Stout Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

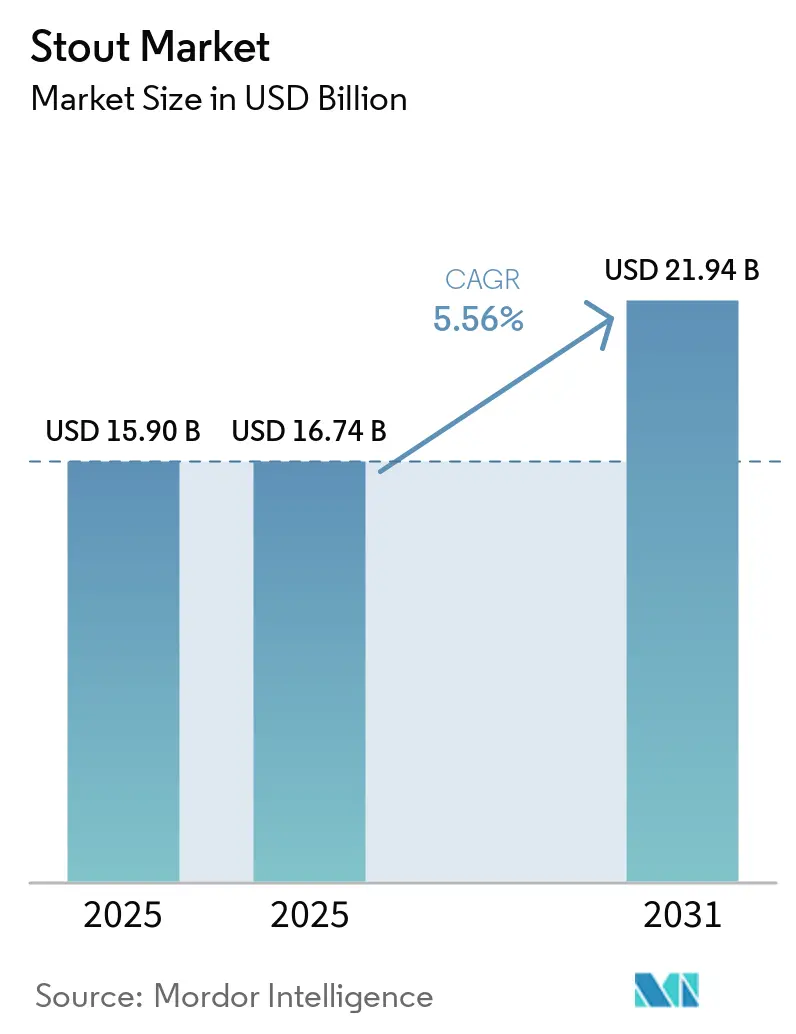

| Market Size (2025) | USD 16.74 Billion |

| Market Size (2031) | USD 21.94 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

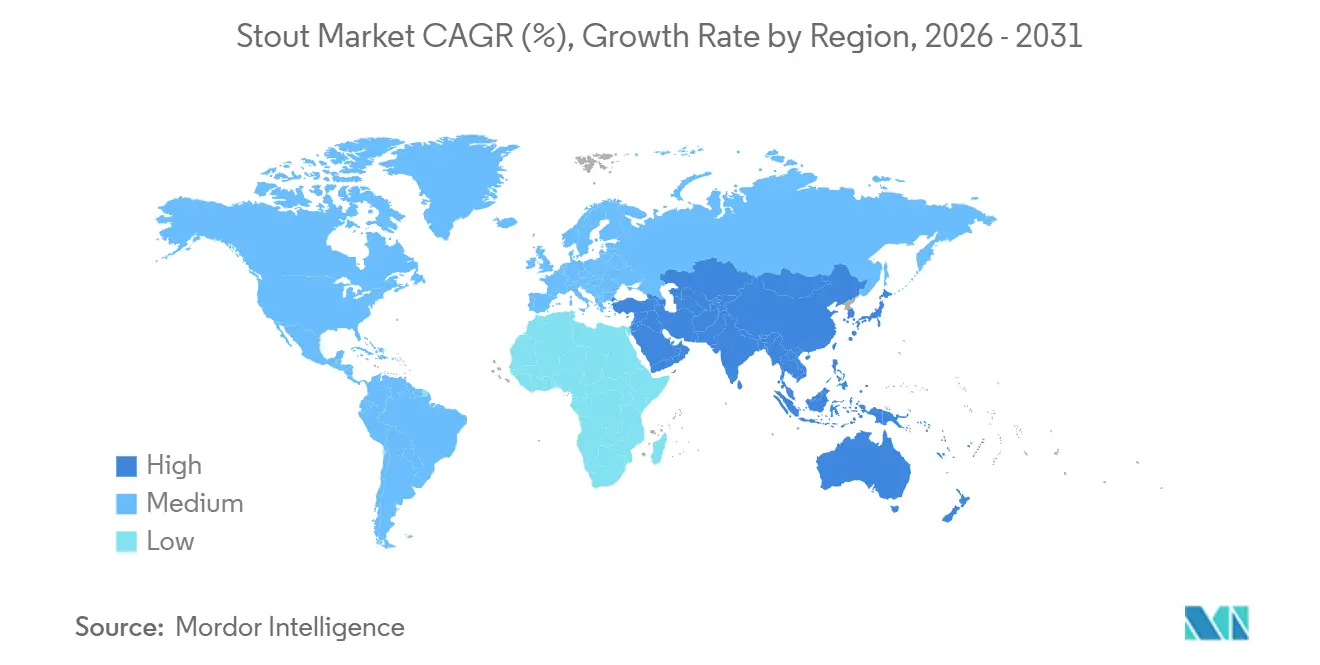

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stout Market Analysis by Mordor Intelligence

The stout market size was valued at USD 15.90 billion in 2025 and estimated to grow from USD 16.74 billion in 2026 to reach USD 21.94 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031). Nitrogen-infusion canning is boosting at-home demand, barrel-aged imperial variants are supporting price mix, and alcohol-free recipes are broadening the consumer base. Heritage brands remain pivotal, yet disruptive craft and zero-ABV players are reshaping innovation cycles. Consumer moderation trends are tempering very high-ABV lines, but sessionable and premiumized SKUs continue to expand margin pools. Regional dynamics favor Europe for scale and Asia-Pacific for velocity, while off-trade formats consolidate their lead in most developed beer markets.

Key Report Takeaways

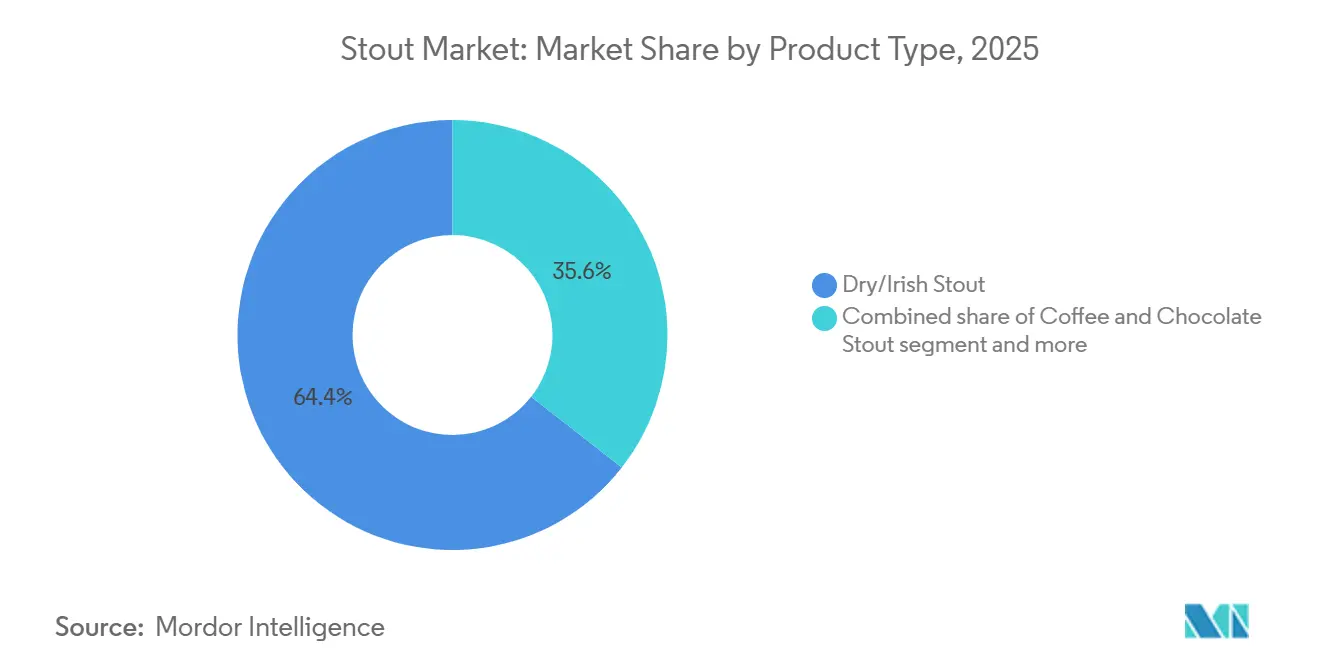

- By product type, dry/Irish stout led with 64.43% revenue share in 2025, whereas coffee/chocolate variants are forecast to grow at a 6.16% CAGR through 2031.

- By packaging format, glass bottles accounted for 52.38% of the stout market share in 2025, while aluminum cans are projected to expand at a 5.97% CAGR to 2031.

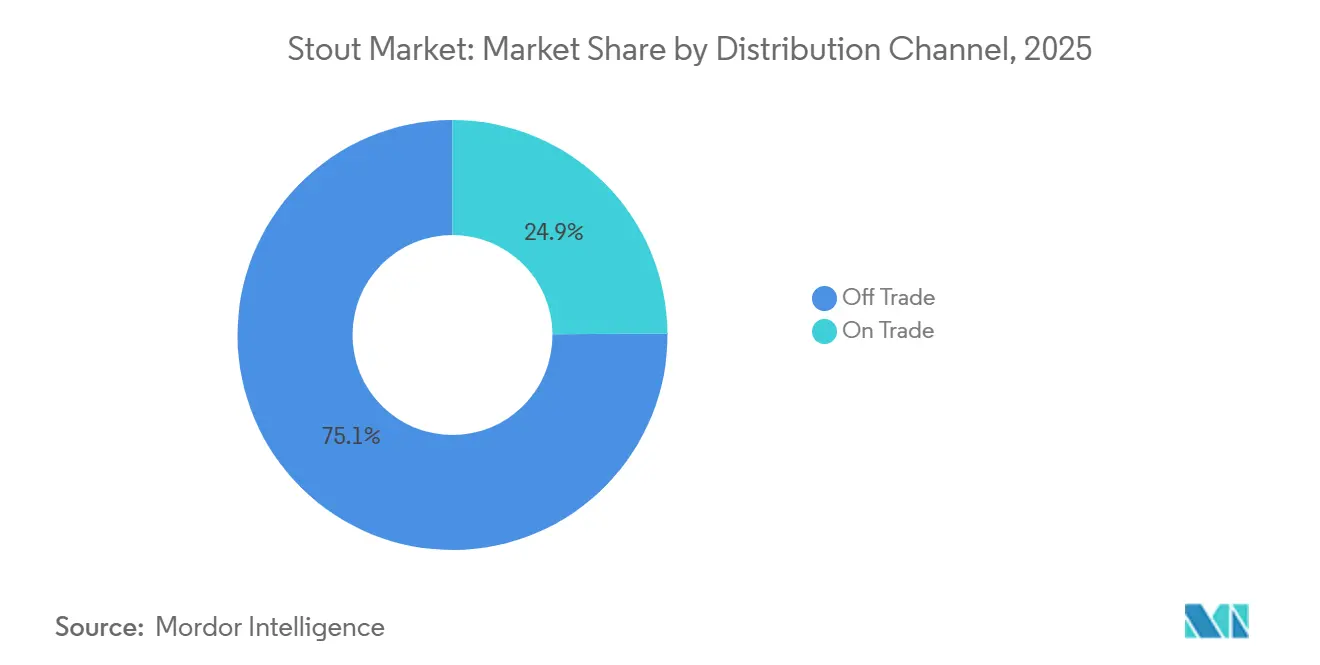

- By distribution channel, off-trade accounted for 75.11% of the stout market in 2025; on-trade is set to grow at a 5.89% CAGR between 2026 and 2031.

- By geography, Europe accounted for 38.13% of 2025 global revenue, whereas Asia-Pacific is expected to register the fastest CAGR of 6.03% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Stout Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nitrogen-infusion cans boost off-trade demand | +1.2% | Global, with early gains in North America, UK, Ireland | Medium term (2-4 years) |

| Barrel-aged and imperial stout premiumisation | +0.9% | North America, Western Europe (UK, Belgium, Netherlands) | Long term (≥ 4 years) |

| Rapid rise of alcohol-free and low-ABV stout variants | +1.4% | Global, led by UK, Ireland, Germany, North America | Short term (≤ 2 years) |

| Growth of Irish and British stout heritage brands | +0.8% | Europe core, spill-over to Asia-Pacific, Latin America | Medium term (2-4 years) |

| Innovation of lactose/milk stouts | +0.5% | North America, Australia, select European markets | Medium term (2-4 years) |

| Sustainability appeal of upcycled malt | +0.4% | Western Europe, North America (craft segment) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nitrogen-infusion cans boost off-trade demand

Nitrogen-infusion canning technology is reshaping stout consumption by delivering draught-quality texture in retail channels without the need for traditional widget hardware. Guinness launched Nitrosurge in 2024, a battery-powered ultrasonic device that activates nitrogen in specially designed cans, replicating the cascade and creamy head of a pub pour at home. Lion Brewery in Australia introduced widget-free nitro cans in 2025 that rely on modified can geometry and pressure profiles to achieve stable foam without mechanical inserts, reducing production costs and improving recyclability. These innovations address a structural constraint: nitrogen is 50 times less soluble in beer than carbon dioxide, requiring specialized dispensing systems that historically confined stout to on-trade kegs. Off-trade stout sales in the UK rose in 2025, with nitro cans accounting for the majority of incremental volume as consumers replicate pub experiences during cost-of-living pressures. The shift is global: Diageo's Guinness Microdraught system, which enables bars and restaurants without traditional draught infrastructure to serve nitrogen-infused pints, expanded to over 2,300 on-trade outlets in Ireland by mid-2025, unlocking casual dining and sports bar channels previously inaccessible to stout.

Barrel-aged and imperial stout premiumisation

Barrel-aged and imperial stout variants are commanding premiums as brewers shift from pastry-stout novelty to barrel-forward complexity that appeals to spirits drinkers. Multi-barrel aging programs, blending stouts finished in bourbon, rum, and wine casks, create layered flavor profiles that justify retail prices above USD 15 per 750ml bottle, double the mainstream stout average. Founders Brewing Co. reported that its Kentucky Breakfast Stout (KBS) and Canadian Breakfast Stout (CBS) barrel-aged series accounted for over 20% of total revenue in 2024 despite representing less than 5% of volume, illustrating the margin contribution of premium stout SKUs. The trend is reshaping inventory economics: barrel-aged stouts require 6-18 months of maturation, tying up working capital but enabling brewers to release limited vintages that sell out within hours and build collector demand. Belgium's Trappist breweries and UK craft producers are leveraging heritage barrel stocks, some dating to the 19th century, to authenticate provenance claims that resonate with affluent consumers seeking artisanal narratives. However, high-ABV imperial stouts (often 10–14% ABV) face tightening regulations in Scandinavia and parts of Canada, where government monopolies are restricting shelf access for beers above 8% ABV to curb binge drinking, creating geographic headwinds for this premium segment.

Rapid rise of alcohol-free and low-ABV stout variants

Alcohol-free and low-ABV stout variants are attracting abstainers and expanding the total addressable market as brewers deploy reverse osmosis and arrested fermentation to preserve roasted malt character without ethanol. Guinness 0.0 became the number-one non-alcoholic beer in Great Britain in 2025 and the fastest-growing non-alcoholic beer in the market, with distribution expanding to over 2,300 on-trade outlets in Ireland by mid-2025[1]Source: Diageo plc, “Annual Report 2025,” diageo.com . Athletic Brewing, the largest US non-alcoholic beer producer, acquired Ballast Point's 107,000-square-foot San Diego facility in May 2024 for an undisclosed sum, doubling its US brewing capacity to approximately 1 million barrels per year and signaling institutional confidence in the zero-ABV segment. The company reported 62% year-over-year growth in the 12 months preceding the acquisition and raised USD 251 million in total funding, including a Series D round in July 2024 that valued the business at USD 800 million. BrewDog's Black Heart stout (0.5% ABV) and Athletic's All Out and Emerald Cliffs stouts are capturing share among wellness-focused demographics, as US alcohol consumption fell 8% between 2021 and 2025, according to BCG data. The 2025-2030 Dietary Guidelines for Americans emphasize "consume less alcohol," creating regulatory tailwinds for zero-ABV innovation. Stout's roasted malt and coffee notes translate effectively to non-alcoholic formats because bitterness and body, rather than hop aroma, define the style, giving stout producers a structural advantage over IPA and lager brewers in the zero-ABV race.

Growth of Irish and British stout heritage brands

Irish and British stout heritage brands are expanding globally as Diageo and Heineken leverage Premier League sponsorships and route-to-market partnerships to recruit younger drinkers in Asia-Pacific and Latin America. Guinness delivered 10.9% organic net sales growth in the first half of fiscal 2026, with double-digit growth across all regions except Asia-Pacific, where route-to-market transitions in Australia and China temporarily reduced volumes. Diageo activated its Guinness Premier League partnership in 81 countries beginning in August 2024, using football to position stout as a social beverage for match-day occasions and to displace lager in sports bars. Heineken reported stout portfolio growth in Nigeria (Legend brand), Myanmar (ABC brand), and the UK (Murphy's) in its 2025 half-year results, with increased marketing investments in Nigeria and Brazil supporting premium stout positioning. Diageo is investing GBP 200 million in its Littleconnell brewery in Ireland to expand Guinness production capacity, anticipating sustained global demand growth through 2030. However, the company divested its stakes in Guinness Nigeria PLC in September 2024 and Guinness Ghana Breweries PLC in July 2025, recording exceptional losses of USD 125 million and USD 114 million, respectively, as it shifted to license-brewing models that reduce capital intensity and preserve cash for brand-building.

Restraints Impact Analysis of Stout Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-driven moderation of high-ABV beers | -0.7% | Global, most acute in North America, Scandinavia | Short term (≤ 2 years) |

| High-ABV imperial stouts facing tightening regulations | -0.4% | Scandinavia, Canada, select EU markets | Medium term (2-4 years) |

| Ingredient cost volatility (roasted barley, cocoa, coffee beans) | -0.5% | Global, with acute pressure in coffee-producing regions | Short term (≤ 2 years) |

| Shelf-life sensitivity of nitro and specialty stouts | -0.3% | Global, particularly affecting export and e-commerce channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-driven moderation of high-ABV beers

Health-driven moderation trends are constraining high-ABV stout consumption as wellness movements and GLP-1 medications reduce alcohol occasions among affluent demographics. US alcohol consumption by volume fell 8% between 2021 and 2025, according to BCG analysis, with the steepest declines in spirits and high-ABV beer categories. The 2025-2030 Dietary Guidelines for Americans emphasize "consume less alcohol," creating regulatory and social pressure that disproportionately affects imperial stouts (10-14% ABV) positioned as indulgent, high-calorie beverages. GLP-1 receptor agonists (semaglutide, tirzepatide) prescribed for weight management reduce appetite and alcohol cravings, with Diageo citing "small impact from GLP-1s and changing lifestyles" in its fiscal 2026 interim results. Stout's caloric density, a 12-ounce serving of imperial stout contains 250-350 calories, double that of light lager, positions the category unfavorably against hard seltzers and low-calorie RTDs that dominate wellness-focused retail sets. Brewers are responding with session stouts (4-5% ABV) and alcohol-free variants, but these SKUs cannibalize premium imperial stout margins and dilute brand equity built on strength and richness.

Ingredient cost volatility (roasted barley, cocoa, coffee beans)

Ingredient cost volatility for roasted barley, cocoa, and coffee beans is compressing stout margins as climate events and geopolitical disruptions disrupt specialty commodity supply chains. Roasted barley prices rose 12% in 2024–2025 due to drought in Australia and Canada, the largest malting barley exporters, which reduced global supply and forced brewers to source from higher-cost European maltsters. Cocoa prices surged to record highs in 2024, driven by crop failures in West Africa (Côte d'Ivoire, Ghana), with chocolate stout brewers facing 30-40% cost increases for cocoa nibs and cacao powder. Coffee bean prices (Arabica) climbed 25% year-on-year in 2025 due to frost damage in Brazil and export restrictions in Vietnam, raising input costs for coffee stouts that rely on cold-brew additions and whole-bean dry-hopping. The Drinks Business. Stout producers cannot easily substitute ingredients without altering flavor profiles: roasted barley provides the burnt, coffee-like bitterness that defines the style, while cocoa and coffee adjuncts are consumer-facing label claims that drive purchase intent. Small craft brewers lack hedging capacity and forward-contract leverage, forcing them to absorb cost increases or pass them to consumers through price hikes that risk volume declines in price-sensitive off-trade channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Stout Market Segment Analysis

By Product Type:

Dry Stout Anchors Volume, Coffee Variants Drive Premium GrowthDry/Irish stout commanded 64.43% market share in 2025, anchored by Guinness, Murphy's, and Beamish heritage brands that dominate on-trade draught and off-trade nitro can segments, yet coffee and chocolate stout is the fastest-growing product type at 6.16% CAGR (2026-2031) as craft brewers co-brand with specialty roasters and chocolatiers to recruit younger consumers. Milk/sweet stout holds a mid-teens share, with Left Hand Milk Stout Nitro and regional lactose variants appealing to dessert-occasion drinkers, while "Others" (oatmeal stout, oyster stout, imperial variants) capture niche premiums through limited releases and barrel-aging programs. Coffee and chocolate stouts are expanding through innovation: Founders Brewing's Breakfast Stout and Sierra Nevada's Stout with coffee and cocoa nibs leverage single-origin beans and direct-trade cacao to justify USD 12-15 per four-pack pricing, double the dry stout average.

Dry stout's dominance reflects entrenched consumer habits in Ireland and the UK, where Guinness accounts for over 80% of stout volumes and benefits from Premier League sponsorship activated in 81 countries since August 2024. Milk stout growth is constrained by the prevalence of lactose intolerance (65% of global adults) and tightening allergen labeling requirements in the EU and UK, prompting brewers to develop oat-milk stout alternatives with beta-glucan for creaminess. Imperial and barrel-aged stouts within "Others" face regulatory headwinds as Scandinavian monopolies and Canadian provinces restrict shelf access for beers above 8% ABV, yet these variants command premiums that offset volume declines, Founders' KBS series generated over 20% of revenue in 2024 despite representing less than 5% of volume.

By Packaging Format:

Glass Premiumization Meets Aluminum SustainabilityGlass bottles held 52.38% of the packaging share in 2025, reflecting stout's premium positioning and shelf-appeal advantages, while aluminum cans are the fastest-growing format at a 5.97% CAGR (2026–2031) as nitro widget innovations and recyclability concerns drive off-trade adoption. Keg/cask formats account for the remainder, concentrated in on-trade draught systems and craft brewery taprooms. Glass bottles dominate the imperial and barrel-aged stout segments because 750ml formats signal premiumization and enable vintage dating, which builds collector demand; brewers use embossed labels and wax seals to enhance shelf presence. Aluminum cans are gaining share through technological advances: Guinness Nitrosurge (launched 2024) uses ultrasonic activation to replicate draught texture without widgets, while Lion Brewery's widget-free nitro cans rely on modified can geometry to achieve stable foam at lower production costs.

Carlsberg reported that aluminum cans reached 38% of its global packaging mix in 2025, up from 32% in 2023, driven by sustainability messaging and off-trade convenience[2]Source: Carlsberg A/S, “Financial Statement FY 2025,” carlsberggroup.com. Recycled content in bottles and cans averaged 51% across Carlsberg's portfolio in 2025, with 95% of packaging recyclable, reusable, or renewable, enabling sustainability claims that resonate with Gen Z consumers. Keg/cask formats are growing in craft taprooms and Guinness Microdraught systems, which expanded to over 2,300 on-trade outlets in Ireland by mid-2025, unlocking casual dining venues without traditional draught infrastructure. Glass faces headwinds from weight-based shipping costs and breakage risk in e-commerce, while aluminum's shelf-life limitations (nitro cans lose cascade within 6-9 months) constrain export to Asia-Pacific and Latin America markets with 60-90 day transit times.

By Distribution Channel:

Off-Trade Dominance, On-Trade Innovation Unlocks GrowthOff-trade channels held 75.11% market share in 2025, driven by nitro can innovations and cost-of-living pressures that shifted consumption from pubs to home. Yet the on-trade is growing faster at a 5.89% CAGR (2026–2031) as Guinness Microdraught and craft taproom expansions unlock venues without traditional draught systems. Off-trade growth accelerated during 2020-2022 pandemic lockdowns and sustained through 2025 as UK consumers replicated pub experiences at home using Guinness Nitrosurge devices and widget-free nitro cans that deliver draught texture in retail formats. Supermarkets and hypermarkets dominate the off-trade, with Tesco, Sainsbury's, and Asda in the UK dedicating expanded shelf space to stout during the 2024-2025 Guinness shortage, which saw Murphy's volumes surge. E-commerce is a fast-growing off-trade sub-channel, with Athletic Brewing's direct-to-consumer subscription club and online shop generating significant revenue, though shelf-life constraints limit international shipping for nitro and coffee stouts.

On-trade growth is driven by Guinness Microdraught systems, which enable bars and restaurants without cellar space or CO2/nitrogen gas lines to serve perfect pints, expanding stout availability in sports bars, casual dining, and airport lounges. Heineken's eB2B platform reached EUR 6.3 billion gross merchandise value in H1 2025, connecting over 720,000 active traditional-channel customers and improving stout availability in fragmented on-trade markets across Africa and Asia-Pacific. Craft brewery taprooms are expanding on-trade share by offering exclusive stout variants (barrel-aged, nitro, limited releases) unavailable in retail, with Athletic Brewing's acquisition of Ballast Point's San Diego facility in May 2024 including a taproom that will remain operational during 18 months of renovations. On-trade faces headwinds from cost-of-living pressures that reduce pub visits and from labor shortages that limit venue operating hours, yet Diageo's Premier League partnership (activated in 81 countries from August 2024) is driving match-day stout consumption in sports bars and pubs.

Geography Analysis

Europe Stout Market

Europe remains the core of the global stout market, holding a 38.13% share in 2025, underpinned by a deeply rooted drinking culture in Ireland and the UK. The region’s strength lies less in short-term expansion and more in tradition, brand loyalty, and a well-established consumer base that continues to evolve through premium and craft variations. The growing presence of independent brewers and experimentation with flavored and barrel-aged stouts reflect a shift toward premiumization, while strong distribution networks and strategic partnerships further reinforce stout visibility across retail and hospitality channels. Overall, Europe’s leadership is sustained by heritage, innovation within tradition, and a resilient demand structure.

APAC Stout Market

Asia-Pacific, by contrast, is defined by momentum rather than legacy, emerging as the fastest-growing region with a 6.03% CAGR through 2031. Growth here is being shaped by urbanization, rising disposable incomes, and shifting consumer preferences toward premium and craft beverages. Markets such as Japan, China, and Australia are seeing increased interest in dark beer styles, particularly in metropolitan areas where consumers are more open to experimentation. Expansion strategies by global brewers, including localized production and portfolio diversification, are helping to build accessibility while aligning with regional taste profiles. The region’s trajectory suggests a gradual but steady repositioning of stout from a niche offering to a premium lifestyle product.

The Americas and MEA Stout Market

Outside these two regions, the stout market presents a more fragmented and opportunity-driven landscape. North America balances strong craft innovation with export-oriented production, while regulatory dynamics and pricing pressures shape profitability. In South America and parts of the Middle East and Africa, growth is more localized, supported by partnerships, domestic production, and increasing urban demand. Across these regions, stout is often positioned as a premium or specialty product, with growth tied to brand positioning, distribution expansion, and evolving consumer awareness rather than broad-based market penetration.

Competitive Landscape

The stout market exhibits moderate concentration, with Diageo, Heineken, Anheuser-Busch InBev, Carlsberg, and Molson Coors controlling heritage brands (Guinness, Murphy's, Beamish) and leveraging global distribution networks, while Athletic Brewing, BrewDog, and regional craft brewers capture share in alcohol-free and specialty segments through rapid innovation cycles and direct-to-consumer models. Diageo's Guinness delivered 10.9% organic net sales growth in H1 fiscal 2026 and gained share in its three largest markets, supported by Premier League sponsorship activated in 81 countries from August 2024 and Guinness 0.0 becoming the number-one non-alcoholic beer in Great Britain in 2025. Carlsberg's acquisition of Britvic for GBP 3.3 billion in January 2025 created the largest Pepsi bottler in Europe and enabled cross-category route-to-market synergies that strengthen stout shelf presence, with the combined business generating DKK 89.1 billion revenue and targeting GBP 110 million in cost synergies by 2027.

Heineken reported stout portfolio growth in Nigeria (Legend), Myanmar (ABC), and the UK (Murphy's) in its 2025 half-year results, with eB2B platforms reaching EUR 6.3 billion gross merchandise value and connecting over 720,000 active customers to improve distribution in fragmented markets[3]Source: Heineken Holding N.V., “2025 Half-Year Results,” heinekenholding.com. Strategic patterns reveal a bifurcation: global brewers are divesting capital-intensive African breweries to focus on brand licensing and route-to-market partnerships, Diageo sold stakes in Guinness Nigeria and Guinness Ghana in 2024-2025, recording USD 239 million in exceptional losses, while shifting to license-brewing in Australia and New Zealand to preserve cash for marketing. Simultaneously, craft brewers are scaling through merger and aquasition and capacity expansion: Athletic Brewing acquired Ballast Point's 107,000-square-foot San Diego facility in May 2024, doubling US capacity to 1 million barrels per year, while BrewDog was acquired by Tilray Brands for GBP 33 million in 2025/2026, with the combined entity targeting USD 200 million annual revenue.

White-space opportunities exist in alcohol-free stout (Guinness 0.0, Athletic Brewing) and coffee/chocolate variants (Founders Breakfast Stout, Sierra Nevada Stout), where premiums of 50–100% versus dry stout justify innovation investments. Emerging disruptors include Athletic Brewing, which raised USD 251 million in total funding and achieved a USD 800 million valuation in July 2024, and regional craft brewers leveraging upcycled malt and regenerative barley sourcing to differentiate on sustainability. Technology is a competitive lever: Guinness Nitrosurge (ultrasonic nitrogen activation) and Lion Brewery's widget-free nitro cans reduce production costs and improve recyclability, while Carlsberg's digital tools (Servd eB2B, One Metric shelf analytics, VMx AI pricing) enhance commercial execution and promotional optimization.

Stout Industry Leaders

Diageo PLC

Heineken NV

Anheuser-Busch InBev

Carlsberg Group

Molson Coors Beverage Co

- *Disclaimer: Major Players sorted in no particular order

Stout Market Companies Covered in this Report

- Diageo PLC

- Heineken N.V.

- Anheuser-Busch InBev

- Carlsberg Group

- Molson Coors Beverage Company

- Asahi Group Holdings

- Kirin Holdings

- Lion Pty Ltd

- BrewDog PLC

- Boston Beer Company

- Left Hand Brewing Company

- Founders Brewing Co.

- Sierra Nevada Brewing Co.

- Deschutes Brewery

- Oskar Blues Brewery

- Athletic Brewing Company

- Anspach & Hobday

- Harpoon Brewery

- Fuller’s Brewery

- Murphy Brewery Ireland

Recent Industry Developments in Stout Market

- July 2025: Goose Island, an Anheuser-Busch brand, unveiled its latest Bourbon County stout lineup, featuring six distinct variants: the original stout, Cherries Julibee Stout, Chocolate Praline Stout, among others. Each variant is elegantly bottled in a 10-ounce glass container.

- July 2025: Supermalt introduced a new stout boasting an ABV of 7.7%. This stout is conveniently packaged in a 330 ml glass bottle and crafted from barley malt, maize, glucose syrup, and hops.

- June 2025: Felons debuted its latest Imperial Stout. The 2025 offering entices with aromas of roasted malt and dark fruits, complemented by a palate rich in toffee, cocoa, and aniseed, culminating in a dry, lingering finish.

- November 2024: Guinness joined forces with Brooklyn Brewery to introduce the limited-edition Guinness Fonio Stout. This unique brew, crafted in alignment with the Brewing for Impact campaign, draws inspiration from Brooklyn Brewery Brewmaster Garrett Oliver's innovative work with fonio, an ancient grain from West Africa.

Global Stout Market Report Scope

Stout is a dark beer known for its rich flavor, roasted malt characteristics, and often notes of coffee, chocolate, or caramel. The stout market is segmented by product type, packaging format, distribution channel, and geography. By product type, the market includes dry/Irish stout, milk/sweet stout, coffee and chocolate stout, and other variants. Based on packaging format, the market is categorized into keg/cask, glass bottle, and aluminum can. By distribution channel, the market is segmented into on-trade and off-trade. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume (Liters).

Segmentation Overview

| Dry/Irish Stout |

| Milk/Sweet Stout |

| Coffee and Chocolate Stout |

| Others |

| Keg/Cask |

| Glass Bottle |

| Aluminium Can |

| On Trade |

| Off Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Rest of Middle East and Africa |

| By Product Type | Dry/Irish Stout | |

| Milk/Sweet Stout | ||

| Coffee and Chocolate Stout | ||

| Others | ||

| By Packaging Format | Keg/Cask | |

| Glass Bottle | ||

| Aluminium Can | ||

| By Distribution Channel | On Trade | |

| Off Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the stout market and its expected growth?

The stout market size reached USD 15.90 billion in 2025 and is projected to hit USD 21.94 billion by 2031, expanding at a 5.56% CAGR between 2026-2031.

Which product type leads volume, and which is growing fastest?

Dry/Irish stout leads with 64.43% 2025 share, while coffee and chocolate stout is the fastest-growing at 6.16% CAGR through 2031.

How are packaging preferences shifting?

Glass still holds the largest share at 52.38%, but aluminum cans are growing quickest at 5.97% CAGR thanks to nitro-technology and recyclability.

Which channel will add the most incremental value?

Off-trade commands 75.11% share today, yet on-trade is forecast to deliver the highest growth at 5.89% CAGR as Microdraught systems widen venue coverage.

Why is Asia-Pacific a priority region?

Asia-Pacific posts the fastest regional CAGR at 6.03%, propelled by urban adoption in Japan, China, and Australia and supported by brand licensing models that trim capital needs.

Page last updated on: