Champagne Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 19.53 Billion |

| Market Size (2031) | USD 24.75 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

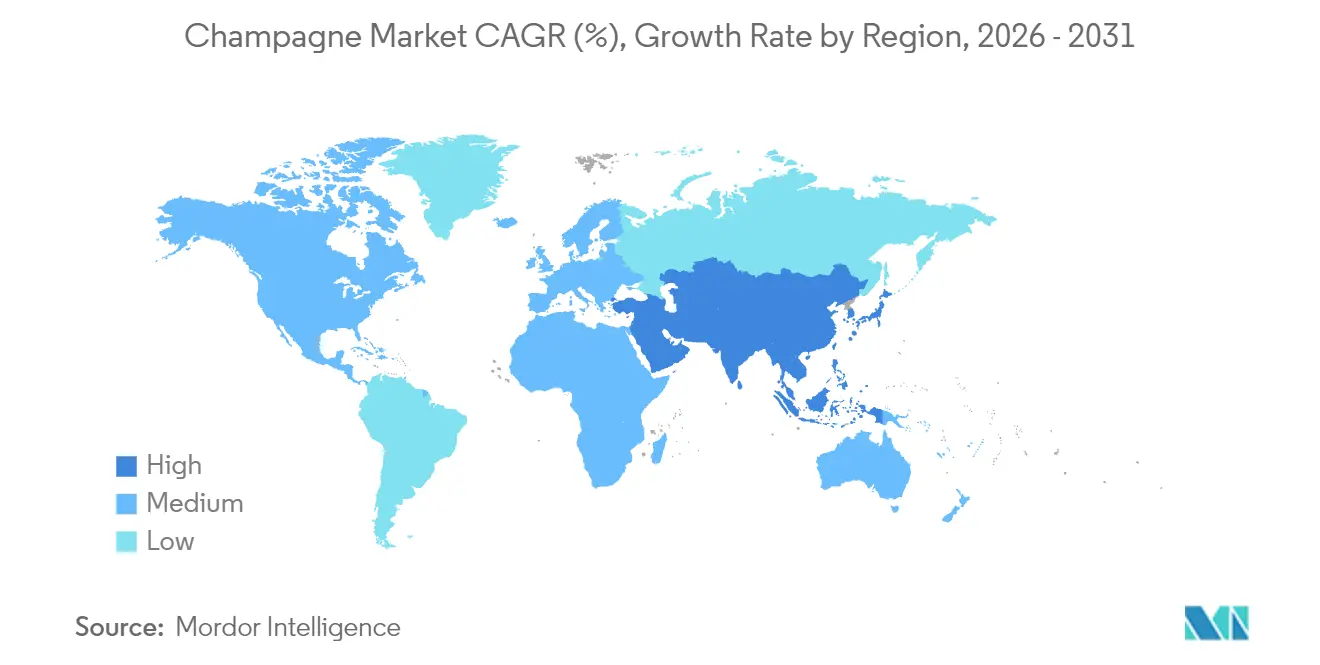

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Champagne Market Analysis by Mordor Intelligence

champagne market size in 2026 is estimated at USD 19.53 billion, growing from 2025 value of USD 18.63 billion with 2031 projections showing USD 24.75 billion, growing at 4.85% CAGR over 2026-2031. Even as overall shipment volumes stabilize, trends like premiumization, climate-smart viticulture, and a resilient demand for luxury continue to drive value expansion. Europe, bolstered by its deep-rooted celebratory culture and stringent AOC protections, maintains its leadership. In contrast, the Asia Pacific region experiences steady growth, fueled by a burgeoning middle class, lively tourism, and the tradition of gifting as a social status symbol. On the supply side, vigilance against spring frost and mildew episodes keeps inventories in check. This discipline allows for price increases that counterbalance rising costs. Additionally, tools for digital authentication and limited editions tied to NFTs not only bolster brand integrity but also unveil new revenue streams. Brands that weave heritage storytelling with sustainable practices and immersive marketing enjoy heightened consumer loyalty.

Key Report Takeaways

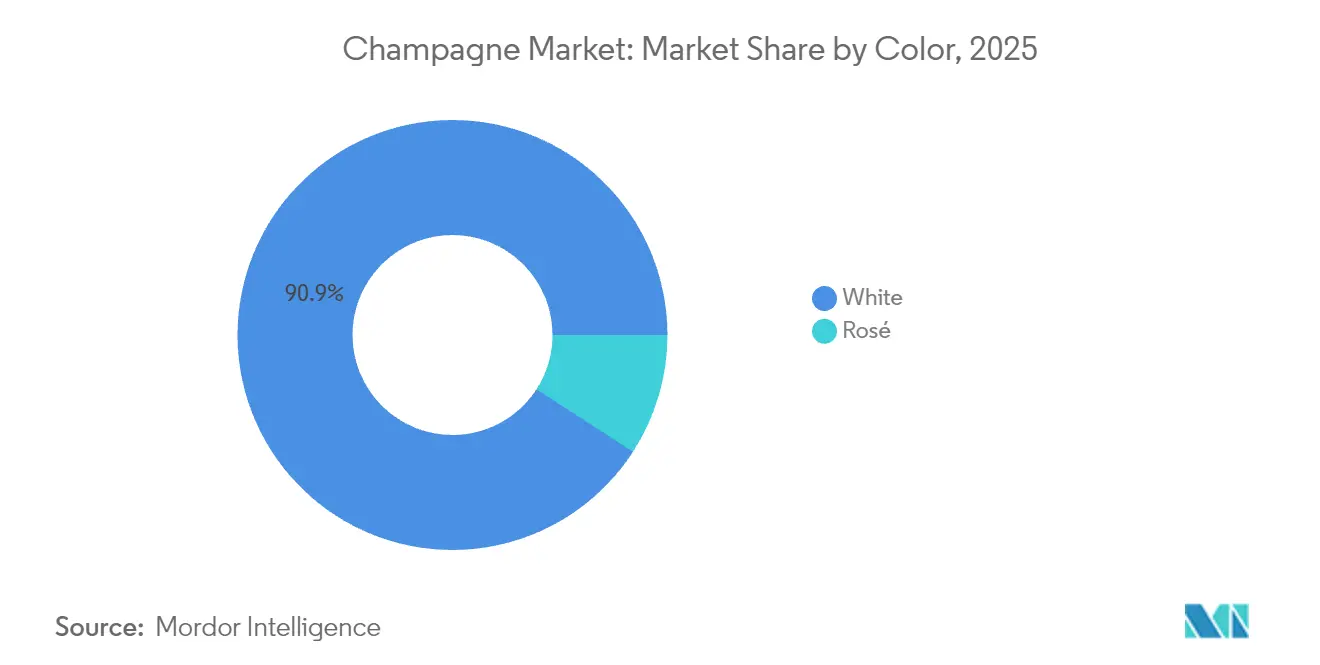

- By color, white champagne led with 90.86% of the champagne market share in 2025, whereas rosé is projected to expand at a 5.61% CAGR through 2031.

- By sweetness level, Brut captured 78.88% of 2025 revenue, while Extra Brut is the fastest climber at a 6.05% CAGR to 2031.

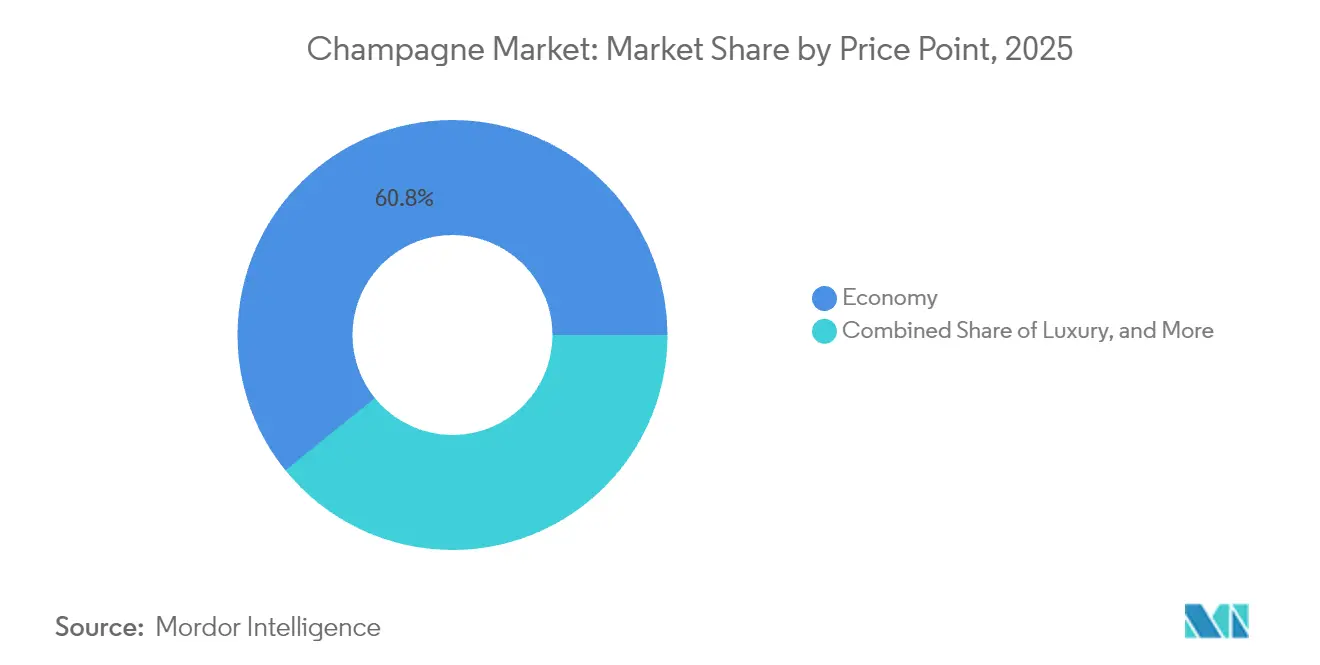

- By price point, economy labels held 60.84% of value in 2025; the ultra-luxury tier is forecast to post an 7.84% CAGR during the outlook.

- By packaging size, the 750 ml standard bottle accounted for 71.78% of shipments in 2025, whereas magnum and larger formats are advancing at a 7.37% CAGR.

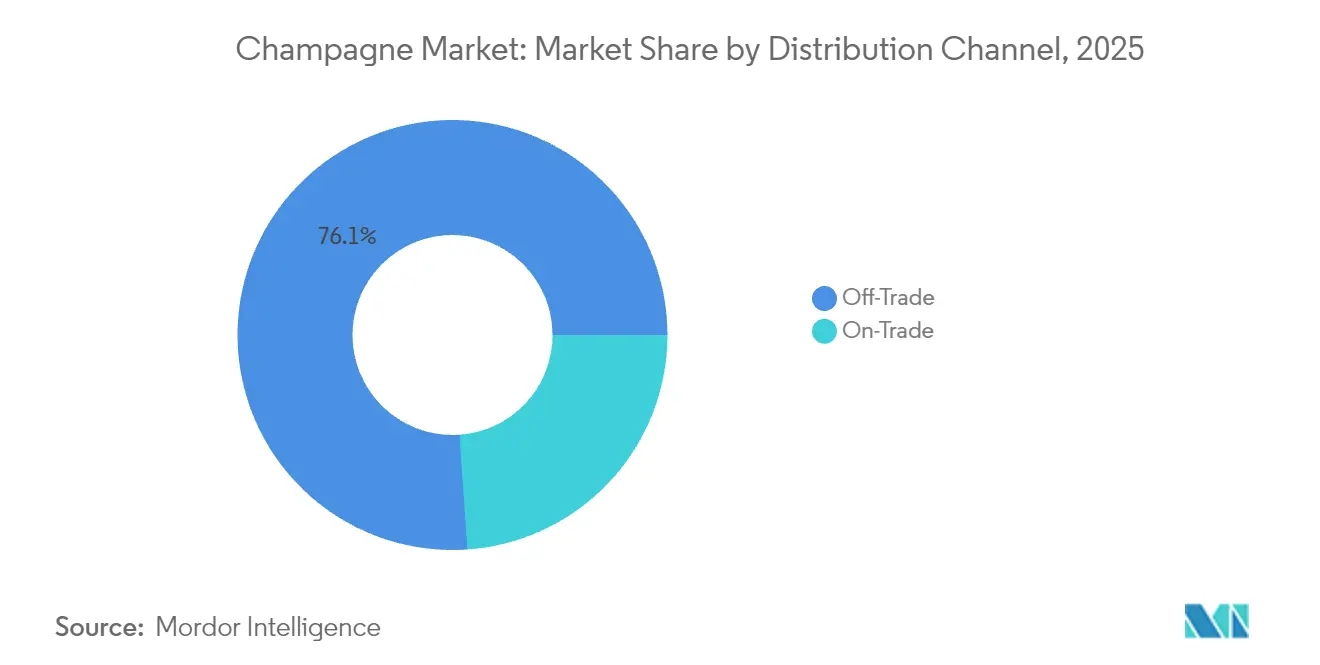

- By distribution, off-trade outlets controlled 76.11% of 2025 sales, but on-trade venues are poised for a 6.86% CAGR as tourism-led experiential drinking rebounds.

- By geography, Europe commanded a 58.01% revenue share in 2025, while the Asia Pacific is on track for a 6.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Champagne Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and luxury positioning of celebratory culture | +1.2% | Global, with strongest impact in North America and Asia Pacific | Medium term (2-4 years) |

| Product innovation and new flavor profiles | +0.8% | Europe and North America core, expanding to Asia Pacific | Short term (≤ 2 years) |

| Growing demand for low-dosage "Brut Nature/Extra Brut" styles | +0.6% | North America and Europe, emerging in Asia Pacific urban centers | Medium term (2-4 years) |

| Innovation in sustainable viticulture and carbon-neutral wineries | +0.4% | Global, with regulatory influence strongest in Europe | Long term (≥ 4 years) |

| Wine tourism and experiential consumption | +0.7% | Europe core, expanding to Asia Pacific and North America | Short term (≤ 2 years) |

| NFT-backed limited-edition cuvées creating new revenue streams | +0.3% | Global luxury markets, concentrated in North America and Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization and luxury positioning of celebratory culture

In a notable pivot, the champagne industry is prioritizing premiumization, mirroring shifts in global consumer behavior that now favor value creation over sheer volume. LVMH's champagne division epitomizes this trend, reporting revenue growth fueled by strategic price hikes, especially in Europe and Japan. This comes even as volumes dipped from 70.9 million bottles in 2022 to 61.7 million in 2024, as highlighted by LVMH[1]Source: LVMH, “Key Figures,” lvmh.com. But premiumization isn't just about price; it's about crafting an experience. Champagne houses are delving into heritage storytelling and rolling out exclusive access programs. Take Veuve Clicquot, for instance. They're honing in on their La Grande Dame prestige cuvée, blending modern imagery to allure younger consumers while steadfastly upholding traditional quality, as noted by Formes de Luxe. The ultra-luxury segment's projected 8.25% CAGR through 2030 underscores this strategy's validity. Today's consumers are increasingly perceiving champagne not just as a drink, but as a savvy investment in social capital. Adding fuel to this trend, France welcomed a record 100 million international tourists in 2024, raking in a staggering EUR 71 billion. This influx, as reported by Campus France, is not just a boon for the economy but a golden opportunity, immersing global visitors in genuine champagne experiences[2]Source: Campus France, “Record Year for International Tourism,” campusfrance.org.

Product innovation and new flavor profiles

Champagne producers are pushing traditional boundaries while adhering to AOC constraints, crafting unique offerings that resonate with shifting consumer tastes. The debut of Voltis, a hybrid grape variety engineered to resist downy and powdery mildew, underscores the industry's proactive stance on climate challenges. However, strict regulations cap its vineyard allocation at 5% and blending at 10%. Sustainability is at the forefront, with champagne houses boasting over 70% environmental certification under the Sustainable Viticulture in Champagne (VDC) framework, eyeing a 100% target by 2030, as highlighted by The Comité Champagne. Packaging is also evolving; Veuve Clicquot has slashed its packaging volume by 40% since 2019 and is experimenting with sustainable materials, such as hemp, for its premium offerings, as reported by Formes de Luxe. These strides not only tackle the twin challenges of climate adaptation and rising consumer sustainability demands but also uphold the exclusivity that champagne is renowned for. Meanwhile, the rosé segment, with a 5.82% CAGR, showcases successful innovations in color and style, resonating with younger audiences while staying true to traditional craftsmanship.

Growing demand for low-dosage "Brut Nature/Extra Brut" styles

As consumers become more discerning and health-conscious, there's a noticeable shift towards low-dosage champagne styles, emphasizing authenticity over mere sweetness. With a projected CAGR of 6.34% through 2030, Extra Brut is outpacing the traditional Brut segment, signaling a pivotal change in the palate of consumers who cherish the true essence of terroir. This movement resonates with Bain & Company’s broader "drink better" ethos, where quality trumps quantity in alcoholic choices, as highlighted by Formes de Luxe. Achieving low-dosage styles demands top-tier grapes and meticulous winemaking, since any flaws become evident without the cover of added sugar, further cementing champagne's premium status. Mature markets, especially North America and Europe, are witnessing this trend, bolstered by a robust wine education that fosters an appreciation for intricate flavor nuances. In Japan, where 40% of sparkling wine imports are French champagne, there's a growing preference for these refined styles, a sentiment echoed by Kirin Holdings, noting a tripling of wine consumption since 1989. This shift positions low-dosage champagnes as the entry point for premium wine enthusiasts moving from still to sparkling varieties.

Innovation in sustainable viticulture and carbon-neutral wineries

Champagne producers are elevating sustainability initiatives from mere regulatory compliance to key competitive differentiators, appealing to both eco-conscious consumers and institutional buyers. The Champagne region, with a goal of achieving 100% environmental certification by 2030, has already seen over 60% of its vineyards certified under esteemed frameworks like Sustainable Viticulture in Champagne (VDC) and ISO 14001, signaling a significant industry-wide shift, as highlighted by The Comité Champagne[3]Source: Champagne.fr, “Objective 100% Certified,” champagne.fr. In a bid to adapt to climate challenges, the region conducts over 200 annual trials in viticulture and oenology, striving for eco-friendly practices without compromising on quality, as noted by Comité Champagne. The Champagne industry is not just reacting but proactively gearing up for climate challenges. They've introduced temperature monitoring systems and spatial analysis tools, refining vineyard management in the face of shifting climatic conditions, according to HAL Science. Over the past 15 years, the industry has notably cut down on chemical usage, all while upholding production quality, underscoring its commitment to reducing the carbon footprint across the value chain. These sustainability endeavors not only safeguard production amidst climate uncertainties but also resonate with ESG-minded investors and consumers, who are increasingly prioritizing environmental considerations in their purchasing choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening advertising regulations on alcohol in key markets | -0.8% | Global, with strongest impact in Europe and Asia Pacific | Medium term (2-4 years) |

| Supply-side pressure from climate-induced grape yield volatility | -1.1% | Global production regions, concentrated in Europe | Long term (≥ 4 years) |

| Regulatory and appellation constraints | -0.5% | Europe core, affecting global expansion strategies | Long term (≥ 4 years) |

| Widespread counterfeiting and brand dilution | -0.7% | Global, with highest impact in Asia Pacific and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening advertising regulations on alcohol in key markets

Major champagne markets are tightening advertising restrictions, limiting brand visibility, and making it harder to attract consumers. This is especially true for digital marketing, which is crucial for engaging younger audiences. Stricter alcohol advertising rules in key European markets are not only curbing traditional promotional avenues but also driving up compliance costs for global champagne brands. In response, these brands are shifting towards experiential marketing and influencer collaborations, both of which demand a heftier investment for each consumer interaction than conventional advertising. The situation is even more pronounced in the Asia Pacific region, where countries have vastly different regulatory frameworks. This disparity creates a challenging compliance environment, benefiting larger champagne houses with the means to navigate legal complexities, while smaller producers struggle. Additionally, restrictions on digital platforms for alcohol advertising pose hurdles for market entry, especially for premium brands aiming to reach affluent younger audiences on social media. As the regulatory landscape increasingly emphasizes health concerns, it poses long-term challenges for the growth of the champagne category. With diminished advertising exposure, there's a risk of stunted brand discovery and fewer opportunities for premiumization in emerging markets, where champagne consumption habits are still evolving.

Supply-side pressure from climate-induced grape yield volatility

Champagne production stability faces a fundamental threat from climate change, as increased weather volatility directly impacts grape yields and quality consistency. The Comité Champagne reports a drop in the 2024 harvest yield to 10,000 kg/ha, down from 11,400 kg/ha in 2023, highlighting the immediate supply constraints caused by spring frosts and mildew pressure. Adverse climatic conditions led to an 18% decline in France's overall wine production in 2024, with champagne seeing a 16% dip. This created supply-demand imbalances, putting pressure on pricing strategies, according to OH Beverage. Research on climate resilience reveals that champagne regions are particularly vulnerable. This vulnerability stems from the legal rigidity of AOC regulations, which limit adaptation strategies, such as introducing new grape varieties or changing cultivation techniques, as noted by Nature Communications. In response, the industry is conducting over 200 annual trials and developing climate-adapted grape varieties like Voltis. However, the regulatory approval processes lead to delays in implementation. As traditional terroirs become less suitable, we might witness shifts in long-term production geography. Such changes could alter the fundamental character of champagne and challenge the authenticity claims of appellations, which are crucial for its premium positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Color: White Dominance Drives Premium Positioning

In 2025, white champagne commands a dominant 90.86% market share, underscoring its entrenched consumer preferences and production mastery. Meanwhile, rosé champagne, with a brisk 5.61% CAGR projected through 2031, hints at burgeoning prospects in premium branding and lifestyle-centric marketing. The white champagne segment thrives on the age-old blending of Chardonnay, Pinot Noir, and Pinot Meunier, cementing its foundational identity. Established production techniques, honed over time, ensure both consistency and quality at scale. On the other hand, rosé champagne's ascent is fueled by its visual allure and the overarching trend of premiumization. This segment fetches elevated price points, a nod to its intricate production methods and the constraints of limited availability. Notably, the color segmentation unveils strategic avenues: rosé's allure resonates with younger audiences, especially those swayed by social media, who prioritize aesthetics as much as taste.

Production limitations shape the dynamics of color segments. Rosé champagne, necessitating meticulous grape selection and processing, faces scalability challenges absent in the more streamlined workflows of white champagne. Furthermore, the repercussions of climate change aren't uniform across these segments. Rosé's reliance on precise grape maturity renders it susceptible to weather fluctuations, a vulnerability not as pronounced in traditional white blends. This segment's trajectory mirrors the broader luxury market's pivot towards exclusivity and distinctiveness. Rosé carves out a niche as a more approachable gateway to the premium champagne realm, yet it cleverly retains a level of scarcity, justifying its price premiums.

By Sweetness Level: Brut Tradition Meets Extra Brut Innovation

In 2025, Brut champagne commands a dominant 78.88% market share, epitomizing the industry's classic sweetness profile that harmonizes widespread consumer appeal with efficient production. Meanwhile, Extra Brut is witnessing a robust 6.05% CAGR through 2031, signaling a shift among discerning premium consumers who now prioritize terroir expression over mere sweetness. The Demi-Sec and Doux segments cater to specialized markets: Demi-Sec finds favor during dessert pairings, while Doux holds significance in certain cultural settings where its sweeter notes resonate with local tastes.

The segmentation by sweetness underscores the technical prowess in winemaking. Producing Extra Brut necessitates top-tier grape quality and meticulous fermentation oversight, as any flavor flaws can't be masked by a reduced dosage. Such stringent quality demands naturally erect barriers to entry, benefiting established houses with deep vineyard ties and seasoned winemaking acumen. As consumers become more educated, especially in mature markets, there's a growing appreciation for the intricate flavor profiles of Extra Brut, unmasked by sugar. This segment's rise also mirrors a broader trend: health-conscious consumers are gravitating towards authenticity and natural production methods, moving away from conventional sweetness norms.

By Price Point: Economy Scale Enables Ultra-Luxury Growth

In 2025, Economy champagne commands a dominant 60.84% market share, laying a robust volume foundation for the industry's infrastructure. Meanwhile, the ultra-luxury segment, boasting an impressive 7.84% CAGR projected through 2031, is at the forefront of driving value creation and enhancing brand positioning. This price segmentation crafts a strategic balance between accessibility and exclusivity. Economy offerings act as gateways for brand introductions, while ultra-luxury products serve to bolster a brand's prestigious image. The luxury segment's performance underscores a broader trend of premiumization, where consumers increasingly prioritize quality over quantity. For many, champagne transcends mere consumption; it's an investment in social capital.

The ultra-luxury segment's growth is fueled by rising trends in collectibility and an expanding gifting culture, especially pronounced in Asia Pacific markets. Here, champagne isn't just a drink; it's a symbol of ceremony and status. This segment's rapid expansion is further amplified by the allure of limited production volumes, enhancing scarcity value. Vintage releases and special cuvées, in particular, are commanding impressive premiums. While economic pressures ripple through various price segments, the ultra-luxury tier showcases notable resilience during downturns. Affluent consumers, steadfast in their luxury spending, contrast sharply with the economy segment, which grapples with volume pressures from more budget-conscious buyers. This nuanced segmentation empowers brands with portfolio strategies that adeptly capture a diverse array of consumer segments, all while ensuring brand coherence across varying price points.

By Packaging Size: Standard Bottles Anchor Magnum Premiumization

In 2025, standard 750ml bottles capture a dominant 71.78% market share, underscoring established consumption habits and a distribution network tailored to traditional serving sizes. Meanwhile, magnum and larger bottles are on a growth trajectory, boasting a 7.37% CAGR through 2031. This surge is fueled by trends in gifting, the allure of collectibility, and the perceived quality benefits tied to the slower aging processes in these larger vessels. Mini and half bottles cater to convenience and sampling, making them popular for individual consumption moments and premium hospitality settings where portion control is paramount.

The rise of large formats underscores a premiumization strategy, where packaging serves as a beacon of quality. Notably, magnums enjoy a price premium that outpaces their volume increase. However, this diverse packaging segmentation introduces operational challenges. Each bottle size demands its own specialized production line and inventory management, a complexity that often benefits larger producers with their scale advantages. Wine enthusiasts, particularly those who appreciate the nuances of aging and presentation, are driving the demand for large formats. They see value in both the aging potential and the visual impact these bottles bring to special occasions. Yet, not all packaging segments face the same distribution hurdles. Large formats, with their need for specialized handling and storage, find themselves at a disadvantage in retail channels, especially when compared to the universal appeal of standard bottles.

By Distribution Channel: Off-Trade Volume Supports On-Trade Value

In 2025, off-trade channels dominate with a 76.11% market share, driven by retail accessibility and competitive pricing. Meanwhile, on-trade channels are witnessing a robust acceleration, boasting a 6.86% CAGR through 2031. This surge underscores a rebound in experiential consumption and highlights opportunities for premium positioning. The segmentation of channels unveils a strategic tug-of-war: off-trade channels prioritize volume distribution, granting consumers easy access, whereas on-trade channels focus on brand experience, facilitating premium positioning and consumer education. Within the off-trade realm, online retailers are carving out a significant niche, leveraging convenience and a diverse selection. This approach resonates especially with younger consumers, who are increasingly at ease with purchasing wine digitally.

The on-trade sector's growth is buoyed by a resurgence in tourism and a trend towards experiential dining. These factors are reshaping the perception of champagne, elevating it from a mere commodity to an essential element of celebrations. Restaurants and hotels, by integrating services and emphasizing occasion-based consumption, are not only enhancing the dining experience but also justifying premium pricing and higher profit margins. This evolution in distribution mirrors a broader retail shift towards omnichannel strategies, seamlessly blending physical and digital touchpoints for an enriched consumer journey. However, as direct-to-consumer approaches vie with traditional distribution partnerships, channel conflicts arise. Navigating these tensions becomes crucial, balancing the need to foster retailer relationships while seizing digital avenues.

Geography Analysis

Europe holds a 58.01% market share in 2025, underpinned by its champagne production heritage and consumption culture. France maintains its leadership in consumption and exports, despite an 11.2% volume decline in 2023, according to Meininger's International. The region's strength stems from established distribution networks and regulatory frameworks, particularly the AOC designations overseen by INAO. Germany, the United Kingdom, and the Netherlands remain primary consumption markets, with the UK retaining its position as the second-largest champagne importer despite Brexit challenges. European consumption patterns demonstrate stability during economic downturns, as champagne remains integral to cultural celebrations and business functions. Tourism further enhances consumption through hospitality channels, with international visitor arrivals exceeding 100 million in 2024, according to Campus France.

Asia Pacific exhibits the highest growth rate at 6.52% CAGR through 2031, supported by middle-class expansion and increasing adoption of Western celebration customs. China represents significant growth potential, with wine imports reaching USD 437.9 million in 2024, despite a 6.16% year-over-year decline. France remains China's primary source at USD 176.3 million, according to the China Food and Native Produce Import and Export Chamber of Commerce. Japan displays mature market characteristics, with wine consumption tripling since 1989 and French champagne representing 40% of sparkling wine imports, as reported by Kirin Holdings. India shows promise with 6% growth in alcoholic beverage consumption, while Southeast Asian markets benefit from tourism recovery. Regional growth depends on economic development, urbanization, and cultural integration of champagne consumption.

North America maintains consistent demand, with the United States as the largest export market consuming 27.4 million bottles and generating EUR 820 million in revenue for 2024, according to the Comité Champagne. The region exhibits mature consumption patterns with established premium positioning. Canada and Mexico provide additional volume, with Mexico showing growth potential through expanding luxury consumption. However, proposed 30% tariffs on EU wines present challenges for market accessibility. American consumers increasingly prioritize premium quality over volume, aligning with champagne's heritage-focused positioning. The region's distribution infrastructure and hospitality sector provide growth foundations, though tariff policies and economic conditions create market uncertainties.

Competitive Landscape

The champagne market exhibits moderate concentration. Established houses, leveraging their heritage, vineyard control, and expansive distribution, dominate the champagne market. These houses navigate pressures from premiumization trends and the need for climate adaptation. LVMH, with its portfolio of Moët & Chandon, Dom Pérignon, Veuve Clicquot, and Ruinart, showcases how vertical integration and brand diversification forge sustainable competitive advantages.

Pernod Ricard's potential divestiture of G.H. Mumm underscores a strategic pivot towards premium brands, highlighting a broader industry trend that values brand prestige over sheer volume. As environmental certifications evolve from mere compliance to market differentiators, houses adept in sustainable viticulture and climate strategies gain a competitive edge. Digital authentication and experiential marketing present untapped avenues, with blockchain technology combating counterfeiting and NFT ventures enticing tech-savvy luxury consumers.

In the face of climate challenges, the industry's embrace of initiatives like the experimental Voltis grape variety underscores a spirit of collaborative innovation. This is especially pertinent as AOC regulations mandate collective industry adaptation. New entrants, such as sustainable packaging pioneers and direct-to-consumer platforms, are reshaping traditional distribution. Yet, established players remain shielded by regulatory hurdles and stringent quality standards. The integration of technology for supply chain transparency and enhanced consumer engagement offers a competitive edge. Notably, systems like Cloé not only bolster brand protection but also elevate the consumer experience, as highlighted by BIO Web of Conferences.

Champagne Industry Leaders

LVMH Moët Hennessy Louis Vuitton SE

Champagne Nicolas Feuillatte

Laurent-Perrier SAS

Vranken-Pommery Monopole SA

Lanson-BCC Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Telmont launched "Réserve de la Terre – Rosé", their first organic rosé made exclusively from organic grapes without synthetic chemicals.

- April 2025: Champagne Telmont introduced the ultra-lightweight champagne bottle (800g), reducing carbon emissions by 4% per bottle and setting new sustainability standards. The innovation eliminates 8,000 tons of CO2 emissions annually if adopted industry-wide.

- April 2025: Champagne Henriot unveiled L'Inattendue 2018, a 100% Chardonnay from Grand Cru Chouilly.

Global Champagne Market Report Scope

Champagne is a sparkling wine that originated and was produced in France. The Champagne Market is segmented by type, distribution channel, and geography. The market is segmented by type into brut champagne, rosé champagne, blanc de Blancs, blanc de noirs, demi-sec, and prestige cuvée and by distribution channel into on-trade and off-trade. Off-Trade is further segmented into online retail stores and offline retail stores. The market is segmented based on geography: North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Rosé |

| White |

| Brut |

| Extra Brut |

| Demi-Sec |

| Doux |

| Economy |

| Luxury |

| Ultra Luxury |

| Mini (187 ml) and Half (375 ml) |

| Standard (750 ml) |

| Magnum (1.5 L) and Large Formats |

| On-Trade | |

| Off-Trade | Online Retailers |

| Offline Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Color | Rosé | |

| White | ||

| By Sweetness Level | Brut | |

| Extra Brut | ||

| Demi-Sec | ||

| Doux | ||

| By Price Point | Economy | |

| Luxury | ||

| Ultra Luxury | ||

| By Packaging Size | Mini (187 ml) and Half (375 ml) | |

| Standard (750 ml) | ||

| Magnum (1.5 L) and Large Formats | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Online Retailers | |

| Offline Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the champagne market in 2031?

The sector is forecast to reach USD 24.75 billion by 2031, expanding at a 4.85% CAGR.

Which region is expected to grow the fastest for champagne sales?

Asia Pacific shows the highest trajectory with a 6.52% CAGR as urban middle-class celebrations and tourism rise.

Why are Extra Brut styles gaining popularity?

Consumers seek lower sugar, terroir-driven profiles; Extra Brut offers a purer taste aligned with health and authenticity trends.

What role do NFTs play in champagne branding?

NFT-backed limited editions provide authenticated scarcity, combat counterfeits, and attract tech-savvy luxury buyers seeking collectible value.

Page last updated on: