Bathroom Vanities Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

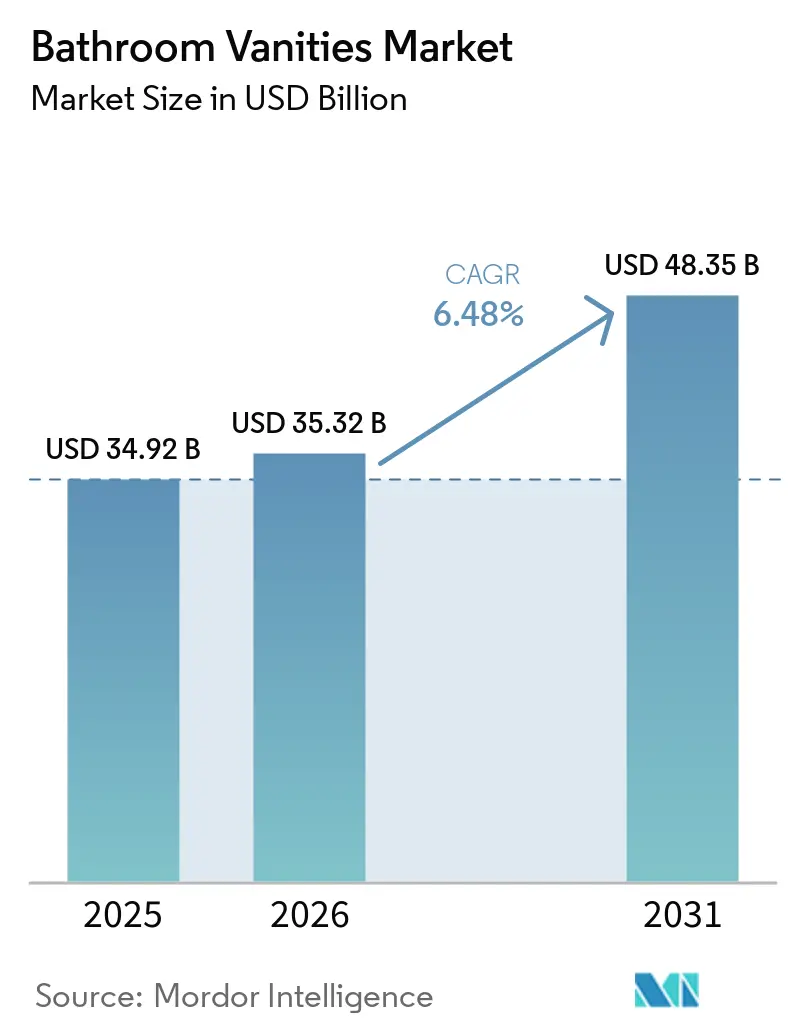

| Market Size (2026) | USD 35.32 Billion |

| Market Size (2031) | USD 48.35 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

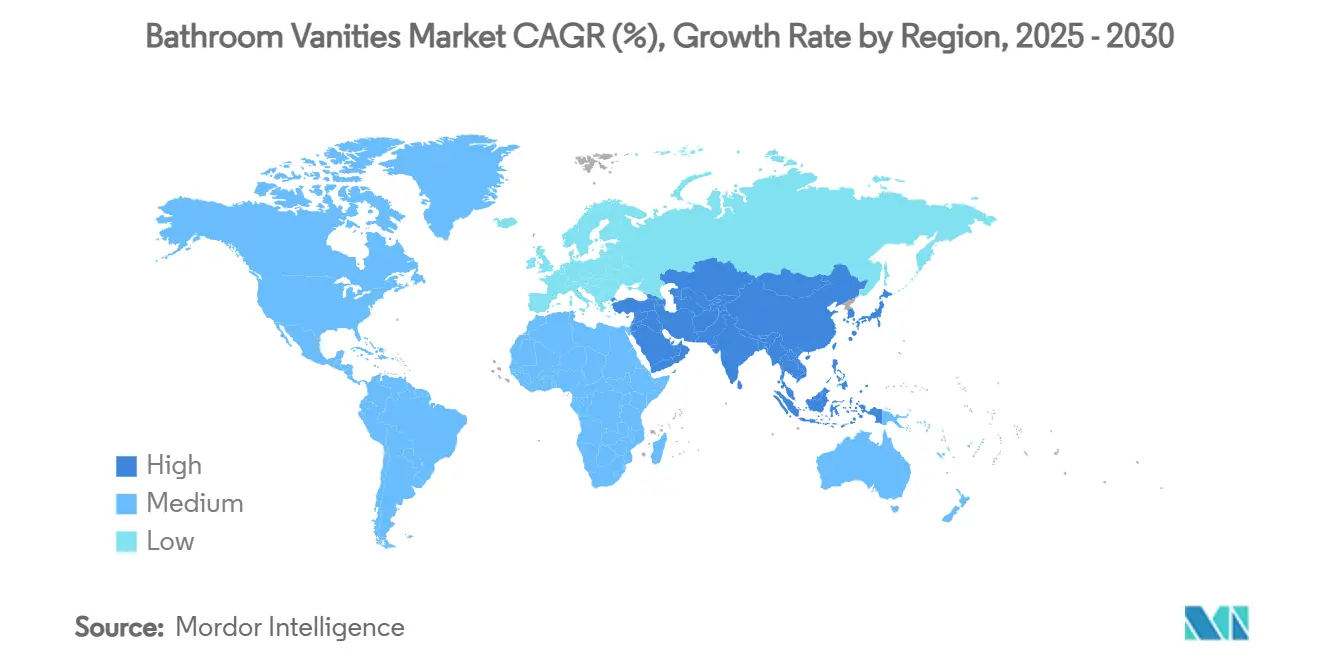

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bathroom Vanities Market Analysis by Mordor Intelligence

The bathroom vanities market size is expected to grow from USD 34.92 billion in 2025 to USD 35.32 billion in 2026 and is forecast to reach USD 48.35 billion by 2031 at 6.48% CAGR over 2026-2031. Urban and suburban renovations are sustaining steady replacement cycles as homeowners increase spending on bathrooms and favor modern aesthetics. Product roadmaps reflect premiumization and smart features that integrate lighting, storage, and device charging into coordinated vanity suites. Suppliers are aligning with sustainability preferences by showcasing low-maintenance surfaces and recycled-content designs in mainstream collections. Strategic moves by leading brands indicate a focus on modularity, faster installation, and localized manufacturing that supports predictable lead times. Partnership models in bathing and fixtures also signal a tighter alignment between product brands and fabricators for broader distribution reach across residential and commercial projects[1]LIXIL Newsroom Staff, “LIXIL Americas and American Bath Group Form Strategic Partnership,” LIXIL Newsroom, newsroom.lixil.com.

Key Report Takeaways

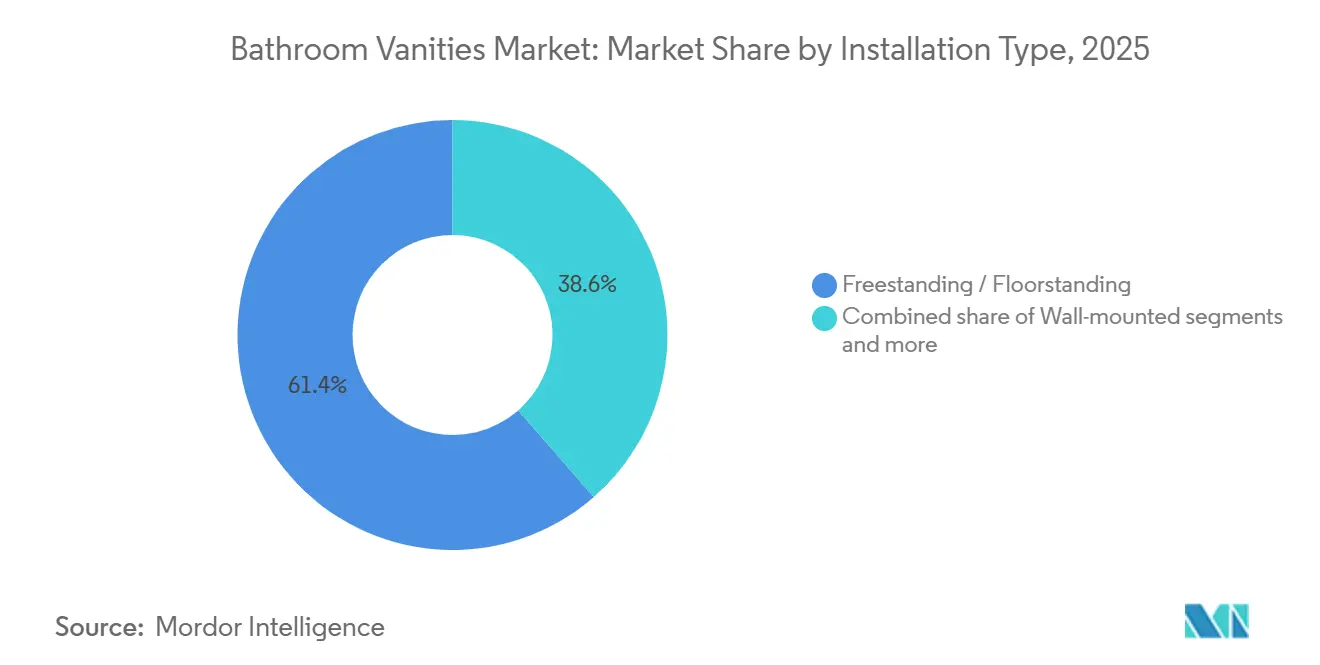

- By installation type, freestanding formats led with 61.43% of the 2025 bathroom vanities market share, while wall-mounted configurations recorded the fastest 7.92% CAGR through 2031.

- By material, wood accounted for 36.71% of the 2025 bathroom vanities market share, and stone posted the highest 8.44% CAGR to 2031.

- By sink configuration, single-sink units accounted for 58.91% of the 2025 bathroom vanities market share for installations, while double-sink units advanced at a 7.62% CAGR.

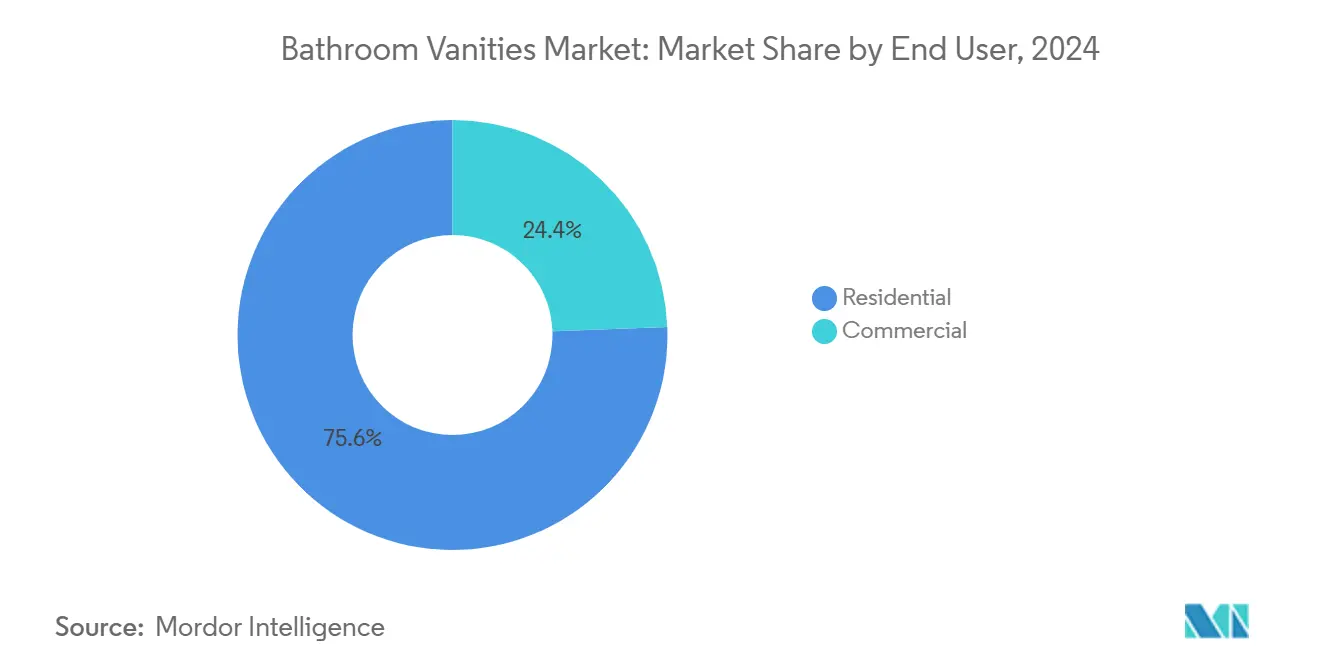

- By end-user, residential commanded 75.61% of the 2025 bathroom vanities market share, while commercial demand expanded at an 8.25% CAGR through 2031.

- By distribution channel, B2C/retail contributed 65.44% of the 2025 bathroom vanities market share, while direct B2B posted the fastest 8.69% CAGR.

- By geography, North America led with 36.82% of the 2025 bathroom vanities market share, while Asia-Pacific recorded the fastest 8.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bathroom Vanities Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Home Renovation and Remodeling Activities | +1.8% | Global, peaking in North America and Europe | Medium term (2-4 years) |

| Increasing Urbanization and New Residential Construction | +1.2% | Asia-Pacific core, spillover to the Middle East and Africa | Long term (≥ 4 years) |

| Growing Disposable Incomes and Demand for Luxury Bathroom Fixtures | +1.0% | Global, concentrated in urban metros | Short term (≤ 2 years) |

| Evolving Consumer Preferences For Modern And Aesthetic Bathroom Designs | +0.9% | North America, Europe, and the emerging Asia-Pacific | Medium term (2-4 years) |

| Expansion in the Hospitality Sector and Commercial Projects | +0.7% | Global hotspots include the United States, China, India, and Saudi Arabia | Long term (≥ 4 years) |

| Advancements in Smart Features and Space-Efficient Designs | +0.6% | North America and Europe lead, Asia-Pacific adoption accelerating | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Home Renovation and Remodeling Activities

Bathroom remodeling ranked as the most common home-improvement project in 2025 among United States remodelers, pointing to a durable upgrade cycle that benefits the bathroom vanities market. Spending on primary bathroom updates stayed resilient, with Houzz reporting higher median outlays for small and large primary baths as homeowners targeted finishes and fixtures that refresh both style and function. Renovation-led demand emphasizes integrated storage, durable surfaces, and coordinated finishes that support a consistent design narrative throughout the room. Baby Boomers led the way and increased their median bathroom spend in 2024, reinforcing aging-in-place upgrades that often include comfort-height options and easy-clean surfaces. These trends sustain project pipelines for installers and drive continuous product refreshes aimed at reducing installation time and simplifying maintenance over the life of the fixture[2]Houzz Research Team, “2025 U.S. Houzz & Home Study,” Houzz, st.hzcdn.com.

Increasing Urbanization and New Residential Construction

Compact homes and high-density living environments are reinforcing demand for space-efficient formats, a shift that supports floating vanities and integrated storage solutions that leave floors clear. Developers and design-build firms continue to weigh footprint and flow in small bathrooms, which favors slim profiles, concealed plumbing, and wall-mounted storage that better utilizes vertical planes. Modular and ready-to-assemble concepts also reduce disruption on site and shorten timelines in multifamily and urban renovations. Brands are aligning with this direction through easier-to-install systems that compress on-site labor and improve predictability for project schedules. These preferences maintain steady support for formats that maximize usable area while preserving a contemporary, minimalist look.

Growing Disposable Incomes and Demand for Luxury Bathroom Fixtures

Higher household spending capacity in urban centers is translating into stronger demand for premium and design-led bathroom suites. Manufacturers are introducing marble-look quartz surfaces, refined lighting, and accessory collections that elevate perceived value in the bathroom vanities market. MSI Surfaces’ LumaLuxe Ultra Quartz line, with enhanced light performance for bold veining, illustrates how materials innovation underpins this move upmarket in countertops paired with vanities[3]MSI Surfaces Editorial Team, “LumaLuxe Ultra Quartz: Where Light Meets Luxury,” MSI Surfaces, msisurfaces.com. Circular and recycled-content designs are establishing a distinct premium tier as well, with initiatives like WasteLAB signaling how sustainability can be a brand differentiator in higher-end ranges. Strategic acquisitions in luxury furniture and fixtures are extending portfolios at the upper end, linking cabinetry, vanities, and companion products for cohesive upgrades across the room

Evolving Consumer Preferences for Modern and Aesthetic Bathroom Designs

Homeowners continue to prioritize clean lines, neutral palettes, and coordinated fixtures that present a modern but warm aesthetic in the bathroom. Engineered quartz retains strong appeal in vanity countertops due to its consistent patterning and low-maintenance attributes, while marble-look designs bridge traditional tastes with contemporary ease of care. New surface technologies that enhance depth and reflectivity meet the desire for dimensional veining that pairs well with slim-profile vanities and integrated lighting. Integrated sink designs are gaining use because they present fewer seams and are easier to clean, a factor that resonates in shared primary baths and high-traffic households. These choices reflect a steady tilt toward minimalist forms that support visual spaciousness and efficient cleaning routines in the bathroom vanities market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Costs and Premium Material Pricing | -0.5% | Developed markets with high labor costs | Short term (≤ 2 years) |

| Fluctuations in Raw Material Prices and Supply Chain Disruptions | -0.4% | Global, acute in import-reliant regions | Short term (≤ 2 years) |

| Limited Space Constraints in Urban and Compact Households | -0.2% | High-density Asian and European cities | Medium term (2-4 years) |

| Health And Environmental Concerns Related to Certain Materials | -0.1% | North America and Europe have stringent standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Costs and Premium Material Pricing

High upfront spend on cabinetry, countertops, and integrated fixtures lifts the entry ticket for a full vanity upgrade, which slows purchase decisions in price-sensitive projects. Premium materials such as engineered stone, natural stone, and solid wood raise unit costs further, and labor-intensive customization amplifies total installed price in developed markets with elevated wages. Tariff and import duty changes on stone, hardware, and fittings can reset quotations mid-cycle, which pressures margins for trade buyers and triggers scope reductions for homeowners. These dynamics extend replacement cycles, encourage value engineering toward standardized sizes and finishes, and limit the adoption of add-ons like smart mirrors and integrated lighting. As a result, the bathroom vanities market experiences demand deferral at the top of the range, while mid-tier assortments capture buyers trading down to meet budget targets. Vendors respond with modular designs, curated bundles, and phased upgrade paths that lower the initial cash outlay without abandoning desired aesthetics.

Fluctuations in Raw Material Prices and Supply Chain Disruptions

Volatile input costs for panels, resin, stone, metals, and glass create pricing uncertainty that complicates budgeting and bid validity periods. Logistics disruptions such as port congestion, container scarcity, and rerouted ocean lanes add freight premiums and extend lead times, which can derail synchronized installations. Exchange rate swings and shifting trade policies further affect landed costs for imported tops and hardware, forcing frequent price list updates. Project owners react by delaying orders, substituting materials, or widening tolerances on color and finish, which can dilute the original design intent. Manufacturers diversify sourcing, build safety stocks on critical SKUs, and localize components where feasible, yet residual variability still carries through to schedules and cash flow. The bathroom vanities market therefore manages a persistent timing risk, with procurement buffers and standardized dimensions used to reduce change orders and rework.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Floating Formats Capture Urban Premiums

Freestanding and floor-standing vanities account for over 61.43% of 2025 placements, reflecting their simple installation and broad compatibility with existing plumbing in older housing stock. In contrast, wall-mounted and floating units are registering a 7.92% CAGR through 2031 as compact homes and modern aesthetics reshape specifications in the bathroom vanities market. The format’s clean lines, open floor visibility, and efficient use of vertical space align with urban layout constraints and contemporary design cues. Installers note that wall-mounted systems may require reinforcement to support combined loads from the cabinet, countertop, and fixtures, which adds cost and planning. Despite the added steps, developers and renovators adopt floating formats for their perceived spaciousness and simplified cleaning in everyday use. This balance of style, function, and upkeep is steering assortments toward slimmer profiles and integrated lighting that highlight the wall as a central design feature.

Floating vanities are also benefiting from product innovations that cut on-site labor and increase assembly certainty. IKEA’s simplified connector systems in select lines demonstrate how manufacturers reduce tools and steps for do-it-yourself use while preserving a refined look in the bathroom vanities market. Ready-to-install floating options that arrive preassembled can further compress timelines and reduce variability across larger projects. These practical improvements help address skilled-trade constraints while keeping design intent intact for both residential and light commercial applications. Together, faster setup and a space-saving footprint are reinforcing floating formats as the growth engine within installation types.

By Material: Stone Surges on Durability and Water Efficiency

Wood maintained a 36.71% share in 2025 on the strength of cost-accessible engineered substrates and broad finish options that span paint, laminate, and veneer. Stone materials, including quartz, marble, and granite, are advancing at 8.44% CAGR as projects favor non-porous surfaces that resist stains and reduce maintenance. Granite pricing tiers vary by grade and region, and well-known reference points support typical budgets in paired countertop and vanity packages. The preference for durable surfaces that stand up to daily use is bolstering quartz and granite in homes and commercial spaces where ease of care is a priority in the bathroom vanities market. Moisture-resistant panel grades also play a role in wood-based cabinets for wet environments, where specified cores and finishes help mitigate swelling and edge degradation. Clear care guidance and finish quality are now core to value propositions in both mid-range and premium categories.

Engineered stone producers have also improved design depth and brightness to satisfy marble-look preferences. MSI’s LumaLuxe Ultra Quartz showcases this push toward dimensional veining and light performance that pairs with modern, slim-profile vanities. Circular or recycled-content designs expand choice in stone-alternative sinks and surfaces, with Kohler’s WasteLAB highlighting how aesthetic and sustainability goals can align without sacrificing design leadership in the bathroom vanities market. In parallel, specification guides encourage moisture-resistant cores and protective finishes for wood-based cabinets in bathrooms, which helps extend service life at accessible price points. These combined advances point to a steady structural pivot toward surfaces that balance aesthetics, durability, and low-effort upkeep.

By Sink Configuration: Dual Basins Rise in Master Suites

Single-sink vanities represented 58.91% of 2025 installations, supported by powder rooms and compact bathrooms where space and budget drive single-basin solutions. Double-sink units, however, are the fastest-growing configuration with a 7.62% CAGR through 2031, reflecting dual-user routines and shared primary suites in the bathroom vanities market. Installation ranges vary by material selection and finish quality, and rough-in conditions can influence cost and scheduling. Product bundles that pair dual sinks with smart mirrors and organized storage are improving value perception at several price points. These attributes are strengthening adoption in mid-to-premium remodels and new builds where space supports wider vanities and coordinated lighting. The result is a shift toward configurations that emphasize simultaneous use, simplified preparation routines, and organized storage.

Commercial specifications and spa-like residential projects also favor integrated sinks for hygiene and housekeeping efficiency. Integrated one-piece surfaces reduce seam lines and present fewer crevices, which supports faster cleaning cycles in hospitality. Vessel sinks and undermount formats continue to address style preferences and design tiers, with undermount adoption advancing due to its compatibility with quartz and granite tops. Across use cases, configuration choices balance space, user routines, and maintenance expectations, and this balance continues to guide showroom displays and assortment planning in the bathroom vanities market. These patterns indicate sustained growth for dual-basin and integrated solutions as households and hotels raise expectations for both design and function.

By End-User: Commercial Channels Accelerate Post-Pandemic

Residential end-users accounted for 75.61% of 2025 demand, reflecting ongoing remodel activity and steady specifications in new housing. The bathroom vanities market continues to benefit from projects that prioritize modern surfaces, cleanable storage, and cohesive finishes in owner-occupied homes. Within multifamily settings, standardized options and quick-install products support unit turnovers and help control service costs. Commercial demand is growing faster at an 8.25% CAGR through 2031 as hotels, offices, and venues update bathrooms to enhance user experience and reduce cleaning time. Product choices in hospitality emphasize durability, touchless accessories, and surfaces that maintain appearance under sustained use. This pull-through favors manufacturers that can coordinate volume orders, deliver consistent finish lots, and support phased rollouts across properties.

Commercial and institutional projects also reflect accessibility and maintenance considerations at the specification stage. ADA-related clearances and comfortable reach heights shape vanity selections alongside faucet and accessory choices. As hospitality pipelines proceed and offices refresh shared spaces, the bathroom vanities market will continue to see commercial requirements that prioritize predictable installation and long-term performance. These requirements reinforce practical surfaces, reinforced cabinetry, and proven hardware systems that stand up to daily use. Residential volumes remain larger in absolute terms, but commercial momentum is redefining what features and finishes flow into mainstream lines.

By Distribution Channel: B2C Retail Dominance and the Rise of Design-Driven Vanity Solutions

B2C/retail accounted for 65.44% of 2025 sales across home centers, specialty showrooms, and online platforms, reflecting continued reliance on curated assortments and in-person guidance for tile and finish coordination. In parallel, direct B2B channels posted the fastest growth at a 8.69% CAGR as developers, hospitality operators, and multifamily owners sought volume discounts, consistent finishes, and control over lead times. This shift supports deeper manufacturer engagement on customization and staged deliveries across properties in the bathroom vanities market. Digital content and visualization tools continue to influence product discovery and specification, even when final selections occur in showrooms. Partnerships that align brands, fabricators, and distributors also expand reach into trade programs that can bypass some retail intermediaries. Company-level collaborations that rationalize manufacturing footprints and strengthen distribution illustrate how B2B structures are evolving to meet project demands.

In retail channels, the bathroom vanities market continues to reward brands that simplify installation, package coordinated components, and provide strong service support. Online assortments that feature clear dimensions, finish swatches, and installation guides help close the loop for design-led buyers. Direct-to-consumer models are also gaining traction for specific styles, with specialized vendors highlighting floating formats and integrated lighting to stand out. For B2B, framework agreements and brand-locked specifications drive repeatable demand across multi-property programs. Taken together, these patterns point to a dual-track future in which retail remains the volume anchor and B2B direct channels drive faster growth in large projects.

Geography Analysis

North America led with 36.82% of 2025 revenue as households prioritized bathroom updates that balance aesthetics with lasting performance. Remodel spending in the United States remained healthy in 2024, and primary bathroom projects featured sustained interest in smart lighting, integrated storage, and cleanable surfaces that suit daily routines. Houzz findings show firm spend levels for small and large primary bathrooms, which support material upgrades and better-organized vanities within the bathroom vanities market. Brand investments in the United States manufacturing and design centers reinforce premium and smart features that resonate with homeowners across metropolitan regions. Product launches at design and building events maintain visibility for new collections and fittings that anchor coordinated bathroom suites.

Asia-Pacific is the fastest-growing region at an 8.09% CAGR through 2031, with urbanization and rising incomes elevating expectations for modern bathrooms. Developers and homeowners are adopting stone surfaces and integrated lighting to deliver a contemporary look in compact layouts. In parallel, brands are deepening their presence with investments that localize manufacturing and showcase premium ranges that align with regional design tastes in the bathroom vanities market. New showrooms and design galleries serve the architecture and interior communities and introduce curated vanities and companion fixtures. These moves expand access to higher-spec materials and establish reliable supply for larger projects across the region[4]Roca Group Newsroom, “Roca to Build Production Plant in Kazakhstan,” Roca Group, rocagroup.com.

Europe remains a design-forward region with strong emphasis on sustainability, circularity, and heritage renovation. Premium ranges place a clear focus on refined finishes and compact solutions that fit within older building footprints while meeting modern performance expectations. Companies are combining recycled-content sinks with elegant finishes to match environmental goals in the bathroom vanities market. Partnerships and selective acquisitions are helping European brands scale in adjacent categories and reach new audiences globally. In the Middle East and parts of Africa, new hospitality and luxury residential projects are raising specifications for durable, easy-clean vanity systems that hold up in high-use environments. South America shows steady upgrade activity in key cities, while broader economic variability shapes adoption rates for premium materials

Competitive Landscape

Global leaders and regional specialists compete across a wide range of styles, materials, and price points, which keeps the bathroom vanities market fragmented. Established brands are doubling down on premium design, smart features, and sustainability to differentiate in a crowded field. Partnerships that pool brand equity and manufacturing assets are also streamlining product development and expanding access for trade customers. The result is a marketplace where product innovation and operational agility often matter more than price alone. Companies that best integrate lighting, storage, and surfaces into cohesive suites are building stronger pull with designers and renovators.

Manufacturers are updating stone and engineered surfaces to match high-demand looks, especially marble-inspired quartz that pairs well with floating cabinets and slim hardware. MSI Surfaces’ LumaLuxe Ultra Quartz is an example of how materials science supports the visual depth and clarity that design-forward homeowners expect. At the same time, circular design initiatives are moving from concept to catalog through recycled-content sinks and vanities that still meet high design standards. These launches show how sustainability attributes can reinforce brand positioning and meet procurement goals in commercial and residential projects within the bathroom vanities market. Together, these product streams are shaping new baselines for performance and visual impact in vanities and coordinated accessories.

Smart and wellness features are becoming mainstream within broader bathroom ecosystems, and leading companies continue to push the frontier. Kohler Health’s Dekoda platform demonstrates how bathroom routines can produce actionable wellness insights that extend product value beyond aesthetics. At major industry shows, top brands are presenting integrated suites that simplify specification and deliver a consistent design language across vanities, lighting, and fixtures. Strategic licensing and manufacturing partnerships are also optimizing product portfolios so that brands can concentrate on their highest-impact categories. These moves support faster innovation cycles, stronger distribution, and better service levels for trade accounts in the bathroom vanities market.

Bathroom Vanities Industry Leaders

Kohler Co

Masco Corporation

LIXIL Group

IKEA Group

American Woodmark Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kohler unveiled “Step into Possibility” at KBIS 2026, including new collections and water-saving innovations that link design leadership with wellness features

- February 2026: TOTO introduced the Aurora Moment at KBIS 2026, highlighting next-generation one-piece systems and expanded finish options for smart toilets and suites

- November 2025: MSI Surfaces launched LumaLuxe Ultra Quartz with enhanced light performance to amplify depth and clarity in marble-look designs for vanity countertops

- July 2025: Roca Group acquired a majority stake in Antonio Lupi Design, adding a high-end bathroom furniture brand with a strong international footprint

Global Bathroom Vanities Market Report Scope

| Freestanding / Floor-standing |

| Wall-mounted / Floating |

| Corner |

| Wood |

| Ceramic |

| Stone (Marble, Quartz, Granite) |

| Laminate / MDF |

| Others (Metal, Glass, Solid Surface) |

| Single Sink |

| Double Sink |

| Others (e.g., Vessel, Integrated Multi-bowl) |

| Residential |

| Commercial |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, warehouse clubs, departmental stores, etc.) | |

| B2B/Directly from Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Installation Type | Freestanding / Floor-standing | |

| Wall-mounted / Floating | ||

| Corner | ||

| By Material | Wood | |

| Ceramic | ||

| Stone (Marble, Quartz, Granite) | ||

| Laminate / MDF | ||

| Others (Metal, Glass, Solid Surface) | ||

| By Sink Configuration | Single Sink | |

| Double Sink | ||

| Others (e.g., Vessel, Integrated Multi-bowl) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Home Centers |

| Specialty Furniture Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, warehouse clubs, departmental stores, etc.) | ||

| B2B/Directly from Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecasted size of the bathroom vanities market?

The bathroom vanities market size is expected to grow from USD 34.92 billion in 2025 to USD 35.32 billion in 2026 and reach USD 48.35 billion by 2031 at a 6.48% CAGR.

Which installation type is growing the fastest in the bathroom vanities market?

Wall-mounted formats are the fastest-growing installation type with a 7.92% CAGR through 2031, supported by compact layouts and modern aesthetics.

Which material category is gaining the most momentum in the bathroom vanities market?

Stone-based materials, including quartz and granite, are advancing at an 8.44% CAGR due to durability and low-maintenance performance.

What end-user segment is driving incremental growth for bathroom vanities?

Commercial buyers, including hotels and offices, are growing at an 8.25% CAGR as projects emphasize durable, easy-clean vanities and coordinated deliveries.

How are direct channels changing procurement in the bathroom vanities market?

Direct B2B channels are expanding at an 8.69% CAGR as developers and hospitality operators seek bulk customization, consistent finishes, and tighter lead-time control.

Page last updated on: