Bovine Gelatin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

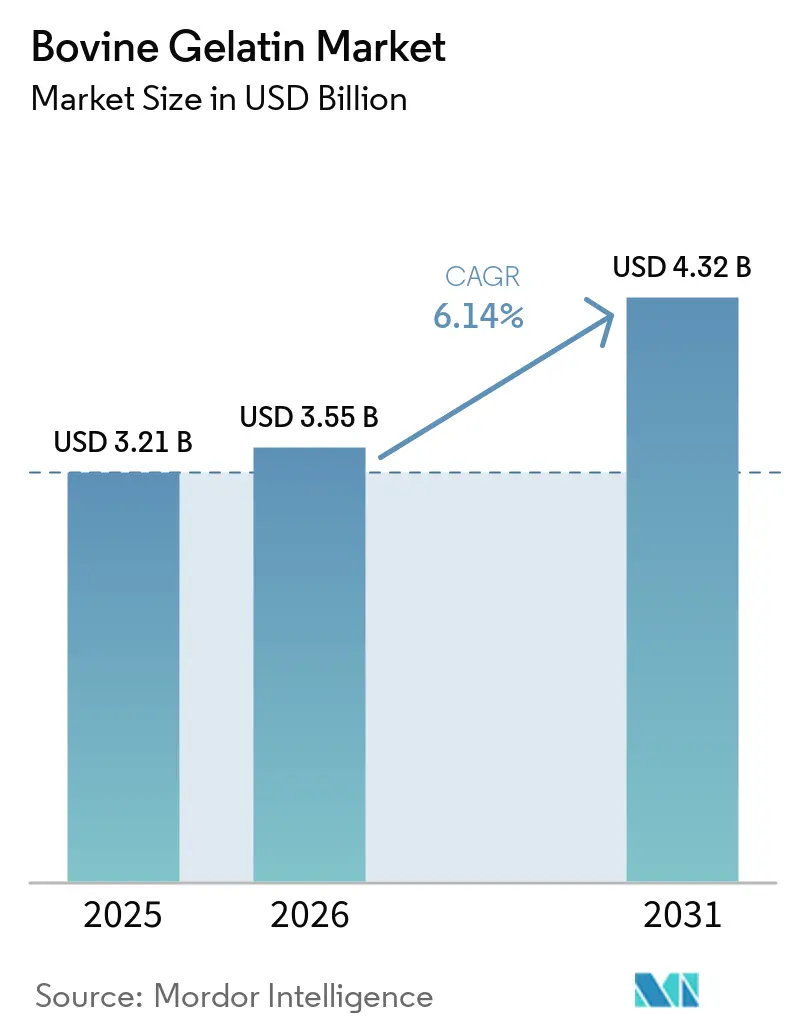

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 4.32 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bovine Gelatin Market Analysis by Mordor Intelligence

The bovine gelatin market size is expected to grow from USD 3.21 billion in 2025 to USD 3.55 billion in 2026, and is forecast to reach USD 4.32 billion by 2031, at a 6.14% CAGR over 2026-2031. Demand in the bovine gelatin market continues to be supported by pharmaceutical capsule production, functional food formats, and rising use of nutraceuticals across major regions. Europe is the fastest-growing region because buyers there are placing greater weight on BSE and TSE documentation, pharmacopoeia compliance, and fully audited supply chains for higher-spec uses. The competitive structure is also changing as Darling Ingredients and Tessenderlo Group agreed to combine Rousselot and PB Leiner into Nextida, which will give the new platform broad global coverage in gelatin and collagen. That shift is pushing the bovine gelatin market further toward collagen peptides and other higher-value ingredients because standard gelatin faces tighter pricing conditions. Even with growing plant-based capsule options and raw material swings, the bovine gelatin market still benefits from its strong gelling performance, reliable dissolution profile, and cost position in capsules, confectionery, and halal applications.

Key Report Takeaways

- By form, powder held 61.31% share in 2025, while liquid is forecast to grow at a 7.5% CAGR through 2031, and at a 7.21% CAGR through 2031.

- By form, powder held 61.31% share in 2025, while liquid is forecast to grow at a 7.55% CAGR through 2031.

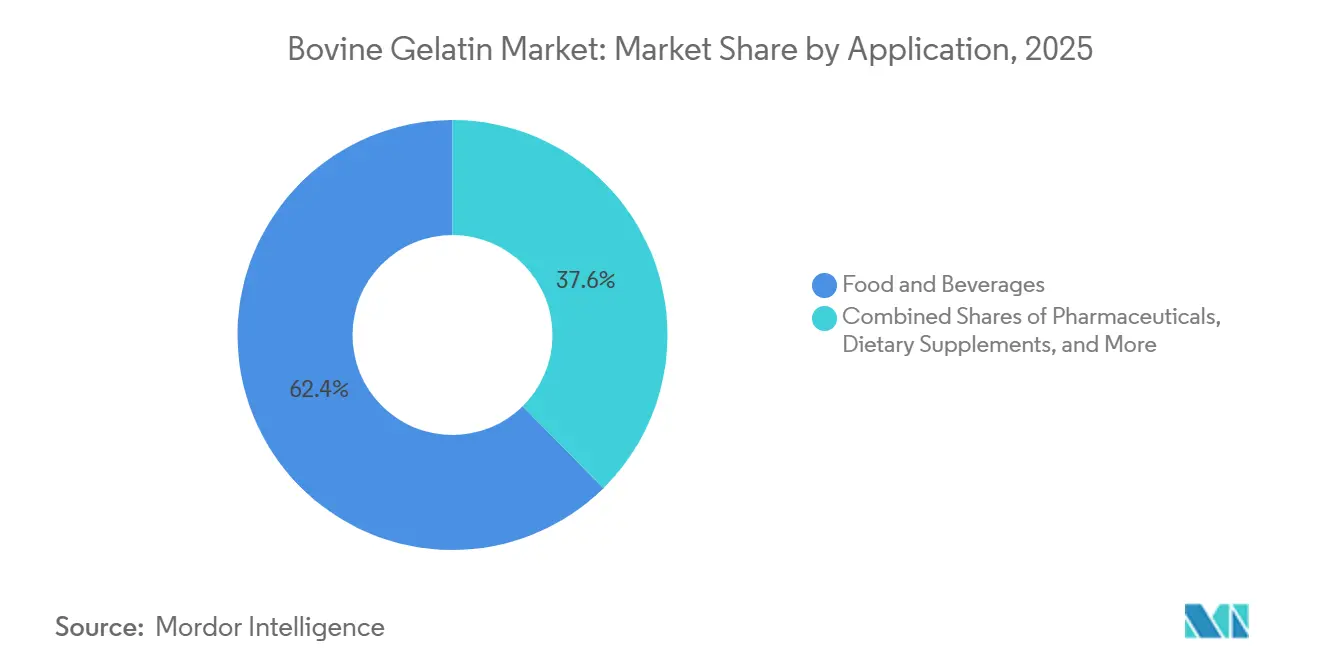

- By application, food and beverages accounted for 62.38% of the bovine gelatin market size in 2025, while pharmaceuticals are advancing at a 7.35% CAGR through 2031.

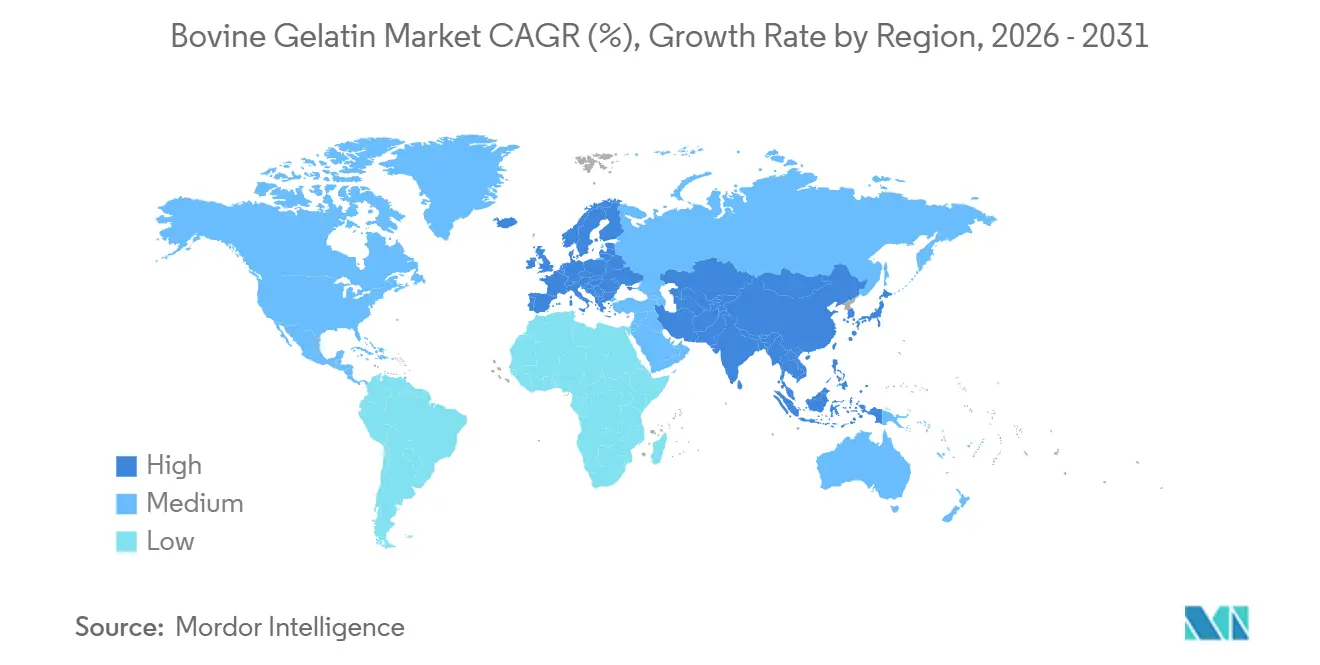

- By geography, Asia-Pacific held a 30.28% share in 2025, while Europe is forecast to expand at a 7.46% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bovine Gelatin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Growth Of Pharmaceutical Capsule Manufacturing | +1.8% | Global, concentrated in North America, Europe, India, and China | Medium term (2-4 years) |

| Expansion Of Nutraceutical And Healthy Aging Markets | +1.3% | North America and Europe, with spillover to Japan and South Korea | Medium term (2-4 years) |

| Strong Momentum In The Global Gummies Market | +1.0% | Global, with rapid penetration in Asia-Pacific and South America | Short term (≤ 2 years) |

| Rapid Expansion Of Confectionery Consumption In Emerging Markets | +0.8% | Asia-Pacific core, with spillover to Middle East and Africa and South America | Long term (≥ 4 years) |

| Cost Advantage Relative To Alternative Collagen And Specialty Hydrocolloids | +0.5% | Global | Short term (≤ 2 years) |

| Technological Advancements In Gelatin Processing | +0.4% | Global, with early adoption in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained Growth Of Pharmaceutical Capsule Manufacturing

Pharmaceutical capsule production remains the clearest structural support for the bovine gelatin market because hard and soft capsules still sit at the center of oral solid dosage manufacturing in most major drug systems. The bovine gelatin market benefits from the fact that bovine gelatin remains widely accepted for capsule use when it meets documented quality, traceability, and treatment requirements across regulated supply chains. That support is not only about volume, because tighter quality expectations raise the value of each kilogram supplied for pharmaceutical use rather than simply increasing throughput. European import and treatment requirements for bovine inputs continue to favor certified producers that can maintain full documentation, which raises entry barriers for smaller spot-market suppliers. The result is that the bovine gelatin market gains from both expanding capsule output and a steady move toward more tightly specified pharmaceutical grades[1]Source: United States Department of Agriculture, Animal and Plant Health Inspection Service, “European Union, Treated Animal Byproducts for the Production of Gelatin and or Collagen for Human Consumption,” aphis.usda.gov.

Expansion Of Nutraceutical And Healthy Aging Markets

The nutraceutical channel is giving the bovine gelatin market a broader demand base because collagen peptide products are being positioned for joint health, skin support, sports recovery, and active aging use. This is creating a split inside the bovine gelatin market between standard material sold for basic encapsulation and higher-value collagen and peptide ingredients sold with stronger health positioning. That shift matters because producers with the ability to separate premium grades from commodity output can protect pricing more effectively than suppliers focused only on bulk gelatin volumes. It also makes formulation quality, amino acid profile, and consistency more important in customer selection, especially in mature supplement markets where buyers are already familiar with collagen-based claims. As a result, the bovine gelatin market is moving beyond pure volume growth and is increasingly shaped by product mix and application quality, even where end-use demand appears similar on the surface.

Strong Momentum In The Global Gummies Market

Gummy formats are one of the most consistent near-term supports for the bovine gelatin market because they combine confectionery demand with supplement demand in a single delivery form. The bovine gelatin market benefits here because gelatin gives manufacturers dependable texture, quick-setting behavior, and flavor neutrality under standard industrial conditions. Functional gummies often require stronger structural support than basic candy products because vitamins, probiotics, collagen, and omega-3 additions can make texture control harder over shelf life. That raises gelatin loading in each unit and increases total demand even when unit volumes do not surge at the same pace. The bovine gelatin market therefore captures both the base growth of confectionery gummies and the added pull from nutrition formats that rely on the same processing advantages.

Rapid Expansion Of Confectionery Consumption In Emerging Markets

Emerging market confectionery demand is creating a longer-duration support line for the bovine gelatin market, especially across Southeast Asia, South Asia, and parts of Sub-Saharan Africa. The key point is not only higher packaged food sales, but also the need for halal-compliant gelling systems in Muslim-majority consumer markets where porcine gelatin is not a practical option. In those settings, bovine gelatin often fits both technical performance needs and commercial price points more effectively than plant-based substitutes, which can cost more and require tighter process control. Halal certification is therefore acting as both a compliance tool and a route to wider market access for ingredient suppliers that want durable positions in these regions. That is why the bovine gelatin market is seeing emerging-market confectionery demand develop on a different path from premium Western substitution trends

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Popularity Of Plant-Based Alternatives | -1.2% | North America and Europe, with early-stage penetration in Asia-Pacific | Medium term (2-4 years) |

| Stringent Regulatory Requirements | -0.8% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Volatility In Raw Material Availability And Pricing | -0.9% | Global, particularly acute in South America and Europe | Short term (≤ 2 years) |

| Environmental Concerns Related To Livestock Production | -0.6% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Popularity Of Plant-Based Alternatives

The strongest visible substitution pressure on the bovine gelatin market comes from plant-based capsule options such as HPMC and pullulan rather than from broad replacement across all gelatin uses. That pressure is concentrated in premium dietary supplements in North America and Europe, where vegan, vegetarian, and label-sensitive positioning has stronger commercial pull. The scale of investment around alternative capsule supply became clearer when Lone Star Funds agreed to acquire Lonza Group AG's Capsules and Health Ingredients division in March 2026. Even so, that pressure is not uniform because pharmaceutical, confectionery, and many emerging-market food applications still rely heavily on bovine gelatin for performance and cost reasons. The outcome is a more segmented bovine gelatin market where high-volume uses remain resilient but some premium growth moves toward plant-based encapsulation platforms.

Volatility In Raw Material Availability And Pricing

Raw material volatility remains a clear restraint for the bovine gelatin market because bovine hides and bones are shaped by separate cycles in slaughter activity, leather demand, and regional processing availability. Hide supply can tighten even when cattle numbers are stable because demand shifts in footwear, fashion, or automotive upholstery alter how much material moves efficiently into gelatin chains. At the same time, suppliers serving regulated markets must maintain treatment, traceability, and documentation standards, which makes it harder to switch quickly to opportunistic raw material sources when costs rise. Bone-based supply helps reduce some of that exposure, but the transition is gradual because pharmaceutical customers still require tight and consistent specifications. The bovine gelatin market therefore faces a cost and sourcing challenge that affects planning, contract structure, and margin stability, especially in periods of uneven raw material flow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Hides Anchor Supply As Bones Accelerate In Pharmaceutical Applications

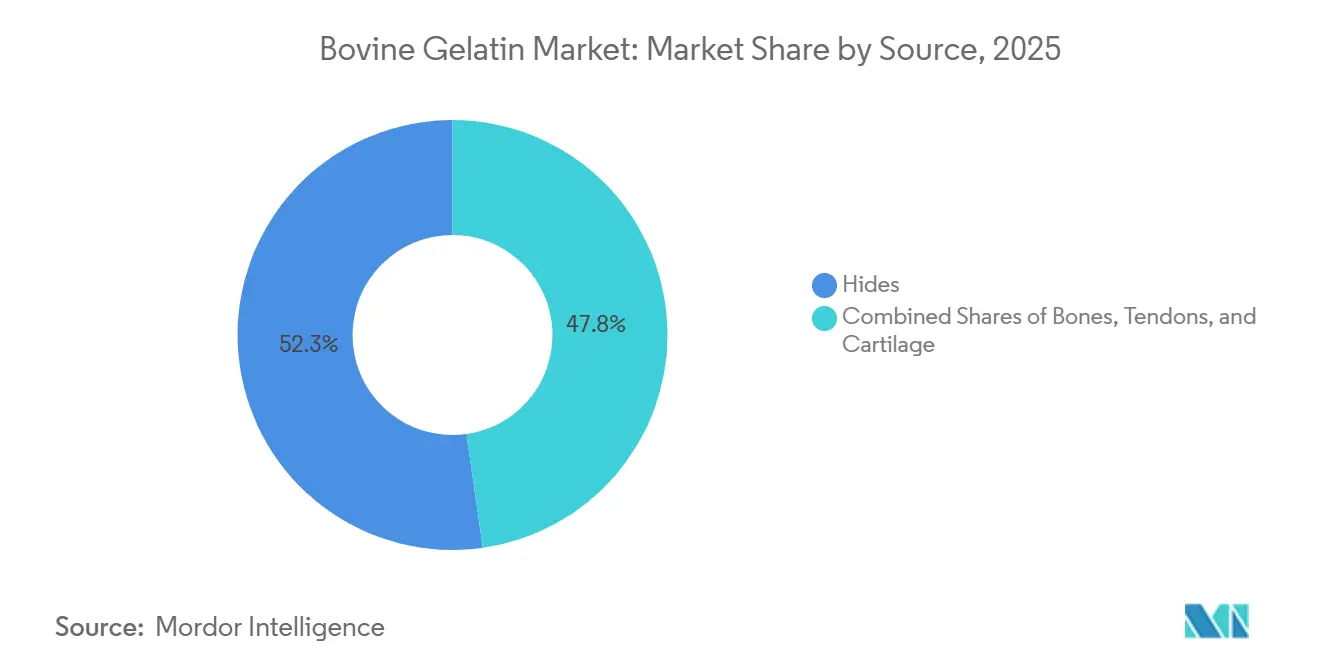

Hides held 52.25% of the bovine gelatin market share by source in 2025, which reflects the long-standing link between tanning activity and gelatin extraction across established producing regions. The bovine gelatin market has depended on hides for decades because this raw material already sits inside well-developed collection and processing networks, which lowers procurement friction for large producers. Hide-derived gelatin remains especially relevant in uses that value clarity, familiar processing behavior, and wide industrial compatibility across capsule and dairy systems. That installed base hides a durable role even as the bovine gelatin industry becomes more selective about traceability and grade separation. Documentation requirements for treated bovine material in regulated export chains also strengthen the position of established producers that can prove origin, handling, and treatment history across the full chain. Those requirements do not eliminate smaller competitors, but they do make scale and compliance much more valuable in the source mix.

Bones are the fastest-growing source segment in the bovine gelatin market and are projected to expand at a 7.21% CAGR through 2031. That rise reflects the closer fit between bone-derived Type B gelatin and several pharmaceutical dissolution and pharmacopoeia requirements used in hard capsule systems. Research published in 2025 showed that papain-assisted enzymatic hydrolysis of bovine cattle bones preserved collagen chain structure more effectively than conventional acid or alkaline extraction routes. The same study found better Bloom strength, viscosity, and molecular weight distribution, which matters because those properties shape performance consistency in higher-spec uses. Bone growth also gives the bovine gelatin market a practical diversification benefit because bone availability tracks slaughter output more directly and is less tied to leather sector swings than hide availability. Over time, that reduces procurement imbalance and makes bones a more important strategic source rather than only a supplementary one, according to the MDPI research[2]Source: Wang X. et al., “Physicochemical and Functional Properties of Yanbian Cattle Bone Gelatin Extracted Using Acid, Alkaline, and Enzymatic Hydrolysis Methods,” Gels, mdpi.com.

By Form: Powder Retains Industrial Dominance As Liquid Gains In Process Efficiency

Powder held 61.31% share by form in 2025, showing how strongly the bovine gelatin market still depends on manufacturing systems built around dry ingredient handling. Powder remains the default format because capsule, confectionery, dairy, and processed food lines have long been designed with reconstitution, dosing, and storage practices that fit dry input materials. It also supports clearer grade separation because Bloom strength and other functional properties can be specified, stored, and transported familiarly across global supply chains. That matters in the bovine gelatin market because a large part of procurement discipline is tied to repeatability rather than to raw input cost alone. Producers serving pharmaceutical users also benefit from the easier handling of differentiated grades when customers demand exact release behavior, stability, or sealing performance. This helps explain why powder keeps its lead even as users look for a simpler process flow.

Liquid is the fastest-growing form in the bovine gelatin market and is expected to grow at a 7.55% CAGR through 2031. The appeal is straightforward because ready-to-use liquid gelatin removes the reconstitution step and can reduce handling time for large food processors with repeat batch production. It also allows tighter viscosity control during production, which supports consistency in functional food formats that are more sensitive to variation in texture and process timing. That makes liquid especially useful in applications where manufacturers value operational speed, fewer preparation steps, and lower risk of performance drift during heat exposure. The form split in the bovine gelatin market is therefore becoming less about basic convenience and more about how each format fits a specific processing setup and quality target. Over the forecast period, suppliers with strong control over specification by format are likely to hold the strongest position in both standard and premium accounts.

By Application: Food And Beverages Leads While Pharmaceuticals Drives Value Growth

Food and beverages accounted for 62.38% of the bovine gelatin market size in 2025, which shows how broad the product's role remains across confectionery, dairy stabilization, and processed meats. The bovine gelatin market still relies on these uses because they combine steady consumption with industrial familiarity, making gelatin the default option in many recipes and production lines. Functional gummies are adding another layer of demand because they sit at the overlap between confectionery and nutrition and often require more structural support than plain candy formats. Cosmetics and personal care also remain relevant because gelatin's film-forming and moisture-supporting properties allow it to fit selected skin and beauty applications. At the same time, technical uses such as photography, adhesives, and similar smaller outlets occupy a shrinking share as higher-value consumer and pharmaceutical uses absorb more production capacity. This keeps the largest application base in food while gradually moving the center of profitability elsewhere.

Pharmaceuticals are the fastest-growing application in the bovine gelatin market and is projected to advance at a 7.35% CAGR through 2031. The main support comes from continued global dependence on oral solid dosage forms, where gelatin-based capsules still offer scale, manufacturing familiarity, and broad acceptance in regulated settings. The bovine gelatin market is also helped by the fact that pharmaceutical buyers are less willing to compromise on dissolution behavior, traceability, and batch consistency than buyers in many lower-value food applications. That gives approved suppliers more room to protect margins and makes product qualification more important than spot availability alone. The overlap with dietary supplements further supports this segment because many supplement capsules rely on similar sourcing and specification disciplines, even when they serve a different consumer channel. Across the forecast period, the bovine gelatin industry will therefore see application value move faster toward pharmaceutical and nutraceutical demand than toward commodity food-grade expansion.

Geography Analysis

Asia-Pacific held 30.28% of the bovine gelatin market in 2025, making it the largest regional base by share. China remains central to the bovine gelatin market because it combines large-scale processing, raw material access, and a deep manufacturing network that supports both domestic and export supply. India is also gaining importance because halal-certified pharmaceutical-grade output fits the needs of capsule buyers and regulated export channels, while Southeast Asian markets add demand from confectionery and healthcare manufacturing. Taken together, these conditions keep Asia-Pacific at the center of both supply scale and volume growth in the bovine gelatin market[3]Source: Foodchem International Corporation, “Foodmate Obtains Indonesia's MUI & BPJPH Halal Certifications,” foodchem.com.

Europe is the fastest-growing region in the bovine gelatin market and is expected to post a 7.46% CAGR through 2031. That growth is being shaped more by quality upgrades and sourcing discipline than by simple volume expansion. Buyers in Europe operate under strict expectations around treatment, origin documentation, and traceability for bovine-derived material, which favors suppliers with audited chains and full compliance records. This raises the value of approved pharmaceutical and premium nutraceutical supply because customers are paying for assurance as much as for the ingredient itself. The result is a regional market where documented quality increasingly separates winners from undifferentiated commodity suppliers.

North America is a high-value demand center in the bovine gelatin market because of its deep pharmaceutical and dietary supplement manufacturing base. The United States remains especially important because capsule and supplement buyers there value specification control, documentation, and dependable supply history. The Middle East and Africa hold a smaller share, but they matter more each year as halal-certified imports support food, nutrition, and pharmaceutical expansion in Muslim-majority markets. Across both North America and the Middle East and Africa, market access depends heavily on suppliers that can align functional performance with recognized certification and traceability standards.

Competitive Landscape

The bovine gelatin market shows medium concentration because a limited group of integrated producers leads pharmaceutical and premium nutraceutical supply, while many regional companies still compete across standard food-grade volumes. GELITA AG, Rousselot, PB Leiner, Gelnex, and Nitta Gelatin remain the most visible names in higher-spec supply, but their influence is uneven across applications and regions. The biggest structural move came in December 2025, when Darling Ingredients and Tessenderlo Group signed definitive agreements to merge Rousselot and PB Leiner into Nextida. The planned platform is expected to have annual revenue of around USD 1.5 billion, a capacity of 200,000 metric tons, and 23 facilities across four continents, which gives it substantial scale in the bovine gelatin market.

That scale matters because it gives Nextida wider control over sourcing, processing, and customer access across both gelatin and collagen categories. It also supports a broader shift inside the bovine gelatin market away from pure commodity supply and toward targeted ingredients with better pricing power. GELITA is pursuing a similar move through adjacent technology, as shown by its March 2026 joint R&D agreement with Black Drop to develop bioinks for tissue models and medical implants. This is important because it shows how leading producers are using collagen and gelatin science to enter fields that sit beyond traditional food and capsule demand. Competition is also being shaped by outside investment in alternative capsule platforms after Lone Star Funds agreed to acquire Lonza Group AG's Capsules and Health Ingredients division in March 2026.

For challengers, the clearest opening in the bovine gelatin market remains halal-certified pharmaceutical-grade supply into North America and Southeast Asia, where documentation and application fit both matter. Process improvements in bone extraction could also help newer producers narrow the quality gap in higher-spec grades if they can match consistency and compliance expectations. That means the most durable edge is no longer simple capacity, but the ability to combine traceability, specialized processing, and application-specific supply. In practice, the bovine gelatin market is becoming more selective, with the strongest positions going to suppliers that can move from bulk output toward certified, high-value, and technically differentiated portfolios.

Bovine Gelatin Industry Leaders

Darling Ingredients Inc.

GELITA AG

Tessenderlo Group

Nitta Gelatin Inc.

Lapi Gelatine S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GELITA AG's Liaoyuan facility in Jilin province, China, operational since 2006, confirmed its position as GELITA's largest global gelatin production base, underscoring China's strategic importance as both a cost-efficient production hub and an expanding domestic gelatin consumer market.

- March 2026: Lone Star Funds signed a definitive agreement to acquire Lonza Group AG's Capsules and Health Ingredients (CHI) division for approximately USD 4.7 billion, with Lonza retaining a 40% equity stake. The CHI division manufactures both hard gelatin capsules and HPMC plant-based capsules for pharmaceutical and nutraceutical customers globally.

- December 2025: Darling Ingredients and Tessenderlo Group signed a definitive agreement to merge Rousselot and PB Leiner into Nextida, with projected annual revenue of approximately USD 1.5 billion, capacity of ~200,000 metric tons, and 23 facilities across four continents. Darling Ingredients holds an 85% stake.

Global Bovine Gelatin Market Report Scope

| Hides |

| Bones |

| Tendons and Cartilage |

| Powder |

| Liquid |

| Food and Beverages |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Dietary Supplements |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Source | Hides | |

| Bones | ||

| Tendons and Cartilage | ||

| Form | Powder | |

| Liquid | ||

| Application | Food and Beverages | |

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Dietary Supplements | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the bovine gelatin market in 2026?

The bovine gelatin market stands at USD 3.55 billion in 2026 and is forecast to reach USD 4.32 billion by 2031 at a 6.14% CAGR.

What is driving demand for bovine gelatin through 2031?

The main supports are pharmaceutical capsule manufacturing, functional gummies, broader nutraceutical use, and halal-compliant confectionery demand in emerging regions.

Which source segment is growing fastest?

Bones is the fastest-growing source segment with a projected 7.21% CAGR through 2031, supported by its fit with pharmaceutical-grade requirements.

Which application area holds the largest share?

Food and beverages led with 62.38% of total demand in 2025 because gelatin remains widely used in confectionery, dairy, and processed meat applications.

Page last updated on: