Yeast And Yeast Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 8.79 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

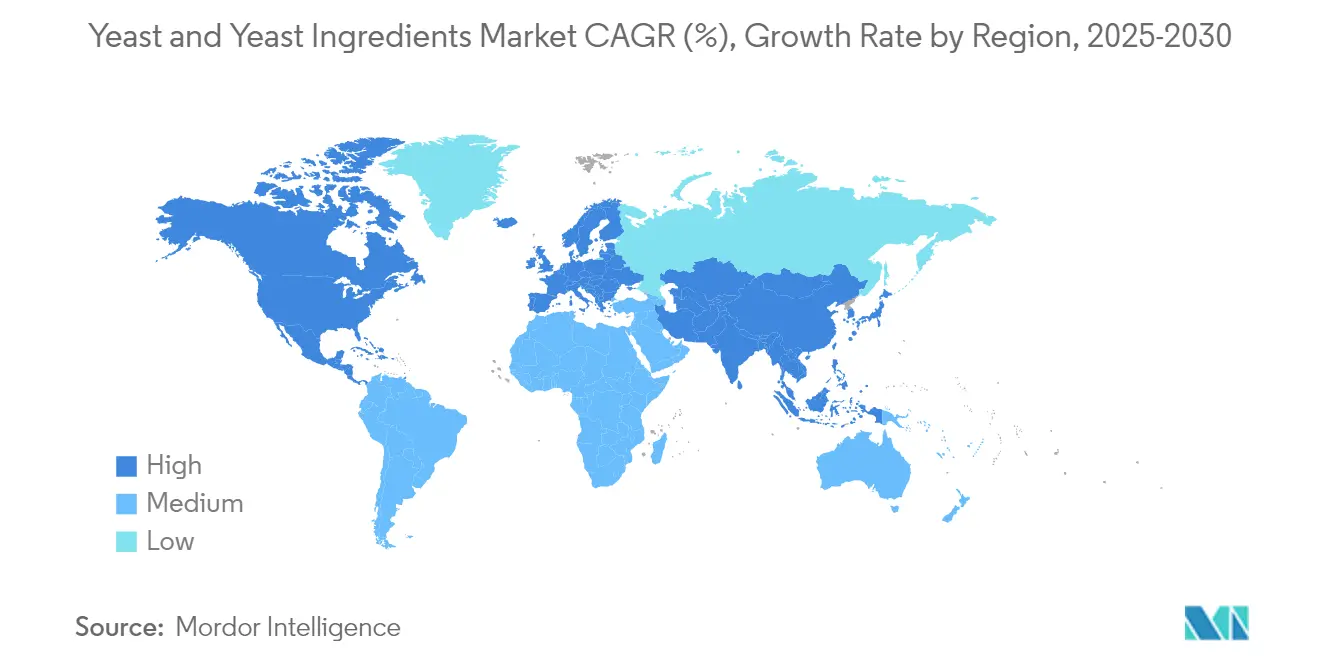

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Yeast And Yeast Ingredients Market Analysis by Mordor Intelligence

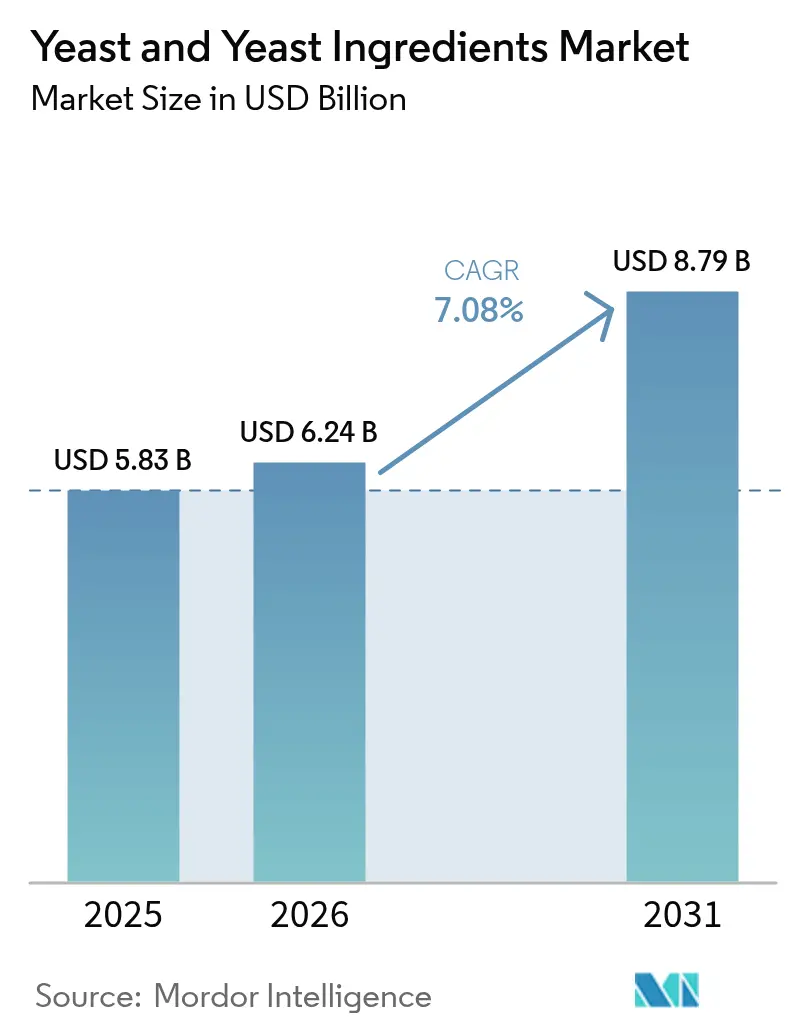

The global yeast and yeast ingredients market size was valued at USD 5.83 billion in 2025 and estimated to grow from USD 6.24 billion in 2026 to reach USD 8.79 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031). Robust expansion reflects a steady pivot from commodity baker’s yeast toward specialty extracts, beta-glucans, nucleotides, and probiotic strains that meet rising demand for clean-label, functional products in food, beverage, nutraceutical, and animal nutrition channels. Growth also benefits from regulatory preference for Generally Recognized as Safe (GRAS) or Qualified Presumption of Safety (QPS) microorganism status, which accelerates time-to-market for Saccharomyces-based innovations. Europe remains the largest regional consumer on the back of historic bakery culture and strict additive oversight, whereas Asia-Pacific emerges as the fastest-growing territory due to rapid food-processing investments in China and India, coupled with widening acceptance of microbiome-targeted supplements. Meanwhile, advances in precision fermentation have opened new revenue pools in pharmaceuticals and sustainable chemicals, further supporting mainstream adoption across end-use industries.

Key Report Takeaways

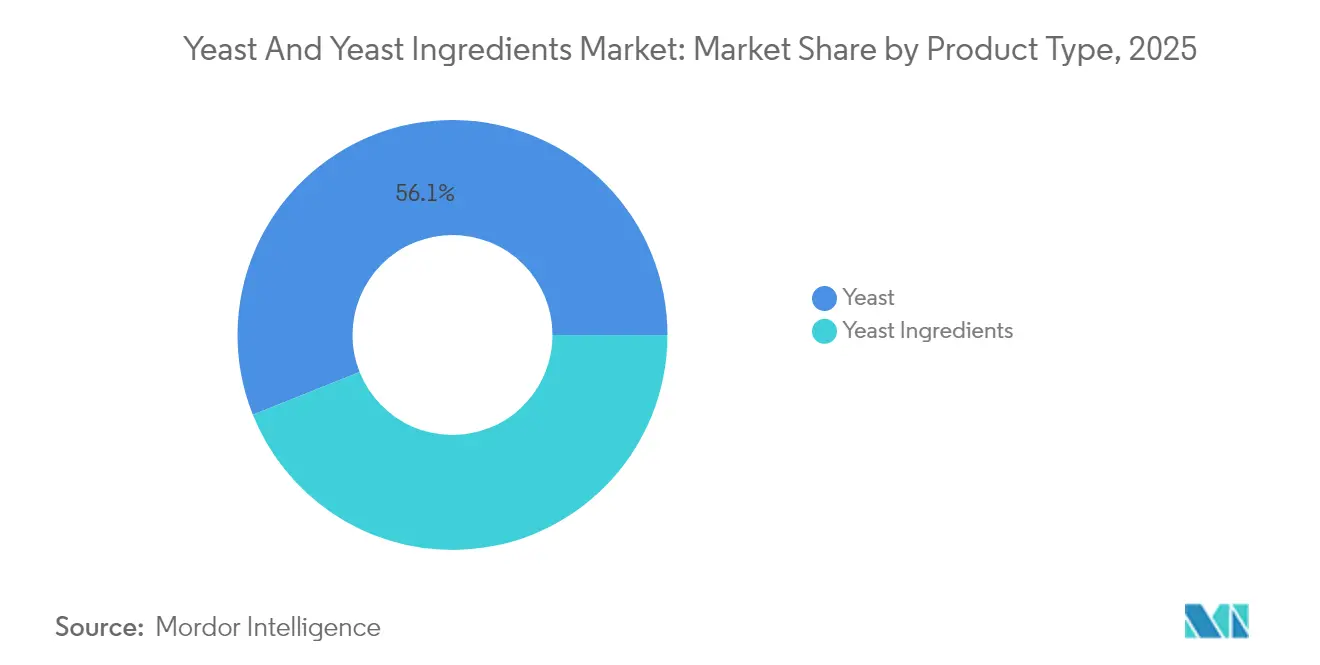

- By product type, yeast commanded 56.05% of the 2025 yeast and yeast ingredients market share, and yeast ingredients are forecast to grow at a 9.18% CAGR through 2031.

- By form, active dry yeast held 39.10% of the 2025 yeast and yeast ingredients market size, while instant dry yeast is expected to expand at a 9.55% CAGR by 2031.

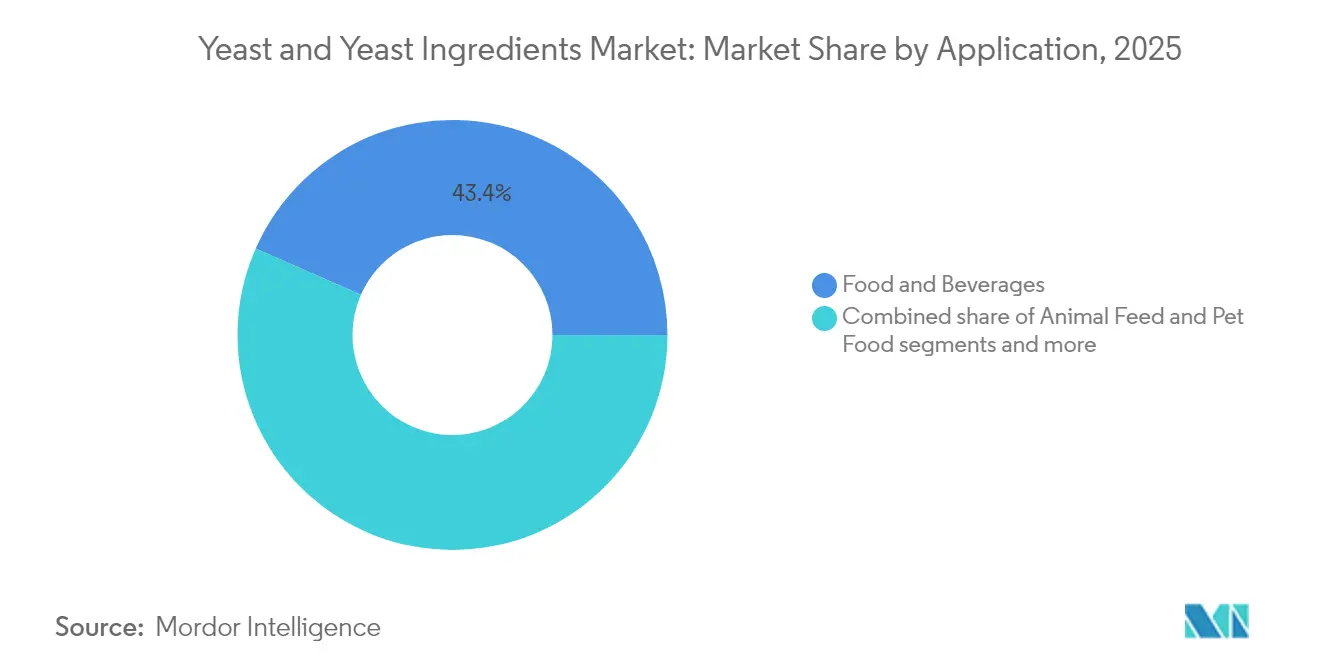

- By application, food and beverages accounted for 43.40% of demand in 2025, and pharmaceuticals and dietary supplements are projected to advance at a 9.62% CAGR to 2031.

- By geography, Europe led with 33.55% revenue share in 2025, and Asia-Pacific is set to clock the fastest 9.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Yeast And Yeast Ingredients Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of natural and clean label ingredients | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Expansion of the bakery industry | +1.5% | Global, with accelerated growth in Asia-Pacific | Long term (≥ 4 years) |

| Increasing use in nutritional supplements and fortified foods | +1.2% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in yeast fermentation | +1.0% | Global, with innovation centers in Europe and North America | Long term (≥ 4 years) |

| Growing adoption in animal nutrition | +0.8% | Global, with strongest growth in Asia-Pacific and South America | Medium term (2-4 years) |

| Expansion of microbiome-targeted nutraceutical yeasts | +0.7% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Natural and Clean Label Ingredients

Consumer skepticism toward synthetic additives drives demand for yeast-based flavor enhancers and nutritional ingredients. According to the International Food Information Council, in 2024, nearly 26% of respondents in the United States indicated that "Natural" best defines healthy food, with yeast extracts increasingly replacing artificial flavor enhancers in savory applications [1]Source: International Food Information Council, “2024 IFIC Food & Health Survey,” Food Insight, foodinsight.org. Yeast extracts have expanded beyond traditional uses, serving as umami enhancers in sodium-reduced formulations, where their natural glutamate content provides flavor depth without synthetic additives. Research shows yeast extract effectively masks off-flavors in sodium-reduced marinated products, functioning as an ingredient that addresses both clean-label requirements and health-conscious reformulation needs. The Generally Recognized as Safe (GRAS) status of yeast ingredients eliminates lengthy approval processes required for synthetic alternatives. Food manufacturers now consider yeast ingredients as protection against evolving clean-label regulations, resulting in sustained demand growth independent of market fluctuations.

Expansion of the Bakery Industry

Global bakery expansion extends beyond traditional bread categories into premium, artisanal, and health-focused segments, increasing the demand for specialized yeast formulations. Yeast enhances product characteristics in baked goods such as pizza, bread, and homemade items. The growth of the bakery and confectionery industry supports this segment's expansion. According to LocalCircles, a November 2023 survey on sugar consumption in India revealed that 31% of respondents consumed bakery products daily. The industry's transition toward gluten-free and allergen-free products necessitates specialized yeast strains and fermentation processes, prompting manufacturers to develop targeted solutions for alternative flour systems. While emerging markets drive volume growth, developed markets emphasize premiumization, creating parallel demand for both commodity and specialty yeast products. The development of portion control and convenience formats generates additional growth opportunities, particularly for instant and active dry yeast formulations that align with contemporary consumption patterns.

Increasing Use in Nutritional Supplements and Fortified Foods

Yeast has evolved from a traditional fermentation agent into a nutritional delivery system, enabling high-value applications in dietary supplements and functional foods. Selenium-enriched yeast demonstrates this advancement, with EFSA approvals allowing selenium content formulations up to 3,000 mg/kg, which enables more concentrated nutritional supplements while maintaining safety standards. The extraction of beta-glucan from yeast cell walls produces immune-supporting ingredients with demonstrated effectiveness, while B-vitamins derived from yeast provide better bioavailability than synthetic versions. The FDA's GRAS status for yeast hydrolysate peptide complexes in nutritional applications validates the regulatory acceptance of modern yeast processing methods. Probiotic yeast applications have expanded beyond conventional Saccharomyces boulardii to include engineered strains with enhanced therapeutic benefits, such as improved gastric acid resistance and specific metabolite production. This integration of biotechnology and nutrition creates opportunities for premium pricing that exceed traditional yeast applications.

Technological Advancements in Yeast Fermentation

Technological advancements in yeast fermentation are driving significant growth in the global yeast and yeast ingredients market. Innovations in strain improvement, metabolic engineering, and precision fermentation have enhanced the efficiency, yield, and versatility of yeast production. These developments enable the production of specialized yeast strains with specific functionalities, including improved flavor profiles, stress tolerance, and productivity. Revyve, a Dutch food technology company, introduced a yeast-based texturizing ingredient in September 2024. This ingredient, developed through a proprietary process using baker's yeast, functions as a clean-label, allergen-free egg replacer with neutral flavor and color. It provides emulsification, gelling, binding, and water retention benefits, making it applicable in sauces, baked goods, confectionery, and plant-based dairy alternatives. Non-conventional yeast platforms, such as Issatchenkia orientalis, are emerging as valuable alternatives due to their enhanced stress tolerance and ability to process diverse substrates compared to traditional Saccharomyces cerevisiae [2]Source: United States Department of Agriculture, “Development of Microbial Platforms Capable of Co-Fermenting Non-Conventional Substrates for Enhanced Production of Value-Added Chemicals,” USDA, usda.gov. Yeast continues to establish itself as a fundamental platform technology for sustainable manufacturing, with growing applications across food, pharmaceuticals, chemicals, and materials industries.

Restraints Impact Analysis of Yeast And Yeast Ingredients Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of specialty yeast ingredients | -1.2% | Global, with strongest impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Fluctuations in raw material prices | -0.9% | Global, with particular impact on molasses-dependent regions | Short term (≤ 2 years) |

| Limited consumer awareness of yeast-based ingredients | -0.6% | Asia-Pacific and emerging markets primarily | Medium term (2-4 years) |

| Competition from alternative flavor enhancers | -0.4% | Global, with strongest competition in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialty Yeast Ingredients

Premium yeast ingredients cost 3-5 times more than commodity yeast, limiting their adoption in price-sensitive applications and emerging markets. The production of selenium-enriched yeast requires specialized fermentation conditions and quality control systems, which increase manufacturing costs. The limited number of approved production facilities restricts supply and maintains high prices. Regulatory compliance requirements for new yeast ingredients add significant costs, especially for applications requiring extensive safety documentation and clinical validation. Small and medium-sized food manufacturers often lack the technical expertise to use specialty yeast ingredients effectively, which limits market penetration despite their proven benefits. The cost-benefit ratio becomes favorable primarily in high-value applications such as nutraceuticals and premium food products, which restricts the widespread adoption of advanced yeast technologies.

Fluctuations in Raw Material Prices

The yeast production industry relies heavily on agricultural feedstocks, primarily molasses and sugar-based substrates, making manufacturers vulnerable to commodity price fluctuations that affect profit margins. While agricultural waste utilization and alternative substrates present opportunities for cost reduction, these solutions require significant capital investment in fermentation technologies and regulatory compliance. The energy-intensive nature of fermentation processes, which demand precise temperature and aeration control, makes production costs sensitive to utility price changes. For companies that source raw materials internationally while serving local markets, currency fluctuations in emerging markets further intensify input cost challenges. Recent global supply chain disruptions have highlighted the industry's vulnerability to input availability and pricing volatility, resulting in periodic margin pressures that limit investments in capacity expansion and innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Yeast And Yeast Ingredients Market Segment Analysis

By Product Type:

Yeast Ingredients Drive Innovation PremiumYeast holds a dominant 56.05% market share in 2025, driven by its essential role in traditional fermentation processes, while the yeast ingredients segment demonstrates the highest growth potential, with a projected CAGR of 9.18% through 2031. This growth pattern indicates a market shift toward specialized applications where yeast ingredients generate higher margins through enhanced functionality. Baker's yeast remains the primary product in conventional applications, supported by steady demand from the expanding global bakery industry. Brewer's yeast maintains its significance in the growing craft beer sector and nutritional supplements market due to its high B-vitamin and protein content.

Wine yeast benefits from the increasing premium wine production globally, as specialized strains enhance wine characteristics and terroir expression. Torula and non-Saccharomyces yeasts are gaining importance in new fermentation applications, particularly in alternative protein development and flavor enhancement. Yeast extracts lead the ingredients segment expansion, primarily due to their role in clean-label product reformulation and natural umami flavor enhancement, replacing artificial flavor compounds.

By Form:

Instant Dry Yeast Captures Convenience PremiumActive dry yeast holds a 39.10% market share in 2025, supported by established distribution networks and familiar handling characteristics. Instant dry yeast demonstrates the highest growth rate at 9.55% CAGR through 2031, driven by its convenience, shelf stability, and consistent performance. Fresh yeast retains its position in commercial bakery operations where immediate use and superior fermentation properties offset its handling requirements and limited shelf life.

Instant dry yeast adoption increases in emerging markets where infrastructure constraints favor products with longer shelf life and enhanced distribution capabilities. Professional bakers select instant formulations for their direct-addition properties and reduced hydration needs, which optimize production efficiency. The growth in home baking, driven by lifestyle changes, supports instant dry yeast demand due to its reliable performance and extended storage life that suits occasional usage.

By Application:

Pharmaceuticals Lead Growth TransformationThe food and beverages segment holds 43.40% market share in 2025, highlighting yeast's essential role in traditional food applications. The pharmaceuticals and dietary supplements segment is projected to grow at 9.62% CAGR through 2031, as yeast transitions from a basic ingredient to a key component in therapeutic and nutritional applications.

Within the food and beverages sector, bakery and confectionery applications maintain consistent growth, driven by the increasing global population and urbanization that boost processed food demand. The savory and snacks segment expands through clean-label initiatives, with manufacturers using yeast extracts to replace artificial flavor enhancers. Dairy and dairy alternatives present new opportunities, particularly in probiotic products where yeast complements bacterial cultures. The animal feed and pet food segments show stable growth due to expanding livestock production in developing markets and increased focus on premium pet nutrition.

Geography Analysis

Europe Yeast And Yeast Ingredients Market

Europe holds a 33.55% market share in 2025, supported by traditional food practices, quality regulations, and biotechnology infrastructure that create premium market positioning. The yeast and yeast ingredients market is driven by consumer demand for clean-label products and natural fermentation processes. Europe's established bakery industry, along with expanding applications in savory snacks, meat alternatives, and functional beverages, positions the region as a significant center for yeast product development.

APAC, The Americas and MEA Yeast And Yeast Ingredients Market

The Asia-Pacific region shows the highest growth potential with a 9.31% CAGR through 2031, fueled by industrial development, increased consumer spending, and government initiatives in food processing modernization. China's expanding food processing sector presents significant opportunities for yeast manufacturers, with regulations emphasizing food safety and quality standards that benefit established international suppliers. North America exhibits consistent growth through product innovation and premiumization, particularly in high-margin specialty segments. South America's agricultural resources and increasing protein consumption support both food and animal feed applications, while the Middle East and Africa show growth potential due to developing food processing capabilities and growing urban populations.

Regulatory Landscape

Regulatory requirements for yeast and yeast-derived ingredients are shaped by food additive, novel food, and microorganism safety frameworks, which affect labeling, permissible uses, and time-to-market for new strains and fractions. In the United States, many yeast-derived ingredients are commercialized via the FDA Generally Recognized as Safe (GRAS) pathway, supported by codified specifications for certain yeast-derived materials (for example, baker's yeast glycan under 21 CFR 172.898) and voluntary GRAS notices listed in the FDA GRAS Notice Inventory.

In the European Union, yeast ingredients used as additives and flavorings fall under Regulation (EC) No 1333/2008 and related implementing measures, while novel yeast biomasses and new ingredient categories require authorization under the EU Novel Food regime (with the Union list under Regulation (EU) 2017/2470). Implementing Regulation (EU) 2024/2044 (July 2024) updated specifications for Yarrowia lipolytica yeast biomass, including heavy metal limits, which increases the need for tighter analytical controls and traceability for yeast-derived novel ingredients sold into food and supplement applications.

Value Chain Analysis

The value chain starts with carbohydrate feedstocks (notably cane and beet molasses and hydrolyzed grains), followed by industrial fermentation to build yeast biomass. Downstream processing includes separation and concentration, autolysis or hydrolysis for extracts, autolysates, and peptides, and drying for active dry and instant formats. Finished products move through ingredient distributors and direct key-account supply to industrial bakeries, beverage and savory manufacturers, feed premixers, and nutraceutical and pharmaceutical formulators, where technical service and application support are often bundled with supply.

Major integrated producers such as Lesaffre, Angel Yeast, Lallemand, AB Mauri (Associated British Foods), and Ohly underpin global capacity and strain development, with differentiation increasingly tied to proprietary strain libraries and process know-how for specialty fractions (beta-glucans, nucleotides, and functional proteins). Key constraints center on fermentation capacity utilization and contamination control. The energy intensity of drying and concentration steps also elevates sensitivity to utility costs, which supports competitive advantage for operators investing in efficient spray drying and modern fermentation assets.

Competitive Landscape

Global leaders like Lesaffre, Angel Yeast, and Associated British Foods dominate the yeast and yeast ingredients market, leveraging scale economies in baker's yeast. Their focus on innovation allows them to meet the growing demand for clean-label ingredients, functional food applications, and sustainable production methods. Additionally, these companies are expanding their global presence through strategic partnerships, acquisitions, and collaborations, further strengthening their competitive position in the market.

The market is witnessing significant growth opportunities in emerging segments such as microbiome therapeutics, sustainable protein manufacturing, and specialized animal feed formulations. These segments are characterized by high technical complexity, including advanced fermentation techniques and compliance with stringent regulatory frameworks, which create substantial barriers to entry. The increasing consumer focus on personalized nutrition and environmentally friendly products further drives the demand for advancements in these segments.

Smaller companies are gaining traction by targeting niche segments and regional markets, leveraging their agility and deep understanding of local regulatory environments. By building strong customer relationships and adopting innovative technologies, smaller players are able to compete effectively with larger global firms. Additionally, many of these companies are embracing sustainable practices and developing specialized products tailored to specific consumer demands, enabling them to differentiate themselves and secure a loyal customer base in an increasingly competitive market.

Yeast And Yeast Ingredients Industry Leaders

Associated British Foods plc

Angel Yeast Co. Ltd.

Lesaffre Yeast Corporation

Lallemand Inc.

Novonesis

- *Disclaimer: Major Players sorted in no particular order

Yeast And Yeast Ingredients Market Companies Covered in this Report

- Lesaffre Group

- Angel Yeast Co. Ltd.

- Associated British Foods (AB Mauri, ABF Ingredients)

- Lallemand Inc.

- Oriental Yeast Co., Ltd.

- Kerry Group

- Enzym Group

- Alltech Inc.

- Kohjin Life Sciences

- Van Wankum Ingredients

- Sensient Technologies

- Titan Biotech

- Pak Group (Pakmaya)

- Mitushi Bio Pharma

- Leiber GmbH

- Imperial Yeast

- Kothari Fermentation & Biochem

- Bioven Ingredients

- Novonesis

- High-Grown Yeast Co.

Market Opportunities and Future Outlook

Opportunities are expanding where customers pay for functional performance and clean-label formulation support rather than commodity leavening alone, particularly in savory taste systems (yeast extracts and specialty high-nucleotide yeast), immune and gut-health ingredients (beta-glucans, postbiotics, probiotic strains), and protein fortification (yeast protein for foods and supplements). In Europe, investment signals include Ohly bringing a new spray drying tower and fermentation facility into operation at its Hamburg, Germany site (announced January 2026), and Lesaffre investing in beer yeast production and packaging facilities at its Algist Bruggeman plant in Ghent, Belgium (announced August 2025), both geared toward higher value formats and tighter quality control expectations.

A second whitespace involves precision fermentation outputs that extend beyond classic bakery and beverage uses, including yeast-derived lipids and tailored bioactives for food, nutraceutical, and adjacent industrial applications. Clean Food Group securing GBP 5.2 million in April 2026 to scale fermentation manufacturing in Knowsley, Liverpool provides a concrete indicator of capital moving toward yeast-enabled alternative ingredient platforms. It also points to continued demand for scalable fermentation infrastructure, downstream drying capability, and robust regulatory dossiers across end-use categories.

Recent Industry Developments in Yeast And Yeast Ingredients Market

- June 2026: Angel Yeast announced a CNY 422.4 million investment to expand an industrial park, adding capacity and capabilities that support higher value yeast-derived products. This investment strengthens supply positioning for specialty yeast ingredients used in nutrition, feed, and food applications where purity and consistent performance are critical.

- May 2026: Biospringer (Lesaffre) acquired bacterial fermentation technologies from PTX Food Corp, including the Bioenhance product line, widening its fermentation toolbox beyond traditional yeast processes. This acquisition supports broader savory and functional ingredient development and enables multi-technology formulation options for customers seeking clean-label taste and performance solutions.

- April 2024: Lesaffre opened a new yeast manufacturing facility in Malang Regency, East Java, Indonesia through PT Lesaffre Sari Nusa (a joint venture with PT Citra Bonang), producing compressed and dry yeast for Indonesia and ASEAN baking markets. The added regional manufacturing footprint improves lead times and supports growth in local industrial baking and food processing.

Yeast And Yeast Ingredients Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the commercial value of yeast and yeast-derived ingredients used by manufacturers across food and beverages, animal feed, nutraceuticals, and pharmaceuticals. It includes common yeast types used for fermentation as well as value-added yeast derivatives sold as functional ingredients.

Scope exclusions: We exclude non-yeast microbial starters and retail home-baking sachets sold to consumers.

Segments Covered in This Report

- By Product Type

- Yeast

- Baker’s Yeast

- Brewer’s Yeast

- Wine Yeast

- Torula/Non-Saccharomyces Yeast

- Yeast Ingredients

- Yeast Extracts

- Autolysates

- Beta-Glucan

- Derivatives

- Specialty/High-nucleotide Yeast

- Yeast

- By Form

- Fresh Yeast

- Active Dry Yeast

- Instant Dry Yeast

- By Application

- Food and Beverages

- Bakery and Confectionery

- Savory and Snacks

- Dairy and Dairy Alternatives

- Beverages

- Others

- Animal Feed and Pet Food

- Pharmaceuticals and Dietary Supplements

- Others

- Food and Beverages

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting view of supply, demand, and pricing patterns for yeast and yeast ingredients, and then to set practical ranges for variables before interviews began. We relied on public sources such as FAOSTAT for agricultural inputs, UN Comtrade for trade flows, USFDA and EFSA pages for additive and food ingredient context, and USDA publications for grain and bakery demand signals, which often move yeast volume demand.

Along with these, we reviewed company annual reports, investor decks, product catalogs, and trade association publications to understand product definitions and where yeast derivatives (like extracts and beta-glucans) are typically sold and labeled. Patent databases were also used to track activity around specialty yeast derivatives and new applications, which helped sanity-check what was truly being commercialized versus what was still experimental. The desk sources listed here are not exhaustive, and other public references were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to convert broad desk signals into realistic conversion factors, price ladders, and adoption assumptions, since yeast products vary by form and end use. We spoke with a mix of ingredient suppliers, distributors, and downstream users in bakery, brewing, processed foods, and animal nutrition across APAC, EMEA, and the Americas, and we re-checked key inputs when responses differed.

To keep the model grounded, we triangulated feedback across roles, and the same pricing and volume logic was reviewed from commercial, technical, and procurement viewpoints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 47% |

| Mid tier: 55% | Functional/Unit leaders: 42% | EMEA: 32% |

| Smaller Players: 20% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where production, trade, and end-use indicators are used to reconstruct the addressable demand pool for yeast and yeast ingredients by region, and then values are derived using application-linked price bands. Once that shape is established, it is corroborated with selective bottom-up approximations, such as sampled supplier revenue ranges, channel checks for major application categories, and simple volume times ASP math for high-visibility products.

Key inputs used in the model include bakery output and packaged food volumes, beer and spirits fermentation activity as a proxy for brewer and distiller yeast usage, animal feed production trends, import and export movements for yeast and yeast derivatives, and observed price differences by form (fresh versus dry) and by ingredient type (whole yeast versus extracts and autolysates). When bottom-up checks are incomplete for smaller countries or niche derivatives, gaps are handled using peer-market analogs and conservative penetration assumptions, which are then adjusted after expert review.

For forecasting, scenario analysis is applied around drivers that most directly move demand, such as processed food growth, fermentation-based beverage production, feed cycles, and gradual mix shifts toward specialty yeast derivatives. The forward view is anchored to consensus ranges gathered from interviews, and then smoothed to avoid unrealistic jumps in volumes or ASPs from one year to the next.

Data Validation & Update Cycle

Validation is done through multiple checks so the final totals stay consistent with independent signals, not just one data stream. We compare implied per-capita consumption and regional import reliance against what trade data and food production indicators suggest, and then outliers are reviewed before sign-off.

When a variance is large, the assumptions behind it are revisited, followed by re-contacting relevant respondents to confirm whether the shift is real or reflects a definition mismatch. Reports are refreshed annually, and interim updates are made when material events change pricing, trade flows, or end-use demand. Before delivery, a final analyst pass is completed so clients receive the most current view available.

Mordor Intelligence's Global Yeast and Yeast Ingredients Market Market Sizing Compared With Other Published Estimates

Published market sizes for yeast and yeast ingredients often differ because the underlying scope and the counting logic are not consistent across sources. In this space, small definition changes, such as whether derivatives are treated as separate ingredients or folded into whole yeast, can change the total value materially.

The main gap comes from what gets counted as yeast ingredients and when specialty derivatives are included, since some estimates focus on ingredients-only and others mix in broader yeast categories. Another driver is how average selling prices are projected, where certain sources apply a single blended inflation factor, while others use different price paths by form and by application. Base year differences and currency timing also contribute to the spread.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.24 B (2026) | |

| Global Consultancy A | USD 7.64 B (2025) | Covers yeast ingredients only, which typically emphasizes extracts and derivatives, and it uses a different base year, which can shift the value when pricing is volatile. |

| Industry Publisher B | USD 9.65 B (2024) | Uses a broader ingredients framing with a different product list and a longer horizon, and the value can rise if nutritional yeast and multiple derivative forms are grouped under one expanded scope. |

The spread in the table is largely explained by scope and timing choices rather than math errors, and it is why we document each inclusion and pricing step clearly. The main gap comes from what gets counted as yeast ingredients and when specialty derivatives are included, a choice applied by Mordor Intelligence by separating whole yeast used for fermentation from value-added derivatives only when they are sold as distinct ingredients.

Key Questions Answered in the Report

How big is the yeast and yeast ingredients market in 2026?

The yeast and yeast ingredients market size is valued at USD 6.24 billion in 2026, with a forecast to reach USD 8.79 billion by 2031 at a 7.08% CAGR.

Which region leads global demand?

Europe holds the largest 33.55% revenue share because of entrenched bakery consumption and a strict clean-label regulatory culture.

What segment is expanding the fastest?

Pharmaceutical and dietary supplement applications are growing at 9.62% annually owing to regulatory approvals for selenium-enriched, chromium-enriched, and probiotic yeast ingredients.

Why are instant dry yeast products gaining traction?

Instant dry yeast offers long shelf life and direct-add convenience, supporting a projected 9.55% CAGR that outpaces all other form factors.

Page last updated on: