Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.75 Billion |

| Market Size (2031) | USD 19.06 Billion |

| Growth Rate (2026 - 2031) | 10.14% CAGR |

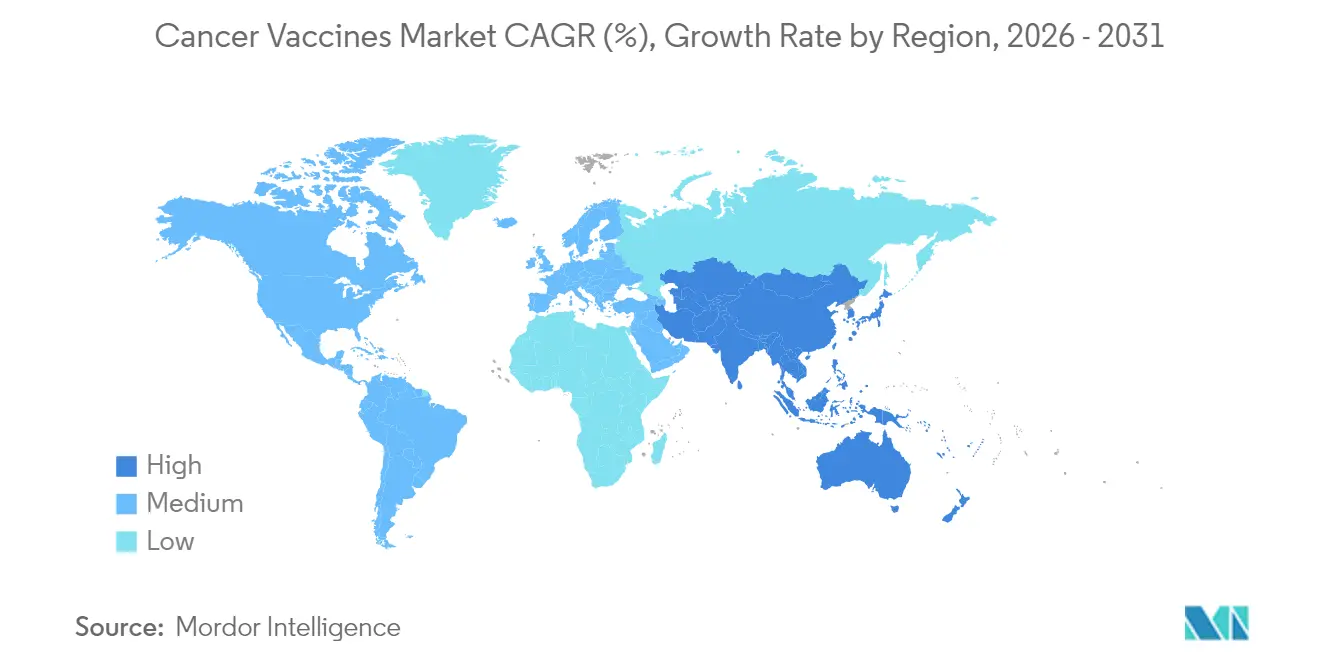

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cancer Vaccines Market Analysis by Mordor Intelligence

The cancer vaccines market size was valued at USD 10.67 billion in 2025 and estimated to grow from USD 11.75 billion in 2026 to reach USD 19.06 billion by 2031, at a CAGR of 10.14% during the forecast period (2026-2031). Accelerated growth reflects the pivot from conventional prophylaxis toward personalized mRNA-based immunotherapies [1]Cormac Sheridan, "Individualized mRNA cancer vaccines make strides," Nature Biotechnology, nature.com that encode patient-specific neoantigens, underpinned by artificial-intelligence antigen prediction and modular micro-factory manufacturing that shortens scale-up cycles. Regulatory harmonization—evident in FDA breakthrough designations and EMA PRIME approvals—lowers cross-border trial friction, while partnership-heavy business models channel capital toward platform differentiation rather than stand-alone products. North America retains leadership yet Asia-Pacific shows the fastest uptake as Chinese developers deliver mRNA vaccines at costs 99% below Western levels.

Key Report Takeaways

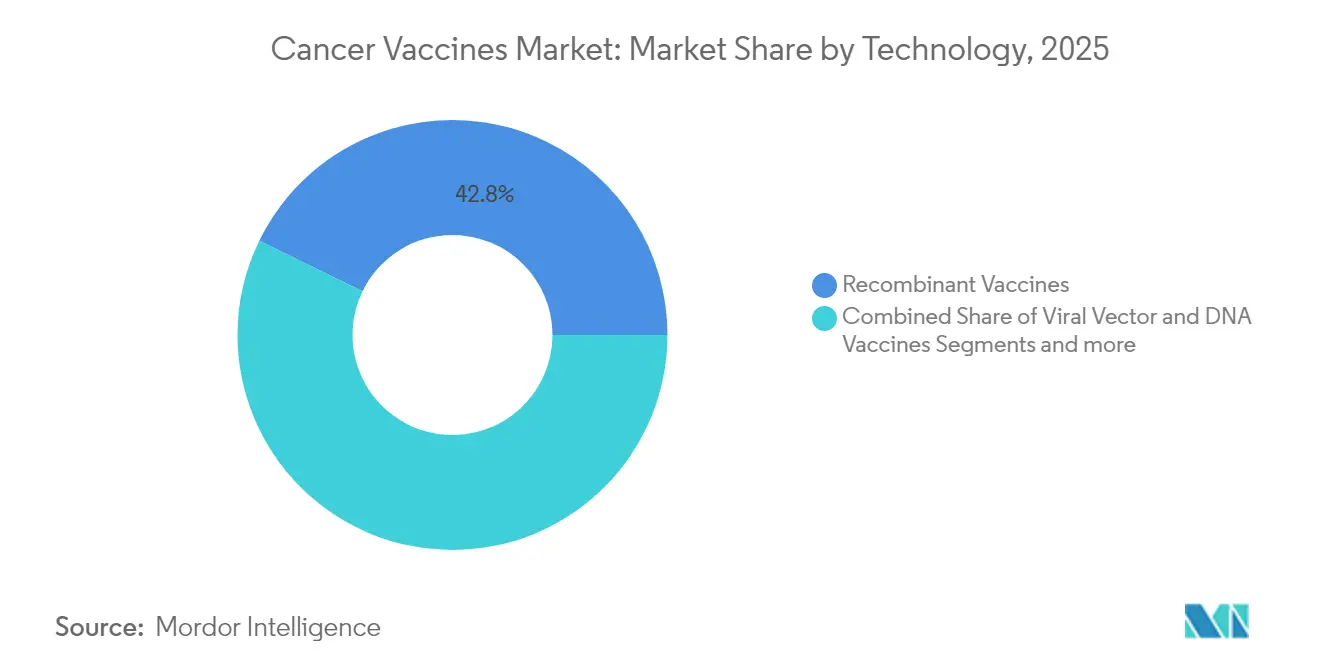

- By technology, recombinant vaccines led with 42.78% revenue share in 2025, while mRNA/neoantigen platforms are projected to expand at an 10.96% CAGR to 2031.

- By treatment method, preventive vaccines held 89.35% of the cancer vaccines market share in 2025, while therapeutic vaccines record the highest projected CAGR at 11.07% through 2031.

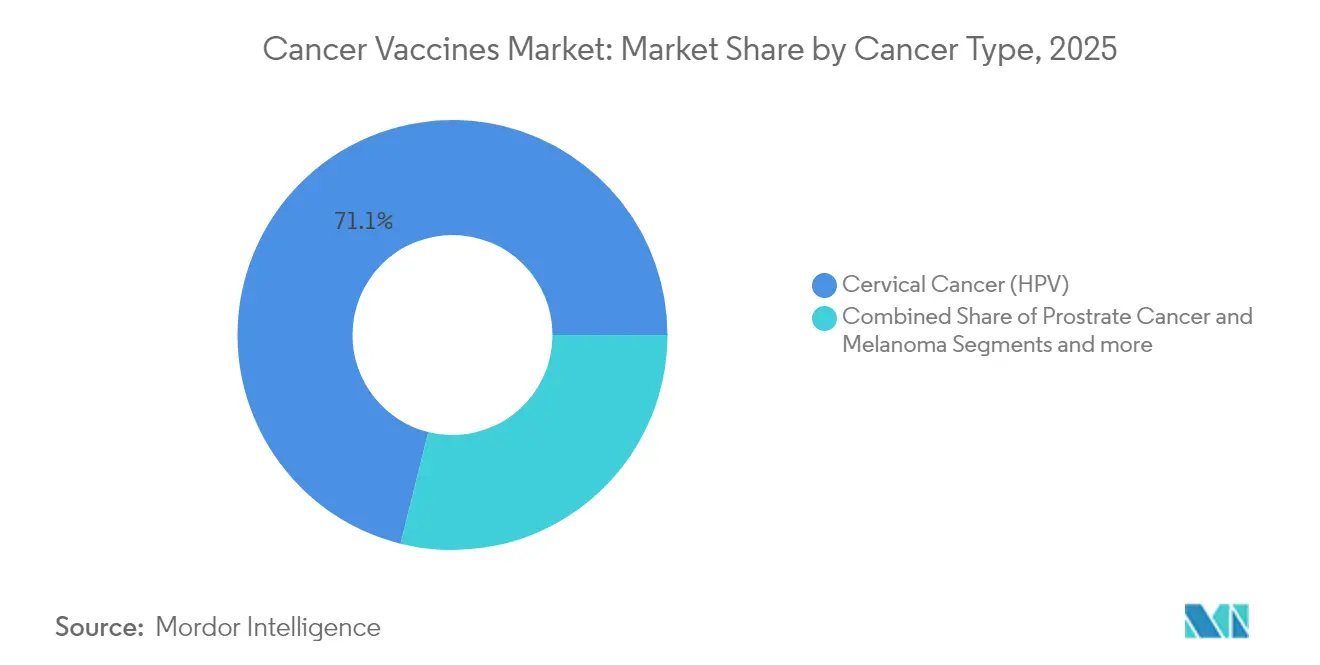

- By cancer type, cervical cancer accounted for 71.12% share of the cancer vaccines market size in 2025, whereas melanoma is advancing at an 10.79% CAGR through 2031.

- By delivery route, intramuscular accounted for 64.96% share of the cancer vaccines market size in 2025, whereas intravenous is advancing at an 10.88% CAGR through 2031.

- By geography, North America captured 45.62% of the cancer vaccines market share in 2025, while Asia-Pacific is forecast to grow at an 11.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cancer Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global cancer incidence | +2.1% | Global; highest in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Increasing R&D investments & government funding | +1.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advances in mRNA & neoantigen platforms | +2.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| AI-driven antigen prediction lowering cost | +1.4% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Modular micro-factory manufacturing hubs | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Combination regimens with CPIs de-risking trials | +1.6% | Global, regulatory precedents in US and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global Cancer Incidence

Cancer diagnoses are projected to rise 47% between 2020 and 2040, with the sharpest increases in regions lacking comprehensive oncology infrastructure; this demographic shift expands the addressable population for both preventive and therapeutic vaccines. Aging societies bring higher mutation loads, while earlier diagnostic practices enlarge the pool of patients eligible for tailored immunotherapies. Outpatient-friendly vaccine regimens align with the transition away from inpatient oncology care, trimming system costs that can exceed USD 150,000 per patient in high-income markets. Payers therefore see vaccines as cost-containment tools when compared with prolonged systemic therapies.

Increasing R&D Investments & Government Funding

Public-private partnership structures increasingly supplant traditional grants, sharing risk and compressing timelines. CEPI’s CMC framework now guides quality standards for cancer vaccine manufacturing, smoothing multi-jurisdictional filings [2]Anna Särnefält, "A Strategic Guide to Improve and De-risk Vaccine Development: CEPI′s CMC Framework," PDA JPST, journal.pda.org. European patent applications for cancer technologies climbed more than 70%, with universities filing a rising share, signaling collaborative innovation momentum. The UK’s BioNTech program pledges personalized vaccines to 10,000 patients by 2030, illustrating how national health systems invest directly in commercialization pathways. Venture capital flows remain skewed toward oncology, leaving a gap that government funds increasingly fill.

Advances in mRNA & Neoantigen Platforms

Industrial-scale mRNA manufacturing now produces patient-specific lots within 6-8 weeks of tumor sequencing, versus 18 months for legacy technologies. Lipid nanoparticles achieve >80% accurate HLA class I presentation, and AI-enabled neoantigen mapping cuts false positives by 60%. Self-amplifying mRNA lowers dose requirements tenfold [3]Alla Bulashevska, "Artificial intelligence and neoantigens: paving the path for precision cancer immunotherapy," PubMed Central, pmc.ncbi.nlm.nih.gov, easing supply constraints and cold-chain stress. Shared-neoantigen atlases now cover 15 SNV and 55 InDel hotspots, paving the way for off-the-shelf vaccines across several solid tumors.

AI-Driven Antigen Prediction Lowering Cost

Automated pipelines shrink discovery expenditures by 75% while raising HLA-binding prediction accuracy above 90%. Funding traction among AI-native biotechs—Infinitopes’ GBP 12.8 million seed round is notable—demonstrates the democratization of high-precision immunomics. Downstream, AI-optimized mRNA sequences require fewer purification steps, boost shelf-life, and cut logistics costs. Integrated proteogenomic workflows such as NeoDisc offer whole-tumor antigen maps, reducing clinical attrition rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory timelines & complexity | -1.9% | Global; highest impact in emerging markets | Long term (≥ 4 years) |

| Availability of alternative immunotherapies | -1.3% | Developed markets | Medium term (2-4 years) |

| Cold-chain gaps for personalised logistics | -0.8% | Asia-Pacific, Latin America, Sub-Saharan Africa | Short term (≤ 2 years) |

| Neoantigen IP clustering limiting entrants | -1.1% | US and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Timelines & Complexity

Personalized batch release protocols and AI-algorithm validation stretch approval cycles by 18-24 months beyond standard biologics. Smaller firms lacking global regulatory teams face disproportionate burdens, even though EMA’s PRIME gives accelerated status once clinical data mature. Absence of common standards on AI model transparency further clouds review processes, adding compliance costs that erode margins.

Availability of Alternative Immunotherapies

Blockbuster checkpoint inhibitors posted USD 25 billion in 2024 sales, creating entrenched clinical pathways that new vaccines must complement or surpass. Bispecific antibodies and next-generation CAR-T solutions deliver fast tumor debulking, encouraging oncologists to prioritize therapies with immediate measurable responses. As CAR-T safety profiles improve in solid tumors, therapeutic vaccines must stake claims on durability and lower toxicity to convince payers and clinicians.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: mRNA Platforms Outpace Recombinant Leaders

Recombinant platforms retained a 42.78% share of the cancer vaccines market in 2025. Their installed manufacturing base and well-known safety records keep them relevant, yet mRNA/neoantigen vaccines are accelerating at an 10.96% CAGR through 2031 as developers prioritize multiplex antigen encoding and rapid customization. Self-amplifying constructs reduce dose volume tenfold and ease cold-chain stress, improving economics for resource-constrained settings. Viral-vector and DNA modalities continue to address niche populations where thermostability is paramount, especially in emerging markets. Whole-cell and dendritic vaccines, though smaller in volume, play specialized roles in highly personalized regimens; Diakonos Oncology’s USD 20 million raise for glioblastoma underscores investor interest.

The technology spectrum is converging toward platform ecosystems that allow antigen swapping within weeks, a key differentiation for first movers. Shared-neoantigen libraries expand addressable populations beyond bespoke products, cutting per-patient costs and shortening regulatory reviews. As a result, the cancer vaccines market size attributed to mRNA constructs is forecast to widen its lead, especially once room-temperature formulations enter late-stage trials.

By Treatment Method: Therapeutic Vaccines Gain Momentum

Cervical cancer accounted for 71.12% of the cancer vaccines market size in 2025, a legacy of widespread HPV immunization campaigns. Melanoma vaccines, however, are advancing at an 10.79% CAGR as robust biomarkers facilitate precise patient matching and regulators grant breakthrough designations. Prostate and glioblastoma programs build on dendritic-cell platforms, while shared-neoantigen strategies open doors for colorectal and gastric cancers. Positive melanoma results reduce risk perceptions for adjacent solid tumors, drawing capital toward multi-cancer platform trials.

The transition from single-tumor success stories to platform-based multi-cancer solutions is expected to dilute cervical dominance over time, distributing the cancer vaccines market share more evenly across indications by 2031.

By Cancer Type: Melanoma Leads Post-HPV Innovation Wave

Cervical cancer accounted for 71.12% of the cancer vaccines market size in 2025, a legacy of widespread HPV immunization campaigns. Melanoma vaccines, however, are advancing at an 10.79% CAGR as robust biomarkers facilitate precise patient matching and regulators grant breakthrough designations. Prostate and glioblastoma programs build on dendritic-cell platforms, while shared-neoantigen strategies open doors for colorectal and gastric cancers. Positive melanoma results reduce risk perceptions for adjacent solid tumors, drawing capital toward multi-cancer platform trials.

The transition from single-tumor success stories to platform-based multi-cancer solutions is expected to dilute cervical dominance over time, distributing the cancer vaccines market share more evenly across indications by 2031.

By Delivery Route: Intravenous Uptake Accelerates

Intramuscular injections held 64.96% of 2025 volume, capitalizing on prevalent vaccine infrastructure, but intravenous delivery is growing at an 10.88% CAGR due to its ability to trigger systemic immune activation critical for metastatic disease. Microneedle arrays and tattoo-like patches under evaluation may boost compliance, particularly in outpatient settings. Thermostable carrier systems further broaden market access in low-resource geographies by reducing cold-chain dependency.

Higher bioavailability and targeted biodistribution make intravenous formats attractive for combination therapy regimens, a trend likely to lift their proportion of the cancer vaccines market by the close of the decade.

Geography Analysis

North America’s 45.62% share in 2025 stems from mature regulatory pathways, extensive trial networks, and steady public funding such as the National Cancer Institute’s USD 2.5 million translational grants. USMCA streamlines cross-border studies, drawing Canadian and Mexican stakeholders into joint manufacturing ventures. Venture investment culture sustains high-risk R&D, keeping the cancer vaccines market growth in the region well above global averages despite mounting cost pressures.

Europe leverages coordinated public-private initiatives; the UK-BioNTech partnership targeting 10,000 patients by 2030 exemplifies how national health systems deploy purchasing power to spur innovation. EMA PRIME accelerates late-stage reviews, while Germany, France, and Italy supply academic expertise and GMP capacity. Reimbursement frameworks that value patient-centric outcomes favor adoption of personalized solutions, maintaining Europe’s competitive weight.

Asia-Pacific posts the fastest 11.05% CAGR owing to state-sponsored biotech programs and low-cost manufacturing that erodes Western price advantages. China funds modular micro-factories and free HPV drives, while Japan and South Korea export advanced process technologies. India’s contract-manufacturing depth and expansive patient base make it a pivotal trial hub. Australia’s regulatory alignment with ICH standards positions it as a bridge market for trans-Pacific commercialization.

Competitive Landscape

Competition in the cancer vaccines market hinges on control of platform technologies rather than individual assets. mRNA specialists BioNTech and Moderna repurpose COVID-19 infrastructure to secure capacity and speed, while AI-driven firms such as Gritstone and Ultimovacs focus on neoantigen analytics. Patent clusters around epitope-prediction algorithms create defensible moats that encourage cross-licensing.

Partnerships dominate strategy; the BioNTech–Bristol Myers Squibb deal carries a USD 1.5 billion upfront and USD 7.6 billion milestones for bispecific exploration, illustrating how large-cap partners supplement modality expertise with commercialization scale. Mid-cap companies pursue geographic alliances to access Asian manufacturing discounts, while big pharma acquires AI startups to shorten discovery timelines.

White-space opportunities include logistics innovations that bypass cold-chain gaps and shared-antigen libraries that break the bespoke cost curve. Market entry barriers remain substantive: regulatory complexity, IP congestion, and the entrenched clinical role of checkpoint inhibitors. Yet rapid technological diffusion keeps competitive intensity high and prevents monopolistic dominance.

Cancer Vaccines Industry Leaders

-

OSE Immunotherapeutics

-

GlaxoSmithKline PLC

-

F Hoffmann-La Roche AG (Genentech)

-

Moderna Inc.

-

Merck & Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Evaxion reported that 80% of EVX-01 targets triggered tumor-specific immune responses in phase 2 melanoma testing.

- March 2025: Icahn School of Medicine released phase 1 data on PGV001, a personalized multi-peptide neoantigen vaccine demonstrating safety and immunogenicity.

- March 2025: FDA approved EVM14, a tumor-associated antigen vaccine for non-small-cell lung and head-and-neck cancers.

- February 2025: Dana-Farber investigators confirmed durable anti-tumor immunity in all nine renal-cell carcinoma patients receiving postoperative personalized vaccines, with zero recurrences at 34.7-month median follow-up.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cancer vaccines market as the cumulative revenue generated from the sale of preventive and therapeutic vaccines that stimulate an immune response against malignant cells across all approved technologies, recombinant, viral-vector & DNA, mRNA/neoantigen, and whole-cell or dendritic platforms. Finished, labeled doses sold to hospitals, public immunization programs, and specialty clinics worldwide form the revenue pool that Mordor Intelligence sizes.

Scope exclusion: investigational candidates still in Phase I/II trials and companion checkpoint inhibitors are not counted.

Segmentation Overview

-

By Technology

- Recombinant Vaccines

- Viral Vector & DNA Vaccines

- mRNA/Neoantigen Personalised Vaccines

- Whole-cell & Dendritic Cell Vaccines

- Other Technologies

-

By Treatment Method

- Preventive Vaccines

- Therapeutic Vaccines

-

By Cancer Type

- Cervical Cancer (HPV)

- Prostate Cancer

- Melanoma

- Other Cancers

-

By Delivery Route

- Intramuscular

- Intradermal / Sub-cutaneous

- Intravenous

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oncologists, immunization-program managers, and manufacturing directors across North America, Europe, and Asia-Pacific. These conversations tested penetration assumptions for HPV doses, realistic near-term mRNA pricing, and likely regulatory timelines, letting us refine desk-based estimates and spot outliers.

Desk Research

We began by harvesting historical shipment and price data from open-access regulators such as the US CDC's Vaccines for Children contracts, the European Centre for Disease Prevention and Control price lists, and Japan's PMDA approvals. Incidence and vaccination coverage statistics from GLOBOCAN, WHO Immunization Monitoring, and national cancer registries anchored disease and uptake baselines. Financial clues from SEC 10-Ks, select investor decks, and trade association releases (BIO, Vaccines Europe) filled recent volume and ASP trends. D&B Hoovers and Dow Jones Factiva supplied supplementary company-level revenue splits. The sources cited here are illustrative; a wider body of literature was reviewed to cross-check figures and definitions.

Market-Sizing & Forecasting

A top-down model converts country-level cancer incidence into vaccine-eligible populations, applies age-specific coverage, and multiplies by weighted average selling prices. Supplier roll-ups of disclosed dose sales provided a selective bottom-up lens that validated the totals before minor alignment. Key variables include HPV vaccination rates, therapeutic dose success rates, average treatment cycles, price erosion in tender markets, R&D success probabilities, and regional reimbursement policies. Five-year forecasts were produced with multivariate regression that links dose demand to incidence growth, technology shift toward mRNA platforms, and announced capacity expansions; scenario analysis adjusted for breakthrough approvals. Data gaps, especially in emerging regions, were bridged by importing proxy coverage ratios from demographically similar markets.

Data Validation & Update Cycle

Outputs undergo variance checks against parallel market signals, after which senior reviewers sign off. We refresh the model each year and trigger interim updates if a major approval, policy change, or safety signal materially shifts demand; a final pre-publication sweep ensures timeliness.

Why Mordor's Cancer Vaccines Baseline Inspires Confidence

Published estimates often diverge because firms choose different technology baskets, patient pools, and price curves. By tracing every dollar back to clearly defined doses sold in the commercial channel, we provide a starting point executives can actually reconcile with procurement data.

Key gap drivers are usually the treatment of pipeline products and the pace at which therapeutic vaccines monetize. Some publishers inflate totals by adding projected sales from late-stage trials, while others undercount mRNA pricing or exclude middle-income tenders. Mordor reports only commercialized formulations yet reflects realistic launch ramps, and our annual update cadence prevents stale baselines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.67 B (2025) | Mordor Intelligence | - |

| USD 9.84 B (2024) | Global Consultancy A | Narrower technology scope, slower uptake assumptions |

| USD 12.14 B (2024) | Research Publisher B | Counts near-term pipeline revenue aggressively |

| USD 9.27 B (2024) | Regional Consultancy C | Uses uniform ASP discounts across high-income markets |

In summary, while figures vary, Mordor's disciplined scope, variable selection, and transparent refresh cycle deliver a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the projected value of the cancer vaccines market by 2031?

The market is forecast to reach USD 19.06 billion by 2031, expanding at a 10.14% CAGR.

Which region is growing fastest for cancer vaccines?

Asia-Pacific shows the highest growth at an 11.05% CAGR, supported by cost-efficient mRNA manufacturing and large patient pools.

How dominant are preventive cancer vaccines today?

Preventive products hold 89.35% of 2025 revenue, though therapeutic vaccines are growing faster at an 11.07% CAGR.

Which technology segment is expanding most quickly?

MRNA/neoantigen platforms lead with an 10.96% CAGR thanks to rapid customization and strong clinical efficacy signals.

What is the main competitive strategy among leading companies?

Partnership-based ecosystem building, such as BioNTech’s alliances, has overtaken stand-alone competition, pooling strengths in AI analytics, manufacturing, and clinical access.

Why is intravenous delivery gaining traction?

It offers superior systemic immune activation, crucial for metastatic tumors, and is advancing at an 10.88% CAGR as formulations improve bioavailability.

Page last updated on: