Organic Yeast Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

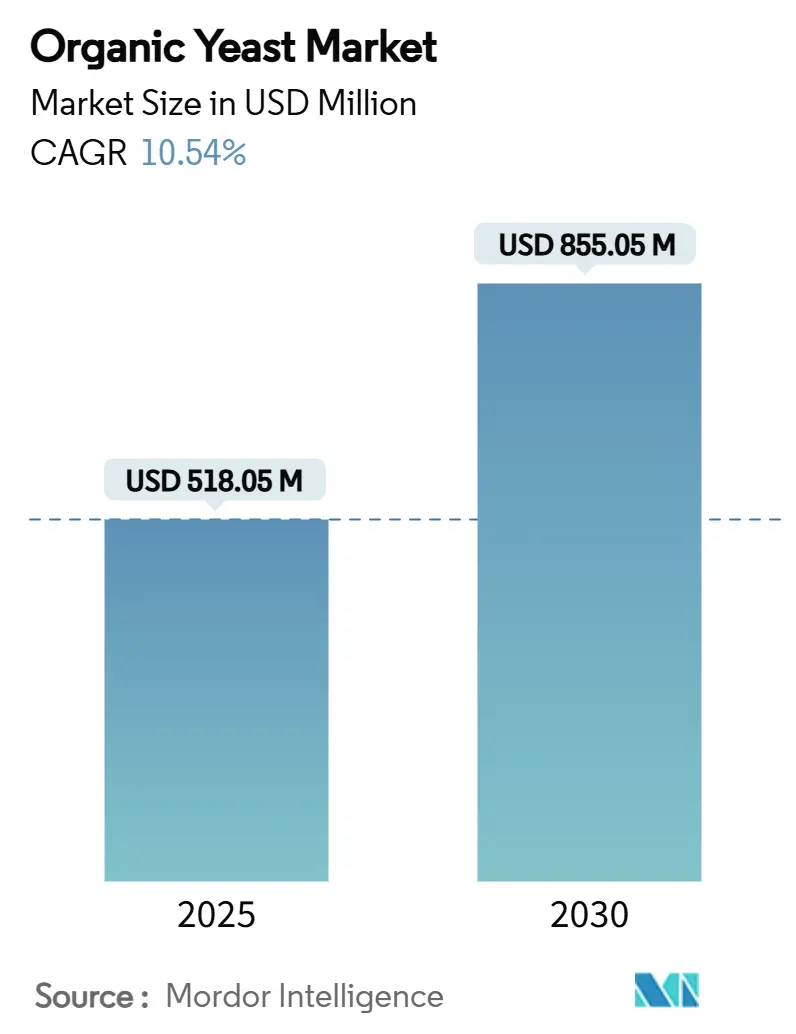

| Market Size (2025) | USD 518.05 Million |

| Market Size (2030) | USD 855.05 Million |

| Growth Rate (2025 - 2030) | 10.54% CAGR |

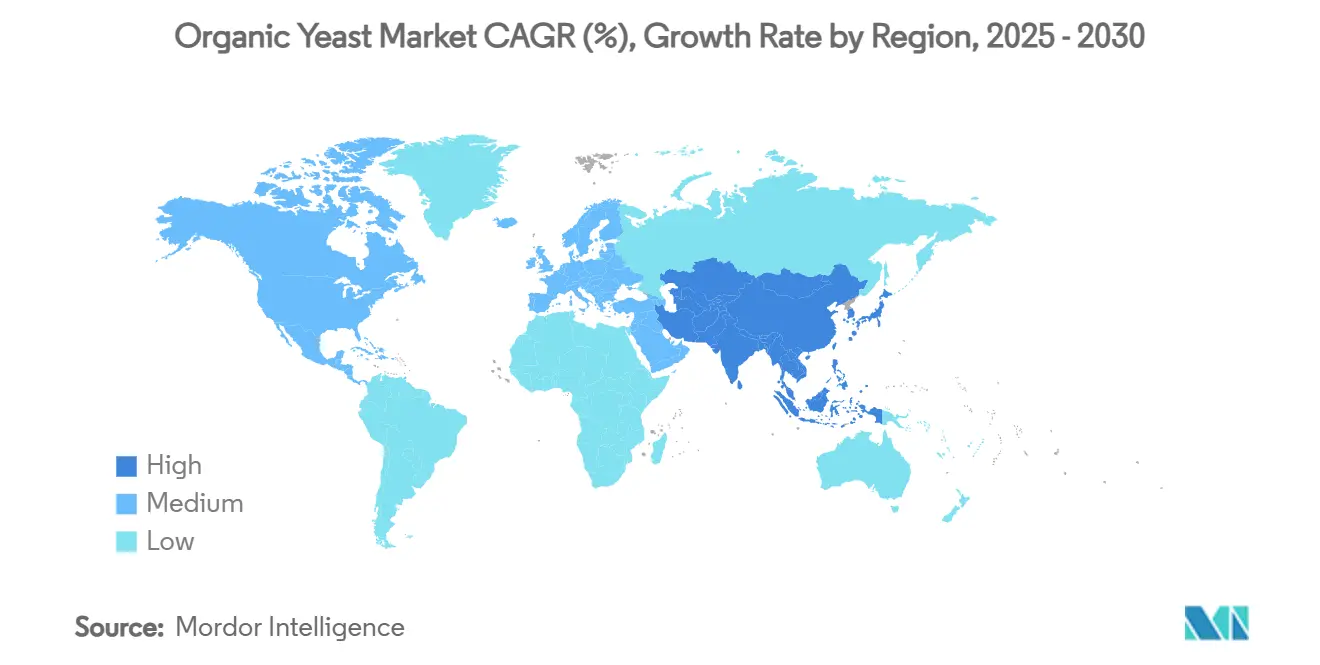

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Yeast Market Analysis by Mordor Intelligence

The Organic Yeast Market size is estimated at USD 518.05 million in 2025, and is expected to reach USD 855.05 million by 2030, at a CAGR of 10.54% during the forecast period (2025-2030). This robust growth trajectory reflects the accelerating consumer shift toward clean-label food products and the expanding applications of organic yeast across diverse end-use industries, particularly in regions where organic food regulations are becoming increasingly stringent. Macro forces driving this expansion include the surge in health-conscious consumption patterns, with over 95% of households purchasing organic items in 2025, and the strategic pivot by food manufacturers toward sustainable ingredient sourcing. The European Union's ambitious target to achieve 25% organic farmland by 2030, supported by a EUR 37.4 billion annual organic food market, creates substantial demand for certified organic ingredients including yeast [1]Source: European Commission, "Organic action plan", agriculture.ec.europa.eu. Meanwhile, Asia-Pacific emerges as the fastest-growing geography, driven by China's, and India’s organic market reaching new heights. Key risks include production cost pressures from organic certification requirements, supply chain complexities in maintaining segregated organic processes, and intensifying competition from conventional yeast alternatives that continue to offer significant cost advantages in price-sensitive applications.

Key Report Takeaways

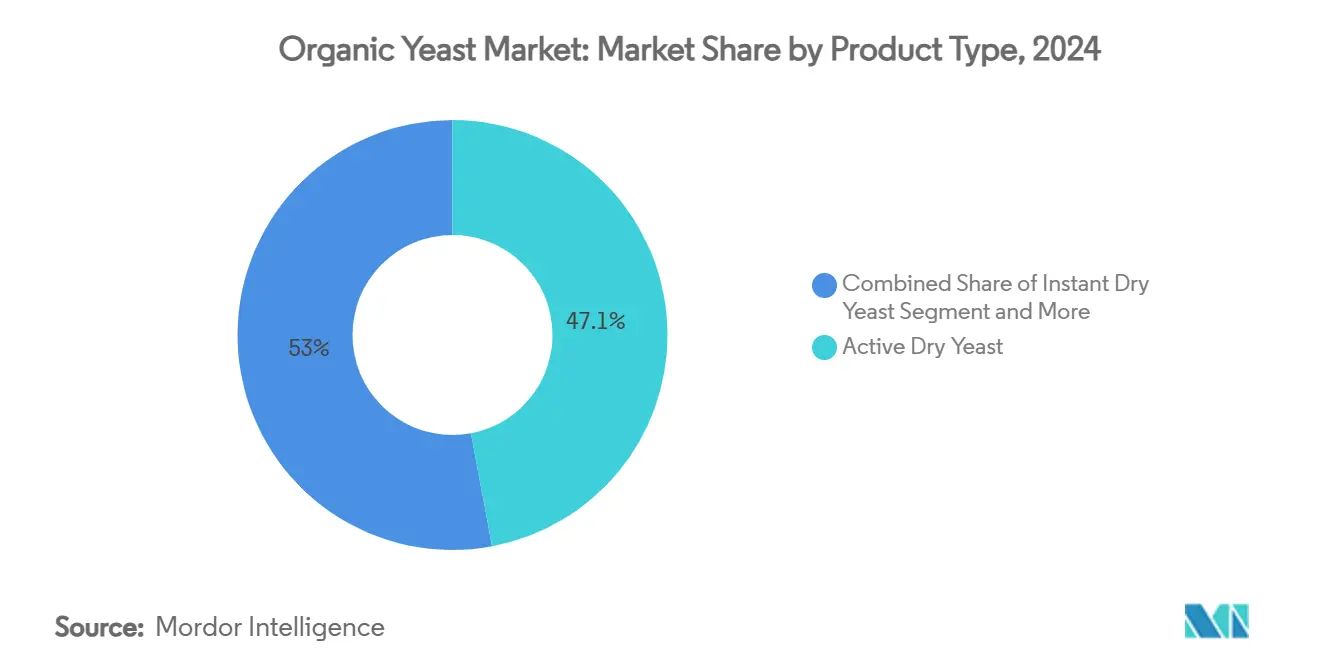

- By product type, active yeast captured 47.05% of the organic yeast market share in 2024, whereas instant dry yeast is forecast to expand at a 10.87% CAGR through 2030.

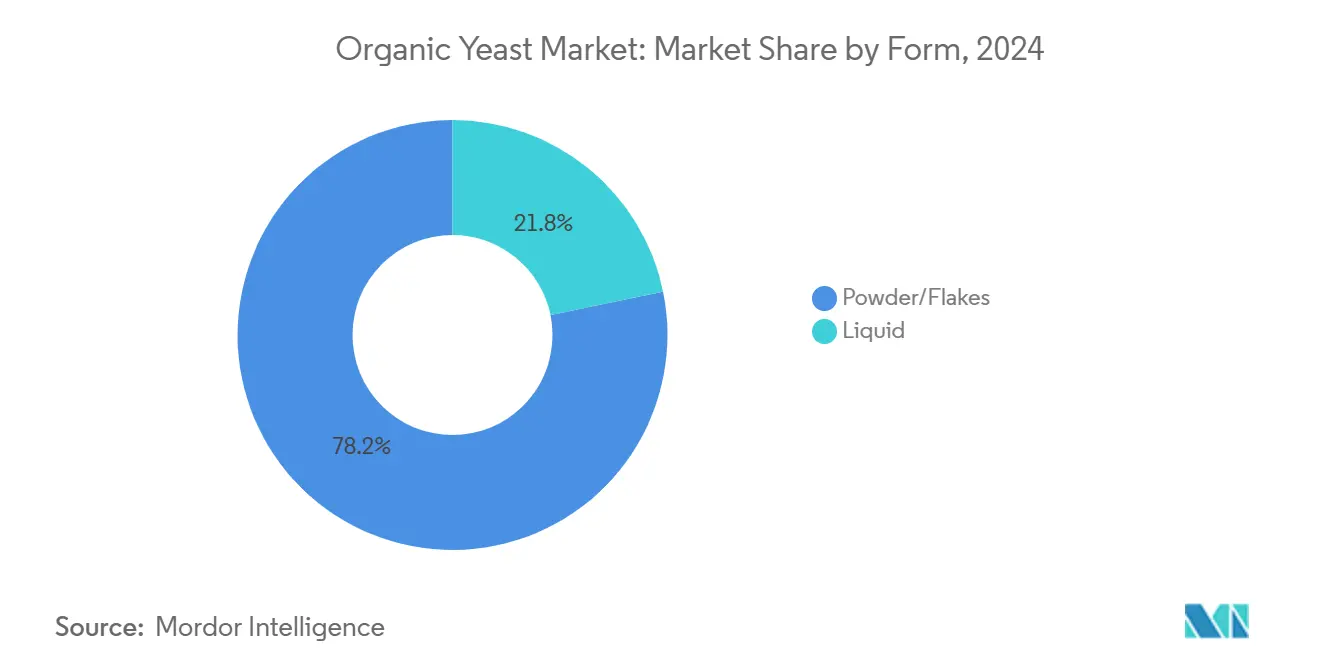

- By form, powder/flakes commanded 78.22% share of the organic yeast market size in 2024, while liquid formats are advancing at an 11.32% CAGR between 2025-2030.

- By end-use industry, food & beverage accounted for 64.37% revenue in 2024; animal feed and pet food is projected to register the fastest 12.36% CAGR to 2030.

- By geography, Europe led with 38.44% of 2024 value, while Asia-Pacific is on track for an 11.73% CAGR over the same horizon.

Global Organic Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand in Clean-Label and Organic Food Sector | +2.8% | Global, with concentration in North America & European Union | Long term (≥ 4 years) |

| Collaborations and Strategic Partnerships | +1.9% | Global, particularly Asia-Pacific expansion | Medium term (2-4 years) |

| Demand for Organic Bakery and Fermented Products | +2.1% | Europe & North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technological Advances | +1.6% | Global, with R&D centers in developed markets | Medium term (2-4 years) |

| Rising Consumer Health and Wellness Awareness | +1.8% | Global, strongest in urban centers | Long term (≥ 4 years) |

| Expansion of Online and Specialty Retail Channels | +1.2% | North America & European Union leading, Asia-Pacific following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand in Clean-Label and Organic Food Sector

The clean-label movement fundamentally reshapes ingredient procurement strategies, with organic yeast emerging as a critical enabler for manufacturers seeking to eliminate synthetic additives while maintaining fermentation efficacy. Unlike conventional yeast production that relies on molasses and chemical nitrogen sources requiring multiple washes, organic yeast utilizes certified organic grain and spring water without chemical additives, producing no contaminated wastewater. This production methodology addresses both environmental sustainability concerns and regulatory compliance requirements under USDA organic standards, which mandate organic yeast usage in certified products unless commercially unavailable[2]Source: USDA, "Certification of Organic Yeast", ams.usda.gov. As per studies, it is identified sourdough and natural fermentation as preferred clean-label alternatives in bakery applications, directly benefiting organic yeast demand as manufacturers reformulate products to meet consumer expectations for transparency and naturalness.

Demand for Organic Bakery and Fermented Products

The fermentation renaissance drives sophisticated applications beyond traditional bread-making, with precision fermentation emerging as a USD 22.8 billion market by 2033, creating substantial demand for specialized organic yeast strains. Biospringer by Lesaffre showcased yeast-based "bitter blockers" at IFT First 2025, demonstrating how organic yeast derivatives enable clean-label flavor enhancement without synthetic additives. Wine applications present particular growth opportunities, with organic yeast producing environmentally friendly wines while maintaining fermentation efficiency and potentially reducing biogenic amine formation compared to conventional alternatives. The global precision fermentation market's expansion creates demand for non-GMO yeast platforms capable of producing complex proteins and metabolites, positioning organic yeast as a preferred substrate for manufacturers seeking clean-label credentials in novel food applications.

Technological Advances

Engineering breakthroughs enable cost-effective organic yeast production through vitamin-independent cultivation methods, with researchers achieving growth rates only 17% lower than vitamin-supplemented controls while eliminating expensive B-vitamin requirements. SMEY's development of a "neobank of yeasts" containing over 1,000 characterized strains with genomic and fatty acid profiles accelerates customized organic yeast development for specific applications, reducing time-to-market for specialized fermentation products. High-cell-density production processes for probiotic yeast achieve 81% viability after gastrointestinal simulation while meeting WHO probiotic standards, expanding organic yeast applications in functional foods and dietary supplements. Patent activity intensifies around microbial cannabinoid production using organic yeast platforms, with Yarrowia lipolytica and Saccharomyces cerevisiae engineered for pharmaceutical and nutraceutical applications.

Rising Consumer Health and Wellness Awareness

Urban consumers increasingly view food as a primary tool for maintaining immunity, digestive balance, and long-term vitality, so they actively seek clean-label ingredients that deliver measurable nutritional benefits. Organic yeast answers this need because it supplies complete protein, B-vitamins, and natural flavor while avoiding synthetic additives that wellness-minded shoppers reject. Trade-fair insights for 2025 highlight holistic health and plant-based eating as core trends, positioning organic yeast as a preferred fermentative backbone for bakery, beverage, and supplement launches. Clinical research further elevates category credibility by showing that yeast protein matches whey in supporting muscle growth and even lowers diastolic blood pressure, reinforcing its appeal to sports and active-lifestyle audiences. As more shoppers read labels and link functional nutrition with disease prevention, the organic yeast market gains a durable demand engine that transcends short-term diet fads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Conventional Yeast | -1.4% | Global, most acute in price-sensitive segments | Long term (≥ 4 years) |

| Supply Chain Constraints | -0.9% | Global, with acute challenges in emerging markets | Medium term (2-4 years) |

| Production Cost and Pricing | -1.1% | Global, particularly impacting smaller producers | Long term (≥ 4 years) |

| Complex Regulatory Compliance | -0.8% | Primarily North America & European Union, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Conventional Yeast

Conventional yeast maintains substantial cost advantages through established molasses-based production systems and economies of scale that organic producers struggle to match, particularly in price-sensitive applications where fermentation performance outweighs clean-label benefits. The USDA permits non-organic yeast usage when organic alternatives are commercially unavailable, creating regulatory flexibility that conventional producers exploit through strategic supply management. Conventional yeast production benefits from decades of process optimization and infrastructure investment, enabling rapid fermentation cycles that organic producers cannot replicate without compromising certification requirements. The FDA's Generally Recognized as Safe (GRAS) status for conventional yeast derivatives provides regulatory certainty that organic alternatives must establish through more complex certification pathways [3]Source: Code of Federal Regulations, "Baker's yeast extract", ecfr.gov.

Supply Chain Constraints

Organic yeast production requires segregated supply chains to prevent contamination from conventional ingredients, creating logistical complexity and cost premiums that conventional producers avoid through integrated production systems. The requirement for organic feedstocks limits sourcing flexibility, with less than 1% of U.S. farmland certified organic, constraining raw material availability during peak demand periods. Kettering University identifies contamination prevention as a critical challenge requiring separate production processes, storage facilities, and transportation systems throughout the organic supply chain. The USDA's prohibition on petrochemical substrates and synthetic processing aids further restricts organic yeast producers' operational flexibility compared to conventional alternatives that utilize cost-effective chemical inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Active Yeast Dominance Amid Specialty Growth

Active yeast commands 47.05% market share in 2024, reflecting its essential role in bread production and fermentation applications where live cultures provide superior leavening performance compared to inactive alternatives. However, instant dry yeast emerges as the fastest-growing segment at 10.87% CAGR through 2030, driven by convenience factors and extended shelf life that appeal to both commercial bakers and home consumers seeking reliable fermentation results. Inactive yeast maintains steady demand in nutritional applications, particularly as a protein source in dietary supplements and animal feed formulations where fermentation activity is unnecessary. Yeast derivatives represent the most specialized segment, encompassing beta-glucans, nucleotides, and flavor compounds that command premium pricing in functional food applications.

The segmentation reflects broader industry trends toward convenience and functionality, with instant formats gaining traction as manufacturers prioritize ease of handling and consistent performance over traditional fresh yeast requirements. Angel Yeast's clinical trials demonstrating yeast protein's effectiveness in muscle building, comparable to whey protein while offering additional cardiovascular benefits, illustrate the expanding applications for yeast derivatives in health-focused products. Saccharomyces cerevisiae remains the dominant species across all product types, though research into non-Saccharomyces strains like Kluyveromyces marxianus expands application possibilities in high-temperature fermentation and waste valorization.

By End-Use Industry: Food Applications Lead While Feed Segments Accelerate

Food & beverage applications account for 64.37% market share in 2024, driven by organic bakery products, fermented beverages, and clean-label processed foods where organic yeast provides both functional and marketing benefits. Animal feed and pet food represents the fastest-growing segment at 12.36% CAGR through 2030, reflecting the premiumization of pet nutrition and livestock feed formulations that emphasize natural ingredients over synthetic alternatives. The "others" category encompasses pharmaceutical, cosmetic, and industrial applications where organic yeast serves as a substrate for specialized compound production.

Within food applications, bakery and confectionery dominate demand, though dairy alternatives and beverages show accelerating adoption as manufacturers reformulate products to meet organic standards. Yeast supplementation in poultry diets enhances gut health and immune system function, with studies demonstrating reduced mortality rates and improved feed conversion ratios under heat stress conditions. Pet food applications benefit from yeast's palatability enhancement properties, with 50% of pet owners prioritizing nutritional intake when selecting products, creating demand for premium organic ingredients. Torula yeast emerges as a sustainable protein alternative in cat food applications, offering superior digestibility and environmental benefits compared to traditional protein sources.

By Form: Powder Dominance Challenged by Liquid Innovation

Powder and flakes formats dominate with 78.22% market share in 2024, benefiting from superior shelf stability, reduced transportation costs, and established handling infrastructure across the food processing industry. The liquid segment, while smaller, accelerates at 11.32% CAGR through 2030 as manufacturers seek simplified integration processes and reduced dust exposure in production environments. Liquid formats offer advantages in automated dosing systems and eliminate rehydration steps that can introduce contamination risks in sensitive applications.

The form preference varies significantly by application, with bakery operations favoring powder formats for inventory management while beverage and dairy applications increasingly adopt liquid systems for precise dosing and immediate bioavailability. Cultivated Biosciences' USD 5 million funding round to develop yeast cream platforms for alternative dairy applications demonstrates the innovation potential in liquid organic yeast formats. The company's non-GMO oleaginous yeast strain produces cream-like textures that enhance mouthfeel in plant-based products while maintaining clean-label credentials essential for organic certification.

Geography Analysis

Europe maintains market leadership with 38.44% share in 2024, supported by comprehensive organic regulations and consumer acceptance of premium-priced organic ingredients across diverse food categories. The European Union's organic action plan targeting 25% organic farmland by 2030, backed by dedicated research funding allocating at least 30% of agricultural research budgets to organic sector topics, creates sustained demand for organic yeast across member states. Germany leads regional consumption through established organic food retail channels and stringent quality standards that favor certified organic ingredients. The EU's new organic regulations emphasize stricter controls and fair competition for non-EU producers, potentially benefiting domestic organic yeast manufacturers while raising barriers for imports from regions with less rigorous certification standards.

Asia-Pacific emerges as the fastest-growing region at 11.73% CAGR through 2030, driven by China's organic market expansion to 12.4 billion Euro in 2022 and India's projected organic food market growth to USD 8.9 billion by 2032 at 21.19% CAGR. China's organic certification system, established in 1994, initially focused on export markets but now serves growing domestic demand as companies like Yili and Mengniu promote organic products through consumer education initiatives. Angel Yeast's launch of probiotics production in Xizang demonstrates the regional expansion of organic yeast manufacturing capabilities to serve local markets. India's metropolitan cities including Mumbai, Pune, and Delhi lead organic food adoption, though non-metropolitan areas show strong growth potential as digital behaviors reflect a 47% increase in searches for organic food manufacturers and retailers.

North America represents a mature market with established organic food retail infrastructure and regulatory frameworks that support organic yeast adoption across diverse applications. The USDA's organic certification requirements create clear market segmentation between organic and conventional products, with organic yeast mandatory for human consumption applications unless commercially unavailable. The region benefits from advanced fermentation technology development and strong consumer willingness to pay premium prices for organic products, though growth rates moderate as market penetration increases in core segments.

Competitive Landscape

The organic yeast market exhibits moderate consolidation, indicating established players maintain significant market positions while leaving opportunities for specialized producers and regional competitors. Strategic patterns emphasize vertical integration and geographic expansion, with major players acquiring complementary capabilities rather than direct competitors to build comprehensive organic ingredient platforms. Major players include Lallemand Inc, Lesaffre Corporation, Alltech., Martin Braun-Gruppe, and Loov Organic, LLC, among others.

Lesaffre's acquisition of Biorigin and DSM-Firmenich's divestiture of yeast extract operations to Lesaffre illustrate the industry's consolidation toward specialized organic fermentation expertise. Technology deployment focuses on production efficiency improvements and application-specific strain development, with companies investing in high-cell-density cultivation methods and vitamin-independent growth systems to reduce production costs while maintaining organic certification compliance.

Patent activity intensifies around engineered yeast platforms for specialized applications, including cannabinoid production and precision fermentation of complex proteins. Opportunities exist in emerging applications such as cultivated meat production, pharmaceutical synthesis, and waste valorization where organic yeast provides sustainable alternatives to conventional chemical processes. The EPA's registration of Saccharomyces cerevisiae as a biopesticide demonstrates regulatory acceptance of yeast in novel applications beyond traditional food uses.

Organic Yeast Industry Leaders

-

Lallemand Inc

-

Lesaffre Corporation

-

Alltech.

-

Martin Braun-Gruppe

-

Loov Organic, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Lesaffre, an independent key global player in fermentation and microorganisms, announced the signing of a transaction with DSM-Firmenich, a leading innovator in nutrition, health and beauty, regarding its yeast extract business.

- January 2023: Lallemand Health Solutions launched the first and unique organic version of probiotic yeast Saccharomyces boulardii to mark the hundredth anniversary of its discovery. This innovative positioning for S. boulardii created new opportunities for consumers looking to make conscious buying choices. Lallemand Health Solutions was a pioneering company recognized as a vertically integrated lab to shelf global leader in the manufacturing of probiotic yeast and bacteria-based formulas for human health supplements, for food applications, and nutricosmetics.

Global Organic Yeast Market Report Scope

| Active yeast |

| Inactive yeast |

| Yeast Derivatives |

| Powder/Flakes |

| Liquid |

| Food & Beverage | Bakery and Confectionery |

| Savory and Snacks | |

| Dairy and Dairy Alternatives | |

| Beverages | |

| Others | |

| Animal Feed and Pet Food | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Active yeast | |

| Inactive yeast | ||

| Yeast Derivatives | ||

| By Form | Powder/Flakes | |

| Liquid | ||

| By End-Use Industry | Food & Beverage | Bakery and Confectionery |

| Savory and Snacks | ||

| Dairy and Dairy Alternatives | ||

| Beverages | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected global value of organic yeast by 2030?

It is expected to reach USD 855.05 million, up from USD 518.05 million in 2024.

How fast is revenue from organic yeast anticipated to expand?

Sales are forecast to grow at a 10.54% CAGR between 2025 and 2030.

Which product format is seeing the quickest uptake?

Instant dry yeast leads expansion, advancing at a 10.87% CAGR through 2030 due to convenience and shelf-life advantages.

Where is demand growing the fastest geographically?

Asia-Pacific is on track for an 11.73% CAGR, propelled by rising clean-label adoption in China and India.

Page last updated on: