Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

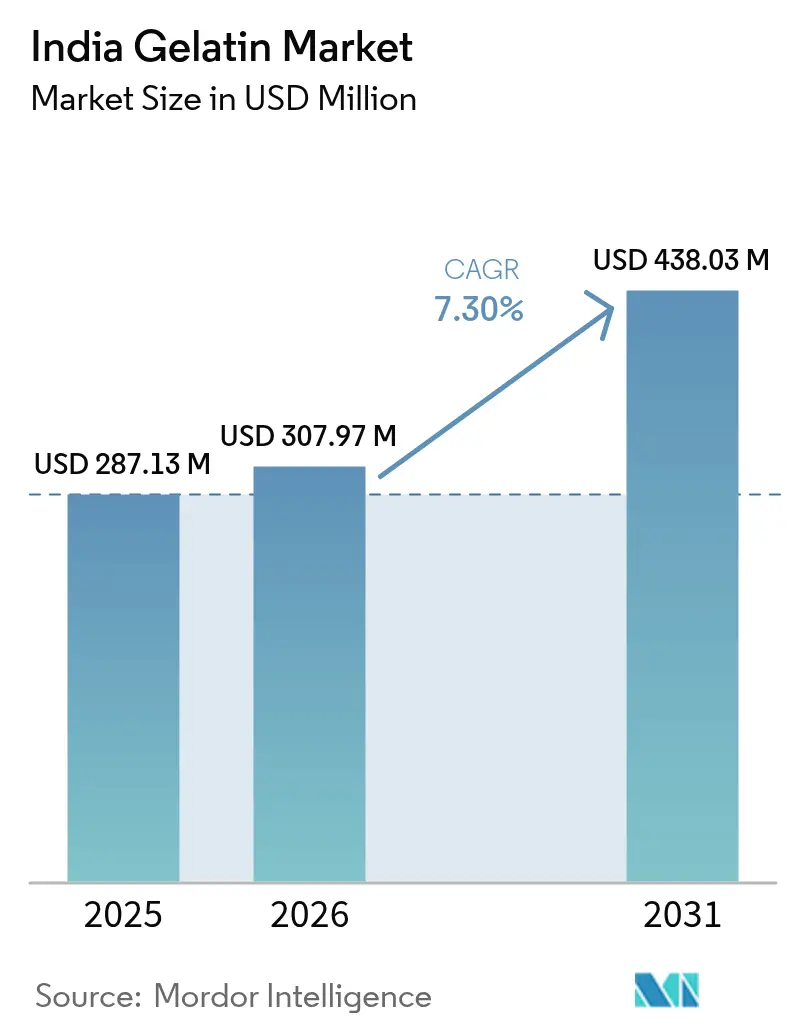

| Base Year Market Size (2025) | USD 287.13 Million |

| Market Size (2026) | USD 307.97 Million |

| Market Size (2031) | USD 438.03 Million |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

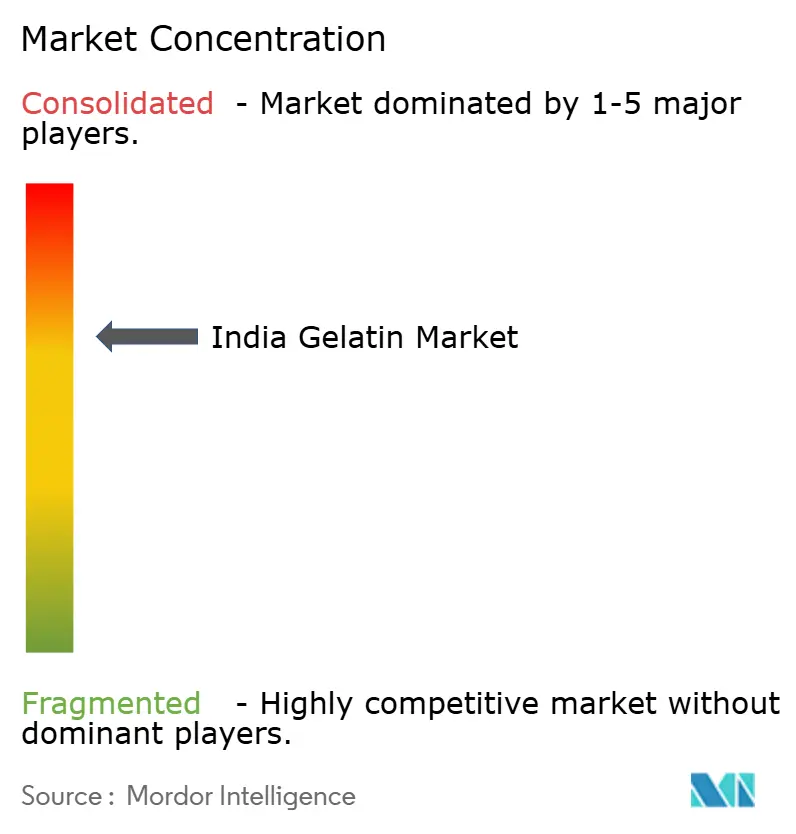

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Gelatin Market Analysis by Mordor Intelligence

The Indian gelatin market size is expected to grow from USD 287.13 million in 2025 to USD 307.97 million in 2026 and is forecast to reach USD 438.03 million by 2031 at 7.30% CAGR over 2026-2031. The market growth is driven by increasing demand from functional foods, pharmaceuticals, and personal care sectors. Manufacturers benefit from reliable access to raw materials through bovine, porcine, and marine collagen sources. The government's production-linked incentives for food processing and mandatory halal certification requirements for specific export markets have prompted major companies to enhance their technological capabilities and quality management systems. The market's growth prospects are strengthened by increasing urbanization, a growing health-conscious consumer base, and clear regulatory guidelines for nutraceutical labeling. The market structure is characterized by moderate consolidation, ongoing developments in marine collagen, and emerging fermentation-based protein technologies that could influence future investment patterns.

Key Report Takeaways

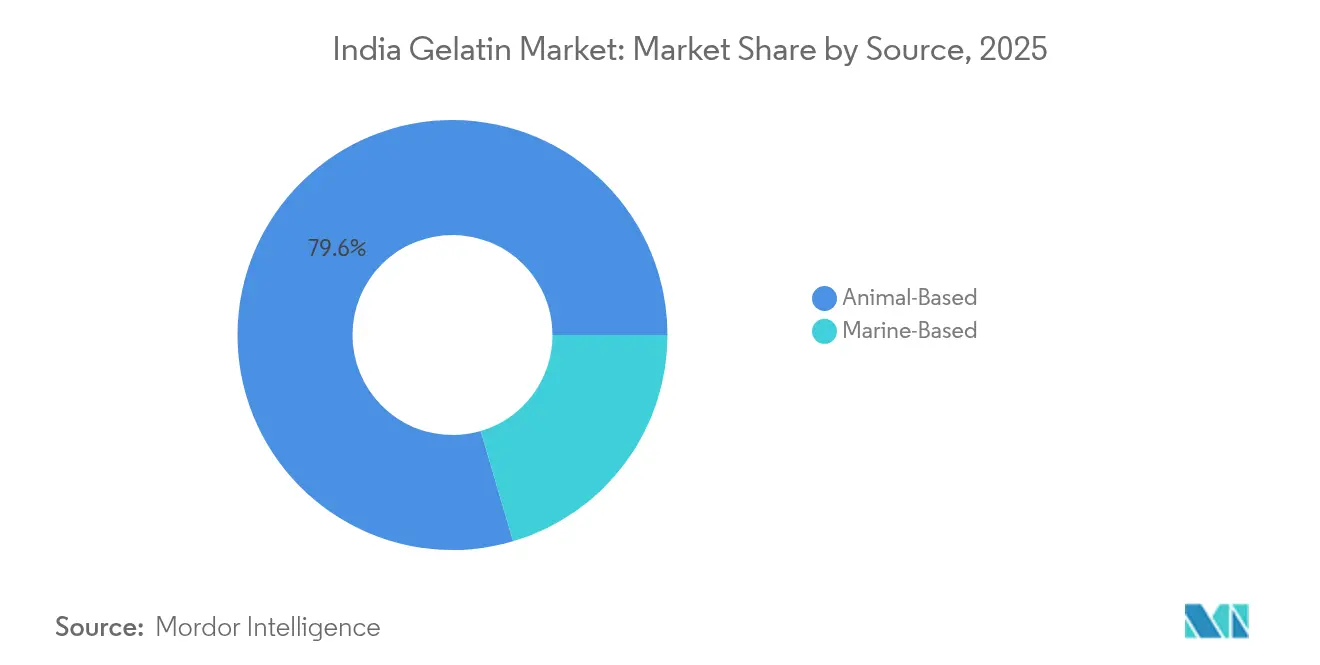

- By source, animal-based gelatin held 79.55% of the gelatin market share in 2025, while marine sources are projected to lead growth at a 7.70% CAGR through 2031.

- By grade, the food-grade segment commanded 55.05% of the gelatin market size in 2025; the pharmaceutical grade is forecast to outpace all grades with a 7.82% CAGR to 2031.

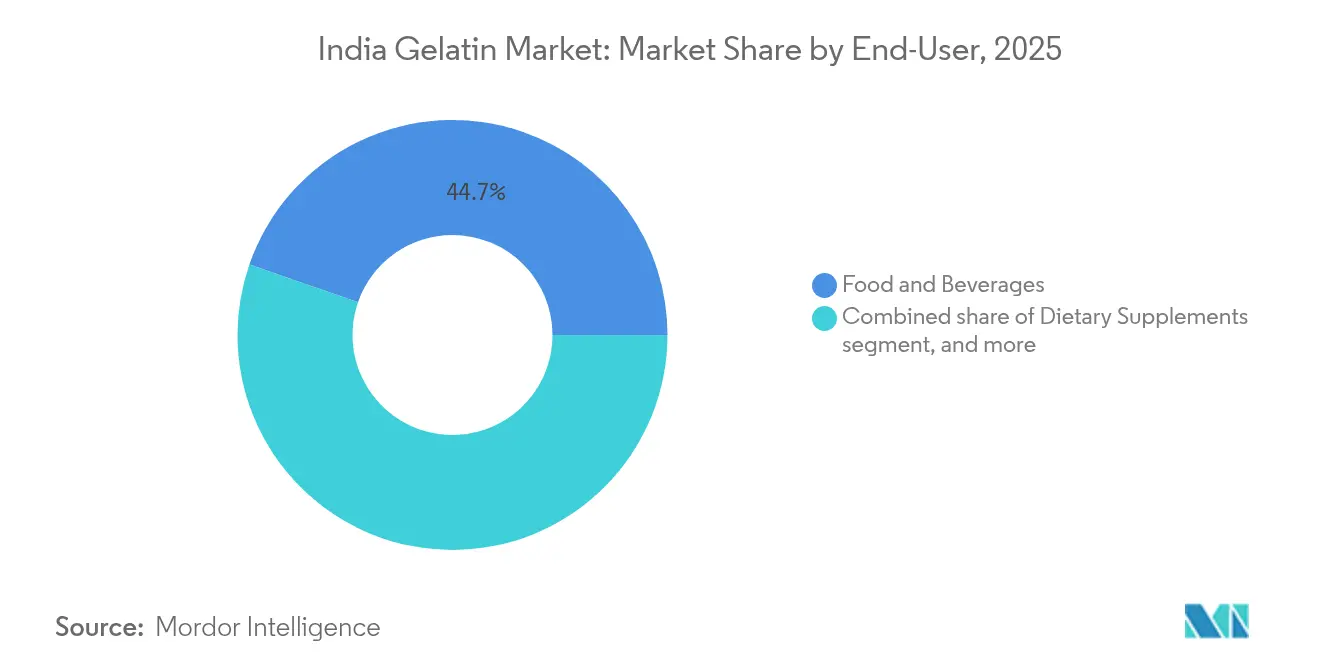

- By end-user, food and beverages dominated at 44.68% gelatin market share in 2025, whereas dietary supplements are set to rise fastest at an 8.06% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Gelatin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding confectionery and processed dairy sector | +1.2% | National, with concentration in Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Growth of functional food and beverages | +1.8% | Urban markets nationwide, early adoption in metros | Short term (≤ 2 years) |

| Shift toward clean label and protein-enriched products | +1.5% | National, premium segments in Tier-1 cities | Medium term (2-4 years) |

| Substantial utilization of gelatin in pharmaceuticals | +1.1% | Gujarat, Hyderabad, Goa pharmaceutical hubs | Long term (≥ 4 years) |

| Rising adoption in personal care and cosmetics | +0.9% | Urban centers, export-oriented manufacturing | Medium term (2-4 years) |

| Government incentives for collagen recovery from meat waste | +0.8% | States with meat processing infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Confectionery and Processed Dairy Sector

India's confectionery market growth has increased the demand for gelatin, as manufacturers use it to enhance texture and extend product shelf life. The market expansion is supported by increasing disposable incomes and changing dietary preferences toward Western products, especially in urban areas where premium confectionery items generate higher margins. The dairy processing segment, supported by India's status as the world's largest milk producer, incorporates gelatin in yogurts, desserts, and functional dairy products to enhance texture and nutritional content. The Ministry of Food Processing Industries (MOFI) provides infrastructure funding to food processing units, enabling them to expand capacity and upgrade technology, which increases gelatin usage in production. The government has identified several growth opportunities in the dairy processing sector for 2025, including advanced dairy processing technologies, cold chain development, and product innovation in cheese, smoothies, flavored milk, custard, yogurt, and traditional Indian products[1]Source: Ministry of Food Processing Industries (MOFPI), "Opportunities in Dairy Sector in India,"mofpi.gov. These developments expand the use of gelatin as a functional ingredient in both confectionery and processed dairy products.

Growth of Functional Food and Beverages

The expansion of India's functional food and beverages segment is driving increased demand for gelatin. Manufacturers are incorporating gelatin into protein-enriched drinks, fortified gummies, and nutritional supplements to meet the needs of health-conscious consumers. In these applications, gelatin serves as both a functional ingredient for texture and stability and an encapsulation medium for vitamins, minerals, and bioactive compounds. The collagen peptides obtained through gelatin hydrolysis provide bioactive properties beneficial for skin health, joint function, and overall wellness, contributing to the development of premium nutrition products. A global study by Wonderful Pistachios revealed that 58% of urban Indians prioritize nutritional benefits over taste when making food purchases, exceeding the global average of 52%. Delhi and Ahmedabad demonstrate the strongest nutrition-first mindset, with over 60% of urban consumers prioritizing health benefits. Bengaluru and Chennai show similar trends, indicating a broader national shift toward health-oriented food choices in 2024[2]Source: Food and Beverage News, "Study reveals majority of Indians prioritise nutrition over taste," fnbnews.com . This increased focus on nutrition among Indian consumers reinforces gelatin's position as an essential ingredient in the functional food and beverage market.

Shift Toward Clean Label and Protein-Enriched Products

The demand for transparent ingredient lists and protein fortification is increasing the use of gelatin as a natural, recognizable ingredient in place of synthetic alternatives. Marine-based gelatin sources are gaining prominence as they meet consumer requirements for sustainable and religiously acceptable protein options. The clean label movement aligns with India's traditional preference for natural ingredients, creating opportunities for suppliers who provide traceability and quality assurance in their supply chains. Manufacturers are developing gelatin products with minimal processing and transparent sourcing documentation to meet consumer expectations. The Healthy Snacking Report (2024) indicates that 73% of Indians examine ingredient lists and nutritional values before purchasing processed snacks, demonstrating a shift toward healthier and informed snacking habits[3]Source: Business Standard, "73% Indians read ingredient lists, nutritional value of snacks: Report," business-standard.com . This increased consumer awareness is driving the incorporation of gelatin in protein-enriched and clean-label formulations across India's food and nutraceutical markets.

Substantial Utilization of Gelatin in Pharmaceuticals

The expansion of India's pharmaceutical sector, driven by domestic demand and export opportunities, creates consistent gelatin demand for capsule manufacturing and drug delivery applications. The sector benefits from government production-linked incentive schemes that promote domestic API manufacturing and reduce import dependence, supporting gelatin demand growth. Gujarat has emerged as India's pharmaceutical hub, with efficient regulatory processes and infrastructure advantages, concentrating gelatin consumption in geographic clusters where pharmaceutical manufacturers achieve economies of scale. Drug delivery systems increasingly use gelatin-based matrices for controlled release formulations, expanding beyond traditional capsule applications into specialized therapeutic areas. The Central Drugs Standard Control Organization's regulatory framework maintains quality standards that favor established gelatin suppliers with pharmaceutical-grade certification capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of plant-based hydrocolloid replacements | -1.1% | Urban markets, export-oriented segments | Short term (≤ 2 years) |

| Regulatory and certification challenges | -0.7% | National, particularly export markets | Medium term (2-4 years) |

| Volatile supply and pricing of bovine bone raw material | -0.9% | Northern and western states with livestock concentration | Short term (≤ 2 years) |

| Religious/vegetarian constraints on animal origin | -0.6% | National, varying by regional demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Plant-Based Hydrocolloid Replacements

Plant-based alternatives including agar-agar, carrageenan, and pectin increasingly challenge gelatin's market position, particularly in vegetarian-conscious segments and export markets with sustainability mandates. Technical research demonstrates that κ-carrageenan combined with locust bean gum can replicate gelatin's gelling properties in specific applications, though limitations remain in thermal stability and texture characteristics. The development of sophisticated plant-based formulations by food technologists creates viable alternatives for cost-sensitive applications, though premium segments continue favoring gelatin for superior functional properties. Consumer awareness campaigns by plant-based ingredient suppliers emphasize environmental and ethical advantages, influencing purchasing decisions in urban markets where sustainability concerns drive product selection. However, plant-based alternatives face their own supply chain constraints and price volatility, limiting their ability to completely displace gelatin in price-sensitive applications.

Regulatory and Certification Challenges

Regulatory requirements across multiple jurisdictions create compliance challenges, particularly affecting smaller gelatin manufacturers and limiting market entry. FSSAI's food safety standards require ongoing investment in quality systems and documentation. Export markets require additional certifications, including halal, kosher, and organic credentials, increasing operational complexity. The implementation of mandatory halal certification for meat product exports to 15 countries through India's Conformity Assessment Scheme has increased compliance costs and extended timelines for gelatin exporters. FSSAI regulations require foreign facility registration, adding administrative requirements for international suppliers, while domestic manufacturers face increased scrutiny of raw material sourcing and processing standards. These regulatory requirements benefit larger, established companies with dedicated compliance resources while creating entry barriers for new competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Alternatives Gain Traction

Marine-based gelatin demonstrates significant growth potential with a 7.70% CAGR through 2031, despite holding a smaller market share. This growth stems from religious dietary preferences and health benefits compared to animal-based alternatives. India's expanding coastal aquaculture industry and improved fish processing capabilities provide collagen-rich by-products for gelatin extraction. Animal-based gelatin maintains market dominance with an 79.55% share in 2025, supported by established supply chains and India's extensive livestock processing infrastructure. The segment benefits from India's position as a major beef exporter and dairy producer, ensuring a steady bovine raw material supply.

Technological advancements in processing have improved marine gelatin's gel strength and thermal stability, broadening its applications. The Food Safety and Standards Authority of India (FSSAI) provides regulatory oversight through established standards for gelatin purity and safety, with additional requirements for marine sources regarding heavy metal contamination and traceability. Government initiatives supporting blue economy development and sustainable fisheries management contribute to the marine gelatin sector's growth by improving raw material quality and availability.

By Grade: Pharmaceutical Applications Drive Premium Growth

Food-grade gelatin holds a 55.05% market share in 2025, maintaining its dominant position in India's expanding confectionery, dairy, and processed food sectors. This segment's growth aligns with the country's developing food processing industry, supported by government production-linked incentive schemes that promote domestic manufacturing and reduce import dependence. The pharmaceutical grade segment, though smaller in volume, demonstrates higher growth at 7.82% CAGR. This growth stems from India's position as a global pharmaceutical manufacturing hub and increasing domestic healthcare consumption.

Pharmaceutical applications include traditional capsule manufacturing and advanced drug delivery systems, such as sustained-release formulations and targeted therapeutic applications. The pharmaceutical segment benefits from Gujarat's pharmaceutical cluster, which offers streamlined regulatory processes and developed infrastructure, reducing manufacturing costs and timelines. The high capital requirements for clean room facilities and quality control systems create significant entry barriers, helping established suppliers maintain their market positions.

By End-User: Dietary Supplements Emerge as Growth Driver

Food and beverages applications hold a dominant 44.68% market share in 2025, driven by gelatin's widespread use in confectionery manufacturing, dairy product texturization, and processed food applications. This market position stems from India's growing food processing industry and increased consumer demand for convenience foods and confectionery products. The personal care and cosmetics segment shows significant growth due to rising consumer adoption of anti-aging skincare products and beauty formulations containing collagen-derived ingredients.

The dietary supplements segment exhibits the highest growth rate at 8.06% CAGR, supported by India's wellness trends and FSSAI's nutraceutical regulations. This expansion reflects increased consumer focus on preventive healthcare and nutritional supplementation, particularly in urban areas with higher disposable incomes. The pharmaceutical segment continues to grow steadily, backed by India's expanding generic drug manufacturing industry and increased healthcare consumption due to an aging population and rising chronic disease cases.

Geography Analysis

India's gelatin market demonstrates distinct regional concentration patterns aligned with food processing and pharmaceutical manufacturing centers. Gujarat leads production, supported by its established pharmaceutical industry cluster, conducive regulatory framework, and efficient logistics infrastructure. The state's strategic location near major ports facilitates both domestic distribution and export operations. Maharashtra and Tamil Nadu serve as major consumption hubs due to their extensive food processing industries and urban markets that demand high-quality confectionery and functional food products. These states leverage their existing dairy processing facilities, cold chain infrastructure, and strategic location near key consumption centers to minimize distribution costs and ensure quick market response.

The northern states, particularly Punjab and Haryana, provide significant raw material through their livestock processing industries and well-developed animal husbandry sector, though their gelatin manufacturing capacity remains smaller compared to western and southern regions. India's expanding international trade relationships create growth opportunities, especially for halal-certified products in Middle Eastern and Southeast Asian markets. The implementation of mandatory halal certification requirements for exports to 15 countries through India's Conformity Assessment Scheme establishes specific compliance requirements while enabling premium market positioning. This certification process involves rigorous quality control measures, documentation requirements, and regular audits by authorized certification bodies.

Government policies supporting circular economy principles and meat waste valorization encourage capacity expansion and technological advancement across regions. These initiatives include financial incentives for waste reduction, research and development support for processing technologies, and infrastructure development grants, though implementation effectiveness varies based on local industrial infrastructure and regulatory capabilities.

Competitive Landscape

The Indian gelatin market demonstrates moderate consolidation, with established companies holding substantial market positions while accommodating specialized competitors and new technologies. Market leaders implement vertical integration strategies by controlling raw material sourcing through livestock processing operations and maintaining downstream connections via pharmaceutical and food industry partnerships.

This integration offers cost benefits and supply chain reliability that smaller competitors find difficult to match without significant capital investments. Companies prioritize technology adoption and capacity expansion, investing in advanced processing equipment and quality control systems to fulfill pharmaceutical-grade requirements and export market standards.

The market presents significant growth opportunities in marine gelatin production, premium collagen peptides, and specialized pharmaceutical applications, where technical expertise and regulatory compliance create competitive advantages. New market entrants concentrate on sustainable sourcing practices, comprehensive traceability systems, and alternative protein technologies to effectively meet the growing demands of environmentally conscious consumers and export markets with strict sustainability requirements.

India Gelatin Industry Leaders

-

Foodchem International Corporation

-

India Gelatine & Chemicals Ltd

-

Jellice Group

-

Nitta Gelatin Inc.

-

Sterling Gelatin (Godrej)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nitta Gelatin India Ltd (NGIL), a joint venture between Nitta Gelatin Inc. of Japan and the Kerala State Industrial Development Corporation, has begun a ₹60 crore expansion at its Kakkanad, Kochi facility. The project, part of a broader ₹200 crore investment in Kerala, includes constructing a collagen peptide plant, gelatin manufacturing unit, and corporate headquarters in Kakkanad to enhance NGIL's manufacturing capabilities.

- June 2023: Pioneer Jellice India Pvt Ltd (a joint venture between Pioneer Asia Group from Sivakasi and Japan's Jellice) and Ashok Matches & Timbers completed the acquisition of Narmada Gelatines Ltd in two phases. Through this acquisition, the Sivakasi-based promoters gained complete ownership of Narmada Gelatines, a manufacturer of gelatines for pharmaceutical, food, industrial, and photographic applications, as well as di-calcium phosphate.

- March 2023: GELITA introduced CONFIXX®, a starch-free gelatin formulation that accelerates fortified gummy production. The product enables rapid setting at low temperatures, reducing production time from two days to several hours while maintaining the desired gummy texture. CONFIXX® eliminates the need for starch molds, preparation, and drying steps, which reduces space requirements, energy consumption, and contamination risks between production batches

India Gelatin Market Report Scope

Gelatin is an animal-based product and a common ingredient in soups, broths, sauces, gummy candies, marshmallows, cosmetics, and medications.

The Indian gelatin market is segmented by form as animal-based and marine-based. By end-users such as personal care and cosmetics and food and beverages, further food and beverages are sub-segmented bakery, beverages, condiments/sauces, confectionery, dairy, and dairy alternative products, RTE/RTC food products snacks.

For each segment, the report offers the market size in value terms in USD and in volume terms in tons for all the abovementioned segments.

By Source

| Animal-Based |

| Marine-Based |

By Grade

| Food Grade |

| Phamaceutical Grade |

By End-User

| Personal Care and Cosmetics | |

| Food and Beverages | Bakery |

| Beverages | |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| RTE/RTC Food Products | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Others |

| By Source | Animal-Based | |

| Marine-Based | ||

| By Grade | Food Grade | |

| Phamaceutical Grade | ||

| By End-User | Personal Care and Cosmetics | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| RTE/RTC Food Products | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Others | ||

Key Questions Answered in the Report

How large is the Gelatin market in India in 2026?

The Gelatin market size stands at USD 307.97 million in 2026 and is projected to reach USD 438.03 million by 2031.

Which source segment is growing fastest?

Marine-based gelatin is forecast to expand at a 7.70% CAGR due to religious neutrality and sustainability appeal.

What grade is expected to see the highest CAGR?

Pharmaceutical-grade gelatin is projected at a 7.82% CAGR, supported by India’s expanding generic drug manufacturing.

Which end-user drives the fastest demand growth?

Dietary supplements lead with an 8.06% CAGR as wellness spending accelerates.

Page last updated on: