Bakers Yeast Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.3 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

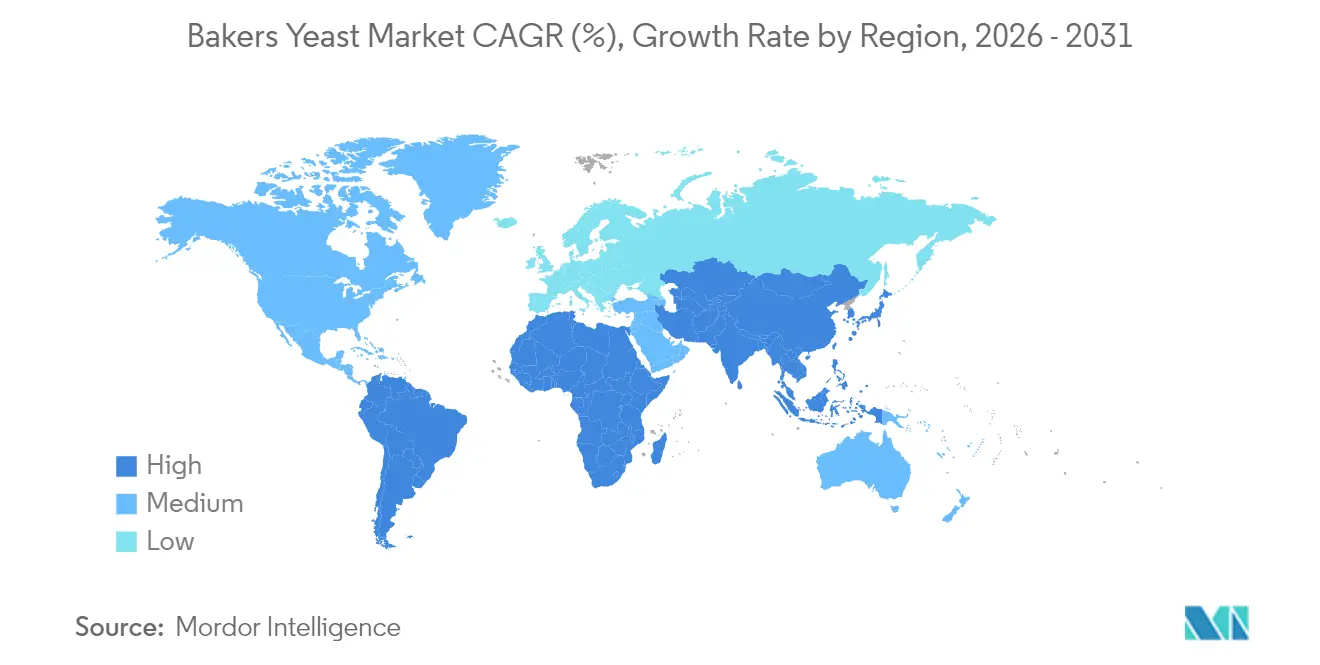

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bakers Yeast Market Analysis by Mordor Intelligence

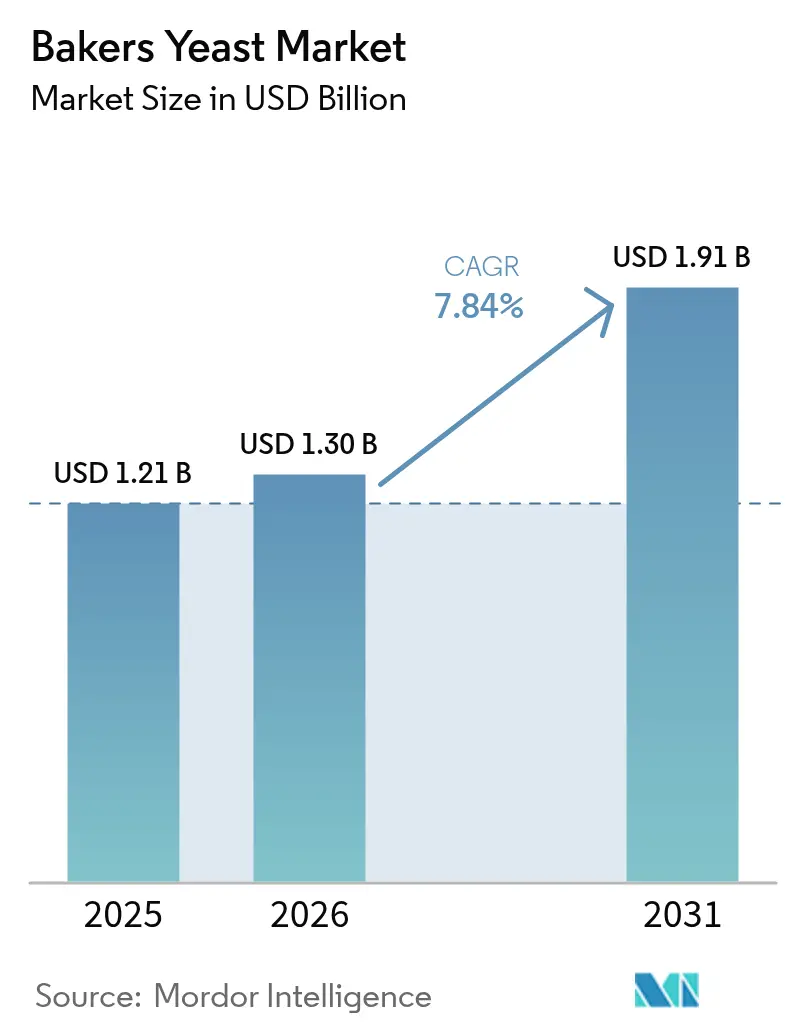

The baker's yeast market size in 2026 is estimated at USD 1.3 billion, growing from 2025 value of USD 1.21 billion with 2031 projections showing USD 1.91 billion, growing at 7.84% CAGR over 2026-2031. Growth momentum stems from the premiumization of everyday bread, quick-service restaurant expansion, and the rapid scale-up of precision-fermentation platforms that widen yeast functionality beyond leavening. Europe preserves leadership through deep artisan traditions and clean-label regulations, while Asia-Pacific contributes the largest incremental volume thanks to rising disposable incomes and urban lifestyles. Fresh/compressed formats remain the workhorse of industrial lines, yet liquid and cream variants gain favour as bakeries automate dosing and cold-chain logistics improve. Engineered Saccharomyces strains that deliver higher yields of vitamins, proteins, and bioactives are moving from pilot to commercial batches, opening new revenue streams for incumbents and start-ups. Overall, the baker's yeast market continues to show resilience despite volatile molasses prices because bakers see yeast as a cost-effective path to clean labels, flavour complexity, and reliable dough performance

Key Report Takeaways

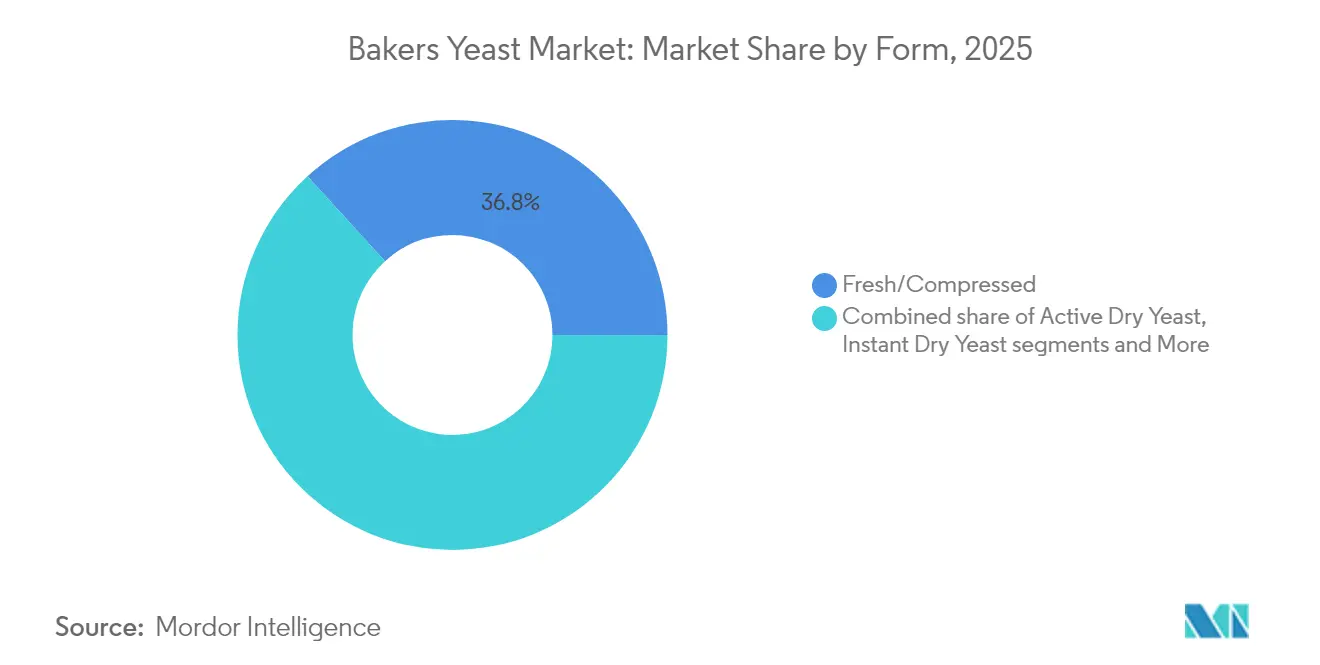

- By form, fresh/compressed yeast led with 36.78% revenue share in 2025, while liquid/cream is projected to post the fastest 8.55% CAGR to 2031.

- By yeast type, Saccharomyces cerevisiae dominated, with 76.22% of the baker's yeast market share in 2025; genetically edited strains are set to expand at a 9.05% CAGR through 2031.

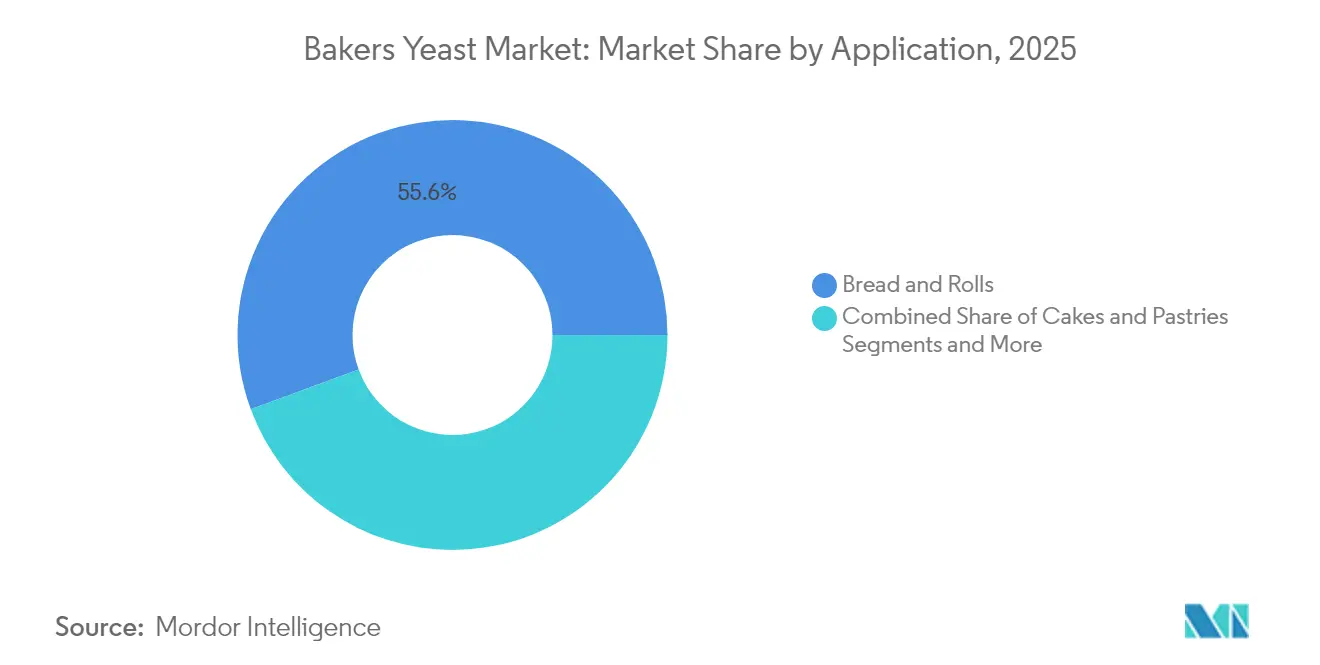

- By application, bread and rolls captured 55.62% of the baker's yeast market size in 2025; pizza and flatbread applications are rising at a 6.12% CAGR.

- By category, conventional products held a 74.68% share in 2025, whereas organic yeast is forecast to grow at 9.98% CAGR to 2031.

- By geography, Europe accounted for 30.84% revenue in 2025; Asia-Pacific is the fastest-growing region with an 8.43% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bakers Yeast Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for packaged and convenience bakery products | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in clean-label artisan and specialty bread consumption | +1.8% | Europe and North America core, expanding to urban centers in Asia-Pacific | Long term (≥ 4 years) |

| Expansion of retail bakery chains in emerging economies | +1.5% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Advancements in precision fermentation for high-performance yeast strains | +1.1% | Global, led by North America and Europe, research and development centers | Long term (≥ 4 years) |

| Fortified baker's yeast positioned as functional ingredient | +0.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Use of bio-ethanol molasses byproducts to reduce yeast production costs | +0.7% | Global, particularly in sugar-producing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for packaged and convenience bakery products

Packaged bread, buns, and snack pastries are gaining shelf space as consumers seek long-lasting baked goods requiring minimal preparation. The convenience and extended shelf life of these products align with modern lifestyle demands. In the United States, premium bread products that depend on consistent yeast functionality are experiencing increased demand, driven by consumer preferences for artisanal quality in packaged formats. While in Asia-Pacific countries such as Indonesia, India, and Vietnam, modern retail formats and e-commerce increase access to branded baked products, particularly in urban areas with rising disposable incomes. Automated production lines with inline quality sensors require yeast strains that can withstand wider temperature variations and minimize proofing inconsistencies, ensuring consistent product quality across large-scale manufacturing. The growing convenience segment continues to drive demand for performance-optimized yeast, supporting sustained growth in the baker's yeast market, as manufacturers focus on product innovation and process optimization.

Growth in clean-label artisan and specialty bread consumption

Consumers increasingly examine ingredient lists for familiar components, making artisanal breads produced through extended fermentation processes more desirable for health-conscious consumers. The extended fermentation periods, typically lasting between 12 to 24 hours, create complex flavors and demonstrate improved digestibility in research studies, enabling premium bakeries to command higher prices. Research from CBI, the Ministry of Foreign Affairs, highlights this trend, projecting that clean-label products will rise from constituting 52% of portfolios in 2021 to over 70% in 2025[1]Source: CBI, Ministry of Foreign Affairs, "Which trends offer opportunities or pose a threat on the European natural food additives market?", cbi.eu.Major companies like Bimbo Bakeries USA and Flowers Foods are developing organic products and seasonal items that highlight natural fermentation methods, incorporating traditional techniques such as sourdough starters and long proofing times. Research facilities such as the Sourdough Institute in Belgium provide bakers with extensive wild-yeast collections that expand flavor possibilities while meeting allergen-free requirements. The institute maintains over 100 unique yeast strains, each offering distinct flavor profiles. This trend drives specialized demand in the baker's yeast market for strains that enhance bread aroma while maintaining simple ingredient declarations, particularly in European and North American markets where clean-label products are increasingly popular.

Expansion of retail bakery chains in emerging economies

The growth of café-bakery franchises across Southeast Asia, the Middle East, and Africa has generated consistent demand cycles, benefiting suppliers with robust logistics and technical support capabilities. These franchises need reliable, high-quality yeast supplies for their operations across diverse locations, including urban centers and suburban areas. Government initiatives support domestic yeast production to lower import expenses and improve food security, especially in regions that rely heavily on imported raw materials. Yeast manufacturers have positioned micro-facilities near sugar mills to reduce molasses transportation costs and enhance production efficiency. They have also developed liquid yeast products adapted to warm climates, using temperature-resistant strains and stabilizers. The liquid format provides improved stability and performance in tropical environments, addressing the requirements of regional bakeries and industrial food processors. Singapore's investment in precision-fermentation research demonstrates the region's commitment to local production of specialized yeast strains. This research emphasizes developing strains suited to local ingredients and climate conditions, driving demand and advancing technological capabilities in the regional yeast industry.

Advancements in precision fermentation for high-performance yeast strains

CRISPR technology enables scientists to modify Saccharomyces genomes to increase the production of vitamins, proteins, and complex flavors through targeted genetic modifications. The precision-fermentation market creates new opportunities for established yeast manufacturers by expanding their product portfolios and technological capabilities. Companies are developing specialized yeasts that produce complete amino acid profiles for sports nutrition products and dairy alternatives, meeting the growing demand for plant-based ingredients. For instance, Phytolon utilizes modified baker's yeast to create natural food colorants through biosynthetic pathways, which await FDA approval. As global food companies commit to reducing carbon emissions in their operations, fermentation technology provides a viable and sustainable pathway for producing animal-free proteins, attracting both venture capital investments and strategic corporate partnerships. The increasing regulatory approvals in this space position the baker's yeast market to generate substantial revenue through royalties, technology licensing agreements, and specialized fermentation contracts.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatile sugar/molasses feedstock prices and availability | -1.4% | Global, particularly acute in sugar-producing regions | Short term (≤ 2 years) |

| Stringent global food-safety and labelling regulations | -0.8% | Global, with varying intensity across regulatory jurisdictions | Medium term (2-4 years) |

| Growing use of chemical leavening agents in rapid-bake products | -1.1% | Global, strongest in cost-sensitive mass production segments | Medium term (2-4 years) |

| Freight and logistics volatility affecting yeast supply and viability | -0.6% | Global, with particular impact on fresh yeast segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile sugar/molasses feedstock prices and availability

Molasses prices fluctuate based on sugarcane harvest yields, ethanol demand, and weather patterns, including El Niño events. The price volatility is particularly pronounced during adverse weather conditions that affect sugarcane cultivation regions and when ethanol production competes for available molasses supply. As yeast production relies on clarified molasses as the primary carbon source, increased input costs directly impact profit margins across the production chain. Small-scale producers, limited by storage capacity and financial constraints, cannot effectively hedge against price fluctuations and must purchase at spot market rates, significantly affecting their competitive position in the market. While some companies investigate lignocellulosic sugars derived from agricultural waste as an alternative, technical challenges in processing, high conversion costs, and potential flavor effects have limited widespread adoption. The baker's yeast market growth may remain constrained unless manufacturers secure long-term supply agreements with reliable molasses suppliers or develop commercially viable alternative raw materials that maintain product quality and consistency.

Stringent global food-safety and labeling regulations

Regulatory bodies enforce increasingly strict microbial specifications and safety standards while closely monitoring genetically modified organisms in food production. In the United States, 21 CFR Parts 170-186 establish comprehensive limits on viable counts, heavy metals, and allergen disclosures, substantially increasing compliance and testing costs[2]Source: US Food and Drug Administration, “21 CFR Parts 170-186 Food Ingredients,” fda.gov. The European Food Safety Authority (EFSA) mandates detailed biannual dossier updates under the Qualified Presumption of Safety list, significantly extending the time-to-market for new strains and product innovations. Organic certification bodies require commercial bakers to use organic yeast when available in the market, restricting supply chain options during shortage periods and production constraints[3]Source: OMRI, “Organic Yeast Usage Guidelines,” omri.org.These complex regulatory requirements create substantial market entry barriers for small companies and delay product innovation cycles, moderately constraining the overall baker's yeast market growth and development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Fresh Retains Leadership while Liquid Gains Momentum

Fresh/compressed yeast accounted for 36.78% of the baker's yeast market share in 2025, maintaining its position as the highest revenue generator. This dominance stems from its rapid activation properties and consistent fermentation performance in industrial baking operations. The format remains particularly important for bakeries producing laminated dough and high-sugar products, where controlled gas formation is essential for product quality. However, the format faces challenges from cold-chain requirements in warm regions and increasing energy costs associated with refrigerated storage and transport.

Liquid and cream yeast formats are experiencing growth at 8.55% CAGR, driven by their compatibility with automated dosing systems that reduce manual handling and lower contamination risks. This growth is particularly notable in large-scale bread manufacturing facilities in Japan and the United States. The integration of digital monitoring systems in modern bakeries supports this transition, as sensors monitor fermentation times and enable precise recipe adjustments to optimize production efficiency. Active dry and instant yeast maintain their presence in retail and food service segments, while nutritional yeast occupies a growing niche in plant-based food products. These various yeast formats reflect the market's adaptation to increasing automation and changing consumer preferences.

By Yeast Type: Genetic Engineering Reshapes Traditions

Saccharomyces cerevisiae maintains its dominant position in commercial bread production, holding a 76.22% market share in 2025. This dominance stems from its proven performance and widespread regulatory approval. The availability of its complete genome sequence enables efficient strain optimization, ensuring its continued market significance. Genetically modified variants are experiencing a 9.05% CAGR, driven by bakery industry demands for improved stress tolerance and specific flavor profiles. CRISPR technology modifications reduce unwanted flavors and enhance trehalose production, resulting in better freeze-thaw stability for frozen dough transportation.

Alternative yeast varieties are gaining market presence. Candida milleri provides distinctive sour characteristics in European rye bread production, while Kluyveromyces marxianus operates effectively at elevated temperatures, reducing energy consumption in tropical facilities. Selenium-fortified yeast is increasing in popularity as a functional component in health-focused bread products. Despite lower production volumes, these specialty yeasts enhance the baker's yeast market value proposition and create additional revenue opportunities beyond traditional white bread production.

By Application: Pizza and Flatbreads Spur Diversification

Rolls and bread market maintain their dominance, representing 55.62% of the baker's yeast market size in 2025. Diversifying into pizza, pita, and naan products drives the market expansion. The growth in quick-service pizza restaurants across China and Latin America, particularly targeting younger consumers through delivery services, requires yeast products that ensure consistent dough performance. Consequently, the pizza and flatbread segment is projected to grow at a 6.12% CAGR, exceeding traditional bread categories. The cakes, pastries, and enriched sweet goods segment maintains stable growth, particularly in markets where gifting traditions emphasize the importance of texture quality through controlled fermentation processes.

The market is further strengthened by functional bakery products. The production of Vitamin D2-fortified doughs using ultraviolet-treated yeast addresses consumer demand for immunity-enhancing products, while high-protein breads incorporate fermentation-derived yeast concentrates to enhance amino acid content. The increasing popularity of special occasion and ethnic celebration products, which often require specialized dough formulations, creates demand for yeast variants capable of performing in high-sugar and high-fat environments. These diverse applications contribute to sustained growth in the baker's yeast market.

By Category: Organic and Non-GMO Gain Premium Shelf Space

Conventional yeast dominates with a 74.68% share in 2025, thanks to cost efficiency and wide availability. Still, organic yeast posts the highest 9.98% CAGR because health-conscious consumers are willing to pay premiums for certified inputs. Supermarket analytics in the United States show visible organic badges driving a price differential of 15-20% per loaf, with minimal volume trade-offs. Non-GMO labels hold middle ground, appealing to shoppers wary of genetic modification but mindful of budgets.

Fortified yeast categories grow as bakery formulators chase nutrition claims. Selenium-fortified options, backed by peer-reviewed bioavailability trials, find slots in multigrain loaves marketed to seniors. Natural food colour producers use engineered baker’s yeast to insert beta-carotene and beet-red hues, a sign that category boundaries blur. Collectively, these shifts confirm that the baker's yeast market now balances mass-production economics with niche premiumisation, offering multiple price points across retail and food service.

Geography Analysis

Europe accounts for 30.84% of revenue in 2025, supported by its established artisan culture, strict clean-label regulations, and extensive network of craft bakeries that utilize natural fermentation processes. Germany leads the region in volume consumption, while France generates higher average selling prices through premium sourdough products. Eastern European markets, particularly Poland, show above-average growth as modern supermarkets replace traditional corner stores. European Union regulations limiting additives maintain demand for yeast over chemical leaveners, supporting stable sales in this mature market.

The Asia-Pacific region exhibits the highest growth rate at 8.43% CAGR, driven by Indonesia's expanding domestic chains and Japanese-style bakeries. Singapore's USD 14.8 million investment in precision-fermentation demonstrates its commitment to local ingredient production and supply chain resilience. China maintains the largest yeast production capacity, while India's consumption increases due to urbanization and café culture growth. Australia, despite its smaller market size, maintains demand for specialized yeast products in gluten-free and organic segments. These regional developments support market growth despite raw material price fluctuations.

North America maintains steady single-digit growth as established manufacturers focus on cost optimization and functional bread products. The United States market emphasizes innovation in low-carb and protein-enhanced breads, increasing demand for specialized yeast formulations. South America leverages its sugarcane industry advantages, particularly in Brazil where integrated facilities reduce molasses transportation costs. The Middle East and Africa region experiences growth in bakery franchises, though limited cold-chain infrastructure restricts fresh yeast distribution. However, improvements in port logistics and free-trade zones enhance supply chain reliability, creating new market opportunities for yeast manufacturers.

Competitive Landscape

The bakers yeast market is moderately concentrated, with the top five suppliers holding substantial market share while allowing space for niche players. Prominent players in the market incldues Lesaffre International, Associated British Foods Plc, Lallemand Inc., Pak Group, and Angel Yeast Co. Ltd. dominate global operations through their multi-continent manufacturing facilities and extensive technical service networks. Lesaffre strengthened its position through a 70% acquisition of Biorigin and the purchase of DSM-Firmenich's yeast extract operations in June 2024, expanding its fermentation capacity and enhancing its savory ingredient portfolio. Angel Yeast focuses on protein extraction research and development to expand into alternative-protein markets.

Digital technology adoption creates competitive advantages in the market. Manufacturers implement AI algorithms to optimize feedstock combinations and minimize off-spec production, reducing production costs. Renaissance BioScience develops non-GMO yeast strains for masking off-flavors in plant-based meat products, securing co-manufacturing agreements with major ingredient companies. Regulatory compliance influences market position, as companies that obtain GRAS certifications for new strains or EFSA QPS approvals gain early market access in health-focused applications. While price competition remains strong in commodity segments, premium product lines rely on specialized strain collections and application expertise. The baker's yeast market leadership depends primarily on innovation capabilities and supply chain reliability.

Lesaffre International offers an organic range of baker's yeast that provides optimum performance in the long term. This gives the company a competitive advantage in the international market, particularly in Europe. Companies in the global baker's yeast market primarily focus on expansion strategies, continuously increasing their production capacity and distribution networks.

Bakers Yeast Industry Leaders

-

Associated British Foods PLC

-

Lesaffre International

-

Lallemand Inc.

-

Pak Group (Pakmaya)

-

AngelYeast Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Angel Yeast introduced Feravor, a natural flavor solution for clean-label baking, at IBA 2025 in Europe and the China Bakery Exhibition in Asia. The Feravor™ series includes Floral-Fruity and Butter variants, providing bakers with natural flavor-enhancing ingredients that align with clean-label requirements.

- October 2024: Lesaffre has acquired a 70% stake in Biorigin, bolstering its portfolio of natural flavor ingredients. This alliance melds Lesaffre's fermentation prowess, through its Biospringer unit, with Biorigin's expertise in yeast-based ingredients derived from sugarcane processing.

- September 2024: Revyve introduced a gluten-free egg replacer made from baker's yeast. The ingredient provides texturizing properties while maintaining neutral flavor and color. It addresses the increasing demand for clean-label, sustainable egg alternatives in gluten-free products.

- February 2024: Renaissance BioScience received a CAD 232,000 grant to develop non-GMO yeast solutions that neutralize off-flavors and aromas in plant-based protein products. The funding supports the development of clean-label, non-GMO yeast technology to eliminate undesirable tastes and smells in plant-based proteins.

Global Bakers Yeast Market Report Scope

Baker's yeast is the common name for the strains of yeast commonly used in baking bread and other bakery products. The scope of the report gives market data on sales of baker's yeast in various forms across the globe. The baker's yeast is present in four forms which include Compressed/ Solid Yeast, Liquid/Cream Yeast, Dry or Powdered Bakers Yeast and other forms across the globe. The market is studied in terms of its growth for different regions which includes North America, Europe, Asia-Pacific and Rest of world. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Liquid/Cream Yeast |

| Fresh/Compressed Yeast |

| Active Dry Yeast |

| Instant Dry Yeast |

| Nutritional Yeast/Specialty Forms |

| Saccharomyces cerevisiae |

| Candida milleri and related |

| High-selenium strains |

| Genetically-edited strains |

| Bread and Rolls |

| Cakes and Pastries |

| Pizza Dough and Flatbreads |

| Other Baked Goods |

| Conventional |

| Organic Certified |

| Non-GMO |

| Fortified/Functional |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Liquid/Cream Yeast | |

| Fresh/Compressed Yeast | ||

| Active Dry Yeast | ||

| Instant Dry Yeast | ||

| Nutritional Yeast/Specialty Forms | ||

| By Yeast Type | Saccharomyces cerevisiae | |

| Candida milleri and related | ||

| High-selenium strains | ||

| Genetically-edited strains | ||

| By Application | Bread and Rolls | |

| Cakes and Pastries | ||

| Pizza Dough and Flatbreads | ||

| Other Baked Goods | ||

| By Category | Conventional | |

| Organic Certified | ||

| Non-GMO | ||

| Fortified/Functional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the baker's yeast market?

The baker's yeast market is valued at USD 1.3 billion in 2026 and is projected to reach USD 1.91 billion by 2031.

Which region leads the baker's yeast market?

Europe leads with 30.84% revenue share in 2025, driven by strong artisan traditions and clean-label regulations.

What segment shows the fastest growth?

Liquid and cream yeast formats record the fastest 8.55% CAGR as automated bakery lines adopt pumpable solutions.

What is the forecast CAGR for the baker's yeast market?

The market is expected to expand at an 7.84% CAGR between 2026 and 2031, supported by convenience trends and clean-label demand.

Page last updated on: