Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

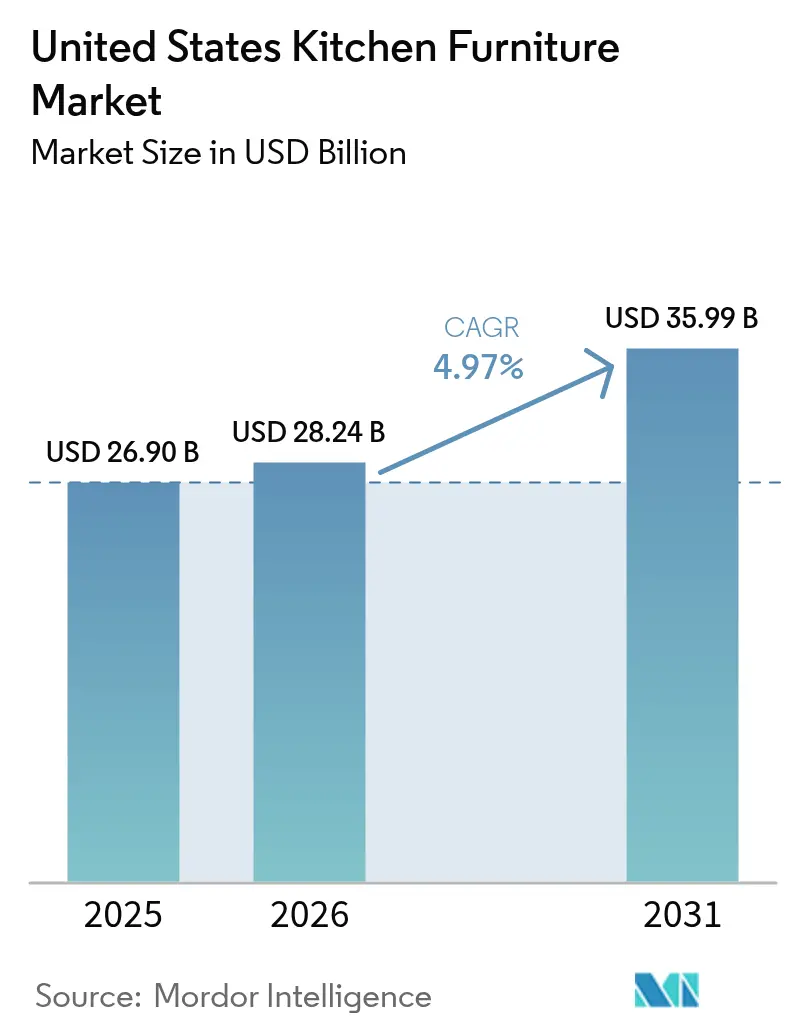

| Base Year Market Size (2025) | USD 26.90 Billion |

| Market Size (2026) | USD 28.24 Billion |

| Market Size (2031) | USD 35.99 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

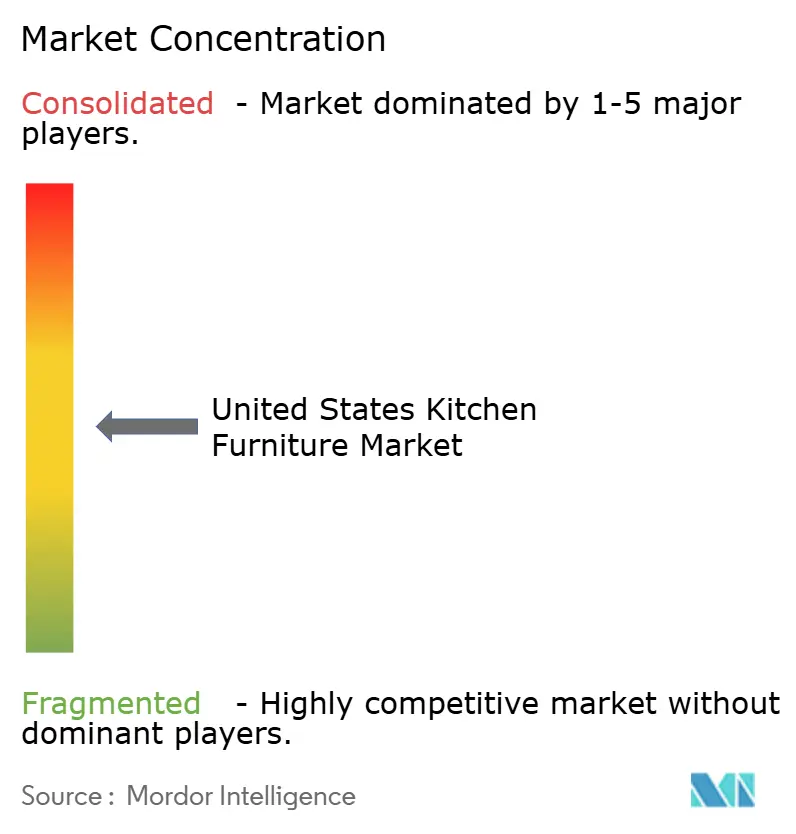

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Kitchen Furniture Market Analysis by Mordor Intelligence

The United States kitchen furniture market size was valued at USD 26.90 billion in 2025 and estimated to grow from USD 28.24 billion in 2026 to reach USD 35.99 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Consumers are increasingly viewing kitchens not just as places to cook, but as multifunctional hubs for socializing and remote work, driving this growth trajectory. Aging housing stock, digital transformation, skilled-labor scarcity, and rising appetite for premium solutions are rewriting design priorities, channel strategies, and pricing dynamics. A robust replacement cycle tied to older housing, persistent labor shortages, and fast-rising demand for ready-to-assemble (RTA) formats is reinforcing growth. The competitive landscape features MasterBrand Cabinets leading through strategic acquisitions and operational efficiencies, while American Woodmark pivots toward automation. Cabinetry remains the focal point of most projects, and frameless European construction, outdoor-rated solutions, and digital planning tools are reshaping product design and routes to market. While volatile lumber prices and installation bottlenecks weigh on margins, mid-range products continue to resonate with value-seeking homeowners, and premium lines are outpacing the overall United States kitchen furniture market as affluent households invest in bespoke, tech-integrated spaces. Together, these trends drive investment in lean production, omnichannel engagement, and selective consolidation as manufacturers seek scale advantages in purchasing, manufacturing, and distribution.

Key Report Takeaways

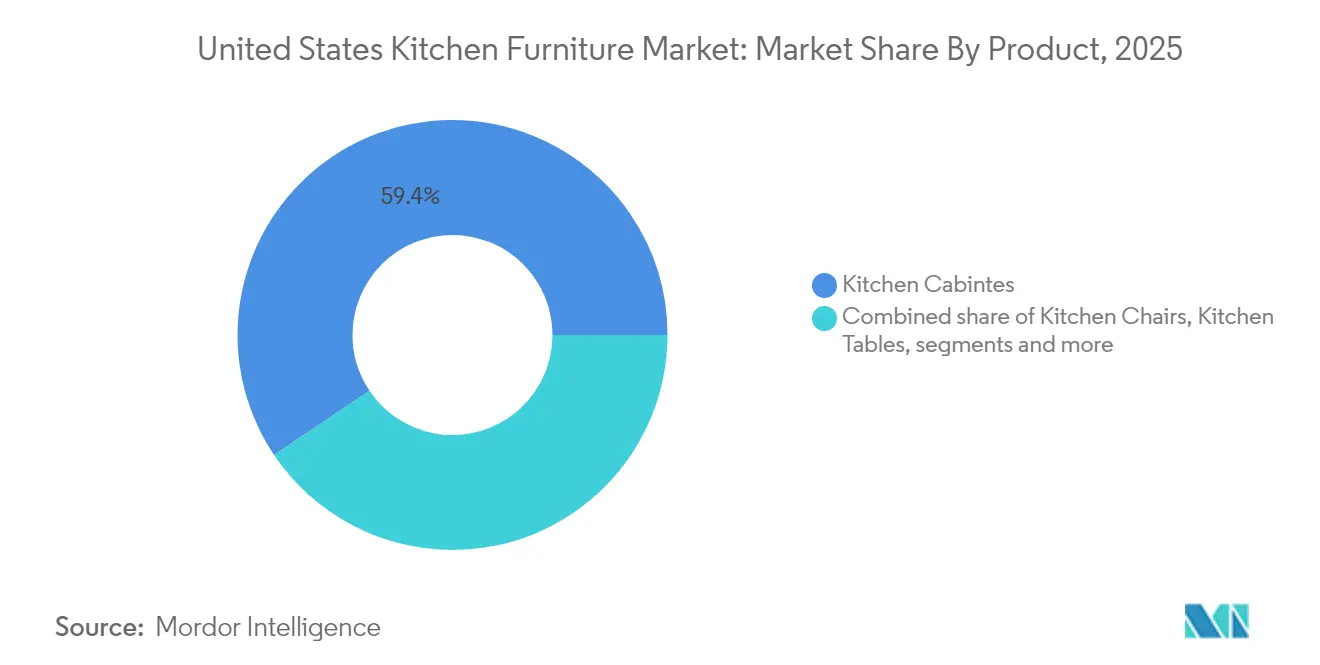

- By product category, kitchen cabinets led with 59.42% of the United States kitchen furniture market share in 2025, while pantry shelving and storage recorded the highest forecast CAGR at 5.72% through 2031.

- By material, wood accounted for 60.88% of the United States kitchen furniture market size in 2025; stainless-steel components are forecast to expand the fastest at a 6.02% CAGR to 2031.

- By price range, the mid-range segment commanded 54.35% of the United States kitchen furniture market size in 2025; the premium tier is set to grow 4.82% annually to 2031.

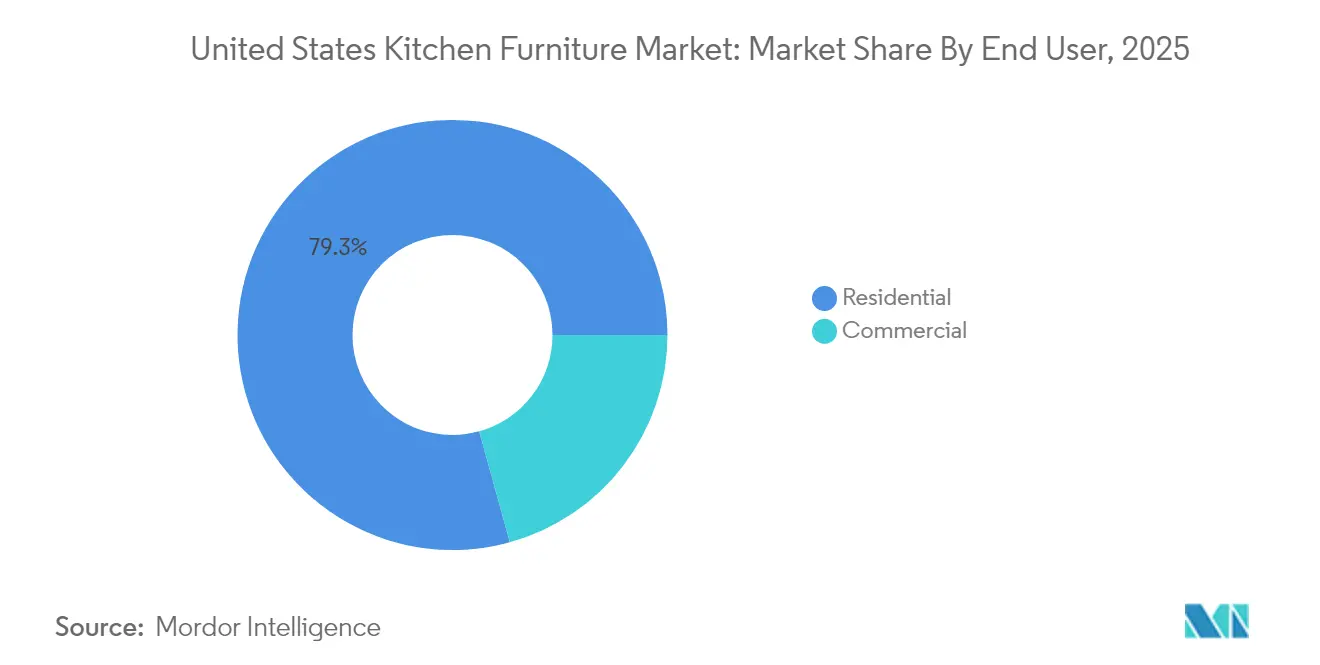

- By end user, residential demand held 79.30% of the United States kitchen furniture market share in 2025, while commercial installations are advancing at a 4.92% CAGR.

- By geography, the South captured 34.65% share of the United States kitchen furniture market in 2025; the West is the fastest-growing region at a 5.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Kitchen Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging housing stock drives remodeling cycles | +1.2% | Northeast & Midwest | Medium term (2-4 years) |

| Online RTA cabinet sales accelerate DIY adoption | +1.0% | Urban centers nationwide | Short term (≤ 2 years) |

| Luxury outdoor kitchens lift demand for weather-resistant materials | +0.8% | Sunbelt states | Medium term (2-4 years) |

| Frameless European-style cabinets gain favor | +0.7% | Coastal metros & suburbs | Medium term (2-4 years) |

| Multifunctional, space-saving furniture preferences grow | +0.6% | Major cities with smaller dwellings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Housing Stock Driving Remodeling Cycles

The pressing need to modernize aging kitchens in America's older homes is witnessing robust demand for kitchen furniture. Harvard University's Joint Center for Housing Studies, "Improving America's Housing 2025" report, on 42,500 housing units, highlighted that homes constructed before 2000 account for 65% of the U.S. housing stock [1]Abbe Will, “Improving America’s Housing 2025: Aging Housing Stock and Remodeling Demand,” Joint Center for Housing Studies of Harvard University, jchs.harvard.edu. Similarly, according to the 2025 Cost vs. Value Report by Hanley Wood, kitchen renovations stand out as the most lucrative interior remodelling endeavour. Homeowners can recoup up to 72% of their renovation costs upon resale. This trend not only underscores a stable market but also highlights a resilience to economic fluctuations; as kitchen components age, their need for replacement remains constant, independent of the housing market's broader health.

Online RTA Cabinet Sales Accelerating DIY Adoption

The ready-to-assemble (RTA) cabinet segment is rapidly growing, outpacing the broader kitchen furniture market. Millennials, the largest homebuying demographic, are driving this trend by favoring cost-effective, direct-to-consumer models. Augmented reality tools offered by online retailers have enhanced the shopping experience, according to the Webstaurant Store's "Restaurant Industry Statistics: Revenue, Labor & More" report (2024), 90% of consumers research kitchen products online before purchasing. The report includes a Q3 2024 National Restaurant Association survey of 4,200 U.S. adults, showing 90% researched online before buying, rising to 94.3% among millennials (ages 28-43).

VividWorks' April 29, 2025 report, "eCommerce Trends in the Furniture Market for 2025," highlights that 3D product configurators increased conversion rates by 27% and reduced returns by 35%. Data from 42 North American furniture retailers (2023-2025) showed AR tool users spent 18 minutes longer on websites and had a 41% higher average order value.

Outdoor Kitchens Boost Weather-Resistant Materials

The kitchen furniture market is evolving as outdoor cooking spaces transition from basic grilling stations to fully equipped kitchens, creating a high-margin category. Traditional indoor cabinet manufacturers must adapt to specialized material demands or lose market share to outdoor-focused specialists. Weather-resistant cabinets for outdoor kitchens command 30-40% price premiums over indoor units. This trend, prominent in sunbelt states, is expanding northward as homeowners prioritize outdoor entertainment. A March 2025 Architectural Digest report highlights the growing demand for outdoor kitchens that combine indoor functionality with weather-resistant materials.

Frameless European-Style Cabinets Reshape Manufacturing

The kitchen furniture sector is shifting as frameless cabinet construction, requiring different machinery and techniques than traditional face-frame methods, gains traction. Urban markets and new constructions drive demand for frameless cabinets, aligning with modern design preferences. Frameless cabinets offer 10-15% more storage than framed options. Manufacturers investing in European-style production gain competitive advantages, while traditional American cabinet makers risk losing market share. Frameless cabinets are growing twice as fast as framed cabinets due to consumer demand for cleaner aesthetics and more storage. Facilities optimized for edge-banding and panel processing benefit from this trend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile lumber & panel prices squeeze margins | -0.8% | Nationwide; heavier in Southeast & Pacific Northwest | Short term (≤ 2 years) |

| Skilled labor shortage extends custom lead times | -0.7% | High-growth South & Southwest | Medium term (2-4 years) |

| Elevated mortgage rates curb new single-family starts | -0.6% | Regions with stretched affordability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Lumber Prices Compress Margins

The volatility of lumber prices is likely to hinder market growth. Hardwood lumber costs rose 23.5% year-over-year despite minor recent retreats, complicating pricing models [2]National Association of Home Builders, “Lumber Price Volatility Tracker,” nahb.org. Furniture manufacturers consistently grapple with the challenge of raw material costs, forcing dynamic surcharges and design shifts toward thinner panels or engineered substrates. Vertically integrated manufacturers that own sawmills buffer price swings better than peers reliant on spot markets, preserving share in the United States kitchen furniture market.

Acute Skilled Labor Shortage in Finish Carpentry Extending Lead-Times

Angi's 2024 State of Home Spending Report, which surveyed 6,500 homeowners, revealed that 54% faced challenges in hiring finish carpenters. The struggle was most pronounced in the West, where 62% reported difficulties, followed closely by the South at 58%. Among those renovating kitchens, 67% encountered project delays of 4 to 6 weeks. This pushed average installation lead times to 6 to 8 weeks and resulted in cost increases of 15 to 20%. National Association of Home Builders data show 85% of Southeast and 82% of Southwest builders tag labor shortages as their chief concern, underscoring regional concentration. Manufacturers are responding: 43% have rolled out low-complexity product lines, and 29% have formed installer training programs, according to the Q3 2024 Kitchen & Bath Market Index [3] National Kitchen & Bath Association, “Kitchen & Bath Market Index Q3 2024,” nkba.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cabinets, Anchor Spending as Pantry Solutions Surge

Cabinets commanded 59.42% of 2025 revenue, reflecting their centrality in layout planning. Frameless formats, hidden hardware, and LED-lit interiors differentiate offerings in the United States kitchen furniture market. Other products (pantry shelves), the fastest-growing sub-segment at 5.72% CAGR, capitalize on bulk-buying habits and the desire for decluttered countertops.

Expanded storage modules—pull-out racks, swing-out corner units, and vertical dividers—command a premium dollar per square foot. Manufacturers meet varied footprints with modular columns and clip-on baskets, accelerating shipments and easing installation pressures.

By Material: Wood Dominates, Metal Gains Ground

Wood held a 60.88% position in the United States kitchen furniture market size for 2025, buoyed by consumer affinity for oak, walnut, and maple in light to medium stains. Certification seals boost trust, and textured veneers satisfy interest in biophilic design.

Metal, led by stainless steel, is projected to grow 6.02% annually through 2031. Weather resistance and commercial aesthetics drive adoption indoors and outside. Hybrid designs—wood fronts with steel drawer boxes—blend warmth with robustness, cushioning the transition rather than displacing wood outright.

By Price Range: Mid-Range Leads, Premium Accelerates

The mid-range tier retained 54.35% of 2025 spend, leveraging scale to package soft-close glides and custom interior kits at approachable price points. Manufacturers employ lean tooling and shared platforms to hold margins despite raw-material volatility.

Premium collections will climb 4.82% a year to 2031, buoyed by households allocating USD 180,000 or more to major remodels. Exotic veneers, integrated lighting, and app-based lift doors define this tier, anchoring profitability for suppliers who can support bespoke configurations.

By End User: Residential Prevails, Commercial Advances

Residential projects represented 79.30% of 2025 turnover, sustained by single-family remodels and multi-family developments. Upgrades now blend storage, entertainment, and assistive features for aging family members, broadening the bill-of-materials scope.

Commercial kitchens, although 20.70% of demand, are set for a 4.92% CAGR as restaurants favor open-prep theatrics and hotels refresh back-of-house for efficiency. NSF-rated surfaces and heavy-duty hinges distinguish these products within the United States kitchen furniture market.

By Distribution Channel: Retail Dominates, Online Accelerates

Retail outlets captured 87.30% of 2025 sales. Big-box chains bundle financing, appliances, and install services, while boutique showrooms curate premium lines. Online sales inside retail are expanding at 6.58% CAGR, fueled by AR viewers and AI-driven personalization. Parcel-friendly RTA packs and omnichannel pick-up options align perfectly with digital journeys that start on mobile devices.

Geography Analysis

The South anchors the United States kitchen furniture market with 34.65% of 2025 revenue, propelled by migration inflows, lower land prices, and a construction pipeline. Installation costs run 12-15% below national averages, letting homeowners upgrade their finishes without straining their budgets. Outdoor living culture drives stainless steel cabinet demand, and transitional aesthetics blend shaker profiles with modern hardware. Supply tightness in skilled labor remains pronounced, so manufacturers pre-assemble modules or partner with production builders to secure volume quickly.

The West is the fastest-growing territory, projected at 5.64% CAGR through 2031. The January 2024 Houzz Kitchen Trends Study, which surveyed 3,437 U.S. homeowners, found that Western homeowners spend 22% more on renovations and lead in sustainable selections, with over 90% including at least one eco-feature in new kitchens. Frameless cabinets, minimalist pulls, and integrated smart appliances dominate in tech-savvy metros such as San Francisco, Seattle, and Denver. Retail foot traffic eased 4% in 2024, but digital research more than compensates, reinforcing omnichannel dynamics in the region. Elevated labor and material costs challenge timelines, yet the culture of design experimentation and home investment sustains premium demand.

Northeast and Midwest patterns diverge yet complement the United States kitchen furniture market growth. Space-efficient inserts and vertical dividers record 35% higher uptake than in other regions, reflecting urban density. The Midwest is stable and value-oriented, with homeowners more likely to emphasize durability over fashion. Functional triggers, such as failing doors or hardware malfunctions, rather than aesthetic updates, dominate project starts. Angi's 2024 State of Home Spending Report, conducted from September 15 to October 20, 2024, surveyed 6,500 homeowners nationwide, shedding light on their renovation priorities and spending habits. Both regions see rising interest in multi-use islands that serve meal prep and remote work, as 38% of Northeastern and 32% of Midwestern respondents cited work-from-home needs in planning decisions.

Competitive Landscape

Competitive intensity in the United States kitchen furniture market remains moderate, with scale leaders leveraging multi-brand portfolios and smaller specialists carving niches. MasterBrand Cabinets, Inc., among the top suppliers, employs lean production and a multi-tier brand strategy to serve the economy through luxury. Its 2025 purchase of Supreme Cabinetry Brands widens reach in premium dealers and adds coastal-influenced design credence.

American Woodmark Corporation prioritizes automation and ERP upgrades after a 10.6% net-sales drop in fiscal 2024, aiming to lift EBITDA by streamlining order-to-delivery processes. The Home Depot’s 2025 acquisition of SRS Distribution broadens building-product logistics, strengthening sourcing clout for private-label kitchen lines and installation accessories.

Innovation also flows from component vendors. Outdoor specialist Brown Jordan Outdoor Kitchens captures affluent buyers with color-matched powder-coated stainless modules engineered for salt-air climates. Digital-native RTA brands exploit SEO, quick-ship logistics, and user-generated content to win millennial loyalty. Across the field, success hinges on supply-chain resilience, omnichannel reach, and the ability to integrate visualization software that reduces buyer uncertainty.

United States Kitchen Furniture Industry Leaders

MasterBrand Cabinets, Inc.

Cabinetworks Group

American Woodmark Corporation

IKEA

Wellborn Cabinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CabinetDIY, Inc. has unveiled a fresh collection of oak kitchen cabinets, catering to homeowners and interior designers who prioritize both aesthetics and durability.

- July 2024: MasterBrand, Inc., via its subsidiary MasterBrand Cabinets LLC, has finalized its USD 520 million cash acquisition of the Supreme Cabinetry Brands, Inc. from GHK Capital Partners LP

- March 2024: American Woodmark Corporation expanded its portfolio with the launch of a new brand, 1951 Cabinetry.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the United States kitchen furniture market as the value generated from the sale of new, factory-built kitchen cabinets, chairs, tables, trolleys, carts, and pantry or shelving units installed in permanent residential or commercial kitchens, expressed in current US dollars.

Scope exclusion: Built-in appliances, countertops, sinks, faucets, and purely outdoor kitchens are outside our model.

Segmentation Overview

- By Product

- Kitchen Cabinets

- Kitchen Chairs

- Kitchen Tables

- Other Products (kitchen trolley, cart, pantry shelves, etc.)

- By Material

- Wood

- Metal

- Plastic and Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B /Project

- B2C/Retail

- By Geography

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured interviews with US-based cabinet producers, design-build contractors, specialty retailers, and buying groups across the four census regions. These conversations validate shipment trends, average selling prices, mix shifts between stock and semi-custom lines, and expected remodel budgets, which then refine model coefficients and stress-test early outputs.

Desk Research

We begin with a broad document sweep that captures macro and micro signals. Public resources such as the US Census Bureau construction starts, Bureau of Labor Statistics Producer Price Index, Housing Permit Survey, and the Federal Reserve's household wealth tables anchor demand and pricing direction. Industry-specific outlets such as the National Kitchen & Bath Association dashboards, Kitchen Cabinet Manufacturers Association shipment survey, and customs records for HS 940340 shipments enrich volume and trade clues. Company 10-Ks, quarterly calls, and investor decks clarify channel mix and price ladders, while respected press stories track project pipelines and store openings. Select proprietary feeds, including D&B Hoovers financials and Dow Jones Factiva news archives, help our team spot revenue inflections. The sources mentioned illustrate our process and are not an exhaustive list.

A second desk review round screens for anomalies, verifies units, and flags any gaps that require primary outreach.

Market-Sizing & Forecasting

A top-down build starts from housing completions, residential remodel outlays, and commercial food-service build counts, which are translated into kitchen furniture demand pools through penetration ratios.

Results are cross-checked with a bottom-up roll-up that samples shipment volumes from KCMA surveys multiplied by blended ASPs reported during interviews.

Key variables include median kitchen remodel spend, average linear-foot cabinet pricing, monthly cabinet shipment index, wood material inflation, and regional remodeling sentiment scores.

Forecasts rely on multivariate regression that ties those drivers to historical market movements and generates scenario spreads; expert consensus then selects the base case.

Where supplier data are partial, interpolation uses three-year moving averages before alignment with top-line totals.

Data Validation & Update Cycle

Outputs pass variance checks against trade, retail scanner, and building-permit indicators, followed by a senior analyst review. Reports refresh every twelve months, with interim revisions when tariff shifts, housing policy changes, or major M&A alter underlying assumptions. A final validation run precedes client delivery, ensuring buyers always receive our latest view.

Why Mordor's United States Kitchen Furniture Baseline Commands Reliability

Published figures often diverge because analysts pick different product baskets, apply varying ASP escalators, and refresh models on dissimilar cadences.

The largest gaps stem from three drivers: some studies bundle dining or outdoor fixtures, a few extrapolate from manufacturer revenue without reconciling channel mark-ups, and others freeze price series at historic CPI averages that understate recent wood-cost swings. Mordor's scope, monthly data pulls, and dual-path triangulation reduce those blind spots.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.9 B (2025) | Mordor Intelligence | - |

| USD 170 B (2024) | Global Consultancy A | Bundles all kitchen appliances and countertops, applies uniform 3% price lift which inflates total |

| USD 21.9 B (2024) | Industrial Economics Firm B | Manufacturer-side supply value only, excludes retail mark-ups and chairs or tables |

| USD 18.1 B (2025) | Private Data Provider C | Limits scope to cabinet and countertop manufacturing NAICS 33711, omits project channels |

These comparisons show that once scope mismatches and channel mark-ups are adjusted, Mordor's disciplined, frequently refreshed approach delivers a balanced baseline that decision-makers can trace to clear variables and replicate with confidence.

Key Questions Answered in the Report

What is the current United States kitchen furniture market size?

The United States kitchen furniture market size is USD 28.24 billion in 2026 and is set to reach USD 35.99 billion by 2031.

Which region leads the United States kitchen furniture market?

The South holds the largest share at 34.65% in 2025, supported by strong population growth, lower installation costs, and a flourishing outdoor-kitchen culture.

What product category dominates spending?

Kitchen cabinets account for 59.42% of expenditure, underscoring their critical role in both layout and aesthetics.

How fast are online sales growing?

Online purchases within the retail channel are expanding at a 6.58% CAGR to 2031, the fastest pace among all distribution modes.

Page last updated on: