Scotch Whisky Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 58.78 Billion |

| Market Size (2031) | USD 73.63 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

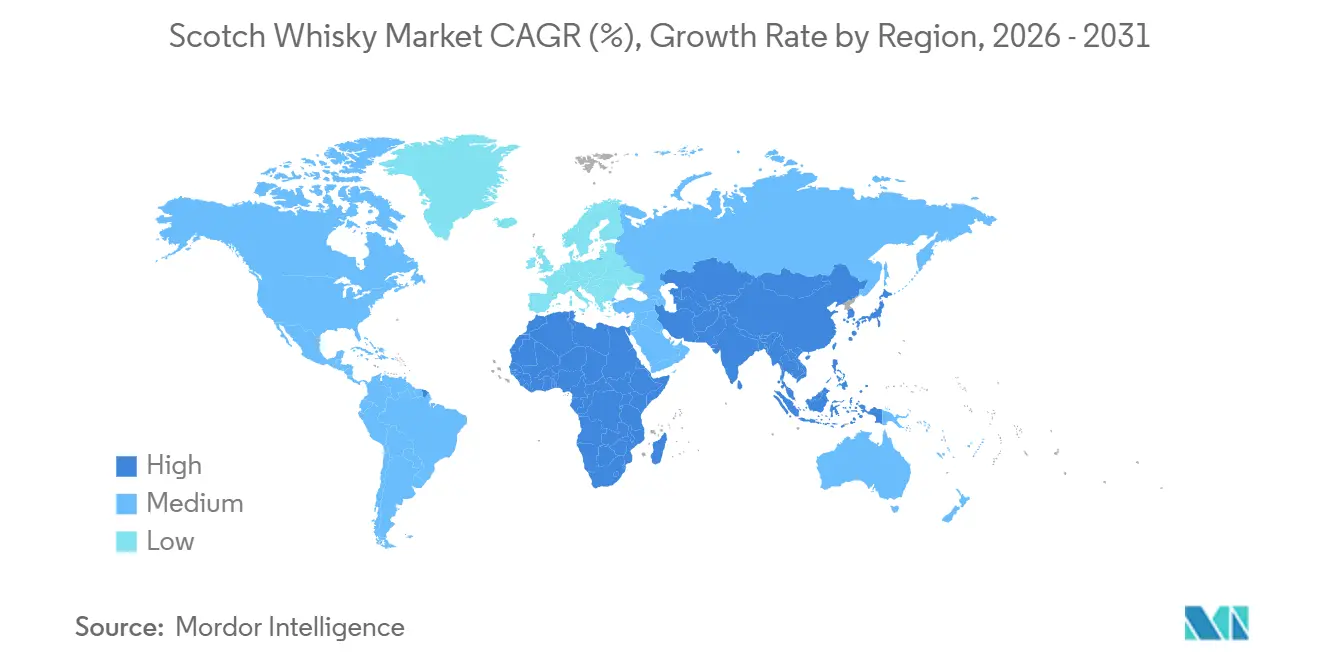

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

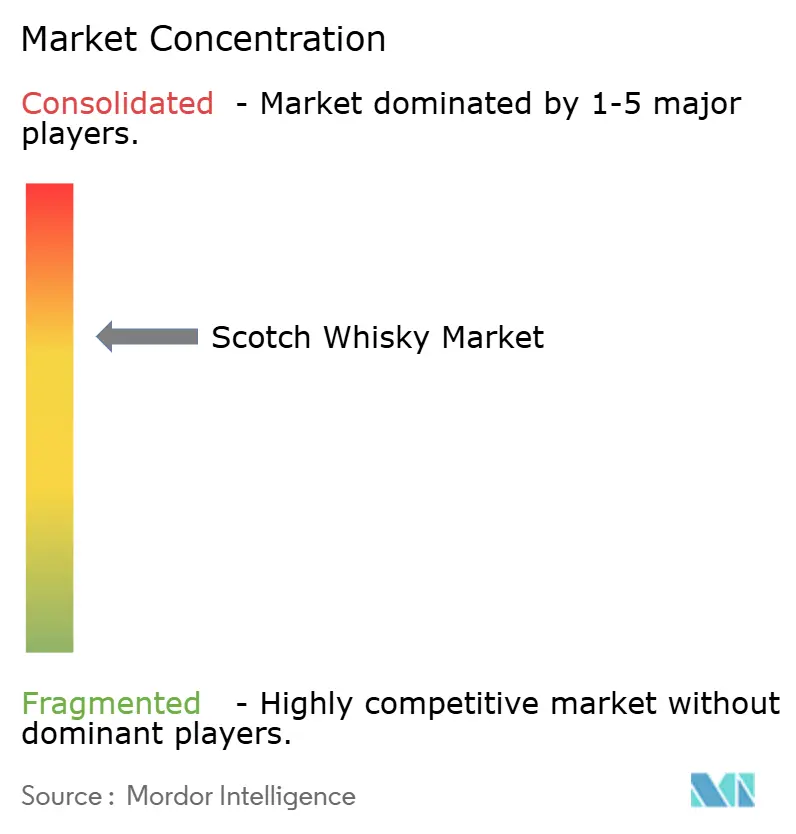

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Scotch Whisky Market Analysis by Mordor Intelligence

The scotch whisky market size was valued at USD 56.51 billion in 2025 and is estimated to grow from USD 58.78 billion in 2026 to reach USD 73.63 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031). The global demand for Scotch whisky has increased due to growing consumer preference for premium and luxury spirits. Consumers are choosing high-quality, authentic spirits with established heritage, making Scotch whisky a prominent choice in the premium alcoholic beverages market. This trend is notable in emerging markets, where increased disposable incomes enable consumers to purchase premium spirits. The popularity of whisky-based cocktails has created new consumption opportunities and attracted younger consumers, especially millennials seeking distinctive drinking experiences. Growth in 2026 reflects consistent premium adoption, stronger digital sales models, and resilient brand equity that supports pricing power across channels.

Key Report Takeaways

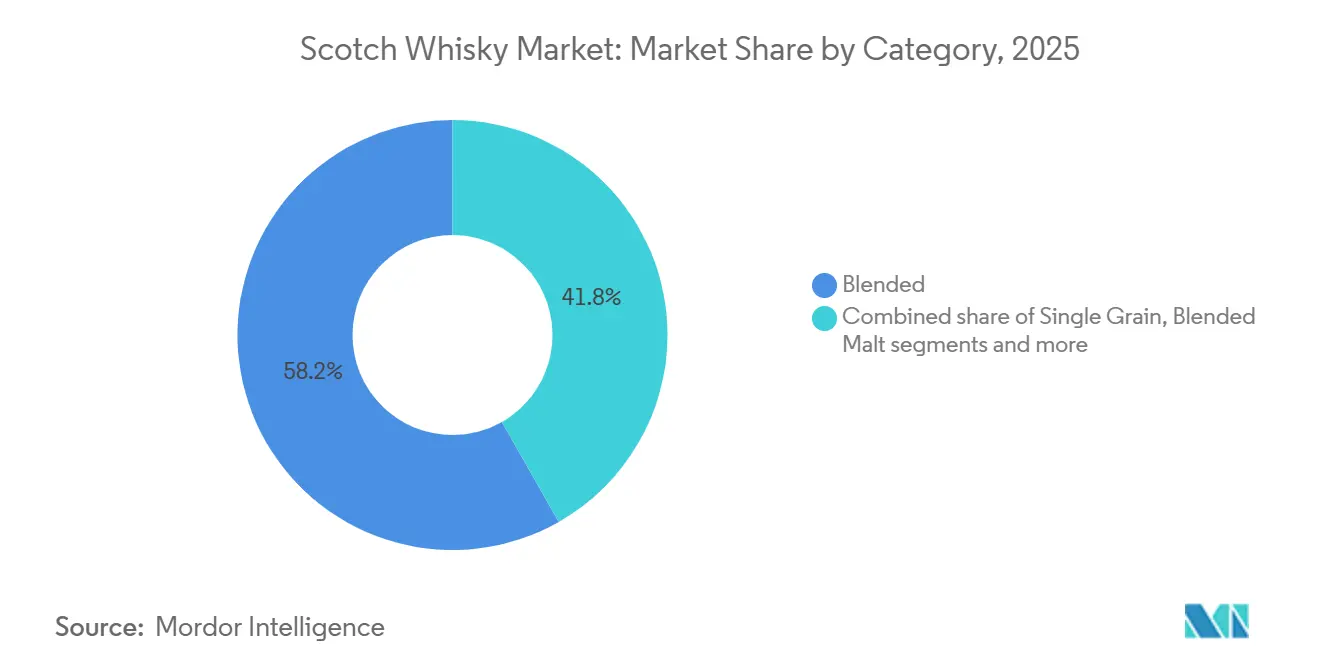

- By category, blended Scotch led with 58.23% revenue share in 2025, while single malts are projected to grow at a 5.55% CAGR through 2031.

- By age, 12–15 years held 40.07% share in 2025, while whiskies aged below 24 years are forecast to advance at a 5.21% CAGR to 2031.

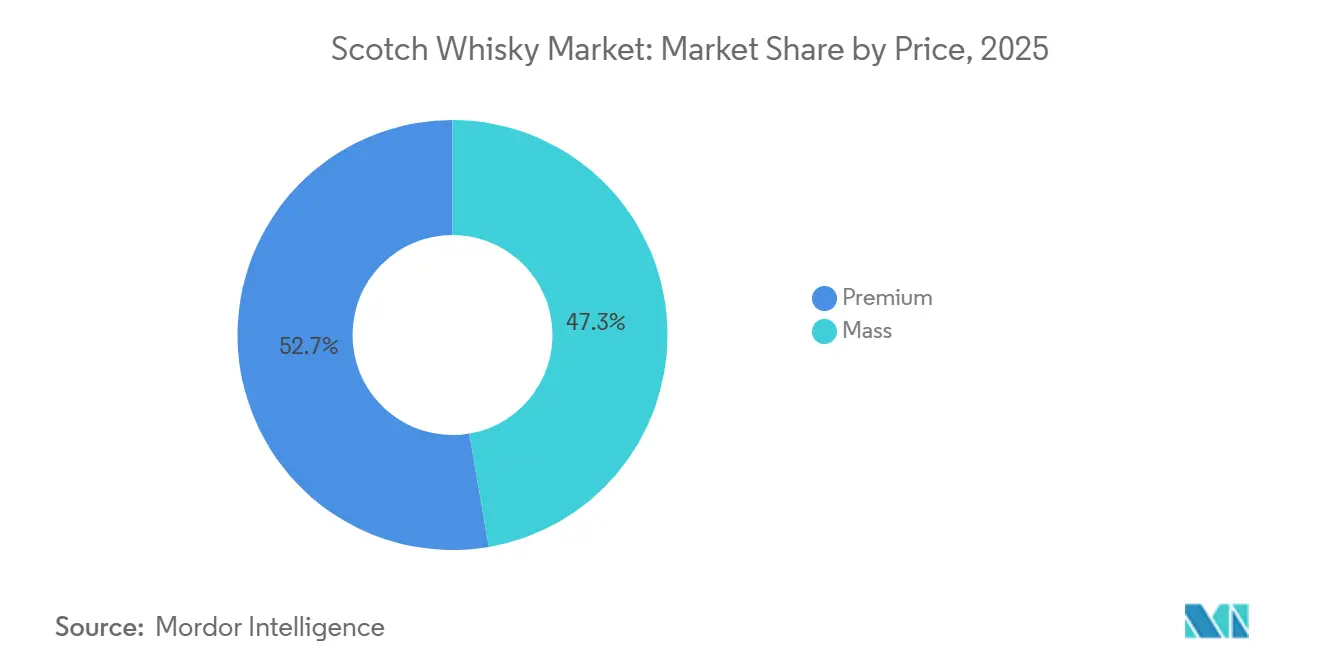

- By price, mass is at 47.31% share in 2025, while premiums are forecast to advance at a 6.76% CAGR to 2031.

- By distribution channel, off-trade accounted for 61.29% of the Scotch whisky market size in 2025, while on-premise is projected at a 4.98% CAGR through 2031.

- By geography, the Asia Pacific held 32.04% of the Scotch whisky market share in 2025, while the Middle East and Africa recorded the fastest projected growth at 5.29% CAGR for 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Scotch Whisky Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and luxury positioning | +1.2% | Global, with concentration in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising demand for single malt and craft expressions | +0.8% | Global, particularly strong in Asia-Pacific and North America | Long term (≥ 4 years) |

| Expansion of e-commerce and DTC logistics | +0.5% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Product innovation and flavors | +0.4% | Global, with focus on developed markets | Medium term (2-4 years) |

| Whisky tourism and experiential offerings | +0.3% | Scotland, with spillover to global markets | Long term (≥ 4 years) |

| Influence of cocktail culture and on-premise trends | +0.2% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and luxury positioning

Premium assortments gain traction as consumers seek provenance, aged statements, and limited releases that carry stronger pricing power and brand storytelling. This tilt supports higher average tickets in travel retail and flagship venues, where curated ranges and giftable formats lift value outcomes for the Scotch whisky market. Diageo exemplified this approach by establishing the Diageo Luxury Group in November 2024, consolidating spirits priced above USD 100 under one strategic unit. This restructuring allows targeted investment in ultra-premium offerings, including Johnnie Walker's Vault, which provides custom blending services starting at GBP 50,000. The luxury market has expanded beyond traditional consumption into investment opportunities, particularly through whisky cask ownership. The premium spirits segment's potential is demonstrated by American whisky market data, where high-end and premium brands recorded 274% revenue growth since 2003, while super-premium brands grew by 2,150% [1]Source: Distilled Spirits Council, “American Whiskey Category Fact Sheet” distilledspirits.org. This shift toward premium offerings helps companies offset regulatory costs while building long-term value in wealthy consumer segments.

Rising demand for single malt and craft expressions

Single malts are set to grow faster than the category baseline as consumers favor clear provenance, distillery identity, and cask nuance over price-led propositions. The Scotch whisky market channels that demand through tasting flights, bartender guidance, and specialist retail that reduces choice overload and guides shoppers toward signature malts. Younger legal drinking age adults in 2026 are expected to show stronger engagement with beverage alcohol than in 2023, which broadens the addressable base for entry to premium malts and builds confidence to explore cask finishes over time. As education improves and online content deepens category knowledge, buyers move more fluidly between accessible malts and higher-end releases, which sustains the mix upgrade within the Scotch whisky market. This reinforces a portfolio strategy that balances volume blends with targeted single malt expansion where urban demand is concentrated.

Expansion of e-commerce and DTC logistics

Digital commerce is transforming direct-to-consumer relationships in the scotch whisky market, enabling companies to increase profit margins while building customer databases. Diageo implemented this approach through its FlavorPrintConnect technology on Malts.com, which combines physical whisky tasting kits with AI-powered digital masterclasses for personalized customer experiences. The UK's revised alcohol duty system, introducing digital approval processes and unified digital returns in March 2025, supports e-commerce channel expansion [2]Source: GOV.UK, "Draft regulations: The Alcoholic Products (Excise Duty) (Amendment) Regulations 2024," gov.uk. In markets with complex distribution networks, direct-to-consumer models help companies maintain price control and direct customer relationships. Companies are implementing blockchain and AI-powered verification systems for product authentication to prevent counterfeiting. The e-commerce channel continues to grow as consumers, especially younger demographics, seek convenient and personalized experiences through digital platforms and subscription services.

Product innovation and flavors

Innovation pipelines now balance tradition with contemporary cues to recruit new drinkers into the Scotch whisky market. Johnnie Walker introduced Black Cask, a permanent expression aged exclusively in American white oak ex-bourbon barrels, which is designed to meet crossover palates while reinforcing Scotch identity and quality cues. Cultural partnerships and content programs align launches with on-premise serves and social discovery, which supports education and lowers barriers to trial among younger legal drinking age audiences. As brands refine cask finishes, small batch releases, and giftable formats, innovation acts as a bridge from accessible blends into the premium ladder within the Scotch whisky market. This approach sustains value growth while preserving heritage, letting producers scale range relevance across retail and hospitality in 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile excise duties and trade tariffs | -0.9% | Global, with particular impact on UK-US and UK-India trade | Short term (≤ 2 years) |

| Competition from other spirits | -0.6% | Global, with intensity varying by region | Medium term (2-4 years) |

| Counterfeiting and Illicit Trade | -0.4% | Global, with concentration in emerging markets | Long term (≥ 4 years) |

| Environmental and sustainability pressures | -0.3% | Global, with stricter requirements in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile excise duties and trade tariffs

The Scotch whisky market faces significant regulatory challenges, primarily through tax policy changes that affect consumer pricing and demand. The United Kingdom's recent double-digit tax increase on Scotch whisky led to decreased sales volumes and resulted in daily revenue losses of over GBP 500,000 for the United Kingdom Exchequer [3]Source: The Scotch Whisky Association, "Treasury has lost half a million pounds a day since double digit tax hike on Scotch," scotch-whisky.org.uk. The potential reimposition of 25% United States tariffs on Scotch whisky within 18 months creates additional uncertainty for the industry's primary export market. However, the UK-India Free Trade Agreement presents growth opportunities by reducing import duties from 150% to 75% initially, followed by a further reduction to 40% over ten years. Companies are responding to these regulatory uncertainties by implementing adaptable pricing strategies and expanding their market presence across multiple regions. Travel retail and on-premise discovery help maintain premium momentum despite policy noise, since occasion-based buying supports willingness to trade up in curated environments in 2026.

Competition from other spirits

The spirits market's fragmentation intensifies competition for consumer spending across gin, vodka, and rum categories, with companies using product innovation and marketing to gain market share. Competition is strong in the cocktail segment, where both bartenders and consumers experiment with various spirits, which may reduce whisky's prominence in premium mixed drinks. Regional preferences present additional challenges, as local spirits maintain cultural significance that imported Scotch whisky must address. The market dynamics are further shaped by the growth of local whisky production in key markets, particularly in India and Japan, where domestic distilleries create products that align with national identity and local tastes. Younger adult engagement with beverage alcohol has risen in 2026 compared with 2023, and that exploration can favor simple, flavored, or lower ABV serves unless Scotch meets drinkers with guidance and approachable styles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Single Malt Drives Premium Evolution

Blended Scotch commanded 58.23% of the Scotch whisky market share in 2025, reflecting the breadth of distribution, affordability, and brand familiarity across large retail and on-trade networks. The category's strength lies in its ability to offer consistent quality across various price points, from entry-level to premium expressions, making it accessible to a diverse consumer base across global markets. Single malt Scotch whisky is projected to grow at a 5.55% CAGR during 2026-2031, driven by increasing consumer sophistication and willingness to explore premium offerings. This growth is supported by substantial investments in production capacity, aging facilities, and specialized distillation processes, enabling distilleries to meet the rising demand for high-quality single malt expressions.

Single grain Scotch whisky holds a distinctive position in the spirits industry, primarily serving as a crucial component in blended whisky expressions. There's a growing consumer awareness and appreciation for the craftsmanship involved in whisky production, leading to increased interest in various whisky categories, including Single Grain Scotch. The market is also benefiting from the premiumization trend, where consumers demonstrate a willingness to invest in authentic, high-quality spirits. The segment's growth is further supported by its versatility in blending, making it an essential ingredient for master blenders creating premium blended Scotch whiskies.

By Age: Ultra-Premium Maturation Commands Growth

The 12–15 years band held 40.07% of 2025 consumption, a middle ground that travels well across channels and serves as a familiar entry point in the Scotch whisky market. This category maintains a stable supply through established production cycles and effective inventory management, enabling consistent market availability to meet consumer demand. The below 12 Years category functions as an entry point for new consumers and price-sensitive buyers, while the 16-20 Years segment targets dedicated enthusiasts seeking extended maturation profiles. The 21-30 Years category focuses on collectors and special occasion purchases, with limited availability supporting premium pricing.

Whiskies aged below 24 years are forecast to expand at 5.21% CAGR through 2031, helped by cocktail adoption and bartender recommendations that favor flavor profiles built for mixing and flights. The growth in this segment demonstrates whisky's emergence as an alternative investment asset, though investors face potential risks due to regulatory uncertainties in cask ownership. The age segmentation distribution reflects historical production limitations, prompting companies to increase production capacity to address future demand for aged expressions.

By Price: Luxury Segment Accelerates Despite Challenges

Premium ranges continue to gain share of attention at 6.76% CAGR as consumers respond to provenance, cask finishes, and curated experiences that justify higher price points in the Scotch whisky market. Range architecture makes the journey clear with good, better, best tiers and visible finish types, helping shoppers rationalize trading up without losing trust in familiar entries. E-commerce amplifies premium discovery by showcasing limited releases, gifting packs, and brand content that deepen understanding and accelerate confident purchases in 2026. On-premise also supports premium momentum through tasting flights and bartender-led serves that translate into off-trade repeats and online subscriptions within the Scotch whisky market.

Mass tier blends remain essential in reach and frequency terms at 47.31% in 2025, yet they now coexist with a premium ladder that strengthens category value without displacing core volume. As inflation and policy changes influence shelf prices, value-added packs and education help maintain satisfaction while protecting mix upgrades in the Scotch whisky market. Portfolio owners focus on clarity and consistency across channels so that exploration does not overwhelm shoppers or fragment brand equity at the shelf or back bar in 2026.

By Distribution Channel: Travel Retail Rebounds Strongly

Off-trade channels hold a dominant 61.29% market share in 2025, primarily through retail outlets such as supermarkets, liquor stores, and others. This dominance stems from consumer preferences for home consumption and the convenience of purchasing whisky alongside regular grocery shopping. The off-trade segment leverages promotional activities, including seasonal discounts and bundle offers, while also developing private label opportunities through retailer-specific brands. Additionally, on-trade channels, comprising bars, restaurants, and hotels, facilitate experiential consumption through cocktail offerings and premium whisky tastings, while serving as crucial platforms for introducing new products to consumers. The performance of on-trade distribution closely aligns with hospitality industry trends and social dining behaviors.

On-trade is set to grow at a 4.98% CAGR to 2031, leveraging cocktails, half serves, and curated lists that make Scotch more accessible and help premium expressions secure placements and higher value occasions in 2026. The channel benefits from travelers' willingness to purchase authentic Scottish products at higher price points, enabling better profit margins and brand development opportunities. The integration of digital services, such as pre-ordering and collection facilities, improves the shopping experience. The channel demonstrates resilience through its adaptation to evolving travel patterns and consumer preferences.

Geography Analysis

Asia-Pacific holds the largest market share at 32.04% in 2025, primarily due to China's expanding whisky market. The region's market position stems from increasing disposable incomes, rapid urbanization, and evolving consumer preferences toward Western spirits. Japan's mature whisky market creates a natural pathway for Scotch whisky adoption, while India presents substantial growth opportunities despite existing tariff restrictions. Australia and South Korea maintain consistent demand, and emerging economies such as Indonesia and Thailand demonstrate growth potential as their markets develop.

The Middle East and Africa region is projected to grow at 5.29% CAGR during 2026-2031, supported by middle-class population growth and enhanced distribution networks. The region's expansion reflects economic progress and evolving attitudes toward alcohol consumption in markets where it is permitted. South Africa dominates regional consumption, while the United Arab Emirates functions as the primary distribution center for the Middle East. In addition, South America demonstrates consistent growth prospects, with Brazil's large consumer base and strengthening economy driving the market, while Argentina and Chile develop premium market segments.

Europe remains a key market for Scotch whisky due to its historical significance, established consumer base, and cultural affinity for aged spirits. The region's traditional appreciation for Scotch whisky is evident through its extensive distribution networks, premium positioning in retail outlets, and strong presence in both on-trade and off-trade channels. European consumers demonstrate sophisticated preferences for single malts and aged blends, supported by well-established tasting clubs and whisky societies. However, the region faces regulatory challenges, including changes in labeling requirements, taxation policies, and trade agreements that impact market dynamics.

Competitive Landscape

The Scotch whisky market exhibits high concentration, indicating significant consolidation opportunities while maintaining competitive dynamics. Global portfolios with multi-tier offerings maintain distribution scale and shopper marketing reach, while a long tail of independents adds provenance stories and specialist releases that keep the category dynamic in the Scotch whisky market. Portfolio owners align range ladders from high volume blends into single malts and limited runs, using education and curated assortments to guide shoppers up the value curve in 2026. This balanced model defends share and supports pricing integrity when cost pressures or policy changes add noise to the baseline. Consistent execution across retail, e-commerce, and on-premises keeps awareness high and protects conversion pathways within the Scotch whisky market.

Recent brand actions show how leaders connect innovation with audience reach. Johnnie Walker launched Black Cask as a permanent expression aged exclusively in American white oak ex-bourbon barrels, aligning with crossover palates without losing Scotch craftsmanship cues that matter for credibility. The brand also entered a multi-year collaboration with a global music artist to modernize rituals and cocktail serves, using content and on-premise activations to engage younger legal drinking age adults who are exploring spirits categories in 2026. These examples reflect a broader shift toward integrated experiences and storytelling that strengthens premium intent across the Scotch whisky market.

Technology integration emerges as a key differentiator, with companies leveraging AI and digital platforms to enhance consumer experiences and operational efficiency. Innovation extends to sustainability initiatives, with manufacturers investing in renewable energy and lightweight packaging to address environmental pressures while maintaining product quality. White-space opportunities exist in emerging markets and direct-to-consumer channels, where regulatory changes enable new business models. The competitive landscape reflects a balance between established heritage brands and innovative approaches to consumer engagement, with success requiring both authenticity and adaptability to changing market conditions.

Scotch Whisky Industry Leaders

-

Diageo plc

-

Edrington Group

-

Pernod Ricard S.A.

-

Bacardi Limited

-

William Grant & Sons Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: William Grant's acquired The Famous Grouse and Naked Malt, marking a significant consolidation move in the blended Scotch whisky segment. This acquisition strengthens William Grant's portfolio and market position in the competitive blended category.

- March 2025: Johnnie Walker launched the Vault experience, offering bespoke Scotch whisky blending services starting at GBP 50,000, targeting ultra-high-net-worth individuals seeking personalized luxury experiences. The initiative represents a new frontier in luxury spirits positioning and experiential marketing.

- November 2024: Diageo launched FlavorPrintConnect technology, combining whisky tasting kits with AI-enhanced digital masterclasses to create personalized consumer experiences. The platform reflects innovation in direct-to-consumer engagement and digital marketing.

- October 2024: Johnnie Walker introduced AI-powered bottle designs in collaboration with artist Andy Gellenberg, producing 5,000 unique collectible designs exclusively for the German market. This initiative demonstrates technology integration in product personalization and marketing.

Global Scotch Whisky Market Report Scope

Scotch whisky is a distilled spirit made from water, malted barley, and optional cereal grains, fermented with yeast. The Scotch Whisky Market is Segmented by Category (Single Malt, Single Grain, Blended Malt, and More), Age Statement (Below 12 Years, 12-15 Years, 16-20 Years, 21-30 Years, Over 30 Years), Price (Mass and Premium), Distribution Channel (Off-Trade, On-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single malt |

| Single grain |

| Blended malt |

| Blended grain |

| Blended |

| Below 12 years |

| 12–15 years |

| 16–20 years |

| 21–30 years |

| Over 30 years |

| Mass |

| Premium |

| Off-trade |

| On-trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Category | Single malt | |

| Single grain | ||

| Blended malt | ||

| Blended grain | ||

| Blended | ||

| By Age | Below 12 years | |

| 12–15 years | ||

| 16–20 years | ||

| 21–30 years | ||

| Over 30 years | ||

| By Price | Mass | |

| Premium | ||

| By Distribution Channel | Off-trade | |

| On-trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Scotch whisky market?

TThe Scotch whisky market size is USD 56.51 billion in 2025 and is projected to reach USD 73.63 billion by 2031 at a 4.61% CAGR during 2026–2031.

Which geographic region leads Scotch whisky sales?

Asia-Pacific leads with 32.04% of global value in 2025, driven mainly by China’s rapid adoption of premium whisky.

What category is growing fastest within Scotch?

Single malt Scotch whisky is expanding at a projected 5.55% CAGR through 2031 as consumers seek authenticity and craft credentials.

What recent developments illustrate brand strategies in Scotch?

Johnnie Walker launched Black Cask and formed a multi-year artist partnership to modernize rituals and engage new audiences across digital and on-premise platforms.

Page last updated on: