Specialty Yeast Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.92 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

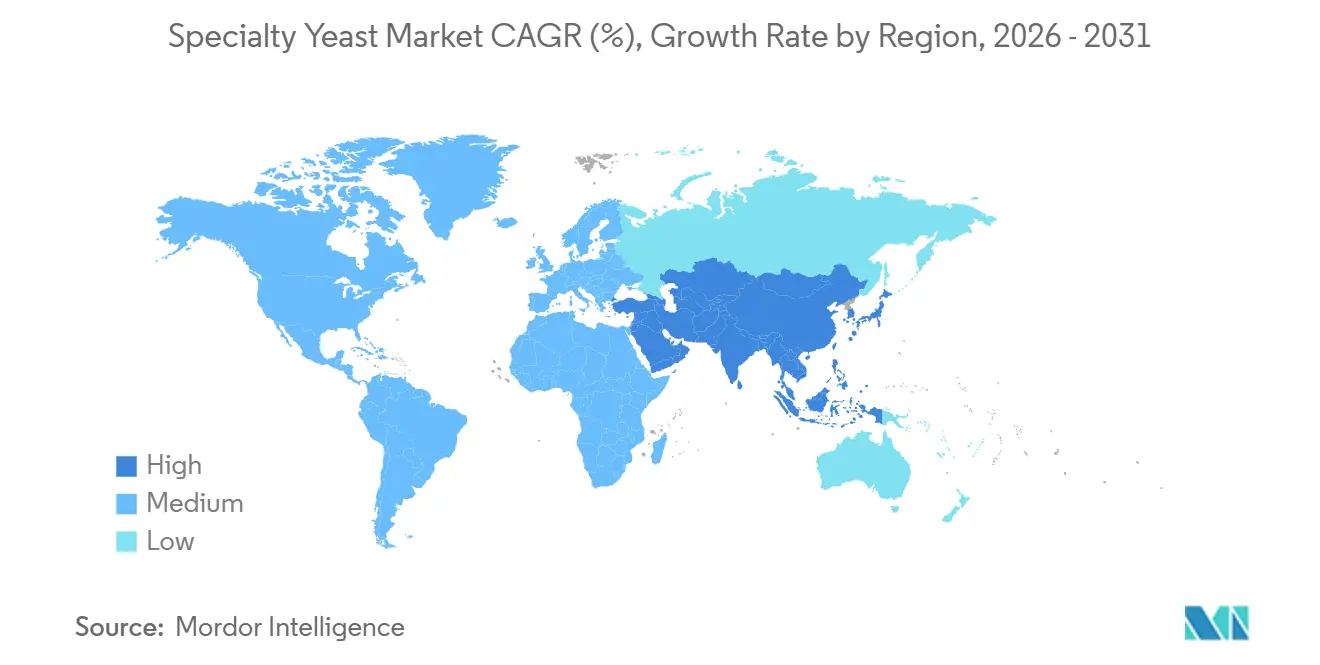

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Yeast Market Analysis by Mordor Intelligence

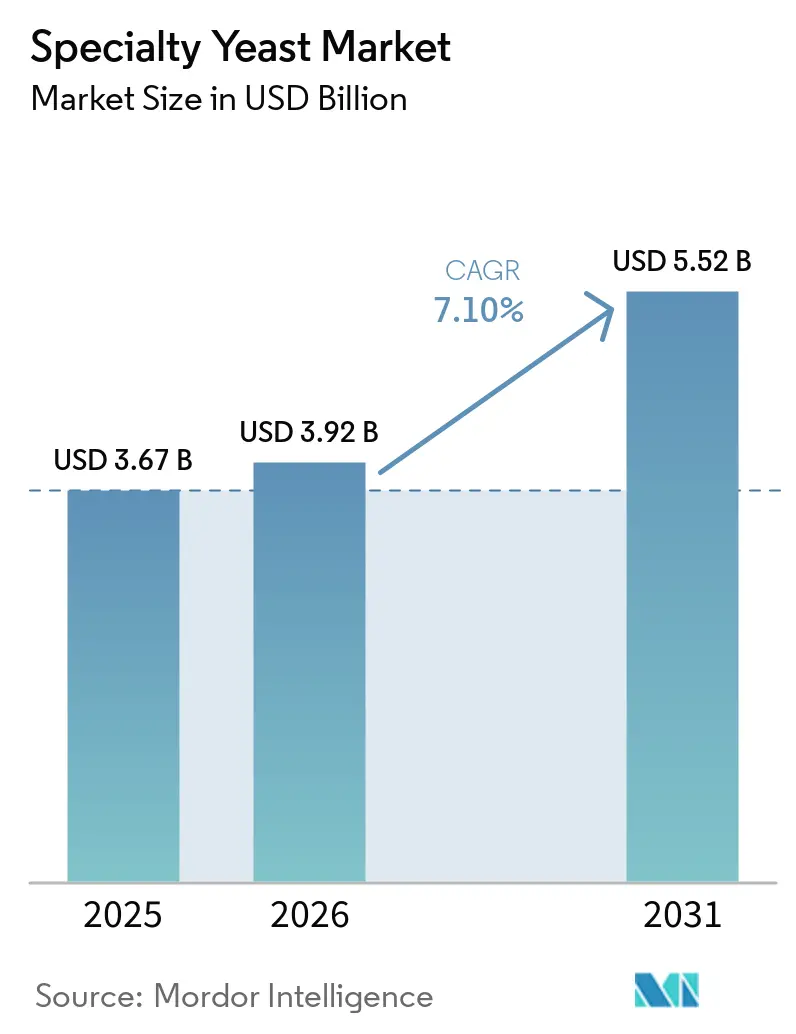

The specialty yeast market size is expected to grow from USD 3.67 billion in 2025 to USD 3.92 billion in 2026 and is forecast to reach USD 5.52 billion by 2031 at 7.10% CAGR over 2026-2031. This growth trajectory demonstrates the market's robust response to shifting consumer preferences, particularly the increasing emphasis on natural, clean-label ingredients and functional food products that deliver enhanced nutritional benefits. The market's expansion is propelled by consumers' growing awareness of health and wellness, coupled with the food industry's commitment to developing innovative, natural solutions. Technological advancements in fermentation processes and genetic engineering capabilities have become instrumental in meeting these evolving demands. A prime example is DTU Biosustain's development of TUNEYALI, an advanced toolkit that enables manufacturers to optimize yeast strains more effectively for diverse industrial biotechnology applications. This innovation has significantly improved production efficiency, product quality, and the ability to meet specific consumer requirements across various food and beverage segments.

Key Report Takeaways

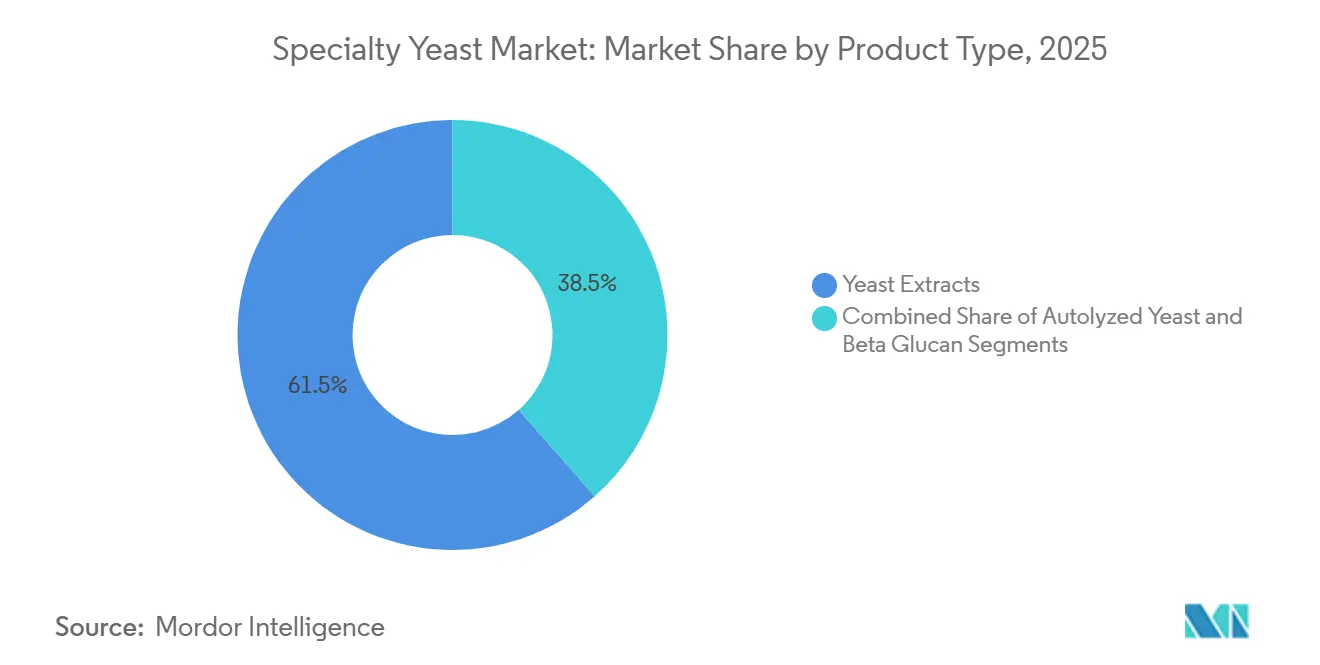

- By product type, yeast extracts held 61.51% share of the specialty yeast market in 2026, whereas beta-glucans are set to grow fastest at 8.23% CAGR through 2031.

- By species, Saccharomyces cerevisiae accounted for 33.21% of the specialty yeast market share in 2025, while Pichia pastoris is projected to advance at an 8.20% CAGR to 2031.

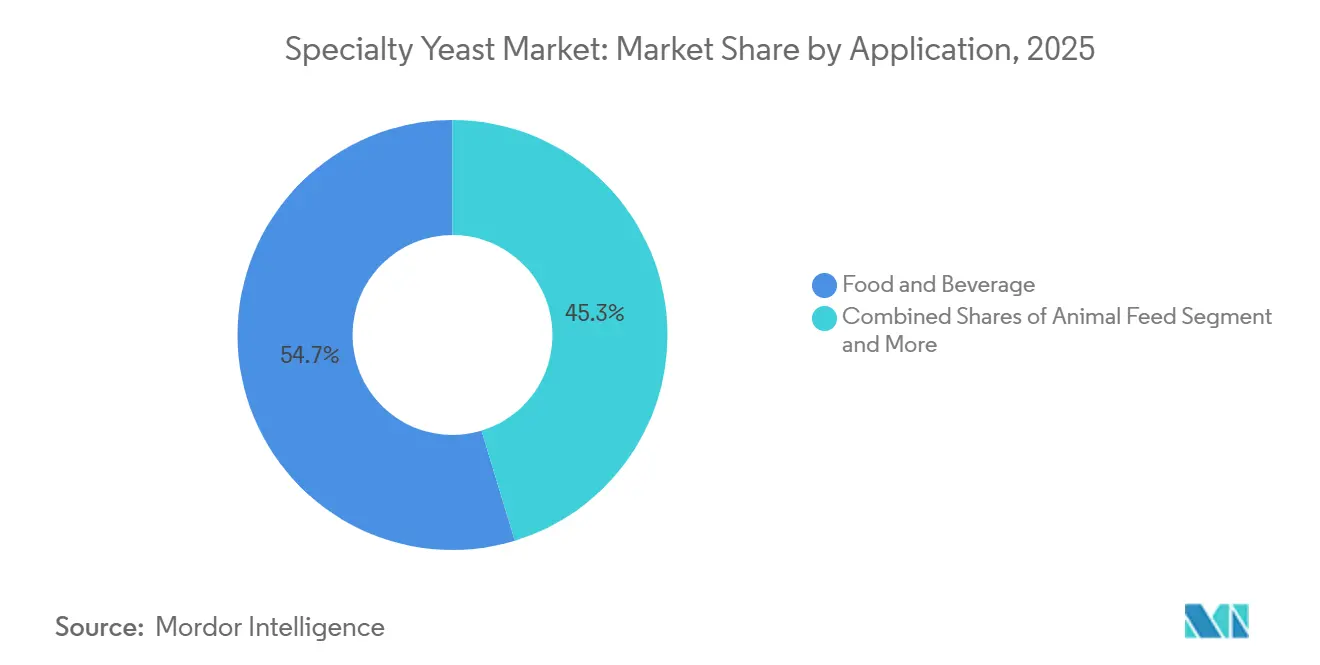

- By application, food and beverage captured 54.7% of the specialty yeast market size in 2025; the nutraceuticals and pharmaceuticals segment is forecast to expand at 8.02% CAGR between 2026 and 2031.

- By geography, Europe led with 33.86% revenue share in 2025, and the Asia–Pacific is poised for the quickest growth at 7.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Specialty Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label and natural ingredient demand | +1.8% | North America, Europe | Medium term (2-4 years) |

| Functional benefits of specialty yeasts | +1.5% | Asia–Pacific, Global | Long term (≥4 years) |

| Expansion in bakery and brewing | +1.2% | Europe, North America | Short term (≤2 years) |

| Rise in gluten-free and allergen-free foods | +1.0% | North America, Europe, Asia–Pacific | Medium term (2-4 years) |

| Animal-nutrition usage | +0.9% | Asia–Pacific, Global | Long term (≥4 years) |

| Fermentation-efficiency improvements | +0.7% | North America, Europe, Global technology hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Clean-label and natural ingredient demand

The increasing consumer awareness and demand for transparent and authentic ingredients are fundamentally transforming the food industry, particularly driving the adoption of specialty yeast as manufacturers actively transition away from synthetic additives. Ingredion's significant 20-year track record in clean-label innovation demonstrates how these natural ingredients enhance product quality while optimizing production costs and improving nutritional profiles. The practical applications of specialty yeast have expanded beyond traditional food categories, with companies investing in research and development to create yeast-based alternatives that successfully maintain product taste and texture characteristics. The market shows sustained momentum as consumers consistently choose GMO-free and additive-free products across various food segments. This industry transformation necessitates substantial improvements in food processing methods and ingredient sourcing practices to ensure safety compliance while upholding clean-label standards. Food manufacturers now face the complex task of balancing evolving consumer preferences with strict regulatory requirements and production efficiency goals.

Functional Benefits of Specialty Yeasts

Beta-glucans extracted from yeast demonstrate significant immune system benefits and play a valuable role in cancer treatment protocols. These compounds help strengthen the body's natural defense mechanisms against tumors while helping patients better manage the side effects of chemotherapy treatments. Saccharomyces cerevisiae yeast serves as an excellent source of essential nutrients, providing high-quality proteins, vital vitamins, and beneficial bioactive compounds. Additionally, this yeast naturally concentrates important trace minerals like selenium and zinc, which further increase its nutritional benefits. In the growing field of probiotics, Saccharomyces boulardii has proven particularly effective in supporting digestive health and strengthening immune system function. Manufacturers focus on optimizing production through high-density cell cultivation methods to ensure cost-effective manufacturing processes. Given these comprehensive health advantages, specialty yeasts have become crucial components in nutraceutical products designed to deliver specific health benefits to consumers.

Expansion in bakery and brewing

Specialty yeast applications in traditional fermentation industries have significantly evolved beyond their conventional leavening roles. Red Star Yeast's enhanced Platinum Yeast formulation incorporates advanced dough improvers that substantially boost gluten strength and volume, while its specialized enzymes effectively combat staling, resulting in products that maintain freshness for longer periods. In premium wine production, carefully selected Saccharomyces cerevisiae strains play a crucial role in enhancing complex flavor profiles and improving fermentation efficiency, particularly in the growing low-alcohol wine segment. The industry's increasing commitment to sustainability has generated substantial demand for specialized yeast strains specifically engineered for efficient lignocellulosic biomass utilization, delivering both improved production efficiency and enhanced environmental performance. These technological advancements have firmly established specialty yeasts as fundamental components in advancing traditional fermentation processes.

Rise in gluten-free and allergen-free foods

The growth of the gluten-free market has increased demand for specialty yeasts that improve texture and nutritional content in alternative grain products. These yeasts provide essential proteins that enhance structure and mouthfeel while delivering necessary amino acids. Torula yeast has emerged as an efficient protein source with minimal environmental impact, as demonstrated in vegan spreads containing 14.7% protein content in 'Leberwurst'-style products. Regional variations in consumer preferences affect product development, with German consumers demanding higher transparency compared to Nordic markets. The market benefits from yeast's natural hypoallergenic qualities and its ability to increase nutritional value without adding common allergens. The efficient production process and sustainability benefits make specialty yeasts valuable ingredients for allergen-free products that meet various dietary needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -1.4% | Global, with Europe and North America having strictest requirements | Short term (≤ 2 years) |

| Cost and complexity of achieving certifications | -1.1% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Variability in product quality and standardization | -0.8% | Global, with particular challenges in Asia-Pacific | Medium term (2-4 years) |

| Shelf-life or stability issues with some high-functionality yeast products | -0.6% | Global, with temperature-sensitive markets most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent food safety and labeling regulations

Regulatory oversight of yeast-based ingredients continues to expand globally. The European Food Safety Authority (EFSA) conducts thorough safety evaluations for genetically modified strains, including Komagataella phaffii used in soy leghemoglobin production [1]Source: European Food Safety Authority, “Safety of soy leghemoglobin from genetically modified Komagataella phaffii,” efsa.europa.eu. In the United States, the FDA's GRAS Notice system requires detailed documentation for new yeast strains, as demonstrated by the Bacillus subtilis NRRL 68053 approval process, which included comprehensive safety assessments and antibiotic resistance gene analysis [2]Source: U.S. Food and Drug Administration, “GRAS Notice 1143, Bacillus subtilis NRRL 68053,” fda.gov. China's new food additive standard GB 2760-2024, taking effect in February 2025, expands the Positive List of approved additives and revises regulations for preservatives and processing aids, affecting yeast product approvals. EFSA's Qualified Presumption of Safety (QPS) process updates occur approximately every six months, creating continuous compliance requirements for manufacturers. While these regulatory frameworks ensure product safety, they extend development timelines and increase costs, particularly impacting smaller companies that lack regulatory expertise.

Cost and complexity of achieving certifications

The certification process for specialty yeast products navigates through a complex web of regulatory requirements. Companies developing precision fermentation products must undergo comprehensive novel food assessments in accordance with EU Regulation 2015/2283. For genetically modified strains, manufacturers face rigorous requirements to prove production strain safety, ensure final product purity, and provide evidence that products are free from viable cells or DNA contamination. In the organic segment, the USDA's 2024 Limited Scope Technical Report implements strict guidelines, requiring manufacturers to use organic yeast in human consumption products unless organic alternatives are not commercially available [3]Source: USDA AMS National Organic Program, “2024 Limited Scope Technical Report – Enzymes, Microorganisms, and Yeast,” usda.gov. The fragmented international regulatory landscape requires companies to obtain individual approvals in each major market, resulting in substantial compliance costs. These extensive regulatory requirements present significant market entry challenges, particularly impacting smaller companies and startups developing innovative yeast applications, which ultimately constrains competitive growth in emerging market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Extracts Lead While Beta-Glucans Accelerate

The market shows a clear preference for yeast extracts, which account for 61.51% of the market share in 2025. This dominance stems from their essential role in enhancing savory food products and meeting the growing demand for clean-label ingredients that can replace artificial flavor enhancers. The recent acquisition of DSM-Firmenich's yeast extract business by Lesaffre in October 2024 has created a more robust global supply chain and manufacturing infrastructure. Meanwhile, autolyzed yeast maintains its position in the market, particularly in processed food applications where it continues to provide both flavor enhancement and nutritional benefits.

The beta-glucans segment is experiencing remarkable growth, with projections showing an 8.23% CAGR from 2026 to 2031. This growth is backed by substantial clinical research demonstrating their value in cancer therapies and immune system support. The segment's expansion is further supported by scientific evidence showing that beta-glucans derived from yeast offer superior biological activity compared to other sources. As consumers become more health-conscious and seek functional ingredients, beta-glucans have established themselves as valuable components in both nutritional supplements and pharmaceutical products. The development of advanced fermentation techniques has improved production efficiency and product quality, making beta-glucans more accessible for various commercial uses.

By Species: Saccharomyces Dominates While Pichia Innovates

The yeast market demonstrates clear leadership from Saccharomyces cerevisiae, which commands a 33.21% market share in 2025. This dominance stems from its Generally Recognized as Safe (GRAS) status and widespread regulatory acceptance globally. The organism's versatility extends beyond traditional baking and brewing applications, as engineered variants now produce specialized compounds like resveratrol at 34.22 mg/L in rice wine production. In the biotechnology sector, S. cerevisiae has established itself as a reliable platform for manufacturing therapeutic proteins and industrial enzymes.

The market also sees significant contributions from other yeast species. Kluyveromyces marxianus has carved out valuable positions in lactose processing and specialized fermentation, particularly in dairy-related applications where its unique lactose-fermenting capabilities offer substantial benefits. Meanwhile, Pichia pastoris (Komagataella phaffii) is experiencing robust growth at 8.20% CAGR (2026-2031), driven by advancements in genetic engineering and expanding pharmaceutical applications. The development of OPENPichia has made high-performance protein production more accessible through its license-free strain and modular expression toolkit. The integration of CRISPR/Cas9 technology has further enhanced production capabilities, enabling efficient manufacturing of recombinant proteins, including U.S.-approved food ingredients.

By Application: Food Sector Leads While Nutraceuticals Surge

The Food and Beverage segment currently leads the market with a 54.7% share in 2025, as companies increasingly incorporate yeast products into clean-label formulations and functional food development. This trend is evident in ADM's recent focus on health-conscious beverages, responding to consumer demand as 45% of buyers actively seek products that combine health benefits with convenience. In the Animal Feed sector, farmers and producers are seeing positive results with Saccharomyces cerevisiae fermentation products, which help livestock better manage production stress while improving feed efficiency and reducing illness rates.

The Cosmetics and Personal Care industry is witnessing a shift toward yeast-derived biosurfactants, with Mannosylerythritol lipids emerging as natural alternatives to traditional synthetic ingredients. The Nutraceuticals and Pharmaceuticals segment shows strong potential with an expected growth rate of 8.02% CAGR from 2026 to 2031, as companies invest in precision fermentation technologies to produce pharmaceutical-grade bioactive compounds. The probiotic market continues to evolve beyond traditional applications, with manufacturers achieving significant progress in Saccharomyces boulardii production, reaching concentrations of 1.46 × 10^8 CFU/mL in high-density production systems.

Geography Analysis

The European market currently dominates the global landscape with a substantial 33.86% share in 2025. This leadership position stems from the region's well-structured regulatory frameworks that actively encourage companies to develop compliant yeast solutions. European food safety standards, particularly EFSA's evaluation processes, maintain high product quality while effectively limiting market entry. In Germany, the emphasis on transparent food value chains influences how companies develop their products, as consumers demand more detailed information compared to their Nordic counterparts. The region's strong fermentation industry and research institutions provide significant advantages in yeast biotechnology development. While Brexit has introduced new compliance requirements, these changes may ultimately simplify market access for innovative products.

The Asia-Pacific region is experiencing remarkable growth, with a projected CAGR of 7.99% from 2026 to 2031. This growth is primarily driven by the expansion of food processing industries and heightened consumer interest in functional ingredients. In China, the implementation of food additive standard GB 2760-2024 in February 2025 will open new opportunities for specialty yeast applications while maintaining safety standards. South Korea is reducing its import dependence by developing local microbial resources, including native Saccharomyces cerevisiae strains for fermentation. Meanwhile, Japan is investing in precision fermentation for sustainability, and India's expanding nutraceutical sector is creating new opportunities for functional yeast ingredients. Despite the complex regulatory environment, the region's urbanization and rising consumer incomes present significant market opportunities.

North American markets continue to show consistent growth, with the United States benefiting from its robust biotechnology infrastructure and favorable regulations for precision fermentation products. The FDA's GRAS notification system provides clear pathways for new yeast applications, while USDA organic certification creates opportunities in premium markets. Canada's alignment with U.S. standards facilitates smooth trade operations, and Mexico's growing food processing sector is increasing the demand for specialty yeast products.

Competitive Landscape

The specialty yeast market shows a balanced mix of established companies and new players competing for market share. The industry experienced significant changes in 2024, with Lesaffre taking a 70% ownership in Biorigin and DSM-Firmenich completing its yeast extract business sale. The creation of Novonesis, through the combination of Novozymes and Chr. Hansen has brought a new EUR 3.7 billion revenue company into the market, changing how businesses compete in the enzyme and fermentation segments. These business moves demonstrate how companies are working to strengthen their supply chains and expand into new regions.

Companies are setting themselves apart by developing better technology, putting money into advanced fermentation methods, and using genetic tools to create their own unique yeast strains. The release of free-to-use platforms like OPENPichia has made it easier for more companies to produce advanced proteins, which challenges the traditional way bigger companies controlled these processes. New business opportunities are opening up in special areas like cosmetic ingredients and medical proteins, where understanding regulations and having technical knowledge give companies a competitive edge in the market.

While new companies are using modern biology techniques to find innovative ways to use yeast, bigger companies maintain their positions through their size advantages and regulatory expertise. These established players focus on large-scale production capabilities and their ability to meet complex regulatory requirements across different regions. The combination of new market entrants and established companies creates a dynamic market environment where innovation and operational efficiency drive success.

Specialty Yeast Industry Leaders

Chr. Hansen Holding

DSM-Firmenich

Associated British Foods plc

Lallemand Inc

Group Lesaffre

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Red Star Yeast launched its improved Platinum Yeast product incorporating dough improvers to enhance gluten strength and volume, along with enzymes that slow staling to extend product freshness. The innovation targets home bakers and represents advancement in specialty yeast formulations

- October 2024: Lesaffre acquired a 70% stake in Biorigin, enhancing its position in the yeast derivatives market and improving production processes for savory ingredients. The acquisition includes Biorigin's production unit in Brazil and addresses growing demand for natural sources in food applications

- January 2024: Lallemand completed acquisition of Evolva, expanding its precision fermentation capabilities and product portfolio in biotechnology applications. The acquisition enhances Lallemand's position in specialty yeast and fermentation technologies

Global Specialty Yeast Market Report Scope

The Specialty Yeast Market Report is Segmented by Product Type (Yeast Extracts, Autolyzed Yeast, and Beta-Glucans), Species (Saccharomyces Cerevisiae, Pichia Pastoris, Kluyveromyces Marxianus, and Others), Application (Food and Beverage, Animal Feed, Dietary Supplement and Pharmaceuticals, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Yeast Extracts |

| Autolyzed Yeast |

| Beta-Glucans |

| Saccharomyces cerevisiae |

| Pichia pastoris |

| Kluyveromyces marxianus |

| Others |

| Food and Beverage |

| Animal Feed |

| Dietary Supplement and Pharmaceuticals |

| Cosmetics and Personal Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Yeast Extracts | |

| Autolyzed Yeast | ||

| Beta-Glucans | ||

| By Species | Saccharomyces cerevisiae | |

| Pichia pastoris | ||

| Kluyveromyces marxianus | ||

| Others | ||

| By Application | Food and Beverage | |

| Animal Feed | ||

| Dietary Supplement and Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the specialty yeast market?

The specialty yeast market size stands at USD 3.67 billion in 2025 and is projected to reach USD 5.52 billion by 2031.

Which product type holds the largest share?

Yeast extracts lead with 61.51% share of the specialty yeast market in 2025.

Which segment is expected to grow fastest through 2031?

Beta-Glucans are forecast to expand at the highest CAGR of 8.23% between 2026 and 2031.

Which region is witnessing the strongest growth?

Asia–Pacific shows the highest regional CAGR at 7.99% for 2026–2031, driven by regulatory updates and rising functional-food demand.

How concentrated is the competitive landscape?

The market exhibits moderate concentration, with the top five players controlling slightly above half of global revenue

Page last updated on: