and geographic footprint where disclosures were available. The sources listed here are illustrative only, and we reviewed additional public and paid references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what the desk indicators could not show cleanly, especially the share split between RTA, stock, semi-custom, and custom cabinets, and how pricing moves with material and labor availability. Interviews were held with manufacturers, distributors, installers, retailers, and commercial project buyers across major regions, so we could adjust assumptions on volume, lead times, and channel margins before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 46% |

| Mid tier: 44% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 20% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started with a top-down build where housing completions, renovation spending intensity, and commercial fit-out activity were converted into a cabinet demand pool, and then filtered by kitchen penetration and replacement cycles. Price was handled through a blended average selling price that moves with cabinet mix (RTA, stock, semi-custom, custom), material choice, and the offline versus online share, and that mix was checked during interviews.

To keep the totals realistic, we also ran selective bottom-up approximations using supplier roll-ups, sampled price points from retail and contractor quotes, and then did basic channel checks on typical order sizes. Where gaps showed up, the model was adjusted. Forecasting relied on scenario analysis tied to forward indicators like housing starts and permits, residential remodeling activity, and commercial construction outlook. Input-cost direction (wood-based panels, hardware, and labor) was used to shape price progression. Where country detail was thin, we filled gaps using regional proxies from trade flows and construction growth, then re-tested the implied per-household and per-project spend with primary feedback.

Data Validation & Update Cycle

Totals were validated through multiple checks so no single data series could overly drive the outcome. We compared the final market values against independent signals like cabinetry trade movement, housing activity, and reported revenue exposure from publicly listed players. We also reviewed outliers at the country and region level before sign-off.

A second analyst review is done to confirm definitions, math flow, and year-to-year movements, followed by re-contacting interviewees when a variance cannot be explained by known events. The report is refreshed annually, and interim updates are made when major shifts occur in housing, remodeling, or input costs. Before delivery, we complete a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Kitchen Cabinets Market Size Compared Against Other Published Estimates

Published market values for kitchen cabinets can differ quite a lot, even when the growth story sounds similar, because the market can be stretched into adjacent kitchen furniture or counted at different points in the supply chain. Differences also come from how each study treats RTA versus custom mixes, how commercial projects are captured, and how currency timing is handled for multi-country totals.

In our work, the spread usually comes from what gets counted as a kitchen cabinet sale, along with whether prices are modeled as a simple inflation uplift or rebuilt from mix changes and input trends. Some estimates include factory-gate revenues for built-in kitchen units, while demand-linked totals count cabinets when they are sold through retail, project, or contractor channels. This scope split shows up in the 2026 value of USD 95.95 B published by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 95.95 B (2026) | |

| Global Consultancy A | USD 107.86 B (2025) | Uses a different base year and a broader product treatment that can extend into wider cabinetry styles and related built-in storage, which lifts the total before forecasting assumptions are applied. |

| Industry Publisher B | USD 177.68 B (2025) | Reported values are framed as factory-gate manufacturer revenues for built-in kitchen units, which can sit above demand-side totals that follow what end users pay through channels. |

Looking at the table, the gap is mainly explained by scope and value-chain placement rather than a disagreement on underlying construction activity. When the definition stays focused on kitchen cabinet demand, and the pricing path is connected to mix and input-cost direction, the resulting market value stays traceable and easier to re-check year over year.

Key Questions Answered in the Report

What is the current valuation of the global kitchen cabinets market?

The kitchen cabinets market is valued at USD 95.95 billion in 2026.

How quickly is the global kitchen cabinets market expected to grow?

It is projected to post a 5.36% CAGR between 2026 and 2031.

Which construction type is expanding fastest within the kitchen cabinets market?

Ready-to-assemble products are growing at a 6.36% CAGR due to e-commerce convenience.

Why is Asia-Pacific the most dynamic geography for kitchen cabinets?

Rapid urbanization and large-scale apartment construction are driving a 6.07% regional CAGR through 2031.

How are sustainability regulations affecting the kitchen cabinets market?

Formaldehyde limits are encouraging the adoption of bamboo, recycled composites, and no-added-formaldehyde resins.

What impact do skilled-installer shortages have on the kitchen cabinets market?

Labor gaps extend project timelines and spur demand for simplified installation systems, slightly tempering shipment growth.

Page last updated on: