Vietnam Specialty Yeast Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

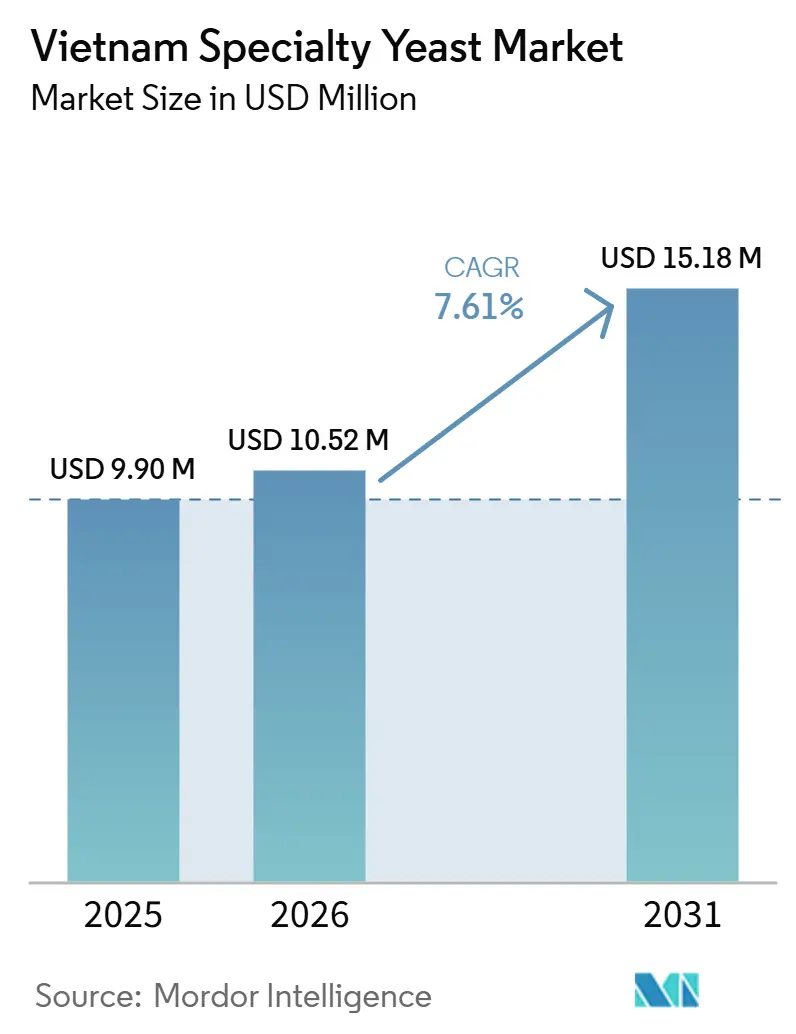

| Base Year Market Size (2025) | USD 9.90 Million |

| Market Size (2026) | USD 10.52 Million |

| Market Size (2031) | USD 15.18 Million |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

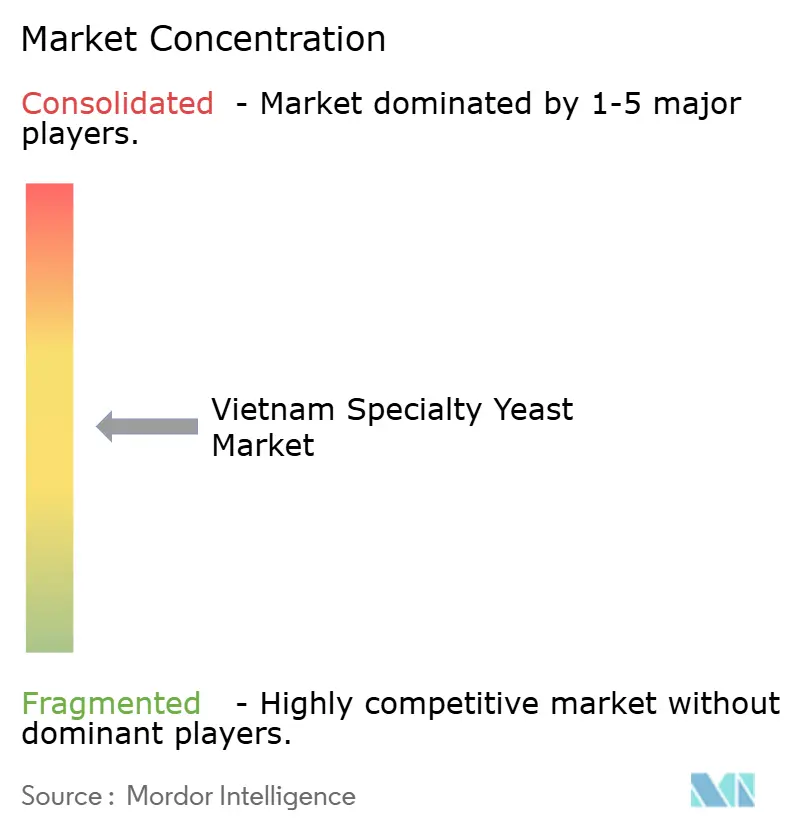

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Specialty Yeast Market Analysis by Mordor Intelligence

The Vietnam specialty yeast market size is projected to be valued at USD 9.9 million in 2025 and is estimated to grow from USD 10.5 million in 2026 to USD 15.2 million by 2031, registering a CAGR of 7.6% during the forecast period 2026-2031. The market is expanding as food and pharmaceutical manufacturers replace standard flavor enhancers and synthetic additives with fermentation-based ingredients that provide traceability and greater formulation flexibility. Vietnam’s food processing sector is expected to reach USD 88 billion in 2025 and grow 11% year over year, providing the Vietnam specialty yeast market with a large manufacturing base, although ingredient adoption per kilogram remains below that of more mature Asian markets, according to the United States Department of Agriculture[1]Source: United States Department of Agriculture, “Food Processing Ingredients Report,” USDA GAIN, usda.gov. Export-oriented processors also face increasing pressure to meet cleaner labeling requirements from buyers in Japan, South Korea, and the European Union, supporting the wider use of yeast extracts in seasonings, instant noodles, sauces, and plant-based foods. The market is also benefiting from stronger demand for functional ingredients in supplements and the government’s push to strengthen pharmaceutical raw material capabilities by 2030, increasing the role of beta-glucans, yeast peptides, and precision fermentation inputs. At the same time, import dependence for feed inputs and food-grade yeast, along with slower regulatory execution in 2026, is shaping competition, pricing discipline, and the timing of new product adoption across the Vietnam specialty yeast market.

Key Report Takeaways

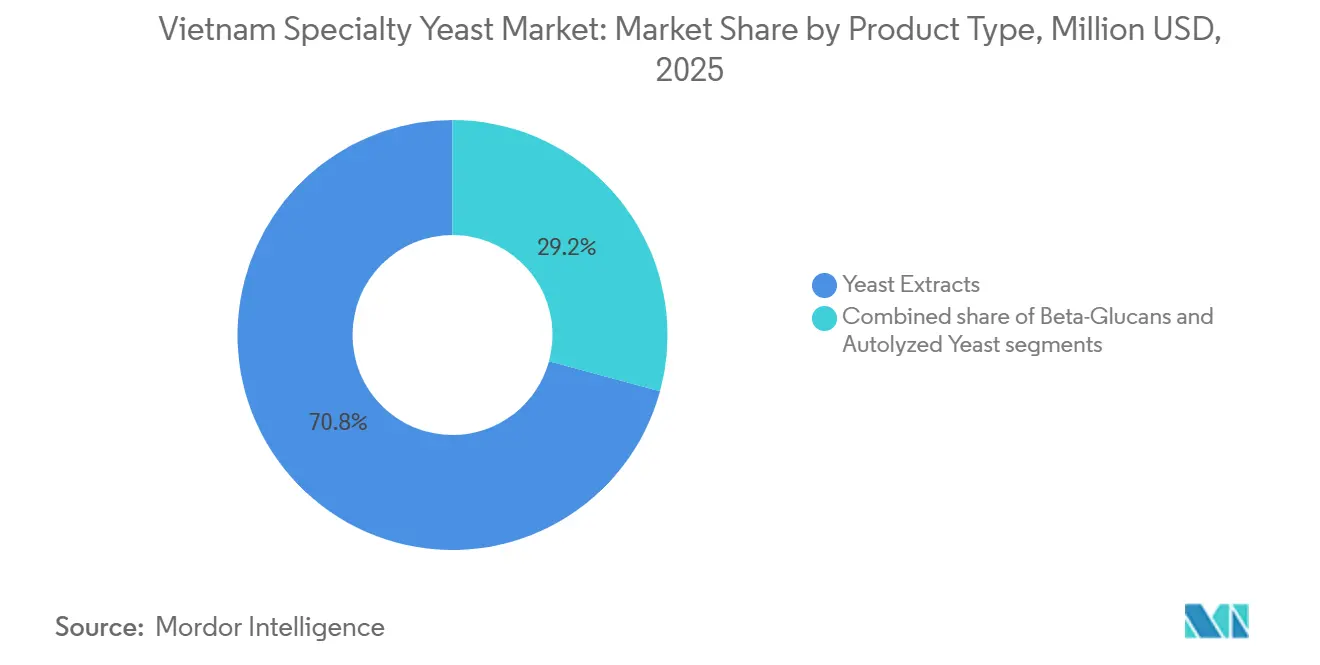

- By product type, yeast extracts held 63.71% of the Vietnam specialty yeast market share in 2025, while beta-glucans are projected to grow at an 8.46% CAGR through 2031.

- By species, Saccharomyces cerevisiae held a 34.62% share in 2025, while Pichia pastoris is forecast to record the highest CAGR at 8.71% through 2031.

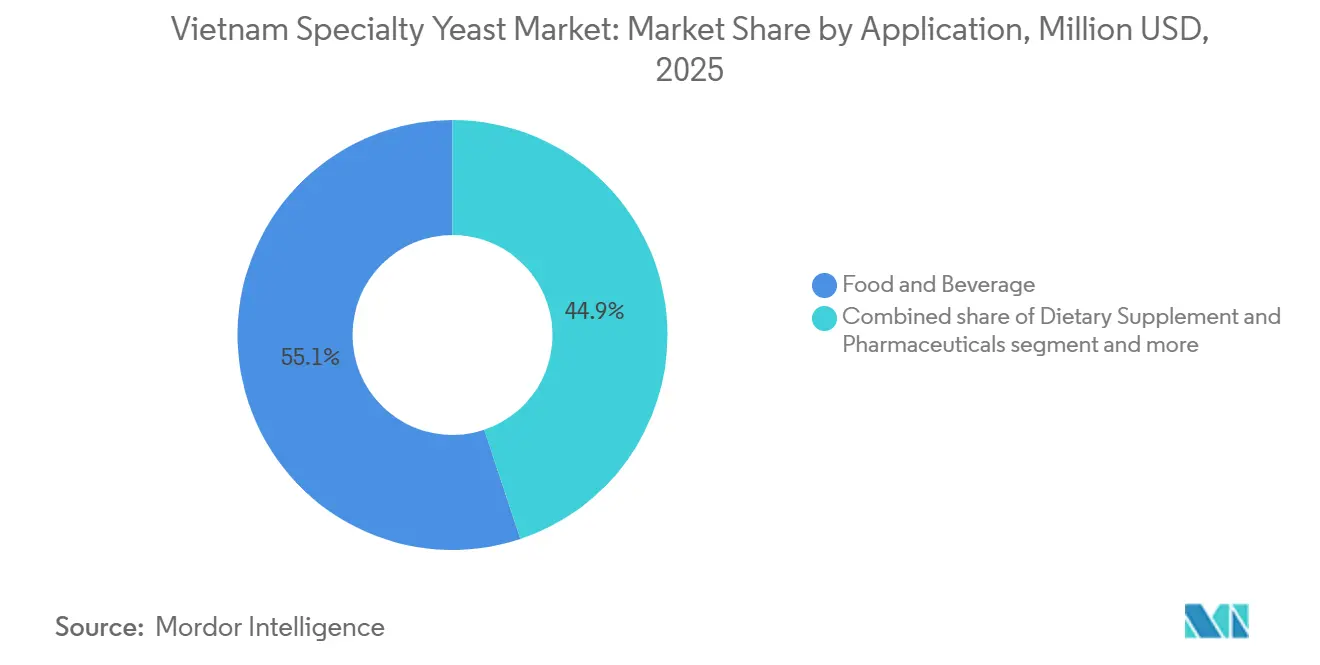

- By application, food and beverage accounted for 55.13% of revenue in 2025, while the Dietary Supplement and Pharma segment is projected to expand at an 8.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Specialty Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label umami ingredients | +1.40% | Nationwide, concentrated in Ho Chi Minh City and Hanoi, food manufacturing clusters | Medium term (2–4 years) |

| Expansion of Vietnam’s bakery and savory food base | +0.70% | Ho Chi Minh City, Hanoi, and Binh Duong industrial corridors | Short term (≤ 2 years) |

| Growth in health-conscious and plant-based consumption | +0.90% | Primarily Southern and Northern urban centers, spill over to Central Vietnam | Medium term (2–4 years) |

| Rising beverage and brewing activity | +0.60% | Primarily Southern Vietnam brewing hubs, extending to Central Vietnam | Short term (≤ 2 years) |

| Increasing use in pharmaceuticals and nutraceuticals | +0.80% | National, with early gains in Ho Chi Minh City and Hanoi, pharma manufacturing corridors | Medium term (2–4 years) |

| Improved yeast production technologies | +0.50% | Global supply chains with direct import implications for Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label umami ingredients

Vietnam’s shift toward clean-label formulations is not only a consumer-facing retail trend; it is also an export-compliance imperative that is reshaping upstream ingredient sourcing. Vietnamese food processors supplying markets under the EVFTA (EU-Vietnam Free Trade Agreement) and CPTPP frameworks face direct pressure to remove synthetic flavor enhancers from ingredient declarations, making yeast extract a strategic procurement priority. Vietnamese trade sources confirm that suppliers actively market yeast extract domestically as a natural alternative to MSG in seasonings, instant noodles, soy sauce, and plant-based products. This positioning aligns with its classification as a “natural flavoring” in Europe, the United States, and Japanese regulatory frameworks. According to the USDA GAIN Report (2026), Vietnam’s food processing sector is expected to reach USD 88 billion in 2025, increasing 11% year-on-year and generating substantial upstream demand for ingredients positioned within clean-label parameters. A key insight is that Vietnam’s role as both a domestic consumer market and an export platform creates a multiplicative demand signal: manufacturers need clean-label compliance for exports while also catering to millions of domestic consumers, whose packaged food consumption is accelerating alongside GDP per capita growth in 2026.

Expansion of Vietnam’s brewing industry

Vietnam produced approximately 4.16 billion liters of beer in the first ten months of 2025, according to the country’s General Statistics Office, making it one of Asia’s largest beer markets by volume[2]Source: General Statistics Office of Vietnam, “Industrial Production and Beer Output Updates,” General Statistics Office of Vietnam, gso.gov.vn. Global brewing majors have expanded production infrastructure significantly. Carlsberg invested nearly USD 90 million to increase capacity at its Phu Bai facility by 50%, positioning it as the group’s largest beer production site in Asia as of 2024, according to Carlsberg Vietnam’s official announcement[3]Source: Carlsberg Vietnam, “Phu Bai Brewery Expansion Announcement,” Carlsberg Vietnam, carlsbergvietnam.vn. AB InBev doubled the capacity of its Binh Duong plant to 100 million liters annually through a USD 238 million investment, according to the Asia Brewers Network. This expansion is critical for the specialty yeast market, as each liter of beer requires proprietary yeast strains maintained under strict quality specifications. As Vietnam’s premium and craft beer segments grow, demand for tailored brewing yeast solutions is increasing, which, in turn, supports demand for autolyzed yeast and yeast nutrients. Rising production volumes also generate spent brewer’s yeast, which specialist players are increasingly recovering and upcycling into value-added animal feed and nutraceutical ingredients. This secondary supply chain dynamic reduces raw material waste and creates margin opportunities.

Growth in health-conscious and plant-based consumption

Vietnam's health supplement market is projected to reach USD 2.9 billion in 2025 and nearly double to USD 4.6 billion by 2030, registering a CAGR of 9.2%. This growth positions it as the fastest-growing complementary medicines market in Southeast Asia, according to Euromonitor International data cited by the Complementary Medicines Association (January 2026). Within this channel, yeast-derived beta-glucans hold a structurally advantageous position. They have clinical evidence supporting immune-modulating efficacy, align with the GRAS regulatory framework, and manufacturers can formulate them relatively easily into capsules, functional beverages, and fortified foods. A key supply chain insight is that Vietnamese supplement brands primarily source beta-glucan as a finished extract from multinational specialty yeast suppliers, creating a concentrated demand funnel that depends entirely on imports. Vietnamnet reported that Vietnam's domestic functional food market is valued at approximately USD 2.4 billion and grows at around 15% annually. The proliferation of counterfeit products is driving consumer preference toward internationally certified ingredient brands, a dynamic that strengthens the position of multinational specialty yeast companies with verifiable quality documentation.

Increasing use in pharmaceuticals and nutraceuticals

Vietnam's pharmaceutical market is projected to reach approximately USD 8.58 billion in 2025, expanding by 6–8% annually, according to the Drug Administration of Vietnam (DAV). The country is expected to have an estimated 245 facilities meeting WHO-GMP standards, as reported in the DHG Pharma Annual Report (2025). The government's February 2025 national pharmaceutical development program aims to meet 20% of domestic raw material demand by 2030 and 50% of input requirements for functional foods and pharmaceutical cosmetics, according to VCCI. This initiative is driving demand for precision fermentation ingredients, including Pichia pastoris-expressed proteins and yeast-derived excipients. Pharmaceutical-grade yeast extracts and autolyzed yeast serve as critical growth media components in cell culture-based vaccine and biologics production, an area receiving direct policy investment. Hanoi's Biotech Hi-Tech Park, scheduled to launch in August 2025, according to BioSpectrum Asia, aims to attract global biotech firms and support technology transfer. This development is expected to stimulate domestic upstream demand for fermentation-grade specialty yeast ingredients. Vietnam is also projected to export pharmaceuticals worth USD 312 million in 2025, ranking fourth in Southeast Asia, according to DHG Pharma's Annual Report. This performance reinforces Vietnam's role not only as a domestic pharmaceutical consumer but also as an active producer with increasing requirements for high-quality ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material and substrate price volatility | -0.90% | Global supply chains: concentrated impact in Southern Vietnam processing hubs | Short term (≤ 2 years) |

| Regulatory compliance burden | -0.50% | National regulatory framework, particularly affecting the supplement and pharma segments | Medium term (2–4 years) |

| Competition from substitute flavor systems | -0.40% | Concentrated in the food manufacturing and animal feed segments | Medium term (2–4 years) |

| Limited awareness of specialty yeast varieties | -0.30% | Nationwide, with a more pronounced impact in smaller cities and rural processing units | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw material and substrate cost volatility

Vietnam's specialty yeast supply chain remains structurally exposed to input cost volatility because the country imports approximately 80% of animal feed ingredients, including the molasses, grain substrates, and nitrogen sources used in yeast fermentation, according to the USDA Grain and Feed Annual (2025). This import dependence means that a weaker Vietnamese dong or a sudden tightening in global sugar and grain markets can directly raise specialty yeast production costs or procurement prices, compressing margins for both suppliers and formulators. Vietnam's total pharmaceutical and raw material import bill is projected to exceed USD 4.1 billion in 2025, according to the PMC Annual Report (2025), highlighting the country's systemic reliance on foreign ingredient supply. A less visible but more strategically significant risk is that substrate cost inflation can trigger a temporary substitution effect. During high-price periods, food manufacturers in margin-sensitive segments, such as instant noodles and fish sauce, often revert to MSG and hydrolyzed vegetable protein. This shift can slow the clean-label transition and reduce the volume consistency that suppliers need to sustain investment in distribution infrastructure.

Regulatory compliance burden

Vietnam's food safety regulatory environment is undergoing structural reform, but the pace of change is creating interim ambiguity rather than clarity. According to the USDA GAIN Report (2026), implementation difficulties and industry opposition led to the suspension of Decree 46/2026/ND-CP in 2026, while amendments to the Food Safety Law are expected to be submitted to the National Assembly for approval in October 2026. For specialty yeast derivatives, particularly novel formats such as beta-glucan concentrates, Pichia pastoris-derived enzymes, and yeast-based bioactive peptides, the lack of clear approval pathways within the pharmaceutical and supplement frameworks increases lead times and compliance costs for market entry. The Ministry of Health's Drug Administration of Vietnam oversees health supplement registration, and approval timelines for novel ingredients can extend to 18–24 months. This compliance friction disproportionately affects smaller distributors and domestic formulation companies, which often lack the regulatory teams available to multinationals. As a result, adoption of specialty yeast ingredients remains concentrated among a narrow tier of large food and pharma manufacturers with established import licensing infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Yeast Extracts Lead, Beta-Glucans Redefine Value Creation

Yeast extracts are projected to account for a 63.71% share of the Vietnam specialty yeast market in 2025, reflecting decades of adoption in savory food processing. Food manufacturers across Vietnam have widely embedded yeast extracts as natural substitutes for MSG and hydrolyzed vegetable protein in soups, sauces, instant noodles, and seasoning blends. Vietnamese-language distributor networks, including companies such as Hương Liệu Việt Đức, which holds exclusive distribution rights for Leiber GmbH, actively serve mid-sized food manufacturers with application-specific yeast extract grades. This presence indicates that downstream penetration extends well beyond major multinationals. Autolyzed yeast holds a complementary position due to its higher nucleotide content and stronger umami profile, with notable traction in premium sauces and condiment formulations targeting the export market.

Beta-glucans are expected to be the fastest-growing product type during the 2026–2031 forecast period, registering a CAGR of 8.46%. The strategic rationale extends beyond demand from immune-health supplements. Vietnam's growing aquaculture feed market increasingly incorporates yeast-derived beta-glucans as antibiotic-free immune adjuvants in shrimp and pangasius diets, as documented by Vietfish Magazine's coverage of Enzym Feed Solutions' commercial trials. Feed-sector demand for beta-glucans differs structurally from supplement demand because it is volume-driven rather than premium-driven. As a result, beta-glucans are expected to broaden the market base while increasing per-unit margins through supplement channels.

By Species: Saccharomyces Cerevisiae Anchors Volume, Pichia Pastoris Leads Value

Saccharomyces cerevisiae is expected to command a 34.62% share of the species segment in 2025, spanning brewing yeast, food-grade yeast extract production, animal feed additives, and bakery leavening. Vietnam's aquaculture sector widely uses inactivated S. cerevisiae preparations enriched with beta-glucans and mannan oligosaccharides to improve shrimp gut health and immunity, reducing dependence on therapeutic antibiotics and aligning with requirements mandated by export certification bodies, including the European Commission's RASFF system for Vietnamese seafood exports. Kluyveromyces marxianus represents a smaller but technically distinct species segment. A 2025 review in Current Research in Food Science classifies it as GRAS and highlights its commercial value in dairy fermentation and enzyme production. Its thermotolerance and lactase activity support lactose-free dairy ingredient manufacturing, an emerging segment in Vietnam's rapidly modernizing dairy value chain. The "Others" species grouping includes emerging commercial strains not yet categorized separately.

Pichia pastoris is projected to be the fastest-growing species, registering an 8.71% CAGR through 2031, driven by its utility as a host organism for pharmaceutical-grade recombinant protein production. Research published in Microbial Cell Factories (2025) shows that producers can fine-tune glycosylation control in P. pastoris fermentation systems by modulating cell density and methanol concentration, improving protein purity and reducing downstream processing costs. This advancement is directly relevant to Vietnam's ambitions in biologic drug manufacturing. IQVIA estimates cited in Imexpharm's FY2025 Annual Report indicate that Vietnam's pharmaceutical sector is expected to grow at approximately 10% annually during 2026–2028, creating demand pull. Compliance remains key: pharmaceutical-grade P. pastoris production must conform to WHO-GMP and EU-GMP standards, making Vietnam's 245 GMP-certified facilities the primary eligible end-user base.

By Application: Food and Beverage Anchors Scale, Dietary Supplement and Pharma Drives Premium

The Food and Beverage segment is expected to capture 55.13% of Vietnam specialty yeast revenues in 2025, supported by the scale of Vietnam’s processed food and beverage manufacturing base. Yeast extracts serve as natural umami boosters in instant noodles, dipping sauces, fish sauce, and plant-based condiments, which form the backbone of Vietnamese consumer food culture. The Animal Feed application segment gains momentum from Vietnam’s position as the world’s fourth-largest aquaculture producer, with output expected to reach 5.98 million tonnes in 2025, according to the Vietnam Directorate of Fisheries. Yeast-derived ingredients serve as immune modulators and palatability enhancers across shrimp, pangasius, and poultry feed systems. Cosmetics and Personal Care remains an early-stage application in Vietnam, with yeast-derived peptides and beta-glucan skin-barrier actives gaining initial traction among premium cosmetic brands importing specialty yeast ingredients for local formulation.

Dietary Supplement and Pharma is expected to be the fastest-growing application segment, registering an 8.51% CAGR through 2031. Government policy, rather than consumer demand, primarily drives this segment’s growth. The Vietnamese government’s pharmaceutical localization agenda targets 50% raw material self-sufficiency for functional foods and pharmaceutical cosmetics by 2030, according to the Vietnam Chamber of Commerce and Industry. This policy is shifting the segment from a fully import-dependent procurement model to a structured domestic sourcing and formulation opportunity. Vietnam’s pharmaceutical market is expected to grow, with pharmaceutical-grade yeast peptides, nucleotides, and beta-glucan extracts increasingly used in vitamin supplements, gut-health formulations, and fermentation-based APIs. The Ministry of Health’s revised supplement registration framework is also shaping this transition and is expected to introduce clearer GMP-equivalent production standards for locally manufactured functional food ingredients during the October 2026 legislative cycle.

Geography Analysis

Southern Vietnam remains the largest demand center in the Vietnam specialty yeast market, as Ho Chi Minh City, Binh Duong, Dong Nai, and Long An host the country’s densest concentration of food processors, breweries, pharmaceutical plants, and feed manufacturers. This cluster is important because Vietnam’s food processing market is expected to reach USD 88 billion in 2025, with a large share of industrial activity linked to the southern manufacturing corridor, according to the United States Department of Agriculture. The region provides the Vietnamese specialty yeast market with its strongest volume base across savory foods, beverages, and feed-related applications. Lesaffre’s Saf-Viet subsidiary, which has operated in Vietnam since 1999 with a local facility and Baking Center, strengthens the south’s role as the primary distribution and technical service hub. Angel Yeast also co-hosted a yeast protein seminar in Ho Chi Minh City in May 2025 with representatives from more than 60 companies, highlighting the concentration of active buyers in the region.

Northern Vietnam is emerging as the main frontier for pharmaceutical-grade demand in the Vietnam specialty yeast market, as Hanoi and nearby manufacturing corridors are well positioned to absorb higher-specification fermentation inputs. Vietnam is expected to export USD 312 million worth of pharmaceuticals from 67 enterprises in 2025, indicating that the country’s pharmaceutical base serves both domestic and export markets, according to DHG Pharma. The national pharmaceutical development program, approved in 2025, is also expected to support northern demand by increasing the need for stronger raw material capabilities and a more developed local value chain. The Mekong Delta remains strategically important for the Vietnam specialty yeast market on the feed side, as it accounts for 70% of the country’s aquaculture area and more than 70% of aquaculture output, according to Rijksdienst voor Ondernemend Nederland. This position makes shrimp and pangasius producers in the delta the most important high-volume buyers of feed-grade beta-glucans and mannan oligosaccharides.

Central Vietnam is gaining importance in the Vietnam specialty yeast market through brewing and hospitality-linked food demand rather than broad industrial scale. Carlsberg expanded its Phu Bai brewery with an investment of nearly USD 90 million, giving the region a long-term fermentation demand anchor. Tourism-led foodservice growth in central resort destinations also supports the use of specialty yeast in sauces, condiments, and premium packaged foods supplied to hotels and restaurants. Central Vietnam still trails the north and south in total consumption, but it is positioned to add steady incremental demand through the forecast period.

Competitive Landscape

The Vietnam specialty yeast market has a moderately concentrated core, with multinational ingredient suppliers holding the strongest positions through import networks, local technical service, and selected domestic operations. Lesaffre et Compagnie maintains the deepest local footprint through Saf-Viet, which has operated in Vietnam since 1999 and runs a production facility and Baking Center that support national reach. Lesaffre strengthened this position in October 2024 by acquiring DSM-Firmenich’s global yeast extract business, including the Biospringer brand and related market access capabilities. Angel Yeast is the most active challenger in the Vietnam specialty yeast market, leveraging its China-based scale to compete on price and portfolio depth. Its planned 2025 commissioning of an 8,500-tonne specialty yeast facility, its 11,000-tonne yeast protein line, and its visible marketing activity in Vietnam indicate a direct effort to build local demand across food, feed, and supplement channels.

Competition is expanding beyond basic extract supply, as the strongest opportunities are emerging in pharmaceutical-grade fermentation inputs and feed-grade immune support ingredients. Suppliers that can serve the GMP biologics space with Pichia pastoris systems, validated excipients, and stable documentation are better positioned to capture premium accounts. The Mekong Delta represents another clear white space, as high-volume aquaculture operations offer a large outlet for beta-glucans and mannan oligosaccharides if suppliers maintain competitive technical support and pricing. AB Mauri’s acquisition of Omega Yeast Labs in August 2024 further indicates that fermentation specialists are strengthening their craft brewing and specialty strain capabilities, which could support future regional offerings. As a result, the Vietnam specialty yeast market is shifting toward competition based less on simple ingredient availability and more on application depth, compliance readiness, and targeted channel development.

Technology and documentation are becoming the clearest points of differentiation in the Vietnam specialty yeast market. Companies that can demonstrate clinical support, ISO-aligned systems, or pharmacopoeial compliance for beta-glucans and nucleotide preparations can better defend pricing with supplement and pharmaceutical buyers. Limited indigenous production means local distributors continue to play an important role, preventing the market from consolidating tightly around a single manufacturer base. Overall rivalry remains moderate, as a few large international suppliers shape the top end, while import dependence and channel fragmentation create room for multiple players below them.

Vietnam Specialty Yeast Industry Leaders

Lesaffre et Compagnie

Associated British Foods plc

Angel Yeast Co., Ltd.

Lallemand Inc.

dsm-firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Angel Yeast announced two AngeoPro yeast protein variants: Hi90-A, with 88% protein content for sports nutrition, and S80-A, a 100% water-soluble variant for RTD beverages. According to Angel Yeast’s Vitafoods Europe 2026 communications, the company’s new production line at Baiyang Biotechnology Park, scheduled for commissioning in November 2025, added more than 10,000 tonnes of annual yeast protein capacity. These launches targeted the premium protein supplement and functional beverage segments globally and had direct supply implications for Southeast Asian markets.

- July 2025: Lallemand Bio-Ingredients acquired Solyve, an enzyme specialist and subsidiary of France’s InVivo Group, to strengthen its enzyme portfolio across food and beverage applications. The acquisition enhanced Lallemand’s capacity to offer integrated yeast and enzyme solutions to food manufacturers in Asia-Pacific, including Vietnam.

- June 2025: Lallemand Inc. completed the acquisition of AIT Ingredients from Moulins Soufflet (Groupe InVivo). The acquisition included AIT's operations in France, Argentina, Brazil, Spain, Asia-Pacific, and Africa, strengthening Lallemand's global footprint in baking, milling, and beverage ingredients.

Vietnam Specialty Yeast Market Report Scope

Specialty yeast refers to processed yeast products and derivatives, such as yeast extracts, autolysates, and beta-glucans, created by breaking down the proteins and cell walls of fresh yeast. The Vietnam specialty yeast market is segmented by product type, species, and application. By product type, the market is segmented into yeast extracts, autolyzed yeast, and beta-glucans. By species, the market is segmented into Saccharomyces cerevisiae, Pichia pastoris, Kluyveromyces marxianus, and others. By Application, the market is segmented into food and beverage, animal feed, dietary supplement and pharma, cosmetics and personal care, and others. The Market Forecasts are Provided in Terms of Value (USD).

| Yeast Extracts |

| Autolyzed Yeast |

| Beta-Glucans |

| Saccharomyces cerevisiae |

| Pichia pastoris |

| Kluyveromyces marxianus |

| Others |

| Food and Beverage |

| Animal Feed |

| Dietary Supplement and Pharmaceuticals |

| Cosmetics and Personal Care |

| Others |

| Product Type | Yeast Extracts |

| Autolyzed Yeast | |

| Beta-Glucans | |

| Species | Saccharomyces cerevisiae |

| Pichia pastoris | |

| Kluyveromyces marxianus | |

| Others | |

| Application | Food and Beverage |

| Animal Feed | |

| Dietary Supplement and Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Others |

Key Questions Answered in the Report

What is the current size of Vietnam specialty yeast demand?

The Vietnam specialty yeast market was valued at USD 9.9 million in 2025 and is estimated at USD 10.52 million in 2026, with growth projected to USD 15.18 million by 2031 at a 7.61% CAGR.

Which product category leads sales in Vietnam?

Yeast extracts led with 63.71% of revenue in 2025 because they are widely used in seasonings, sauces, soups, and instant noodles, where natural umami and cleaner labeling matter.

Which product segment is growing the fastest?

Beta-glucans are projected to grow at an 8.46% CAGR through 2031, helped by rising use in supplements and by expanding demand from aquaculture and animal nutrition applications.

Why are food companies increasing their use of specialty yeast ingredients?

Food processors are responding to stricter label expectations from export buyers and to the need for natural flavor support in processed foods, which makes yeast extracts a practical alternative to synthetic enhancers.

Page last updated on: