BCG Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 189.47 Million |

| Market Size (2031) | USD 255.76 Million |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

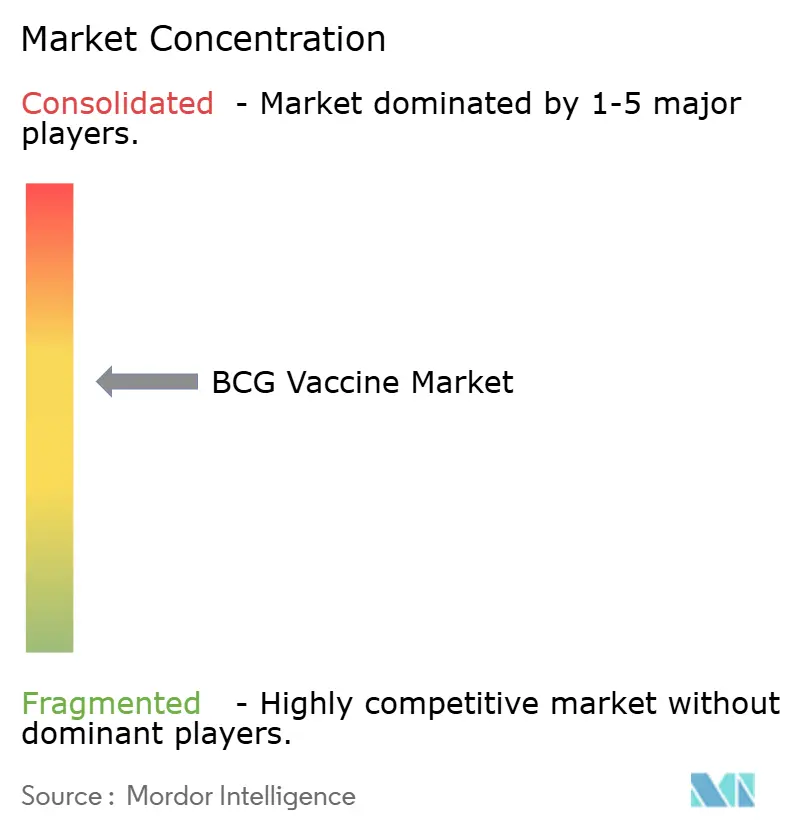

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

BCG Vaccine Market Analysis by Mordor Intelligence

The BCG vaccine market size in 2026 is estimated at USD 189.47 million, growing from 2025 value of USD 178.44 million with 2031 projections showing USD 255.76 million, growing at 6.18% CAGR over 2026-2031. Universal newborn immunization mandates across tuberculosis‐endemic countries, widening oncology use in non-muscle-invasive bladder cancer, and active government stockpiling programs together sustain a healthy demand pipeline while creating strategic procurement opportunities. Manufacturers are racing to expand capacity because persistent supply shortages underscore the importance of resilient production footprints, and investment announcements from Merck as well as Serum Institute of India suggest that new lines will come online within the next five years. Regulatory tailwinds, including the FDA’s revised guidance for BCG-unresponsive bladder cancer and the WHO’s updated tuberculosis prevention framework [1]World Health Organization, “Tuberculosis Preventive Treatment Guidelines,” who.int, further broaden the commercial scope of the BCG vaccine market while encouraging product differentiation through recombinant strains and novel delivery platforms.

Key Report Takeaways

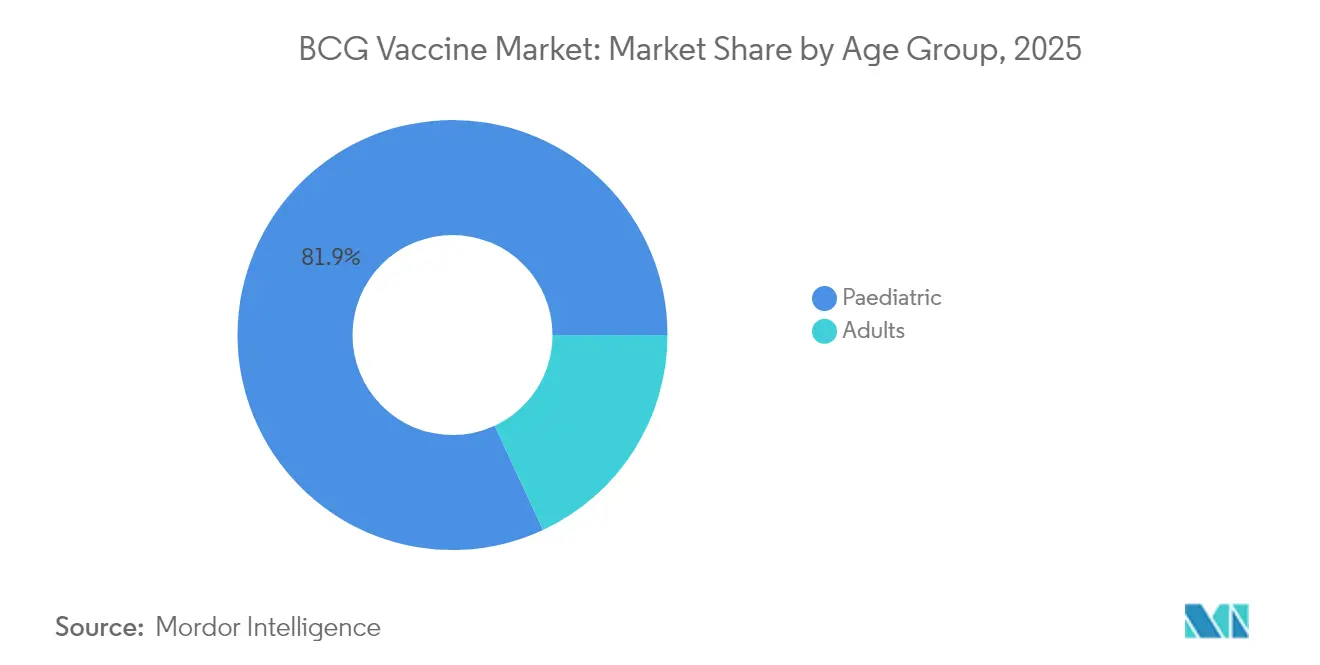

- By age group, pediatric vaccination held 81.92% share of the BCG vaccine market in 2025, and adult use is expected to grow at 6.95% CAGR to 2031.

- By application, tuberculosis prevention commanded 81.45% of the BCG vaccine market share in 2025, while bladder cancer therapy is set to advance at 7.05% CAGR to 2031.

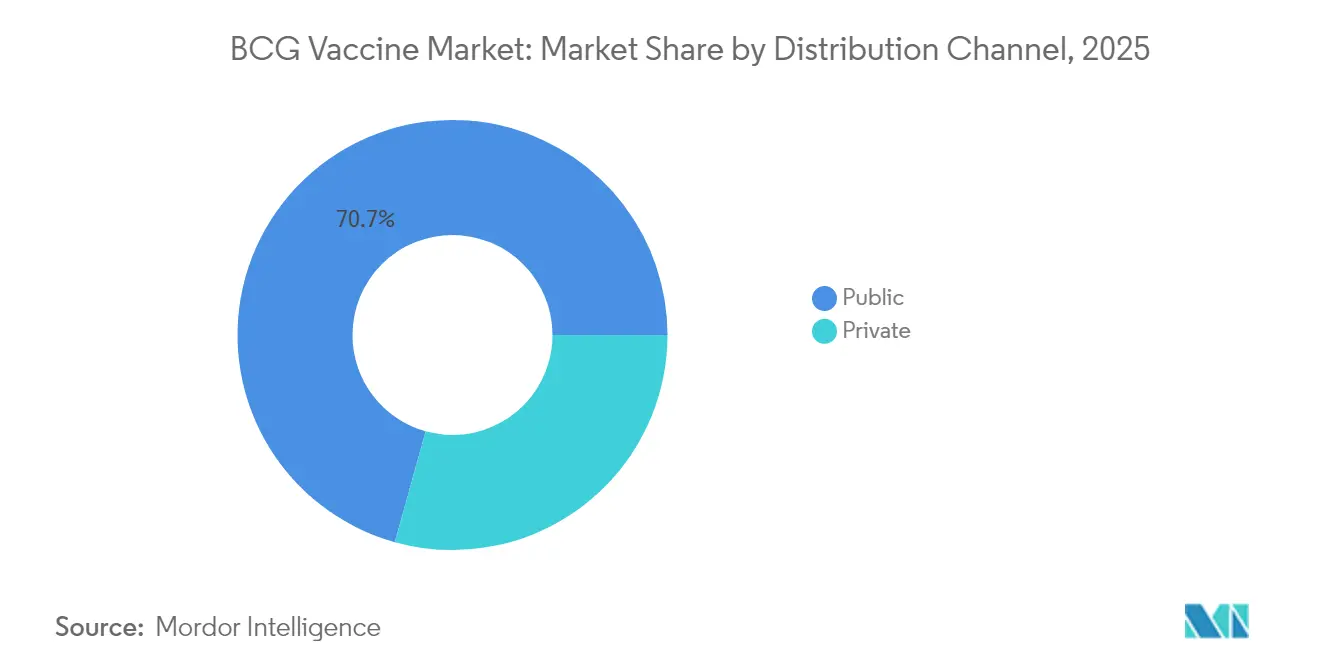

- By distribution channel, public procurement accounted for 70.68% of the BCG vaccine market size in 2025, whereas private channels are projected to rise at 7.11% CAGR during the same horizon.

- By geography, Asia-Pacific led with 37.52% revenue share in 2025 and is forecast to expand at 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global BCG Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of drug-resistant & latent tuberculosis | +1.8% | South-East Asia, Sub-Saharan Africa, other high-burden areas | Long term (≥ 4 years) |

| Expanding universal newborn immunization mandates | +1.2% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Government-funded stockpiling & catch-up campaigns | +0.9% | Global focus on TB-endemic countries | Short term (≤ 2 years) |

| Growing adoption of BCG as adjunct immunotherapy for non-muscle-invasive bladder cancer | +1.4% | North America, EU, developed APAC | Medium term (2-4 years) |

| Evidence for BCG-induced trained immunity against emerging respiratory pathogens | +0.7% | Early adoption in high-income economies | Long term (≥ 4 years) |

| R&D into recombinant BCG strains with multi-antigen expression | +0.5% | North America and EU innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of drug-resistant & latent tuberculosis

Drug-resistant strains now influence national vaccination strategies, prompting intensified BCG coverage across South-East Asia where 45% of global tuberculosis cases were recorded in 2023 [2]World Health Organization, “Global Tuberculosis Report 2024,” who.int. Indonesia’s leadership in Phase 3 trials for the M72/AS01E candidate underscores how endemic regions fund next-generation solutions while upholding current BCG schedules. Clinical evidence shows 45.4% efficacy for adolescent revaccination, supporting programs aimed at preventing latent infection progression. High-burden geographies therefore represent the largest addressable pool for incremental doses as health agencies integrate revaccination policies. This driver will affect demand for the BCG vaccine market through the decade because multidrug resistance remains a persistent epidemiological threat.

Expanding universal newborn immunization mandates

Policy makers increasingly view BCG as part of holistic infant health strategies; Finland’s 2026 procurement plan confirms adoption even in low-incidence settings. WHO guidelines recommend BCG for HIV-exposed infants and family contacts, adding scale to national rollouts. Indonesia’s National Immunization Strategy recorded 80% coverage in 2024 despite pandemic-related disruptions, showing how middle-income economies turn mandates into executable programs. Infrastructure upgrades funded by Asia-Pacific governments now include cold chain expansion, ensuring dose stability from factory to clinic. Medium-term growth momentum in the BCG vaccine market will therefore track the rollout cadence of these newly legislated schedules.

Government-funded stockpiling & catch-up campaigns

UNICEF’s emergency tenders, modelled during the mpox outbreak, now serve as templates for rapid BCG acquisition when shortages arise [3]UNICEF, “Immunization Catch-up Campaigns 2024,” unicef.org. CEPI’s USD 30 million investment in Serum Institute of India strengthens surge capacity, offering global producers financial incentives to maintain buffer inventories. WHO and UNICEF counted 14.3 million unvaccinated infants in 2024, energizing catch-up drives that spike short-term demand. Stockpiling aligns with multi-year contracts that give manufacturers order visibility, thereby improving capital-expenditure planning. Such procurement strategies are expected to support sustained growth in the BCG vaccine market because they decouple demand from annual budget cycles.

Growing adoption of BCG as adjunct immunotherapy for non-muscle-invasive bladder cancer

The FDA cleared Anktiva in April 2024, validating combination regimens that enhance BCG efficacy for patients unresponsive to monotherapy. The UK MHRA echoed this decision in July 2025, fast-tracking clinician uptake across Europe. ImmunityBio’s expanded-access program, enabled by Serum Institute supply, highlights how oncology demand stimulates manufacturer partnerships to safeguard continuity. TAR-200 trials reported 82.4% complete response rates, illustrating competitive entrants that nonetheless rely on BCG as foundational therapy. These developments should raise procedural volumes, directly boosting the BCG vaccine market in high-income healthcare systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse events & contraindications in immunocompromised recipients | -0.8% | HIV-endemic regions globally | Medium term (2-4 years) |

| Supply shortages linked to limited global producers | -1.2% | Acute in North America and Europe | Short term (≤ 2 years) |

| Cold-chain logistics costs in low-income settings | -0.6% | Sub-Saharan Africa, South Asia, rural Latin America | Medium term (2-4 years) |

| Capacity constraints for GMP-grade seed-lot expansion | -0.4% | Manufacturing hubs worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse events & contraindications in immunocompromised recipients

WHO classifies known HIV infection as a formal contraindication to BCG because disseminated disease reaches mortality rates nearing 75% in affected infants. Protocols now delay vaccination for neonates born to tuberculosis-positive mothers until preventive therapy is completed, complicating workflow in resource-limited facilities. Oman’s surveillance data revealed 9.2 BCG-linked adverse events per 100,000 doses, primarily abscesses, prompting calls for stronger pre-screening. These safety concerns reduce coverage in precisely the regions with the highest tuberculosis burden, narrowing the addressable pool for the BCG vaccine market. Medium-term headwinds persist while clinician education and improved diagnostics scale across endemic zones.

Supply shortages linked to limited global producers

Merck remains the only U.S. supplier after Sanofi’s exit, triggering rationing for high-risk bladder cancer patients and prompting federal appeals for alternative import channels. Construction of Merck’s new North Carolina facility will take at least five years, highlighting the long lead times inherent in sterile biologics manufacturing. Japan’s biosimilar support framework, although currently focused on monoclonal antibodies, illustrates policy models that could expand domestic BCG output and reduce import dependence. During shortages, clinics in Canada and Spain reported postponements of intravesical therapy, directly impacting patient outcomes. These disruptions shave growth off the BCG vaccine market until new capacity becomes operational.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Age Group: Pediatric Adoption Remains the Anchor While Adult Oncology Uptake Accelerates

Pediatric immunization continued to dominate in 2025, accounting for 81.92% of total doses distributed and anchoring public-health funding decisions. Newborn vaccination coverage regularly tops 90% in 154 countries, underscoring how early-life protection shapes the BCG vaccine market. Bladder cancer treatment is driving faster expansion on the adult side, where 6.95% CAGR is forecast through 2031 as oncologists adopt combination regimens validated by recent approvals. Adult demand is further reinforced by growing interest in booster strategies for trained immunity, with multiple university trials evaluating respiratory infection outcomes among older populations. Over the forecast horizon, pediatric volumes will maintain scale advantages, yet the adult segment offers higher marginal revenue per vial because oncology doses command premium pricing in hospital settings. Hospitals therefore form dedicated procurement units that lock in multi-year contracts, boosting visibility for suppliers planning capacity upgrades. Although pediatric subsidy mechanisms keep prices in check, rising production costs are likely to flow more easily into adult oncology list prices, providing margin upside for manufacturers.

The adult opportunity also benefits from payer willingness to reimburse immunotherapies that delay radical cystectomy, lowering overall treatment costs for healthcare systems. Regulatory agencies now encourage adaptive licensing pathways that expedite access for BCG-unresponsive indications, setting precedents that could be replicated for new recombinant strains. Together these dynamics illustrate how the BCG vaccine market balances volume stability in pediatrics with value growth in adults, creating a diversified revenue stream resilient to single-segment shocks.

By Application: Tuberculosis Prevention Commands Volume While Bladder Cancer Therapy Lifts Value

Tuberculosis prevention retained 81.45% share in 2025, supported by universal schedules in Asia-Pacific and Africa that sustain baseline demand levels even during supply shortages. Governments finance bulk orders through UNICEF and the PAHO Revolving Fund, locking in preferential prices that stabilize procurement budgets year over year. The BCG vaccine market size attributable to preventive use is set to rise steadily as revaccination pilots expand in adolescent cohorts across India, Indonesia and South Africa. Meanwhile, bladder cancer therapy advances at a brisk 7.05% CAGR, propelled by positive trial read-outs and expanding payer coverage for combination regimens. Oncology guidelines in the United States and Europe continue recommending intravesical BCG as first-line treatment, ensuring consistent utilization despite emergent competitors.

Recombinant BCG pipelines add depth to both application pillars, with multi-antigen tuberculosis candidates progressing in parallel with engineered strains designed to heighten antitumor immunity. Cross-indication innovation can thus unlock manufacturing synergies by leveraging common upstream processes. Stakeholders expect that once recombinant options clear pivotal trials, incremental volumes will feed into the BCG vaccine market without cannibalizing existing products, because legacy formulations will remain necessary for lower-income settings due to cost considerations.

By Distribution Channel: Public Sector Retains Primacy But Private Oncology Supply Chains Tighten

Public procurement represented 70.68% of global shipments in 2025, reflecting the enduring centrality of government budgets and multilateral agencies in infectious-disease control. Ministries negotiate multi-year framework agreements that include performance clauses for on-time delivery, incentivizing suppliers to prioritize public orders when shortages occur. Still, private channels are expanding at 7.11% CAGR as specialized oncology centers in high-income and emerging economies increasingly source directly from manufacturers to guarantee uninterrupted therapy schedules. These private buyers are often willing to pre-pay or maintain safety stocks, raising their attractiveness to producers balancing finite output across customers.

Hybrid public-private partnerships, such as South Africa’s Biovac, demonstrate how public health objectives can coexist with commercial imperatives to localize supply, mitigate currency risk, and cultivate skilled labor. Such models could influence future tender designs, integrating value-based criteria like local investment commitments. Consequently, competition within the BCG vaccine market is shifting from pure price battles toward multi-dimensional evaluations that also weigh supply security, cold-chain performance, and technological innovation.

Geography Analysis

Asia-Pacific maintained leadership with 37.52% of global revenue in 2025, and its 7.12% CAGR outlook through 2031 outpaces every other region. High tuberculosis incidence, rising healthcare expenditure, and robust manufacturing ecosystems in India and China collectively sustain the largest regional slice of the BCG vaccine market. Indonesia’s participation in M72/AS01E Phase 3 trials highlights simultaneous investment in next-generation solutions while national immunization programs continue distributing classical BCG formulations. China’s vaccine output meets domestic needs and supports exports via bilateral aid channels, further anchoring Asia-Pacific supply dominance.

North America and Europe form the second-tier cluster, delivering steady demand anchored in oncology use and policy frameworks that reward innovation. The United States is addressing chronic shortages by supporting Merck’s multi-hundred-million-dollar facility in North Carolina, expected to triple domestic capacity upon completion in 2030. Europe benefits from coordinated procurement under joint tender programs that negotiate favorable pricing while promoting supply diversification; the UK’s rapid approval of Anktiva exemplifies regulatory momentum favoring BCG-based combination regimens.

Middle East & Africa and South America collectively exhibit untapped potential as tuberculosis elimination initiatives gain traction alongside improvements in cold-chain logistics. WHO’s TB-Free Central Asia initiative emboldens Central Asian republics to accelerate vaccination throughput, while South Africa’s past shortage-driven morbidity spikes have prompted the treasury to ring-fence funding for emergency buffer stocks. Brazil’s integration of tuberculosis screening into prenatal care signals an emerging maternal-child health paradigm that amplifies BCG coverage in public hospitals. These developments suggest that the BCG vaccine market will experience progressively balanced geographical contributions, replacing the historic reliance on a handful of Asian buyers.

Competitive Landscape

The competitive field remains moderately concentrated, with fewer than ten WHO-prequalified producers and even fewer holding registrations in high-income oncology markets. Merck’s decade-long status as sole U.S. supplier illustrates how stringent regulatory standards and high fixed costs deter fast follower entry. Sanofi’s exit clarified the capital intensity required to modernize legacy facilities for mycobacterial fermentation, while simultaneously opening white space for newcomers advancing recombinant strains. ImmunityBio’s tie-up with Serum Institute demonstrates the strategic value of marrying innovative platforms with large-scale low-cost capacity, potentially redrawing competitive lines from 2026 onward.

Manufacturers increasingly pursue geographic diversification to hedge against single-site outages. Serum Institute’s acquisition of a Netherlands facility extends its reach into the European Economic Area, reducing tariff exposure and shortening shipping lanes to high-price oncology markets. In parallel, Japan’s Ministry of Health, Labour and Welfare explores incentives for domestic mycobacterial vaccine production, signalling policy-driven opportunities for local players to break foreign supply dominance.

Product strategies now emphasize value-added differentiation rather than volume alone. Recombinant pipelines target heightened immunogenicity and broader antigen coverage, while formulation scientists work on freeze-stable or intradermal micro-needle patches that simplify delivery in rural settings. Companies able to bring these enhancements to market first will likely secure premium segments, potentially shifting market share away from incumbents that focus exclusively on scaling classical BCG. Accordingly, competitive rivalry in the BCG vaccine market is set to revolve around technological innovation, capacity resilience, and regulatory agility rather than mere manufacturing scale.

BCG Vaccine Industry Leaders

Serum Institute of India Pvt. Ltd.

AJ Biologics Sdn Bhd

Microgen

Merck & Co., Inc.

Japan BCG Laboratory

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA authorized ImmunityBio’s recombinant BCG alternative for bladder cancer through an expanded-access program, easing U.S. shortages while offering an improved safety and immunogenicity profile.

- November 2024: Indonesia announced a leadership role in global tuberculosis vaccine development by joining WHO-facilitated Phase 3 trials for M72/AS01E while sustaining comprehensive BCG vaccination programs.

- May 2024: ImmunityBio and Serum Institute of India formed an exclusive worldwide supply agreement for oncology-grade BCG, reshaping competitive positioning in bladder cancer therapy

- January 2024: Serum Institute of India joined CEPI’s global network via a USD 30 million investment aimed at expanding affordable outbreak-vaccine production capability, strengthening pandemic preparedness infrastructure

Global BCG Vaccine Market Report Scope

The Bacillus of Calmette-Guerin (BCG) vaccine is made from a weakened strain of tuberculosis bacteria. As the bacteria in the vaccine is weak, it triggers a person's immune system to protect them against tuberculosis, but it does not cause the infection. It provides constant protection against tuberculosis throughout the lifespan of a person.

The BCG Vaccine Market is segmented by Age Group (Pediatrics and Adults), Application (Tuberculosis and Bladder Cancer), Distribution Channel (Hospitals, Clinics, and Other Distribution Channels), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD million) for the above segments.

| Paediatric |

| Adults |

| Tuberculosis |

| Bladder Cancer |

| Public |

| Private |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Age Group | Paediatric | |

| Adults | ||

| By Application | Tuberculosis | |

| Bladder Cancer | ||

| By Distribution Channel | Public | |

| Private | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the BCG vaccine market?

The BCG vaccine market size is valued at USD 189.47 million in 2026 and is expected to reach USD 255.76 million by 2031, reflecting a 6.18% CAGR.

Why are supply shortages a recurring problem?

Only a handful of WHO-prequalified manufacturers produce GMP-grade BCG, and facility upgrades take up to six years, causing periodic disruptions that constrain patient access in North America and Europe.

Which region holds the largest share of the market?

Asia-Pacific leads with 37.52% of global revenue, driven by high tuberculosis incidence, strong newborn immunization mandates, and regional manufacturing capacity.

How is BCG used in oncology?

Intravesical BCG remains first-line therapy for non-muscle-invasive bladder cancer, and recent approvals of combination agents like Anktiva have improved complete response rates, bolstering adult demand.

What innovations could change the competitive landscape?

Recombinant BCG strains expressing multiple antigens, freeze-stable formulations, and micro-needle patches are in development and could command premium pricing once regulatory approvals are secured.

How are governments mitigating the impact of supply shortages?

Agencies such as UNICEF and CEPI deploy emergency tenders, finance new manufacturing lines, and build buffer stocks to maintain vaccination programs during production gaps, stabilizing medium-term market growth.

Page last updated on: